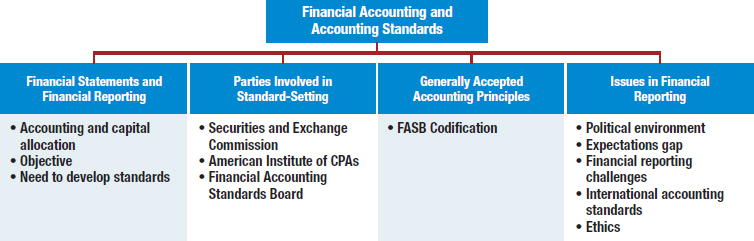

CHAPTER 1 Financial Accounting and Accounting Standards

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Identify the major financial statements and other means of financial reporting.

- Explain how accounting assists in the efficient use of scarce resources.

- Identify the objective of financial reporting.

- Explain the need for accounting standards.

- Identify the major policy-setting bodies and their role in the standard-setting process.

- Explain the meaning of generally accepted accounting principles (GAAP) and the role of the Codification for GAAP.

- Describe the impact of user groups on the rule-making process.

- Describe some of the challenges facing financial reporting.

- Understand issues related to ethics and financial accounting.

We Can Do Better

A recent report says it best: “Accounting information is central to the functioning of international capital markets and to managing small businesses, conducting effective government, understanding business processes, and … how economic decisions are made. … Across the globe, a common characteristic of economies that flourish is the presence of reliable accounting information.”

Many in the United States take pride in our system of financial reporting as being the most robust and transparent in the world. But most would also comment that we can do better, particularly in light of the many accounting scandals that have occurred at companies like AIG, WorldCom, and Lehman Brothers, and the financial crisis of 2008.

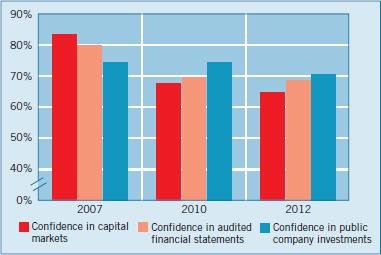

To better understand where we are today, the Center for Audit Quality conducts a yearly survey that measures investor confidence in such categories as U.S. capital markets, audited financial information, and U.S. publicly traded companies. Here are the results:

The results indicate that the 2008 financial crisis took a bite out of investor confidence. While investor confidence in U.S. markets, auditors, and public companies has stabilized, the question is how can we improve? Here are some possibilities on how we can enhance the existing system of financial reporting.

- Today, equity securities are broadly held, with approximately half of American households investing in stocks. This presents a challenge—investors have expressed concerns that one-size-fits-all financial reports do not meet the needs of the spectrum of investors who rely on those reports. While many individual investors are more interested in summarized, plain-English reports, market analysts and other investment professionals may desire information at a far more detailed level than is currently provided. Technology may help customize the information that the different types of investors desire.

- Companies also express concerns with the complexity of the financial reporting system. Companies assert that when preparing financial reports, it is difficult to ensure compliance with the voluminous and complex requirements contained in U.S. GAAP and SEC reporting rules. This is a particularly heavy burden on smaller, non-public companies, which may have fewer resources to comply with the wide range of rules.

- We also need to consider the broader array of information that investors need to make informed decisions. As some have noted, the percentage of a company's market value that can be attributed to accounting book value has declined significantly from the days of a bricks-and-mortar economy. Thus, we may want to consider a more comprehensive business reporting model, including both financial and nonfinancial key performance indicators.

CONCEPTUAL FOCUS

CONCEPTUAL FOCUS- See the Underlying Concepts on pages 6 and 7.

- Read the Evolving Issue on page 17 for a discussion of the use of fair value accounting.

INTERNATIONAL FOCUS

INTERNATIONAL FOCUS- See the International Perspectives on pages 8, 9, 10, 17, and 20.

- Read the IFRS Insights on pages 31–39 for a discussion of:

- International standard-setting organizations

- Hierarchy of IFRS

- International accounting convergence

- Finally, we must also consider how to deliver all of this information in a timelier manner. In a world where messages can be sent across the world in a blink of an eye, it is ironic that the analysis of financial information is still subject to many manual processes, resulting in delays, increased costs, and errors.

Thus, improving financial reporting involves more than simply trimming or reworking the existing accounting literature. In some cases, major change is already underway. For example:

- The FASB and IASB are working on a convergence project, which will contribute to less-complex, more-understandable standards in the important areas of revenue recognition, leasing, and financial instruments.

- Standard-setters are exploring expanded reporting of key performance indicators, including reports on sustainability and a disclosure framework project to improve the effectiveness of disclosures to clearly communicate the information that is most important to users of financial statements. This project, combined with the introduction of a private-company reporting framework, could go a long way to address one-size-fits-all challenges.

- The SEC now requires the delivery of financial reports using eXtensible Business Reporting Language (XBRL). Reporting through XBRL allows timelier reporting via the Internet and allows statement users to transform accounting reports to meet their specific needs.

Each of these projects will hopefully support improvements in the quality of financial reporting and increase confidence in U.S. capital markets.

Sources: Adapted from The Pathways Commission, “Charting a National Strategy for the Next Generation of Accountants” (AAA, AICPA, July 2012); Conrad W. Hewitt, “Opening Remarks Before the Initial Meeting of the SEC Advisory Committee on Improvements to Financial Reporting,” U.S. Securities and Exchange Commission, Washington, D.C. (August 2, 2007); and Center for Audit Quality, Main Street Investor Survey (September 2012). See www.fasb.org for updates on FASB/IASB convergence, disclosure, and private company decision-making projects.

PREVIEW OF CHAPTER 1

As our opening story indicates, the U.S. system of financial reporting has long been the most robust and transparent in the world. However, to ensure that it continues to provide the most relevant and reliable financial information to users, a number of financial reporting issues must be resolved. These issues include such matters as adopting global standards, increasing fair value reporting, and meeting multiple user needs. This chapter explains the environment of financial reporting and the many factors affecting it, as follows.

FINANCIAL STATEMENTS AND FINANCIAL REPORTING

The essential characteristics of accounting are (1) the identification, measurement, and communication of financial information about (2) economic entities to (3) interested parties. Financial accounting is the process that culminates in the preparation of financial reports on the enterprise for use by both internal and external parties. Users of these financial reports include investors, creditors, managers, unions, and government agencies. In contrast, managerial accounting is the process of identifying, measuring, analyzing, and communicating financial information needed by management to plan, control, and evaluate a company's operations.

Financial statements are the principal means through which a company communicates its financial information to those outside it. These statements provide a company's history quantified in money terms. The financial statements most frequently provided are (1) the balance sheet, (2) the income statement, (3) the statement of cash flows, and (4) the statement of owners' or stockholders' equity. Note disclosures are an integral part of each financial statement.

Some financial information is better provided, or can be provided only, by means of financial reporting other than formal financial statements. Examples include the president's letter or supplementary schedules in the corporate annual report, prospectuses, reports filed with government agencies, news releases, management's forecasts, and social or environmental impact statements. Companies may need to provide such information because of authoritative pronouncement, regulatory rule, or custom. Or they may supply it because management wishes to disclose it voluntarily.

In this textbook, we focus on the development of two types of financial information: (1) the basic financial statements and (2) related disclosures.

Accounting and Capital Allocation

LEARNING OBJECTIVE ![]()

Explain how accounting assists in the efficient use of scarce resources.

Resources are limited. As a result, people try to conserve them and ensure that they are used effectively. Efficient use of resources often determines whether a business thrives. This fact places a substantial burden on the accounting profession.

Accountants must measure performance accurately and fairly on a timely basis, so that the right managers and companies are able to attract investment capital. For example, relevant and reliable financial information allows investors and creditors to compare the income and assets employed by such companies as IBM, McDonald's, Microsoft, and Ford. Because these users can assess the relative return and risks associated with investment opportunities, they channel resources more effectively. Illustration 1-1 shows how this process of capital allocation works.

An effective process of capital allocation is critical to a healthy economy. It promotes productivity, encourages innovation, and provides an efficient and liquid market for buying and selling securities and obtaining and granting credit. Unreliable and irrelevant information leads to poor capital allocation, which adversely affects the securities markets.

What do the numbers mean? IT'S THE ACCOUNTING

“It's the accounting.” That's what many investors seem to be saying these days. Even the slightest hint of any accounting irregularity at a company leads to a subsequent pounding of the company's stock price. For example, the Wall Street Journal has run the following headlines related to accounting and its effects on the economy.

- Stocks take a beating as accounting woes spread beyond Enron.

- Quarterly reports from IBM and Goldman Sachs sent stocks tumbling.

- VeriFone finds accounting issues; stock price cut in half.

- Bank of America admits hiding debt.

- Facebook, Zynga, Groupon: IPO drops due to accounting, not valuation.

It now has become clear that investors must trust the accounting numbers, or they will abandon the market and put their resources elsewhere. With investor uncertainty, the cost of capital increases for companies who need additional resources. In short, relevant and reliable financial information is necessary for markets to be efficient.

Objective of Financial Reporting

LEARNING OBJECTIVE ![]()

Identify the objective of financial reporting.

What is the objective (or purpose) of financial reporting? The objective of general-purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in decisions about providing resources to the entity. Those decisions involve buying, selling, or holding equity and debt instruments, and providing or settling loans and other forms of credit. Information that is decision-useful to capital providers (investors) may also be helpful to other users of financial reporting who are not investors. Let's examine each of the elements of this objective.1

General-Purpose Financial Statements

General-purpose financial statements provide financial reporting information to a wide variety of users. For example, when The Hershey Company issues its financial statements, these statements help shareholders, creditors, suppliers, employees, and regulators to better understand its financial position and related performance. Hershey's users need this type of information to make effective decisions. To be cost-effective in providing this information, general-purpose financial statements are most appropriate. In other words, general-purpose financial statements provide at the least cost the most useful information possible.

Equity Investors and Creditors

The objective of financial reporting identifies investors and creditors as the primary users for general-purpose financial statements. Identifying investors and creditors as the primary users provides an important focus of general-purpose financial reporting. For example, when Hershey issues its financial statements, its primary focus is on investors and creditors because they have the most critical and immediate need for information in financial reports. Investors and creditors need this financial information to assess Hershey's ability to generate net cash inflow and to understand management's ability to protect and enhance the assets of the company, which will be used to generate future net cash inflows. As a result, the primary user groups are not management, regulators, or some other non-investor group.

![]() Underlying Concepts

Underlying Concepts

While the objective of financial reporting is focused on investors and creditors, financial statements may still meet the needs of others.

Entity Perspective

As part of the objective of general-purpose financial reporting, an entity perspective is adopted. Companies are viewed as separate and distinct from their owners (present shareholders) using this perspective. The assets of Hershey are viewed as assets of the company and not of a specific creditor or shareholder. Rather, these investors have claims on Hershey's assets in the form of liability or equity claims. The entity perspective is consistent with the present business environment where most companies engaged in financial reporting have substance distinct from their investors (both shareholders and creditors). Thus, a perspective that financial reporting should be focused only on the needs of shareholders—often referred to as the proprietary perspective—is not considered appropriate.

What do the numbers mean? DON’T FORGET STEWARDSHIP

In addition to providing decision-useful information about future cash flows, management also is accountable to investors for the custody and safekeeping of the company's economic resources and for their efficient and profitable use. For example, the management of The Hershey Company has the responsibility for protecting its economic resources from unfavorable effects of economic factors, such as price changes, and technological and social changes. Because Hershey's performance in discharging its responsibilities (referred to as its stewardship responsibilities) usually affects its ability to generate net cash inflows, financial reporting may also provide decision-useful information to assess management performance in this role.

Source: Chapter 1, “The Objective of General Purpose Financial Reporting,” and Chapter 3, “Qualitative Characteristics of Useful Financial Information,” Statement of Financial Accounting Concepts No. 8 (Norwalk, Conn.: FASB, September 2010), paras. OB4–OB10.

Decision-Usefulness

Investors are interested in financial reporting because it provides information that is useful for making decisions (referred to as the decision-usefulness approach). As indicated earlier, when making these decisions, investors are interested in assessing (1) the company's ability to generate net cash inflows and (2) management's ability to protect and enhance the capital providers' investments. Financial reporting should therefore help investors assess the amounts, timing, and uncertainty of prospective cash inflows from dividends or interest, and the proceeds from the sale, redemption, or maturity of securities or loans. In order for investors to make these assessments, the economic resources of an enterprise, the claims to those resources, and the changes in them must be understood. Financial statements and related explanations should be a primary source for determining this information.

The emphasis on “assessing cash flow prospects” does not mean that the cash basis is preferred over the accrual basis of accounting. Information based on accrual accounting better indicates a company's present and continuing ability to generate favorable cash flows than does information limited to the financial effects of cash receipts and payments.

Recall from your first accounting course the objective of accrual-basis accounting: It ensures that a company records events that change its financial statements in the periods in which the events occur, rather than only in the periods in which it receives or pays cash. Using the accrual basis to determine net income means that a company recognizes revenues when it provides the goods or services rather than when it receives cash. Similarly, it recognizes expenses when it incurs them rather than when it pays them. Under accrual accounting, a company generally recognizes revenues when it makes sales. The company can then relate the revenues to the economic environment of the period in which they occurred. Over the long run, trends in revenues and expenses are generally more meaningful than trends in cash receipts and disbursements.2

The Need to Develop Standards

LEARNING OBJECTIVE ![]()

Explain the need for accounting standards.

The main controversy in setting accounting standards is, “Whose rules should we play by, and what should they be?” The answer is not immediately clear. Users of financial accounting statements have both coinciding and conflicting needs for information of various types. To meet these needs, and to satisfy the stewardship reporting responsibility of management, companies prepare a single set of general-purpose financial statements. Users expect these statements to present fairly, clearly, and completely the company's financial operations.

![]() Underlying Concepts

Underlying Concepts

Preparing financial statements prepared according to accepted accounting standards contributes to the comparability of accounting information.

The accounting profession has attempted to develop a set of standards that are generally accepted and universally practiced. Otherwise, each company would have to develop its own standards. Further, readers of financial statements would have to familiarize themselves with every company's peculiar accounting and reporting practices. It would be almost impossible to prepare statements that could be compared.

This common set of standards and procedures is called generally accepted accounting principles (GAAP). The term “generally accepted” means either that an authoritative accounting rule-making body has established a principle of reporting in a given area or that over time a given practice has been accepted as appropriate because of its universal application.3 Although principles and practices continue to provoke both debate and criticism, most members of the financial community recognize them as the standards that over time have proven to be most useful. We present a more extensive discussion of what constitutes GAAP later in this chapter.

PARTIES INVOLVED IN STANDARD-SETTING

LEARNING OBJECTIVE ![]()

Identify the major policy-setting bodies and their role in the standard-setting process.

Three organizations are instrumental in the development of financial accounting standards (GAAP) in the United States:

- Securities and Exchange Commission (SEC)

- American Institute of Certified Public Accountants (AICPA)

- Financial Accounting Standards Board (FASB)

Securities and Exchange Commission (SEC)

External financial reporting and auditing developed in tandem with the growth of the industrial economy and its capital markets. However, when the stock market crashed in 1929 and the nation's economy plunged into the Great Depression, there were calls for increased government regulation of business, especially financial institutions and the stock market.

![]() International Perspective

International Perspective

The International Organization of Securities Commissions (IOSCO), established in 1987, consists of more than 100 securities regulatory agencies or securities exchanges from all over the world. Collectively, its members represent a substantial proportion of the world's capital markets. The SEC is a member of IOSCO.

As a result of these events, the federal government established the Securities and Exchange Commission (SEC) to help develop and standardize financial information presented to stockholders. The SEC is a federal agency. It administers the Securities Exchange Act of 1934 and several other acts. Most companies that issue securities to the public or are listed on a stock exchange are required to file audited financial statements with the SEC. In addition, the SEC has broad powers to prescribe, in whatever detail it desires, the accounting practices and standards to be employed by companies that fall within its jurisdiction. The SEC currently exercises oversight over 12,000 companies that are listed on the major exchanges (e.g., the New York Stock Exchange and the Nasdaq).

Public/Private Partnership

At the time the SEC was created, no group—public or private—issued accounting standards. The SEC encouraged the creation of a private standard-setting body because it believed that the private sector had the appropriate resources and talent to achieve this daunting task. As a result, accounting standards have developed in the private sector either through the American Institute of Certified Public Accountants (AICPA) or the Financial Accounting Standards Board (FASB).

The SEC has affirmed its support for the FASB by indicating that financial statements conforming to standards set by the FASB are presumed to have substantial authoritative support. In short, the SEC requires registrants to adhere to GAAP. In addition, the SEC indicated in its reports to Congress that “it continues to believe that the initiative for establishing and improving accounting standards should remain in the private sector, subject to Commission oversight.”

SEC Oversight

The SEC's partnership with the private sector works well. The SEC acts with remarkable restraint in the area of developing accounting standards. Generally, the SEC relies on the FASB to develop accounting standards.

The SEC's involvement in the development of accounting standards varies. In some cases, the SEC rejects a standard proposed by the private sector. In other cases, the SEC prods the private sector into taking quicker action on certain reporting problems, such as accounting for investments in debt and equity securities and the reporting of derivative instruments. In still other situations, the SEC communicates problems to the FASB, responds to FASB exposure drafts, and provides the FASB with counsel and advice upon request.

The SEC's mandate is to establish accounting principles. The private sector, therefore, must listen carefully to the views of the SEC. In some sense, the private sector is the formulator and the implementor of the standards.4 However, when the private sector fails to address accounting problems as quickly as the SEC would like, the partnership between the SEC and the private sector can be strained. This occurred in the deliberations on the accounting for business combinations and intangible assets. It is also highlighted by concerns over the accounting for off-balance-sheet special-purpose entities, highlighted in the failure of Enron and, more recently, the subprime crises that led to the failure of IndyMac Bank.

![]() International Perspective

International Perspective

The U.S. legal system is based on English common law, whereby the government generally allows professionals to make the rules. The private sector, therefore, develops these rules (standards). Conversely, some countries have followed codified law, which leads to government-run accounting systems.

Enforcement

As we indicated earlier, companies listed on a stock exchange must submit their financial statements to the SEC. If the SEC believes that an accounting or disclosure irregularity exists regarding the form or content of the financial statements, it sends a deficiency letter to the company. Companies usually resolve these deficiency letters quickly. If disagreement continues, the SEC may issue a “stop order,” which prevents the registrant from issuing or trading securities on the exchanges. The Department of Justice may also file criminal charges for violations of certain laws. The SEC process, private sector initiatives, and civil and criminal litigation help to ensure the integrity of financial reporting for public companies.

American Institute of Certified Public Accountants (AICPA)

The American Institute of Certified Public Accountants (AICPA), which is the national professional organization of practicing Certified Public Accountants (CPAs), has been an important contributor to the development of GAAP. Various committees and boards established since the founding of the AICPA have contributed to this effort.

Committee on Accounting Procedure

At the urging of the SEC, the AICPA appointed the Committee on Accounting Procedure in 1939. The Committee on Accounting Procedure (CAP) composed of practicing CPAs, issued 51 Accounting Research Bulletins during the years 1939 to 1959. These bulletins dealt with a variety of accounting problems. But this problem-by-problem approach failed to provide the needed structured body of accounting principles. In response, in 1959 the AICPA created the Accounting Principles Board.

Accounting Principles Board

The major purposes of the Accounting Principles Board (APB) were to (1) advance the written expression of accounting principles, (2) determine appropriate practices, and (3) narrow the areas of difference and inconsistency in practice. To achieve these objectives, the APB's mission was twofold: to develop an overall conceptual framework to assist in the resolution of problems as they become evident and to substantively research individual issues before the AICPA issued pronouncements. The Board's 18 to 21 members, selected primarily from public accounting, also included representatives from industry and academia. The Board's official pronouncements, called APB Opinions, were intended to be based mainly on research studies and be supported by reason and analysis. Between its inception in 1959 and its dissolution in 1973, the APB issued 31 opinions.

Unfortunately, the APB came under fire early, charged with lack of productivity and failing to act promptly to correct alleged accounting abuses. Later, the APB tackled numerous thorny accounting issues, only to meet a buzz saw of opposition from industry and CPA firms. It also ran into occasional governmental interference. In 1971, the accounting profession's leaders, anxious to avoid governmental rule-making, appointed a Study Group on Establishment of Accounting Principles. Commonly known as the Wheat Committee for its chair Francis Wheat, this group examined the organization and operation of the APB and determined the necessary changes to attain better results. The Study Group submitted its recommendations to the AICPA Council in the spring of 1972, which led to the replacement of the APB with the Financial Accounting Standards Board (FASB) in 1973.

Changing Role of the AICPA

When the FASB replaced the Accounting Principles Board, the AICPA established the Accounting Standards Executive Committee (AcSEC) as the committee authorized to speak for the AICPA in the area of financial accounting and reporting. It does so through various written communications:

Audit and Accounting Guides summarize the accounting practices of specific industries and provide specific guidance on matters not addressed by the FASB. Examples are accounting for casinos, airlines, colleges and universities, banks, insurance companies, and many others.

![]() International Perspective

International Perspective

The CPA exam is administered internationally at testing sites in Bahrain, Kuwait, Japan, Lebanon, United Arab Emirates (UAE), and Brazil. The CPA exam now has some coverage of IFRS knowledge as part of the financial reporting section of the exam (see www.aicpa.org/cpa-exam).

Statements of Position (SOPs) provide guidance on financial reporting topics until the FASB sets standards on the issue in question. SOPs may update, revise, and clarify audit and accounting guides or provide free-standing guidance.

Practice Bulletins indicate the AcSEC's views on narrow financial reporting issues not considered by the FASB.

The role of the AICPA in standard-setting has diminished. The FASB and the AICPA agree that the AICPA and AcSEC no longer will issue authoritative accounting guidance for public companies. Furthermore, while the AICPA has been the leader in developing auditing standards through its Auditing Standards Board, the Sarbanes-Oxley Act of 2002 requires the Public Company Accounting Oversight Board to oversee the development of auditing standards. The AICPA continues to develop and grade the CPA examination, which is administered in all 50 states.

Financial Accounting Standards Board (FASB)

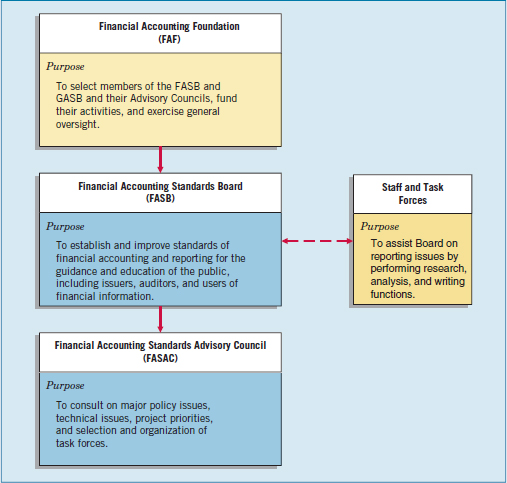

The Wheat Committee's recommendations resulted in the creation of a new standard-setting structure composed of three organizations—the Financial Accounting Foundation (FAF), the Financial Accounting Standards Board (FASB), and the Financial Accounting Standards Advisory Council (FASAC). The Financial Accounting Foundation selects the members of the FASB and the Advisory Council, funds their activities, and generally oversees the FASB's activities.

The major operating organization in this three-part structure is the Financial Accounting Standards Board (FASB). Its mission is to establish and improve standards of financial accounting and reporting for the guidance and education of the public, which includes issuers, auditors, and users of financial information. The expectations of success and support for the new FASB relied on several significant differences between it and its predecessor, the APB:

- Smaller membership. The FASB consists of seven members, replacing the relatively large 18-member APB.

- Full-time, remunerated membership. FASB members are well-paid, full-time members appointed for renewable 5-year terms. The APB members volunteered their part-time work.

- Greater autonomy. The APB was a senior committee of the AICPA. The FASB is not part of any single professional organization. It is appointed by and answerable only to the Financial Accounting Foundation.

- Increased independence. APB members retained their private positions with firms, companies, or institutions. FASB members must sever all such ties.

- Broader representation. All APB members were required to be CPAs and members of the AICPA. Currently, it is not necessary to be a CPA to be a member of the FASB.

In addition to research help from its own staff, the FASB relies on the expertise of various task force groups formed for various projects and on the Financial Accounting Standards Advisory Council (FASAC). The FASAC consults with the FASB on major policy and technical issues and also helps select task force members. Illustration 1-2 shows the current organizational structure for the development of financial reporting standards.5

Due Process

In establishing financial accounting standards, the FASB relies on two basic premises. (1) The FASB should be responsive to the needs and viewpoints of the entire economic community, not just the public accounting profession. (2) It should operate in full view of the public through a “due process” system that gives interested persons ample opportunity to make their views known. To ensure the achievement of these goals, the FASB follows specific steps to develop a typical FASB pronouncement, as Illustration 1-3 (page 12) shows.

The passage of new FASB guidance in the form of an Accounting Standards Update requires the support of four of the seven Board members. FASB pronouncements are considered GAAP and thereby binding in practice. All ARBs and APB Opinions implemented by 1973 (when the FASB formed) continue to be effective until amended or superseded by FASB pronouncements. In recognition of possible misconceptions of the term “principles,” the FASB uses the term financial accounting standards in its pronouncements.

Types of Pronouncements

The FASB issues two major types of pronouncements:

- Accounting Standards Updates.

- Financial Accounting Concepts.

Accounting Standards Updates. The FASB issues accounting pronouncements through Accounting Standards Updates (Updates). These Updates amend the Accounting Standards Codification, which represents the source of authoritative accounting standards, other than standards issued by the SEC. Each Update explains how the Codification has been amended and also includes information to help the reader understand the changes and when those changes will be effective. Common forms of amendments are accounting standards issued that address a broad area of accounting practice (such as the accounting for leases) or interpretations that modify or extend existing standards. Prior standard-setters such as the APB also issued interpretations of APB Opinions.

A second type of Update is a consensus of the Emerging Issues Task Force (EITF), created in 1984 by the FASB. The EITF is comprised of representatives from CPA firms and financial statement preparers. Observers from the SEC and AICPA also attend EITF meetings. The purpose of the task force is to reach a consensus on how to account for new and unusual financial transactions that may potentially create differing financial reporting practices. Examples include accounting for pension plan terminations, revenue from barter transactions by Internet companies, and excessive amounts paid to takeover specialists. The EITF also provided timely guidance for the accounting for loans and investments in the wake of the credit crisis.

The EITF helps the FASB in many ways. The EITF identifies controversial accounting problems as they arise. The EITF determines whether it can quickly resolve them or whether to involve the FASB in solving them. In essence, it becomes a “problem filter” for the FASB. Thus, the FASB will hopefully work on more pervasive long-term problems, while the EITF deals with short-term emerging issues.

We cannot overestimate the importance of the EITF. In one year, for example, the task force examined 61 emerging financial reporting issues and arrived at a consensus on approximately 75 percent of them. The FASB reviews and approves all EITF consensuses. And the SEC indicated that it will view consensus solutions as preferred accounting. Further, it requires persuasive justification for departing from them.

Financial Accounting Concepts. As part of a long-range effort to move away from the problem-by-problem approach, the FASB in November 1978 issued the first in a series of Statements of Financial Accounting Concepts as part of its conceptual framework project. (The Concepts Statement can be accessed at http://www.fasb.org/.) The series sets forth fundamental objectives and concepts that the Board uses in developing future standards of financial accounting and reporting. The Board intends to form a cohesive set of interrelated concepts—a conceptual framework—that will serve as tools for solving existing and emerging problems in a consistent manner. Unlike a Statement of Financial Accounting Standards, a Statement of Financial Accounting Concepts does not establish GAAP. Concepts statements, however, pass through the same due process system (preliminary views, public hearing, exposure draft, etc.) as do standards statements.

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES

LEARNING OBJECTIVE ![]()

Explain the meaning of generally accepted accounting principles (GAAP) and the role of the Codification for GAAP.

Generally accepted accounting principles (GAAP) have substantial authoritative support. The AICPA's Code of Professional Conduct requires that members prepare financial statements in accordance with GAAP. Specifically, Rule 203 of this Code prohibits a member from expressing an unqualified opinion on financial statements that contain a material departure from generally accepted accounting principles.

What is GAAP? The major sources of GAAP come from the organizations discussed earlier in this chapter. It is composed of a mixture of over 2,000 documents that have been developed over the last 70 years or so. It includes APB Opinions, FASB Standards, and AICPA Research Bulletins. In addition, the FASB has issued interpretations and FASB Staff Positions that modified or extended existing standards. The APB also issued interpretations of APB Opinions. Both types of interpretations are considered authoritative for purposes of determining GAAP. Since replacing the APB, the FASB has issued over 160 standards, 48 interpretations, and nearly 100 staff positions. Illustration 1-4 highlights the many different types of documents that comprise GAAP.

What do the numbers mean? YOU HAVE TO STEP BACK

Should the accounting profession have principles-based standards or rules-based standards? Critics of the profession today say that over the past three decades, standard-setters have moved away from broad accounting principles aimed at ensuring that companies' financial statements are fairly presented.

Instead, these critics say, standard-setters have moved toward drafting voluminous rules that, if technically followed in “check-box” fashion, may shield auditors and companies from legal liability. That has resulted in companies creating complex capital structures that comply with GAAP but hide billions of dollars of debt and other obligations. To add fuel to the fire, the chief accountant of the enforcement division of the SEC noted, “One can violate SEC laws and still comply with GAAP.”

In short, what he is saying is that it is not enough just to check the boxes. This point was reinforced by the Chief Accountant of the SEC, who remarked that judgments should result in “accounting that reflects the substance of the transaction, as well as being in accordance with the literature.” That is, you have to exercise judgment in applying GAAP to achieve high-quality reporting.

Sources: Adapted from S. Liesman, “SEC Accounting Cop's Warning: Playing by the Rules May Not Head Off Fraud Issues,” Wall Street Journal (February 12, 2002), p. C7. See also “Study Pursuant to Section 108(d) of the Sarbanes-Oxley Act of 2002 on the Adoption by the United States Financial Reporting System of a Principles-Based Accounting System,” SEC (July 25, 2003); and E. Orenstein, “Accounting as Art vs. Science, and the Role of Professional Judgment,” Accounting Matters, FEI Financial Reporting Blog (November, 2009).

FASB Codification

Historically, the documents that comprised GAAP varied in format, completeness, and structure. In some cases, these documents were inconsistent and difficult to interpret. As a result, financial statement preparers sometimes were not sure whether they had the right GAAP. Determining what was authoritative and what was not became difficult.

In response to these concerns, the FASB developed the Financial Accounting Standards Board Accounting Standards Codification (or more simply, “the Codification”). The FASB's primary goal in developing the Codification is to provide in one place all the authoritative literature related to a particular topic. This will simplify user access to all authoritative U.S. generally accepted accounting principles. The Codification changes the way GAAP is documented, presented, and updated. It explains what GAAP is and eliminates nonessential information such as redundant document summaries, basis for conclusions sections, and historical content. In short, the Codification integrates and synthesizes existing GAAP; it does not create new GAAP. It creates one level of GAAP, which is considered authoritative. All other accounting literature is considered nonauthoritative.6

To provide easy access to this Codification, the FASB also developed the Financial Accounting Standards Board Codification Research System (CRS). CRS is an online, real-time database that provides easy access to the Codification. The Codification and the related CRS provide a topically organized structure, subdivided into topic, subtopics, sections, and paragraphs, using a numerical index system.

For purposes of referencing authoritative GAAP material in this textbook, we will use the Codification framework. Here is an example of how the Codification framework is cited, using Receivables as the example. The purpose of the search shown below is to determine GAAP for accounting for loans and trade receivables not held for sale subsequent to initial measurement.

| Topic | Go to FASB ASC 310 to access the Receivables topic. |

| Subtopics | Go to FASB ASC 310-10 to access the Overall Subtopic of the Topic 310. |

| Sections | Go to FASB ASC 310-10-35 to access the Subsequent Measurement Section of the Subtopic 310-10. |

| Paragraph | Go to FASB ASC 310-10-35-47 to access the Loans and Trade Receivables not Held for Sale paragraph of Section 310-10-35. |

Illustration 1-5 shows the Codification framework graphically.

What happens if the Codification does not cover a certain type of transaction or event? In that case, other accounting literature should be considered, such as FASB Concept Statements, international financial reporting standards, and other professional literature. This will happen only rarely.

The expectations for the Codification are high. It is hoped that the Codification will enable users to better understand what GAAP is. As a result, the time to research accounting issues and the risk of noncompliance with GAAP will be reduced, sometimes substantially. In addition, the Web-based format will make updating easier, which will help users stay current with GAAP.7

![]() See the FASB Codification section at the end of each chapter for Codification references and exercises.

See the FASB Codification section at the end of each chapter for Codification references and exercises.

For individuals (like you) attempting to learn GAAP, the Codification will be invaluable. It streamlines and simplifies how to determine what GAAP is, which will lead to better financial accounting and reporting. We provide references to the Codification throughout this textbook, using a numbering system. For example, a bracket with a number, such as [1], indicates that the citation to the FASB Codification can be found in the FASB Codification section at the end of the chapter (immediately before the assignment materials).

ISSUES IN FINANCIAL REPORTING

LEARNING OBJECTIVE ![]()

Describe the impact of user groups on the rule-making process.

Since the implementation of GAAP may affect many interests, much discussion occurs about who should develop GAAP and to whom it should apply. We discuss some of the major issues below.

GAAP in a Political Environment

User groups are possibly the most powerful force influencing the development of GAAP. User groups consist of those most interested in or affected by accounting rules. Like lobbyists in our state and national capitals, user groups play a significant role. GAAP is as much a product of political action as it is of careful logic or empirical findings. User groups may want particular economic events accounted for or reported in a particular way, and they fight hard to get what they want. They know that the most effective way to influence GAAP is to participate in the formulation of these rules or to try to influence or persuade the formulator of them.

These user groups often target the FASB, to pressure it to influence changes in the existing rules and the development of new ones.8 In fact, these pressures have been multiplying. Some influential groups demand that the accounting profession act more quickly and decisively to solve its problems. Other groups resist such action, preferring to implement change more slowly, if at all. Illustration 1-6 shows the various user groups that apply pressure.

Should there be politics in establishing GAAP for financial accounting and reporting? Why not? We have politics at home; at school; at the fraternity, sorority, and dormitory; at the office; and at church, temple, and mosque. Politics is everywhere. GAAP is part of the real world, and it cannot escape politics and political pressures.

That is not to say that politics in establishing GAAP is a negative force. Considering the economic consequences9 of many accounting rules, special interest groups should vocalize their reactions to proposed rules. What the Board should not do is issue pronouncements that are primarily politically motivated. While paying attention to its constituencies, the Board should base GAAP on sound research and a conceptual framework that has its foundation in economic reality.

Evolving Issue FAIR VALUE, FAIR CONSEQUENCES?

No recent accounting issue better illustrates the economic consequences of accounting than the current debate over the use of fair value accounting for financial assets. Both the FASB and the International Accounting Standards Board (IASB) have standards requiring the use of fair value accounting for financial assets, such as investments and other financial instruments. Fair value provides the most relevant and reliable information for investors about these assets and liabilities. However, in the wake of the recent credit crisis, some countries, their central banks, and bank regulators want to suspend fair value accounting, based on concerns that use of fair value accounting, which calls for recording significant losses on poorly performing loans and investments, could scare investors and depositors and lead to a “run on the bank.”

For example, in 2009, Congress ordered the FASB to change its accounting rules so as to reduce the losses banks reported, as the values of their securities had crumbled. These changes were generally supported by banks. But these changes produced a strong reaction from some investors, with one investor group complaining that the changes would “effectively gut the transparent application of fair value measurement.” The group also says suspending fair value accounting would delay the recovery of the banking system.

Such political pressure on accounting standard-setters is not confined to the United States. For example, French President Nicolas Sarkozy urged his European Union counterparts to back changes to accounting rules and give banks and insurers some breathing space amid the market turmoil. And more recently, international finance ministers are urging the FASB and IASB to accelerate their work on accounting standards, including the fair value guidance for financial instruments. It is unclear whether these political pressures will have an effect on fair value accounting, but there is no question that the issue has stirred significant worldwide political debate. In short, the numbers have consequences.

Sources: Adapted from Ben Hall and Nikki Tait, “Sarkozy Seeks EU Accounting Change,” The Financial Times Limited (September 30, 2008); Floyd Norris, “Banks Are Set to Receive More Leeway on Asset Values,” The New York Times (March 31, 2009); and E. Orenstein, “G20 Finance Ministers Urge FASB, IASB Converge Key Standards by Mid-2013 at the Latest,” FEI Financial Reporting Blog (April 2012).

The Expectations Gap

![]() International Perspective

International Perspective

Foreign accounting firms that provide an audit report for a U.S.-listed company are subject to the authority of the accounting oversight board (mandated by the Sarbanes-Oxley Act).

The Sarbanes-Oxley Act was passed in response to a string of accounting scandals at companies like Enron, Cendant, Sunbeam, Rite-Aid, Xerox, and WorldCom. This law increased the resources for the SEC to combat fraud and curb poor reporting practices.10 And the SEC has increased its policing efforts, approving new auditor independence rules and materiality guidelines for financial reporting. In addition, the Sarbanes-Oxley Act introduces sweeping changes to the institutional structure of the accounting profession. The following are some of the key provisions of the legislation.

- Establishes an oversight board, the Public Company Accounting Oversight Board (PCAOB), for accounting practices. The PCAOB has oversight and enforcement authority and establishes auditing, quality control, and independence standards and rules.

- Implements stronger independence rules for auditors. Audit partners, for example, are required to rotate every five years, and auditors are prohibited from offering certain types of consulting services to corporate clients.

- Requires CEOs and CFOs to personally certify that financial statements and disclosures are accurate and complete, and requires CEOs and CFOs to forfeit bonuses and profits when there is an accounting restatement.

- Requires audit committees to be comprised of independent members and members with financial expertise.

- Requires codes of ethics for senior financial officers.

In addition, Section 404 of the Sarbanes-Oxley Act requires public companies to attest to the effectiveness of their internal controls over financial reporting. Internal controls are a system of checks and balances designed to prevent and detect fraud and errors. Most companies have these systems in place, but many have never completely documented them. Companies are finding that it is a costly process but perhaps badly needed.

While there continues to be debate about the benefits and costs of Sarbanes-Oxley (especially for smaller companies), studies at the time of the act's implementation provide compelling evidence that there was much room for improvement. For example, one study documented 424 companies with deficiencies in internal control.11 Many problems involved closing the books, revenue recognition deficiencies, reconciling accounts, or dealing with inventory. SunTrust Bank, for example, fired three officers after discovering errors in how the company calculates its allowance for bad debts. And Visteon, a car parts supplier, said it found problems recording and managing receivables from its largest customer, Ford Motor.

Will these changes be enough? The expectations gap—what the public thinks accountants should do and what accountants think they can do—is difficult to close. Due to the number of fraudulent reporting cases, some question whether the profession is doing enough. Although the profession can argue rightfully that accounting cannot be responsible for every financial catastrophe, it must continue to strive to meet the needs of society. However, efforts to meet these needs will become more costly to society. The development of a highly transparent, clear, and reliable system will require considerable resources.

Financial Reporting Challenges

LEARNING OBJECTIVE ![]()

Describe some of the challenges facing financial reporting.

While our reporting model has worked well in capturing and organizing financial information in a useful and reliable fashion, much still needs to be done. For example, if we move to the year 2025 and look back at financial reporting today, we might read the following.

- Nonfinancial measurements. Financial reports failed to provide some key performance measures widely used by management, such as customer satisfaction indexes, backlog information, reject rates on goods purchased, as well as the results of companies' sustainability efforts.

- Forward-looking information. Financial reports failed to provide forward-looking information needed by present and potential investors and creditors. One individual noted that financial statements in 2014 should have started with the phrase, “Once upon a time,” to signify their use of historical cost and accumulation of past events.

- Soft assets. Financial reports focused on hard assets (inventory, plant assets) but failed to provide much information about a company's soft assets (intangibles). The best assets are often intangible. Consider Microsoft's know-how and market dominance, Wal-Mart's expertise in supply chain management, and Procter & Gamble's brand image.

- Timeliness. Companies only prepared financial statements quarterly and provided audited financials annually. Little to no real-time financial statement information was available.

- Understandability. Investors and market regulators were raising concerns about the complexity and lack of understandability of financial reports.

We believe each of these challenges must be met for the accounting profession to provide the type of information needed for an efficient capital allocation process. We are confident that changes will occur, based on these positive signs:

- Already, some companies voluntarily disclose information deemed relevant to investors. Often such information is nonfinancial. For example, banking companies now disclose data on loan growth, credit quality, fee income, operating efficiency, capital management, and management strategy. Increasingly, companies are preparing reports on their sustainability efforts by reporting such information as water use and conservation, carbon impacts, and labor practices. In some cases, “integrated reports” are provided, which incorporate sustainability reports into the traditional annual report, leading some to call for standards for sustainability reporting.

- Initially, companies used the Internet to provide limited financial data. Now, most companies publish their annual reports in several formats on the Web. The most innovative companies offer sections of their annual reports in a format that the user can readily manipulate, such as in an electronic spreadsheet format. Companies also format their financial reports using eXtensible Business Reporting Language (XBRL), which permits quicker and lower-cost access to companies' financial information.

- More accounting standards now require the recording or disclosing of fair value information. For example, companies either record investments in stocks and bonds, debt obligations, and derivatives at fair value, or companies show information related to fair values in the notes to the financial statements. The FASB and the IASB have a converged standard on fair value measures, which should enhance the usefulness of fair value measures in financial statements.

- The FASB is now working on projects that address disclosure effectiveness and a reporting framework for non-public companies. The projects could go a long way toward addressing complexity and understandability of the information in financial statements, allowing for more-effective, less-complex, and flexible reporting to meet the needs of investors.

Changes in these directions will enhance the relevance of financial reporting and provide useful information to financial statement readers.

International Accounting Standards

Former Secretary of the Treasury, Lawrence Summers, has indicated that the single most important innovation shaping the capital markets was the idea of generally accepted accounting principles. He went on to say that we need something similar internationally.

We believe that the Secretary is right. Relevant and reliable financial information is a necessity for viable capital markets. Unfortunately, companies outside the United States often prepare financial statements using standards different from U.S. GAAP (or simply GAAP). As a result, international companies such as Coca-Cola, Microsoft, and IBM have to develop financial information in different ways. Beyond the additional costs these companies incur, users of the financial statements often must understand at least two sets of accounting standards. (Understanding one set is hard enough!) It is not surprising, therefore, that there is a growing demand for one set of high-quality international standards.

![]() International Perspective

International Perspective

IFRS includes the standards, referred to as International Financial Reporting Standards (IFRS), developed by the IASB. The predecessor to the IASB issued International Accounting Standards (IAS).

Presently, there are two sets of rules accepted for international use—GAAP and International Financial Reporting Standards (IFRS), issued by the London-based International Accounting Standards Board (IASB). U.S. companies that list overseas are still permitted to use GAAP, and foreign companies listed on U.S. exchanges are permitted to use IFRS. As you will learn, there are many similarities between GAAP and IFRS.

Already over 115 countries use IFRS, and the European Union now requires all listed companies in Europe (over 7,000 companies) to use it. The SEC laid out a roadmap by which all U.S. companies might be required to use IFRS by 2015. Most parties recognize that global markets will best be served if only one set of accounting standards is used. For example, the FASB and the IASB formalized their commitment to the convergence of GAAP and IFRS by issuing a memorandum of understanding (often referred to as the Norwalk agreement). The two Boards agreed to use their best efforts to:

- Make their existing financial reporting standards fully compatible as soon as practicable, and

- Coordinate their future work programs to ensure that once achieved, compatibility is maintained.

![]() International Perspective

International Perspective

The adoption of IFRS by U.S. companies would make it easier to compare U.S. and foreign companies, as well as for U.S. companies to raise capital in foreign markets.

As a result of this agreement, the two Boards identified a number of short-term and long-term projects that would lead to convergence. For example, one short-term project was for the FASB to issue a rule that permits a fair value option for financial instruments. This rule was issued in 2007, and now the FASB and the IASB follow the same accounting in this area. Conversely, the IASB completed a project related to borrowing costs, which makes IFRS consistent with GAAP. Long-term convergence projects relate to such issues as revenue recognition, the conceptual framework, and leases.

Because convergence is such an important issue, we provide a discussion of international accounting standards at the end of each chapter called IFRS Insights. This feature will help you understand the changes that are taking place in the financial reporting area as we move to one set of international standards. In addition, throughout the textbook, we provide International Perspectives in the margins to help you understand the international reporting environment.

What do the numbers mean? CAN YOU DO THAT?

One of the more difficult issues related to convergence and international accounting standards is that countries have different cultures and customs. For example, the former chair of the IASB explained it this way regarding Europe:

“In the U.K. everything is permitted unless it is prohibited. In Germany, it is the other way around; everything is prohibited unless it is permitted. In the Netherlands, everything is prohibited even if it is permitted. And in France, everything is permitted even if it is prohibited. Add in countries like Japan, the United States and China, it becomes very difficult to meet the needs of each of these countries.”

With this diversity of thinking around the world, it understandable why accounting convergence has been so elusive.

Source: Sir D. Tweedie, “Remarks at the Robert P. Maxon Lectureship,” George Washington University (April 7, 2010).

Ethics in the Environment of Financial Accounting

LEARNING OBJECTIVE ![]()

Understand issues related to ethics and financial accounting.

Robert Sack, a noted commentator on the subject of accounting ethics, observed, “Based on my experience, new graduates tend to be idealistic … thank goodness for that! Still it is very dangerous to think that your armor is all in place and say to yourself, ‘I would have never given in to that.’ The pressures don't explode on us; they build, and we often don't recognize them until they have us.”

These observations are particularly appropriate for anyone entering the business world. In accounting, as in other areas of business, we frequently encounter ethical dilemmas. Some of these dilemmas are simple and easy to resolve. However, many are not, requiring difficult choices among allowable alternatives.

Companies that concentrate on “maximizing the bottom line,” “facing the challenges of competition,” and “stressing short-term results” place accountants in an environment of conflict and pressure. Basic questions such as, “Is this way of communicating financial information good or bad?” “Is it right or wrong?” and “What should I do in the circumstance?” cannot always be answered by simply adhering to GAAP or following the rules of the profession. Technical competence is not enough when encountering ethical decisions.

Doing the right thing is not always easy or obvious. The pressures “to bend the rules,” “to play the game,” or “to just ignore it” can be considerable. For example, “Will my decision affect my job performance negatively?” “Will my superiors be upset?” and “Will my colleagues be unhappy with me?” are often questions business people face in making a tough ethical decision. The decision is more difficult because there is no comprehensive ethical system to provide guidelines.

Time, job, client, personal, and peer pressures can complicate the process of ethical sensitivity and selection among alternatives. Throughout this textbook, we present ethical considerations to help sensitize you to the type of situations you may encounter in the performance of your professional responsibility.

Conclusion

Bob Herz, former FASB chairman, believes that there are three fundamental considerations the FASB must keep in mind in its rule-making activities: (1) improvement in financial reporting, (2) simplification of the accounting literature and the rule-making process, and (3) international convergence. These are notable objectives, and the Board is making good progress on all three dimensions. Issues such as off-balance-sheet financing, measurement of fair values, enhanced criteria for revenue recognition, and stock option accounting are examples of where the Board has exerted leadership. Improvements in financial reporting should follow.

![]() You will want to read the IFRS INSIGHTS on pages 31–39 for discussion of IFRS and the international reporting environment.

You will want to read the IFRS INSIGHTS on pages 31–39 for discussion of IFRS and the international reporting environment.

Also, the Board is making it easier to understand what GAAP is. GAAP has been contained in a number of different documents. The lack of a single source makes it difficult to access and understand generally accepted principles. As discussed earlier, the Codification now organizes existing GAAP by accounting topic regardless of its source (FASB Statements, APB Opinions, and so on). The codified standards are then considered to be GAAP and to be authoritative. All other literature will be considered nonauthoritative.

Finally, international convergence is underway. Some projects already are completed and differences eliminated. Many more are on the drawing board. It appears to be only a matter of time until we will have one set of global accounting standards that will be established by the IASB. The profession has many challenges, but it has responded in a timely, comprehensive, and effective manner.

KEY TERMS

Accounting Principles Board (APB), 9

Accounting Research Bulletins, 9

Accounting Standards Updates, 12

accrual-basis accounting, 6

American Institute of Certified Public Accountants (AICPA), 9

APB Opinions, 9

Auditing Standards Board, 10

Committee on Accounting Procedure (CAP), 9

decision-usefulness, 6

Emerging Issues Task Force (EITF), 12

entity perspective, 6

expectations gap, 18

FASB Staff Positions, 13

financial accounting, 4

Financial Accounting Standards Board (FASB), 10

Financial Accounting Standards Board Accounting Standards Codification (Codification), 14

Financial Accounting Standards Board Codification Research System (CRS), 14

financial reporting, 4

financial statements, 4

generally accepted accounting principles (GAAP), 7

general-purpose financial statements, 5

International Accounting Standards Board (IASB), 20

International Financial Reporting Standards (IFRS), 20

interpretations, 13

objective of financial reporting, 5

Public Company Accounting Oversight Board (PCAOB), 18

Sarbanes-Oxley Act, 17

Securities and Exchange Commission (SEC), 8

Statements of Financial Accounting Concepts, 13

Wheat Committee, 9

SUMMARY OF LEARNING OBJECTIVES

![]() Identify the major financial statements and other means of financial reporting. Companies most frequently provide (1) the balance sheet, (2) the income statement, (3) the statement of cash flows, and (4) the statement of owners' or stockholders' equity. Financial reporting other than financial statements may take various forms. Examples include the president's letter and supplementary schedules in the corporate annual report, prospectuses, reports filed with government agencies, news releases, management's forecasts, and descriptions of a company's social or environmental impact.

Identify the major financial statements and other means of financial reporting. Companies most frequently provide (1) the balance sheet, (2) the income statement, (3) the statement of cash flows, and (4) the statement of owners' or stockholders' equity. Financial reporting other than financial statements may take various forms. Examples include the president's letter and supplementary schedules in the corporate annual report, prospectuses, reports filed with government agencies, news releases, management's forecasts, and descriptions of a company's social or environmental impact.

![]() Explain how accounting assists in the efficient use of scarce resources. Accounting provides reliable, relevant, and timely information to managers, investors, and creditors to allow resource allocation to the most efficient enterprises. Accounting also provides measurements of efficiency (profitability) and financial soundness.

Explain how accounting assists in the efficient use of scarce resources. Accounting provides reliable, relevant, and timely information to managers, investors, and creditors to allow resource allocation to the most efficient enterprises. Accounting also provides measurements of efficiency (profitability) and financial soundness.

![]() Identify the objective of financial reporting. The objective of general-purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in decisions about providing resources to the entity through equity investments and loans or other forms of credit. Information that is decision-useful to investors may also be helpful to other users of financial reporting who are not investors.

Identify the objective of financial reporting. The objective of general-purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in decisions about providing resources to the entity through equity investments and loans or other forms of credit. Information that is decision-useful to investors may also be helpful to other users of financial reporting who are not investors.

![]() Explain the need for accounting standards. The accounting profession has attempted to develop a set of standards that is generally accepted and universally practiced. Without this set of standards, each company would have to develop its own standards. Readers of financial statements would have to familiarize themselves with every company's peculiar accounting and reporting practices. As a result, it would be almost impossible to prepare statements that could be compared.

Explain the need for accounting standards. The accounting profession has attempted to develop a set of standards that is generally accepted and universally practiced. Without this set of standards, each company would have to develop its own standards. Readers of financial statements would have to familiarize themselves with every company's peculiar accounting and reporting practices. As a result, it would be almost impossible to prepare statements that could be compared.

![]() Identify the major policy-setting bodies and their role in the standard-setting process. The Securities and Exchange Commission (SEC) is a federal agency that has the broad powers to prescribe, in whatever detail it desires, the accounting standards to be employed by companies that fall within its jurisdiction. The American Institute of Certified Public Accountants (AICPA) issued standards through its Committee on Accounting Procedure and Accounting Principles Board. The Financial Accounting Standards Board (FASB) establishes and improves standards of financial accounting and reporting for the guidance and education of the public.

Identify the major policy-setting bodies and their role in the standard-setting process. The Securities and Exchange Commission (SEC) is a federal agency that has the broad powers to prescribe, in whatever detail it desires, the accounting standards to be employed by companies that fall within its jurisdiction. The American Institute of Certified Public Accountants (AICPA) issued standards through its Committee on Accounting Procedure and Accounting Principles Board. The Financial Accounting Standards Board (FASB) establishes and improves standards of financial accounting and reporting for the guidance and education of the public.

![]() Explain the meaning of generally accepted accounting principles (GAAP) and the role of the Codification for GAAP. Generally accepted accounting principles (GAAP) are those principles that have substantial authoritative support, such as FASB standards, interpretations, and Staff Positions, APB Opinions and interpretations, AICPA Accounting Research Bulletins, and other authoritative pronouncements. All these documents and others are now classified in one document referred to as the Codification. The purpose of the Codification is to simplify user access to all authoritative U.S. GAAP. The Codification changes the way GAAP is documented, presented, and updated.

Explain the meaning of generally accepted accounting principles (GAAP) and the role of the Codification for GAAP. Generally accepted accounting principles (GAAP) are those principles that have substantial authoritative support, such as FASB standards, interpretations, and Staff Positions, APB Opinions and interpretations, AICPA Accounting Research Bulletins, and other authoritative pronouncements. All these documents and others are now classified in one document referred to as the Codification. The purpose of the Codification is to simplify user access to all authoritative U.S. GAAP. The Codification changes the way GAAP is documented, presented, and updated.

![]() Describe the impact of user groups on the rule-making process. User groups may want particular economic events accounted for or reported in a particular way, and they fight hard to get what they want. They especially target the FASB to influence changes in existing GAAP and in the development of new rules. Because of the accelerated rate of change and the increased complexity of our economy, these pressures have been multiplying. GAAP is as much a product of political action as it is of careful logic or empirical findings. The IASB is working with the FASB toward international convergence of GAAP.

Describe the impact of user groups on the rule-making process. User groups may want particular economic events accounted for or reported in a particular way, and they fight hard to get what they want. They especially target the FASB to influence changes in existing GAAP and in the development of new rules. Because of the accelerated rate of change and the increased complexity of our economy, these pressures have been multiplying. GAAP is as much a product of political action as it is of careful logic or empirical findings. The IASB is working with the FASB toward international convergence of GAAP.

![]() Describe some of the challenges facing financial reporting. Financial reports fail to provide (1) some key performance measures widely used by management, (2) forward-looking information needed by investors and creditors, (3) sufficient information on a company's soft assets (intangibles), (4) real-time financial information, and (5) easy-to-comprehend information.

Describe some of the challenges facing financial reporting. Financial reports fail to provide (1) some key performance measures widely used by management, (2) forward-looking information needed by investors and creditors, (3) sufficient information on a company's soft assets (intangibles), (4) real-time financial information, and (5) easy-to-comprehend information.

![]() Understand issues related to ethics and financial accounting. Financial accountants are called on for moral discernment and ethical decision-making. Decisions sometimes are difficult because a public consensus has not emerged to formulate a comprehensive ethical system that provides guidelines in making ethical judgments.

Understand issues related to ethics and financial accounting. Financial accountants are called on for moral discernment and ethical decision-making. Decisions sometimes are difficult because a public consensus has not emerged to formulate a comprehensive ethical system that provides guidelines in making ethical judgments.

FASB CODIFICATION

FASB CODIFICATION

Exercises

Academic access to the FASB Codification is available through university subscriptions, obtained from the American Accounting Association (at http://aaahq.org/FASB/Access.cfm), for an annual fee of $150. This subscription covers an unlimited number of students within a single institution. Once this access has been obtained by your school, you should log in (at http://aaahq.org/ascLogin.cfm) to prepare responses to the following exercises.

| CE1-1 | Describe the main elements of the link labeled “Help, FAQ, Learning Guide, and About the Codification.” |

| CE1-2 | Describe the procedures for providing feedback. |

| CE1-3 | Briefly describe the purpose and content of the “What's New” link. |

An additional accounting research case can be found in the Using Your Judgment section, on page 30.

Be sure to check the book's companion website for a Review and Analysis Exercise, with solution.

![]() Brief Exercises, Exercises, Problems, and many more learning and assessment tools and resources are available for practice in WileyPLUS.

Brief Exercises, Exercises, Problems, and many more learning and assessment tools and resources are available for practice in WileyPLUS.

QUESTIONS

- Differentiate broadly between financial accounting and managerial accounting.

- Differentiate between “financial statements” and “financial reporting.”

- How does accounting help the capital allocation process?

- What is the objective of financial reporting?

- Briefly explain the meaning of decision-usefulness in the context of financial reporting.

- Of what value is a common set of standards in financial accounting and reporting?

- What is the likely limitation of “general-purpose financial statements”?

- In what way is the Securities and Exchange Commission concerned about and supportive of accounting principles and standards?

- What was the Committee on Accounting Procedure, and what were its accomplishments and failings?

- For what purposes did the AICPA in 1959 create the Accounting Principles Board?

- Distinguish among Accounting Research Bulletins, Opinions of the Accounting Principles Board, and Statements of the Financial Accounting Standards Board.

- If you had to explain or define “generally accepted accounting principles or standards,” what essential characteristics would you include in your explanation?

- In what ways was it felt that the pronouncements issued by the Financial Accounting Standards Board would carry greater weight than the opinions issued by the Accounting Principles Board?

- How are FASB preliminary views and FASB exposure drafts related to FASB “statements”?

- Distinguish between FASB Accounting Standards Updates and FASB Statements of Financial Accounting Concepts.

- What is Rule 203 of the Code of Professional Conduct?

- The chairman of the FASB at one time noted that “the flow of standards can only be slowed if (1) producers focus less on quarterly earnings per share and tax benefits and more on quality products, and (2) accountants and lawyers rely less on rules and law and more on professional judgment and conduct.” Explain his comment.

- What is the purpose of FASB Staff Positions?

- Explain the role of the Emerging Issues Task Force in establishing generally accepted accounting principles.

- What is the difference between the Codification and the Codification Research System?

- What are the primary advantages of having a Codification of generally accepted accounting principles?

- What are the sources of pressure that change and influence the development of GAAP?

- Some individuals have indicated that the FASB must be cognizant of the economic consequences of its pronouncements. What is meant by “economic consequences”? What dangers exist if politics play too much of a role in the development of GAAP?

- If you were given complete authority in the matter, how would you propose that GAAP should be developed and enforced?

- One writer recently noted that 99.4 percent of all companies prepare statements that are in accordance with GAAP. Why then is there such concern about fraudulent financial reporting?

- What is the “expectations gap”? What is the profession doing to try to close this gap?