Chapter 17

Myths and Misconceptions of PCI DSS

Information in this chapter:

Myth #3 PCI DSS is Too Onerous

Myth #4 Breaches Prove PCI DSS Irrelevant

Myth #5 PCI is All We Need for Security

Myth #6 PCI DSS is Really Easy

As we previously discussed, Payment Card Industry Data Security Standard (PCI DSS), now updated to version 2.0, has transformed the way many organizations practice information security. While we’ve heard that something will take information security from the wire closet to the boardroom many times before, PCI actually accomplishes this for many organizations—both large and small. While it should be clear to our readers that following all of the PCI DSS guidance will not magically make your organization secure or prevent all incidents, the standard contains many of the common security requirements that are essential for protecting cardholder data and can be useful for other types of sensitive data as well.

As of today, “PCI DSS applies to all entities involved in payment card processing—including merchants, processors, acquirers, issuers, and service providers, as well as all other entities that store, process or transmit cardholder data” The aforementioned quote from the PCI DSS document reminds us that the applicability of PCI DSS is in fact nearly universal.

In this chapter, we look at common PCI DSS myths and misconceptions. We will also dispel those myths and provide a few useful tips on approaching PCI DSS.

Let’s get to the myths.

Myth #1 PCI Doesn’t Apply to Me

Myth #1 is pretty simple, but, sadly, very common: “PCI DSS just doesn’t apply to us, because we are small, or we are a University, or we don’t do e-commerce, or we outsource “everything,” or we don’t store cards, or we are not a permanent entity, etc.” More recent versions include “we use tokenization,” “we use EMV” (yeah right!—most of our US-based readers would say) or “we encrypt end to end.” “We outsource everything and thus have no PCI responsibilities” may in fact occasionally be true, but in most cases that is just that—a myth.

This myth takes over an organization and makes it oblivious to PCI DSS requirements and, almost always, to information risks and security requirements in general.

Here is one recent example: a campaign of Norm Coleman for U.S. Senate in 2008 has announced [1] that “If you donated online to Norm Coleman’s 2008 Senate campaign, or his recount efforts, you should call and cancel the credit card you used to make that donation.” The reason? Attackers compromised the site and stole both the credit cards numbers of donors and other private information. From the circumstances disclosed in the media, one can deduce that the information was stored in clear violation of PCI DSS rules.

Another example is more blatant: health care providers have been so busy with HIPAA that many became oblivious of PCI DSS arrival. A recent paper in “SC Magazine” called “PCI-DSS: Not on health care provider’s radar” [2] (notice the incorrectly hyphened “PCI–DSS” in the title…) reports:

However, since Medicare reimbursement is not at risk with PCI-DSS compliancy, it has been virtually ignored. It doesn’t help that major health care publications are openly misinterpreting the PCI-DSS standards for health care providers, with statements such as: “[Providers] do not have to worry about compliance with PCI standards… they aren’t storing any card numbers”[2].

A Perfect Example of Myth #1 at Work!

PCI DSS is not about storing cardholder data; it is about those who accept payment cards or capture, store, transmit, or process such card data. Want to guess whether most health care providers accept cards? Didn’t think so—the number is probably close to 100.00 percent, as most US readers can attest from their experiences. Indeed, the paper mentioned earlier [2] confirms: “In 2009, virtually all health care providers take credit cards—and virtually none of them are PCI compliant.” Now in 2012, the situation has barely changed. While HIPAA enforcement seems to have increased across Health Care providers, PCI DSS still remains “a big black hole” for many of them. Additionally, most such Health Care providers do not run a compliance program that can accommodate the needs of multiple regulations. They deal solely with HIPAA and adjusting the controls and practices to another regulation becomes fairly hard for them.

NOTE

Question: If I only accept cards from June to August each year and I only use a dial-up terminal, I am “safe from PCI,” right?

Answer: Wrong. Even though your scope of PCI DSS validation is very, very small, you are definitely subject to its rules because you—surprise!—accept payment cards. PCI DSS applies to those who “accept, capture, store, transmit, or process credit and debit card data.” If you do, it applies to you—end of the story. No myths can change that.

Interestingly enough, one of the data elements required to be protected under HIPAA is customer payment information, which often means “credit card data.” This means that HIPAA technically preceded PCI DSS when it comes to cardholder data security! However, this doesn’t stop health care providers from ignoring both regulations in one fell swoop.

NOTE

Question: If I use external tokenization and cardholder information never enters my environment, am I “PCI OK?”

Answer: Possibly! If your merchant agreement does not mention PCI DSS, none of your employees can see the data, and it is not handled anywhere on your systems, your PCI responsibility might be nonexistent.

The reality, as we mentioned earlier is pretty simple: PCI DSS does apply to your organization if you accept payment cards or capture, store, process, or transmit any sensitive payment card data (such as PAN) with no exceptions. If the data touches your systems, they are in scope for PCI DSS assessment and, obviously, your organization has PCI DSS responsibilities. Whether you cure, educate, rent, offer, sell, or provide services doesn’t matter—what matters is whether you charge! If you do, PCI DSS does apply. Hopefully, if you picked up this book while being unsure whether PCI DSS applies to your organization, reading this book convinced you that becoming compliant and secure is indeed in your future if you deal with payment cards.

Admittedly, different things need to happen at your organization if you have absolutely no electronic processing or storage of digital cardholder data compared to having an Internet-connected payment application system. The scope of compliance validation will be much more limited in the former case and so your PCI project will be much, much simpler. For example, if a small merchant “does not store, process, or transmit any cardholder data on merchant premises but relies entirely on third-party service providers to handle these functions” he is only responsible for validating a small part of PCI DSS. Specifically, he would be responsible for the parts of “Requirement 9: Restrict physical access to cardholder data” as well as a small part of “Requirement 12: Maintain a policy that addresses information security for employees and contractors” via a self-assessment questionnaire (SAQ) Type A (13 questions overall).

Let’s explore this example in more detail. As we covered in Chapter 3, “Why Is PCI Here?,” payment card brands such as Visa and MasterCard label merchants that process fewer than 20,000 e-commerce transactions a year or fewer than 1 million card present transactions as “Level 4.” As you now know, such merchants currently are recommended to validate their PCI compliance using a SAQ.

In addition, as described in PCI DSS standards, if a merchant matches the criteria below, he is considered to be “validation type 1” and needs to fill the SAQ Type A (the shortest). The criteria are as follows:

• Merchant accepts ONLY card-not-present (i.e. eCommerce) transactions.

• Merchant does not store, process, or transmit any cardholder data on merchant premises but relies entirely on third-party service providers to handle these functions.

• The third-party service providers handling storage, processing, or transmission of cardholder data is confirmed to be PCI DSS compliant.

• Merchant retains only paper reports or receipts with cardholder data, and such documents are not received electronically.

• Merchant does not store any cardholder data in electronic format.

Explained simply, the aforementioned criteria describe a situation where a merchant accepts credit cards as payment, but does not have any electronic storage, processing, or transmission of cardholder data. Think about it for a moment! PCI DSS doesn’t apply if you do not store, process, or transmit any card data on your premises (or your systems located off your premises such as outsourced, hosted or shared cloud systems) at all! This example highlights that fact that card acceptance is sufficient to make the merchant to fall under PCI.

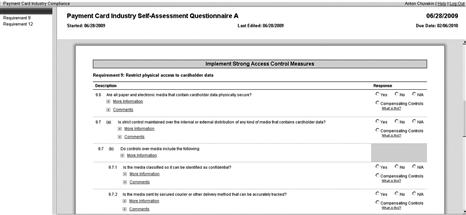

The exact scope of its validation as covered by SAQ Type A is shown in Figure 17.1.

Figure 17.1 Self-Assessment Questionnaire (SAQ), Type A

The merchant needs to validate part of Requirement 9 and part of Requirement 12. Specifically, sections of Requirement 9 cover the storage of physical media (printouts, receipts, etc.) that has cardholder data. For example, quoting from PCI DSS SAQ Type A [3]:

• 9.6 Are all paper and electronic media that contain cardholder data physically secure?

• 9.7 Is strict control maintained over the internal or external distribution of any kind of media that contains cardholder data?

• 9.8 Are processes and procedures in place to ensure management approval is obtained prior to moving any and all media containing cardholder data from a secured area (especially when media is distributed to individuals)?

• 9.9 Is strict control maintained over the storage and accessibility of media that contains cardholder data?

• 9.10 Is media containing cardholder data destroyed when it is no longer needed for business or legal reasons?

All of the above deal with the physical media such as printouts that may contain card data. The merchant is also subject to one section of Requirement 12, which covers the merchant’s relationship with service providers that actually handle data (again, see PCI DSS SAQ Type A [3]):

• 12.8 If cardholder data is shared with service providers, are policies and procedures maintained and implemented to manage service providers, and do the policies and procedures include the following?

• 12.8.1 A list of service providers is maintained.

• 12.8.2 A written agreement is maintained that includes an acknowledgement that the service providers are responsible for the security of cardholder data the service providers possess.

• 12.8.3 There is an established process for engaging service providers, including proper due diligence prior to engagement.

• 12.8.4 A program is maintained to monitor service providers’ PCI DSS compliance status [3].

All of the above deal with the responsibilities of the third party that handles processing, storage, and transmission of data.

Overall, the choice is pretty simple: either you comprehend PCI DSS now and start working on security and PCI requirements or your acquirer will make it clear to you at some point when you won’t have much room to maneuver.

A subtle point brought to life by an increasing use of EMV Technologies needs to be clarified: payment card brands may relax some of the PCI DSS validation requirements if the merchant uses new (and presumably more secure) payment methods, however merchants will still be required to maintain PCI compliance at all times.

Myth #2 PCI is Confusing and Ambiguous

Myth #2 is just as pervasive: PCI is confusing and not specific. At first, it might seem like it is true: after all, this whole book is written about it! However, this is actually a myth, despite the fact that people who didn’t invest enough time into learning about PCI compliance might be more than a little confused about it.

In addition, this myth seems to be purposefully propagated by some people to “muddy the waters” and thus to make PCI DSS seem impossible to achieve and thus not worthy of even trying. Said people frequently have something to sell to merchants, something that presumably simplifies PCI compliance to nearly nothing. For example, when confronted with the need to change their business process to avoid storing the card data (simpler task as you now know) or with the need to secure card data (a harder task compared to not storing it), many smaller organizations go into the “ostrich in the sand” mode and try to pretend the problem is unclear, unsolvable, or confusing, instead of tacking it head on.

Namely, those under its influence often proclaim things such as

• “PCI just confuses us—we can’t do it.”

• “We don’t know what to do, who to ask, what exactly to change.”

• “We don’t know whether we are compliant and hiring somebody to tell us is expensive.”

• “PCI is confusing; until you give us something better, we will not do anything to protect the data.”

• Sometimes it also devolves into the following:

• “Just give us a simple task list and we will do it. Promise!”

The reality is quite different: PCI DSS documents explain both what to do and then how to validate it. Apart from people who propagate this myth, you just need to take the time to understand the “why” (the spirit of the standard and cardholder data security), the “what” (the list of PCI DSS requirements), and “how” (common approaches and practices related to PCI).

PCI is actually much easier to understand than most other existing security and risk management frameworks and regulatory guidance in spite of its length and breadth. Looking at some of the advanced information risk management documents (such as ISO27005 “Information security risk management” or NIST 800-30 “Risk Management Guide for Information Technology Systems”), with their hundreds of pages of sometimes esoteric guidance, is a refreshing reminder that PCI DSS is, in fact, pretty simple and straightforward.

Most of the gray area talk you hear about PCI DSS typically comes from companies that are trying to find creative ways not to do anything to their business or their technology or take risky shortcuts with other peoples precious data. Most of these can be solved by removing the emotion from the situation, and logically laying out the costs and risk associated with making a change versus staying in violation of the rules until caught and punished.

Let’s compare what PCI says and what some other guidance documents say:

PCI DSS in Requirement 5 states:

“5.1 Deploy anti-virus software on all systems commonly affected by malicious software (particularly personal computers and servers).

5.1.1 Ensure that all anti-virus programs are capable of detecting, removing, and protecting against all known types of malicious software.

5.2 Ensure that all anti-virus mechanisms are current, actively running, and capable of generating audit logs.”

ISO27002 states [4]: “Precautions are required to prevent and detect the introduction of malicious software, such as computer viruses, network worms, Trojan horses, and logic bombs.”

NIST 800-53 document “Recommended Security Controls for Federal Information Systems,” itself a 174 page tome, states [5] “The information system implements malicious code protection.” Additional NIST documents, such as 800-83 “Guide to Malware Incident Prevention and Handling: Recommendations of the National Institute of Standards and Technology,” do provide useful additional guidance on malware protection, but that is another 101 pages to read (!).

The aforementioned example demonstrates that even though PCI DSS needs some focused attention from the merchants, it is not confusing, but more specific than other industry security guidance. While the original PCI creators had BS7799/ISO17799 in mind, their standard ended up being much simpler than its ISO-created inspiration, but lost of few things that people consider important (e.g. all the security project management requirements).

Still, there are definitely areas in PCI security guidance that can be made more specific. For example, when PCI DSS document was updated from version 1.2.1 to version 2.0, the updated document contained several dozen clarifications and explanations, brought up during the review phase (see the PCI DSS v2 Summary of Changes document available on the PCI Council website for details).

As PCI DSS grows up, all the remaining ambiguity should be reduced through the efforts of participating organizations and by adopting to the needs and requirement of the merchants as well as the evolution of the threats.

Finally, security cannot and will not ever be reduced to a simple checklist. Even today some criticize PCI DSS for being a manifestation of “checklist security” which does not account for individual organization’s risk profile. PCI guidance is as close to a checklist as we can get without actually leading to increased, not reduced, risk.

Myth #3 PCI DSS is Too Onerous

The next myth, Myth #3 is closely related to the above: PCI DSS is just too hard. Sometimes, it becomes too expensive, too complicated, too burdensome, just too much for a small business, about too many technologies or even simply “unreasonable” and “too much security.”

Sometimes this myth is close to reality, but not for reasons people think. “PCI is too hard” becomes true if merchants are treating their card data in a particularly negligent way. Think giant text files with unencrypted PANs on a website or payment terminals allowing remote access open with no password!

For example, we introduced a concept of “flat network” in Chapter 4, “Building and Maintaining a Secure Network.” To remind, it means a network that is not segmented by firewalls or filtering routers into zones or segments. Such network design means that if a single system handles card data, the whole network is in-scope for PCI DSS. Yes, that means all servers, all desktops, all network devices and everything else connected to it becomes subject to all PCI DSS requirements! Such situation, even if relatively rare nowadays, has been known to happen at large and medium merchants and thus make PCI DSS compliance very hard as the scope grows from a single system or a handful of systems to hundreds or thousands of systems. Every such system will need to be scanned for vulnerabilities, have its security configuration verified (these include the password length and complexity, use of encryption, etc.), have logging enabled and monitored, etc. In this case, “PCI is hard” will not be a myth, but PCI DSS guidance will not be the reason to blame: the operators of such a network will be.

WARNING

If you think PCI is too onerous, please stop and consider this: do you think that wearing a seat belt while driving is too onerous? How about brushing your teeth every day? How about actually operating your business?

Tasks unlike ones you have been doing are often first seen as onerous. When you were three years old, it is very likely that brushing your teeth was seen as a huge task—and an annoying one as well.

So, if you happen to think PCI and data security is too onerous, you simply need to start paying attention to it—and it will stop being onerous after you get good at it.

Similarly, if a simple change in a business process will lead to removal of stored cardholder data, continuing to operate without such change and engaging in attempts to protect such data, rather than remove it will be shortsighted and lead to PCI being indeed “too hard.” As we say in the book “delete the data—and then secure what you absolutely CANNOT delete.”

On the other hand, the reality is that PCI DSS exemplifies common, baseline security practices, which every organization needs to take into account when planning their IT and business operations. PCI only seems hard if you were not doing anything for the security of your data before; hopefully this book will help to make PCI DSS easier and actually useful for your organization. PCI might not be easy for a large, distributed organization, but it is clearly much easier than creating and running a well-managed security program based on a good understanding of your risk across all types of data.

As observed by one of the authors, people who complain about PCI DSS being too hard and emitting loud calls for “Make PCI Easier!!!” are often split into two camps:

• “Please, please make PCI easier by letting us skip the requirements; or, better, they just let us ‘JUST SAY YES ON THE SAQ!’” camp. We can call them “laggards” or “losers” for extra hilarity.

• “We know that our security program makes us PCI compliant; please make it easier for us to prove it!” camp. We can call them “leaders” or “snobs,” if you wish.

As you can guess, the organizations that fit into the first camp and those that fit into the second camp are very different. While some in the first will miss the joke in ScanlessPCI (a joke site set up by a band of security experts to poke fun at some of the organizations that ignore security), the second camp is often concerned with relating their “risk-focused” approach to PCI’s mostly “control-focused” approach.

It is possible to make PCI easier even for those in the first camp, those people who just “want it gone:” make doing the right thing easier for them (while making doing the wrong thing harder): not storing card data, outsourcing processing, using tokenization, etc. For example, a lot of merchants store card data because they are under the mistaken impression that such data falls under the “Financial Rule of Thumb” of storing financial records for seven years. Such actions are making PCI DSS much more difficult or, in the case of storing CVV2 or other prohibited data, impossible. Even for chargebacks, which obviously don’t go back seven years, storing the PAN and other sensitive data is just not needed today.

On the other hand, while in the second camp, one sometimes hears things like “we have a good security program and we manage our risk well!—why should we spend time on that PCI thing? We are probably in good shape already!” These organizations are likely doing a good job with security and want to use all that to quickly “prove compliance.” In this case, making PCI easier will include making it easier to assess, validate, and prove compliance and overall make the whole “assessment experience” a little less painful. Still, it will not be harder than building that risk management program that they already have built.

So, as we mentioned, you can make PCI harder for yourself by making the wrong decisions. For example, developing your own web application complete with credit card processing will increase your PCI scope likely beyond your ability to handle. On the opposite, using a third-party checkout service will do just the opposite and make PCI and data security easier. Review the previous section on Myth #2 and notice that not touching the cards will make your PCI experience so much easier—without going into the application security esoterics such as OWASP guides, SQL injection, cross-site request forgery, and other things better be left to those who enjoy writing books about PCI DSS compliance.

Myth #4 Breaches Prove PCI DSS Irrelevant

Myth #4 seems mostly driven by the media: it claims that “Recent card data breaches prove PCI irrelevant.” We suspect it stems from the fact that reporting failures and other “bad stuff” typically draws more listeners, readers, and watchers compared to reporting successes and thus attracts more media attention. Note how much press time the catastrophes, corrupt politicians, weather anomalies, and various technology failures get; and the bigger the better!

However, it encourages some organizations to develop a negative, destructive mindset and thus to do a bad job with PCI DSS and data security. As a result, they would suffer from a devastating data breach, which is more than a little ironic because they were trying to “focus on the breaches, not on compliance.” Breaches of organizations that validated their PCI compliance should get more people to focus on security as well as on maintaining compliant and secure state, not the other way around. If a similar organization to you was breached, you now need to do a better job to not end up like them.

It is worthwhile to mention that QSAs carry part of the blame as well: cases where blatant security mistakes, severe configuration weaknesses, forbidden data storage, and even compromised systems were missed by the “easy grader” assessor who focused much more on writing a report quickly enough to make his margin and not enough on actually collecting the data for the report. In selecting a QSA—your “mandatory security consultant”—it helps a lot to focus on value delivered to an organization and not simply on price. Try to squeeze every penny of valuable security advice during that face time in the assessment process. In some cases, you can “get your own QSA”—have somebody from your organization certify as “ISA”—a new Council certification for internal security assessors.

WARNING

It is often assumed by security professionals that people outside of security industry will not take advice to protect data from mainstream media. Sadly, people often do and sometimes even IT people and IT managers do so. In light of this, the author team would make this into an explicit warning.

Dear reader! Newspapers, magazines, and even IT “trader rags” and information security press are NOT a reliable source of security guidance, whether for technology or for policy security guidance. Read them to know the news, but go to experts for detailed guidance on how to secure your data.

Today the media is much obsessed about “cyber war” with a lot of truly idiotic advice being passed around this topic. If you made it to RSA Conference 2012, you probably noticed that the conversations had changed from basic compliance or anti-virus to advanced threats and advanced security. The discussions are starting to happen, which means the money and behavior will follow in time.

Again, the reality is exactly the opposite: data breaches remind us that basic security mandated by PCI DSS is necessary but not sufficient. You have to start from the basics before you can advance in your security education. As you learn more about security, you usually come to realize that nothing guarantees breach free operation. Let’s pick a few examples from PCI DSS and check whether they are a good idea as well as whether they guarantee the absence of breaches. Table 17.1 shows excerpts from PCI DSS as well as their relation to data protection and data breach prevention.

Table 17.1 PCI DSS Requirements for Data Security

Table 17.1 allows us to conclude that PCI DSS controls are necessary to prevent card data loss and theft, but few of them can be considered sufficient.

NOTE

Recent breaches remind us that PCI DSS is insufficient—and it is. Only ongoing and adaptable risk management program with quality strategy and execution can be considered an end-state, but it is an ongoing end state that never really “ends.”

Please remember—you are never “done” with information security!

Finally, one of the authors’ colleagues likes to say that every breach proves that PCI DSS is even more necessary. PCI DSS is a great start for security, but a really bad finish, as we discover in the next myth.

Myth #5 PCI is All We Need For Security

Myth #5 is probably the scariest one of all: PCI is all we ever need to do for security. People in the grasp of this myth would proclaim things that will shock every security professional; for example:

• “We have handled PCI—we are secure now.”

• “We worked hard and we passed an ‘assessment’; now we are secure!”

• “Our QSA told us we are secure.”

• Or even, in its more extreme form,

• “I filed my PCI compliance documents; now I am compliant and secure for a year.” (insanity, you say? Such views are heard even now in 2012 when these words are being written).

The above maxims remind the authors of how many executives in the 1990s proudly proclaimed, “I have a firewall, I’m secure” and then refused to pay attention to “overblown” security concerns. At the very least, a firewall might block some suspicious connections, while report on compliance paperwork on its own does not provide any protection—and in fact only introduces additional risk of fire.

Recently, one of the authors was shocked to read the following on what purports to be a security blog post that talked about the now-infamous Heartland Payment Systems data breach: “Is complying to PCI not enough anymore?” It seems that even security professionals can somehow fall victim to this myth. Another common manifestation is an organization that doesn’t pay much, if any, attention to data security is being suddenly jabbed by PCI DSS requirements. More often than not senior management will “make” IT do “that PCI security thing.”

It often leads organizations to focus on “pleasing the assessor” and then forgetting that a happy assessor does not mean that your organization is protected from information security risks.

Moreover, this myth is actually wrong on multiple levels! First, validating PCI DSS via an assessment or self-assessment does not mean that you are done with PCI DSS as you now need to maintain compliance—something that needs to happen daily (!). Also, it certainly does not mean that you are done with security. In addition, it also doesn’t mean that you are secure, just that you validated PCI compliance and hopefully made an honest step towards reducing your risk; now you need to maintain your compliant status and data security! As a reminder, while your QSA validates your compliance and is responsible for the Report on Compliance, merchant is solely responsible for maintaining compliance status between assessments.

Again:

Validating PCI compliance via on-site assessment or self-assessment does NOT mean that:

• You are “done with PCI” and now can ignore it.

• You are “done with security” and now cannot do anything to protect your data.

The reality is again different: PCI just mandates minimum security, not maximum or optimal. And PCI validation attests that such minimum security was present at the time of assessment (an astute reader will make a note that the word “present” needs to be replaced with “shown to or identified by a QSA”, but we will not succumb to such cynical urges).

PCI is basic security; it is a necessary baseline, a low watermark, which was never meant to be the “end state” of guaranteed secure data. No external guidance document, even well-written and followed with utmost diligence, can guarantee that—just as excellent police work can never guarantee “crime-free” environment. People don’t expect police, prosecutors, and laws to “end crime”—so why do some people think that QSAs, approved scanning vendors (ASVs), security vendors, card brands, and PCI DSS document will end cybercrime? This is a useful thought to keep in your head as you are finishing that PCI validation.

WARNING

If you hear somebody lament the fact that he was PCI compliant and then got breached and had all card data stolen, please pause before bashing PCI DSS for this unfortunate course of events. It is hard to say for sure without having the details, but in most case the authors have seen in the field, such breach was the fault of the merchant and not of PCI DSS, PCI Council, or any other regulatory entity. In fact, even when they say “they were compliant,” they rarely mention WHEN in fact they think they were compliant.

Finally, PCI is about cardholder data security, not the rest of your private or regulated information, not your organization intellectual property, not identity information such as SSNs, not the availability or fewer Internet-facing services or employee productivity. It only covers confidentiality, and not availability of cardholder data. These quick examples show that there is a lot more to data security than PCI DSS, and there are clear areas where PCI does not focus—for a good reason.

Specifically, perfect PCI DSS compliance and validation will not:

• Make your “out of scope,” non-cardholder data such as SSNs secure.

• Make your trade secrets and other intellectual property secure.

• Make your “out of scope” systems and networks secure.

• Make your card data, other data and information systems more reliably available.

• Make you automatically compliant with any other international, national, state or industry regulation.

• Make employees use Internet productively.

• It might only minimally affect:

• Security of your other data—the implemented network safeguard might help and so might the change of organization culture due to security.

Thus, you are certainly not “done with security” even if you maintain ongoing PCI compliance. For example, one of notable PCI QSAs likes to say that you likely need “PCI+” or even “PCI++” to deal with risks to your systems and data today.

Myth #6 PCI DSS is Really Easy

The next myth, #6, is the opposite of myth #4: PCI is easy: we just have to “say Yes” on a questionnaire and “get scanned.” As merchants become more familiar with PCI DSS, some start to feel that PCI is not that scary—it is about getting a mysterious “scan” from an entity called “an ASV,” then answering “Yes” to a bunch of lengthy questions and paying an “outrageous” fee of $8.95 with their monthly merchant account bill. Given that their view of PCI DSS as “annoying but tolerable” such merchants have fully succumbed to this myth. Their misconceptions are expressed in claims that PCI is about getting a scan and answering some questions or that it is a paperwork exercise or even that it can be bought for $8.95 monthly compliance fee (or, occasionally, a $100/year noncompliance fee)…

For merchants and service providers that don’t have to go through an on-site QSA assessment, PCI DSS compliance is indeed validated via external vulnerability scanning by an ASV and via filing an SAQ consisting of 13-220+ questions. However, it is worthwhile to mention that there is some work involved before many of the merchants can truthfully (!) answer “yes” to those questions and would be able to prove this, if requested by their acquiring bank.

WARNING

PCI DSS is not easy. It is definitely not easy for a large company that needs to collect all the evidence for compliance validation from different systems and then maintain such evidence between assessments. However, these activities, if not easy, are actually useful for security and overall manageability in that company.

PCI DSS is pretty easy if all card processing is outsourced to a reliable and secure processing provider who does not allow you to touch the data. Some external tokenization solutions offer similar benefits for simplifying PCI compliance.

Here is an example: Requirement 1.1.2 mandates a “current network diagram with all connections to cardholder data, including any wireless networks.” We show a few examples of such diagrams in Chapter 4, “Building and Maintaining a Secure Network.” Answering “Yes” to this question entails:

1. Having a diagram available,

2. Making sure that the diagram is indeed current and all network connections are reflected on it,

3. Knowing the locations of cardholder data (itself a massive project at many organizations!),

4. Verify that there are no other locations of cardholder data (PCI DSS 2.0 places additional emphasis on such discovery efforts),

5. Confirming that it shows all connections to all locations of cardholder data,

6. Knowing which wireless networks are deployed and where, including those deployed by divisions and other business units (and possibly rogue as well),

7. Maps out connections from networks and systems that can manage systems housing cardholder data.

Clearly, this takes more than reading a book (we suggest “PCI Compliance”, 3rd edition!) or clicking “Y” on a computer. This is what turns minutes into months and simple tasks into projects.

A slightly simplified reality is that a typical small merchant who processes cards online would at least need to do the following:

a. Get a network vulnerability scan of the external systems from an ASV, resolve the vulnerabilities found, and then rescan to verify.

b. Do the things that the SAQ questions refer to and maintain evidence that they were performed.

c. Answer the questions affirmatively (providing details were needed) and retain proof of that validation.

d. Keep up with periodic maintenance and other requirements until you no longer wish to accept credit cards, i.e. maintain compliance.

In other words, achieve PCI DSS validation and then maintain PCI DSS compliance for as long as you plan to accept cards. You can only answer “yes” if you have grounds for saying “yes” on the questionnaire and can prove it, even with no assessors or acquiring banks looking over your shoulder.

NOTE

Question: My management told me to ignore everything, including security hardening of my servers and even response to an ongoing hacking incident and go focus on “pleasing the QSA.” What should I do?

Answer: Apart from changing a job, you mean? Sorry, bad joke. What you need to do is try to tie all the key security things you know you need to do (we are assuming here that you actually know what those things are) and tie them to PCI DSS requirements. Under such PCI umbrella, the management should be more accepting of what you actually need to do for security. Result: achieve both security and PCI DSS compliance. Some people might object to such tactics as “gray area” or “unethical,” but there is nothing unethical in use in security regulation—PCI DSS in this case—to improve security.

Specifically, even on the vulnerability scanning side, the typical perception that “get a PCI scan and you are done” is essentially misguided. PCI DSS requires you to run both internal and external network vulnerability scans at least quarterly (in reality, twice a quarter since you’d need to fix the vulnerabilities and then rescan to confirm it!) as well as after every major network change. Internal scans can be run by in-house security staff, while the external scans must be performed by an ASV, and these are then used to satisfy your PCI Validation Requirements and are submitted to your acquiring bank. By default, all Internet-facing IP addresses are “in-scope.” For larger businesses, companies can work with their QSA and ASV to reduce the scope of that external footprint if certain controls are in place and enforced.

Furthermore, the specific requirements placed on the depth of such scans. There is also a requirement to remediate all vulnerabilities, scored higher than 4.0 with CVSS for external scans or all “High” vulnerabilities as defined in PCI DSS Requirement 6.2 are resolved for internal scans. In essence, this is not “scan and done,” but “scan-fix-maintain” lifecycle.

NOTE

It is a common misconception that the PCI DSS scanning validation requirement applies only to systems that process card data. If you are subject to PCI DSS scanning requirements (which happens when you have systems connected to the Internet), all of your externally visible systems are subject to security scanning (by an ASV) as well as those systems involved in processing, storing, and transmitting the data and the ones “directly connected” to them (by an internal team or a consultant). Many organizations have a lot of challenges scanning systems with cardholder data especially when such systems up virtual or located at other environments, or not under full control of the merchant.

Myth #7 My Tool is PCI Compliant Thus I Am Compliant

Myth #7 is in believing that your network, application, tool is PCI compliant with the resulting conclusion that this achieves compliance for your organization. This myth manifests itself in statements from merchants such as “My payment application vendor said his tool is “PCI compliant”” or “They put together a network and it is PCI compliant.” However, no tool can make you compliant. In fact, people often confuse PA-DSS certified application with PCI DSS compliant organization, which literally have little to do with each other, even though both come from PCI Council. PCI DSS 2.0 states that “Use of a PA-DSS compliant application by itself does not make an entity PCI DSS compliant, since that application must be implemented into a PCI DSS compliant environment and according to the PA-DSS Implementation Guide provided by the payment application vendor (per PA-DSS Requirement 13.1).”

Just to remind you, PCI DSS is a “multifaceted security standard that includes requirements for security management, policies, procedures, network architecture, software design, and other critical protective measures. This comprehensive standard is intended to help organizations proactively protect customer account data.” (PCI Council website [6]) On the other hand, PA-DSS is “to help software vendors and others develop secure payment applications that do not store prohibited data, such as full magnetic stripe, CVV2 or PIN data, and ensure their payment applications support compliance with the PCI DSS.” (PCI Council Web site [6]) The former applies to an entire organization while the latter applies to a payment application only.

TOOLS

PA-DSS list contains all of the validated payment applications that can be used by merchants. It is not uncommon for an acquirer to refuse to onboard merchants that use applications which are not on the list or even the versions of the applications which are not on the list.

However, using this list will get you a list of tools, but you still must deploy the tools in the manner prescribed by the DSS document as well as maintain them as required by PCI DSS.

In reality, there is no such thing as “PCI compliant tool, application, configuration or network,” regardless of what a vendor’s marketing department says. PCI DSS compliance applies to organizations only. You can struggle toward, achieve, and validate PCI DSS compliance only as an organization. Using PA-DSS compliant, application is only a small piece of the entire puzzle.

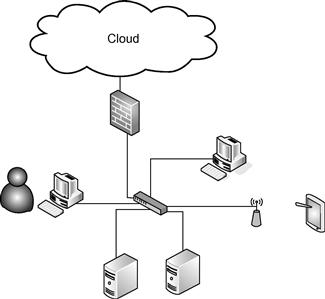

Despite that, the authors have been asked multiple times by various industry colleagues about certain pieces of IT infrastructure being PCI compliant. Here is one recent example—Figure 17.2.

Figure 17.2 Is This Network PCI Compliant?

Figure 17.2 was shown to one of the authors with the question of “Is this PCI compliant?” Even though some people will start debating this with crafty arguments for “yes” and “no,” the immediate (and correct!) response was “no way to tell.” There are simply too many things that can make or break PCI DSS compliant status of an organization. For example:

• What are the password policies on these servers? Are the compliant with the whole host of requirements 8.5, such as “8.5.5 Remove/disable inactive user accounts at least every 90 days” or “8.5.9 Change user passwords at least every 90 days.”

• Is there logging performed? Is such logging as good as requirement 10.2 mandates. Namely, is logging sufficient to reconstruct the prescribed events.

• Is vulnerability scanning done? Are scans “run [..] at least quarterly and after any significant change in the network?” Are discovered vulnerabilities remediated?

• Is file-integrity monitoring software deployed to “alert personnel to unauthorized modification of critical system files” (requirement 11.5 in PCI DSS)?

• Moreover, are the security policies “established, published, maintained, and disseminated” (Requirement 12.1 in PCI DSS)? Or is there “a formal security awareness program to make all employees aware of the importance of cardholder data security” prescribed by PCI DSS Requirement 12.6?

WARNING

Security policy is pretty darn important for your PCI DSS compliance program (since it is mandated in Requirement 12 which we cover in Chapter 6, “Protecting Cardholder Data”) as well as for data security. However, here is the dirty truth about policy: it does nada, none, zero to secure the data unless it is actually followed in reality and enforced by security technology and process.

Furthermore, the authors hypothesize that this is exactly why policy development is listed in Phase 6 of “PCI DSS Prioritized Approach” [7]. Security professionals say “policy comes first,” but policy needs to be actually implemented have ANY impact on data security and risk.

The above lists only a few of the reasons for why the above pictured environment might or might not be part of a PCI DSS compliant organization.

Thus, “no way to tell” is the only genuine response. There is no way to judge PCI compliance on just isolated servers, pictured on a diagram.

NOTE

Your networks, applications, or tools are not PCI compliant, even though the payment application can be PA-DSS compliant. PCI DSS compliance, however, applies to the entire organization. PCI DSS also does not have any “partial compliance”—there is only “compliant with all relevant requirements” (was clear evidence and league are so their relevance) or “not compliant.” In some cases, payment brands or acquiring banks may allow for you to complete certain phases of the Prioritized Approach, but those are either associated with technology advancements and implementations or special one-off cases.

Answering the question is only possible “in bulk,” considering all the conditions, criteria, and requirements, and the only way to achieve this is to follow your own path through the PCI DSS requirements. The “PCI DSS Prioritized Approach” lists the recommended, risk-derived order for following the requirements that can be helpful on your journey. The document can be found on the PCI Council Web site [6]. Figure 17.3 shows an example from the PCI Council document called “Prioritized Approach to PCI” [7].

Figure 17.3 PCI DSS Prioritized Approach

As we mentioned, PCI DSS combines technology, process, policy, awareness, and practices as well. For example, Requirement 12 covers security policy, incident response practices, security awareness, and other nontechnical safeguards and controls. Don’t focus on isolated pieces; rather, build the big picture, track a path, and move ahead towards PCI DCC compliance and data security.

Myth #8 PCI is Toothless

Myth #8 is simply a view that “PCI DSS Is Toothless.” This myth shows a completely wrong worldview of PCI DSS and security; a dangerous delusion that is also wrong on several levels.

First, it embodies the view that data security measures are only deployed due to regulatory pressure, such as from PCI DSS, and not from genuine need to reduce risk to information and transactions. This myth is often used to justify not doing anything about data security with merchants believing—erroneously that if even they are breached and then also found noncompliant, their business will not suffer. Similarly, people read the popular media and then ignorantly claim that companies are breached and then continue being profitable so they should not care about PCI and security. Just ask that question of a recently fired CSO and see what he says about “no impact on an organization.” Finally, they claim that compliance costs more than noncompliance without doing any research into this subject, which then leads to faulty decision making.

Honestly, such views are often held by merchants who are used to just accepting the risk of card data theft—until their businesses are no more (in some cases). In fact, in the pre-PCI era it made good sense to accept such risk because it was not the merchant’s loss, but the issuing banks that would need to reissue the stolen cards. Here is a commonly utilized conceptual risk formula1:

![]()

If we apply it to this situation, we’d realize that before PCI the merchant’s risk was indeed exactly 0 and absolutely didn’t depend on threats that the merchant faced, as well as vulnerabilities his environment had. PCI DSS transferred the risk back to where it should belong—wherever the data is lost or stolen. Thus, one can say that PCI DSS created the risk for merchants to motivate them to protect the data as well as educate them about Data Security.

Second, in addition to being a wrong mindset, it is also simply wrong. PCI DSS noncompliance and resulting loss of cardholder data packs a lot of bite which includes fines, possible lawsuits, mandatory breach disclosure costs, investigation costs, possible card processing rate increases, cost of additional security measures, and cost of victim credit monitoring. It is really not only about the fines; among the above “teeth” the following were actually frequently observed:

• Breach disclosure costs: Although it is not the direct consequence of PCI DSS noncompliance, these costs always result from the breaches, frequently caused by blatant disregard for both data security and PCI compliance.

• Consulting fees: Companies breached have to pay guys like us to whip them into shape quickly. We’re not cheap.

• Legal costs: In case of suffering a breach and then being found noncompliant, the chance of a lawsuit mentioning negligence is higher.

• Fines: The card brands are not very vocal about fines, but public reporting of recent large breaches did mention fines ranging all the way up to $10 m.

• Publicity: The experts can debate how the negative publicity maps into actually dollar losses, there is no denying that the name “Heartland Payment Systems” was not known outside of a narrow segment of payment professionals and now the query on Google for its name finds more than 240,000 pages related to the massive breach. Do you really want your company name to become a synonym for “data breaches?” Exactly, neither did they!

To top it off, a victim merchant can be labeled “Level 1” and thus subjected to an annual QSA assessment—at their own expense. Admittedly, not every breach will incur all of the above, but some are simply unavoidable.

NOTE

If breached and then found noncompliant, your business will suffer. The exact amount of loss that you will take cannot really be predicted up front, but it will be there. In the very worst case, your business will simply be gone, as happened with some merchants over the years. Or, its name will become synonymous with “data breach,” just as Heartland Payment Systems did. And even though TJX (TJ Maxx), the victim of the second largest breach before Heartland, is doing better now than they were doing before the breach, the documented losses were significant. If compliance costs look to be too much for you to handle, your only course of action should be to completely outsource your payment processing to someone else. Besides, in what right mind would a retailer want to be a payment processor?

Overall, it is much more useful to think of customer and cardholder data protection as your “social responsibility” and not as something you do because of some scary “PCI teeth” somewhere! The companies talk about corporate social responsibility (CSR),2 but often forget that caring for the private data of their customers that was entrusted it to them due to the current predominant paradigm—use of a payment card with a magnetic stripe – is the simplest form of corporate social responsibility. What more fits the definition of “embracing responsibility for the impact of their activities on the environment, consumers, employees, communities, stakeholders, and all other members of the public sphere,” than caring for those precious bits and bytes from the magnetic stripe?

Case Study

Next, we present a case study that illustrates what is covered in this chapter.

The Case of the Cardless Merchant

Sometimes, merchants unknowingly accept PCI-related risk and can be left facing substantial fines.

Payton’s “P-Funk All Stars” Party Palace is a recent startup company attacking the ever-popular children’s birthday party celebration location market. Payton recently left her position at a retailer to start her company, and her previous experience included a basic understanding of PCI and that compliance was important and mandatory. When Payton was looking for the ability to accept major credit and debit cards, she made sure to find an Independent Sales Organization (ISO) that offered management of her POS devices.

Upon receiving the contract from her ISO, she noticed that she would still be filing for her own Merchant ID, but one of the ISO’s divisions, PayProcess Express, would be leasing and managing her POS equipment. For an extra fee, they also agreed to perform settlement services and reconciliation reports. Payton’s funding was not substantial, and preferred the transactional-based fees instead of hiring someone part time to perform this function.

Six months into her venture, her business was booming. She received a peculiar call from someone in the fraud department of her ISO asking very odd questions about her setup. She learned that her business was identified as the possible source of a cardholder data breach. After explaining that she outsourced all of her maintenance and upkeep to PayProcess Express, she was informed the business unit was sold to another company, and that the merchant ID was still issued to her directly, therefore she was responsible for paying for fines and the forensic investigation.

Payton was crushed. How did she end up in this situation? She was now facing significant fines that could affect her ability to meet her creditors and payroll.

Payton made one critical error. While her knowledge of PCI was critical to how she set up her payment processing environment, she mistakenly thought that having a third party manage her systems would cover her in the case a breach occurred. In reality, Payton was responsible for keeping up with her compliance, and she failed to ensure that Requirement 12.8 was met with respect to her outsourcer.

Had Payton processed under PayProcess Express’s merchant ID, she may only be facing lost business due to consumer confidence versus facing fines and fees associated with the breach.

Summary

Here are all the myths again:

• PCI just doesn’t apply to us, because…we are special.

• PCI is confusing and ambiguous.

• Recent breaches prove PCI irrelevant.

• PCI is easy: we just have to “say Yes” on SAQ and “get scanned.”

• My network, application, tool is PCI compliant.

• PCI is all we need to do for security!

• Even if breached and then found noncompliant, our business will not suffer.

Now that you know what the myths are and what the reality is, you are one step closer to painless, effective PCI DSS program as well as to secure and compliant organization that cares about its customers by protecting their data.

Remember that PCI is basic security; stop complaining about it – start doing it! By focusing on immediately useful parts of PCI DSS, you can start towards a full-scale risk management program, backed up by implemented and maintained controls. Then, after validating that you are compliant, don’t stop: continuous compliance and security is your goal, not “passing an assessment.” For example, remember that compensating controls are usually temporary controls, not excuses to never do the right thing.

Overall, it is much more useful to develop “security and risk” mindset, not “compliance and assessment” mindset. Just as there is no true guaranteed “job security” today, there is no “guaranteed information security;” there is only one thing: doing the best you can do and being above average, so that attackers leave for greener pastures.

REFERENCES

1. Web site <www.kare11.com/news/news_article.aspx?storyid=542102>; 2011 [accessed 12.07.11].

2. “PCI-DSS: Not on health care provider’s radar” in “SC Magazine” online. <www.scmagazineus.com/PCI-DSS-Not-on-health-care-providers-radar/article/138783/>; 2011 [accessed 12.07.11].

3. PCI DSS SAQ. <www.pcisecuritystandards.org/saq/index.shtml>; 2011 [accessed 12.07.11].

4. ISO/IEC 27001:2005.

5. NIST 800-53. Recommended Security Controls for Federal Information Systems and Organizations. <http://csrc.nist.gov/publications/drafts/800-53/800-53-rev3-FPD-clean.pdf>; 2011 [accessed 12.07.11].

6. PCI Council. Website <www.pcisecuritystandards.org>; 2011 [accessed 12.07.11].

7. The Prioritized Approach to Pursue PCI DSS Compliance. <www.pcisecuritystandards.org/education/docs/Prioritized_Approach_PCI_DSS_1_2.pdf>; 2011 [accessed 12.07.11].

1 As this formula is conceptual and not strictly mathematical, it is often written with many different variations, many including the concept of “Probability” or “Likelihood” of an event occurring.

2 Sometimes corporate social responsibility (CSR) is defined by stating that the business must accept all responsibility for the results of its activities on the nature, environment, customers, employees, and even public at large. Moreover, commercial orgs must actually work in the public interest by encouraging community and choosing to discontinue practices that harm the public sphere or can be seen as unethical. CSR concept is surely controversial but evidences suggests that business are more often pushed to focus on things other than profit, whether it is good or bad.