12.2.1 Solution to the Finite-Horizon Discrete-Time Mixed H2/H∞ Nonlinear Filtering Problem

We similarly consider the following class of estimators:

∑daf:{ˆxk+1=f(xk)+L(ˆxk,k)[yk−h2(xk)], ˆx(k0)=ˆx0 ˆz=h1(ˆxk) |

(12.46) |

where ˆxk∈X is the estimated state, L(.,.)∈ℳn×m(X×Z) is the error-gain matrix which is smooth and has to be determined, and ˆz∈ℜs is the estimated output of the filter. We can now define the estimation error or penalty variable, ⌣z, which has to be controlled as:

⌣zk:=zk−ˆz=h1(ˆxk)−h1(ˆxk).

Then, we combine the plant (12.42) and estimator (12.46) dynamics to obtain the following augmented system:

(12.47) |

where

⌣xk=(xkxk),⌣f(⌣x)=( f(xk)f(ˆxk)+L(ˆxk,k)(h2(xk)−h2(ˆxk))),⌣g(⌣x)=(g1(xk)L(ˆxk,k)k21(xk)),⌣h(⌣xk)=h1(xk)−h1(ˆxk).

The problem is then similarly formulated as a two-player nonzero-sum differential game with the following cost functionals:

(12.48) |

(12.49) |

where w := {wk}. The first functional is associated with the H∞-constraint criterion, while the second functional is related to the output energy of the system or H2-criterion. It is seen that, by making J1 ≥ 0, the H∞ constraint ‖ℱk o ∑da‖ℋ∞≤γ is satisfied. Then, similarly, a Nash-equilibrium solution to the above game is said to exist if we can find a pair (L⋆ , w⋆) such that

(12.50) |

(12.51) |

Sufficient conditions for the solvability of the above game are well known (Chapter 3, also [59]), and are given in the following theorem.

Theorem 12.2.1 For the two-person discrete-time nonzero-sum game (12.48)-(12.49), (12.47), under memoryless perfect information structure, there exists a feedback Nash-equilibrium solution if, and only if, there exist 2(K − k0) functions Y,V:N⊂X×Z→ℜ,N⊂X such that the following coupled recursive equations (discrete-time Hamilton-Jacobi-Isaacs equations (DHJIE)) are satisfied:

Y(⌣x,k)=infw∈W{12[γ2‖wk‖−‖⌣zk(⌣x)‖2]+Y(⌣xk+1,k+1)},Y(⌣x,K+1)=0, k=k0,…,K,∀⌣x∈N×N |

(12.52) |

V(⌣x,k)=minL∈ℳn×m{12‖⌣zk(⌣x)‖2+V(⌣xk+1,k+1)},V(⌣x,K+1)=0, k=k0,…,k,∀⌣x∈N×N |

(12.53) |

where ⌣x=⌣xk,L=L(xk,k),w:={wk}.

Thus, we can apply the above theorem to derive sufficient conditions for the solvability of the D M H 2 H I N L F P. To do that, we define the Hamiltonian functions Hi:(X×X)×W×ℳn×m×ℜ→ℜ,i=1,2 associated with the cost functionals (12.48), (12.49) respectively:

H1(⌣x,wkL,Y)=Y(⌣f(⌣x)+⌣g(⌣x)wk,K+1)−Y(⌣x,k)+12γ2‖wk‖2−12‖⌣zk‖2, |

(12.54) |

(12.55) |

for some smooth functions Y,V:X→ℜ,Y<0,V>0 where the adjoint variables corresponding to the cost functionals (12.48), (12.49) are set as p1 = Y, p2 = V respectively.

The following theorem then presents sufficient conditions for the solvability of the D M H 2 H I N L F P on a finite-horizon.

Theorem 12.2.2 Consider the nonlinear system (12.42) and the D MH 2 H I N L F P for it. Suppose the function h1 is one-to-one (or injective) and the plant Σda is locally asymptotically-stable about the equilibrium-point x = 0. Further, suppose there exists a pair of C2 negative and positive-definite functions Y,V:N×N×Z→ℜ respectively, locally defined in a neighborhood N×N×X×X of the origin ⌣x =0, and a matrix function L:N×Z→ℳn×m satisfying the following pair of coupled HJIEs:

Y(⌣x,k) = Y(⌣f⋆(⌣x)+⌣g⋆(⌣x)w⋆k(⌣x),k+1)+12γ2‖w⋆k(⌣x)‖2−12‖⌣zk(⌣x)‖2,Y(⌣x,K+1) =0, |

(12.56) |

V(⌣x,k) =V(⌣f⋆(⌣x)+⌣g⋆(⌣x)w⋆k(⌣x),k+1)+12‖⌣zk(⌣x)‖2,V(⌣x,K+1) =0,k=k0,…..K. |

(12.57) |

k = k0,…, K, together with the side-conditions

(12.58) |

(12.59) |

(12.60) |

(12.61) |

where

⌣f⋆(⌣x)=⌣f(⌣x)|L=L⋆ , ⌣g⋆(⌣x)=⌣g(⌣x)|L=L⋆.

Then:

(i) there exists locally a Nash-equilibrium solution (w⋆,L⋆) for the game (12.48), (12.49), (12.42) locally in N

(ii) the augmented system (12.47) is locally dissipative with respect to the supply-rate s(wk,⌣zk)=12(γ2‖wk‖2−‖⌣zk‖2) and hence has ℓ2-gain from w to ⌣z less or equal to γ;

(iii) the optimal costs or performance objectives of the game are J⋆1(L⋆,w⋆)=Y(⌣x0,k0) and J⋆2(L⋆,w⋆)=V(⌣x0,k0);

(iv) the filter Σdaf with the gain matrix L(⌣xk,k) satisfying (12.59) solves the finite-horizon D M H 2 H I N L F P for the system locally in N.

Proof: Assume there exist definite solutions Y, V to the DHJIEs (12.56)-(12.57), and (i) consider the Hamiltonian function H1(., ., ., .). Then applying the necessary condition for the worst-case noise, we have

∂TH1∂w|w=w⋆k = ⌣gT(⌣x)∂TY(λ, k+1)∂λ|λ=⌣f(⌣x)+⌣g(⌣x)w⋆k +γ2w⋆k=0,

to get

w⋆k := −1γ2⌣gT(⌣x)∂TY(λ, k+1)∂λ|λ=⌣f(⌣x)+⌣g(⌣x)w⋆k := α0(⌣x,w⋆k). |

(12.62) |

Thus, w⋆ is expressed implicitly. Moreover, since

∂2H1∂w2 = ⌣gT(⌣x)∂2Y(λ, k+1)∂λ2|λ=⌣f(⌣x)+⌣g(⌣x)w⋆k ⌣g(⌣x)+γ2I

is nonsingular about (⌣x, w) = (0, 0), equation (12.62) has a unique solution α1(⌣x), α1(0) = 0 in the neighborhood N0 × W0 of (x, w) = (0, 0) by the Implicit-function Theorem [234].

Now, substitute w⋆ in the expression for H2(., ., ., .) (12.55), to get

H2(⌣x,w⋆k,L,V) = V(⌣f(⌣x)+⌣g(⌣x)w⋆k(⌣x),k+1)−V(⌣x,k)+12‖⌣zk(⌣x)‖2 ,

and let

L⋆ = arg minL {H2(⌣x,w⋆k,L,V)}.

Then by Taylor’s theorem, we can expand H2(., w⋆ , ., .) about L⋆ [267] as

H2(⌣x,w⋆,L,Y) = H2(⌣x,w⋆,L⋆,YT⌣x)+ 12Tr{[In ⊗(L−L⋆)T]∂2H2∂L2(w⋆,L)[Im ⊗(L−L⋆)T]}+ O(‖L−L⋆‖3).

Therefore, taking L⋆ as in (12.59) and if the condition (12.61) holds, then H2(., ., w⋆ , .) is minimized, and the Nash-equilibrium condition

H2(w⋆,L⋆) ≤ H2(w⋆,L) ∀L∈ℳn×m, k=k0,…,K

is satisfied. Moreover, substituting (w⋆,L⋆) in (12.53) gives the DHJIE (12.57).

Now substitute L⋆ as given by (12.59) in the expression for H1(., ., ., .) and expand it in Taylor’s-series about w⋆ to obtain

H1(⌣x,wk,L⋆,Y) = Y(⌣f⋆(⌣x)+⌣g⋆(⌣x)w,k+1)−Y(x,k)+12γ2||wk||2−12||⌣zk||2 = H1(⌣x,w⋆k,L⋆,Y) +12(wk−w⋆k)T∂2H2∂w2k(wk,L⋆), (wk−w⋆k)+ O(‖wk−w⋆k‖3).

Further, substituting w = w⋆ as given by (12.62) in the above, and if the condition (12.60) is satisfied, we see that the second Nash-equilibrium condition

H1(w⋆,L⋆) ≤ H1(w,L⋆), ∀w∈W

is also satisfied. Therefore, the pair (w⋆,L⋆) constitute a Nash-equilibrium solution to the two-player nonzero-sum dynamic game. Moreover, substituting (w⋆,L⋆) in (12.52) gives the DHJIE (12.56).

(ii) The Nash-equilibrium condition

H1(⌣x,w,L⋆,Y) ≥ H1(⌣x,w⋆,L⋆,Y) = 0 ∀⌣x ∈U , ∀w∈W

implies

Y(⌣x,k)−Y(⌣xk+1,k+1) ≤ 12γ2‖wk‖2−12‖⌣zk‖2 , ∀⌣x ∈U , ∀w∈W ⇔ ⌣Y(⌣xk+1,k+1) − ⌣Y(⌣xk,k) ≤ 12γ2‖wk‖2−12‖⌣zk‖2 , ∀⌣x ∈U , ∀w∈W |

(12.63) |

for some positive-definite function ⌣Y=−Y>0. Summing now the above inequality from k = k0 to k = K we get the dissipation-inequality

(12.64) |

Thus, from Chapter 3, the system has ℓ2-gain from w to ⌣z less or equal to γ.

(iii) Consider the cost functional J1(L, w) first, and rewrite it as

J1(L,w)+Y(⌣xk+1,k+1)− Y(⌣x(k0),k0) ≤ K∑k=k0 {12γ2‖wk‖2−12‖⌣zk‖2 + Y(⌣xk+1,k+1) − Y(⌣xk,k) } = K∑k=k0H1(⌣x,wk,Lk,Y) .

Substituting (L⋆, w⋆) in the above equation and using the DHJIE (12.56) gives H1(⌣x, w⋆ , L⋆ , Y) = 0 and the result follows. Similarly, consider the cost functional J2(L, w) and rewrite it as

J2(L,w)+V(⌣xk+1,k+1)− V(⌣xk0,k0) = K∑k=k0{12‖⌣zk‖2+V(⌣xk+1,k+1) − V(⌣xk,k)} = K∑k=k0H2(⌣x,wk,Lk,V) .

Since V (⌣x, K + 1) = 0, substituting (L⋆ , w⋆) in the above and using the DHJIE (12.57) the result similarly follows.

(iv) Notice that the inequality (12.63) implies that with wk ≡ 0,

(12.65) |

and since ⌣Y is positive-definite, by Lyapunov’s theorem, the augmented system is locally stable. Finally, combining (i)-(iii), (iv) follows. □

12.2.2 Solution to the Infinite-Horizon Discrete-Time Mixed H2/H∞ Nonlinear Filtering Problem

In this subsection, we discuss the infinite-horizon filtering problem, in which case we let K → ∞. Moreover, in this case, we seek a time-invariant gain ˆL(ˆx) for the filter, and consequently time-independent functions Y,V:˜NטN→ℜ locally defined in a neighborhood ˜NטN⊂X×X of (x,ˆx)=(0,0), such that the following steady-state DHJIEs:

Y(⌣f⋆(⌣x)+⌣g⋆(⌣x)˜w⋆(⌣x)−Y(⌣x)+12γ2‖˜w⋆k(⌣x‖2−12‖⌣z(⌣x‖2 =0 Y(0) =0, |

(12.66) |

(12.67) |

are satisfied together with the side-conditions:

(12.68) |

(12.69) |

(12.70) |

(12.71) |

where ˜w⋆,˜L⋆ are the asymptotic values of w⋆,L⋆

⌣f⋆(⌣x) = ⌣f(⌣x)|˜L=˜L⋆ , ⌣g⋆(⌣x) = ⌣g(⌣x)|˜L=˜L⋆,˜H1(⌣x,wk,˜L,Y) = Y(⌣f(⌣x)+⌣g(⌣x)wk)−Y(⌣x)+12γ2‖wk‖2−12‖⌣zk‖2,˜H2(⌣x,wk,˜L,V) = V(⌣f(⌣x)+⌣g(⌣x)wk)−V(⌣x)+12‖⌣zk‖2 .

Again here, since the estimation is carried over an infinite-horizon, it is necessary to ensure that the augmented system (12.47) is stable with w = 0. However, in this case, we can relax the requirement of asymptotic-stability for the original system (12.42) with a milder requirement of detectability which we define next.

Definition 12.2.2 The pair {f, h} is said to be locally zero-state detectable if there exists a neighborhood O of x = 0 such that, if xk is a trajectory of xk+1 = f(xk) satisfying x(k0) ∈ O, then h(xk) is defined for all k ≥ k0 and h(xk) = 0, for all k ≥ ks, implies limk→∞ xk = 0. Moreover {f, h} is zero-state detectable if O = X.

The “admissibility” of the discrete-time filter is similarly defined as follows.

Definition 12.2.3 A filter F is admissible if it is asymptotically (or internally) stable for any given initial condition x(k0) of the plant Σda, and with w ≡ 0

limk→∞ ⌣zk = 0.

The following proposition can now be proven along the same lines as Theorem 12.2.2.

Proposition 12.2.1 Consider the nonlinear system (12.42) and the infinite-horizon D M H 2 H I N L F P for it. Suppose the function h1 is one-to-one (or injective) and the plant Σda is zero-state detectable. Suppose further, there exists a pair of C2 negative and positive-definite functions Y,V:˜NטN→ℜ, respectively, locally defined in a neighborhood ˜NטN⊂X×X of the origin ⌣x = 0, and a matrix function ˜L:˜N→ℳn×m satisfying the pair of coupled DHJIEs (12.66), (12.67) together with (12.68)-(12.71). Then:

(i) there exists locally a Nash-equilibrium solution (˜w⋆,˜L⋆) for the game;

(ii) the augmented system (12.47) is dissipative with respect to the supply-rate s(wk,⌣zk)=12(γ2‖wk‖2−‖⌣zk‖2) and hence has ℓ2-gain from w to ⌣z less or equal to γ;

(iii) the optimal costs or performance objectives of the game are J⋆1(˜L⋆,˜w⋆)=Y(⌣x0) and J⋆2(˜L⋆,˜w⋆)=V(⌣x0)

(iv) the filter Σdaf with the gain matrix L(ˆx)=˜L⋆(ˆx) satisfying (12.69) solves the infinite horizon D M H 2 H I N L F P locally in ˜N.

Proof: Since the proof of items (i)-(iii) is similar to that of Theorem 12.2.2, we prove only item (iv).

(iv) Using similar manipulations as in the proof of Theorem 12.2.2, it can be shown that a similar inequality as (12.63) also holds. This implies that with wk ≡ 0,

(12.72) |

and since ⌣Y is positive-definite, by Lyapunov’s theorem, the augmented system is locally stable. Furthermore, for any trajectory of the system ⌣xk such that ⌣Y(⌣xk+1)−⌣Y(⌣xk) = 0 for all k ≥ kc > k0, it implies that zk ≡ 0. This in turn implies h1(xk) = h1(ˆxk), and xk = ˆxk ∀k ≥ kc since h1 is injective. This further implies that h2(xk) = h2(ˆxk) ∀k ≥ kc and it is a trajectory of the free system:

⌣xk+1 = (f(xk)f(ˆxk)) .

By zero-state of the detectability of {f, h1}, we have limk→∞ xk = 0, and we have internal stability of the augmented system with limk→∞ zk = 0. Hence, Σdaf is admissible. Finally, combining (i)-(iii), (iv) follows. □

In this subsection, we discuss how the D M H 2 H I N L F P can be solved approximately to obtain explicit solutions [126]. We consider the infinite-horizon problem for this purpose, but the approach can also be used for the finite-horizon problem. For simplicity, we make the following assumption on the system matrices.

Assumption 12.2.1 The system matrices are such that

k21(x)gT1(x) =0 , k21(x)kT21(x) = I.

Consider now the infinite-horizon Hamiltonian functions

˜H1(⌣x,w,ˆL,˜Y) = ˜Y(⌣f(⌣x)+⌣g(⌣x)w)−˜Y(⌣x)+12γ2‖w‖2−12‖⌣z‖2,˜H2(⌣x,w,ˆL,˜V) = ˜V(⌣f(⌣x)+⌣g(⌣x)w)−˜V(⌣x)+12‖⌣z‖2 .

for some negative and positive-definite functions ˜Y,˜V:ˆN׈N→ℜ,ˆN⊂X a neighborhood of x = 0, and where ⌣x=⌣xk,w=wk,z=zk. Expanding them in Taylor series1 about ˆf(⌣x)up to first-order:

ˆH1(⌣x,w,ˆL,˜Y) = {˜Y(ˆf(⌣x))+˜Yx(ˆf(⌣x))g1(x)w)+˜Yˆx(ˆf(⌣x))[ˆL(ˆx)(h2(x)−h2(ˆx)+k21(x)w)] +O(‖˜υ‖2}−˜Y(⌣x)+12γ2‖w‖2−12‖⌣z‖2, ∀⌣x ∈ˆN ׈N, w∈W |

(12.73) |

ˆH2(⌣x,w,ˆL,˜V) = {˜V(ˆf(⌣x))+˜Vx(ˆf(⌣x))g1(x)w)+˜Vˆx(ˆf(⌣x))[ˆL(ˆx)(h2(x)−h2(ˆx)+k21(x)w)] +O(‖˜υ‖2}−˜V(⌣x)+12‖⌣z‖2, ∀⌣x ∈ˆN ׈N, w∈W |

(12.74) |

where ˜Yx,˜Vx are the row-vectors of the partial-derivatives of ˜Y and ˜V respectively,

˜υ = ( g1(x)wˆL(ˆx)[h2(x)−h2(ˆx)+k21(x)w])

and

lim˜υ→∞ O(‖˜υ‖2)‖˜υ‖2 = 0.

Then, applying the necessary conditions for the worst-case noise, we get

∂H1∂w =0 ⇒ˆw⋆ := −1γ2[gT1(x)˜YTx(ˆf(⌣x))+kT21(x)ˆLT(ˆx)˜YTˆx(ˆf(⌣x))]. |

(12.75) |

Now substitute ˆw⋆ in (12.74) to obtain

ˆH2(⌣x,ˆw⋆,ˆL,V) ≈ V(ˆf(⌣x)) −˜V(⌣x)−1γ2˜Vx(ˆf(⌣x))g1(x)gT1(x)˜YTx(ˆf(⌣x))+ ˜Vˆx(ˆf(⌣x))ˆL(ˆx)[h2(x)−h2(ˆx)− 1γ2˜Vx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜YTx(ˆf(⌣x))+ 12‖z‖2.

Then, completing the squares for ˆL in the above expression for ˆH2(., ., ., .), we have

ˆH2(⌣x,ˆw⋆,ˆL,˜V) ≈ ˜V(ˆf(⌣x)) −˜V(⌣x)−1γ2˜Vx(ˆf(⌣x))g1(x)gT1(x)˜YTx(ˆf(⌣x))+12||z||2+ 12γ2‖ˆLT(ˆx)˜VTˆx(ˆf(⌣x))+γ2(h2(x)−h2(ˆx))‖2 −γ22‖h2(x)−h2(ˆx)‖2+ 12γ2‖ˆLT(ˆx)˜YTˆx(ˆf(⌣x))‖2− 12γ2‖ˆLT(ˆx)˜VTˆx(ˆf(⌣x))+ˆLT(ˆx)˜YTx(ˆf(⌣x))‖2 .

Therefore, taking ˆL⋆ as

(12.76) |

minimizes ˆH2(., ., ., .) and renders the Nash-equilibrium condition

ˆH2(ˆw⋆,ˆL⋆) ≤ ˆH2(ˆw⋆,ˆL) ∀ˆL ∈ℳn×m

satisfied.

Substitute now ˆL⋆ as given by (12.76) in the expression for H1(., ., ., .) and complete the squares in w to obtain:

ˆH1(⌣x,ˆw,ˆL⋆,˜Y) = ˜Y(ˆf(⌣x)) −˜Y(⌣x)−1γ2˜Yˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜VTˆx(ˆf(⌣x)− 12γ2˜Yx(ˆf(⌣x)g1(x)gT1(x)˜YTx(ˆf(⌣x))−12γ2˜Yˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜YTx(ˆf(⌣x)) −12‖z‖2+γ22‖w+1γ2gT1(x)˜YTx(ˆf(⌣x))+1γ2kT21(x)ˆLT(ˆx)˜YTˆx(ˆf(⌣x))‖2 .

Similarly, substituting w = ˆw⋆ as given by (12.75), we see that, the second Nash-equilibrium condition

ˆH1(ˆw⋆,ˆL⋆) ≤ H1(w,ˆL⋆), ∀w∈W

is also satisfied. Thus, the pair (ˆw⋆ , ˆL⋆) constitutes a Nash-equilibrium solution to the two-player nonzero-sum dynamic game corresponding to the Hamiltonians ˆH1(.,.,.,.) and ˆH2(.,.,.,). With this analysis, we have the following important theorem.

Theorem 12.2.3 Consider the nonlinear system (12.42) and the infinite-horizon D M H 2 H I N L F P for it. Suppose the function h1 is one-to-one (or injective) and the plant Σda is zero-state detectable. Suppose further, there exists a pair of C1 negative and positive-definite functions ˜Y,˜V:ˆN׈N→ℜ respectively, locally defined in a neighborhood ˆN׈N⊂X×X of the origin ⌣x=0 , and a matrix function ˆL:ˆN→ℳn×m satisfying the pair of coupled DHJIEs:

˜Y(ˆf(⌣x)) −˜Y(⌣x)−12γ2˜Yx(ˆf(⌣x)g1(x)gT1(x)˜YTx(ˆf(⌣x))−12γ2˜Yˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜YTx(ˆf(⌣x))− 1γ2˜Yˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜VTˆx(ˆf(⌣x))− 12(h1(x)−h1(ˆx))T(h1(x)−h1(ˆx))=0, ˜Y(0)=0, |

(12.77) |

˜V(ˆf(⌣x)) −˜V(⌣x)−1γ2˜Vx(ˆf(⌣x)g1(x)gT1(x)˜YTx(ˆf(⌣x))−1γ2˜Vˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜YTx(ˆf(⌣x)− γ2(h2(x)−h2(ˆx))T(h2(x)−h2(ˆx))+ 12(h1(x)−h1(ˆx))T(h1(x)−h1(ˆx))=0, ˜V(0)=0, |

(12.78) |

together with the coupling condition (12.76). Then:

(i) there exists locally in ˆN a Nash-equilibrium solution (ˆw⋆ , ˆL⋆) for the dynamic game corresponding to (12.48), (12.49), (12.47);

(ii) the augmented system (12.47) is locally dissipative with respect to the supply rate s(w,⌣z)=12(γ2‖w‖2−‖⌣z‖2) in ˆN, and hence has ℓ2-gain from w to ⌣z less or equal to γ;

(iii) the optimal costs or performance objectives of the game are approximately J⋆1(ˆL⋆,ˆw⋆) =˜Y(⌣x0) and J⋆2(ˆL⋆,ˆw⋆) =˜V(⌣x0);

(iv) the filter Σdaf with the gain-matrix ˆL(ˆx) = ˆL⋆(ˆx) satisfying (12.76) solves the infinitehorizon D M H 2 H I N L F P for the system locally in ˆN

Proof: Part (i) has already been shown above. To complete it, we substitute (ˆL⋆,ˆw⋆) in the DHJIEs (12.66), (12.67) with ˆH1(.,.,.,.) and ˆH2(.,.,.,) replacing H1(.,.,.,.),H2(.,.,.,.) respectively, to get the DHJIEs (12.77), (12.78) respectively.

(ii) Consider the time-variation of ˜Y along a trajectory of the system (12.47) with ˆL=ˆL⋆::

˜Y(⌣xk+1) = ˜Y(⌣f⋆(x)+⌣g⋆(x)w) ∀⌣x ∈ˆN, ∀w∈W ≈ ˜Y(ˆf(⌣x)) +˜Yx(ˆf(⌣x)g1(x)w+˜Yˆx(ˆf(⌣x))[ˆL⋆(ˆx)(h2(x)−h2(ˆx)+k21(x)w)] = ˜Y(ˆf(⌣x))−12γ2˜Yx(ˆf(⌣x)g1(x)gT1(x)˜YTx(ˆf(⌣x))− 1γ2˜Yˆx(ˆf(⌣x))ˆL⋆(ˆx)ˆL⋆T(ˆx)˜VTˆx(ˆf(⌣x))− 12γ2˜Yˆx(ˆf(⌣x))ˆL⋆(ˆx)ˆL⋆T(ˆx)˜YTˆx(ˆf(⌣x))+ γ22‖w+1γ2gT1(x)˜YTx(ˆf(⌣x))+1γ2kT21(x)ˆL⋆T(ˆx)˜YTˆx(ˆf(⌣x))‖2−γ22‖w‖2 = ˜Y(⌣x) +12‖⌣z‖2−γ22‖w‖2+γ22‖w+1γ2gT1(x)˜YTx(ˆf(⌣x))+ 1γ2kT21(x)ˆL⋆T(ˆx)˜YTˆx(ˆf(⌣x))‖2 ≥ ˜Y(⌣x) +12‖⌣z‖2−γ22‖w‖2 ∀⌣x ∈ˆN, ∀w∈W

where use has been made of the first-order Taylor-approximation, equation (12.76), and the DHJIE (12.77) in the above manipulations. The last inequality further implies that

˜Y(⌣xk+1)−˜Y(⌣x) ≤ γ22‖w‖2 −12‖⌣z‖2 ∀⌣x ∈ˆN, ∀w∈W

for some ˜Y=−˜Y>0, which is the infinitesimal dissipation-inequality [180]. Therefore, the system has ℓ2-gain ≤ γ. The proof of asymptotic-stability can now be pursued along the same lines as in Proposition 12.2.1.

The proofs of items (iii)-(iv) are similar to those in Theorem 12.2.2. □

Remark 12.2.2 The benefits of the Theorem 12.2.3 can be summarized as follows. First and foremost is the benefit of the explicit solutions for computational purposes. Secondly, the approximation is reasonably accurate, as it captures a great deal of the dynamics of the system. Thirdly, it greatly simplifies the solution as it does away with extra sufficient conditions (see e.g., the conditions (12.60), (12.61) in Theorem 12.2.1). Fourthly, it opens the way also to develop an iterative procedure for solving the coupled DHJIEs.

Remark 12.2.3 In view of the coupling condition (12.76), the DHJIE can be represented as

˜V(ˆf(⌣x)) −˜V(⌣x)−1γ2˜Vx(ˆf(⌣x)g1(x)gT1(x)˜YTx(ˆf(⌣x))−1γ2˜Vˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜VTx(ˆf(⌣x))− 1γ2˜Vˆx(ˆf(⌣x))ˆL(ˆx)ˆLT(ˆx)˜YTˆx(ˆf(⌣x))+ 12(h1(x)−h1(ˆx))T(h1(x)−h1(ˆx))=0, ˜V(0)=0. |

(12.79) |

The result of the theorem can similarly be specialized to the linear-time-invariant (LTI) system:

∑dl: {˙xk+1 = Axk+ G1wk, x(k0)=x0 ⌣zk = C1(xk−ˆxk) yk = c2xk + D21wk, |

(12.80) |

where all the variables have their previous meanings, and F∈ℜn×n , G1∈ℜn×n ,C1∈ℜs×n ,C2∈ℜm×n and D21∈ℜm×r are constant real matrices. We have the following corollary to Theorem 12.2.3.

Corollary 12.2.1 Consider the LTI system Σdl defined by (12.80) and the D M H 2 H I N L F P for it. Suppose C1 is full column rank and A is Hurwitz. Suppose further, there exist a negative and a positive-definite real-symmetric solutions ˆP1,ˆP2 (respectively) to the coupled discrete-algebraic-Riccati equations (DAREs):

ATˆP1A−ˆP1−12γ2ATˆP1G1GT1ˆP1A−12γ2ATˆP1ˆLˆLTˆP1A−1γ2ATˆP1ˆLˆLTˆP2A−CT1C1 = 0 |

(12.81) |

ATˆP2A−ˆP2−1γ2ATˆP2G1GT1ˆP2A−1γ2ATˆP2ˆLˆLTˆP1A−1γ2ATˆP2ˆLˆLTˆP2A+CT1C1 = 0 |

(12.82) |

together with the coupling condition:

(12.83) |

Then:

(i) there exists a Nash-equilibrium solution (ˆw⋆l , ˆL⋆) for the game given by

ˆw⋆ = −1γ2(GT1+DT21ˆL⋆)ˆP1A(x−ˆx),(x−ˆx)TATˆP2ˆL⋆ = −γ2(x−ˆx)TCT2;

(ii) the augmented system

∑dlf : {⌣xk+1 = [A0ˆL⋆C2A−ˆL⋆C2]⌣xk+ [G1ˆL⋆D21]w, ⌣x(k0)=[x0ˆx0] ⌣zk = [C1 −C1]⌣xk :=⌣C⌣xk

has H∞ -norm from w to ⌣z less than or equal to γ;

(iii) the optimal costs or performance objectives of the game are approximately

J⋆1(ˆL⋆,ˆw⋆k) =12(x0−ˆx0)TˆP1(x0−ˆx0) and J⋆2(ˆL⋆,ˆw⋆k) =12(x0−ˆx0)TˆP2(x0−ˆx0);

the filter ℱ defined by

∑ldf : ˆxk+1 = Aˆxk+ ˆL(y−C2ˆxk), ˆx(k0)=ˆx0

with the gain matrix ˆL = ˆL⋆ satisfying (12.83) solves the infinite-horizon D M H 2 H I N L F P for the discrete-time linear system.

Proof: Take:

˜Y(⌣x) = 12(x−ˆx)TˆP1(x−ˆx), ˆP1 = ˆPT1 < 0, ˜V(⌣x) = 12(x−ˆx)TˆP2(x−ˆx), ˆP2 = ˆPT2 > 0,

and apply the result of the theorem. □

12.2.4 Discrete-Time Certainty-Equivalent Filters (CEFs)

Again, it should be observed as in the continuous-time case Sections 12.2.1, 12.2.2 and 12.2.3, the filter gains (12.59), (12.69), (12.76) may also depend on the original state, x, of the system which is to be estimated. Therefore in this section, we develop the discrete-time counterparts of the results of Section 12.1.3.

Definition 12.2.4 For the nonlinear system (12.42), we say that it is locally zero-input observable, if for all states xk,xk′ ∈ U⊂X and input w(.) ≡ 0,

y(ˉk,xk,w) = y(ˉk,xk′,w) ⇒ xk= xk′

where y(., x,w) is the output of the system with the initial condition x(k0) = x. Moreover, the system is said to be zero-input observable if it is locally observable at each xk ∈X or U=X .

We similarly consider the following class of certainty-equivalent filters:

∑˜af : {ˆxk+1 = f(ˆxk)+g1(ˆxk)w⋆k+˜L(ˆxk,yk)[y−h2(ˆxk)−k12(ˆxk)˜w⋆k]; ˆx(k0)=ˆx0 ˆzk = h2(ˆxk) ˜zk = yk−h2(ˆxk), |

(12.84) |

where ˜L(.,.) ∈ℳn×m is the gain of the filter, ˜w⋆ is the estimated worst-case system noise (hence the name certainty-equivalent filter) and ˜z is the new penalty variable. Then, if we consider the infinite-horizon mixed H2/H∞ dynamic game problem with the cost functionals (12.48), (12.49) and the above filter, we can similarly define the associated corresponding approximate Hamiltonians (as in Section 12.2.3) ˜Hi:X×W×Y×ℳn×m×ℜ→ℜ, i=1,2 as

ˆK1(ˆx,w,y,˜L,˜Y) = ˜Y(˜f(ˆx),y)−˜Y(ˆx,yk−1)+˜Yˆx(ˆx,y)[f(ˆx)+g1(ˆx)w+ ˜L(ˆx,y)(y−h2(ˆx)−k21(ˆx)w]+12γ2||w||2−12||˜z||2ˆK2(ˆx,w,y,˜L,˜V) = ˜V(˜f(ˆx),y)−˜V(ˆx,yk−1)+˜Vˆx(ˆx,y)[f(ˆx)+g1(ˆx)w+ ˜L(ˆx,y)(y−h2(ˆx)−k21(ˆx)w]+12||˜z||2

for some smooth functions ˜V,˜Y:X×Y→ℜ, where ˆx=ˆxk , w=wk, y=yk, ˜z=˜zk , and the adjoint variables are set as ˜p1=˜Y,˜p2=˜V. Then

∂ˆK1∂w|w=˜w⋆ = [g1(ˆx)−˜L(ˆx,y)k21(ˆx)]T˜YTx(ˆf(ˆx),y)+γ2w=0 ⇒˜w⋆ = −1γ2[g1(ˆx)−˜L(ˆx,y)k21(ˆx)]T˜YTx(ˆf(ˆx),y).

Consequently, repeating the steps as in Section 12.2.3 and Theorem 12.2.3, we arrive at the following result.

Theorem 12.2.4 Consider the nonlinear system (12.42) and the D M H 2 H I N L F P for it. Suppose the plant Σda is locally asymptotically-stable about the equilibrium point x = 0 and zero-input observable. Suppose further, there exists a pair of C1 (with respect to the first argument) negative and positive-definite functions ˜Y,˜V:˜N×ϒ→ℜ respectively, locally defined in a neighborhood ˜N×ϒ⊂X×Y of the origin (ˆx,y)=(0,0), and a matrix function ˜L:˜N×ϒ→ℳn×m satisfying the following pair of coupled DHJIEs:

˜Y(ˆf(ˆx),y)−˜Y(ˆx,yk−1)−12γ2˜Yˆx(ˆf(ˆx),y)g1(ˆx)gT1(ˆx)˜YTˆx(ˆf(ˆx),y)−12γ2˜Yx(ˆx,y)−˜L(ˆx,y)˜LT(ˆx,y)YTˆx(ˆx,y)−1γ2˜Yˆx(ˆf(ˆx),y)˜LT(ˆx,y)˜VTˆx(ˆf(x),y)−12(y−h2(ˆx))T(y−h2(ˆx))=0,˜Y(0,0)=0, |

(12.85) |

FIGURE 12.4

Discrete-Time H2/H∞-Filter Performance with Unknown Initial Condition and ℓ2-Bounded Disturbance; Reprinted from Int. J. of Robust and Nonlinear Control, RNC1643 (published online August) © 2010, “Discrete-time Mixed H2/H∞ Nonlinear Filtering,” by M. D. S. Aliyu and E. K. Boukas, with permission from Wiley Blackwell.

ˆx∈˜N,y∈ϒ, together with the coupling condition

(12.87) |

Then the filter ˜Σaf with the gain matrix ˜L(ˆx,y) satisfying (12.87) solves the infinite-horizon D M H 2 H I N L F P for the system locally in ˜N.

Proof: Follows the same lines as Theorem 12.2.3. □

Remark 12.2.4 Comparing the HJIEs (12.85)-(12.86) with (12.77)-(12.78) reveals that they are similar, but we have gained by reducing the dimensionality of the PDEs, and more importantly, the filter gain does not depend on x any longer.

We consider a simple example to illustrate the result of the previous section.

Example 12.3.1 We consider the following scalar system

xk+1 = x15k+x13k yk = xk+wk

where wk=e−0.3ksin(0.25πk) is an ℓ2 -bounded disturbance.

Approximate solutions of the coupled DHJIEs (12.85) and (12.86) can be calculated using an iterative approach. With γ= 1, and g1 (x) = 0, we can rewrite the coupled DHJIEs as j = 0, 1,…. Then, with the initial filter gain l0 = 1, initial guess for solutions as ˜Y0(ˆx,y)=−12(ˆx2+y2), ˜V0(ˆx,y)=12(ˆx2+y2) respectively, we perform one iteration of the above recursive equations (12.88), (12.89) to get

˜Yj+1(ˆx,y)≜˜Yj(ˆx,yk−1)+12(y−x)2=˜Yj(ˆf,y)−12˜Yj2ˆx(ˆf,y)lj2−˜Yjˆx(ˆf,y)˜Vjˆx(ˆf,y)lj2, |

(12.88) |

˜Vj+1(ˆx,y)≜˜Vj(ˆx,yk−1)−12(y−x)2=˜Vj(ˆf,y)−12˜Vj2ˆx(ˆf,y)lj2−˜Yjˆx(ˆf,y)˜Vjˆx(ˆf,y)lj2, |

(12.89) |

FIGURE 12.5

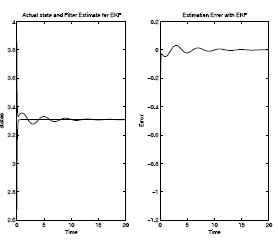

Extended-Kalman-Filter Performance with Unknown Initial Condition and ℓ2-Bounded Disturbance; Reprinted from Int. J. of Robust and Nonlinear Control, RNC1643 (published online August) © 2010, “Discrete-time mixed H2/H∞ nonlinear filtering,” by M. D. S. Aliyu and E. K. Boukas, with permission from Wiley Blackwell.

˜Y=−12[(ˆx1/5+ˆx1/3)+y2]+12(ˆx1/5+ˆx1/3)2, ˜V1=12[(ˆx1/5+ˆx1/3)2+y2].

Therefore,

˜Y1(ˆx,yk−1)=−12(y−x)2−12y2,˜V(ˆx,yk−1)=12(y−x)2+12[(ˆx1/5+ˆx1/3)2+y2].

We can use the above approximate solution ˜V1(ˆx,yk−1) to the DHJIE to estimate the states of the system, since the gain of the filter depends only on ˜V1ˆx(ˆx,y). Consequently, we can compute the filter gain as

(12.90) |

The result of simulation with this filter is then shown in Figure 12.4. We also compare this result with that of an extended-Kalman filter for the same system shown in Figure 12.5. It can clearly be seen that, the mixed H2/H∞ filter performance is superior to that of the EKF.

This chapter is entirely based on the authors’ contributions [18, 19, 21]. The reader is referred to these references for more details.

1 A second-order Taylor series approximation would be more accurate, but the first-order method gives a solution that is very close to the continuous-time case.