CHAPTER 6

Controlling Costs and Schedule

Systems That Really Work

In the design and implementation of a project cost control system, the individual characteristics of the organization performing the project and of the project itself must be considered. However, the following criteria should be considered regardless of the specific situation:

• Validity. The information reported must accurately reflect actual versus estimated costs.

• Timeliness. The cost data must be reported early enough so that managerial action can be taken if a problem arises.

• Cost effectiveness. Collection and reporting of cost data must be done in a way that does not hinder project progress.1

Cost control systems can work if they are set up with these criteria in mind. This chapter covers how to design and implement an effective project cost control system. The examples given are drawn from the construction industry, yet these same principles are applicable to other types of projects.

DEVELOPING A PROJECT COST CONTROL SYSTEM

Establishing a Project Cost Control Baseline

The project cost control baseline is developed from the project cost estimate.2 Initially, during the conceptual phase, the cost estimate exists only as a preliminary or order of magnitude estimate3; as the engineering design progresses, more precise estimates of cost can be developed. A detailed cost estimate, based on work quantities determined from completed project drawings and specifications, provides the most precise estimate of cost. This detailed cost estimate forms the basis of the project cost control baseline.

However, the detailed cost estimate often cannot be directly used as a control budget. Usually, some transformation is required. For example, for bidding or negotiating purposes, the estimate may originally have been organized in a form convenient for the project owner. The project contractor may find it advantageous to reorganize the estimate into a form that matches his or her cost control preferences. In addition, the level of detail provided by the estimate may not be appropriate for the control budget.

Several factors should be considered when deciding on the appropriate level of detail for the cost control budget:

• How many individual cost elements can the office and field personnel be expected to break actual project costs into for reporting purposes?

• How many individual cost elements can the project management team effectively review and monitor?

• How can Pareto’s Law be taken into account—that 80 percent of the total project cost is probably represented by only 20 percent of the cost items?

The answers to these questions and the selection of an appropriate level of detail depends on the characteristics of the project and on the management resources allocated to manage the project. If, for instance, a cost engineer is assigned to assist the project manager in supervising the collection and reporting of cost control information, greater detail may be practical. Generally, it is desirable to maintain more detail on cost items that represent a more significant portion of the project cost.

Consider a project in which structural concrete represents a large percentage of the total project cost. In this case the structural concrete costs should be broken down into a number of cost subaccounts categorized by work operation, such as formwork, reinforcing, and concrete placement. Further subclassification by structural component, such as foundation, slabs, columns, and beams, may also be appropriate. On the other hand, if only a relatively small percentage of the total project cost involves masonry, then all of the masonry cost items in the estimate might be transferred to the project cost control budget as a single summary. Figure 6-1 provides an illustration of how the project cost estimate information might be transferred to the cost control budget.

Establishing a standard organizational listing and coding of all cost items is a prerequisite to the preparation of both the detailed cost estimate and the cost control budget. The standard organization listing consists of a comprehensive list of all conceivable cost items. In the construction industry, such a list might be prepared using the Masterformat published by the Construction Specifications Institute (CSI).4 The CSI Masterformat provides an extensive classification and coding of cost items relevant to the construction industry and is widely used by manufacturers, architects, contractors, and other professionals.

The standard cost code system should be tailored to the organization’s needs. Some cost items found in the CSI standard can be deleted if not within the scope of work performed. Other cost categories can be expanded to provide additional detail in critical areas.

The level of detail resulting from the cost coding system can be adjusted by means of a system of account hierarchy. The highest category is represented as a major account. Each major account is subdivided into subaccounts and subsubaccounts. Cost data can be summarized and collected at any level within the account hierarchy. The CSI contains 16 major cost accounts. Figure 6-2 provides an example of how the account hierarchy system can be used.

FIGURE 6-1. TRANSFER OF PROJECT COST ESTIMATE INFORMATION TO THE COST CONTROL BUDGET

Just as the standard cost code is tailored to the general operation of the organization, the project cost control budget is tailored to satisfy the cost control needs of the specific project. Cost control account categories and levels of detail are matched to the particular characteristics of the project. Then the cost figures are transferred from the cost estimate to the appropriate account in the cost control budget.

A well-designed and accurately prepared cost control budget is an essential requirement for a successful project cost control system. The cost control budget becomes a cost baseline used as a benchmark for monitoring actual cost and progress during the entire project. The cost control budget is also an important ingredient for practically all of the project management activities.

Collecting Actual Cost Data

FIGURE 6-2. EXAMPLE OF COST CODE HIERARCHY

The collection of project cost data falls within the scope of activities normally conducted by the organization’s accounting system.5 Project costs are collected, classified, and recorded as a routine accounting function. Individual project costs, when collected at the organizational level and compared with overall income, are a basic component in determining profitability of the enterprise.

Although job cost accounting is a fundamental part of most accounting systems, the job cost accounting format used frequently does not satisfy the requirements of project cost control. Classification and level of detail used in the accounting system may not match with the cost control budget developed for the project. For example, we may wish to examine the labor and material costs associated with a certain category of work tasks such as formwork for cast-in-place concrete. However, the job cost accounting system may provide only a summary of all concrete costs.

Obviously, the greatest efficiency is obtained when the accounting system can directly provide the information required by the cost control system. A great deal of progress has been made in this area, particularly with the use of computerized cost accounting systems. Increased flexibility in the assignment of cost account codes and the production of specialized reports have significantly improved recent computerized accounting packages.

However, as a practical matter, some of the detailed cost breakdown data required by the cost control system may have to be generated separately from the general accounting system. This involves reviewing source documents such as supplier’s invoices, purchase orders, and labor time sheets at the project level. The cost data required for cost control purposes can be extracted and recorded in the cost control records.

Regardless of how the actual cost data are collected, they must be organized in accord with the project cost control budget. Comparisons of actual to budget costs can be made only when both categories of costs are classified, summarized, and presented in identical formats. We do not want to compare apples with oranges.

Determining Earned Value

Earned value is the portion of the budgeted cost that has been earned as a result of the work performed to date. Cost values originally assigned to the various items in the cost control budget represent total costs. However, as work on the project progresses, actual costs must periodically be compared with budget costs. To make this comparison, the amount of earned value of the total budget must be determined.

Several methods are available for measuring project progress. Each method has different features and provides a somewhat different measure of progress. Sound managerial judgment must be applied no matter which method is used. Progress estimates require honest and realistic assessment of the work accomplished versus the work remaining.

Some of the more common methods of determining earned value are as follows:

![]() Units completed. This method involves measuring the number of work units that have been accomplished and comparing the number of completed units with the total number of units in the project.6 No subtasks are considered, and partially completed units are generally not credited. For example, suppose that 420 linear feet (LF) of 4-inch diameter steel pipe has been installed. If the total project requires 2,100 LF of pipe, then the percentage of completion is 20 percent (420 LF divided by 2,100 LF).

Units completed. This method involves measuring the number of work units that have been accomplished and comparing the number of completed units with the total number of units in the project.6 No subtasks are considered, and partially completed units are generally not credited. For example, suppose that 420 linear feet (LF) of 4-inch diameter steel pipe has been installed. If the total project requires 2,100 LF of pipe, then the percentage of completion is 20 percent (420 LF divided by 2,100 LF).

![]() Incremental milestones. When the work task involves a sequential series of subtasks, the percentage of completion may be estimated by assigning a proportionate percentage to each of the subtasks.7 For example, the installation of a major item of equipment might be broken down as follows:

Incremental milestones. When the work task involves a sequential series of subtasks, the percentage of completion may be estimated by assigning a proportionate percentage to each of the subtasks.7 For example, the installation of a major item of equipment might be broken down as follows:

• Construct foundation pad 10 percent

• Set equipment on foundation 60 percent

• Connect mechanical piping 75 percent

• Connect electrical 90 percent

• Performance testing and start up 100 percent.

Percentage of completion is estimated by determining which of the milestones have been reached. The accuracy of this procedure depends on a fair allocation of percentage to the subtask in relation to costs.

![]() Cost to complete. When properly applied, this method can provide the most accurate representation of project cost status.8 The cost to complete the remaining work for a given task is first estimated. This detailed cost estimate uses both the original cost estimate and any historical cost data acquired so far on the project. The idea is to develop the best possible estimate of the cost required to complete the task. The percentage of completion is calculated as follows:

Cost to complete. When properly applied, this method can provide the most accurate representation of project cost status.8 The cost to complete the remaining work for a given task is first estimated. This detailed cost estimate uses both the original cost estimate and any historical cost data acquired so far on the project. The idea is to develop the best possible estimate of the cost required to complete the task. The percentage of completion is calculated as follows:

For example, if the actual cost to date for structural steel erection is $18,500 and the estimated cost to complete the task is $6,500, the percentage of completion is calculated as follows:

With each of the methods used to estimate the percentage of completion, earned value is calculated as the percentage of completion times the original budget cost for the task.

Reporting and Evaluating Cost Control Information

Cost control status reports can be custom-tailored to suit the preferences of individual managers and to accommodate specific project differences. However, in general, cost status reports should provide an item-by-item comparison of actual cost to earned value.9 Estimated cost to complete and projected total cost can also be shown. Variations from the cost budget can be presented as a percentage or as an actual value, and categorical breakdowns of the cost status can also be shown. It is often useful to separate material, labor, equipment, and subcontract costs.

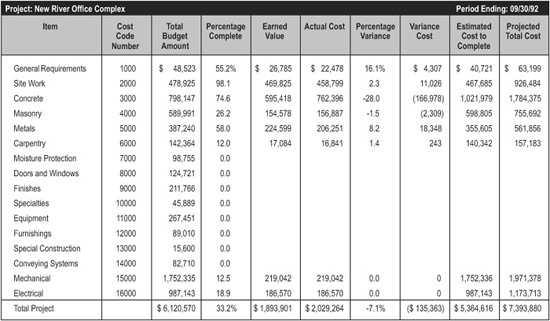

Figure 6-3 is an example of a monthly cost control status report. The figures listed as “Total Budget Amount” represent the originally estimated costs for each of the cost account categories. Actual costs to date are compared with earned values, and variances are listed. Estimated costs to complete are also given. The projected total cost has been calculated by adding the actual cost to the estimated cost to complete. This report could have been expanded to provide a separate listing of material, labor, equipment, and subcontract costs. The amount of detail can be structured to meet the requirements of the project manager. Managers will be particularly interested in the variance between actual cost and earned value, and the resulting total cost projection. Accuracy and timeliness are equally important in reporting cost control status. If the information is to be of any value to the project manager, it must be provided soon enough to allow for corrective action. Monthly cost control reports should be provided as soon as possible after the end of the month. The time lag between the cutoff of the cost period and production of the report should be as small as possible.

FIGURE 6-3. MONTHLY COST CONTROL STATUS REPORT

Material suppliers and subcontractors are normally paid monthly. Therefore, a monthly cost report seems appropriate for summarizing these costs. However, labor costs are typically paid on a shorter interval, such as weekly. Labor costs are also likely to be more variable and consequently are normally the subject of greater management attention. It may be appropriate to generate weekly status reports of labor costs.

FIGURE 6-4. COST-SCHEDULE GRAPH

Graphical representations of the cost-schedule data are often useful in providing a quick visualization of cost control status. One of the most common is a cost-schedule graph in which actual and budget costs are plotted against performance time. Figure 6-4 is an example of a cost-schedule graph. This example provides a graphical representation of the data included in the cost control status report given in Figure 6-3. In this example, the project is approximately one week behind schedule in time, and total actual costs have exceeded the cost budget by 7.1 percent.

Taking Corrective Action

One of the primary functions of the cost control system is to identify problem areas to the manager early enough so that corrective action can be taken. Although we would not expect actual costs and earned values to be identical, a significant variance indicates a problem. Determining the source of the problem requires an investigation by the project manager. There are many possible causes, such as an estimating mistake, a change in material prices, a change in labor wage rates, or a change in work productivity. The cost control system cannot identify the cause of the problem, but tells the manager where to look for the cause. Additionally, the cost control system furnishes feedback to the manager, showing the effect of any corrective action.

Achieving Project Success by Controlling Costs

Project success depends to a great extent upon management’s ability to control cost. Although there may be other important project goals, cost remains a universal measure of success. Projects with substantial cost overruns are rarely considered successful.

Maintaining cost control requires a well-designed and implemented project cost control system. A sound project cost control system performs four basic functions:

1. Establishes baseline cost.

2. Collects actual cost data.

3. Reports and evaluates (including earned value).

4. Takes corrective action.

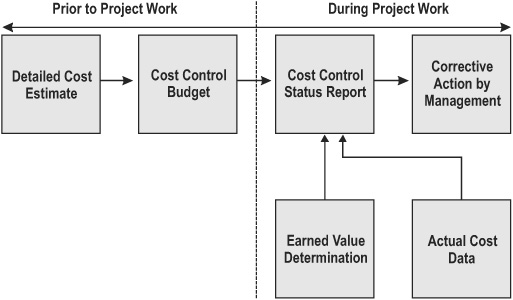

FIGURE 6-5. ELEMENTS OF A COST CONTROL SYSTEM

The level of cost detail and the format of the report documents should be matched to the requirements of the specific project and the management team. Figure 6-5 provides an illustration of the elements involved in a project cost control system and their interrelationship.

Establishing an adequate project cost control system requires an investment. Project managers must take the time before starting project work to develop the structure of the cost control system. They must decide upon cost classification and the appropriate level of cost detail to be monitored. They need to work out actual cost collection procedures.

How will the cost control system interface with the organization’s accounting system? Reporting frequencies, procedures, and formats must be determined. Administration of the cost control system also requires the allocation of staff time. However, if management is willing to commit the necessary systems, it is possible to have a project cost control system that really works. Operating without effective cost control is gambling in the dark.

![]() What are the four basic functions of a project cost control system, and how are they interrelated?

What are the four basic functions of a project cost control system, and how are they interrelated?

![]() What are three common methods for determining earned value on a project? What are the relative advantages of each?

What are three common methods for determining earned value on a project? What are the relative advantages of each?

![]() How much cost control is enough? What factors should be taken into account when deciding on the right level of cost control?

How much cost control is enough? What factors should be taken into account when deciding on the right level of cost control?

REFERENCES

1 D. Bain. The Productivity Prescription. New York: McGraw-Hill, 1982, p. 62.

2 Construction Industry Institute. Project Control for Construction. Austin, TX: CII, 1989, p. 6.

3 R. L. Peurifoy, and G. D. Oberlender. Estimating Construction Costs. New York: McGraw-Hill, 1989, p. 422.

4 Construction Specifications Institute, Masterformat. Washington, D.C.: CSI, 1989.

5 K. Collier. Fundamentals of Construction Estimating and Cost Accounting With Computer Applications. Englewood Cliffs, N.J.: Prentice-Hall, 1987, p. 44.

6 Construction Industry Institute, p. 14.

7 Ibid.

8 Fails Management Institute, Financial Management for Contractors. New York: McGraw-Hill, 1981, p. 4.

9 Powers, S. E., and B. H. Brown. Walker’s Practical Accounting and Cost Keeping for Contractors. Chicago: Frank R. Walker, 1982, p. 116.