The Importance of Functional Interdependencies in Financial Services Systems

The events of 2007–2009 in the global financial markets clearly illustrated the need of an improved understanding of how the global Financial Services System (FSS) functions. In particular, the crisis made it clear that national FSSs, or components of such systems such as individual banks, were highly dependent on the normal functioning of other components of the global FSS. The primary goal of this chapter is to introduce a functional framework that enables a proactive identification of risk associated with outcomes of actions – either planned or already taken. Key concepts from Resilience Engineering and functional modelling are leveraged to define the approach. The primary goal of the proposed framework is to identify key functional dependencies between an individual firm’s business functions and the functions that drive key behaviours of global financial markets. The rapid demise of the UK-based residential mortgage firm Northern Rock is used to illustrate the proposed framework.

The events of 2007–2009 sent shockwaves through the global financial services industry. The shockwaves were triggered by an unexampled event (Westrum, 2006), namely the global credit market crunch and its impact on other parts of the global FSS. Many reputable global financial services organisations (e.g., Bank of America, UBS, Citigroup and the Royal Bank of Scotland) experienced unprecedented losses and found themselves in need of financial support from national governments. Several other financial services firms suffered catastrophic business failures, for example, the US-based global investment banking firm Bear Stearns and the UK-based residential mortgage lending firm Northern Rock.

The 2007 global credit market crunch required extreme imagination to be comprehended and consequently pushed organisations outside of their experience envelope. What happened was that an event in the US sub-prime market rapidly propagated through the global FSS with an unprecedented impact on it, and eventually, on the world economy. The turmoil showed that using historical data to predict the future obviously did not provide the required forward-looking assessment of financial market behaviour (Bernstein, 2007). Unfortunately, many traditional risk metrics and forecasting techniques of the financial services industry do rely on historical data, including the Value-at-Risk (VaR) approaches used to determine market risk (Manganelli and Engle, 2001).

In this chapter we demonstrate how Resilience Engineering can provide the financial services industry with a better way to understand the potential impact of both past and future actions by identifying how system components are interconnected. The term ‘functional’ is used in the present context to emphasise that the focus is on capturing the behaviour of financial services functions and not on describing implementation details, that is, the mechanisms of any specific function. (cf., Merton, 1995; Merton and Bodie, 2005). Throughout the chapter, the term ‘risk’ will be used to denote a state in which a FSS in part, or in whole, is exposed to uncertain outcomes that can be either positive or negative.

The Financial Services System 2007–2009

The turmoil in the global financial markets has been the subject of several financial stability reports, published by central banks since 1996–1997, as well as reports published by the Financial Stability Board (FSB) previously known as the Financial Stability Forum. A recent FSB report (2009), highlighted procyclicality as one of the major contributors to the disruptions in the global financial markets. The report defined ‘procyclicality’ as ‘the dynamic interactions (positive feedback mechanisms) between the financial and the real sectors of the economy. These mutually reinforcing interactions tend to amplify business cycle fluctuations and cause or exacerbate financial instability’ (p. 10). In other words, there are functional dependencies between the economy and the global financial markets that can provide mutually amplifying reinforcements. Thus, if global financial markets contract, the economies also tend to contract. In their report FSB states that ‘amplifying feedback mechanisms can be as potent in the expansion phase of the [business] cycle as they are in downturns.’

The FSB highlighted two primary sources of procyclicality:

• Risk Management limitations: ‘Measures of risk often spike once tensions arise, but may be quite low even as vulnerabilities and risk build up during the [business] expansion phase.’

• Inherent conflict between providers and users (i.e., lenders and borrowers) of funds, that is, the so-called ‘Principal-Agent problem’. FSB sees this conflict as particularly difficult if there is a close link between asset valuations and funding. An example of such a conflict between lenders and borrowers is the need for individual lenders to retain capital; as a result they cannot make economic resources available to borrowers. One key event during the financial crisis was the compound systemic impact of seemingly unrelated individual lender decisions not to lend to borrowers.

Figure 13.1 shows a traditional linear- and event-based view expressed by Bank of England (2007). The global financial market turmoil was triggered by an increased default rate in the US sub-prime mortgage market. In response to this increase in default rates, asset backed securities were downgraded; investors became more risk averse and as a result lost interest in financial instruments that seemed to be exposed to the sub-prime markets. Investor weariness spilled over to the short-term global credit markets and as a result major financial services firms faced increased liquidity risk. Due to the need to provide cover for funds typically available to investors on the short-term credit markets, global financial firms experienced a major deterioration of their balance sheets. The result was a tendency to ‘hoard’ cash and an increased aversion to risk. This triggered tensions on the inter banking lending market resulting in reduced liquidity and higher inter banking interest rates.

In parallel, complex asset classes experienced continued devaluation leading to an increased need for capital, and this forced some firms to shed assets. For instance, Merrill Lynch (later acquired by Bank of America), a US-based financial services company, sold 30 billion dollars worth of assets in July–August 2008. As a result, asset valuations decreased and firms needed yet more capital. At the same time credit agencies started to revise their risk ratings (i.e., risks were perceived as being much higher) and individual firms therefore required more capital to cover potential losses. At this point the procyclical forces outlined by the FSB report were in full play and this, as we all know now, ultimately had a very negative impact on all major developed economies.

Figure 13.1 Crisis ‘Phases’ of the 2007 Financial Markets Turmoil (Based on Bank of England’s 2007 Financial Stability Report’s Chart 1)

In April 2008, the Financial Stability Forum provided a summary of how various risk management processes ‘broke down’ during the crisis (p. 16).

• Regulators and supervisory bodies failed to identify the risks associated with financial services firms’ structured products and other types of off-balance sheet entities. As a result firms ended by having insufficient capital buffers to deal with asset devaluations and decreased investor risk appetite.

• Financial firms misjudged the risk associated with offbalance sheet entities, often due to an over-reliance on risk ratings provided by credit rating agencies. Instead of making their own analysis, firms relied on ratings provided by specialised companies such as Standard & Poor’s.

• Commonly used metrics to assess market risk, that is, ‘… the risk of losses in on-and off-balance sheet positions arising from movements in market prices’ (Gallati, 2003: 34), such as VaR, could not be leveraged. A primary reasons for this was that VaR required historical data and the ability to Mark-to-Market, that is, to assign an asset a value based on the current market price of the same or similar type of asset. But this could not be done because there were no markets for the particular asset type! The reason for this was that risk aversive investors had caused markets to quickly ‘dry up’. As a result, valuations were model-based and therefore did no reflect a realistic market value.

• Investors (i.e., market participants) misjudged at least one of the following: a) borrowers risk of defaulting, b) the dangers associated with making too many investments in a single type of assets or financial instrument, and c) the risks associated with reduced liquidity, that is, the ability to turn an asset into cash without any impact on the value.

Central banks, such as the Bank of England, the European Central Bank, and the US Federal Reserve Bank reacted by cutting interest rates and by pouring money into the global Financial Services System. Many national governments also provided funds to key financial institutions with the intention to kickstart the key process between providers and users of funds. In addition, unprecedented efforts began to create macro-prudential processes, operating at a system level in the FSS.

One of the key lessons from the recent crisis is that most risk-management efforts by regulatory bodies typically focused on individual firms and not on understanding systemic risk. In Europe, the de Larosière report proposed to establish a European Systemic Risk Council with a charter to ‘… form judgments and make recommendations on macro-prudential policy, issue risk warnings, compare observations on macro-economic and prudential developments and give direction on these issues’ (de Larosière, 2009: 44). In March 2009, the US Treasury department similarly recommended to form a so-called ‘Systemic Risk Regulator’ focused on capturing systemic risk. A key capability of both of these proposed systemic regulatory bodies is the need to understand how various components of the FSS are interconnected and how their behaviour can possibly impact the broader economy. In addition, systemic regulatory bodies must be able to assess if the ‘sum is larger than its parts’ from a risk perspective. In other words, how do risks associated with individual components of a FSS ‘add up’ or combine? One question is whether they behave linearly at all? Most important of all, the proposed regulatory bodies need to have a shared understanding of what constitutes the ‘Financial Services System’.

What is the Financial Services System?

General Systems Theory, developed by the Austrian biologist Ludwig von Bertalanffy, defines a system as ‘… a complex of elements standing in [dynamic] interaction’ (von Bertalanffy, 1975: 159). The primary focus of General Systems Theory is to identify how systems reorganise and self-regulate to achieve their objectives. Von Bertalanffy spent most of his life trying to understand so-called ‘open systems’, that is, systems that constantly exchange material – matter and energy – with their environments, very much as cells do in a biological organism. Financial Services Systems are open systems that must adapt to a changing environment by means of constant ‘exchanges’ with their environments. Without these exchanges open systems cannot sustain performance and will ultimately enter a catastrophic state, i.e., an irreversible state of failure (cf., Sundström and Hollnagel, 2006).

Conceptually, exchanges between a FSS and its environment, as well as within the system itself, are a mixture of the following two types:

• Proactive Exchanges driven by the FSS’s goal, such as the perpetual need to identify demands for its services, to meet the demands by providing financial services, and ideally to do it so that its assets and resources are either preserved and/or increase in value.

• Reactive Exchanges that are ‘forced’ upon the system by the sheer dynamics of the environment. For example, a general reduction in households’ disposable income is likely to drive up delinquency rates on loans and thus eventually will force a FSS to take actions, including a write-off of delinquent loan related losses.

Most FSSs are regulated by various types of regulatory bodies such as central banks, or organisations like the UK’s Financial Services Authority. The primary goal of these entities is to make sure that any particular FSS is not in a state that results in increased systemic risk. The primary material exchanged between a regulatory entity and a FSS is information. This information is used by regulatory bodies to assess the state of the system, to provide regulatory guidance, and to formulate action plans. Other types of entities, such as credit agencies, are also part of the Financial Services System. A credit agency is basically an organisation dedicated to collecting information about the credit worthiness of individuals and organisations. This information is provided to other entities in the system that often leverage this information to make lending, or, investment decisions.

Figure 13.2 illustrates the following key points about Financial Services Systems (or any system):

• System boundaries are defined relative to a particular perspective. An economist looking at the FSS from a global perspective is likely to include everything in the two white rectangles. A ‘Micro Regulator’ is likely to focus on the entity it is regulating. For example, in Figure 13.2, ‘Micro Regulator A’ regulates financial services firm B, whereas ‘Macro Regulator A’ is responsible for monitoring the overall FSS. The key lesson from Figure 13.2 is that system boundaries will be ‘drawn’ as needed by the entity looking at the system.

• The types of entities (‘institutions’) included in a view of a FSS will depend on what attributes and behaviour an entity must display to be considered part of the FSS.

Following von Bertalanffy’s definition of a system, we obviously need to answer the question of what creates the dynamic interactions in Financial Services Systems. To accomplish this, we will use the definition that a FSS ‘can be defined in general terms as the interaction between supply of and the demand of the provision of capital and other finance related resources’ (Schmidt and Tyrell, 2004: 21). From this definition we can infer that the interaction of demand and supply functions will have an impact on any FSS.

Figure 13.2 Different views of financial services systems and entities

What Creates the Dynamic Interactions?

The financial services literature often makes a distinction between a so-called institutional and a functional perspective (Merton, 1995). The institutional perspective builds on the structure of existing institutions in the Financial Services industry, whereas a functional perspective ‘… takes as given the economic functions performed by financial intermediaries and asks what the best institutional structure to perform those functions is’ (Merton, 1995). In the present chapter we assume that interactions of economic functions are the primary source of the behaviour of a FSS, both from a micro-and a macro-prudential perspective.

To understand the behaviour associated with the dynamic interactions within and between FSSs, and of course to determine the system boundaries, we need to have a model or a representation of the FSS. Generally speaking, a model is a simplified representation of the salient features of an object system that can be used to analyse or reason about it. Some models can be explicit and visualised while others are implicit, e.g., embedded in a program or a set of equations. A key feature of any model is that it determines what information is relevant and how information is organised and processed. A model will influence how we define system boundaries and make decisions about what we consider to be entities of a particular FSS.

While there is a large variety of models, few are able to address the risks that arise from performance variability, even though this variability may lead to both negative and positive outcomes. The Functional Resonance Analysis Method (FRAM), proposed by Hollnagel (2004) offers a way to understand how functions can be coupled or interconnected. The principle of ‘functional resonance’ makes use of the definition of stochastic resonance concepts used in physics. Formally defined, stochastic resonance happens when a non-linear input is superimposed on a periodic modulated signal that normally is too weak to be detected, so that a resonance between the weak signal and the stochastic noise pushes the result over the threshold (Hollnagel, 2004: 168).

Stochastic resonance is generally used to illustrate the noise-controlled onset of order in complex systems. The difference between stochastic and functional resonance is that the variability that constitutes the ‘noise’ in the latter case is systematic, hence predictable, rather than random. From a functional perspective, resonance means that the variability of a set of interconnected functions may combine to affect the normal but otherwise undetectable variability in other functions and thereby lead to significant unexpected outcomes.

While the details of FRAM modelling still are being refined, the basic principles have been established and demonstrated particularly in the aviation domain (e.g., Hollnagel et al., 2008). In the next section, we will highlight the modelling steps, leverage some of them and also introduce the visual notation used by the method.

This section will demonstrate how functions of a FSS can be modelled and how this can help to uncover interdependencies. The primary purpose is to illustrate the modeling process rather than to present a validated model of the functions of a FSS.

A FRAM modelling process typically consists of four phases:

1. Identify what functions need to be modelled.

2. Identify conditions that could lead to change in performance.

3. Identify areas where functional resonance could emerge.

4. Identify how performance variance can be monitored and controlled.

In the following, we will focus on phases 1, 3 and 4.

Identifying the Core Functions

The primary purpose of this modelling step is to identify the critical functions of a system. Merton and Bodie (1995) proposed a functional view of FSSs, cf., also Merton and Bodie (2005), which comprises the following functions:

• Clearing and Settlement – payment services related to the exchange of goods and services.

• Risk Management – manage uncertainty and development and implementation of mitigation strategies and action plans.

• Transfer Economic Resources – facilitate the flow of economic resources targeting efficient use of capital.

• Information Sharing – provide stakeholders with access to risk ratings, price information and other types of information perceived as critical for making decisions in, or about, FSSs.

Following Schmidt and Tyrell (2004), we need to add Demand and Supply functions to the four functions mentioned above. Finally, we view the Resource Pooling function as being part of a mechanism that can be used to transfer economic resources and as a result combine functions the Transfer Economic Resources and Resource Pooling functions into one.

After the key functions have been identified, the next step is to generate a high-level description of each function. In the FRAM modelling framework, a function can be described by the following attributes:

• Input (I): that which the function processes or transforms, or that which starts the function. In financial services, this could be the information that is modified, interpreted, or used in any other way by the function.

• Output (O): that which is the result of the function, either an entity or a state change. In financial services, this can be economic resources for a party that previously did not have any economic resources. For example, Mr. Smith goes to a bank to apply for a mortgage and the bank decides to transfer economic resources to Mr. Smith, that is, provide Mr. Smith with a loan of some type.

• Preconditions (P): conditions that must be exist before a function can be executed. An example in financial services is the existence of a financial market with a defined demand and supply.

• Resources (R): that which the function needs, or consumes, to produce the output. This could be some type of financial assets and/or market participants such as investors.

• Time (T): temporal constraints affecting the function (with regard to starting time, finishing time, or duration). For example, the time of a transaction can greatly influence the value of an output in the financial services industry.

• Control (C): how the function is monitored or controlled. In financial services this can be a firm’s risk management function and /or a regulatory function such as a Central Bank. Table 13.1 lists the instantiations of the attributes of the two functions Risk Management and Transfer Economic Resources for Firm A.

In Table 13.1, the values of the attributes are shown as simple labels. Each value can, however, be described as the output of a function and the description of the initial functions can therefore be expanded until all the necessary functions have been defined. Notice also that the actual ‘mechanisms’ associated with execution of the functions do not need to be specified at this stage.

Table 13.1 also shows how two functions can be coupled by means of shared attribute values. For example, Risk Assessment is an output of ‘Risk Management’ as well as a pre-condition for ‘Transfer Economic Resources’. Functions can also be coupled by means of common attribute values, such as Regulators and Management that are part of the control attribute for both functions.

Table 13.1 FRAM descriptions of the functions ‘Risk Management’ and ‘Transfer Economic Resources’

Firm A: Risk management |

|

Attribute |

Assignments/values |

Input (I) |

Risk related data; Risk ratings; Risk ‘appetite’ |

Output (O) |

Risk assessment; Decisions |

Preconditions (P) |

Required data available; Perceived need to manage risks |

Resources (R) |

Risk methodology/processes |

Time (T) |

Deadline for risk assessment |

Control (C) |

Regulators; Management; Risk policies and procedures |

Firm A: Transfer economic resources |

|

Attribute |

Assignments / values |

Input (I) |

Request for economic resources |

Output (O) |

Economic resources available to requestor |

Preconditions (P) |

Risk assessment; Transfer mechanisms |

Resources (R) |

Funds |

Time (T) |

Deadline for transfer |

Control (C) |

Regulators; Management; Transfer policies and procedures |

Identifying Potential for Functional Resonance

Functional resonance is an emergent attribute of a system, which means that it cannot simply be derived from descriptions of the constituent parts of the system. Unlike the traditional safety paradigm, Resilience Engineering does not assume that there is a simple causal relation between the parts and the whole. In a FSS, a single entity with a high default risk (i.e., the risk that a borrower will not be able to meet debt obligations) may be coupled to other entities with a high default risk via a securitisation process. When otherwise independent entities become interconnected this can create the potential of functional resonance in the overall system, that is, an amplification of the impact of outcomes that may lead to disproportionate losses (or gains). The output of one function may, for instance, provide the resources of another function. Or, the output of one function may be a pre-condition for another function. Table 13.2 lists the values that are used to describe the attributes of the two functions ‘Demand Economic Resources’ and ‘Supply Economic Resources’. Figure 13.3 provides a graphical illustration of the most important couplings between the functions described in Tables 13.1 and 13.2.

Some key lessons from Figure 13.3 include:

• If Firm A completely depends on markets to generate its ‘raw material’ (funds) in order to be able to transfer economic resources, any unusual variation in the system level functions will have impact on Firm A’s ability to meet customers’ requests.

• While Firm A might be able to generate funds to fulfil customer requests, the ability to sustain performance depends on how Firm A can replenish the ‘raw material’, that is, capital. One way for Firm A to replenish funds is by having a traditional banking function. Another method is to leverage capital markets.

• The Demand and Supply functions are interconnected, that is, Supply requires a certain Demand and vice versa. The interaction between these two functions is the key subject for economists interested in the laws of demand and supply. From a functional modelling perspective, the focus should be on how the behaviour of the two functions impact individual firms. From a systemic perspective, the impact of financial services’ demand and supply functions on the overall system should be the primary interest of economists and macro-prudential regulatory bodies such as central banks.

Figure 13.3 Interdependency of Firm A’s risk management and transfer of economic resources functions

Table 13.2 Two FRAM functions with assigned values

System: Demand Economic Resources |

|

Attribute |

Assignments/values |

Input (I) |

Cost of credit; Preference for economic resources type |

Output (O) |

Market demand for economic resource |

Preconditions (P) |

Raw material (capital); Potential ‘buyers’ |

Resources (R) |

Not defined |

Time (T) |

Deadline for risk assessment |

Control (C) |

Regulators; Management |

System: Supply Economic Resources |

|

Attribute |

Assignments/values |

Input (I) |

Cost to produce economic resource |

Output (O) |

Raw material (capital) |

Preconditions (P) |

Knowledge and tools to establish resources; Market demand for economic resource |

Resources (R) |

‘Raw’ material (capital) |

Time (T) |

Request fulfilment deadline |

Control (C) |

Regulators; Management |

Identifying How Performance Variance can be Monitored and Controlled

There are three types of management and control functions in a FSS. First, an individual firm’s management function responsible for driving business results while managing risks at the same time. Second, a micro-prudential regulatory function responsible for oversight of individual firms. Third, a macro-prudential regulatory function responsible for oversight of the overall FSS. In order to be able to monitor and, as required, control and regulate performance of individual firms, groups of firms and of course the overall FSS, each of these functions needs the following:

• A view of the system that is being monitored.

• A view of what needs to be monitored.

• Data and metrics required to perform the monitoring.

A functional model can provide guidance with respect to the first two. A risk assessment and monitoring methodology may provide guidance for the third. We can use a functional model to consider how a micro-prudential regulator might choose to monitor Firm A, based on the functional interdependencies illustrated in Figure 13.3. Table 13.3 lists the values that are used to describe the attributes of how a micro-prudential regulator may choose to monitor Firm A.

The description of the main function of a micro-prudential regulator in Table 13.3 shows the following:

• A micro-prudential regulator cannot monitor and/or determine Firm A’s risk profile without including data about system level components such as the Demand and Supply functions.

• A micro-prudential regulator needs to know what data is required to perform risk assessments, that is, the regulator needs to understand Firm A’s business model and services and have a risk assessment and monitoring methodology that helps to specify what data is required.

• The Information Sharing function is a critical component of the overall Financial Services System. Without transparency, various stakeholders are likely to lose trust.

Table 13.3 The FRAM functions of a micro-prudential regulator (of Firm A)

Micro-prudential Regulator: Firm A |

|

Attribute |

Assignments/values |

Input (I) |

Firm A’s credit portfolio risk; Risk rating; Firm A’s risk ‘appetite’; Demand/supply of economic resources; Firm A’s business model; Risk profile of comparable firms |

Output (O) |

Firm A’s risk profile; Decisions; Guidance |

Preconditions (P) |

Perceived need to assess Firm A’s risk profile |

Resources (R) |

Risk methodology & processes; Data |

Time (T) |

Per examination schedule; ad hoc based on (P) |

Control (C) |

Regulators; Risk policies and procedures |

Micro-prudential Regulator: Information Sharing |

|

Attribute |

Assignments/values |

Input (I) |

Information sharing request |

Output (O) |

Economic resources available to requestor |

Preconditions (P) |

Required data available (from overall system and Firm A) |

Resources (R) |

Data from Firm A; Processing mechanism |

Time (T) |

Per examination schedule; ad hoc |

Control (C) |

Regulators; Firm A’s management |

The next section will use the above principles to show why Northern Rock’s leaders and regulators failed to have a valid view of Northern Rock and its interdependencies with other system level components.

Example: The Demise of Northern Rock

Northern Rock was listed on the London Stock Exchange in 1997 and was seen as a very successful financial services firm. All of this changed when on 14 September, 2007 Northern Rock had to ask the Bank of England for a line of credit to overcome a ‘liquidity crunch’. The damage to Northern Rock’s reputation was lethal and the firm experienced a classic bank run. In February 2008, Northern Rock was nationalised and as a result is no longer traded as a public company. In retrospect, Northern Rock was one of the first institutions outside the US that experienced the impact of the 2007–2009 crisis in the global financial system.

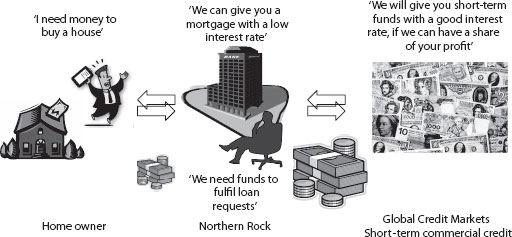

Northern Rock’s business model is illustrated in Figure 13.4. Basically, Northern Rock’s business consisted of transfer of economic resources to retail customers. Northern Rock’s ability to transfer economic resources depended on two sources of funding:

• Twenty-five per cent of customers’ requests for mortgages were met by bank deposits, that is, funds from banking customers’ deposits.

• The remaining 75 per cent were fulfilled by getting funds from the global credit markets. As we all know these markets started to experience major distress in the summer of 2007.

Figure 13.4 Northern Rock’s business model

The simplified representation in Figure 13.5 illustrates the risks that were a consequence of Northern Rock’s reliance on funding from global credit markets to fulfil 75 per cent of the mortgages. (Grey hexagons indicate that a function operates outside of Northern Rock’s control.) This funding depended on a consistently positive output from the Global Credit Markets’ ‘Transfer Economic Resources’ function. However, key preconditions for this were good credit ratings and positive Investor risk assessments of the financial instruments offered by Northern Rock.

When financial markets became increasingly distressed in 2007, investors’ trust in mortgage backed financial instruments severely deteriorated resulting in zero demand. As a result Northern Rock experienced an acute liquidity crisis due to its high dependence on mortgaged backed securitisation as a method of creating funds to fulfil loan requests by their customers.

The primary purpose of the present chapter was to illustrate how Resilience Engineering can provide the financial services industry with a different way to understand risk at both a macro- and micro-prudential level. We discussed the need of the various stakeholders to be clear about what the FSS is in any particular situation. In addition, multiple stakeholders will need a shared view of the system. As discussed in the chapter, creating such a shared view requires a common model of the FSS. In this chapter, we suggested to use a functional approach leveraging the work by Merton (1995) and others. Such an approach enables stakeholders and decision makers to focus on behaviour rather than on the specifics of an individual financial services institution. A key advantage of a functional perspective is that it becomes possible to discover risks created by functional interdependencies among individual institutions and system components, as illustrated by the case of Northern Rock. The concepts and functional modelling approach outlined in the present chapter thus provides the basis for the development of a standardised method to capture and better understand risk in the financial services industry.

Figure 13.5 Functional view of northern Rock’s risk exposure