Vanilla Options Iron Condor Spread Strategies

The iron condor is a strategy that profits if the underlying stock or index keeps within a certain range over the duration of an investment.

Investors obviously make money when stocks go up or down a lot. If you buy a stock for cash, you only make money when the share price increases. On the other hand, iron condors make money irrespective of stock direction. As long as the stock stays within a small range, investors will make money whether the stock moves down or up a little or moves sideways. This is possible because an iron condor is a combination of a bear call spread and a bull put spread on the same underlying stock. It consists of one long and one short call option and one long and one short put option. Each option is at a different strike price but they all have the same expiry date.

Let’s look at the bear call spread first.

Bear Call Spread

The bear call spread strategy entails selling a call option and buying another call option with a higher strike price in the same expiry month. The investor’s outlook on the underlying stock is neutral to slightly bearish. See following example:

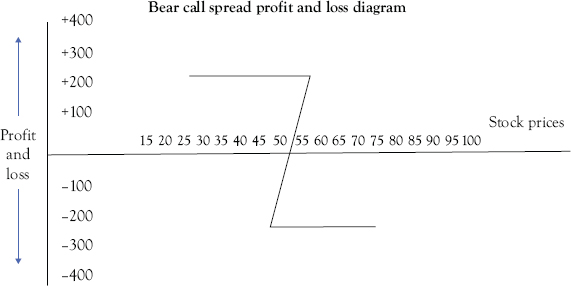

XYZ stock is trading at $56 in October.

The investor thinks that XYZ will not rise above $60 before November options expiration date. So, the investor enters a bear call spread by selling an OTM November $60 call for $3 and buying an OTM October $65 call for $1.

The net premium received in the investors account is $200 ($2 x 100 shares per contract).

The maximum risk on the trade is $300 ($5 difference in strike prices, less $2 premium received times 100). At expiry, if XYZ finishes below $60, the investor keeps the $200 premium for a return of 40 percent on capital at risk. See Figure 11.1 below.

Figure 11.1 Bear call spread profit and loss diagram

Bull Put Spread

The bull put spread strategy entails selling a put option and buying another put option with a lower strike price in the same expiry month. The investor’s outlook on the underlying stock is neutral to slightly bullish. See following example:

XYZ stock is trading at $56 in October. The investor thinks that XYZ will not fall below $53 before November options expiration. The investor enters a bull put spread by selling an OTM October $53 put for $3 and buying an OTM October $48 put for $1. The net premium received in the investors account is $200 ($2 × 100 shares per contract). The maximum risk on the trade is $300 ($5 difference in strike prices, less $2 premium received times 100). At expiry, if XYZ finishes above $53, the trader keeps the $200 premium for a return of 40 percent on capital at risk.

Now by placing these two strategies together, we can create an iron condor which as the name suggests, the profit-and-loss diagram resembles a large bird as shown in Figure 11.2.

In our short iron condor example, the strategy is considered neutral as the two short options are roughly equidistant from the current stock price. It is possible to select different strike prices for the two options to reflect a more bullish or bearish outlook. Whichever strategy is chosen, the maximum profit will always be when the underlying stock price remains between the strike prices of the two short options. The wings of the short iron condor reflect the two long options which have strike prices furthest away from the current underlying stock price are purchased to cap the loss potential from extreme downward or upward movements of the underlying stock. As we mentioned before, the best case scenario is when the underlying stock price remains in between the inner strike prices at expiration.

Figure 11.2 Bull put spread profit-and-loss diagram

Figure 11.3 Short iron condor profit-and-loss diagram

The bottom line is that a short iron condor (See Figure 11.3 above) earns a profit for the investor when the two short strikes earn more than the investor pays for the two long strikes. In our previous example, the return on capital at risk is more than 75 percent.

Long Iron Condor

The long iron condor is the polar opposite of the short iron condor both functionally and visually as seen on the profit-and-loss diagram described in Figure 11.4 below.

Figure 11.4 Long iron condor profit-and-loss diagram

An investor would construct the long iron condor by selling the two outer strikes and buying the two inner strikes. This strategy is designed to take advantage of a large movement in price of the underlying stock. It is structured with two debit spreads as opposed to the short iron condor which is constructed with two credit spreads. The debit that is paid to open this position is the maximum potential risk and requires a considerable price change and/or increase in implied volatility to profit from this strategy. It is for this reason that the long iron condor is not that popular with investors.