19

Government Policies and Regulations: For Industry Growth, Consumer Protection and Operational Controls

After reading the chapter, the students should be able to understand:

- Government Acts affecting logistics operations

- Logistics documentation

- Government policies for infrastructure development

The scope of legislation affecting business has steadily increased over the years. The industrial policies implemented and regulations enforced by the government from time to time are basically for streamlining the growth of the industry; protecting the companies from unfair competition; shielding the consumers from unfair business practices; and safeguarding the society from unethical business behaviour. The new laws and the growing number of pressure groups, such as consumer forums, have put more restraints on the businesses than ever. The Indian logistical industry is undergoing a sea change after the liberalization of the Indian economy in 1991. The deregulation of transportation, privatization of ports, rationalization of duties and tax structure, and enforcement of environment protection laws are a few measures that have affected this industry. New policies and regulations are being evolved and enforced keeping in view the objectives of globalization, privatization and liberalization, with the additional regulatory dimension for environment protection.

“Ignorance of law is no excuse in any country. If it were, laws will lose their effect, because it can always be pretended.”

—Thomas Jefferson

19.1 WAREHOUSING

Historically, way back in 1928, the Royal Commission on Agriculture formulated the concept of warehousing. In 1945 the Sub-Committee on Agriculture (Gadgil Committee) stressed the need for the establishment of licensed warehouses that will issue warehouse receipts for the goods received for storage. During the 1950s, the Reserve Bank of India circulated a model bill and state governments passed the legislation to regulate the warehouses in the country. In 1950 the Rural Banking Enquiry Committee stressed the need of a warehousing system for agricultural produce. This paved the way for the enactment of Agricultural Produce (Development and Warehousing) Corporation Act, 1956. This was replaced by the Warehousing Corporation Act, 1962 for Public Sector Warehousing.

Policies

Government policy decisions on warehousing are mostly concerned with the storage of food grains and farm products. It had long been felt that to achieve food security, the need of the hour is that the country should strive hard to reduce the enormous post-harvest losses on account of inefficient storage of food grains, both at the farm and the market levels. The same end required upgradation and modernization of the infrastructure for sorting, handling, storage and transportation of food grains.

The Ministry of Consumer Affairs and Public Distribution is engaged in evolving a national storage policy to harness resources of the public and private sectors, both domestic and foreign, to build and operate infrastructure for bulk handling, storage and transportation of food grains. The government was also considering according infrastructure status to bulk storage and handling operations and making improvement in the legal framework to create a more investment-friendly environment in the sector. The policy also envisages suitable incentive for development of appropriate storage structures for safe storage of food grains at the farm level, where a substantial quantity of the produce is used for food, feed and seed purposes.

In July 2000 the union government accorded infrastructure status to “food grain storage” sector. This now forms part of the “National Storage Policy” evolved in 2000. Under infrastructure development “storage and warehousing services” are included in the list of industries (No. C-9, NIC Code 741) wherein automatic approval for foreign equity up to 50/51/74 per cent is allowed. The Department of Surface and Sea Transport now allows 100 per cent private or foreign investment to develop infrastructure facilities at seaports in India. It includes:

- Construction and operation of container terminals

- Construction of warehouses and storage facility at ports to help growing export/import cargo

- Providing material-handling facility at ports and warehouses therein

- Construction of multi-purpose and specialized cargo berth

According to the new policy guidelines, the central government has plans to invite private participation in building adequate storage facility for food grains, which suffer heavy loses every year. Recognizing this as a serious problem, the government has decided to offer a plethora of incentives such as income tax exemptions (tax holiday for five years and 30 per cent deduction of profits for the next five years) and loan from National Bank for Agriculture and Rural Development (NABARD) at lower interest rates to attract private investment.

As regards cold warehouses, these are controlled by the Cold Storage Order, 1980. This order was promulgated under the Essential Commodity Act, 1955 and has the objectives of ensuring hygienic and proper refrigeration conditions in cold storages. It regulates the growth of the cold storage industry in a planned manner, rendering technical guidance for scientific preservation of foodstuff in a cold storage and prevents the exploitation of farmers by the cold storage owners. The aforesaid order was rescinded by the Cold Storage Order, 1997, for allowing a free mechanism for demand-based growth of the cold storage industry.

The Warehousing Corporation Act, 1962

This act provides for the incorporation and regulation of corporations for the purpose of warehousing of agricultural produce and other commodities, and for matters connected with it. The objectives of this act are:

- To issue a warehouse receipt to the depositor that can be used as a negotiable document for transaction with producer, depositor, dealer and bank

- To reduce wastage and storage losses by establishing, developing and running warehouses on scientific principles

- To help depositors in marketing the warehoused goods

- To train and develop manpower to manage warehouses built and run on scientific principles

The Act specifies the formulation of Central Warehousing Corporation (CWC) and State Warehousing Corporations (SWCs) for storage of agricultural produce. The CWC and SWCs are empowered to establish and run large-size warehouses at the production centres, marketing centres and ports involving a huge capital outlay. These corporations can store agricultural produce, seeds, manures, fertilizers and other notified commodities offered by industries, cooperative societies and government agencies. The Act allows these corporations to function as agents on behalf of the government for the purpose of purchase, sale, storage and distribution of the abovementioned goods.

Warehousing (Development and Regulation) Act, 2007

This Act proposes to regulate the warehousing business. However, till the government issues a notification, the existing law will remain in operation. Currently, the law of contracts governs the business of warehousing, and it is left to the contracting parties to decide the terms and conditions of the warehousing arrangements.

A significant aspect of the business of warehousing is the status accorded to the warehouse receipt and whether such receipt is transferable by endorsement and delivery, along with the property in the goods represented by such receipt. Under section 2(4) of the Sale of Goods Act, 1930, a warehouse receipt is also included in the definition of documents relating to the goods title. But the law does not provide sanctity to such a receipt as a negotiable document, nor does it provide for the rights and obligations of warehouseman and holder of warehouse receipt. Since it is not a negotiable instrument or document, it is not possible to deal in the document title for trading in commodities and raise finance against the security of warehouse receipts. The new law fills these gaps and provides a new regulatory regime for warehouse business. It facilitates the issue of negotiable warehouse receipts by any person carrying on the business of warehousing. The salient features of this Act are:

- The object of the Act is to make provision for the development and regulation of warehouse, negotiability of warehouse receipts and establishment of a Warehouse Development and Regulatory Authority

- A person who delivers goods to the warehousemen for storage is defined as a depositor and the goods are defined as all tangible goods excluding actionable claims, money and securities whether fungible or not

- Definition of negotiable warehouse receipt recognizes negotiability of such receipt and provides for effect of transfer of goods represented thereby, when the receipt is endorsed and delivered (negotiated)

- The law applies to any person who is registered as a warehouseman with the authority of carrying on the business of warehouse, that is, maintaining warehouses for storage of goods and issuing negotiable warehouse receipts

- The law recognizes a warehouse receipt in electronic form issued by the warehouseman or by his duly authorized representative

- Any person desirous of undertaking the business of maintaining warehouse and issuing negotiable warehouse receipt has to obtain registration. Any person, firm, cooperative society or any association of persons, whether incorporated or not, can function as warehouseman

- Existing warehouse business has to apply for registration within 30 days from the date of commencement of the Act

- The law makes detailed provisions about particulars to be included in the warehouse receipts, their negotiability by endorsement and delivery, warranties on negotiation of warehouse (w/h) receipt and issue of duplicate receipts

- The law provides for registration of accreditation agencies for issue of certificate of accreditation to the w/h issuing negotiable w/h receipts

- Any existing or future warehouseman not intending to issue negotiable w/h receipts is not governed by this law. Such a person can continue his business activity without obtaining registration

This law has distinct advantages for the agriculturist as well as commodity traders. Negotiable warehouse receipts will facilitate trade in commodities without physical handling of the stocks of commodities and other goods. Warehouse receipts being documents of title to goods can be easily offered as security for a loan. Development of modern warehouses would also facilitate storage of surplus crops and sale at a future date when there is demand for such goods/commodities.

Licensing of Warehouses

For operating a warehouse a promoter has to obtain a licence from the appropriate authority. The licence issuing authority is the local municipal corporation.

However, in the case of warehousing of pharmaceutical products, approval from the Food and Drug Authority (FDA) is a must for regulating the upkeep of proper hygienic conditions because of the nature of the product. The licensing of warehousing is governed by the following conditions:

- Maintenance of proper storage conditions, depending on the type of goods to be warehoused

- Payment of the prescribed fee as stipulated by the authority

- To issue warehouse receipts against goods deposited in the warehouse

- To run the warehouse on scientific principles by taking necessary precautions against damage or loss of goods due to water, attack of pests and rats

- To make available proper facilities for inspection, segregation and movement of goods

- To insure the goods

For opening of warehouse for industrial goods, the warehouseman is required to get a licence from the local municipal corporation under the Establishment Act, 1948. In the case of bonded warehouses, the licensing authority is the customs department. Imported cargo is kept in warehouses called bonded warehouses until it is cleared through customs formalities. The goods are released to the consignee after the duties are paid. Bonded warehouses may be under private or public authority. The commissioner of customs issues the licence for the operation of bonded warehouses to parties who fulfil the requirements stipulated in the Indian Customs Act. These licences are issued against security deposits and under certain term and conditions.

19.2 TRANSPORTATION

The country has entered into a deregulation environment in transportation except for rail transportation. Due to globalization and the emerging socio-economic trends, customer expectations are increasing so fast that the just-in-time (JIT) transportation system, still uncommon in India, will soon become the norm rather than the exception. The change in the air was in fact visible in the mid-1980s with the deregulation of road transportation. Air transportation witnessed a change in the early 1990s. Ports and highways have already been taken up and it will not be long before rail transportation also witnesses far-reaching changes. A closer look at the logistics network at the macro-level highlights the fact that a large number of issues still need resolution for the development of an integrated logistics network. Aware of the manifold increase in trade and commerce activities and the growing need of a good logistics system to support it, the Indian government has since the liberalization of the economy taken the following policy initiatives to build a supporting infrastructure.

Policy Guidelines for Infrastructure Development

Air Transportation

- The repeal of the Air Corporation Act, 1953, on 1 March 1994 ended the monopoly of public sector air carriers, both for passenger and cargo transportation. The steps include allowing foreign equity holding up to 40 per cent. Hundred per cent holding by non-resident Indians is permitted in domestic airlines. No direct or indirect equity from foreign airlines is allowed in domestic air transportation. Management contract with foreign airlines is not permitted

- Private sector participation in the construction and operation of new airports on “build, own and transfer” basis is allowed

- Hundred per cent FDI in airports is permitted. However, FDI above 74 per cent requires prior government approval

- The government had allowed ten years tax holiday for 100 per cent profits derived from the development of airports for a period of ten consecutive assessment years out of the first fifteen assessment years

- Airport warehousing, a critical issue particularly for perishable products, is being seriously reviewed for the growth of exports

Sea Transportation

- Most of the categories of ships, that is, crude tanker, product tanker and bulk carriers have been brought under open general licence to facilitate acquisition at competitive price

- Freedom to time charter out ships by Indian shipping companies

- Hundred per cent investment by NRIs in shipping with full repatriation benefits

- Automatic approval for foreign direct investment up to 74 per cent in shipping

- The shipping companies allowed to retain sale proceeds of their ships abroad and utilize them for fresh acquisition. Similarly, they are allowed to get their ships repaired at any shipyard without seeking permission from the Indian government.

- Private investment in building ports and setting up related facilities (warehousing, material-handling equipment, container stations, dry docks, repairs and captive power plant) is allowed

- Leasing of equipment and floating crafts for port operations from the private sector is allowed

Road Transportation

- Private sector including foreign equity participation up to 100 per cent in the construction of highways on build-operate-transfer (BOT) basis allowed. The investors in highway projects are allowed to recover their investment by way of collection of toll for a specified period

- Enactment of Multi-modal Transportation Act, 1993 for speedy cargo movement within and outside India

- Towards environment protection, the emission norms have been enforced in 1996 (equivalent to Euro I) and in 2001 (equivalent to Euro II).

Inland Waterways

- Private sector participation in inland waterways projects is allowed. The government participation will be limited to 40 per cent for BOT projects.

- Hundred per cent FDI is permitted

- The areas of private sector participation are ownership of vessels, fairway development and maintenance, construction and operation of river terminals, providing cargo-handling systems, and providing pilotage services

Regulations

Logistics in India has to operate under a regulatory environment, which sometimes hampers the healthy growth of industry. However, the various laws enacted from time to time are for protecting the interest of the common citizen and checking malpractices. Logistics industry in India is operating in the environs of the following Acts:

- The Motor Vehicles Act, 1988

- The Carriage by Air Act, 1972

- The Carriage of Goods by Sea Act, 1925

- The Multi-modal Transportation of Goods Act, 1993

- The Central Excise Act, 1944

- The Central Sales Tax Act, 1956

- Environmental Protection Act, 1986

- Consumer Protection Act, 1986

The most important ones are discussed below.

The Motor Vehicles Act, 1988. Motor transport in India was first regulated under the Motor Vehicles Act, 1914, which had limited functions. However, with the growth of road traffic, the need for regulation on public safety and convenience was realized. This resulted in the passing of the Motor Vehicles Act, 1939, which was further amended in 1988 when the Motor Vehicles Act, 1988 came into force. The major provisions of the Act are maintenance of state registers for driving licence and vehicle registration; constitution of road safety councils; control of air and noise pollution; liberalization of permits for owners of transport vehicles on the national routes; and fixing age limit for different types of vehicles. The Act prohibits overloading of the truck to ensure safety during transit.

The Carriage by Air Act, 1972. This covers the conventions relating to the rights and liabilities of the carriers, consigner and the consignee. According to this law, the air carrier must deliver an air consignment note for carriage of goods by air, which will cover the name and address of the consigner and consignee, the goods details (type, quantity, package, freight and so on) and value of the goods. The carrier is liable for damage or loss of goods sustained during transit and the compensation has to be paid as per the terms stipulated.

The Carriage of Goods by Sea Act, 1925. A bill of lading was originally a receipt of goods placed on a ship and also a document for transferring the title of goods to consignee. However, with the development of trade, it became a negotiable instrument in which the supplier, shipper, bankers and carriers became interested. Concurrent with this, it became customary to show on the bill of lading the terms of the contract on which the goods were delivered to and received by the ship. There were many differences among shippers and carriers in preparing a bill of lading. Hence, the need arose for uniformity in the preparation of bills of lading among all maritime countries involved in international trade. As a result, the Carriage of Goods by Sea Act, 1925 was enacted. According to this Act, a bill of lading is a must for transport of goods by sea. The content of a bill of lading serves three purposes:

- It is a receipt of goods shipped containing the terms on which they have been received

- It is the evidence of a contract for carriage of goods

- It is a document of title to goods specified in it

This Act also covers the responsibilities, liabilities and risk involved on the part of the consigner, the carrier and the consignee.

The Multimodal Transportation of Goods Act, 1993. The Multimodal Transportation of Goods bill was passed by both Houses of Indian Parliament on 2 April 1993 and came on the statute book as Transportation of Goods Act, 1993. This is an Act to provide for the regulation of multimodal transportation (rail, road, sea and inland waterways) of goods from any place in India to a place outside India, or multimodal transportation contracts and matters or incidents connected therewith. Its jurisdiction extends to the whole of India except the state ofJammu and Kashmir. The Act provides for registration (with payment of prescribed fees) of multimodal transportation activities with the proper regulatory authority in the area of operations. The operator has to maintain and issue the prescribed documentation for the movement of goods.

Central Excise Act, 1944. This Act empowers the government to collect the levied tax, called excise duty, imposed on the commodities produced and products manufactured as per the goods classification in 1st and 2nd Schedules of Section 3 of the Act. According to the regulations, excisable goods cannot be removed form the manufacturing premises unless the excise duty is paid to the excise authority. The holder of the goods has to maintain a proper record of the inventory of excisable goods in store. The goods dispatch documents, which are sent along with the vehicle carrying the goods, should include the excise gate pass, duly endorsed by the excise authority. Transporting goods without the excise gate pass is an offence and heavy penalties for evading the tax, such as fine or imprisonment, may be imposed on the parties involved.

MODVAT, which stands for modified value-added tax, was subsequently introduced in 1986 to avoid the double charging of excise duty on an item used in the manufacture of finished products. When a raw material or component is used in the manufacture of finished products, the manufacturer gets the credit to the extent of the excise duty paid on these inputs, which is subsequently deducted from the excise duty charged on the finished products being removed from the factory. MODVAT eliminates the need for prepayment and future collection of the refund of excise duty.

The government is contemplating introduction of CENVAT for simplicity and transparency in tax assessment and collection. However, an issue that still remains to be resolved relates to the differential duty for which the manufacturer can avail credit against the supplementary invoice.

The Central Sales Tax Act, 1956. The Central Sales Tax (CST) Act provides for levy on inter-state sales. The local state sales authority administers the collection of CST. Also, each state has imposed a levy on sales within the state. For the incidence of sales tax (ST), two things are necessary, e.g. the movement of goods and the completion of sales as per the agreement between buyer and seller. The sales tax thus collected by the seller from the buyer has to be deposited with the sales tax authority. Sales tax rates differ with the product and its classification as indicated in the Sales Tax Manual. The value of the applicable ST should be reflected in the sales invoice, which forms a part of the documents accompanying the goods during their movement. According to the regulation, the invoice must have CST and ST numbers of both the consignee and consigner. In the absence of the CST number of the consignee, a flat 10 per cent ST is applicable and it must appear on the invoice. The consignment should be accompanied with the proper ST form or permit. Each of the Indian states has specific requirements of ST formalities to be completed by the consigner as shown in Table 19.1.

VAT, which stands for value-added taxation, was introduced in the Finance Bill 2002 (for implementation by 1 April 2003) for assessment and collection of sales tax along the lines of MODVAT or CENVAT for excise duty. It eliminates the multi-point incidence of sales tax in the value-addition process of converting product inputs to finished products. Most states currently levy an entry tax or octroi on select commodities and plan to continue with them in VAT. This levy over and above the local sales tax creates tax cascading and results in higher consumer prices. However, a fully vatable entry tax on sales within the state, levied at a rate equal to the VAT rate, will eliminate tax cascading. Under this system, a registered dealer who pays an entry tax on imports into the state would be entitled to a 100 per cent tax credit of entry tax paid on further sale of the goods within or outside the state. VAT will eliminate the disparities in local ST applicable in different Indian states. With uniformity in the incidence of ST across the country, manufacturers can do away with the distribution centres that were opened to take advantage of tax disparities in different sates.

Table 19.1 Reference Guide for Sales Tax & Octroi in India

Environmental Protection Act, 1986. This Act empowers the government to take all such measures as it deems necessary or expedient for the purpose of protecting the quality of environment and preventing, controlling and abating the environmental pollution. Under this Act, the following two rules regulate the storage, handling and transportation of hazardous material and chemicals:

- Hazardous Waste (Management and Handling) Rule, 2000

- Manufacture, Storage and Transportation of Hazardous Chemicals Rule, 1984

These rules lay down the guidelines for the manufacture, storage, handling and transportation of hazardous material and waste. The materials and waste are covered in schedules 1, 2 and 3 of the above rules. The guidelines are for operational safety in manufacture, storage, handling and transportation of hazardous materials to avoid contamination, protect living beings and maintain a clean environment. According to the Act, a carrier is required to follow the procedure as shown in Figure 19.1 for transporting hazardous goods.

Fig. 19.1 Procedure for transporting hazardous material

Consumer Protection Act, 1986. [Act No. 68 of Year 1986, dated 24th December 1986]—An Act to provide for better protection of the interests of consumers and for that purpose to make provision for the establishment of consumer councils and other authorities for the settlement of consumer’ disputes and for matters connected therewith. It extends to the whole of India except the State of Jammu and Kashmir.

Documentation

The importance of transportation documentation cannot be denied in today’s complex business environment. Documentation becomes legally binding on the carrier on acceptance of goods for moving from one place to other one. Documentation of the contract between the shipper and carrier is duly executed by the carrier. This document has legal status, as it is issued according to the applicable laws of the land and acts as a proof of acceptance of goods for transportation. The nomenclature of this document differs for the different modes of transportation, but its function and purpose is the same. The major documents used in the transportation business are discussed below.

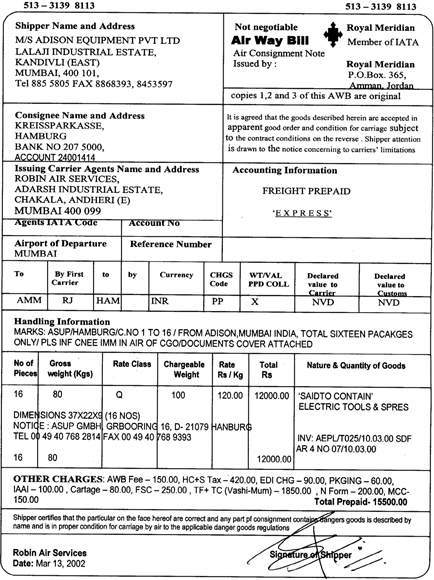

Airway Bill. Airway Bill (AWB) is a negotiable document issued by the Airlines towards the receipt of a goods consignment. This is a receipt of goods from the consigner, after these are accepted by the airlines. The AWB shall have an endorsement for “freight paid” or “freight to be paid at destination” as the case may be. The consignee may collect the goods at the destination, after surrendering the AWB. It is part of the import and export documentation for customs clearance (Figure 19.2).

Railway Receipt. The Railway authority issues the Railway Receipt (RR) after the consignment has been accepted for booking. The consignment is weighed, marked and the RR is issued to the consigner. This document is prepared in four copies. The first copy is given to the consigner and the second copy is sent to the destination station. The railway accounts department gets the third copy and the fourth is retained with the railway station. The RR is used as a negotiable instrument and changes hands before it is finally presented at the destination station for taking delivery of the consignment (Figure 19.3).

Goods Consignment Note or Lorry Receipt. For transporting the goods by road carrier, the shipper or consigner has to inform the carrier operator about the nature of the consignment, place of loading, destination, quantity of goods and route to be followed. After receipt of the goods, the carrier issues Lorry Receipt (LR) or Goods Consignment Note (GCN) to the shipper or consigner as the proof of acceptance of goods for transportation (Figure 19.4). This is a contract document between the consigner and the carrier. It is used as a document of proof of dispatch for the bank to make payment to the consigner. The LR or GC note includes the following:

- Name of the consigner

- Destination and name of the consignee

- Description of goods

- Details of boxes or packages

- Weight of goods

- Nature of freight payment (freight paid or freight to pay)

Fig. 19.2 Airway bill

Fig. 19.3 Railway receipt

The other terms and conditions of the contract between the consigner and the carrier governed by the Carrier Act, 1880.

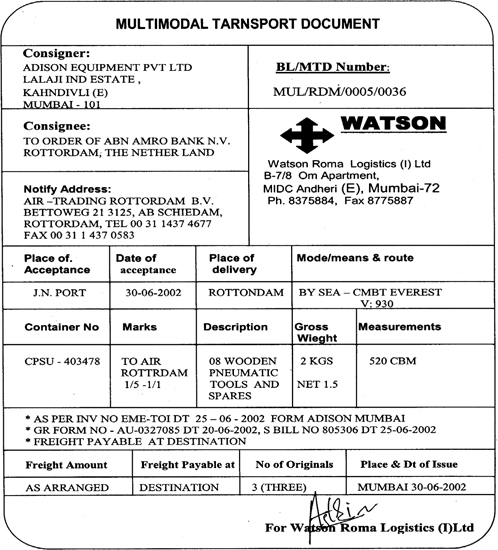

Bill of Lading. This is an important negotiable document for sea transportation. The shipper will get this document from the shipping company duly stamped with the required number of copies. The Bill of Lading (BL) will contain an endorsement of “Freight paid” or “Freight payable at destination,” depending on whether the freight on the shipment is paid or is to be paid at destination (Figure 19.5).

The following details are incorporated in this document:

- Name of the shipping company

- Flag of nationality

- Name of the consigner or shipper

- Description of goods

- Number of packages/boxes

- Country of origin of goods

- Markings on the packets

- Gross and net weight of the goods

- Freight rates

- Date of booking

If the negotiation is through bank, the BL is forwarded to the bank with the invoice copy, LC (Letter of credit) copy, inspection certificate and certificate of origin and so on.

Fig. 19.4 Goods consignment note or lorry receipt

19.3 PACKAGING

In developed countries, the regulations on packaging are more stringent because of the strict laws in force for the protection of consumers’ interests and the environment. In developing countries, such as India, various legislations have been enacted at various points of time. These can be broadly categorized into the following:

- Operational safety

- Public health and hygiene

- Consumer protection

- Export promotion

- Transportation

- Quality of product

Fig. 19.5 Bill of lading

Operational Safety

These regulations are aimed towards the safety of operational people. The packaging requirement for hazardous and explosive materials has to be satisfying as per the orders issued by the Department of Explosives and Hazardous Materials. Indian Railways and the International Air Travels Association (IATA) have listed the restricted articles for transportation. The article with a particular commodity code is not accepted for movement.

Public Health and Hygiene

These regulations are covered under the Drug and Cosmetic Act and are more concerned about the integrity of the product in relation to what is printed on the packaging. The guidelines for packaging as laid down have to be meticulously followed to avoid penalty.

Consumer Protection

Under the consumer protection regulations, all manufactured products are covered. It is statutory for the manufacturer to put a label on the product packaging to enable the customer to identify the product and compare it with other brands of the same product available in the market.

Transportation

Packages for transportation are required to be marked or labelled containing the following information:

- Consigner and consignee details

- Type of the product

- Handling instructions

- Shipping weight

- Symbols for dangerous products

Exports

Export regulations issued by the government are implemented by the Export Inspection Agency. The regulations are covered under Heavy Package Act, 1951. They cover the guidelines for quality standards, protecting, testing and packaging. The export consignment needs to have identification marks on the package. The information should include the name of the manufacturer, name of the consigner, name and address of the consignee, port of destination, country of origin, product type, quantity, shipping weight and handling instructions. The above information is put in the languages of the country of origin and the country of destination (if required). The package should be duly inspected and stamped by the export inspection agency for clearance through customs. The blind or coded marking is recommended for high-value cargo susceptible to pilferage or theft (see Figure 19.6).

The instructions markings on their contents and positioning on the package should be in accordance with the guidelines covered under the regulations. These are more specifically mentioned under the regulations issued by International Maritime Organization (IMO) and International Air Transport Association for dangerous and general goods cargo.

19.4 INVENTORY VALUATION

Inventory valuation comes under the purview of the financial accounting system and not under logistical management. The standards issued for valuation of inventories fall under Accounting Standard 2 (AS 2) issued by the Council of the Institute of Chartered Accountants of India. The standard deals with the principles of valuating inventories for financial statements of the firm. The basic philosophy behind the inventory valuation is as follows: inventories are held in expectations of deriving the revenue directly or indirectly from their sale or use. In order to determine the results of a business for a given period, it is necessary to carry forward the cost related to inventories until the inventories are sold or used. The inventories are normally stated at the historical costs (purchase prices) and net realizable value. Several different formulae for assigning the costs are used. These are first-in-first-out, average cost, last-in-last-out, base stock, standard cost, special identification, adjusted selling price and the latest purchase price and so on.

Fig. 19.6 Export packaging marking

SUMMARY

The government of any country in the world monitors and controls the growth of industry and commerce in that country through legislation. The regulatory environment in the country is normally in line with the policies adopted by the government for the nation’s economic growth. The logistical industry in India is no exception. The current regulations are in line with the liberalization measures adopted by the Indian government since 1991. The transportation industry except the railways is privatized long back. Private investments are welcome for infrastructure development projects such as roads, airports and seaports, which are necessary for the growth of the logistical industry in the country. The various Acts passed by the government are for curbing the malpractices in the industry and the exploitation of gullible customers by organizations possessing financial muscles. The regulatory environment today is much more conducive for industrial growth in the country than it was before the liberalization of the Indian economy in 1991. The deregulation of transportation, privatization of ports, rationalization of duties and tax structure and enforcement of environmental protection laws are a few measures that have had positive effects on the industry. New policies and regulations are being evolved and enforced, keeping in view the objectives of globalization, privatization and liberalization, with the additional regulatory dimension for environment protection.

REVIEW QUESTIONS

- Explain the importance of documentation in transportation.

- Discuss the role of regulations in the growth of logistical industry in India.

- Are the current government policies and regulations with respect to the logistics industry in line with the policy of economic liberalization adopted by the Indian government in 1991?

INTERNET EXERCISES

- Log on to http://www.logisticsfocus.com and study the legal and regulatory resources for the logistics industry in India.

- Visit the Asian Institute for Transport Development at www.aitd.net and study transportation planning and policies in India.

BIBLIOGRAPHY

Chandrachud, Y.C. 2000. Laws of India, Vols. 1–3. Delhi: Bharat Law House.

Heinze, Carolyn. May 2006. Cross-Border Transport: Keeping Free Trade Safe and Sound. http://www.inboundlogistics.com/articles/features/0506_feature04.shtml (last accessed on___).

Indian Logistics—Industry Report. 18 January 2008 by bharatbookbureau http://bharatbookreport.wordpress.com/2008/01/18/indian-logistics-industry-report/(last accessed on 18 January 2008)

Malik, PL. 2001. Industrial Laws, Vols. 1 and 2. Lucknow: Eastern Book Co.

Raghuram, G. and Janak Shah. 2003. ‘Roadmap to Logistics Excellence: Need to Break Unholy Equilibrium.’ www.iimhd.ernet. Presented at CII Logistics Convention, Chennai, India, Oct. 2003.

The Institute of Chartered Accountants. 2000. Management Accounting and Financial Accounting.

Vashishth, Vikas. 1999. Laws & Praof Environmental Laws. Delhi: Bharat Law House.

Web site. www.sarkantel.com/ministries/shipping_roadtransport_highways.