Session B

Analysis of costs and

benefits

If you are thinking about buying a new car you will have a number of points in mind. Cost will be important, as will the condition of the car and its reliability. If you have a family and a dog you are likely to look for a different kind of car than if you are single. But once you have narrowed your choices to, say, three different cars, you will need specific measures to help you make the final choice. Price, fuel economy and servicing costs are likely to be important in your choice.

Money is also an important measure in organizations. There is little point in spending money on anything if it is not likely to bring in more money than it costs or if it does not provide other benefits to the organization. Financial considerations are important and various techniques are available to judge the potential financial success of projects.

Not all projects lead to profits, as we saw in Session A. For instance, a road cleaning machine will not earn money for a local authority but it will meet the organizational aims of improving the environment of the council tax payers and others. In situations like this, other measures are needed, which compare the costs of the project with the benefits that arise.

In this session we will look at different financial and other techniques for analysing the costs and benefits of projects. This involves looking at separate projects and the implications of projects for the organization as a whole.

First we will cover different ways of looking at the costs of projects, depending on whether the costs are committed already, or not, and are capital in nature or not.

When you are considering a change which involves spending money in your workplace, it is important that you are clear about how much needs to be spent. If the change is inevitable you have no choice in what you have to spend, but at other times you have greater choice and flexibility.

Certain expenditure is required by the law and the requirements of the industry you work in.

Activity 12

Think about your workplace. State two examples where changes involving expenditure have been required by legislation or industry standard rather than being decided upon by your organization.

There are a number of possibilities you may have suggested. Typically this required change will involve:

![]() health and safety equipment such as first-aid kit, machine guards, face masks, eye glasses;

health and safety equipment such as first-aid kit, machine guards, face masks, eye glasses;

![]() training costs associated with handling equipment safely;

training costs associated with handling equipment safely;

![]() toilet and washing facilities and rest areas;

toilet and washing facilities and rest areas;

![]() removal of waste materials and cleaning.

removal of waste materials and cleaning.

The organization must spend money on these matters and they are known as committed costs.

You will still need to make some sort of financial case, because there are different ways of meeting such requirements, of course. For instance, waste disposal may be carried out by your organization or by using contractors. Such decisions have an impact on the overall cost but, nevertheless, some expenditure is still essential on these matters.

As a first line manager, it is important for you to ensure that your organization adheres to the law and industry standards, so you will find from time to time that you will need to update safety materials and so on. Although you will have a good chance of having your request for funds agreed, this could reduce the budget you have for other projects.

Organizations also have other committed costs and these arise when a decision has been taken to go ahead with a major change. For instance, say a decision has been made for your organization to operate from your workplace, which may be a single site or one of a number. The rent or mortgage paid for the work area is a committed cost because, to continue, your organization must continue to pay the monthly amount. Although it is not a statutory requirement to pay the rent or mortgage, the organization cannot continue its plans without meeting this commitment.

Other costs are discretionary, otherwise known as managed or programmed costs. Advertising is a good example because the amount of expenditure on advertising is completely under the control of the organization.

The total cost for any project is likely to be made up partly of committed and partly of discretionary costs.

The Work-based assignment suggests that you speak to your manager, finance director or to your colleagues in the accounts office about the way in which you should go about making a case for finance or a share of the budget in your organization. You might like to start thinking now about whom to approach and arrange to speak with them.

Katy Gorden is a first line manager in charge of a design office. She wishes to update the computers, mainly in preparation for the future time when her workteam will be required to undertake more complex design work. Katy says that she needs new computer equipment:

| Discretionary | Committed | |

| so that it will be powerful enough to run new computer-aided design (CAD) programs | ||

| to meet current health and safety standards for computer screen emissions | ||

| to reduce ‘down-time’ because of faults with the existing equipment | ||

Tick the cost(s) above which are discretionary and those which are committed.

You should have spotted that the health and safety requirements are likely to be committed costs. The expenditure on new equipment to reduce ‘downtime’ and to run new CAD programs would be discretionary in view of the situation described.

However, had Katy's team already been chosen to undertake more complex work, the computers needed to run more powerful programs would be essential and the costs would be committed rather than discretionary.

In the situation described in Activity 13, Katy has a good case for expenditure based on the changes needed for health and safety aspects. Committing expenditure to the replacement of computers would most likely be linked to the required implementation date for health and safety standards. But, if the organization had a need for new equipment within wider-ranging plans, it is likely that Katy would be given the go-ahead to spend money on the new computers earlier.

Have you been involved in situations like this? By understanding the overall plans and strategy of your organization, you will have a better idea of how likely you are to be successful in making the changes you need.

Now let us turn to an important distinction: between capital and revenue costs.

Most projects arising from changes require a certain amount of investment upfront – that is, they cost money initially, which we hope will be repaid over time by the project's benefits. When you are putting a financial case together, it is often this initial or capital outlay that will be at issue first.

What the capital cost actually comprises will depend on the project. Here are some common capital costs:

![]() new buildings, or lease premiums payable on buildings;

new buildings, or lease premiums payable on buildings;

![]() new equipment, such as factory machinery, office or shop fixtures and fittings, computers, laboratory equipment and assembly robots;

new equipment, such as factory machinery, office or shop fixtures and fittings, computers, laboratory equipment and assembly robots;

![]() new vehicles, such as aeroplanes, ships, lorries, cars, and forklifts;

new vehicles, such as aeroplanes, ships, lorries, cars, and forklifts;

![]() site preparation, installation, initial training and software costs.

site preparation, installation, initial training and software costs.

Say you are a first line manager in charge of opening a new shop selling ladies' clothing. What sort of capital costs would the project initially incur?

You probably thought of a number of items, such as the initial lease premium on the premises, the cost of refitting the shop (counters, fitting rooms, lights, décor, shopfront, security system), computer and point of sale equipment, and maybe a delivery van.

Clearly, the actual list of capital costs that a project will incur depends wholly on the nature of the project. The point to bear in mind is that they can often be more extensive than initially appears to be the case, and trying to quantify them for presentation in a financial case can be quite tricky.

Costs which are not incurred as the initial outlay but which do recur over time are classified as revenue costs. These are not only the day-to-day costs of, say, buying stock and selling it on (in the shop example) but also the costs of maintaining use of the capital items. On top of the capital cost of the lease premium, for instance, you will have to pay regular rent, which is a revenue cost.

Activity 15

Referring back to the situation in Activity 14, for each of the following items of initial capital cost, try to identify a related revenue cost which will be incurred over time.

Lights _________________________________________________

Security system _________________________________________

Point of sale equipment ___________________________________

Delivery van ____________________________________________

Lighting will require replacement bulbs over time, the security system will need maintaining, till rolls will be required by the point of sale equipment, and the van will need fuel.

3.1 Making savings

One of the most important reasons for distinguishing between capital and revenue items is that the former can generally be depreciated over time in the organization's accounts, whereas the latter is expensed immediately in the period in which it is incurred. We shall see the significance of this in the next section.

Another important reason is that, by incurring initial upfront capital costs, savings can be made on future revenue costs, which mean that, in total, the organization experiences a net cost saving.

An example of this is where a piece of machinery that costs £5,000 per year to maintain is replaced at a capital cost of £20,000, but annual maintenance costs are only £500. This is a revenue saving of £4,500 per year.

This is probably the most frequently used technique for assessing the financial viability of projects. It regards projects which repay their capital cost most quickly as being best. For example, if a café purchases a new cooker for £1,000 and makes an average of £0.50 profit on each meal, the cooker will be paid for after £l,000/£0.50 = 2,000 meals. If the café sells 40 meals a day, the full price of the cooker is paid back after 2,000/40 = 50 days.

50 days is the payback period.

4.1 Use of the technique

Try the following Activity to apply the technique of payback period.

Zoë and Hamid decided to set up a carpet cleaning business. They purchased carpet cleaning equipment for £800. On average they expect to earn £5 per carpet after expenses and to be able to clean two carpets a day, five days a week.

Calculate their payback period in weeks.

The payback period is

![]()

You will appreciate as a first line manager that the calculations above are rather simplistic. The capital cost of equipment or machinery is fairly easy to work out. It is how much the organization paid for it together with delivery, installation and other costs incurred to get it up and running. But how is income calculated? And you know that income does not always flow in evenly.

4.2 Gathering information for analysis

In practice you will have a number of things to think about when making an analysis of costs and benefits. Gathering information is a very important skill.

Activity 17

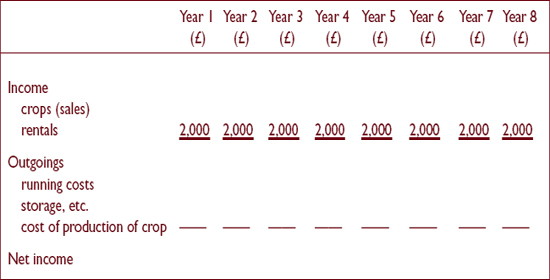

Hampdene Ltd is a company specializing in arable farming. It is thinking about purchasing a combine harvester for a capital cost of £160,000, to be used from August to early October on its fields. It will also be rented out to a neighbouring farm for the remainder of October.

Harvest income flows in from October to December and total sales are expected to bring in £60,000 in Year 1, £66,000 in Year 2 and £70,000 for each year from Year 3 to Year 8 (additional competition in world markets is faced in the later years). Running costs of the combine harvester are estimated at £4,000 a year for Year 1 and Year 2 and £5,000 for each year thereafter. Seeds, fertilizers and other costs of production are generally 50 per cent of the sales income.

Rental income from hiring out the vehicle is estimated at £2,000 per year for the foreseeable future.

While not in use, storage, security and maintenance expenses of the combine harvester are estimated at £1,000 per year.

Each year from Year I calculate the net income for the company generated from the use of the combine harvester, and complete the following table.

The combine harvester generates income from the sale of crops and from rentals. But certain revenue costs, such as storage, security, maintenance and running costs need to be paid, because without the combine harvester they would not be needed.

And not all the income from sale of crops should be seen as paying back the capital cost of the combine harvester because it must first pay back the cost of growing and planting. Without allowing for this, the company could not buy seeds and fertilizers for future years.

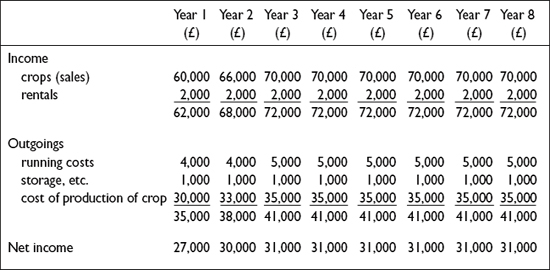

Your calculations of net income should be as follows:

Having put together the information you would be able to work out the payback period. But first, are there any other items of income or cost we have forgotten? Sometimes you will not have all the information you need and will have to ask for more.

Activity 18

Note down three other financial costs or income items to Hampdene Ltd, which could be relevant.

There are a number of other possible revenue costs you may have identified, although no further income appears to be available:

![]() insurance of the combine harvester;

insurance of the combine harvester;

![]() bank overdraft or loan interest if money is borrowed to buy the vehicle;

bank overdraft or loan interest if money is borrowed to buy the vehicle;

![]() any wages and salaries not already included in the expenses quoted. These would include the wage costs of planting and tending the crops and, as other equipment might be involved in these stages of production, you might need to decide what proportion should be set against the combine harvester and how much against other equipment;

any wages and salaries not already included in the expenses quoted. These would include the wage costs of planting and tending the crops and, as other equipment might be involved in these stages of production, you might need to decide what proportion should be set against the combine harvester and how much against other equipment;

![]() management overheads. Part of the cost of growing and selling crops and renting out the vehicle involves action by management;

management overheads. Part of the cost of growing and selling crops and renting out the vehicle involves action by management;

![]() depreciation of the combine harvester (over time the combine harvester will decline in value, and this needs to be recognized each year).

depreciation of the combine harvester (over time the combine harvester will decline in value, and this needs to be recognized each year).

Many of the expenses are approximations. You cannot expect to calculate answers to the nearest pound. The best you can hope for is a reasonable estimate.

These revenue costs, which are not always possible to attribute to a specific business activity but which arise from support which the business needs in order to operate, are known as overheads.

Having made sure that you have all the necessary information you can then calculate the payback period.

Activity 19

Again referring to Hampdene Ltd, and assuming total overheads of £8,000 in Year 1, £7,000 in Year 2, £6,000 in Year 3, £5,000 in Year 4 and thereafter, calculate the payback period for the combine harvester up to and including Year 8.

The calculations for Year 1 and Year 2 are shown to start you off.

The completed calculations are as follows. These show that the combine harvester ‘pays back’ in Year 7.

Despite the obvious limitation of payback, it is widely used because it emphasizes how quickly cash flows into an organization. And cash is usually in short supply in organizations. Cash income which only occurs several years in the future is probably only of importance to stronger businesses which have a regular cash flow from operations and have less immediate concerns about additional cash.

Some firms have a set cut-off point or payback period of, say three years. Any project which does not produce payback of the initial capital cost within three years would not be looked at further. Clearly this eliminates good longerterm projects.

Payback is a useful cautious approach where it is particularly difficult to assess the future, such as where:

![]() projects are risky;

projects are risky;

![]() the organization operates in uncertain markets;

the organization operates in uncertain markets;

![]() design and product changes occur rapidly.

design and product changes occur rapidly.

Let's look at another common method of financial project appraisal – return on investment.

Return on investment, which you may also hear called accounting rate of return is a financial appraisal technique which tackles the problem that payback takes no account of income after the payback period. Return on investment looks at the overall income and expenditure over an entire project and is calculated as the:

![]()

How do you calculate the average investment. If a business purchased equipment for £8,000 with an expected four-year life and no projected scrap value at the end of its life, the average investment would be £8,000/4 = £2,000.

Assuming an average annual project net profit of £500 each year from the use of the equipment, the return on investment would be:

![]()

If an organization has a choice between investments, the one with the highest return on investment would be selected, using this method of financial appraisal.

Activity 20

Media Advertising Associates offer two advertising packages to their clients for advertising cosmetics:

![]() television and cinema advertising, which costs £1,000,000 annually and is likely to generate an average annual net profit of £140,000;

television and cinema advertising, which costs £1,000,000 annually and is likely to generate an average annual net profit of £140,000;

![]() newspaper, magazine and hoarding advertising, which costs £220,000 annually and is likely to generate an average annual net profit of £33,000.

newspaper, magazine and hoarding advertising, which costs £220,000 annually and is likely to generate an average annual net profit of £33,000.

Use the return on investment method to decide which is the best option for clients.

The calculations for the two advertising packages are:

![]()

and

![]()

The cheaper investment using newspapers, magazines and advertising hoardings represents better value for money.

However, if a client has £1,000,000 to spend, an additional £107,000 would be generated. The client must consider how the additional £780,000 investment would be spent otherwise. It might be more sensible to spend the higher amount to generate the higher income, unless other projects are available which would generate at least £107,000 from the ‘spare’ £780,000.

As with the payback method you can see that there are limitations to this method of appraisal too.

Let's now look at return on investment in more detail.

5.1 Profit-based measures

You will remember that payback period concentrates on cash. You deduct the net cash generated by an investment from its initial capital cost.

Return on investment is, instead, linked to profit-based measures. The main impact of this is that the cost of an investment is spread over the full period of its use. For example, if machinery costs £120,000 and is expected to have a five-year working life in the organization, after which it will be sold for £20,000, the total investment is regarded as £100,000 (£120,000 less £20,000). The average investment would be £20,000 each year for the five-year period (£100,000/5). Another way of looking at this annual investment in the machinery is as the worth of the machinery used up each year (depreciation). Depreciation is an expense deducted, like wages and salaries and heat and lighting, when calculating profit. Try the following activity so that you can compare payback method and return on investment.

Activity 21

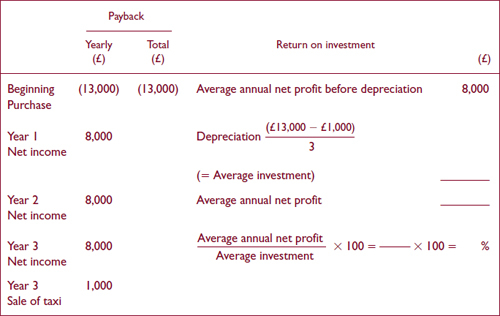

Henry bought a second-hand taxi for a capital cost of £13,000, which he expects to operate for three years, after which he should be able to sell it for £1,000. His projected earnings from fares over the threeyear period are £8,000 per year after deducting expenses.

Complete the following to calculate payback period and return on investment.

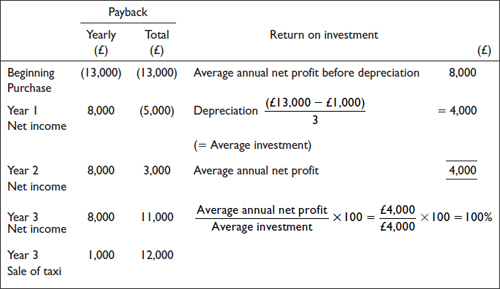

Your completed table, comparing the two approaches, should be as follows.

Payback occurs in Year 2 and the rate of return is 100 per cent. There is no obvious connection between the two but, as you have calculated, the average annual net profit for each of the three years is £4,000, or £12,000 in total over the period. This is the same as the total generated after payback, if you follow the payback calculation through to the end of Year 3.

Organizations which use rate of return to appraise projects tend to have a cut-off point, as with the payback period. No project will be considered if the return on investment is below a certain level, say 40 per cent. If an organization has to borrow to finance a project, the rate of interest that the organization pays on the borrowing is the minimum possible return on investment that the organization could possibly consider without making a loss. And there is little point in an organization undertaking a project which will yield a lower return than would be generated by simply leaving money on deposit at the bank, with very little risk of loss.

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Find out the payback period and rate of return on investment used in your organization for projects. Make a note of these below for future reference.

Other popular methods of financial appraisal are discounted cash flow (DCF) and internal rate of return. Neither of these techniques are covered in this workbook but your ILM Centre will be able to advise you about books covering these topics if you wish to explore them.

![]() Payback period

Payback period

![]() Return on investment

Return on investment

Your answer is very dependent on the industry in which you work. If it is a high-tech or a risky area, required payback is likely to be short and return on investment high. If you are in a long-term and well-established industry with low risk, payback may be much longer and return on investment lower. Forestry, for example, requires growing trees over a long period so payback is, naturally, also over a long period. Some measure of risk analysis may be included in calculations and, for example, an estimate of risk added by an expectation of a generally higher rate of return to allow for riskier projects.

EXTENSION 3

Part 9 covers other techniques of financial appraisal.

5.2 Information gathering

As with payback period, if you are to use the return on investment technique, you will need to be sure that you have gathered all relevant information on which to base your appraisal.

Typically, you will have certain information to hand and have to search out further details and think through the implications of options.

Activity 23

Tony's workteam is involved in conservation work, which is financed by the local council, national grants and donations. Income is reducing from all sources because of external pressures so Tony has been asked to generate income from his workteam's activities.

There are a couple of possible ways of using the woodland managed by Tony and his team, in a sustainable way, which could generate money.

![]() Providing guided walks on certain themes, such as ‘the morning chorus’,‘colours of autumn’, ‘tracking for beginners’ and so on. Specialist experts from local naturalist groups, whom Tony has talked to informally, have said that they would be available for a nominal fee of £10 each. The public could have limited free access to the woodland at other times. Tony feels that by charging £2 each for those wishing to go on the walks it would be easy to recover the cost of the guide. He expects an average of ten people on each walk and twenty-four walks a year.

Providing guided walks on certain themes, such as ‘the morning chorus’,‘colours of autumn’, ‘tracking for beginners’ and so on. Specialist experts from local naturalist groups, whom Tony has talked to informally, have said that they would be available for a nominal fee of £10 each. The public could have limited free access to the woodland at other times. Tony feels that by charging £2 each for those wishing to go on the walks it would be easy to recover the cost of the guide. He expects an average of ten people on each walk and twenty-four walks a year.

![]() Using the wood gained from managing the woodland to make charcoal. This would involve an investment of £1,000 in equipment with a life of twenty years, and £200 to train and provide protective clothing for a couple of people to make the charcoal. This would then be sold for barbecues through local garden centres. Tony expects to be able to sell enough charcoal to provide an income of £600 a year.

Using the wood gained from managing the woodland to make charcoal. This would involve an investment of £1,000 in equipment with a life of twenty years, and £200 to train and provide protective clothing for a couple of people to make the charcoal. This would then be sold for barbecues through local garden centres. Tony expects to be able to sell enough charcoal to provide an income of £600 a year.

Neither option would involve additional labour costs but new people would need to be trained and clothed for charcoal burning every year.

Calculate the return on investment over a three-year period.

How would you recommend Tony should proceed?

Let's put together the information:

![]() The revenue cost of paying guides throughout a year would be 24 × £10 × £240. This would provide an income of 10 × £2 × 24 = £480 in a year. This gives a profit of £240 per year and £720 over the three-year period. The return on investment is:

The revenue cost of paying guides throughout a year would be 24 × £10 × £240. This would provide an income of 10 × £2 × 24 = £480 in a year. This gives a profit of £240 per year and £720 over the three-year period. The return on investment is:

![]()

![]() The equipment has an initial capital cost of £1,000 and lasts for twenty years which, assuming no scrap value for the equipment, requires depreciation of £1,000/20 = £50 to be charged each year. By adding this to training and clothing costs each year, the expenses of the charcoal burning option are £250. Income is estimated at £600 annually, so profit is £600 − £250 = £350 each year, and a total of £1,050 over three years. The return on investment is:

The equipment has an initial capital cost of £1,000 and lasts for twenty years which, assuming no scrap value for the equipment, requires depreciation of £1,000/20 = £50 to be charged each year. By adding this to training and clothing costs each year, the expenses of the charcoal burning option are £250. Income is estimated at £600 annually, so profit is £600 − £250 = £350 each year, and a total of £1,050 over three years. The return on investment is:

![]()

The charcoal burning option provides the greatest return on investment. Financially this appears to be the best option.

However, questions need to be asked before advising Tony which option to take.

![]() Does Tony have any other options which should be included in a full appraisal of the situation? For instance, is there another market for the wood, such as providing small garden fencing or bark mulch for gardens?

Does Tony have any other options which should be included in a full appraisal of the situation? For instance, is there another market for the wood, such as providing small garden fencing or bark mulch for gardens?

![]() Does Tony have £1,200 cash to spend on charcoal burning equipment and training? The first option of guided tours provided immediate payback so long as five people or more attend the first walk. It takes nearly three years to achieve payback on the charcoal burning equipment. If he does spend £1,200, does this limit what else his workteam can do?

Does Tony have £1,200 cash to spend on charcoal burning equipment and training? The first option of guided tours provided immediate payback so long as five people or more attend the first walk. It takes nearly three years to achieve payback on the charcoal burning equipment. If he does spend £1,200, does this limit what else his workteam can do?

![]() Can only one option be undertaken or is it possible to do both? The guided walk option seems, financially, only to require the risk of £10 on each occasion to pay the guide.

Can only one option be undertaken or is it possible to do both? The guided walk option seems, financially, only to require the risk of £10 on each occasion to pay the guide.

![]() How certain is Tony about his figures and the markets? It is essential that the charcoal could be sold for three years to repay the initial cost of the equipment. But will people still require barbecue charcoal in ten to twenty years time? If not, is there another market for charcoal? Guided tours are far less risky financially.

How certain is Tony about his figures and the markets? It is essential that the charcoal could be sold for three years to repay the initial cost of the equipment. But will people still require barbecue charcoal in ten to twenty years time? If not, is there another market for charcoal? Guided tours are far less risky financially.

You may also have thought of matters other than purely financial ones.

![]() Is it acceptable environmentally to take people through the woodland twentyfour times a year on tours? Will this damage the environment?

Is it acceptable environmentally to take people through the woodland twentyfour times a year on tours? Will this damage the environment?

![]() Will charcoal burning damage the environment and cause pollution for, say, local farmers and villages?

Will charcoal burning damage the environment and cause pollution for, say, local farmers and villages?

![]() If Tony wishes to run both charcoal burning and guided tours, will the charcoal burning activities reduce (or increase) the number of people who take the guided tours?

If Tony wishes to run both charcoal burning and guided tours, will the charcoal burning activities reduce (or increase) the number of people who take the guided tours?

It is difficult to measure the cost of such points but, particularly in the public sector, such matters do need to be thought about.

The technique of cost-benefit analysis itself is used as a way of trying to measure the impact of such matters in an overall appraisal of projects.

The technique of cost-benefit analysis attempts to identify and quantify the non-financial costs and benefits of a project. For instance, if a county council wants to put a by-pass around a village, it will be able to calculate the capital costs of building the road in terms of labour and tarmac. But there are other costs associated with the by-pass, some of which are non-financial:

![]() maintenance costs;

maintenance costs;

![]() pollution from exhaust fumes and dirt;

pollution from exhaust fumes and dirt;

![]() water pollution from a mixture of rain and rubber, heavy metals and so on, which accumulate on the road through use, as the mixture runs off into ditches and fields:

water pollution from a mixture of rain and rubber, heavy metals and so on, which accumulate on the road through use, as the mixture runs off into ditches and fields:

![]() noise;

noise;

![]() loss of green fields;

loss of green fields;

![]() general damage to the landscape.

general damage to the landscape.

There are benefits, though:

![]() savings in journey time;

savings in journey time;

![]() fewer accidents;

fewer accidents;

![]() better quality of life for villagers along the existing road;

better quality of life for villagers along the existing road;

![]() fewer large commercial vehicles may replace an extra number of smaller ones previously needed to handle smaller village roads.

fewer large commercial vehicles may replace an extra number of smaller ones previously needed to handle smaller village roads.

Activity 24

Select one cost and one benefit of the by-pass project discussed above. How would you place a value on the effects?

Some costs, such as maintenance, are financial in nature and can be estimated in monetary terms by including potential material and labour costs. Pollution is more difficult to quantify, but you can measure the costs of cleaning up pollution in the village over a few years. You can find a similar by-pass in another part of the country and work out the costs associated with cleaning up pollution there over a similar period. This provides a monetary measure of improved conditions along the road in the village against the worsened conditions along the by-pass.

Savings in travelling time for people could, perhaps, be linked to an average rate of pay per hour as a typical measure of their time.

The cost of accidents can be measured by the costs of treating the victims in hospital. Any resulting deaths can also be given a monetary value by reference to the actuarial tables used in the insurance industry to estimate the likely life span of individuals. There is then the problem of putting a value on each person and their likely contribution to the community.

Even more difficult to put a monetary value on is a view over a landscape. But if you buy a house which looks out over rolling downland, you would expect to pay more for it than for a similar house with a view of the local gasworks. So that gives a basis on which to make some estimation.

Of course, the above measures are purely estimates and someone who works for Friends of the Earth will put a different value on the environment than would a land developer.

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Do you use cost-benefit analysis at work when appraising projects? How far does your organization go in trying to put a value on matters which are not easily measured in financial terms? If applicable, give two examples.

If your organization does not use cost-benefit analysis, think about a recent project at work and say how you would have valued non-financial aspects related to the project.

Much depends on the view of your organization about cost-benefit analysis. Some consider that social costs cannot be measured with certainty, so it is not logical to try to put a monetary value on them. Others take social costs and benefits into consideration as well as making a financial appraisal, but take a subjective approach. Some people try to put a clear monetary value on such matters, for instance linking time saved to an average wage. Costs measured in this way are known as shadow prices.

6.1 Externalities

Acid rain is an example of an externality which crosses international boundaries and cannot be linked to specific producers. Perhaps a country could be made to compensate?

Externalities are the effects that organizations have on society. Conventional accounting does not recognize the costs of, say, discharging toxic waste into a river. The government has a policy of ‘the polluter pays’ so the charge for cleaning up the waste is passed on by the water companies or the appropriate agency to the polluter. This is a social cost with a clearly defined price and is a useful basis for a shadow price. But if the polluter cannot be identified the public funds pick up the bill.

Externalities can also be social benefits. A new factory in an area of high unemployment not only provides jobs and income for employees. It also removes the need for unemployment and other benefits to be paid to individuals and families. This is the social benefit.

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Select an item of equipment or machinery in your workplace which will need replacement soon. Find out the capital cost of two possible replacements and discuss with your manager the income and profits likely to be generated by the replacements, together with their potential life.

1 Prepare a financial appraisal of the replacements, using the payback period and return on investment techniques.

2 Undertake a cost-benefit analysis of the new machinery or equipment compared with the present situation.

3 Choose the preferable option and say why.

If you are compiling an S/NVQ portfolio you may be able to develop your notes into a full report recommending selection of new machinery or equipment to provide to management. You may be able to use your report and feedback on it as the basis of possible acceptable evidence.

As you or your manager may actually have to undertake this task, you are more likely to receive help if you give details of your investigation to your manager and save your organization time.

Your choice and options for replacements suggested depend on the industry in which you work.

However, you are likely to have identified a number of financial and other benefits and costs:

![]() tangible costs (capital or revenue) – can be quantified in monetary terms, such as the cost of equipment or services;

tangible costs (capital or revenue) – can be quantified in monetary terms, such as the cost of equipment or services;

![]() non-recurring costs – comprise capital costs of equipment, site preparation, initial studies, software conversion, one-off training on the new equipment, cost of reallocating human resources, contractual and support services;

non-recurring costs – comprise capital costs of equipment, site preparation, initial studies, software conversion, one-off training on the new equipment, cost of reallocating human resources, contractual and support services;

![]() recurring revenue costs – are paid throughout the life of the project and comprise rentals, leases, licence fees, wages and salaries, travel and ongoing training costs, maintenance and support services;

recurring revenue costs – are paid throughout the life of the project and comprise rentals, leases, licence fees, wages and salaries, travel and ongoing training costs, maintenance and support services;

![]() intangible costs – such as efficiency loss during training on the new project;

intangible costs – such as efficiency loss during training on the new project;

![]() tangible benefits – such as income generated from the new equipment and avoidance of costs previously incurred;

tangible benefits – such as income generated from the new equipment and avoidance of costs previously incurred;

![]() non-recurring benefits – comprising operational effectiveness and saving of resources;

non-recurring benefits – comprising operational effectiveness and saving of resources;

![]() recurring benefits – comprising operational effectiveness and saving of resources;

recurring benefits – comprising operational effectiveness and saving of resources;

![]() intangible benefits – like improved service to the public, improved accuracy and delivery times, better control and security, productivity savings.

intangible benefits – like improved service to the public, improved accuracy and delivery times, better control and security, productivity savings.

Self-assessment 2

1 Calculate the payback period for the following.

![]() Chan Kam Wan invested £2,000 from her budget in equipment to reduce wastage in her work area. In the first year this saved her organization £600 and £800 each year after.

Chan Kam Wan invested £2,000 from her budget in equipment to reduce wastage in her work area. In the first year this saved her organization £600 and £800 each year after.

2 ![]() Paris Ltd bought machinery for £10,000 with a life of five years and no scrap value. Before depreciation the profit generated by the machinery was £3,000. Calculate the return on investment.

Paris Ltd bought machinery for £10,000 with a life of five years and no scrap value. Before depreciation the profit generated by the machinery was £3,000. Calculate the return on investment.

3 Complete the following by filling in the missing words.

Some costs and benefits are easily measured financially. Others are less tangible and measured through the use of ____________ ____________ analysis. One way of putting a price on such intangibles is by using ____________ prices.

4 Identify whether the following examples are tangible or intangible costs, tangible or intangible benefits.

a cost of equipment ________________ ________________

b productivity savings ________________ ________________

c avoidance of costs ________________ ________________

d efficiency loss ________________ ________________

Answers to these questions can be found on page 85.

![]() The total cost of projects usually comprises committed and discretionary costs.

The total cost of projects usually comprises committed and discretionary costs.

![]() Committed costs are required by legislation and industry standards and cannot usually be avoided.

Committed costs are required by legislation and industry standards and cannot usually be avoided.

![]() Discretionary costs are controlled by the organization.

Discretionary costs are controlled by the organization.

![]() Capital costs are incurred by the organization on the initial outlay on a project.

Capital costs are incurred by the organization on the initial outlay on a project.

![]() Revenue costs are incurred over time.

Revenue costs are incurred over time.

![]() Payback and return on investment are financial appraisal methods commonly used.

Payback and return on investment are financial appraisal methods commonly used.

![]() Payback selects projects by regarding the best option as being the project which returns its capital cost the most quickly. It is particularly useful where:

Payback selects projects by regarding the best option as being the project which returns its capital cost the most quickly. It is particularly useful where:

![]() projects are risky;

projects are risky;

![]() the organization operates in uncertain markets;

the organization operates in uncertain markets;

![]() design and product changes occur rapidly.

design and product changes occur rapidly.

![]() Payback does not consider income after the payback period.

Payback does not consider income after the payback period.

![]() Return on investment looks at the overall income and expenditure over an entire project and rates projects according to their level of return.

Return on investment looks at the overall income and expenditure over an entire project and rates projects according to their level of return.

![]() Return on investment is calculated using the formula:

Return on investment is calculated using the formula:

![]()

![]() Payback uses cash measures and return on investment makes calculations through profit-based measures.

Payback uses cash measures and return on investment makes calculations through profit-based measures.

![]() Return on investment rejects investments with a potential return under a given cut-off point.

Return on investment rejects investments with a potential return under a given cut-off point.

![]() Some costs and benefits are more difficult to measure and cost-benefit analysis is used to approve these. Shadow prices are sometimes used to put a financial measure on intangible costs and benefits.

Some costs and benefits are more difficult to measure and cost-benefit analysis is used to approve these. Shadow prices are sometimes used to put a financial measure on intangible costs and benefits.

![]() Cost-benefit analysis sets out to measure externalities and is used in conjunction with financial analysis techniques to assess projects.

Cost-benefit analysis sets out to measure externalities and is used in conjunction with financial analysis techniques to assess projects.