CHAPTER 5

Writing Off Vehicle, Travel, Meals, and Gifts Expenses

- Vehicle Expenses

- Local Transportation

- Business Meals

- Business Travel

- Business Gifts

- Strategies for Saving on Travel Costs

- What's Ahead

Almost every self-employed person has a vehicle, travel, meals, and gift costs related to his or her business. The costs may be taking a customer to lunch, giving a gift to a vendor on the birth of her child, or using a personal car for business travel. While the expenses are commonplace, the tax rules are very strict when it comes to deductions for them. The reason for restrictions: The government believes there is considerable room for abuse here, with personal outlays incorrectly treated too often as deductible business costs.

When it comes to these expenses, you have two layers of complexity. First, you have to understand the deduction rules, which for certain expenses may include limitations on how much can be written off. Second, you have to follow cumbersome recordkeeping rules. The failure to do so may cause you to lose legitimate write-offs. As a general rule, you're supposed to keep records contemporaneous with the expense, which means at or near the time you have the expense. This is a tax rule that makes sense because it's often difficult if not impossible to remember particulars long after an event.

What types of vehicle, travel, meals, and gift expenses are deductible? What limits apply? And what strategies can you use to help with recordkeeping and containing costs? Let's find out.

Vehicle Expenses

If you use your personal car, van, or truck for business, you're not alone. Most self-employed people do. You can claim a deduction for business use of a vehicle. Expenses related to the time you use the vehicle for personal driving are not a deductible business expense. The allocation between personal and business driving is based solely on mileage.

Example

You are a sole proprietor who owns a flower shop and use a personal van to deliver flowers. You put on 16,000 miles in the year making deliveries and 4,000 miles commuting to and from your shop (which is not deductible). Because 80% of the van's use (16,000 ÷ 20,000) is for business, then 80% of the cost of operating the van is deductible (see ahead for the way in which to take the deduction).

What Constitutes Business Driving?

If you have a home office for which you claim a deduction (see Chapter 6), then all business-related driving from and to home are considered to be for business.

Example

You operate solely from home and drive to the bank to deposit a check from a customer. (Maybe your bank app for making remote deposits couldn't read the check.) The trip from home to the bank and back again is deductible.

Other business activities and destinations that give rise to deductible driving include:

- Courses that are deductible (e.g., a continuing education course in your field)

- Customers and clients

- Networking events

- Office supply store

- Post office or shipper

- Trade shows

- Vendors

Putting a sign on your vehicle advertising your business doesn't transform your personal driving into business driving. The cost of the sign is a deductible advertising expense (see Chapter 7).

If you work from an office or other location outside your home, you cannot deduct travel from home to your office or other business destination and back again. This is considered commuting, which is a nondeductible personal expense. However, once you're at the office or other business location, you can then deduct travel to and from business destinations. For example, you run a travel agency in a strip mall near your home. The cost of driving to your office isn't deductible. However, travel from your office to the UPS store to ship travel documents to a customer and back to your office is deductible business travel.

Ways to Figure Deductions

There are two ways to figure your deductible expenses:

- Actual expenses. With this option you track all of your driving costs, including gas and oil, repairs and maintenance (including car washes), and insurance, and then deduct the portion of the costs related to business driving. The actual expense method also includes depreciation if you own the vehicle or lease payments if you lease it. You can find details about depreciation and rules related to deducting lease payments in IRS Publication 463.

- IRS standard mileage rate. With this option you deduct a fixed cents-per-mile for business driving. The rate in 2019 is 58¢ per mile. This rate is adjusted annually, or even more frequently, by the IRS as driving costs rise. (The IRS has never said how it figures the cents-per-mile rate.) With this method you simply multiply the miles you drive for business by 0.58. The same rate applies whether you drive a car, van, or truck.

Regardless of which method you use, you can also deduct:

- Parking and tolls for business travel. However, parking and tolls related to nondeductible commuting are not deductible.

- Interest on a loan to buy a vehicle. Remember, if the vehicle is used partly for personal purposes, you must allocate the interest between business and personal; only the business portion is deductible.

- State and local property taxes on your motor vehicle if you itemize your personal deductions on Schedule A of Form 1040 or 1040-SR (subject to the overall limit on the deduction for state and local taxes, called the SALT cap).

Which Method to Choose

Obviously you want to use the method that gives you the greater write-off for vehicle use. Factors impacting your choice include the cost of the vehicle (for example, an expensive vehicle will have high monthly lease payments). If, for example, you buy an expensive vehicle, you can deduct depreciation (an annual allowance related to the cost of the vehicle) up to a set dollar limit. The depreciation rates are 20% for the first year, 32% for the second year, 19.2% for the third year, 11.52% for the fourth and fifth years, and 5.76% for the sixth year. But the depreciation allowance can't exceed a dollar limit. Just to give you an idea of what the annual dollar limits on depreciating are, see the 2019 limits in Table 5.1. However, the dollar limits for 2019 aren't triggered and the depreciation percentages apply unless the vehicle costs more than $90,500.

Special Rules for Special Vehicles

Not every vehicle is subject to the dollar limits:

- Heavy SUVs (weighing more than 6,000 pounds). These vehicles, such as Hummers, Lincoln Navigator SUVs, and Porsche Cayenne SUVs, are subject to regular depreciation. In addition, a first-year (Section 179) deduction up to $25,500 for 2019 (the dollar amount can be adjusted for inflation annually), plus bonus depreciation if in effect (e.g., 100% in 2019), can be claimed; any cost not already recovered is then subject to regular depreciation. Such vehicle has a 20% depreciation allowance in the first year. Thus, the entire cost is deductible in the year the SUV is bought and placed in use for your business.

- Non-personal-use vehicles. If the vehicle isn't meant for personal use, its cost is written off as any other type of machinery or equipment. Such vehicles include, for example, vans outfitted with shelving and a jump seat so that it is not suitable for personal use. However, merely putting a sign for your business on the vehicle doesn't make the vehicle non-personal use.

Be aware that if you want to use the standard mileage rate, you must do so for the first year in which you use the vehicle for business. In later years you can choose to deduct actual expenses. But if you deduct actual expenses in the first year, you can never use the IRS standard mileage rate.

Example

In 2019, you buy a van and deduct depreciation and actual expenses for that year. You can never use the IRS standard mileage rate and will have to continue deducting actual costs for as long as you use the van for business.

Recordkeeping Requirements

In order to deduct the business use of your vehicle, you must keep specific records documenting business driving. When you complete Schedule C (Part IV, Information on Your Vehicle), in addition to listing your mileage, whether your vehicle was available for personal use in off-duty hours, and whether you have another vehicle available for personal use, you are asked two questions related to recordkeeping:

- Do you have evidence to support your deduction?

- If yes, is this evidence written?

Because you sign your return under penalty of perjury, declaring all of the information in the return to be accurate and correct, you don't want to lie on your tax return or falsify records. The IRS can usually detect a fabricated car log created when a taxpayer becomes subject to an audit.

Under tax rules, the records related to business driving must show:

- The cost of the vehicle and any improvements (unless you rely on the IRS standard mileage rate)

- The mileage for each business use as well as the total miles for the year

- The date of the vehicle use for business

- The business destination

- The purpose of the trip

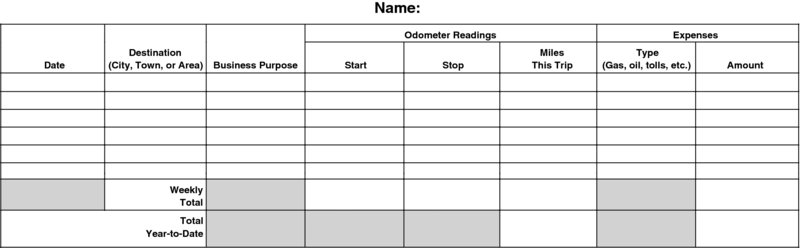

You can use a log similar to the sample log found in Table 5.2 for your recordkeeping. It provides space to enter all of the required elements for your record.

Did you know …

Simply noting your odometer on January 1 and December 31 each year goes a long way in helping you keep the necessary records of your business driving. Remember you have to enter on Schedule C that you have records and they are written records. Put this activity on your to-do list for these dates.

Strategies for Recordkeeping

Recordkeeping isn't fun, but it's a necessary activity if you want to claim the maximum deduction to which you are entitled. Fortunately, there are some ways to simplify this activity.

- Use apps on your smartphone or tablet. There are numerous apps for tracking vehicle mileage. Some are free; some have a modest cost (which is tax deductible). They work off a GPS to track each trip. Explore the apps available for your device and choose the one that you're most likely to use consistently to meet your tax-recordkeeping burden.

Table 5.2 Sample Daily Business Mileage and Expense Log

Source: IRS Publication 463.

- Use sampling. Instead of keeping meticulous records for the entire year, you're allowed to do this for a certain period and then extrapolate the mileage for the full year. For example, if you keep good records for the first three months of the year and you expect your business driving to be fairly constant for the balance of the year, you can simply multiply the miles you drive in the first quarter by four to find your mileage for the year. Alternatively, you can track driving in the first week of every month and then extrapolate for the year, provided that your driving is fairly constant throughout the month.

Buy or Lease?

From a tax perspective, it doesn't usually make a lot of difference. As you have seen, you can use the same standard mileage rate to deduct your business driving whether you own or lease the vehicle.

However, from a financial perspective leasing may enable you to drive a more expensive vehicle than you could if you buy it. Before you make any decision, understand the costs and obligations of a lease agreement and whether this arrangement is suitable for you. For example, leasing may not make financial sense if you put on a lot of miles each year; leases typically limit annual mileage to 15,000 and impose substantial fees for excess mileage.

Getting Out of a Vehicle Lease

If you already leased a vehicle but it no longer suits your needs (e.g., you leased a small car but now need a van for your business), understand how to escape your lease obligation.

- Return the car and pay off the lease. This is the most costly way to end the lease. Costs may even be higher than the total remaining lease payments because the leasing company may tack on a termination fee and even penalties.

- Transfer the lease. If you know someone who wants the car and is willing to pick up the lease payment obligation, this option doesn't cost you a thing and is usually your best way out. However, to do this legally, the leasing company probably has to approve the assignment of the lease (i.e., get approval from the leasing company and make it official). If you don't know someone but still want to transfer the lease, there are online options to find willing parties, such as LeaseTrader.com and Swapalease.com.

- Trade in the old car for a new one. The dealer may cut you an attractive lease if you are stepping up to a higher-priced vehicle. This arrangement usually works well if you are nearing the end of your current lease; the dealer picks up the remaining lease payments. However, if there is still quite some time remaining on the original lease, the costs that the dealer has not recouped will likely be rolled over into the new lease. In effect, you're paying one way or the other.

- Buy the vehicle. Depending on the model you've leased, it could make sense for you to buy it and then resell it. The lease typically specifies the buyout cost. Check the market value of the car to compare it to the buyout cost. If the buyout is less than the car's value in the Kelley Blue Book, this option could make sense for you. However, be prepared to sell the car, which usually is not hassle-free.

- Walk away. If you stop making lease payments, the car will be repossessed by the dealer. While this option may be a cash-flow dream, it is a credit-rating nightmare. This damage to your credit rating not only impacts your ability to obtain a car lease in the future (or at least impacts what you'll pay), but also impairs future borrowing, including bank loans, mortgages, and lines of credit for your business.

Local Transportation

Depending on where you live, you may not necessarily use a car to get around. You may rely on various modes of local transportation, including buses, trains, taxis and ride-sharing services, and other car services. Whether your fare is tax deductible depends on the purpose of the trip. As explained earlier, commuting costs are not deductible. Only the costs of business-related transportation can be deducted, regardless of the mode of transportation.

The same recordkeeping rules applicable to business use of your vehicle (other than mileage) apply to substantiating local transportation costs. Thus, note the amount of the expense, the time, the destination, and the business purpose of the trip.

Did you know …

You don't have to retain a receipt if the expense is no more than $75, but getting one wouldn't hurt. Today, many taxis are equipped to issue receipts.

Business Meals

If you take a customer or other business associate to the theater or a sporting event, you cannot deduct the cost of tickets. No deduction is allowed for entertainment costs. But different rules apply to business meals.

Whether you're wining and dining a customer, vendor, or other business associate at a fancy restaurant, or simply meeting a business associate for breakfast at a local diner, you may be able to deduct half of the bill as a business expense. Despite the fact that the meal expense is solely for business, the tax law generally limits the deduction to 50% of the cost for you and your business guest.

Did you know …

As a self-employed person, you can deduct 100% of your expenses if you meet all of the following conditions:

- You have expenses as an independent contractor.

- Your customer or client reimburses you for these expenses or gives you an allowance for them.

- You substantiate your expenses to your customer or client.

If you meet these conditions, then you get to deduct all of the expenses while your customer or client is subject to the 50% limit. Consider this opportunity when you negotiate a contract or agreement with customers so that you can obtain the 100% deduction.

Special Rule for Those in the Transportation Industry

Do you own your own long hauler? If you're subject to the “hours-of-service” limits from the Department of Transportation (DOT), then the percentage of your meals that is deductible becomes 80%, rather than the usual 50%. You can find a summary of the regulations on hours-of-service limits from the DOT at www.fmcsa.dot.gov/rules-regulations/topics/hos/index.htm.

Business Meals

Meals are rather easy to nail down as deductible expenses. All you need to show is that there is a business reason for the meal. The cost cannot be lavish or extravagant, which is all relative to your business.

Meals can even take place in your home and be treated as a deductible business expense. However, check your guest list before you take a deduction. If the attendees are primarily members of your family, friends, or neighbors, the meal probably won't be viewed as business, but rather personal. Don't try to deduct the cost of having businesspeople attend your personal social events, such as weddings, bar mitzvahs, and birthday parties. Since the event is personal, all of the cost is, too. Similarly, don't try to create deductions through reciprocal meals, where you pay for an associate one day and she pays the next. Unless there's real business going on and you can prove it if the IRS questions your return, pay for yourself and let your associate do the same!

Special Rules for Meals at Entertainment Events

While you can't deduct the cost of tickets at an entertainment event, you may be able to deduct food and beverages there. To do so, you must show:

- The expense is not lavish or extravagant under the circumstances

- You (or your employee) were present when the food and beverages were furnished

- The food and beverages are provided to a current or potential business customer, client, consultant, or similar business contact, and

- The food and beverages are separately billed from the entertainment activity.

Example

You take a customer to a baseball game. You buy the tickets and pay for hot dogs and drinks. You can't deduct the cost of the tickets, but you can deduct 50% of the cost of the food and beverages (assuming you substantiate this).

Recordkeeping Requirements

For business meals, keep track of each separate expense, the date of the meal, the place of the meal, and the business purpose for the expense (e.g., a business discussion or meeting, a transaction, or negotiation).

Per Diem Rates for Meals

Instead of tracking your actual meal costs while you are away from home on business, you can rely on a government-set per diem rate. The rate covers both meals and incidental expenses. The rate can change from year to year and the rate you use depends on whether the travel was within the continental United States (CONUS) or in Alaska, Hawaii, or other U.S. areas (OCONUS).

Just to give you some idea of what these rates are, for October 1, 2019, through September 30, 2020, the standard rate for meals and incidental costs is $55. The rates vary with locality. Higher rates apply in certain locations and at certain times of the year.

You can find current rates, which you can search by Zip code, at the General Services Administration at www.gsa.gov and click on “per diem rates.”

Did you know …

As a self-employed individual, you cannot use per diem rates for lodging. You'll need to keep track of your actual lodging costs on out-of-town trips.

Business Travel

Business these days isn't confined to any particular area, and travel can help you broaden your customer base and business opportunities. While most of your work may take place within the general vicinity of home, there may be times you need to travel to other cities or destinations.

If you have to be away from home on business, you can deduct your travel-related costs. These include:

- Transportation to get to your business destination. Travel can be by plane (including added baggage fees), train, bus, or car from your home to your destination and back again.

Example

You are based in Philadelphia but must meet a client in Atlanta. You can deduct the cost of a car service to take you to the airport, the cost of plane fare, and the cost of a taxi from the Atlanta airport to your hotel (and similar costs for the return trip).

- Local transportation. You can deduct fares to get from your motel/hotel to your business destination, such as a customer's office, and back again. The same local transportation within your home area qualifies for a deduction when you're away from home on business.

- Accommodations. You can deduct the full cost of motel/hotel stays on business. The fact that your significant other accompanies you does not prevent you from taking the write-off as long as the lodging cost for two is the same as for one.

- Meals. While you can't deduct the costs of meals you eat alone while in your home area, even if you have to eat out because of business, you can deduct your own costs when you're on the road. However, only 50% of the cost is tax deductible.

- Incidental costs. Dry cleaning and laundry services, using business services in a hotel, and other incidental costs are fully deductible as part of your travel expenses.

Part Business, Part Pleasure Trips

You can combine business with pleasure and still get maximum tax relief if you know the rules. You can deduct the cost of travel, such as airfare, on a trip within the United States as long as the primary purpose of the trip is for business. There's no set ratio of business to personal days that must be met to satisfy this requirement. As long as you can show that you would not have made the trip but for the business reason, then you probably can deduct all of the airfare. If you spend the majority of days on business, this helps to prove the primary purpose of the trip was business.

Personal days are those on which you sightsee, visit with family or friends, golf, go shopping, fish, or otherwise relax. The cost of lodging and meals on these days is not deductible. A Saturday stayover to obtain a lower airfare is treated as a business day even though you spend it in personal pursuits. The cost of lodging and meals (up to 50%) on the extra day or days is deductible.

If you travel abroad, different rules apply to determine whether you can treat airfare as fully deductible on a trip that combines business with pleasure. The rules can be found in IRS Publication 463 and in J.K. Lasser's Small Business Taxes.

Recordkeeping Requirements for Business Travel

In order to deduct the costs of business travel, you must keep specific records documenting business travel. You typically need a receipt for each expense as well as certain documentary evidence that you create.

The documentary records must show:

- Amount. The cost of each separate expense for travel, lodging, meals, and incidental expenses. Costs in each category, such as taxis, fees, and tips, can be totaled.

- Time. The dates you left and returned for each trip. Also note the number of days you spent on business during your trip.

- Place or description. The destination or area of travel, which means the name of the city, town, or other destination.

- Business purpose. The business reason for the trip, which is the business benefit to be gained or expected to be gained from making the trip.

Did you know …

You don't need to keep receipts for any travel or transportation expense under $75 other than for lodging. So, if you stay in a Motel 6 for $49 per night for one night while on business, you need a receipt for the room charges.

Strategies for Recordkeeping

Again, technology can go a long way in helping you meet substantiation requirements in the tax law. You can use:

- Apps for your mobile device to track your expenses and include all of the required information

- Scanners (desktop or mobile apps) to retain receipts in a handy electronic format

Did you know …

If you fail to keep required books and records, all is not necessarily lost. You may be able to rely on the Cohan Rule to estimate your travel expenses. Named after the noted songwriter/showman George M. Cohan, who didn't have records for his travel and entertainment costs (entertainment costs were deductible prior to 2018), the rule is an approximation that may be used by a court. The Cohan Rule is only a last resort for claiming unsubstantiated travel expenses. You have to fight the IRS and then go to court and argue your case, all of which costs you time and money, and may not be worth the effort relative to the amount of the deduction you seek.

Business Gifts

Someone you do business with, a customer or client, a vendor, or other business associate, may have a life event, such as a wedding or birth of a child, that leads you to give a gift. Because the person has a business relationship with you, the gift may be a tax-deductible one. However, the most you can deduct for a gift to a specific person each year is limited to $25 (the same limit that's been in place since 1962).

The $25 limit does not include the cost of shipping. Usually, your shipping costs for the year will fall within their own category, so whether you ship a business gift or business cards you've designed for a customer, the costs will fall within a single entry in your books.

Recordkeeping for Gifts

Even though the amount of the deduction for business gifts is modest, you still have a strict recordkeeping obligation. In addition to a receipt for the cost of the gift or a statement showing a credit card charge or electronic payment for the gift, it's vital that you record information related to the gift in the manner required by law. The records must show:

- The cost of the gift

- The date of the gift

- A description of the gift

- The business purpose of the gift

- The relationship of the recipient to your business

Strategies for Saving on Travel Costs

The costs of travel can mount up if you're not watchful of these expenses. This is especially true when the cost of gasoline rises, as it does from time to time. While tax deductions for travel costs effectively help to reduce your outlays, it's even better to minimize your expenses. There are some helpful strategies for this purpose.

Use Low-Cost Travel

You can save on airfare, hotels, and other travel costs by going online yourself. Check out:

- Discount sites, such as Priceline.com

- Online travel agencies, such as Expedia, Orbitz, or Travelocity

- Metasearch engines, such as Kayak and Booking.com

However, these sites may not give you access to small lower-cost airlines, such as JetBlue and Spirit. You may prefer to save yourself time and ensure that you make the best travel arrangements at a favorable price by using a travel professional, such as a travel agent, or if you do extensive travel, a travel concierge. You pay for the service, but save on your travel costs and have help in rebooking when flights are canceled or other travel disasters arise.

Use Technology in Place of Travel

While there are certainly instances where travel is unavoidable and you must see people in person, in many situations you may be able to use virtual meetings instead. Consider using such free or low-cost tools as GoToMeeting, Skype, and Zoom to connect visually and with sound to customers and other business associates who are not conveniently near you.

What's Ahead

Just as almost every self-employed individual has some vehicle, travel, meals, and gift costs each year, you're likely to have expenses related to your office. Whether your office is part of your home, or in a strip mall, office building, garage, or other location, you have utilities, supplies, and other costs each month. How do you handle them from a tax perspective? What is the “home office deduction” everyone talks about? You'll find out in Chapter 6.

Chapter Takeaways

- You can deduct costs related to business use of your personal vehicle as long as you maintain sufficient records of business driving.

- The cost of business meals is usually only 50% deductible.

- Most travel-related costs are deductible as long as you maintain required records.

- The deduction for business gifts is capped at $25 per recipient per year.

- Even though write-offs are helpful, look for ways to save on travel costs, which is an even better way to keep money in your pocket.