73Promises, promises

Thirty-ve, thirty-six, thirty-seven. Please Brenda, I was silently

begging, keep your jacket on. Jerry bared his teeth, keeping his

gaze xed on head of compliance. ‘Come on,’ he muttered, ‘it

must be eighty degrees in there.’

Forty seconds. I’d been holding my breath because of the tension.

My maximum exposure was £400, which was £20 multiplied by

twenty seconds. And after that, my upside was unlimited.

Forty-nine seconds in and disaster struck. No! Brenda picked up

a manila le and fanned herself. ‘Looks like you’ll be making a

visit to the cash point soon.’

‘Don’t be so sure, Jerry. In six – no, ve – seconds I’ll be in the

kill zone.’

‘Don’t think so, mate.’ And, immediately he’d nished, Brenda

suddenly stood up and struggled to slip her green jacket from her

bulky shoulders.

‘Stop the clock!’ Jerry shouted out. ‘I make that four seconds. You

owe me eighty quid. Cash only, I’m afraid.’

But I’d stopped listening. A woman with long black hair elegantly

waved her manicured hands in front of her beautiful face. The

rst time I saw Perrine’s face was while I was losing money.

Sad to say, this was to prove an omen.

The time value of money

Perrine had been brought up in Paris, Madrid and Milan. She’d

studied art history in Turin and philosophy at Columbia. From a

purely rational point of view, it wasn’t entirely clear what Perrine

brought to Saiwai in terms of hard business skills. But I – like 90

per cent of Saiwai’s male staff – had fallen head over heels in love.

I smiled every time she mangled English, which was her third

or fourth language. Jerry was playing devil’s avocado with the

market. Old-time risk-averse investors were dinosaurs voting for

Christmas.

Welcome to the jungle74

Jerry – who never missed a trick – teased me mercilessly. But his

cruellest trick was to assign me to be Perrine’s mentor. I blushed

at the very thought of her and stammered in her presence. I

bought a book called The Time Value of Money Made Easy and

prepared our rst lesson.

‘This topic is much easier than you think.’ I imagined that would

be a good opening: it showed I was condent and it was designed

to relax Perrine.

‘No it isn’t,’ she said. You know you’ve got it bad when you nd

a girl’s sulking attractive.

‘All you need to do is imagine you lend €10 to a friend for a year.’

I thought Euros would make me seem more Continental in her

eyes. The currency hadn’t even been invented at this stage so I

thought I’d also look pretty cutting-edge. ‘Why does your friend

need to pay back more than he borrowed?’

‘What’s my friend called?’

‘Eh?’ The question threw me. ‘Anything you like.’

‘Good. I will call him Armin.’

It sounds stupid but I was jealous of this imaginary Armin. In

fact, it sounds really pathetic, doesn’t it?

The promise of money is not worth the same as money today

I went on. ‘There are three reasons why Armin will need to pay

you back more.’

1. Inflation

This erodes the value of money. Suppose ination is very low at

2 per cent. If Armin gives you €10 after a year, you’ll really only

receive €9.80. What’s happened to the 20c? Ination has bitten

off a chunk.

Ination erodes the value of savings and hyper-ination

can destroy a country’s economy. In 2008 ination reached

75Promises, promises

231,150,888 per cent per year in Zimbabwe. (That was the ofcial

estimate, which probably understated the real gure.)

2. Opportunity cost

Armin has borrowed your €10 for a year, and that stopped you

from doing anything with the money. You need a reward for

renting your money out to Armin. How about the interest you

would have made if you’d tied up the money in a bank deposit

for twelve months? Perhaps 3 per cent would be enough?

3. Risk of the borrower

This is a very variable factor. A lender will charge more if they

think the borrower is risky.

What are the signs of a bad bet?

Not long in a new job? (Perrine ticked that one).

Already got big debts (tick).

Credit cards that can’t be paid off within a month (tick).

But Armin has none of these problems. His individual risk as a

borrower was only 5 per cent. This number reects the riskiness

of the borrower. It varies from one borrower to another, and will

be much higher if the lender has doubts about being paid back.

After my explanation, Perrine added these three elements

together.

She begins with inflation . . . 2%

. . . then adds opportunity cost . . . 3%

. . . and the risk of the borrower. 5%

The total is the cost of borrowing 10%

Armin was going to pay interest at the rate of 10 per cent per

annum.

It’s just the same as compounding. If you lend €10 and think

Armin is a 10 per cent risk, he will need to pay back €11 next

year. That’s the initial €10 multiplied by 1.1, because Armin’s

Welcome to the jungle76

going to have to pay you 10 per cent interest for borrowing your

money.

Compounding

A Money borrowed €10

B Interest rate 10%

C 5 A 3 (11B) Amount to pay back €11.00

‘Perrine, let me ask you a question. You can have €10 now, cash

in your hands. Or you can have the promise of €10 in exactly one

year’s time. Which option do you prefer?’

She considered for a second. ‘Everyone

should choose the cash now. It’s certain,

you’ve got it, there’s no chance of the

borrower not paying. The promise is just

that. It’s not guaranteed, and your borrower

may go bust, go on the run, spend all their

cash on drink or just plain die. The lender

needs compensation because of these added

risks. And the longer you lend the money, the more compen-

sation you will demand because there is more time for bad things

to happen.’

‘So what does this mean for bankers?’

Perrine delicately chewed the top of her pen.

‘€10 today does not have the same value as the promise of €10 in

one year. Since all of us prefer to take €10 today, it must follow

that €10 next year is worth less than €10 today.’

‘How much less?’

‘I don’t know.’

‘Well, let me tell you.’ She smiled at me. Perrine actually smiled

at me! This teaching lark was better than I had ever imagined.

‘‘

your borrower

may go bust, go on

the run, spend all

their cash on drink

or just plain die

’’

77Promises, promises

Discounting is compounding in reverse

Perrine was determined to get the next bit done and dusted. She

knew that the total risk of lending money was worth a return of

10 per cent. She also knew she would be paid €10 in one year’s

time. But what was that future payment worth to her today?

She divided the payment of €10 by 1.1 to discount the value of the

repayment in the future. Why 1.1? Because it’s 1 plus 10 per cent.

The 10 per cent is called the discount rate. And 1 divided by 1.1,

which is 90.9 per cent, is the discount factor. It’s like saying the

promise of €10 in one year is only worth 90.9 per cent. It follows

that €10 in one year is only worth €9.09 today.

Discounting

A Cash fl ow at the end of Year 1 €10

B Discount rate 10%

C 5 1/(1 1 B) Discount factor 90.9%

D 5 A 3 C Value of cash fl ow to us now €9.09

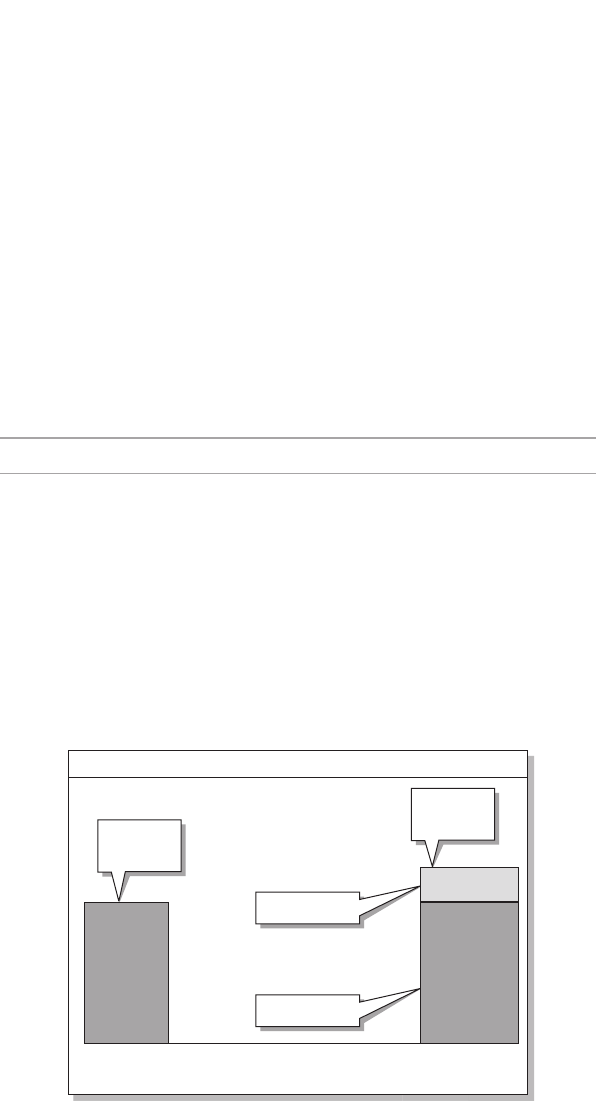

She sketched out a couple of simple diagrams. In the rst, Armin

borrows €10 and has to pay back €11. The difference (€1) is the

interest. As you move from today (on the left) to the future (the

right) the value of the amount to repay increases.

Compounding

Borrow

€10

€10

Today Last day of

the year

Interest €1

Principal €10

Repay

€11

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.