CHAPTER 11

Illiquidity

THE CHALLENGE

One of the most vexing challenges of asset allocation is determining how to treat illiquid asset classes. For the most part, investors have employed arbitrary techniques to address this issue. For example, some investors impose a direct constraint on the allocation to illiquid asset classes. Others assign a liquidity score to asset classes and optimize subject to a constraint that this score meet a certain threshold. It has also been proposed that liquidity be added as the third dimension in the optimization process.1 These approaches require investors to relate liquidity to expected return and risk in an arbitrary fashion. We describe an alternative technique that translates illiquidity directly into units of expected return and risk, so that investors need not address this trade‐off arbitrarily.

SHADOW ASSETS AND LIABILITIES

We begin by considering the many ways in which investors use liquidity. For example, investors depend on liquidity to meet capital demands. They rely on liquidity to rebalance their portfolios. To the extent investors are skillful at tactical asset allocation, they depend on liquidity to profit from this skill. Investors require liquidity to exploit new opportunities or to exit from strategies they no longer expect to add value. And they require liquidity to respond to shifts in their risk tolerance. These considerations reveal that liquidity has value beyond the need to meet demands for cash. Therefore, investors bear an illiquidity cost to the extent they are unable to trade any portion of their portfolios.

Our approach for unifying illiquidity with expected return and risk is to create shadow assets and liabilities whose expected return and risk reflect the manner in which investors deploy liquidity. Shadow assets and liabilities do not require additional capital beyond what is already contained in the portfolio. Instead, we treat them as overlays just as we treat forward contracts for currency hedging.

If investors deploy liquidity to improve the expected utility of a portfolio, we attach a shadow asset to the liquid asset classes in the portfolio, because these asset classes enable investors to improve the portfolio. We think of activities that are intended to improve a portfolio as “playing offense.”

Consider tactical asset allocation. Some investors choose to allocate funds to an external manager who then engages in tactical asset allocation. In this situation, we would consider the expected return and risk2 of this allocation to comprise the expected return and risk associated with the default or average allocation of the strategy (the beta component) as well as the expected return and risk associated with the active deviations of the strategy (the alpha component).

Other investors engage in tactical asset allocation through internal management by shifting the allocation across some of the liquid asset classes within the portfolio. Strategic asset allocation typically accounts for the expected return and risk of the liquid asset classes, assuming they are held constant, but ignores the incremental return and risk associated with tactical deviations from the constant weights. We argue that investors should attach a shadow asset to the liquid asset classes in the portfolio to account for the incremental return and risk expected from the internally executed tactical shifts. This approach is consistent with the way in which external managers who engage in tactical asset allocation are treated in the asset allocation process.

Investors also use liquidity to preserve the expected utility of a portfolio. We think of these activities as “playing defense.” Consider rebalancing a portfolio. Investors construct portfolios they believe are optimal, given their views and attitudes about expected return and risk. Once the portfolio is established, however, prices change and the portfolio's weights drift away from the optimal weights, thus rendering the portfolio suboptimal. To the extent the portfolio includes illiquid asset classes, it may not be possible to rebalance to the optimal weights, in which case the portfolio will remain suboptimal. We should, therefore, attach a shadow liability to those asset classes in the portfolio that cannot be moved, because they limit the extent to which an investor is able to restore the optimal weights.

Conceptually, our approach to illiquidity is straightforward. We attach a shadow asset to the liquid asset classes of a portfolio to account for the way liquidity is deployed to improve its expected utility. And we add a shadow liability to the illiquid asset classes in a portfolio to account for the extent to which illiquidity prevents investors from preserving the portfolio's expected utility. The challenge is to measure the expected return and risk of these shadow allocations, which we discuss next.

EXPECTED RETURN AND RISK OF SHADOW ALLOCATIONS

Investors typically estimate the expected return and risk of explicit asset classes from some combination of historical data and theoretical asset pricing models. Unfortunately, there are no data for shadow allocations, nor are there any theories on which to rely. We must, therefore, resort to simulation or backtests to estimate the expected return and risk of shadow allocations. We focus on three common uses of liquidity: tactical asset allocation, portfolio rebalancing, and cash demands.

Tactical Asset Allocation

It is becoming more common for investors to manage the asset mix of their portfolios dynamically, either in response to their expectations about the relative performance of asset classes or to maintain a particular risk profile. As we discussed in Chapter 3, Samuelson (1998) presented a compelling rationale for tactically managing the asset mix of a portfolio, arguing that markets are microefficient and macroinefficient.

Be that as it may, many investors engage in tactical asset allocation; therefore, we must estimate the expected return and risk of this activity if we are to introduce this activity as a shadow asset. If the investor relies on objective and quantifiable trading rules, we simply backtest these rules to estimate their expected return, standard deviation, and correlation. If, instead, the investor relies on a subjective and nonquantifiable process, we are left to estimate the risk and return properties of this activity subjectively. Once we estimate the expected return and risk of the tactical asset allocation shadow asset, we include it in the optimization menu and set its weight equal to the sum of the weights of the liquid asset classes that are being tactically managed. Of course, we must adjust for the extent to which investors employ leverage or derivatives to execute the tactical shifts when setting the weight of the shadow asset.

Portfolio Rebalancing

As we mentioned earlier, price changes cause the actual asset mix of a portfolio to drift away from its target weights, thus rendering the portfolio suboptimal. Some investors rely on heuristic rebalancing rules to rebalance their portfolios. For example, some investors rebalance quarterly or at some other frequency, while others rebalance when asset class weights have drifted a certain distance from their target weights. Other investors apply a more rigorous method to determine the optimal rebalancing schedule. They compare the cost of rebalancing with the cost of suboptimality and employ a variation of dynamic programming to determine the optimal rebalancing schedule. We discuss this approach to rebalancing in Chapter 15. In any event, an investor must periodically rebalance a portfolio to preserve its optimality. Because rebalancing is intended to preserve the optimality of a portfolio rather than enhance it, we attach a shadow liability to the illiquid asset classes within the portfolio that prevent an investor from fully restoring the optimal weights. Because we attach a shadow liability to the illiquid asset classes that cannot be rebalanced, we estimate the expected cost of not rebalancing rather than the expected return of rebalancing. In the optimization process, we treat this cost as a negative expected return. We must resort to simulation to estimate the expected cost of not rebalancing. Moreover, we estimate this cost as a certainty equivalent, which means we do not need to estimate the uncertainty of the cost. Chapter 18 discusses certainty equivalents in detail, and we also describe them in Chapter 4.

Based on our assumptions for the expected returns, standard deviations, and correlations of the portfolio's asset classes, we apply Monte Carlo simulation to generate a large number of paths for the value of the portfolio over a given horizon at a specified frequency. We conduct this simulation under two scenarios: one in which we do not rebalance the portfolio and one in which we rebalance the portfolio at the chosen frequency, assuming a particular transaction cost.

These simulations produce two distributions for the portfolio's value at the end of the horizon. We convert each distribution into a certainty equivalent and subtract the certainty equivalent of the rebalancing simulation from the certainty equivalent of the simulation without rebalancing. This value, which will be negative, is the cost we assign to the shadow liability. We constrain the weight of this shadow liability to equal the sum of the weights of the illiquid asset classes.

Cash Demands

Investors periodically need to raise cash in order to meet demands for capital. Pension funds, for example, need to make benefit payments. Many endowment funds and foundations invest in private equity and real estate funds, which demand cash periodically as investment opportunities emerge. Private investors occasionally may need to replace lost income to meet their consumption requirements. If the cash flows into a portfolio are insufficient to satisfy these payments, the investor will need to liquidate some of the assets. These liquidations can drive a portfolio away from its optimal mix and, to the extent a portfolio is allocated to illiquid asset classes, the investors may not be able to restore full optimality. Just as is the case with rebalancing, we measure this cost in certainty equivalent units and attach it to the illiquid asset classes as a shadow liability.

In rare instances, investors may not be able to liquidate a sufficient fraction of their portfolio to meet all cash demands, in which case the investor may need to borrow funds. In these circumstances we attach another shadow liability to the illiquid asset classes to reflect the cost and uncertainty of borrowing.

OTHER CONSIDERATIONS

Before we illustrate our approach for incorporating illiquidity into the asset allocation process, we must address several complications: the effect of performance fees on risk and expected return, the valuation of illiquid assets, and the distinction between partial and absolute illiquidity.

Performance Fees

Performance fees cause the observed standard deviation of illiquid asset classes to understate their risk, because performance fees reduce upside returns but not downside returns. We correct for this bias by reverse engineering the fee calculation to derive a volatility measure that correctly captures downside deviations.3

Moreover, performance fees overstate the expected return of a group of funds, because a fund collects a performance fee when it outperforms but does not reimburse the investor when it underperforms. Consider, for example, a fund that charges a 2 percent base fee and a performance fee of 20 percent. A fund that delivers a 10 percent return in excess of the benchmark on a $100 million portfolio collects a $2 million base fee and a $1.6 million performance fee, for a total fee of $3.6 million. The investor's return net of fees, therefore, is 6.4 percent. Now suppose an investor hires two funds, each of which charges a base fee of 2 percent and a performance fee of 20 percent. Assume that both these funds have an expected return of 10 percent over the benchmark. The investor might expect an aggregate net return from these two funds of 6.4 percent. However, if one fund produces an excess return of 30 percent and the other fund delivers an excess return of −10 percent, the investor pays an aggregate fee of $4.8 million, and the net return to the investor is 5.2 percent instead of 6.4 percent. Therefore, if the illiquid asset classes comprise funds that charge performance fees, we should adjust their risk and return to account for the effect of performance fees.

Valuation

Fair‐value pricing dampens the observed standard deviation of many illiquid asset classes such as infrastructure, private equity, and real estate, because underlying asset valuations are assessed in a way that anchors them to prior‐period values. We therefore need to de‐smooth their returns to eliminate this bias. We do so by specifying an autoregressive model of returns.4 Then we invert it to derive a de‐smoothed series of returns. We estimate standard deviations and correlations from this de‐smoothed return series.

Absolute versus Partial Illiquidity

Thus far, we have implicitly treated illiquidity and liquidity as binary features. We should instead distinguish between absolute illiquidity and partial illiquidity. Absolute illiquidity pertains to asset classes that cannot be traded for a specified period of time by contractual agreement or asset classes that are prohibitively expensive to trade within a certain time frame. These are the asset classes to which we attach shadow liabilities.

The asset classes that we describe as liquid asset classes are not perfectly liquid because they are costly to trade or may require significant time to trade. We therefore adjust their expected returns by the cost of trading or by the extent to which trading delays reduce the benefit of trading. We, nonetheless, attach shadow assets to these partially illiquid asset classes because ultimately they are tradeable, which must confer at least some benefit.

CASE STUDY

We now illustrate this process by introducing U.S. real estate to the moderate portfolio from Chapter 2. Our objective is to determine how the optimal allocation to real estate changes when we account for its illiquidity. We use the NCREIF Property Index to measure the standard deviation of real estate and its correlations with the other asset classes.5 Table 11.1 shows the expected returns, standard deviations, and correlations of our liquid asset classes augmented with estimates for real estate.6

TABLE 11.1 Expected Returns, Standard Deviations, and Correlations (unadjusted)

| Correlations | ||||||||||

| Expected Return | Standard Deviation | A | B | C | D | E | F | G | ||

| A | U.S. Equities | 8.8% | 16.6% | 1.00 | ||||||

| B | Foreign Developed Market Equities | 9.5% | 18.6% | 0.66 | 1.00 | |||||

| C | Emerging Market Equities | 11.4% | 26.6% | 0.63 | 0.68 | 1.00 | ||||

| D | Treasury Bonds | 4.1% | 5.7% | 0.10 | 0.03 | −0.02 | 1.00 | |||

| E | U.S. Corporate Bonds | 4.9% | 7.3% | 0.31 | 0.24 | 0.22 | 0.86 | 1.00 | ||

| F | Commodities | 6.2% | 20.6% | 0.16 | 0.29 | 0.27 | −0.07 | 0.02 | 1.00 | |

| G | Real Estate | 6.0% | 4.3% | 0.07 | 0.10 | −0.07 | −0.09 | −0.18 | 0.15 | 1.00 |

We derive the real estate standard deviation and correlations using the “raw” NCREIF returns; we do not yet adjust for performance fees or valuation smoothing. Real estate has characteristics of both equity (because the principal is invested in real estate equity) and fixed income (because it provides a relatively stable yield). Therefore, most investors expect real estate to offer an expected return that is higher than fixed income but lower than equities. For this illustration, we choose a value of 6 percent. It would be straightforward for an investor with a different view to change this assumption and update these results.

Table 11.1 suggests that real estate is a highly attractive asset class. It has the lowest standard deviation and the lowest average correlation with the other asset classes. It offers the highest return‐to‐risk ratio by far; this would be true even if its expected return were only 4 percent, equal to that of Treasury bonds. Table 11.2 shows the optimal allocation excluding real estate (which is the moderate portfolio from Chapter 2) as well as the optimal portfolio including real estate, based on the assumptions in Table 11.1. When we include real estate, we constrain the portfolio to have the same expected return as the moderate portfolio (7.5 percent), so that the two allocations are comparable.

TABLE 11.2 Optimal Allocations Including and Excluding Real Estate (unadjusted)

| Asset Classes | Excluding Real Estate | Including Real Estate |

| U.S. Equities | 25.5 | 8.2 |

| Foreign Developed Market Equities | 23.2 | 11.3 |

| Emerging Market Equities | 9.1 | 16.3 |

| Treasury Bonds | 14.3 | 0.0 |

| U.S. Corporate Bonds | 22.0 | 0.0 |

| Commodities | 5.9 | 0.0 |

| Real Estate | n/a | 64.3 |

Table 11.2 confirms the ostensible attraction of real estate; nearly two‐thirds of the portfolio is allocated to it. Few, if any, experienced investors, however, would find this portfolio acceptable. A closer inspection reveals that real estate is riskier than its 4.25 percent standard deviation suggests. The NCREIF index declined by nearly 24 percent, more than five times its standard deviation, during the global financial crisis (Q3 2008 through Q4 2009). This drawdown is especially surprising given that it was included in the sample from which we estimated the 4.3 percent standard deviation.

To derive more reasonable allocations, we must first adjust our standard deviation and correlation estimates to correct the bias introduced by performance fees and valuation smoothing. As we mentioned earlier, performance fees reduce upside volatility but not downside volatility. The standard deviation does not distinguish between upside and downside volatility. The formula for this adjustment is presented in the Appendix to this chapter. Specifically, we assume that the real estate portfolio is managed by a single fund and that this fund charges a base fee of 2 percent annually and a performance fee equal to 20 percent of returns that exceed a 2 percent hurdle rate. After this adjustment, the standard deviation of real estate rises from 4.3 percent to 4.9 percent.

Next, we adjust for the downward bias that fair‐value pricing imposes on the standard deviation of real estate returns. This bias arises from the way in which appraisers value individual properties. Specifically, they compile a sample of comparable properties that have sold recently and use this sample to estimate fair value. To improve precision, the appraiser must look further back in time to identify more comparable observations. This creates a smoothing effect, akin to a moving average, which reduces the standard deviation of returns. Implicit in this process is an inherent trade‐off between precision and timeliness. A large sample results in a valuation estimate that is more precise but stale, whereas a small sample results in a valuation estimate that is timely but less precise.

However appraisers choose to manage this trade‐off, it is an empirical fact that real estate returns are highly smoothed; the first‐order autocorrelation of the quarterly returns in our sample is 78 percent. To de‐smooth the returns, we invert a first‐order autoregressive model as we described in the previous section. We show the detail of this adjustment in the Appendix to this chapter. After this adjustment, the standard deviation of real estate rises threefold, from 4.9 to 15.0 percent. This estimate is much more realistic. For example, it renders more probable the 24 percent loss that U.S. real estate experienced during the global financial crisis. This adjustment also increases slightly the correlation between real estate and equity asset classes and decreases slightly the correlation between real estate and fixed‐income asset classes. These adjusted estimates are shown in Table 11.3.

TABLE 11.3 Expected Returns, Standard Deviations, and Correlations (adjusted for performance fees and valuation smoothing)

| Correlations | ||||||||||||

| Expected Return | Standard Deviation | A | B | C | D | E | F | G | H | I | ||

| A | U.S. Equities | 8.8% | 16.6% | 1.00 | ||||||||

| B | Foreign Developed Market Equities | 9.5% | 18.6% | 0.66 | 1.00 | |||||||

| C | Emerging Market Equities | 11.4% | 26.6% | 0.63 | 0.68 | 1.00 | ||||||

| D | Treasury Bonds | 4.1% | 5.7% | 0.10 | 0.03 | −0.02 | 1.00 | |||||

| E | U.S. Corporate Bonds | 4.9% | 7.3% | 0.31 | 0.24 | 0.22 | 0.86 | 1.00 | ||||

| F | Commodities | 6.2% | 20.6% | 0.16 | 0.29 | 0.27 | −0.07 | 0.02 | 1.00 | |||

| G | Real Estate | 6.0% | 15.0% | 0.14 | 0.13 | 0.01 | −0.19 | −0.12 | 0.12 | 1.00 | ||

Next, we show how to identify optimal allocations that account for liquidity. We begin by estimating the return and standard deviation arising from three uses of liquidity: tactical asset allocation, portfolio rebalancing, and funding cash demands.

Tactical Asset Allocation

Based on past performance, we assume that the investor's tactical asset allocation program will produce an excess return of 40 basis points and tracking error of 80 basis points per year, resulting in an information ratio of 0.50 after costs. If there were no track record, an investor could also derive these estimates by backtesting a tactical asset allocation strategy. Tactical asset allocation is a proactive use of liquidity; it serves to improve the expected utility of the portfolio. We therefore attach these return and standard deviation values as a shadow asset to the liquid asset classes within the portfolio.

Rebalancing

To estimate the benefit that rebalancing brings to the portfolio, we simulate 10,000 five‐year paths given the assumptions presented in Table 11.1. Along each path, we record the performance of two portfolios: one that we rebalance at the end of each year and one that we never rebalance. When we rebalance the first portfolio, we deduct transaction costs, which we assume to equal 20 basis points for all asset classes. We then compute the difference between the two portfolios' certainty equivalents based on their end‐of‐horizon return distributions. This difference, which represents the suboptimality cost that arises from asset weight drift, is equal to 16 basis points yearly. We use certainty equivalents to reflect the fact that any drift in weights is undesirable; portfolios with higher expected returns will have too much risk, while those with lower risk will have too little expected return. By definition, there is no risk associated with a certainty equivalent, so we assume that the standard deviation associated with this benefit is zero. Rebalancing is a defensive use of liquidity; it preserves the utility of the portfolio. We therefore attach this value to the illiquid component of the portfolio (in this case, real estate) as a shadow liability.

Cash Demands

We employ simulation to estimate the benefit that comes from an investor's ability to meet cash demands. Specifically, we assume that:

Cash demands arise randomly in sizes equal to 1, 2, or 3 percent of portfolio value with probabilities of 10, 10, and 5 percent, respectively. We therefore assume that, in any given quarter, there is a 25 percent (10 + 10 + 5) chance that a cash demand will arise and a 75 percent chance that there will be no cash demand.

Cash demands arise randomly in sizes equal to 1, 2, or 3 percent of portfolio value with probabilities of 10, 10, and 5 percent, respectively. We therefore assume that, in any given quarter, there is a 25 percent (10 + 10 + 5) chance that a cash demand will arise and a 75 percent chance that there will be no cash demand.- To meet cash demands, the investor sells U.S. equities, foreign developed market equities, and Treasury bonds in amounts proportional to their allocations.

- When cumulative cash demands along any particular path exceed 10 percent of the starting portfolio value, the investor ceases to deplete liquid assets and begins borrowing at an annualized rate of 5 percent to meet further cash demands.

- We do not allow cash demands along any particular path to exceed 20 percent of the starting portfolio value.

Of course, the actual values for these assumptions vary significantly from one investor to the next. A major advantage of this approach is that we can customize the simulation to account for the unique circumstances of any given investor. Some investors may calibrate the simulation to include cash inflows that can help to offset cash demands.

TABLE 11.4 Expected Return and Standard Deviation of Shadow Asset and Liability

| Return (basis points) | Standard Deviation (basis points) | Attached to: | |

| Shadow Asset | |||

| Tactical Asset Allocation | 40 | 80 | Liquid Assets |

| Total Shadow Asset | 40 | 80 | Liquid Assets |

| Shadow Liability | |||

| Suboptimality Cost from Weight Changes | 16 | 0 | Illiquid Assets |

| Suboptimality Cost from Cash Demands | 18 | 0 | Illiquid Assets |

| Borrowing Cost from Cash Demands | 17 | 10 | Illiquid Assets |

| Total Shadow Liability | 51 | 10 | Illiquid Assets |

We measure two distinct costs associated with these simulations: borrowing cost and suboptimality cost. Borrowing cost is straightforward: It is the average annual interest incurred along each path expressed as a percentage of the illiquid assets. Suboptimality cost is the incremental suboptimality that arises when we tap liquid assets to fund cash demands, which distorts the portfolio's allocation. To measure suboptimality cost, we first compute the certainty equivalent of a scenario in which we never rebalance and we tap a subset of liquid assets (or borrow) to meet cash demands, as described above. We then compute the certainty equivalent of a scenario in which we rebalance annually and we withdraw funds from all asset classes, proportionally, to meet cash demands. The difference between these two certainty equivalents represents the suboptimality costs attributable to cash demands. It is incremental to the suboptimality cost associated with rebalancing, which is driven purely by the immobility of illiquid asset classes.

The ability to meet cash demands without borrowing or distorting portfolio weights is a defensive use of liquidity; it preserves the utility of the portfolio. We therefore attach these values to real estate as a shadow liability. Exposure to illiquid assets is more costly to investors who have high cash demands than to investors who have low cash demands, all else being equal.

Table 11.4 shows the expected return and standard deviation of the shadow asset and liability as well as their components.

To identify the optimal allocation that accounts for liquidity, we must attach the shadow asset and liability to the appropriate explicit assets in the portfolio. Table 11.5 combines the expected returns, standard deviations, and correlations for the liquid assets and real estate from Table 11.3 with the expected return and standard deviation for the shadow asset and liability.

TABLE 11.5 Expected Returns, Standard Deviations, and Correlations (adjusted for performance fees and valuation smoothing) and Including Shadow Asset and Liability

| Correlations | |||||||||||

| Expected Return | Standard Deviation | A | B | C | D | E | F | G | H | I | |

| A U.S. Equities | 8.8% | 16.6% | 1.00 | ||||||||

| B Foreign Developed Market Equities | 9.5% | 18.6% | 0.66 | 1.00 | |||||||

| C Emerging Market Equities | 11.4% | 26.6% | 0.63 | 0.68 | 1.00 | ||||||

| D Treasury Bonds | 4.1% | 5.7% | 0.10 | 0.03 | −0.02 | 1.00 | |||||

| E U.S. Corporate Bonds | 4.9% | 7.3% | 0.31 | 0.24 | 0.22 | 0.86 | 1.00 | ||||

| F Commodities | 6.2% | 20.6% | 0.16 | 0.29 | 0.27 | −0.07 | 0.02 | 1.00 | |||

| G Real Estate | 6.0% | 15.0% | 0.14 | 0.13 | 0.01 | −0.19 | −0.12 | 0.12 | 1.00 | ||

| Shadow Asset | 0.4% | 0.8% | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | |

| Shadow Liability | −0.5% | 0.1% | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 |

In this example, we assume that the shadow asset and liability are uncorrelated with the explicit assets. We could relax this assumption. For example, if the performance of the tactical asset allocation strategy were negatively correlated with broad equity market performance, we could assume a negative correlation between the shadow asset and the equity asset classes. This would result in a higher optimal allocation to liquid assets because the deployment of liquidity would introduce beneficial diversification to the underlying portfolio.

To compute optimal allocations with the shadow asset and liability, we must impose two additional constraints on the mean‐variance analysis:

- We constrain the allocation to the shadow asset to equal the sum of allocations to the liquid asset classes.

- We constrain the allocation to the shadow liability to equal the allocation to real estate.

We also continue to constrain the expected return of the portfolio to equal 7.5 percent in order to isolate the impact of the adjustments for performance fees, valuation smoothing, and liquidity on the optimal allocations. Table 11.6 shows this sequence of optimal allocations. In this example, we assume that real estate is fully illiquid and the other asset classes are perfectly liquid. In practice, we could account for partial illiquidity by adjusting their expected returns to account for transaction costs.

TABLE 11.6 Optimal Allocations Accounting for Performance Fees, Valuation Smoothing, and Liquidity (%)

| Asset Classes | Excluding Real Estate | No Adjustments | Adjusted for Fees and Smoothing | Adjusted for Fees, Smoothing, and Liquidity |

| U.S. Equities | 25.5 | 8.2 | 18.5 | 19.6 |

| Foreign Developed Market Equities | 23.2 | 11.3 | 18.7 | 18.8 |

| Emerging Market Equities | 9.1 | 16.3 | 11.6 | 9.7 |

| Treasury Bonds | 14.3 | 0.0 | 0.1 | 15.4 |

| U.S. Corporate Bonds | 22.0 | 0.0 | 26.2 | 19.5 |

| Commodities | 5.9 | 0.0 | 2.2 | 3.9 |

| Real Estate | 0.0 | 64.3 | 22.8 | 13.0 |

| Shadow Asset | n/a | n/a | n/a | 87.0 |

| Shadow Liability | n/a | n/a | n/a | 13.0 |

| Expected Return | 7.5 | 7.5 | 7.5 | 7.5 |

| Standard Deviation | 10.8 | 7.48* | 10.2 | 9.6 |

*The standard deviation of this portfolio is artificially low because it is based on real estate returns that have not been adjusted for performance fees or valuation smoothing.

The first two columns of Table 11.6 are restated from Table 11.1 to facilitate comparison. The third column shows the optimal allocation that accounts for the fee and de‐smoothing adjustments to real estate, but not for liquidity. Collectively, these two adjustments result in a dramatic, two‐thirds reduction in the real estate allocation. The last column shows the optimal allocation in which we have adjusted for illiquidity by including the shadow asset and liability. The 13.0 percent allocation to the shadow liability is equal to the 13.0 percent allocation to real estate. The 87.0 percent allocation to the shadow asset is equal to the total allocation to liquid assets. Overall, the allocation to real estate falls from 64.3 percent with no adjustments to 13.0 percent when adjusted for fees, smoothing, and liquidity. This impact is presented graphically in Figure 11.1. We suspect that the allocation represented in the final column of Table 11.4 would strike most investors as reasonable.

FIGURE 11.1 Optimal Allocation to Real Estate with and without Adjustments

In this example, we have assumed that the investor has only three uses for liquidity. In practice, investors are likely to derive other benefits from liquidity (and costs from illiquidity) as well. We can expand this simulation framework to account for a wide array of liquidity benefits and illiquidity costs. We have also assumed that there is only one illiquid asset class—real estate. We could easily expand this framework to incorporate other illiquid asset classes such as private equity and infrastructure, each of which may have different degrees of illiquidity.

THE BOTTOM LINE

Most investors recognize there are costs associated with holding illiquid assets, but they have struggled to account for them explicitly when constructing portfolios. We propose that investors identify the specific benefits they derive from liquidity as well as the costs they incur from illiquidity. We introduce a simulation framework to estimate the return and standard deviation associated with these benefits and costs. We then determine whether liquidity is used offensively to improve a portfolio or defensively to preserve the quality of a portfolio. In the former case, we attach a shadow asset to the liquid portion of the portfolio, and in the latter case, we attach a shadow liability to the illiquid portion of the portfolio. These shadow allocations enable us to account for liquidity when we estimate the optimal allocation to illiquid asset classes. But we must first adjust for the biases that performance fees and appraisal‐based valuations introduce to illiquid assets.

This approach explicitly accounts for the impact of liquidity on a portfolio in units of expected return and risk, thereby enabling investors to compare liquid and illiquid asset classes within a single, unified framework. It also highlights several important features of liquidity.

- Liquidity can be used offensively as well as defensively. Therefore, even long‐horizon investors with positive cash flows incur opportunity costs to the extent any fraction of their portfolio is illiquid.

- The optimal exposure to illiquid assets is specific to each investor. The illiquidity premium that is priced into illiquid asset classes reflects the average investor's liquidity needs. To the extent a particular investor's liquidity needs differ from the average, the investor must take this into account. Failing to do so is akin to ignoring tax brackets or liabilities; it will almost certainly produce a suboptimal result.

- Liquidity affects explicitly a portfolio's expected return and risk. It need not be treated as a distinct feature of a portfolio nor measured in arbitrary units.

APPENDIX

Performance Fee Adjustment

For a single fund that charges a base fee and a performance fee on an annual basis, Equation (11.A1) computes the net return ![]() , where

, where ![]() is the gross return,

is the gross return, ![]() is the performance fee, and

is the performance fee, and ![]() is the base fee. We reverse this formula to solve for the gross return, as shown in Equation (11.A2). The standard deviation of gross returns is not influenced by the dampening effect of performance fees, which truncates the upside of the return distribution but not the downside.

is the base fee. We reverse this formula to solve for the gross return, as shown in Equation (11.A2). The standard deviation of gross returns is not influenced by the dampening effect of performance fees, which truncates the upside of the return distribution but not the downside.

In practice, performance fees may be subject to additional hurdle rates (beyond the base fee) and are often accrued on a monthly basis throughout the year. It is straightforward to measure the impact of performance fees in these contexts using simulation.

De‐smoothing Adjustment

To de‐smooth a return series, we employ a simple first‐order autoregressive model as shown by Equation (11.A3). This equation assumes that the return in a given period, ![]() , is a linear function of the return in the previous period plus an intercept and an error term:

, is a linear function of the return in the previous period plus an intercept and an error term:

![]() is the autoregressive coefficient,

is the autoregressive coefficient, ![]() is the intercept term, and

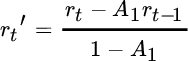

is the intercept term, and ![]() is the error term. To estimate the de‐smoothed return in period t, we first subtract the smoothed component of the return in period

is the error term. To estimate the de‐smoothed return in period t, we first subtract the smoothed component of the return in period ![]() , which is explained by the return in period

, which is explained by the return in period ![]() . We then divide this residual by (

. We then divide this residual by (![]() ) to “gross up” the de‐smoothed component to account for the portion of the return that we removed. This calculation is given by Equation (11.A1):

) to “gross up” the de‐smoothed component to account for the portion of the return that we removed. This calculation is given by Equation (11.A1):

where ![]() is the de‐smoothed return.

is the de‐smoothed return.

REFERENCES

- W. Kinlaw, M. Kritzman, and D. Turkington. 2013. “Liquidity and Portfolio Choice: A Unified Approach,” Journal of Portfolio Management, Vol. 39, No. 2 (Winter).

- A. Lo, C. Petrov, and M. Wierzbicki. 2003. “It's 11pm—Do You Know Where Your Liquidity Is? The Mean‐Variance Liquidity Frontier,” Journal of Investment Management, Vol. 1, No. 1 (First Quarter).

- P. A. Samuelson. 1998. “Summing Up on Business Cycles: Opening Address,” in Beyond Shocks: What Causes Business Cycles, edited by J. C. Fuhrer and S. Schuh (Boston: Federal Reserve Bank of Boston).