Chapter 4d

Accounting Process – From Journal to Trial Balance

LEARNING OBJECTIVES

At the end of the chapter, you would be able to understand

What a Trial Balance Really Means

Objectives and Salient Features of a Trial Balance

Methods of Preparation of Trial Balance. Preparation of a Trial Balance by Applying “Balances Method”

Concept of Errors – Kinds of Errors – Classification of Errors – Rectification of Errors

Various Steps Involved in Locating the Errors in a Trial Balance

Meaning of Suspense Account and Its Accounting Treatment

To Record Various Transactions (Passing Entries into Journal), Classify These Trans-actions Under Various Heads of Account (Posting to Ledger) and Balancing Them, Some Important Subsidiary Books and Procedure of Recording in Such Books of Original Entry and Finally to Prepare Trial Balance. [This is the first part of Accounting Process, which starts from the recording of transactions and ends with the preparation of Trial Balance.]

In the previous chapters, we have learnt how to record various transactions (passing entries into journal), classify these transactions under various heads of account (posting to ledger) and balancing them and some important subsidiary books and procedure of recording in such books of original entry. The next step in the process of accounting is the preparation of a statement to check the arithmetical accuracy of transactions recorded so far. This statement is known as “Trial Balance.”

OBJECTIVE 1: MEANING OF TRIAL BALANCE

Trial Balance is a statement, which shows debit balances and credit balances of all the accounts in the ledger. As per the rules of double entry, every debit must have a corresponding credit. Hence, the total of all debit entries must be equal to that of all credit entries in the ledger. The total of the debit balances and credit balances must be equal. In case any difference arises, that is, the totals of debit balances and credit balances do not tally, the correctness of the balances brought forward from the respective accounts must be checked by preparing this statement. This process is known as preparation of a Trial Balance. “Trial Balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books.”

OBJECTIVE 2: OBJECTIVES AND SALIENT FEATURES OF TRIAL BALANCE

2.1 Objectives of a Trial Balance

The main objectives in the preparation of a Trial Balance are:

- to check the arithmetical accuracy of the ledger account,

- to locate the errors and rectify them,

- to provide basis for the preparation of final accounts,

- to serve as a ready reckoner (it provides a summary of all transactions during an accounting period at one place, i.e. this statement).

2.2 Salient Features of a Trial Balance

- It is only a statement. It is not an account. It is simply a list of balances of all accounts.

- It is prepared on a particular date.

- It may be prepared at any time during the year.

- It is one method of checking the accuracy of transactions.

- It can be prepared only by the firms, which adopt double entry system.

- Some errors may not be detected.

OBJECTIVE 3: METHODS OF PREPARATION OF A TRIAL BALANCE

A Trial Balance can be prepared in the following three ways:

- Totals Method

- Balances Method

- Totals cum Balances Method

3.1 Totals Method

Under this method, each side in the ledger (debit and credit) is totalled. Then they are recorded in the Trial Balance in respective columns. The total of the debit column of Trial Balance and the total of credit column of Trial Balance should be equal. But this method is not widely used.

3.2 Balances Method

This is the method, which is used widely in the preparation of a Trial Balance. Trial Balance is prepared by recording the balances of all ledger accounts. Then debit column and credit column of the Trial Balance is totalled. As the balance summarises the net effect of all transactions relating to a particular account, balances are taken as a base for preparing a Trial Balance. Further, it helps in the preparation of final accounts.

3.3 Totals cum Balances Method

Under this method, the Trial Balance is prepared by combining the above methods. This method is also not adopted widely.

In practice, Balances Method is widely used. Trial Balances are prepared with debit and credit balances of various accounts in the ledger. Under this method, taking into account of balances in Cash Book also is followed.

Format of a Trial Balance

Trial Balance of ………………… as on…………………

Illustration: 1

The following balances were extracted from the ledger of Vas Dev on Mar 31, 2009. Prepare a Trial Balance as on that date in the proper form.

|

|

Rs |

|

Salaries |

72,640 |

|

Sales |

3,47,000 |

|

Plant and machinery |

68,600 |

|

Commission paid |

3,760 |

|

Purchases |

2,89,340 |

|

Stock on 1.4.2009 |

22,200 |

|

Repairs |

3,340 |

|

Sundry expenses |

920 |

|

Sundry debtors |

2,860 |

|

Returns inward |

2,000 |

|

Returns outward |

800 |

|

Discount allowed |

2,300 |

|

Rent and rates |

6,440 |

|

Sundry creditors |

28,520 |

|

Carriage inward |

480 |

|

Travelling expenses |

5,260 |

|

Drawings |

7,000 |

|

Investments |

12,000 |

|

Capital 1.4.2009 |

1,25,000 |

|

Cash at Bank |

2,180 |

Solution: Keep in mind, the general rules and classify and then enter in the Trial Balance in its format.

Step 1:

Debit balances: Assets, Drawings, Debtors, Losses and Expenses

Credit balances: Liabilities, Capital, Creditors, Gains and Incomes

Each item is explained here, why it is classified as Debit balance or Credit balance.

|

1. Salaries – Nominal A/c – Expense |

Dr. Balance |

|

2. Sales – Real A/c – Goods |

Cr. Balance |

|

3. Plant and Machinery – Real A/c – Assets |

Dr. Balance |

|

4. Commission paid – Nominal A/c – Expense |

Dr. Balance |

|

5. Purchases – Real A/c – Goods |

Dr. Balance |

|

6. Stock – Real A/c – Goods |

Dr. Balance |

|

7. Repairs – Nominal A/c – Expense |

Dr. Balance |

|

8. Sundry Expenses – Nominal A/c – Expense |

Dr. Balance |

|

9. Returns Inward – Real A/c – Goods |

Dr. Balance |

|

10. Returns Outward – Real A/c – Goods |

Cr. Balance |

|

11. Discount allowed – Nominal A/c – Loss |

Dr. Balance |

|

12. Rent and rates – Nominal A/c – Expense |

Dr. Balance |

|

13. Sundry creditors – Personal A/c – Supplier |

Cr. Balance |

|

14. Sundry debtors – Personal A/c – Customer |

Dr. Balance |

|

15. Carriage inwards – Nominal A/c – Expenses |

Dr. Balance |

|

16. Travelling expenses – Nominal A/c – Expenses |

Dr. Balance |

|

17. Drawings – Personal A/c – Proprietor (owner) |

Dr. Balance |

|

Dr. Balance |

|

|

19. Capital 1.4.2009 – Personal A/c – Owner |

Cr. Balance |

|

20. Cash at Bank – Real A/c – Asset |

Dr. Balance |

| Step 2: | For any item (of account or transaction), apply the Rules of Debit and Credit and thereby determine whether it is a Dr. balance or Cr. balance. |

| Step 3: | Now, draw the format of a Trial Balance and record as it is classified in the columns of debit balance and credit balance, respectively. |

| Step 4: | Finally, total both the debit and credit columns separately and ascertain both the totals should tally. |

Trial Balance of Vas Dev as at Mar 31, 2009

N.B. Items shown as on 1.4.2009 have to be taken into account as the closing balance for the accounting period is included in the Trial Balance at 31.3.2009.

Closing Balance = Opening Balance of the next accounting year.

OBJECTIVE 4: CONCEPT OF ERRORS

The preparation of a Trial Balance is to ensure accuracy. A tallied Trial Balance ensures only arithmetic accuracy but not accounting accuracies. A tallied Trial Balance reveals that the posting to the ledger is arithmetically correct. It does not guarantee the entry itself is in accordance with the principles of accountancy. As such, there may be an agreement of Trial Balance (i.e., the total of debit balance and credit balance are equal) without disclosing such defects or errors. In some other circumstances, the two totals will not tally explicitly. These errors must be detected at an early stage, to present a true final account.

One has to be careful to locate such errors and rectify the errors once detected. All the errors may be classified as follows:

OBJECTIVE 5: KINDS OF ERRORS

5.1 Errors of Principle

Transactions are recorded as per Generally Accepted Accounting Principles (GAAP). In case, the principles are violated or ignored, errors of principle take place in such transactions, which will not affect the Trial Balance.

Example: Credit sale of land (asset) recorded in Sales Book.

This is an error of principle because credit sale of assets is not recorded in subsidiary book. It has to be recorded in Journal Proper.

Amount spent on additions to fixed assets has to be treated as capital expenditure and not of revenue nature.

Example: Spent Rs 15,000 for additional accessory to an existing machine. Recording as Repairs A/c debit, is an accounting error of principle. Instead, Machinery A/c is to be debited. Such an error will not affect trial balance but will affect the final accounts due to this wrong classification of capital expenditure and revenue expenditure.

5.2 Clerical Errors

These errors occur due to mistakes made by the concerned accounting clerks, which can be further classified into the following categories:

5.2.1 Errors of Omission

When a transaction is omitted in the books of account, this type of error occur. This may be further classified as:

5.2.1.1 Error of Complete Omission: When a transaction is totally omitted for recording in the books of accounts, this type of error arises.

Example: Credit sale of Rs 10,000 to Anand. If this transaction is omitted entirely, such error is called error of complete omission. This error will not affect the Trial Balance.

5.2.1.2 Error of Partial Omission: When only one aspect of the transaction is recorded, this type of error arises. In the above example, one aspect, credit sales, is recorded duly in Sales A/c, but the aspect, Anand’s Account, is omitted while recording, this error of partial omission arises. This will affect the Trial Balance.

5.2.2 Errors of Commission

This type of error occurs due to various factors such as wrong recording, wrong posting, wrong balancing and the like. This may further be classified as follows:

5.2.2.1 Error of Recording: This error arises when a transaction is wrongly recorded in the books of original entry.

Example: Credit purchase of goods from Renu for Rs 17,500 recorded in the books as Rs 15,700.

5.2.2.2 Error of Posting: This error occurs when information recorded in the books of original entry is entered wrongly in the ledger. This error may arise due to:

- Recording the right amount in the wrong side of correct account.

- Recording the right amount in the right side of wrong account.

- Entering the wrong amount in the right side of correct account.

- Entering the wrong amount in the wrong side of correct account.

- Entering the wrong amount in the right side of wrong account.

- Entering wrong amount in the wrong side of wrong account.

5.2.2.3 Error of Casting: When a mistake is committed while totalling in a subsidiary book, this error arises.

Example: If the total is Rs 11,000 in a subsidiary book, it may be wrongly totalled and entered as Rs 16,000. This is an error of overcasting. If it is wrongly totalled as Rs 10,000, it is an error of undercasting.

5.2.2.4 Error of Carrying Forward: When a total of one page is written wrongly on the next page, this error occurs.

Example: Total of Cash Book in page number 151 of the ledger is Rs 1,01,000. While carrying forward to the next page 152, if it is recorded as Rs 1,10,000, this error of carrying forward arises.

5.3 Compensating Errors

When two or more errors are committed in such a way that the net effect of these errors on the debits and credits of accounts is NIL, these errors arise, which are called “Compensating Errors.”

Example: If purchases book is overcast, say, by Rs 6,000, which results in excess debit of Rs 6,000 in Purchases Account and if the Sales Returns Book is undercast by the same amount of Rs 6,000, which results in shortage of debit in Sales Returns Account. These type of errors compensate each other. One excess of Rs 6000 is set off by the other deficit (of the same amount Rs 6,000). The net effect is nil. Hence, these types of errors do not affect the Trial Balance.

OBJECTIVE 6: CLASSIFICATION OF ERRORS (BASED ON THE IMPACT OF ERRORS ON TRIAL BALANCE)

Net effect of these errors in Trial Balance has to be considered while preparing a Trial Balance, so as to present an accurate Trial Balance for preparing final accounts. Based on the impact of the errors on Trial Balance, errors may be classified as follows:

Illustration: 2

Mention the type of error involved in the transactions and its impact on the agreement of Trial Balance.

- The Sales Book is cast short by Rs 6,000.

- The Sales Returns Book is overcast by Rs 3,000.

- The Purchase Book is overcast by Rs 2,500.

- The Purchases Return Book is overcast by Rs 1,600.

- Goods returned by Sharma for Rs 2,200 were not entered.

- Goods sold to Raj for Rs 7,000 has been debited to Ravi A/c.

- Credit sale of Rs 11,000 to Gupta was entered as Rs 10,100.

- A purchase of machine has been passed through the Purchases Book.

- A credit purchase from Renu for Rs 25,000 was debited to Venu A/c from Purchases book.

- Cash received for commission Rs 1,008 was posted to Commission Account as Rs 1,080.

- The monthly discount column on the debit side of the Cash Book Rs 3,000 was credited to Discount Allowed Account.

- Depreciation on machinery Rs 1,000 is not posted to Depreciation Account.

- Life Insurance Premium Rs 2,640 paid on behalf of the proprietor by a cheque was debited to General Expenses A/c.

- The total of the discount column in the Cash Book on the debit side was Rs 2,302 on page 56, which was carried forward to the page 57 as Rs 2,032.

- An amount of Rs 1,600 received from Shweta was entered in the credit side of her account.

Solution

- This is an error of casting. Sales Book is given Rs 6,000 less credit. So the Trial Balance (credit side) will be less by Rs 6,000. The Trial Balance will not tally.

- This is an error of casting. Sales Return Book is given over debit of Rs 3,000. Debit balance will be higher. This will affect the Trial Balance to the extent of Rs 3,000. The total affects the Trial Balance to the extent of Rs 3,000. The total column in the debit balance will be Rs 3,000 more than credit balance.

- This is an error of casting. Purchases Book is given an over debit of Rs 2,500. Hence, the debit balance column total will be Rs 2,500 more than the credit balance in Trial Balance.

- This is an error of casting. Purchases Return Book is given an over credit of Rs 1,600. It will affect the Trial Balance. The total of credit column in Trial Balance is more than the total of debit column by Rs 1,600.

- This is an error of complete omission. As both the aspects are not recorded, Trial Balance will not be affected.

- This is an error of posting. Right amount in the right side of the wrong account. This will not affect the Trial Balance.

- This is an error of recording. Wrong entry in the subsidiary book. The mistake is found in both debit and credit aspects to the same extent (on both sides Rs 10,100 instead of Rs 11,000). The agreement of Trial Balance is not affected.

- This is an error of principle. This will not be disclosed in the Trial Balance and hence no effect on Trial Balance.

- This is an error of recording. The mistake is committed simultaneously affecting both the debit and credit aspects. The agreement of Trial Balance will not be affected.

- This is an error of posting and that too posting of wrong amount. Commission has an excess credit of (Rs 1,080 – Rs 1,008) Rs 72. The total credit balance column will be excess to an extent of Rs 72.

- This is an error of posting. Posted on the wrong side of the account. This amount instead of debiting is credited. As such, the Trial Balance will be affected to an extent of Rs 3,000 × 2 = Rs 6,000.

- Depreciation on machinery Rs 1,000 is not debited to Depreciation Account. As such, the debit side of the Trial Balance will be short by Rs 1,000.

- This is an error of principle. The amount of Rs 2,640 is debited but in a different account. It will not affect the Trial Balance.

- Discount Account is debited in the ledger as Rs 2,032, instead of Rs 2,302. Hence, the credit side of Trial Balance will be short by (Rs 2,302 – Rs 2,032) = Rs 270.

- Shweta’s A/c is given less credit of Rs 1,600. As such, the Trial Balance (credit side less by Rs 1,600) will be affected.

OBJECTIVE 7: RECTIFICATION OF ERRORS

The process of correcting the errors is termed as “Rectification”. From the point of view of rectification, errors may be classified as follows:

- Errors which do not affect the Trial Balance

- Errors which affect the Trial Balance

The errors which do not affect the Trial Balance is due to the fact that errors are committed on both the accounts (double sided errors) in the transaction. This type of error can be rectified by recording a journal entry. The errors which affect the Trial Balance is due to the fact that errors affect one side of an account (single sided error). This type of error cannot be rectified by a single journal entry. This can be rectified by opening a Suspense Account.

Irrespective of the nature, errors arise due to any one of the following positions in one or more accounts:

Position 1: |

Excess debit in one or more accounts: This will be rectified by “crediting” the excess amount to the respective account(s). |

Position 2: |

Short debit in one or more accounts: This has to be rectified by a “further debit” to the respective account(s). |

Position 3: |

Excess credit in one or more accounts: This will be rectified by “debiting” the excess amount to the respective account(s). |

Position 4: |

Short credit in one or more accounts: This will be rectified by a “further credit” to the respective account(s). |

7.1 Rectification of Errors which do not Affect the Trial Balance

As these errors are committed in two more accounts, they can be rectified by recording a journal entry by way of giving the correct debit and credit to the concerned accounts.

Errors of complete omission and errors of principle belong to this category.

Rectification process involves the following steps:

- Cancel the effect of wrong debit or credit by reversing it.

- Restore the effect of correct debit or credit.

Illustration: 3

Rectify the following errors:

- Purchases Book overcast by Rs 1,000

- Purchases Return Book overcast by Rs 100

- Sales Book undercast by Rs 500

- Sales Return Book undercast by Rs 200

Solution

-

Mistake →

Purchases Book

Overcast

↓

↓

Debit

Excess

- Effect → Excess debit

- Rectifi cation → Credit the Purchases A/c

Credit the Purchases Account with Rs 1,000.

-

-

Mistake →

Purchases Return book

Overcast

↓

↓

Credit

Excess

- Effect → Excess credit

- Rectifi cation → Debit the Purchases Return A/c

Debit the Purchases Return A/c with Rs 100.

-

-

Mistake →

Sales Book

Undercast

↓

↓

Credit

Short

- Effect → Shortage in credit

- Rectifi cation → Further credit has to be made

Credit the Sales A/c with Rs 500.

-

-

Mistake →

Sales Return Book

Undercast

↓

↓

Debit

Shortage

- Effect → Shortage in debit

- Rectifi cation → Further debit has to be made

Debit the Sales Return A/c with Rs 200.

-

Illustration: 4

Rectify the following errors:

- The total of the Purchases Book Rs 5,300 on page 28 was carried forward to page 29 as Rs 3,500.

- The total of the Sales Book Rs 6,800 on page 51 was carried forward to page 52 as Rs 8,600.

Solution

-

- Mistake → Carrying forward lower amount in Purchases Book (Rs 5,300 as Rs 3,500)

- Effect → Short debit in Purchases A/c

- Rectification → Debit the Purchases A/c with Rs 1,800 (Rs 5,300 – Rs 3,500)

-

- Mistake → Carrying forward higher amount in Sales Book (Rs 6,800 as Rs 8,600)

- Effect → Excess credit in Sales A/c

- Rectification → Debit the Sales A/c with Rs 1,800 (Rs 8,600 – Rs 6,800)

Illustration: 5

Rectify the following errors:

- Purchases from Antony for Rs 12,500 was omitted (to be posted to the Personal A/c).

- Purchases from Vincent for Rs 25,000 was posted to the debit side of his account.

- Sales to Thomas for Rs 10,700 was posted to his credit side of his account as Rs 10,070.

Solution

-

- Mistake → Antony’s A/c is not recorded. Not credited (error of omission).

- Effect → Shortage credit

- Rectification → Credit Antony’s A/c with the entire amount. Credit Antony’s A/c with Rs 12,500.

-

- Mistake → Credited in Thomas’s A/c (wrong side).

Credited with Rs 10,070 (wrong amount)

- Effect → Double mistake. Side → To be debited. Amount: Add both (Rs 10,700 + Rs 10,070)

- Rectification → Debit Thomas’s A/c with Rs 20,770

- Mistake → Credited in Thomas’s A/c (wrong side).

Illustration: 6 (Rectification by Journal Entry)

Credit Sales to Rahman Rs 1,05,000 were not recorded in the Sales Book. Rectify the error.

Solution

This is an error of complete omission. That means this transaction is not at all recorded.

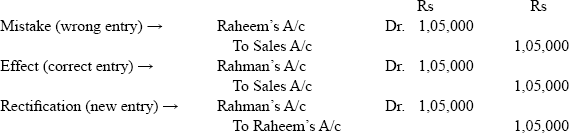

Illustration: 7

Credit Sales to Rahman Rs 1,05,000 were recorded as Rs 10,500 in the Sales Book. Rectify the error.

Solution

This is an error of commission.

Shortage of debit (i.e., Rs 1,05,000 – Rs 10,500 = Rs 94,500), as it is undercast. So, further debit of Rs 94,500 has to be made.

Illustration: 8

Credit Sales to Rahman Rs 10,50,000 were recorded as Rs 15,00,000. Rectify the error.

Solution

This is an error of commission.

[There is an excess debit (Rs 15,00,000 – Rs 10,50,000) Rs 4,50,000. Excess debit in Rahman’s A/c is credited now with that excess amount or excess credit in Sales A/c is now debited.]

Illustration: 9

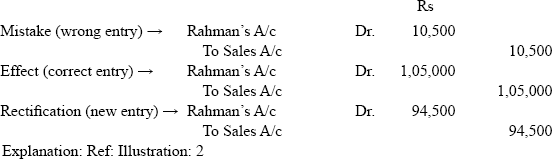

Credit Sales to Rahman Rs 1,05,000 was recorded in the Sales Book but was posted to Raheem’s Account. Rectify the error.

Solution

This is an error of commission.

Recorded correctly in one aspect of transaction: Sales A/c

Recorded wrongly in the second aspect of transaction: Raheem’s A/c

[There is no error in Sales Book (Sales A/c) but Raheem’s A/c is debited instead of Rahman’s A/c. So Raheem’s A/c is to be credited now and Rahman’s A/c is debited.]

SUMMARISED PROCEDURE: For rectifying errors through journal entries.

Step 1: |

First write the entry as it is given in the transaction to find out what the real mistake is. |

Step 2: |

Then enter the correct entry for the given transaction. |

Step 3: |

Compare these two entries to rectify the error and pass the new journal entry for rectification. |

7.2 Rectification of Errors Affecting Trial Balance

The errors that affect only one aspect of account can be rectified by recording a journal entry with an additional entry under the caption “Suspense Account.” As already explained, creation of Suspense Account is a stop-gap arrangement till the error is detected and rectified.

The following procedure is adopted when we use Suspense Account to rectify errors (one sided):

Step 1: |

The account affected due to error is identified. |

Step 2: |

The difference amount (excess or shortage) in the affected account is determined. |

Step 3: |

In case, the difference arises due to “excess debit” or “short credit,” credit the account with the difference. |

Step 4: |

In case, the difference arises due “excess credit” or “short debit,” debit the account with the difference amount (resulted in excess credit or short debit). |

Step 5: |

Journal entry is to be completed with the debit or credit of Suspense Account. |

Illustration: 10

Rectify the following errors:

Credit purchases from Sathyan Rs 50,000 in the following alternative cases

- were not recorded

- were recorded as Rs 25,000

- were recorded as Rs 60,000

- were not posted to his account

- were posted to his account as Rs 5,000

- were posted to Sathish A/c

- were posted to the debit of Sathyan’s A/c

- were posted to the debit of Sathish

- were recorded through Sales book

Solution

The rectified new entry is recorded in the Books of Journal as follows:

Journal

Illustration: 11

Rectify the following errors:

- Cash sales Rs 20,000 were not posted to Sales account

- Cash sales Rs 20,000 were posted as Rs 2,000 in Sales A/c

- Sales Return Book overcast by Rs 3,000

- Depreciation on machinery Rs 700 was not posted

- Depreciation on machinery Rs 700 was not posted to Depreciation A/c

- Goods returned to Krishna Rs 2,500 were recorded through Sales book

Solution

Rectifying Journal Entries

Illustration: 12

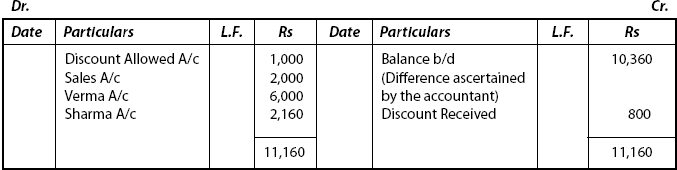

An Accountant could not tally the Trial Balance. The difference of Rs 10,360 was temporarily placed to the credit of Suspense Account to prepare final accounts. The following errors were located:

- Commission of Rs 1,000 paid, was posted twice, once to Discount Allowed Account and once to Commission Account.

- The Purchase Returns Account was undercast by Rs 2,000.

- A credit purchase from Verma of Rs 3,000 entered in Purchases Book, was wrongly debited to his Personal Account.

- A credit sale of Rs 6,200 to Sharma was entered in Sales Book, but posted wrongly to his account as Rs 8,360.

- Discount column of the payments side of the Cash Book was wrongly totalled as Rs 8,800 instead of Rs 8,000.

Pass the necessary rectifying journal entries and prepare Suspense Account to ascertain the difference in the Trial Balance.

Solution

Rectifying Journal Entries

Suspense A/c

OBJECTIVE 8: STEPS TO LOCATE THE ERRORS IN TRIAL BALANCE

In case, when the Trial Balance does not tally, it indicates that there may be some errors in the books of accounts. The following is the procedure adopted generally to locate such errors:

Step 1: |

Re-check the totals of debit and credit columns of the Trial Balance. Thereby ascertain the exact amount of difference in Trial Balance. |

Step 2: |

That difference is divided by “2.” Find out from the Trial Balance, columns having the same amount and, if it appears, note the account pertaining to that amount. Compare the ledger account and Trial Balance. Find out any mistake has been made. |

Step 3: |

If the error is not detected in Step 2, divide the balance amount by “9.” If it is divisible without any remainder, the error is due to transposition of the figures (position of number is misplaced). |

Step 4: |

Even if the error is not detected, check whether the balances of all ledger accounts (including cash and bank balances) are included in Trial Balance. |

Step 5: |

Ensure whether all the opening balances have been correctly brought forward in the current year’s books. |

Step 6: |

If the Trial Balance differences is of a larger amount, compare the Trial Balance of the current accounting period with that of previous year. Account showing a large difference over the figure in the previous Trial Balance is to be re-checked. |

Step 7: |

Amount carried forward from one page to another page is to be verified again. |

Step 8: |

Re-check the balances in each ledger account to ascertain any mistake has been made while recording the balancing figures. |

Step 9: |

Even if the error cannot be detected after following the above steps, hand over the work of re-check to other staff. |

OBJECTIVE 9: MEANING OF SUSPENSE ACCOUNT AND ITS ACCOUNTING TREATMENT

Before preparing final accounts, if it is not possible to detect the errors, the difference in Trial Balance is transferred to a new account called “Suspense Account.” Thereby, the Trial Balance is tallied. This account has been introduced to avoid delay in the preparation of final accounts.

When errors are located, they will be rectified through the Suspense Account and the same will be eliminated. The Suspense Account is recorded without double entry effect because Suspense Account is not a Personal Account, not a Real Account and not even a Nominal Account.

Illustration: 13

The following balances were extracted from the ledger of Mrs. Devi as on Mar 31, 2009. You are required to prepare a Trial Balance as on that date:

|

|

Rs |

|

Capital |

90,000 |

|

Drawings |

3,000 |

|

Purchases |

1,00,000 |

|

Sales |

1,40,000 |

|

Returns inward |

500 |

|

Returns outward |

1,000 |

|

Carriage inward |

1,500 |

|

Carriage outward |

1,000 |

|

Opening stock |

15,000 |

|

Scooter |

20,000 |

|

Salaries |

7,000 |

|

Rent |

3,000 |

|

Taxes |

1,500 |

|

Insurance |

1,200 |

|

Sundry creditors |

9,000 |

|

Sundry debtors |

2,000 |

|

Cash-in-hand |

300 |

|

Cash at Bank |

3,000 |

|

Furniture |

6,500 |

|

Bank overdraft |

20,000 |

|

Land |

73,000 |

Solution

In the Books of Mrs. Devi

Trial Balance as on Mar 31, 2009

Illustration: 14

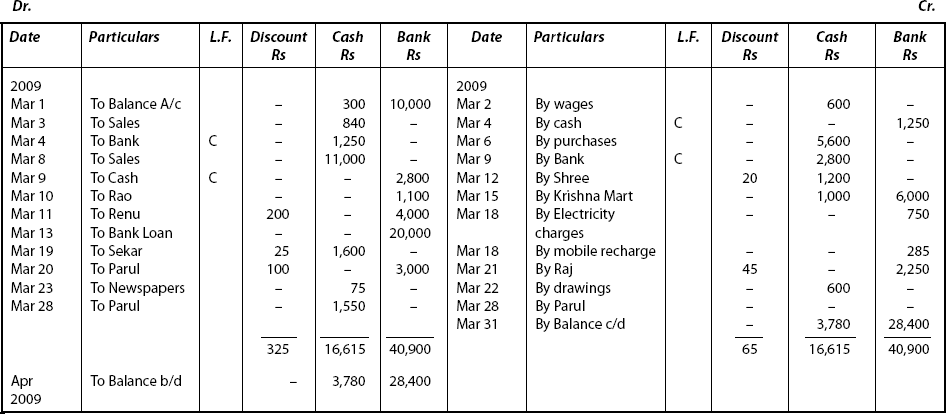

Enter the following transactions of Narayana in the proper books of original entry, post them into the ledger, balance the accounts and extract a Trial Balance as on Mar 31, 2009.

2009 |

|

Mar 1 |

Cash-in-hand Rs 300; Cash at Bank Rs 10,000; Stock Rs 7,500; Debtors: Sekhar Rs 2,250, Parul Rs 3,100, Renu Rs 4,200; Furniture Rs 2,700; Computers Rs 29,250; Creditors: Shree Rs 2,400, Raj Rs 3,400 |

Mar 2 |

Paid wages Rs 600 |

Mar 3 |

Cash sales Rs 840 |

Mar 4 |

Withdrawn from Bank Rs 1,250 |

Mar 5 |

Sold to Rao 15 pieces of T-Shirts @ Rs 100 per T-Shirt |

Mar 6 |

Purchased 80 pieces of T-Shirts @ Rs 70 per T-Shirt |

Mar 7 |

Purchased a computer table for Rs 2,900 from Royal and Co. |

Mar 8 |

Cash sales Rs 11,000 |

Mar 9 |

Deposited with Bank Rs 2,800 |

Mar 10 |

Received a cheque from Rao Rs 1,100 |

Mar 11 |

Renu pays a cheque Rs 4,000 in full settlement of her account |

Mar 12 |

Paid to Shree Rs 1,200; Discount received Rs 20 |

Mar 13 |

Loan from Bank Rs 20,000 |

Mar 14 |

Purchased from Khuber 40 T-Shirts @ Rs 75 each; 50 pieces of casual wears @ Rs 125 each. Trade discount 25% |

Mar 15 |

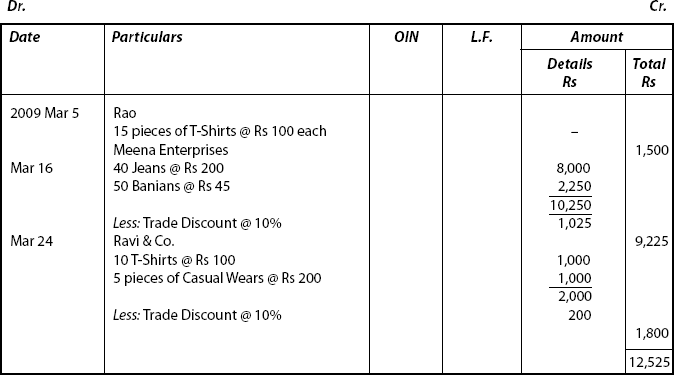

Purchased from Krishna Mart: 50 jeans @ Rs 120 each; 100 banians @ Rs 25 each. Trade discount 10% |

Mar 16 |

Sold to Meena Enterprises: 40 jeans @ Rs 200 each; 50 banians @ Rs 45 each. Trade discount 10% |

Mar 17 |

Paid Krishna Mart Rs 6,000 by cheque and Rs 1,000 cash |

Mar 18 |

Paid Electricity bills Rs 750; Mobile recharges Rs 285 |

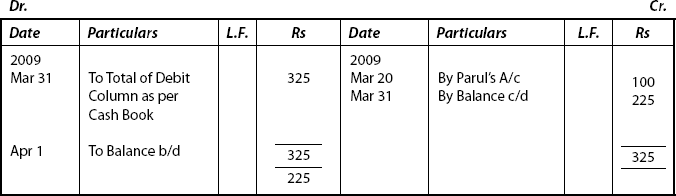

Sekhar pays Rs 1,600; Discount allowed Rs 25 |

|

Mar 20 |

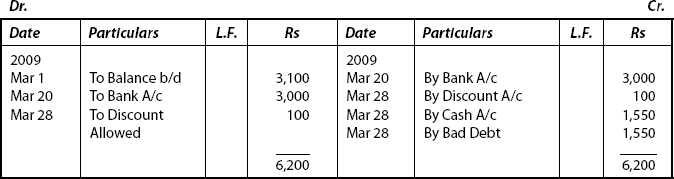

Parul settles her account by cheque Rs 3,000 |

Mar 21 |

Paid to Raj by cheque Rs 2,250; Discount received Rs 45 |

Mar 22 |

Cash withdrawn for physician consultation Rs 600 |

Mar 23 |

Old newspapers sold for Rs 75 |

Mar 24 |

Sold to Ravi & Co. 10 T-Shirts @ Rs 100 each; 5 pieces of casual wears @ Rs 200 each. Trade discount 10% |

Mar 25 |

Received acceptance from Ravi & Co. for Rs 1,250 |

Mar 26 |

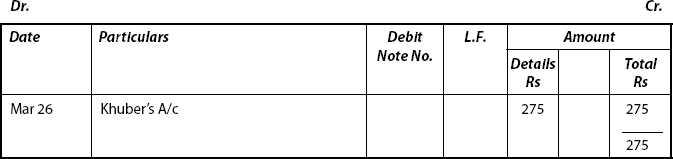

Goods returned to Khuber Rs 275 |

Mar 27 |

Sales returns from Meena Enterprises Rs 700 |

Mar 28 |

Cheque received from Parul returned dishonoured. Parul found insolvent. Only 50% recovered. |

Solution

First, transactions which cannot be recorded in the books of original entry (subsidiary books), have to be entered in General Journal or Journal Proper as follows:

Columnar Cash Book

(Cash Book with Discount, Cash and Bank Columns)

Accounting Process — Starting from recording of transactions under various heads of account (posting to ledger) and balancing them, recording in the needed subsidiary books and fi nally preparing a Trial Balance (Illustrated).

Sales Book

Sales Return Book

Purchases Book

Purchases Returns Book

Ledger Accounts

Computer’s Account

Furniture Account

Sekhar’s Account

Parul’s Account

Renu’s Account

Shree’s Account

Raj’s Account

Narayana’s Capital Account

Computer Table’s Account

Royal & Co. Account

Bad Debt Account

Discount Allowed Account

Purchases Account

Rao’s Account

Krishna Mart’s Account

Khuber’s Account

Ravi & Co. Account

Bills Receivable Account

Sales Account

Old Newspaper Account

Wages Account

Drawings Account

Purchase Returns Account

Sales Returns Book

Electricity Bill A/C

Phone (Mobile) Charges A/C

Meena Enterprises A/C

Bank Loan Account

Discount Received Account

Note: Normally nominal accounts are not balanced.

Trial Balance As on Apr 1, 2009

Note:

- Trial Balance may be presented in this format also.

- Paise may be rounded off to the next higher value.

Summary

- Trial Balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books.

- Objectives: (i) To check the arithmetical accuracy. (ii) To locate the errors and rectify them. (iii) To provide basis for the preparation of final accounts. (iv) To serve as a ready reckoner.

- Features: (i) It is a statement. (ii) It is a list of balances of all accounts. (iii) It is prepared on a particular date. (iv) It is one method of checking the accuracy of transactions. (v) It can be prepared only from double entry system of accounts.

- Preparation of Trial Balance (i) Totals Method (ii) Balances Method and (iii) Total-cum-Balances Method.

- Errors – Kind of errors: (1) Errors of principle – occur due to violation or ignorance of accounting principles (2) Clerical errors (i) Errors of omission (ii) Errors of commission (iii) Errors of casting (3) Carrying forward and Compensation Errors.

- Errors disclosed by Trial Balance: (i) Errors of partial omission (ii) Errors of casting (iii) Errors of carrying forward (iv) Errors of posting in the wrong side of the correct account (v) Errors of posting correct account with wrong amount (vi) Double posting in the same account.

- Errors not disclosed by Trial Balance: (i) Errors of complete omission (ii) Errors of recording (iii) Errors of Principle (iv) Errors of posting to wrong account in the right side of the correct amount (v) Compensating errors.

- Different steps to locate the errors in the Trial Balance (refer the main part of the text).

- Suspense Account: In case, it is not possible to detect the errors before preparing final accounts, the difference in the Trial Balance caused due to errors, is to be transferred to an account referred as Suspense Account. When errors are located, they will be rectified through the Suspense Account and the Suspense Account will be eliminated consequently.

Key Terms

Ledger: Record containing all the individual accounts in a summarised and classified form.

Balancing: The process of equalising the two sides of an account.

Posting: The process of formal transcribing of amounts from the journal to the ledger or transferring of entries from the journal to the ledger is termed as posting.

Bills Receivable: A bill that shows money (an amount) due to the firm from those whose names are mentioned in it.

Bills Payable: A bill showing that a firm owes money to those whose names are mentioned in it.

Bills Payable Book: A book of original entry in which the names of the drawer, the payee, the due date and other particulars are recorded.

Cash Book: A book of entry for cash receipts and payments Cash Book is a book of original entry as well as a ledger account.

Cash Book – Single Column: A type of cash book containing one amount column on each side.

Cash Book with Discount Column: An additional column on the debit side (for discount allowed) and on the credit side (for discount received) are provided in addition to cash columns.

Cash Book with Discount, Cash and Bank Columns: Cash Book which is ruled with three amount columns on either side of the book, the additional column for bank transactions.

Cash Discount: Allowed to customers as an incentive to pay their bills within a specified time.

Credit Note: A document issued by the “seller” to the “buyer.” On the basis of credit note, Sales Returns Book is to be prepared.

Debit Note: A document issued by the “buyer” to the “seller” consisting details of return of goods. It serves as a basis for preparation of “Purchases Returns Book.”

Imprest System: Cash maintained to meet sundry or pretty expenses.

Petty Cash Book: A type of cash book to record payment of expenses of small value.

Purchase Book: A record to enter purchase of goods on credit.

Purchases Returns Book: Another book of original entry, to record transactions relating to purchase returns. This is also known as “Returns Outwards Book.”

Sales Book: A special subsidiary book to record goods returned to the business enterprise from the customers. It is also called “Returns Inward Book.”

Subsidiary Book: Book of original entry to record only one type of business transactions.

Trade Discount: A form of allowance given by the suppliers to the retailers to allow a margin of profit to them. It is deducted from the list price. It is not recorded in the books of account.

Trial Balance: A statement in which debit and credit balances of all the accounts of the ledger are listed to test the arithmetical accuracy of books of accounts.

References

“Accountancy – Financial Accounting,” National Council of Educational Research and Training, New Delhi, 2004.

R.L. Gupta and V.K. Gupta, “Principles and Practice of Accountancy,” Sultan Chand and Sons, New Delhi, 2000.

P.C. Tulsian, “Financial Accounting,” Pearson Education, New Delhi, 2004.

A Objective-type Questions

I State whether the following statements are True or False

- Trial Balance is a statement which shows debit balances and credit balances of all accounts in the ledger.

- The total of debit balances and the total of credit balances need not tally, always.

- Trial Balance can be prepared only at the end of an accounting period. It cannot be prepared at any date.

- Trial Balance is the basis on which final accounts are prepared.

- If any error is found in the preparation of a Trial Balance, such errors can be rectified only when the balance sheet is prepared.

- A debit balance is either an asset or expense or loss.

- All the errors committed are not disclosed by the Trial Balance.

- A Trial Balance will disclose errors of principle.

- If any of the GAAP is violated, error resulting from such violation is called “errors of principle.”

- Error of complete omission affects the Trial Balance.

- Error of partial omission does not affect the Trial Balance.

- Error of recording does not affect the Trial Balance.

- Error of posting may or may not affect the Trial Balance.

- When it is difficult to locate and rectify errors, the difference caused due to such errors is transferred to a new and temporary account known as “Suspense Account.”

- When all the errors affecting the Trial Balance are located and rectified, the “Suspense Account” gets closed automatically.

- Journal entries passed to rectify the errors are called “rectifying entries.”

- Suspense Account having credit balance will be shown on the assets side of a balance sheet.

- Excess debit of an account can be rectified by debiting the same amount.

- Short debit of an account can be rectified by further debit (of the short amount) of the same account.

- Suspense Account in the Trial Balance is entered in the Profit and Loss Account.

Answers

1. True |

2. False |

3. False |

4. True |

5. False |

|

6. True |

7. True |

8. False |

9. True |

10. False |

|

11. False |

12. True |

13. True |

14. True |

15. True |

|

16. True |

17. False |

18. False |

19. True |

20. False |

|

II Fill in the blanks with suitable words

- Trial Balance is prepared as per the rules of _____ system.

- Trial Balance is a statement prepared with the debit and credit balances of ______accounts.

- Trial Balance is the basis on which _______ are prepared.

- List of names with debit balances are grouped under a common caption known as ________

- List of names with credit balances are grouped together under a single heading called _________

- A ______balance is either a liability or income or gain.

- If the totals of debit balances and credit balances in a Trial Balance do not tally, it implies that some ________would have been committed.

- If the debit column or credit column is totaled wrongly in a Trial Balance as Rs 15,100 instead of Rs 11,500, it is called _________.

- In the same case (as in Q.8), if it is wrongly totalled as Rs 10,150 it is called __________

- Errors of posting in the wrong side of the correct account are ________by Trial Balance.

Answers

- Double entry

- Ledger

- Final Accounts

- Sundry debtors

- Sundry creditors

- Credit

- Errors

- Overcasting

- Undercasting

- Disclosed

III Choose the correct answer

- Trial Balance is prepared to find out

- profit or loss

- financial position

- arithmetical accuracy of accounts

- none of the above

- Suspense Account in the Trial Balance is to be shown in

- Trading Account

- Profit and Loss Account

- Balance Sheet

- none of the above

- Suspense Account having debit balance will be shown in the

- assets side of the Balance Sheet

- liabilities side of the Balance Sheet

- debit side of the Profit and Loss Account

- credit side of the Profit and Loss Account

- Suspense Account will get closed when

- Trading Account is prepared

- Profit and Loss Account is prepared

- Balance Sheet is drawn

- errors are rectified

- Errors which are not disclosed by Trial Balance are

- Errors of partial omission

- Errors of complete omission

- Errors of carrying forward

- Wrong totalling to ledger

- Trial Balance can be prepared on

- the end of an accounting period

- any date

- directions by the statutory provision

- none of the above

- Errors that affect one side of an account are called

- Single sided errors

- Double sided errors

- Absolute errors

- none of the above

- Wages paid to workers for erection of a new machinery will have to be debited to

- Wages Account

- Machinery Account

- Production Expenses Account

- none of the above

- Goods taken by the Proprietor for own use will be credited to

- Drawings Account

- Sales Account

- Office Account

- Purchases Account

- While totalling a subsidiary book, errors that are committed belong to

- Error of recording

- Error of posting

- Error of casting

- Error of omission

Answers

- (c)

- (c)

- (a)

- (d)

- (b)

- (b)

- (a)

- (b)

- (d)

- (c)

B Short Answer-type Questions

- What is a Trial Balance?

- What are the objectives of Trial Balance?

- What are the main advantages of a Trial Balance?

- State the principle on which the agreement of Trial Balance is based.

- Explain the term “Sundry Debtors.”

- What are the limitations of a Trial Balance?

- “The Trial Balance ensures arithmetical accuracy and not accounting accuracy” – why?

- Why do errors occur in the preparation of Trial Balance?

- Name the two main classification of errors.

- What do you mean by errors of principle? Give two examples.

- What are the two types of “errors of omission”?

- What are the types of “errors of commission”?

- Explain: (i) overcasting (ii) undercasting

- Give any four examples of errors which are disclosed by Trial Balance.

- Give any four examples of errors which are not disclosed by Trial Balance.

- What do you mean by “Suspense Account”?

- How will you close a “Suspense Account”?

- Mention the main three steps to be adopted to rectify an error.

- Mention the two important stages involved in the rectification process.

- How will you rectify the following:

- Short debit

- Excess debit

C Essay-type Questions

- Define “Trial Balance.” What are its objectives? Explain the significances of Trial Balance. What are its limitations?

- Draw a format of a Trial Balance. Explain it.

- Explain the various kinds of errors with due examples.

- Explain the impact of errors on Trial Balance by giving suitable examples – errors disclosed and not disclosed by Trial Balance.

- Explain the steps to be taken to locate the error and rectify the same.

D Exercises

1. Prepare Trial Balance as on 31.12.2009 from the following balances of Mr. Raj.

Answer: Rs 2,54,450

2. The following balances are extracted from the books of Mr. Vas. Prepare Trial Balance as on 31.12.2009.

Answer: Rs 4,06,525

3. Mr. Dev is the owner of a factory. From the following balances that are extracted from his ledger, you are required to prepare a Trial Balance as on Mar 31, 2010.

Answer: Rs 8,82,900

4. From the following information taken from the ledger of Sathyan, prepare a Trial Balance as on 31.3.2010.

Answer: Capital Rs 26,000;

Total of Trial Balance Rs 1,00,200

5. Prepare a Trial Balance from the following balances of Mrs. Renuka as on 31.12.2009.

Answer: Suspense Account Rs 10,500 (Credit)

6. The following balances have been taken from the ledger of Mr. Vasanth as on Mar 31, 2010. You are required to prepare the Trial Balance as on 31.3.2010.

Answer: Rs 4,80,000

7. The following Trial Balance is drawn by a person who is not well versed in accounting process. You are required to re-draft the Trial Balance correctly.

Trial Balance for the year ended Mar 31, 2010

| Debit Rs |

Credit Rs |

|

|---|---|---|

Capital |

53,700 |

− |

Stock 1.4.2009 |

22,350 |

− |

Insurance |

− |

6,300 |

Purchases |

1,38,600 |

− |

Sales |

− |

2,36,550 |

Salary Expenses |

37,230 |

− |

Lighting and Heating |

1,860 |

− |

Plant and Machinery |

21,600 |

− |

Delivery Expenses |

− |

1,380 |

Rates Paid |

2,340 |

− |

Depreciation Accumulated |

2,100 |

− |

Rent Paid |

− |

− |

Rent Received |

− |

3,630 |

Delivery Vehicle |

8,850 |

− |

Cash |

660 |

− |

Trade Creditors |

29,550 |

− |

Trade Debtors |

− |

83,520 |

Carriage Outwards |

− |

3,000 |

Outstanding Rent |

3,000 |

− |

Bank Overdraft |

5,850 |

− |

− |

3,34,380 |

3,34,380 |

Answer: Rs 3,34,380

8. Rectify the following errors:

- Received Rs 15,000 from Patel debited to his account.

- The Sales Book undercast by Rs 3,500.

- The Purchases Return Book overcast by Rs 2,500.

- Sale of old furniture for Rs 700, treated as sale of goods.

- Rs 5,000 received from Bhagya was entered on the debit side of the Cash Book. No posting was done to Bhagya’s Account.

- An amount of Rs 2,000 withdrawn by the proprietor for his personal use has been debited to Trade Expenses Account.

- Cash received from Mala Rs 1,000 was credited to Kala.

- A credit sale of Rs 15,000 to Jain has been wrongly passed through the Purchases Book.

- Credit purchase of goods from Reddy of Rs 7,500 has been wrongly entered in the Sales Book.

- Sales Book total Rs 9,190 was wrongly totalled as Rs 9,910.

- Rs 9,950 received from Vincent in full settlement of his account of Rs 10,000 was posted in Cash Book but omitted to enter into his account.

- Discount allowed Rs 100 to Vijaya has been credited to Discount Account.

- The total of the discount column on the debit side of the Cash Book Rs 50 was omitted to be posted in the ledger.

- Rs 40,000 paid for the purchase of a computer was charged to Office Expenses Account.

- Repairs made were debited to Building Account Rs 1,750.

9. As the Trial Balance does not get balanced, the book-keeper of a trader placed the difference in the Suspense Account and subsequently found the following errors:

- Sales Book was overcast by Rs 4,500.

- Rs 8,700 received from Rita in full settlement of her account of Rs 9,000 was posted in Cash Book but omitted to be entered in her account.

- The total of Sales book Rs 36,000 was debited to Sales Returns Account.

- Rs 3000 received as interest was credited to Interest Account as Rs 300.

Rectify the errors and show the Suspense Account.

10. A book-keeper could not tally the Trial Balance. The difference of Rs 1,040 was temporarily placed to the credit of Suspense Account and subsequently the following errors have been detected.

- A sale of Rs 1,000 to Shankar has been entered in the Purchase Book.

- The total of Purchase Book was short by Rs 1,200.

- The total of the “Discount column” on the debit side of the Cash Book Rs 300 was omitted to be posted in the ledger.

- The total of the “Discount column” on the credit side of the Cash Book of Rs 460 was not posted in the ledger.

- A sale of Rs 6,390 was entered in the Sales Book as Rs 6,990.

You are required to rectify the errors through Suspense Account. Give rectifying entries also.

11. The following Trial Balance was drawn by an apprentice in the field. Although both sides were equal, it has been done incorrectly. You are required to re-draft the Trial Balance correctly.

Trial Balance for the year ended Mar 31, 2010

| Debit Rs |

Credit Rs |

|

|---|---|---|

Capital |

|

3,00,000 |

Opening Stock |

49,770 |

− |

Closing Stock |

− |

61,740 |

Sundry Creditors |

− |

37,500 |

Sundry Debtors |

62,280 |

− |

Machinery |

2,37,000 |

− |

Gross Purchases |

1,82,760 |

− |

Gross Sales |

− |

3,07,800 |

Returns Inwards |

7,200 |

− |

Returns Outwards |

− |

3,690 |

Carriage Inwards |

2,400 |

− |

Carriage Outwards |

− |

5,550 |

Import Duty |

3,600 |

− |

Export Duty |

− |

2,400 |

Wages and Salaries |

94,200 |

− |

Bills Receivables |

45,000 |

24,000 |

Bills Payable |

− |

− |

Rent Receivable |

11,400 |

3,300 |

Rent Paid |

− |

2,610 |

Commission Received |

− |

2,280 |

Discount Allowed |

− |

− |

Rates and Taxes |

21,390 |

− |

Bank Overdraft |

33,000 |

− |

Cash-in-Hand |

1,140 |

− |

|

7,50,870 |

7,50,870 |

Answer: Rs 7,20,000

12. Record the following transactions in proper books, post them to ledger and extract a Trial Balance.

|

Date |

|

|

Rs |

|

2009 |

|

|

|

|

Dec |

1 |

Bhamini commenced business with cash |

1,20,000 |

|

|

2 |

Goods purchased for cash |

18,000 |

|

|

3 |

Goods purchased from Lal |

24,000 |

|

|

4 |

Goods sold for cash |

36,000 |

|

|

5 |

Goods sold to Krishna |

30,000 |

|

|

6 |

Goods returned by Krishna |

6,000 |

|

|

7 |

Goods returned to Lal |

1,200 |

|

|

8 |

Furniture bought for cash |

2,400 |

|

|

9 |

Cartage paid |

600 |

|

|

10 |

Cash received from Krishna allowed discount 5% |

24,000 |

|

|

11 |

Cash paid to Lal |

22,200 |

|

|

|

Lal allowed us discount |

600 |

|

|

12 |

Paid charities |

1,200 |

|

|

13 |

Goods sold for cash |

36,000 |

|

|

14 |

Goods purchased for cash |

18,000 |

|

|

15 |

Goods sold to Singh |

30,000 |

|

|

16 |

Goods purchased from Hemant |

12,000 |

|

|

17 |

Goods returned by Singh |

1,200 |

|

|

18 |

Cash paid by Singh |

28,200 |

|

|

|

Discount received |

600 |

|

|

19 |

Goods returned to Hemant |

1,200 |

|

|

21 |

Cash paid to Hemant |

9,000 |

|

|

|

Discount received |

300 |

|

|

22 |

Old newspapers sold to Mohan on credit |

150 |

|

|

27 |

Paid for interest |

600 |

|

|

31 |

Paid for salaries |

3,000 |

|

|

31 |

Deposited with bank |

1,50,000 |

Answer: Rs 2,56,950

13. Enter the following transactions in proper books, post them to ledger and draw out a Trial Balance:

Answer: Rs 10,72,336