Introduction to Professional Research

LEARNING OBJECTIVES

After completing this chapter, you should understand:

- The importance of research in the daily activities of the professional accountant.

- The definition and nature of professional accounting research.

- The navigation steps to narrow one's research.

- The U.S. Securities and Exchange Commission's view on the importance of research.

- The role of research within a public accounting firm or within an accounting department of a business or governmental entity.

- The basic steps of the research process.

- The importance of critical thinking and effective communication skills.

- The importance of research on the U.S. CPA exam.

The accounting profession, like other professions, is witnessing major changes due to changes in the law, new services, technologies, and an ever-increasing number of professional standards. In addition to accounting, auditing, and tax compliance services, accountants are involved in such services as attestation reviews, forensic accounting, fraud examinations, and tax planning. Today's professional accountant must possess the knowledge to remain current and the skills to critically analyze various problems. Listening effectively and understanding opposing points of view are also critical skills for accountants. Often, one must present and defend his or her own views through formal and informal communications. Professional research and communication skills are essential in this environment.

QUICK FACTS

Accounting research is a combination of using accounting theory and existing authoritative accounting literature.

Varying views and interpretations exist as to the meaning of the term research. In the accounting profession, research points to what the accounting practitioner does as a normal, everyday part of his or her job. In today's environment, to become proficient in accounting, auditing, and tax research, one must also possess the skills to use various professional databases, which are increasingly available on the Web. Using professional databases for research is even required on the computerized CPA exam.

The professional accountant, whether in public accounting, industry, or government, frequently becomes involved with the investigation and analysis of an accounting, auditing, or tax issue. Resolving these issues requires formulating a clear definition of the problem, using professional databases to search for the relevant authorities, reviewing the authoritative literature, evaluating alternatives, drawing conclusions, and communicating the results. This research process often requires an analysis of very complex and detailed issues. Therefore, researching such issues will challenge the critical thinking abilities of the professional. That is, the professional must possess the expertise to understand the relevant facts and render a professional judgment, even in some situations where no single definitive answer or solution exists. In such cases, the researcher would apply professional judgment in the development of an answer to the issue or problem at hand.

WHAT IS RESEARCH?

The objective of conducting any type of research, including professional accounting, auditing, and tax research, is a systematic investigation of an issue or problem utilizing the researcher's professional judgment.

Below are two examples of generalized research problems that can provide insight as to the types of research questions confronting the accounting practitioner:

- A client is engaged in land sales, primarily commercial and agricultural. The company recently acquired a retail land sales project under an agreement stating that, if the company did not desire to pursue the project further, the property could be returned with no liability to the company.

After the company invests a considerable amount of money into the project, the state of the economy concerning retail land sales declines, and the company decides to return the land. As a result, the client turns to you, the CPA, and requests the proper accounting treatment of the returned project. At issue is whether the abandonment represents a disposal of a segment of the business, an unusual and nonrecurring extraordinary loss, or an ordinary loss. The client may also want to understand the tax consequences.

- A controller for a construction contracting company faces the following problem. The company pays for rights allowing it to extract a specified volume of landfill from a project for a specified period of time. How should the company classify the payments for such landfill rights in its financial statements?1

Research is often classified as either theoretical research or applied research. Theoretical research investigates questions that appear interesting to the researcher, generally an academician, but may have little or no practical application at the present time. In conducting theoretical research, one attempts to create new knowledge in a particular subject. Theoretical research sometimes uses empirical data based upon experimentation or observation. For example, a theoretical researcher may conduct a controlled experiment to determine the effects of informational complexity on analysts' forecasts.2 Thus, theoretical research adds to the body of knowledge in a particular field and may ultimately contribute directly or indirectly to practical problem solutions. Theoretical research using empirical research studies based on experimentation or observation are frequently reviewed and evaluated by standard-setting bodies in drafting authoritative accounting and auditing pronouncements.

QUICK FACTS

Professional accountants primarily conduct applied research to practice issues.

Applied research, the focus of this text, investigates an issue of immediate practical importance. One type of applied research is known as a priori (before the fact) research. This research is conducted before the client actually enters into the transaction. For example, assume that a public accounting firm needs to evaluate a client's proposed new accounting treatment for environmental costs. The client expects an answer within two days as to the acceptability of the new method and its impact on the financial statements. In such a case, a member of the accounting firm's professional staff would investigate to determine if the authoritative literature addresses the issue. If no authoritative pronouncement exists, the accountant would develop a theoretical justification for or against the new method.

Applied research relating to a completed event is known as a posteriori (after the fact) research. For example, a client may request assistance preparing his or her tax return for a transaction that was previously executed. Frequently, many advantages accrue to conducting a priori rather than a posteriori research. For example, if research reveals that a proposed transaction will have an unfavorable impact on financial statements, the client can abandon the transaction or possibly restructure it to avoid undesirable consequences. These options are not available, however, after a transaction is completed.

Society needs both theoretical and applied research. Both types of research require sound research design to effectively and efficiently resolve the issue under investigation. No matter how knowledgeable a professional becomes in any aspect of accounting, auditing, or tax, he or she will always have research challenges. However, using a systematic research approach will greatly help in resolving the problem.

RESEARCH QUESTIONS

Individual companies and CPA firms conduct research to resolve specific accounting, auditing, and tax issues relating to a company or client. The results of this research may lead to new firm policies or procedures in the application of existing authorities. In this research process, the practitioner (researcher) must answer the following basic questions:

- Do I have complete knowledge to answer the question, or must I conduct research to consult authoritative references?

- What is the law (tax law) or authoritative literature?

- Does the law or authoritative literature address the issue under review?

- Where can I find the law or authoritative literature and effectively and efficiently research tips develop a conclusion

- Where can I find international accounting and auditing standards?

- If there is no law or authoritative literature directly addressing the topic at issue, what approach do I follow in reaching a conclusion?

- What professional databases or other sources on the Internet should I access for the research process?

- If more than one alternative solution exists, what alternative do I select?

- How do I document my findings or conclusions?

RESEARCH TIPS

Successful research requires answering various questions to find and apply relevant authorities.

The purpose of this text is to provide an understanding of the research process and the research skills needed to answer these questions. The whats, whys, and hows of practical professional accounting, auditing, and tax research are discussed with emphasis on the following topics:

- How do I research effectively?

- How do I apply a practical research methodology in a timely manner?

- What are the generally accepted accounting principles, auditing standards, and tax authorities?

- What constitutes substantial authoritative support?

- What are the available sources of authority for accounting, auditing, and tax?

- What databases are available forfinding relevant authorities or assisting in researching a particular problem?

- What role does the Internet (the information superhighway) have in the modern research process?

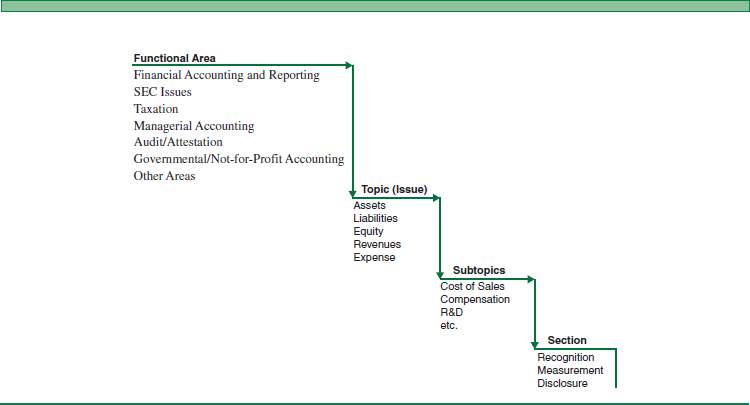

In conducting research for an issue or question at hand, one of the primary tools utilized in financial accounting research is the Financial Accounting Standards Board (FASB) Codification System™, which is discussed in detail in Chapter 4. Similar to understanding the Codification's structure, navigating through the authoritative literature is necessary to analyze a variety of questions or issues. A useful instrument to help focus or narrow your research would be a navigation guide, such as the one depicted in Figure 1-1.

In navigating through the literature or Codification, the researcher should first focus on the functional area(s) that will help guide one to the appropriate professional literature and/or database as well as the authoritative body that issued the related literature. For instance, is the problem or issue under review a financial accounting question, managerial accounting issue, or technical SEC problem? Once the functional area is determined, the next step in the navigation is to determine the broad categorization of the topic, such as an asset, revenue, or expense issue. Then focus on the subtopic that allows for further segregation and navigation of the issue. For example, if the topical area is an expense issue, the subtopic might relate to cost of sales, compensation, or research and development.

The final phase in the navigation process is to focus on the section or nature of the content, which is often a recognition, measurement, or disclosure issue. For instance, if the functional area is financial accounting, the topic is assets, and the subtopic is financial instruments, the section or nature might address the proper measurement of the financial instrument either at cost or fair value. This navigation guide is explained in detail later in the text.

FIGURE 1-1 RESEARCH NAVIGATION GUIDE

A practical research approach, along with discussions of various research tools, is also presented in the text, as are demonstrations of this research approach using a number of end-of-chapter questions and exercises. The text also addresses the importance of critical thinking and effective writing skills that the researcher should possess and utilize in executing the research process. Specific tips on developing these skills are presented in subsequent chapters.

NATURE OF PROFESSIONAL RESEARCH

This text focuses on applied research, known as professional accounting research. Today's practitioner must conduct research effectively and efficiently to arrive at appropriate and timely conclusions regarding the issues at hand. Effectiveness is critical in order to confirm:

- The proper recording, classification, and disclosure of economic events.

- Compliance with authoritative pronouncements.

- The absence of preferable alternative procedures.

Efficiency is needed to meet deadlines and manage research costs.

Additional examples of issues frequently encountered by the practitioner include such questions as:

- What are the accounting, auditing, or tax implications of a new transaction?

- Does the accounting treatment of the transaction conform with generally accepted accounting principles (GAAP)? Does the tax treatment conform with the law?

- What are the disclosure requirements for the financial statements or tax returns?

- What is the auditor's responsibility when confronted with supplemental information presented in annual reports but not as part of the basic financial statements?

- What responsibilities and potential penalties exist for tax accountants?

- How does an accountant proceed in a fraud investigation?

QUICK FACTS

The accounting researcher is an investigator with strong analytical and communication skills.

Responding to these often-complex questions has generally become more difficult and time-consuming as the financial accounting and reporting requirements, auditing standards, and tax authorities increase in number and complexity. The research process is often complicated further when the accountant or auditor researches a practical issue or question for which no applicable authoritative literature exists.

RESEARCH TIPS

Conducting research requires the use of various electronic databases often available on the Web.

As a researcher, the accountant should possess certain desired characteristics that aid in the research process. These characteristics include inquisitiveness, open-mindedness, thoroughness, patience, and perseverance.3 Inquisitiveness is needed while gathering the relevant facts to obtain a clear picture of the research problem. Proper problem definition or issue identification is the most critical component in research. An improperly stated issue usually leads to the wrong conclusion, no matter how carefully the research process is executed. Likewise, the researcher should avoid drawing conclusions before the research process is completed. A preconceived solution can result in biased research in which the researcher merely seeks evidence to support that position rather than search for the most appropriate solution. The researcher must carefully examine the facts, obtain and review authoritative literature, evaluate alternatives, and then draw conclusions based upon research evidence. The execution of an efficient research project requires thoroughness and patience. This is emphasized in both the planning stage, where all relevant facts are identified, and the research stage, where all extraneous information is controlled. Finally, the researcher must work persistently in order to finish the research on a timely basis.

Perhaps the most important characteristic of the research process is its ability to add value to the services provided. A professional auditor not only renders an opinion on a client's financial statements, but also identifies available reporting alternatives that may benefit the client. A professional tax accountant not only prepares the returns, but suggests tax planning for future transactions. The ability of a researcher to provide relevant information becomes more important as the competition among accounting firms for clients becomes more intense and the potential significance and enforcement of penalties become more common. Researchers who identify reporting alternatives that provide benefits or avoid pitfalls will provide a strong competitive edge for their employers. Providing these tangible benefits to clients through careful and thorough research is essential in today's accounting environment.

CRITICAL THINKING AND EFFECTIVE COMMUNICATION

The researcher needs to know how to think. That is, he or she must identify the problem or issue, gather the relevant facts, analyze the issue(s), synthesize and evaluate alternatives, develop an appropriate solution, and effectively communicate the desired information. Such skills are essential for the professional accountant in providing services in today's complex, dynamic, and changing profession. In this environment, the professional accountant must possess not only the ability to think critically, which includes the ability to understand a variety of contexts and circumstances, but also apply and adapt various accounting, auditing, tax, and business concepts and principles to these circumstances to develop the best solutions. The development and nurturing of critical thinking skills will also contribute to the process of life-long learning that is needed for today's professional.

RESEARCH TIPS

Successful research requires critical thinking and effective communication.

Certain research efforts may culminate in memos or work papers, letters to clients, journal articles, or firm reports. The dissemination of your research, in whatever form, will require effective communication skills for both oral presentations and written documents. One's research output must demonstrate coherence, conciseness, appropriate use of Standard English, and achievement of the purpose for the intended reader. Critical thinking and effective writing skills are the focus of Chapter 2.

ECONOMIC CONSEQUENCES OF STANDARDS SETTING

Various accounting standards have far-reaching economic consequences. This was demonstrated by the Financial Accounting Standards Board (FASB) in addressing such issues as restructuring costs, financial instruments and fair value accounting, stock options, and post-employment benefits. Various difficulties sometimes arise in the proper accounting for the economic substance of a transaction within the current accounting framework.

Because financial statements must conform to GAAP, the standard-setting bodies, such as the FASB or Governmental Accounting Standards Board (GASB), will conduct research on the economic impact of a proposed standard. For example, the handling of off–balance sheet transactions has sometimes encouraged the selection of one business decision over another, producing results that may be less oriented to the users of financial statements.

In today's complex business and legal environment, the researcher conducting accounting and auditing research should understand the economic and social impact that various accepted accounting alternatives may have on society in general and individual entities in particular. Such economic and social concerns are becoming a greater factor in the evaluation and issuance of new accounting standards, as discussed more thoroughly in Chapter 4.

ROLE OF RESEARCH IN THE ACCOUNTING FIRM

Although research is often conducted by accountants in education, industry, and government, accounting, auditing, and tax research is particularly important in a public accounting firm. As a reflection of today's society, significant changes have occurred in the accounting environment. The practitioner today requires greater knowledge because of greater complexity in many business transactions, the proliferation of new authoritative pronouncements, and advances in technology. As a result, practitioners should possess the ability to conduct efficient research. An accountant's responsibility to conduct accounting/auditing research is analogous to an attorney's responsibility to conduct legal research. For example,

A lawyer should provide competent representation to a client. Competent representation requires the legal knowledge, skill, thoroughness, and preparation reasonably necessary for the representation.4

A California court interpreted the research requirement to mean that each lawyer must have the ability to research the law completely, know the applicable legal principles, and find “the rules which, although not commonly known” are discovered through standard research techniques.5 Thus, in the California case, the plaintiff recovered a judgment of $100,000 in a malpractice suit that was based upon the malpractice of the defendant in researching the applicable law.

The U.S. Securities and Exchange Commission (SEC) has also stressed the importance of effective accounting research through an enforcement action brought against an accountant. In Accounting and Auditing Enforcement Release No. 420, the SEC instituted a public administrative proceeding against a CPA. The SEC charged that the CPA failed to exercise due care in the conduct of an audit. The enforcement release specifically stated the following:

QUICK FACTS

The accounting practitioner may be held liable for inappropriate or incomplete accounting or tax research.

In determining whether the [company] valued the lease properly, the [CPA] failed to consult pertinent provisions of GAAP or any other accounting authorities. This failure to conduct any research on the appropriate method of valuation constitutes a failure to act with due professional care.

Thus, it is vital that the professional accountant possess the ability to use relevant sources to locate applicable authoritative pronouncements or law and ascertain their current status. Due to the expanding complex environment and proliferation of pronouncements, many accounting firms have created a research specialization within the firm. Common approaches used in practice include the following:

- The staff at the local office conducts day-to-day research with industry-specific questions referred to industry specialists within the firm.

- Selected individuals in the local or regional office are designated as research specialists, and all research questions within the office or region are brought to their attention for research.

- The accounting firm establishes at the executive office of the firm a centralized research function that handles questions for the firm as a whole on technical issues.

- Computerized files of previous research maintained by the firm provide consolidated expertise on how the firm has handled various issues in the past.

The task of accurate and comprehensive research is often complex and challenging. However, one can meet the challenge by becoming familiar with the suggested research process to solve the accounting, auditing, or tax issues.

RESEARCH TIPS

At times, conducting research will require consulting with research specialists.

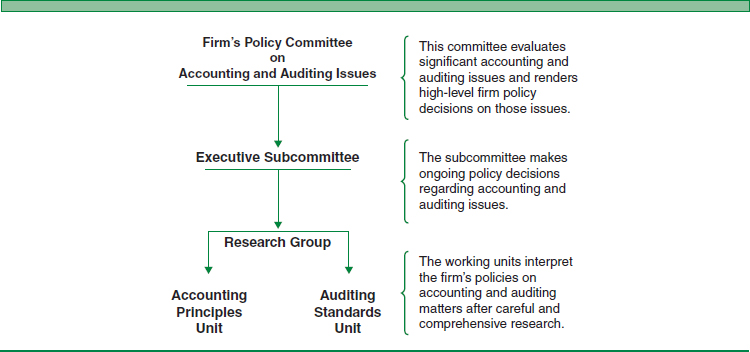

A more in-depth look at a typical organizational structure for policy decision-making and research on accounting and auditing matters within a multi-office firm that maintains a research department is depicted in Figure 1-2. The responsibilities of a firmwide accounting and auditing policy decision function include:

- Maintaining a high level of professional competence in accounting and auditing matters.

- Developing and rendering high-level policies and procedures on accounting and auditing issues for the firm.

- Disseminating the firm's policies and procedures to appropriate personnel within the firm on a timely basis.

- Supervising the quality control of the firm's practice.

Research plays an important role in this decision-making process. A CPA firm's policy committee and executive subcommittee, as shown in Figure 1-2, generally consist of highly competent partners with many years of practical experience. The policy committee's primary function is to evaluate significant accounting and auditing issues and establish firmwide policies on these issues. The executive subcommittee's function is to handle the daily ongoing policy decisions (lower-level decisions) for the firm as a whole. The responsibility of the accounting and auditing research personnel is to interpret firm policies in the context of specific client situations. Frequently, technical accounting and auditing issues that arise during the course of a client engagement are resolved through research conducted by personnel assigned to the engagement. When a local office cannot resolve a research matter satisfactorily, assistance is requested from the firm's specialized research units. These units conduct careful and comprehensive research in arriving at the firm's response to technical inquiries. This response is then disseminated to the various geographic offices of the firm for future reference in handling similar technical issues.

FIGURE 1-2 ORGANIZATIONAL FRAMEWORK FOR POLICY DECISION-MAKING AND RESEARCH WITHIN A TYPICAL MULTIOFFICE ACCOUNTING FIRM

Practical accounting and auditing research is not confined to public accounting firms. All accountants should possess the ability to conduct effective research and develop logical and well-supported conclusions on a timely basis. The basic research process is similar whether the researcher is engaged in public accounting, management accounting, governmental accounting, auditing, or even taxation.

RESEARCH AND THE CPA EXAM

In licensing a new CPA, state laws or regulations typically require a combination of education, examination, and experience. State legislatures, state boards of accountancy, the Public Company Accounting Oversight Board (PCAOB), and the American Institute of Certified Public Accountants (AICPA) have strived to assure the professional competencies of CPAs. The important role that a CPA plays in society is so significant that the AICPA Board of Examiners have identified certain skills that are necessary for the beginning CPA to possess in order to protect the public interest. These skills and their definition are as follows:

- Understanding: The ability to recognize and comprehend the meaning and application of a particular matter.

- Analysis: The ability to organize, process, and interpret data to develop options for making decisions.

- Judgment: The ability to evaluate options for making decisions and provide an appropriate conclusion.

- Communication: The ability to effectively elicit and/or express information through written or oral means.

- Research: The ability to locate and extract relevant information from available resource materials.

- Synthesis (deductive reasoning): The ability to develop a solution based upon the data gathered from the research process (putting the pieces together).

For the CPA exam, not only are CPA candidates required to demonstrate their research ability in simulated problems, but they must also demonstrate understanding, analysis, and judgment through questions that will require the candidate to:

QUICK FACTS

The CPM exam simulations (case studies) require conducting research by using professional literature in computerized databases.

- Interpret and apply the relevant professional literature to specific fact patterns in various cases.

- Identify relevant information and draw appropriate conclusions from searching the professional literature.

- Recognize business-related issues as one evaluates an entity's financial condition.

- Identify, evaluate, analyze, and process an entity's accounting and reporting information.

On the computer-based CPA examination, candidates must demonstrate their research abilities by accessing various professional databases and searching through the legal or professional literature in order to identify the relevant authorities and draw conclusions related to the issues at hand. A candidate's research skills are tested by completing various simulations or case studies as part of the exam. The appendix to this chapter provides an overview of the basic format of the CPA exam's simulations. Examples of simulations are presented throughout subsequent chapters. This text will help you develop the necessary skills to utilize these databases for the computerized CPA exam and help you develop and refine the necessary skill sets and competencies necessary for your professional career. The following chapters will further focus on these skills, with particular emphasis on research skills.

OVERVIEW OF THE RESEARCH PROCESS

The research process in general is often defined as a scientific method of inquiry, a systematic study of a particular field of knowledge in order to discover scientific facts or principles. An operational definition of research encompasses the following process:6

RESEARCH TIPS

Carefully conduct each step in the research process.

- Investigate and analyze a clearly defined issue or problem.

- Use an appropriate scientific approach.

- Gather and document adequate and representative evidence.

- Employ logical reasoning in drawing conclusions.

- Support the validity or reasonableness of the conclusions.

With this general understanding of the research process, practical accounting, auditing, and tax research is defined as follows:

Accounting, auditing, or tax research: A systematic and logical approach employing critical thinking skills to obtain and document evidence (authorities) underlying a conclusion relating to an accounting, auditing, or tax issue or problem.

The basic steps in the research process are illustrated in Figure 1-3, with an overview presented in the following sections. As indicated in the illustration, carefully document each step of the research process. When executing each step, the researcher may also find it necessary to refine the work done in previous steps. The refinement of the research process is discussed more fully in Chapter 9.

Step One: Identify the Relevant Facts and Issues

QUICK FACTS

The research process is appropriate to any type of accounting or tax issue confronted.

The researcher's first task is to gather the facts surrounding the particular problem. However, problem-solving research cannot begin until the researcher clearly and concisely defines the problem. One needs to analyze and understand the “why” and “what” about the issue in order to begin the research process. Unless the researcher knows why the issue was brought to his or her attention, he or she might have difficulty knowing what to research. The novice researcher may find it difficult to distinguish between relevant and irrelevant information. When this happens, it is advisable to err on the side of gathering too many facts rather than too few. As the researcher becomes more knowledgeable, he or she will become more skilled at quickly isolating the relevant facts.

FIGURE 1-3 THE RESEARCH PROCESS

In most cases, the basic issue is identified before the research process begins, for example, when a client requests advice as to the proper handling of a specific transaction. However, further refinement of the exact issue is often required. This process of refining the issue at hand is referred to as problem distillation, where a general issue is restated in sufficiently specific terms. If the statement of the issue is too broad or general, the researcher is apt to waste valuable time consulting sources irrelevant to the specific issue.

Factors to consider in the identification and statement of the issue include the exact source of the issue, justification for the issue, and determination of the scope of the issue. To successfully design and execute an investigation, state the critical issue clearly and precisely. As explained in Chapters 4 and 6, many research tools, especially computerized databases, are indexed by a set of descriptive words. Because keywords aid in reference identification, failure to use the appropriate keywords or understand the facts in sufficient detail can cause a researcher to overlook important authorities. Undoubtedly, writing a clear, concise statement of the problem is the most important task in research. Failure to frame all the facts can, and often will, lead to an erroneous conclusion.

Step Two: Collect the Evidence

As previously stated, problem-solving research cannot begin until the researcher defines the problem. Once the issues are adequately defined, the researcher is ready to proceed with step two of the research process, the collection of evidence. This step usually encompasses a detailed review of relevant authoritative accounting or auditing literature and a survey of present practice. In collecting evidence, the researcher should have familiarity with the various sources available, know which sources to use, and know the order in which to examine the sources and applicable authorities.

RESEARCH TIPS

Use electronic databases and the Internet to help collect the evidence.

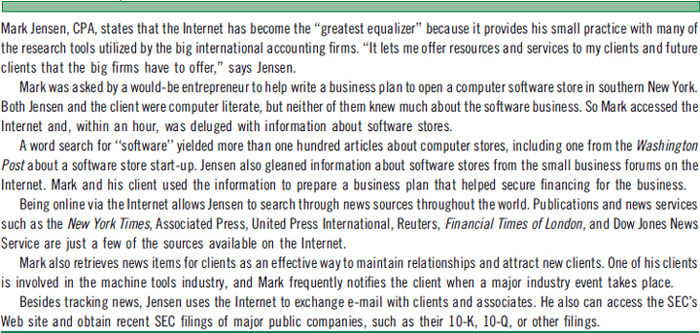

This early identification of the relevant sources will aid in the efficient conduct of the research. A number of research tools, including electronic databases and the Internet, that will aid in the collection of evidence are available and discussed in detail in Chapters 4 through 8. With the Internet growing at an exponential rate as new Web sites are added on a daily basis, this tool provides an increasingly significant impact on the way people, including accountants, auditors, and tax professionals, conduct business. The Internet permits an accounting professional to use various discussion groups or webinars whereby professionals discuss topics on accounting, auditing, or tax issues. Accountants use the Internet to search for federal and state legislation that may have an impact on clients and retrieve financial statements from SEC filings. Figure 1-4 provides an example of how a small CPA firm might utilize the Internet. Many accountants also use the Internet to interact quickly and effectively with the client to assist in collecting the appropriate evidence, such as requesting additional facts that may influence the evidence needed or results from the relevant authorities.

QUICK FACTS

The Internet opens a vast world of information for the professional accountant/researcher.

RESEARCH TIPS

Different search engines on the Internet can give you different hits. Therefore, use more than one search engine when conducting research.

In cases where authoritative literature does not exist on a specific issue, the practitioner should develop a theoretical resolution of the issue based upon a logical analysis of the factors or analogous authorities involved. In addition, the researcher needs to evaluate the economic consequences of the various alternatives in the development of a conclusion. Note that, in practice, a solution is sometimes not readily apparent. Professional judgment and theoretical analysis are key elements in the research process.

FIGURE 1-4 AN EXAMPLE OF A SMALL CPA FIRM UTILIZING THE INTERNET

Step Three: Analyze the Results and Identify the Alternatives

Once a practitioner has completed a thorough investigation of the facts and collection of evidence, the next step is to evaluate the results and identify alternatives for one or more tentative conclusions to the issue. Fully support each alternative by authoritative literature or a theoretical justification with complete and concise documentation. One cannot expect to draw sound conclusions from faulty information. Soundly documented conclusions are possible only when the information has been properly collected, organized, and interpreted.

Further analysis and research are sometimes needed as to the appropriateness of the various alternatives identified. This reevaluation may require further discussions with the client or consultations with colleagues. In discussing an issue with a client, the researcher should use professional skepticism and recognize that management is not always objective in evaluating alternatives. For example, the issue may involve the acceptability of an accounting method that is currently being used by the client. In such cases, the research is directed toward the support or rejection of an alternative already decided on by management. The possibility of bias should cause the researcher to retain a degree of professional skepticism in discussions with the client regarding a conclusion.

Step Four: Develop a Conclusion

After a detailed analysis of the alternatives, including economic consequences, the researcher develops a conclusion and thoroughly documents the final conclusion selected from the alternatives identified. The conclusions should be well supported by the evidence gathered. The conclusion and details of the proposed solution are then presented to the client.

Step Five: Communicate the Results

The most important point in the communication is the conclusion reached. The communication often takes the form of a research memorandum, requiring an objective and unbiased analysis and report. The memorandum should contain a statement of facts, a clear and precise statement of the issue, a brief and straightforward conclusion, and discussion of the authoritative literature and explanation as to how it applies to the set of facts. The written communication should communicate clearly and follow the conventional rules of grammar, spelling, and punctuation. Particularly, because a client often cannot evaluate the quality of research, nothing diminishes a professional's credibility with the client faster than misspellings, incorrect grammar, or misuse of words. Sloppy communications may suggest sloppy research and analysis.

RESEARCH TIPS

After analyzing the results, develop a conclusion and communicate the results.

In drafting the appropriate written communication, avoid making common errors such as:

- Excessive discussion of the issue and facts in a memo, which indicates the memo was not drafted with sufficient precision.

- Excessive citations to authoritative sources (cite only the relevant authorities for the conclusion reached).

- Appearing to avoid a conclusion by pleading the need for additional facts.

Novice researchers too often include irrelevant information. This distracts from the fact that the proposed solution to the problem is appropriate.

A serious weakness in any part of the research and communication process undermines the entire effort. Therefore, address each segment of the process with equal seriousness as to its impact on the entire research project.

SUMMARY

The research work of a practicing professional accountant is very important. Few practitioners ever experience a workweek that does not include the investigation and analysis of an accounting, auditing, or tax issue. Thus, every professional accountant should possess the ability to conduct practical research in a systematic way. The goal of this text is to aid current and future practitioners in developing a basic framework or methodology to assist in the research process.

The emphasis of the following chapters is on practical applied research that deals with solutions to immediate issues rather than theoretical research that has little or no present-day application. Chapter 2 presents an overview of the importance of critical thinking and effective writing skills that every researcher (accountant/auditor/tax professional) must possess to be effective. Chapters 3 and 8 provide an overview of the environment of accounting and auditing/attestation research, with an emphasis on the standard-setting process. The FASB's Codification Research System™ is presented in Chapter 4. The sources of authoritative literature in dealing with international accounting issues is discussed in Chapter 5. Chapter 6 presents other available research tools that may aid in the effective and efficient conduct of practical research, with an emphasis on computerized research via various databases that exist. Chapter 7 provides the basic steps of tax research and valuable databases and Web sites. The chapter highlights the RIA tax database, part of which is also utilized on the CPA exam. Chapter 9 concludes with a refinement of the research process by presenting specific annotated procedures for conducting and documenting the research process via a comprehensive problem.

Chapter 10 provides an overview of fraud and insights into the basic techniques of fraud investigation, an area that is particularly pertinent as more practitioners are entering the specialized field of forensic accounting. The basic steps of a fraud investigation are quite similar to accounting research.

DISCUSSION QUESTIONS

- Define the term research.

- Explain what accounting, auditing, and tax research are.

- Why are accounting, auditing, and tax research necessary?

- What is the objective of accounting, auditing, and tax research?

- What role does professional research play within an accounting firm or department? Who primarily conducts the research?

- What are the functions or responsibilities of the policy committee and executive subcommittee within a multi-office firm?

- Identify and explain some basic questions the researcher must address in performing accounting, auditing, or tax research.

- Differentiate between theoretical and applied research.

- Identify the characteristics that an accounting practitioner should possess.

- Provide an example of utilizing the research navigation guide.

- Distinguish between a priori and a posteriori research. Which research is used more for planning work?

- Explain the analogy of the California court decision dealing with legal research as it relates to the accounting practitioner.

- Explain how the research process adds value to the services offered by an accounting firm.

- What consequences are considered in the standard-setting process?

- Explain the importance of identifying keywords when identifying relevant facts and issues.

- Explain the five basic steps involved in the research process.

- Discuss how research can support or refute a biased alternative.

- Explain what is meant by problem distillation and its importance in the research process.

- What skills are important and tested on the CPA exam?

- Your conclusion to the research is often presented to your boss or client in the form of a research memorandum. Identify the basic points to include in this memo. Also, identify at least two common errors to avoid in the drafting of the memo.

- Explain the necessity of critical thinking in the research process.

- Why did the SEC bring an enforcement action against a CPA concerning research?

- If authoritative literature does not exist, what steps might the researcher take?

APPENDIX

Research Focus on the CPA Exam

Skills in practice identified for the CPA are classified in three categories: knowledge and understanding; application skills, which include research and analysis; and communication skills. Knowledge is acquired through education or experience, and familiarity with information. Understanding is the process of using concepts to address the facts or situation. Knowledge and understanding skills represent almost half of the skills tested on the CPA exam.

Application skills of judgment, research, analysis, and synthesis are required to transform knowledge. Judgment includes devising a plan of action for any problem, identifying potential problems, and applying professional skepticism. Research skills include recognizing keywords, searching through large volumes of electronic data, and organizing data from multiple sources. Analysis includes verifying compliance with standards, noticing trends and variances, and performing appropriate calculations. Synthesis includes solving unstructured problems, examining alternative solutions, developing logical conclusions, and integrating information to make decisions. Application skills require technological competencies in using spreadsheets, databases, and computer software programs. Application skills represent one-third to almost one-half of the skills tested on the CPA exam.

Communication skills include oral, written, graphical, and supervisory skills. Oral skills include attentively listening, presenting information, asking questions, and exchanging technical ideas within the firm. Written skills include organization, clarity, conciseness, proper English, and documentation skills. Graphical skills include organizing and processing symbols, graphs, and pictures. Supervisory skills include providing clear directions, mentoring staff, persuading others, negotiating solutions, and working well with others. Communication skills represent 10 to 20 percent of the skills tested on the CPA exam. Using the five-step research process demonstrated in this chapter substantially helps to develop the necessary skills for the CPA exam. For any research problem, learn the facts, and understand the problem or issues. Acquire knowledge about the client's needs and desires in order to understand the alternative and best solutions to the problem. Knowledge and understanding of accounting should also include the various standard setters and their authoritative sources and the nonauthoritative sources available in various databases, Web sites, hardbound books, newsletters, and other secondary sources.

Use application skills, such as identifying keywords for research. Develop the skills of locating and reviewing the relevant authorities. Analyze how the authorities apply to the particular facts in the research problem. Synthesize information with the help of insightful, nonauthoritative sources. Use professional judgment as you refine the issues with greater specificity and develop well-reasoned conclusions. Develop strong communication skills not only for the CPA exam and research memos, but in handling the day-to-day tasks and interactions that typify the work of accountants and business professionals. Communicate the results of the research, as appropriate.

Many of the previously mentioned skills are tested on the CPA exam in what are called simulations. The AICPA defines a simulation as “an assessment of knowledge and skills in context approximating that found on the job through the use of realistic scenarios and tasks and access to normally available and familiar resources.” In other words, simulations are condensed case studies that utilize real-life, work-related examples. These case studies require the use of tools (computerized databases) and skills that accountants use in the real world. These primary computerized databases are similar in functionality to the AICPA Professional Standards (Auditing and Attestation literature), FASB Codification Research System, and Thomson Reuters/RIA Checkpoint® tax database.

To successfully complete a simulation, the CPA candidate is expected to possess basic computer skills that include the use of spreadsheets and word processing functions. As to the research component of the simulation, the candidate will be required to search various authoritative literature databases in order to answer accounting, auditing, and tax questions to support his or her judgments and prepare formal communications.

Figure A1-1 presents the opening screen shot of the Auditing and Attestation simulation. Notice the Professional Standards entry on the left. This database is explained in Chapter 8, which provides access to the auditing literature to carry out the simulation. Figure A1-2 provides the opening screen shot for the FARS simulation, whereby one accesses the FASB literature to obtain a solution. Finally, Figure A1-3 provides the opening screen shot for Regulations, where the candidate conducts research in the tax code. Notice the Internal Revenue Code selection on the left, which opens up the IRS Code for research. Chapter 7 provides further details of tax research. Each of these databases is explained in detail, with examples, in Chapters 4, 7, and 8. Note on each screen the simulation question being tested under Step One: Research Question.

FIGURE A1-1 OPENING SCREEN SHOT OF THE AUDITING AND ATTESTATION SIMULATION

FIGURE A1-2 OPENING SCREEN SHOT OF FARS SIMULATION

FIGURE A1-3 OPENING SCREEN SHOT OF REGULATIONS SIMULATION

1 AICPA Technical Practice Aids, vol. 1 (Chicago: Commerce Clearing House, Inc.).

2 Leslie Holder et al., “The Effects of Financial Statement and Informational Complexity on Analysts' Cash Flow Forecasts,” The Accounting Review 83, no. 4 (July 2008): 915–956.

3 Wanda Wallace, “A Profile of a Researcher,” Auditor's Report, American Accounting Association (Fall 1984): 1–3.

4 Model Rules of Professional Conduct of the American Bar Association, Rule One.

5 Smith and Lewis, 13 Cal. 3d 349, 530 P.2d 589, 118 Cal Rptr. 621 (1975).

6 David J. Luck, Hugh C. Wales, and Donald A. Taylor, Marketing Research (Englewood Cliffs, N.J.: Prentice Hall, Inc., 1961), 5.