CHAPTER 3

Using Schedule C

As a self-employed person without any co-owners, your annual business tax return is not a standalone filing. Instead, your business return is part of your personal income tax return.

Who are Schedule C filers? According to recent IRS statistics, the largest sectors in terms of the number of returns are the professional, scientific, and technical services sectors. Other sectors include construction, merchant wholesalers, retail, and the performing arts. A growing sector is taxis, limousines, Uber, Lyft, and other ride-sharing services. Whatever sector your business activities fall in, there's some basic information you should know about Schedule C.

Tax Filing on Schedule C

Partnerships, multi-owner limited liability companies, and corporations (both C and S) have their own separate tax returns. These returns are filed independently from the returns of their owners. But as a self-employed person, you must file Schedule C, Profit or Loss from Business with your personal income tax return, Form 1040 or 1040-SR. If you have formed a limited liability company but are the only owner (technically called a member), for tax purposes you are a “disregarded entity,” which means you also file Schedule C with your Form 1040 or 1040-SR. (As an LLC, you can opt to be taxed as a corporation, but this isn't the usual thing and is not discussed further here.)

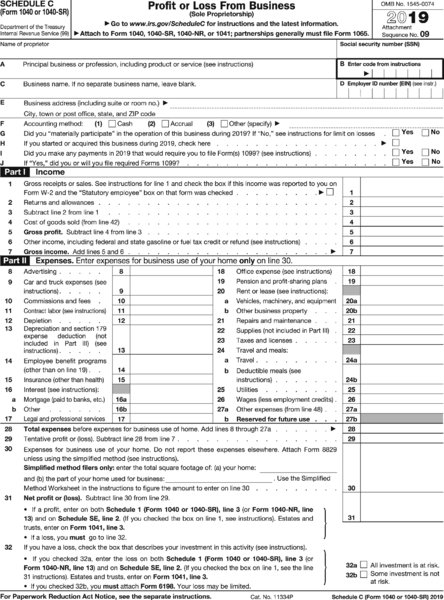

Schedule C paints a picture of your business activities, including your income and expenses. You can see the 2019 version of these schedules. Schedule C is in Figure 3.1. Do not use this for filing your return, but refer to it during the discussion that follows in this chapter and throughout the book to better understand how entries are made on your business return. Of course, using return preparation software or a tax pro means the entries at tax time will flow to the proper part of the form; this is just for information purposes. And subsequent versions of these forms may differ, but the general information likely will continue to apply.

Figure 3.1 Schedule C.

Entries on Schedule C

Before you enter any of your income and expenses, you must share certain information about yourself and your business.

The basic information required on Schedule C includes:

- Your name and address. If you use a fictitious business name, include it as well. Say you are a bookkeeper doing business as Sunshine Bookkeeping Service. Since you are not doing business under your personal name but rather under a fictitious business name, list it here as well. Note: Check with your city, state, or county to determine whether you have to file a DBA (“doing business as”) form (see Chapter 2). This onetime process is easy and usually entails only a modest filing fee.

- Your tax identification number (TIN). Many self-employed people use their Social Security number for this purpose, but you can or may be required to have an employer identification number (EIN) (see Chapter 2).

- Your business code. This is a six-digit code from the North American Industry Classification System (NAICS) that applies to the industry (and segment and category of that industry) you fall within. For example, if you are a freelance writer, your code is 711510 for independent artists, writers, and performers. You fall within the segment of performing arts and related industries, which is within the industry of arts, entertainment, and recreation. You can find a list of the NAICS codes in the instructions to Schedule C.

Did you know …

The same code is also used for government contracting purposes. By law, the federal government is supposed to award 23% of its contracting dollars to small business contractors. Contract opportunities are tied to the NAICS codes, so make sure to use the code that best describes your business activity.

- Your accounting method. This is the reporting method you use for your income and expenses (see Chapter 2).

- Your business participation. You must indicate whether you are active or passive in the business. If you're the only one running things, you are active and considered to “materially participate” in the business. If you're the silent investor with a manager who is in charge of day-to-day activities, then your participation is passive. There are some specific tests used to determine material participation for certain tax rules when its not clear one way or the other.

- Startup. You must also indicate whether this is your first year, as a startup or as the owner of a business you've just acquired.

- Your 1099 reporting. You must indicate whether you're required to file Form 1099-MISC (Form 1099-NEC after 2019) for payments of $600 or more your business made to another self-employed person, and whether in fact you filed the form(s) as required. For example, if you use a virtual assistant who is self-employed and pay that person $2,000 a month in 2019, you'll have to report $24,000 on Form 1099-MISC and indicate on your Schedule C that you've done this.

Schedule C is divided into five parts. Part I of Schedule C is for reporting your income (explained in Chapter 3). Part II allows you to list your expenses. If you don't see the appropriate line or you just need more space, use Part V to enter your other deductible expenses. These are explained in Chapters 4 through 7. Part III of Schedule C is used only by businesses that maintain inventory, which is explained briefly in Chapter 4. Part IV is where you enter information about your personal car, van, or truck if you use a vehicle for business.

Multiple Businesses

If you run two or more sole proprietorships, you must file separate Schedule Cs for each business.

Example

You are a freelance writer and also sell your handcrafted jewelry on Etsy. You need two Schedule Cs.

Spousal Partnerships

If you and your spouse each “materially participate” as the only members of a jointly owned and operated business, and you file a joint return for the tax year, you can both elect to be treated as a qualified joint venture instead of a partnership for the tax year. Making this election probably won't save you any taxes but will allow you to avoid the complexity of Form 1065, while still giving each spouse credit for Social Security earnings on which retirement benefits are based.

Once you make this election, you divide all items of income, gain, loss, deduction, and credit attributable to the business between you and your spouse in accordance with your respective interests in the venture. If you're 50–50 owners, then simply divide every item in half. Each of you must file a separate Schedule C and a separate Schedule SE for self-employment taxes (see Chapter 11), all of which is attached to your joint Form 1040 or 1040-SR.

Other Forms

In addition to Schedule C, you may have to complete other forms or schedules to supplement the information on Schedule C. Common forms you may also need are:

- Form 3800, General Business Credit. Use this form if you claim business credits (see Chapter 9).

- Form 4562, Depreciation and Amortization. Use this form if you buy equipment or machine used in your business, such as a drafting table for your engineering work.

- Form 4684, Casualties and Thefts. Use this form if your business suffered a casualty or theft, causing you loss of property that wasn't covered by insurance.

- Form 4797, Sales of Business Property. Use this form if you've sold business property or the use of listed property drops below 50% (listed property is explained in Chapter 5).

- Form 8829, Expenses for Business Use of Your Home. Use this form if you work from your residence and figure a home office deduction using the actual expense method (explained in Chaper 6).

- Form 8824, Like-Kind Exchanges. Use this form if you've exchanged business real property for other business real property that is of like kind, such as one office building for another.

When, Where, and How to File

Schedule C is due at the time you file your Form 1040 or 1040-SR. The filing deadline is April 15 following your business year. For example, file your 2019 return by April 15, 2020. If the filing deadline falls on a Saturday, Sunday, or legal holiday, the filing deadline becomes the next business day.

Filing Extension

If, for any reason, you need more time to file, just request a filing extension. The six-month extension is obtained by filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. You can file for an extension electronically or by snail mail.

You don't have to specify your reason for making an extension request, but you must estimate the taxes you expect to owe on your return. Pay as much of this estimate as possible to minimize or avoid underpayment penalties. (Paying estimated taxes throughout the year, which avoids the need to make a payment with an extension request, is explained in Chapter 9.)

Where to File

Your return is filed with the IRS service center for the state in which you live. If you file a paper return, the IRS service centers are listed in the instructions to Form 1040 or 1040-SR. If you file electronically, as more than 90% of taxpayers do, your return automatically goes to the appropriate service center based on your address.

How to File

Of course, you're allowed to prepare the return by hand and send it by mail to the IRS. However, because most small business owners use paid preparers or their own computers to prepare their returns, it's a good idea to file electronically, called e-file. The IRS lists these benefits for e-filing:

- Accuracy. It reduces the chances you'll receive an error notice from the IRS.

- Security. Privacy and security are assured.

- Proof of acceptance. You know almost immediately that your return has been accepted for filing.

- Simplicity. You can e-file your federal and state returns together.

- Faster refund. If the government owes you money, you'll receive it faster than with a paper-filed return.

Paying Your Taxes

This topic is discussed in Chapter 9.

What's Ahead

Now that you know the basics about Schedule C and how to file, it's time to get to the details of reporting your business activities. What income do you have to report and when, where, and how? This information is discussed in Chapter 4.

Chapter Takeaways

- You file Schedule C to report your business income and expenses.

- You must enter certain information about your business on Schedule C.

- You file Schedule C along with your personal income tax return, Form 1040 or 1040-SR.

- Schedule C, along with your return, is due April 15 unless you obtain a filing extension.

- Filing electronically has many advantages over sending a paper return by snail mail.