Deciding whether you need a budget

Discovering tips for personal and business budgets

Setting up and reviewing a budget

I don't think that a budget amounts to financial handcuffs, and neither should you. A budget is really a plan that outlines the way you need to spend your money to achieve the maximum amount of fun or the way a business needs to spend its money to make the most profit.

A budget, as you probably know, is a list of the ways you earn and spend your money. If you create a good, workable category list with Quicken (see Chapter 2), you're halfway to a good, solid budget. (In fact, the only step left is to specify how much you earn in each income category and how much you spend in each expense category.)

Does everybody need a budget? No, of course not. Maybe, at your house, you're already having a bunch of fun with your money. Maybe, in your business, you make money so effortlessly that you really don't plan your income and outgo.

For the rest of us, though, a budget improves our chances of getting to wherever it is we want to go financially. In fact, I'll stop calling it a budget. The word has such negative connotations. I know — I'll call it a Secret Plan.

Before I walk you through the mechanics of outlining your Secret Plan (your budget), I want to give you a few tips.

Tip

You can do four things to make your Secret Plan more likely to work:

Plan your income and expenses as a family.

With this sort of planning, two heads are invariably better than one. What's more, though I don't really want to get into marriage counseling here, a family's budget — oops, I mean Secret Plan — needs to reflect the priorities and feelings of everyone who has to live within the plan. Don't use a Secret Plan as a way to minimize what your spouse spends on clothing or on long-distance telephone charges talking to relatives in the old country. You need to resolve issues regarding your clothing and long-distance charges before you finalize your Secret Plan.

Include some cushion in your plan.

In other words, don't budget to spend every last dollar. If you plan from the start to spend every dollar you make, you undoubtedly have to fight the mother of all financial battles: paying for unexpected expenses when you don't have any money. (You know the sort of things I mean — car repairs, medical expenses, or that cocktail dress or tuxedo you absolutely must have for a special party.)

Regularly compare your actual income and outgo to your planned income and outgo.

This part of your plan is probably the most important and also the part that Quicken helps you with the most. As long as you use Quicken to record what you receive and spend, you can print reports showing what you planned and what actually occurred.

Make adjustments as necessary.

When you have problems with your Secret Plan — and you will — you'll know that your plan isn't working. You can then make adjustments, for example, by spending a little less calling the old country.

Tip

Because I'm talking about you-know-what, let me touch on a couple of things that really goof up your financial plans: windfalls and monster changes.

Your boss smiles, calls you into his office, and then gives you the good news. You're getting a $5,000 bonus! "It's about time," you think. Outside, of course, you maintain your dignity. You act grateful but not gushy. Then you call your husband.

Here's what happens next. Bob (that's your husband's name) gets excited, congratulates you, and tells you he'll pick up a bottle of wine on the way home to celebrate.

On your drive home, you mull over the possibilities and conclude that you can use the $5,000 as a big down payment for that new family minivan you've been looking at. (With the trade-in and the $5,000, your payments will be a manageable $300 per month.)

On his way home, Bob stops to look at those golf clubs he's been coveting, charges $800 on his credit card, and then, feeling slightly guilty, buys you the $600 set. (Pretend that you're just starting to play golf.)

You may laugh at this scenario, but suppose that it really happened. Furthermore, pretend that you really do buy the minivan. At this point, you spent $6,400 on a van and golf clubs, and you've signed up for what you're guessing will be another $300-per-month payment.

This turn of events doesn't sound all that bad now, does it?

Here's the problem: When you get your check, it's not going to be $5,000. You're probably going to pay roughly $400 in Social Security and Medicare taxes, and maybe around $1,500 in federal and state income taxes. Other money may be taken out, too, for forced savings plans — such as a 401(k) plan — or for charitable giving. After all is said and done, you get maybe half the bonus in cash — say $2,500.

Now you see the problem. You have $2,500 in cold hard cash, but with Bob's help, you've already spent $6,400 and signed up for $300-per-month minivan payments.

In a nutshell, you face two big problems with windfalls:

You never get the entire windfall, yet spending as if you will is quite easy.

Windfalls, by their very nature, tend to get used for big purchases (often as down payments) that ratchet up your living expenses: boats, new houses, cars, etc.

Tip

Regarding windfalls, my advice to you is simple:

Don't spend a windfall until you actually hold the check in your hot little hand. (You're even better off to wait, say, six months. That way, Bob can really think about whether he needs those new golf clubs.)

Don't spend a windfall on something that increases your monthly living expenses without first redoing your budget.

If your income changes radically, planning a budget becomes really hard. Suppose that your income more than doubles. One day you're cruising along making $70,000, and the next day you're suddenly making $170,000. (Congratulations, by the way.) I'll tell you what you'll discover, however, should you find yourself in this position: You'll find that $170,000 a year isn't as much money as you may think. (By the way, this business about monster income changes is true no matter what your income level. Like, if you're cruising along making $500,000 and see your income rocket to $1,000,000, everything I'm saying here still applies.)

Go ahead. Laugh. But for one thing — if your income doubles, your income taxes almost certainly more than quadruple.

One of the great myths about income taxes is that the rich don't pay very much or that they pay the same percentage. But that's not actually true. If you make $70,000 per year and you have an average family, you might pay about $2,000 in federal income taxes. If you make $170,000 a year, though, you pay about $20,000 per year. So, if your salary slightly more than doubles from $70,000 to $170,000 (perhaps your spouse gets a really good job), your income taxes increase almost tenfold, going from $2,000 to $20,000. I don't bring this fact up to get you agitated about whether it's right or fair that you should pay a bunch of any extra income you make in taxes. I bring it up so that you can better plan for any monster income changes you experience.

Another thing — and I know it sounds crazy — is that you'll find it hard to spend an extra $100,000 wisely when you've been making a lot less. And if you start making some big purchases, such as houses and cars and speedboats, you'll not only burn through a great deal of cash, but you'll also ratchet up your monthly living expenses.

Monster income changes that go the other way are even more difficult. If you've been making, say, $170,000 a year and then see your salary drop to a darn respectable $70,000, it's going to hurt, too. And probably more than you think. That old living-expense ratcheting effect comes into play here. Presumably, if you've been making $170,000 a year, you've been spending it — or most of it.

But other reasons contribute — at least initially — to making a monster salary drop very difficult. You've probably chosen friends (nice people, such as the Joneses), clothing stores, and hobbies that are in line with your income.

Another thing about a monster salary drop is sort of subtle. You probably denominate your purchases in amounts related to your income. Make $70,000, and you think in terms of $10 purchases. But make $170,000 a year, and you think in terms of $20 purchases. This observation all makes perfect sense. But if your income drops from $170,000 down to $70,000, you'll probably still find yourself thinking of those old $20 purchases.

So what to do? If you experience a monster income change, redo your Secret Plan. And be particularly careful and thoughtful.

Okay, now you're ready to set up your budget — er, I mean, Secret Plan.

To get to the window in which you enter your budget, click the Planning tab, open the Other Tools menu (by clicking on the Other Tools button), and then choose the Budget command. (Note: In some versions of Quicken, you open the Planning menu and then choose the Budget command.)

Quicken displays the Setup tab in the Budget window. Click the Automatic button if you want Quicken to create a starting budget using any existing financial data. Otherwise, click the Manual button. After you make this choice, click the Create Budget button.

If you indicate that you want to create an automatic budget by, essentially, recycling your old "actual numbers," Quicken displays the Create Budget: Automatic dialog box, in which you can specify which old actual numbers to use (see Figure 3-1). This window allows you to

Choose a date range to scan. Use the From and To boxes to identify the range of dates that span the months or the year you want to use.

Select a budget method. Use the Select Budget Method option buttons and text box to indicate how you want Quicken to budget:

Using average monthly amounts (the default)

Using the exact monthly amounts

Using the exact quarterly amounts

Set your options. Use the Options check boxes to tell Quicken how to handle rounding and one-time, extraordinary transactions. (By default, Quicken rounds budget amounts to the nearest dollar and does not exclude one-time transactions.)

After you describe the automatic budget, click OK.

After you indicate that you want a manual budget (if you're creating a manual budget) or after you describe how you want an automatic budget corrected (if you're creating an automatic budget), Quicken displays the Choose Categories dialog box. When prompted, select the categories and accounts you want to budget and then click OK; Quicken next displays the Income tab in the Budget window, shown in Figure 3-2.

You use the Income tab to enter your budget for income amounts, and use the Expenses tab to budget for expense amounts. If you want to budget savings, you can enter these by using the Savings tab. (Budgeted savings, by the way, are just planned account transfers — money you plan to move, for example, into a savings account.)

Initially, none of the tabs show categories or accounts, which are what you use for your budgeting. To display categories and accounts, follow these three simple steps:

Click the Choose Categories button so that Quicken displays the Choose Categories dialog box. (Or, if you're looking at the Savings tab, click Choose Accounts so that Quicken displays the Choose Accounts dialog box.)

Click the Mark All button.

Click OK.

Categories or accounts appear along the left edge in the window (see Figure 3-3). Any categories with subcategories (if you have these) contain subtotals for the total inflows and for the total outflows.

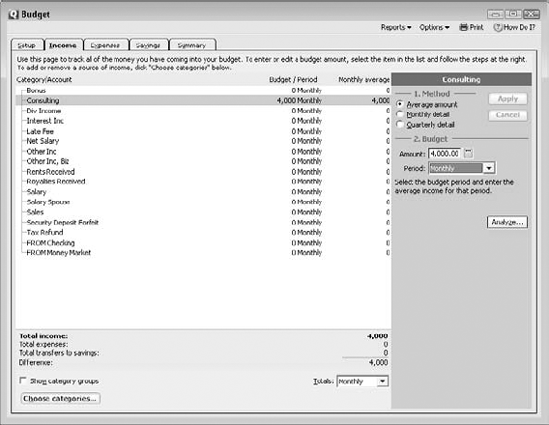

In a pane along the right edge in the Budget window, Quicken displays option buttons and check boxes you use to budget the selected income, expense, or savings amount, which I talk about in the next section.

To budget an income or expense amount, select the category and then enter the budget into the Amount box or boxes. Use the Method option buttons to specify how you want to budget the amount: using an average amount, using different monthly amounts (indicated by marking the Monthly Detail option button), or using different quarterly amounts (indicated by marking the Quarterly Detail option button). Different Amount text boxes appear for different budgeting methods. After you specify your budget amounts, click the Apply button (which is grayed out in Figure 3-4).

As you enter amounts, Quicken updates any subtotals and grand totals that use those amounts.

If you click the Options menu, which appears near the upper-right corner in the Budget window, Quicken displays a menu of several useful commands and switches:

Save Budget: Saves a copy of the current budget.

Restore Budget: Replaces whatever information shows in the Budget window with the information contained in the last saved copy of your budget.

Show Cents: Turns on and off the display of cents. This baby is a real lifesaver if you need to literally watch your pennies.

Separate View: Tells Quicken to separate income, expenses, and savings budgeting information on separate Income, Expenses, and Savings tabs. This is the default view.

Income/Expense View: Tells Quicken to separate income and expense budgeting information on different tabs.

Combined View: Tells Quicken not to separate income, expenses, and savings budgeting information on separate tabs.

Set Up Alerts: Displays the Alerts Center dialog box, which lets you tell Quicken that it should alert you when your actual spending begins to approach a specified limit (see Figure 3-5).

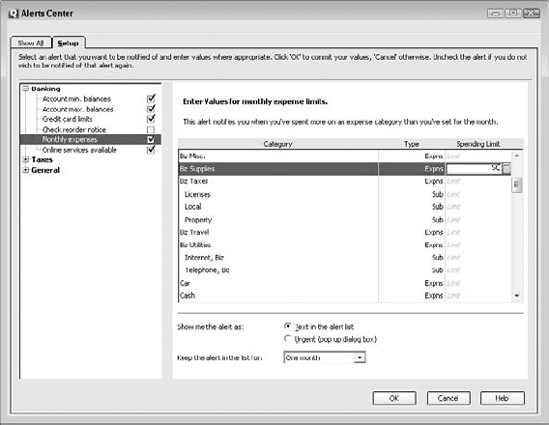

Select the Monthly Expenses check box.

Select the category you want to monitor.

Enter the spending limit into the Spending Limit column.

Go To Category List: Displays the Category List window, which lets you add, edit, and delete income and expense categories.

After you enter your budget, click the Summary tab to see a summarized version of your income and expense budgets and a pie chart of your budget (see Figure 3-6). Use the Summary tab's Top Yearly Budget Items drop-down list box to select the budget data you want to plot in the pie chart.

Tip

If a careful review of your budget shows things have become, well, rather a mess, you can click the Setup tab and then the Start Over button to, er, start over.

After you create your Secret Plan, you don't have to do anything special to save your work. Oh, sure, you can tell Quicken to save your budget by choosing Options

If you want to revert to the previously saved version of the budget, choose Options

I talk more about using the budget in later chapters (Chapter 7, for example). If you want to print a hard copy (computerese for paper) of the budget, choose Reports

You're not going to use the Secret Plan for a while. But don't worry; in Chapter 7, I explain how to print reports, including a report that compares your actual spending with, uh, your budget.