Chapter 8

Measurement of Business Income

LEARNING OBJECTIVES

After studying this chapter, you will be able to

Understand the Meaning of Business Income.

Know the Important Definitions of “Income”

Understand the Terms “Revenues” and “Expenses”

Understand the Meaning of “Measurement of Business Income”

Measure Business Income by Computing the Increase in Owner’s Capital – Net Worth Method

Measure “Net Income” or “Net Profit”

Measure “Net Income” by Applying the Principle of “Matching of Incomes and Expenses” Method

Understand the Terms “Income and Expenses” and Other Inherent Elements Associated with These Terms

Compare “Net Worth Method” with “Matching Costs Against Revenue Method”

Understand the Procedure for “Measurement of Business Income”

Know the Salient Features of “Business Income”

Understand the “Economic Concept of Income” and Its Salient Features

Measure Economic Income: “Ex-ante Income” and “Ex-post Income”

Compare the Accounting Income of Individuals

Introduction

For any type of business organisation, the prime motive is to earn income. Income or profit is the yardstick to assess the performance of the business entities. Though the word “income” is easily and readily comprehended by even the common man, it is difficult to define precisely. Everyone (owners, employees, investors and creditors) is interested in knowing the capacity that a business entity can earn in a specific period or periodically.

OBJECTIVE 1: DEFINITION OF INCOME

Some of the important definitions are analysed to understand the salient features of “business income” and “measurement of business income.”

Sir John Hicks defined income as “the maximum value which a man can consume during a week and still expect to be well off at the end of the week as he was at the beginning.” Though this definition is related to a common man stressing the aspect of economics, it is the foundation stone on which so many eminent economists raised superficial structures by way of inventing definitions in keeping with the latest socioeconomic trends. The next important definition is the one defined by the Sandilands Committee (UK). It defined the company’s profit for the year as “the maximum value which the company can distribute during the year and still expect to be as well off at the end of the year as it was at the beginning.” The important feature to be noted, at this juncture, is that the group of words “as well off” at the end of the period (week or year) stresses the importance to compare the net worth of businesses between two periods to assess whether they are “well off”.

Another important definition is expounded by Eric L. Kohler. He defined income as “money or money equivalent earned or accrued during an accounting period, increasing the total of previously existing net assets, and arising from sales and rentals, of any types of goods or services, commissions, interest, gifts, recoveries from damage and windfalls from any outside source.”

This definition stresses the importance on “… increasing the total of previously existing net assets.” We have to understand what “net assets” are and how they can be measured. This aspect is given due recognition in the definition of American Accounting Association (AAA). It defines business income as “the increase in net assets measured (determined) by the excess of revenues over expenses.”

OBJECTIVE 2: REVENUES AND EXPENSES

The terms used in this definition (revenues and expenses) are explained as follows:

2.1 Revenues

Revenues may be measured by the inflow of assets. Inflow of assets represent any increase in the value of assets such as increase in cash, debtors and the like and also decrease in liabilities such as decrease in bills payable, creditors and the like. Such inflow of cash arises from various business activities such as selling of goods, providing services and so on. There is no uniformity in generation of revenue among the business entities. Each enterprise differs from the other in this aspect.

2.2 Expenses

Expenses may be measured by the outflow of assets such as decrease in value of assets and also increase in liabilities. Such outflow of cash are incurred or consumed in the activities of business enterprises. Here also, expenses differ from one enterprise to other as the nature of business dictates the type of expense.

OBJECTIVE 3: MEANING OF MEASUREMENT OF BUSINESS INCOME

“The process of applying a quantitative (in terms of monetary unit) amount to revenue and expenses is called measurement of income.” This is the summarised version of measurement of business income.

3.1 Net Worth Method

Business income may be measured by computing the increase in the owner’s capital. In ordinary terms, we used to say income is what the business earns over and above the capital employed. In accounting terms, any accretion to the capital may be considered as income, as capital is not construed as income. In going concern, capital means capital introduced in the first year plus income retained in the business. This is referred to as “net worth” of the business. Business income for a period may be measured on the basis of “net worth” [total assets – total liabilities (owing to outsiders)]. The net worth of a business at the beginning of a period is compared with net worth at the end of the period. Increase in net worth represents a profit whereas a decrease in net worth indicates a loss. This method of measuring net income facilitates the task of capital maintenance, especially in going concerns.

OBJECTIVE 4: MEASUREMENT OF “NET INCOME” OR “NET PROFIT”

In accounting practice both the terms “net income” and “net profit” are synonyms. Net income is measured by comparing sales revenues and costs related to sales revenues. This is usually compared by preparing income statements (i.e., Profit and Loss Account). The total revenues earned during a specified period and total expenses incurred in earning these revenues are shown in this account. The difference between these two will indicate either profit/income or loss. If revenues are in excess of expenses, such net result is profit or income. If expenses are in excess of revenues the net result will be loss.

OBJECTIVE 5: MEASUREMENT OF NET INCOME: MATCHING OF INCOMES AND EXPENSES METHOD

This approach to measurement of net income of the business is “matching of incomes and expenses.” This concept of matching principle is defined by Finney and Miller: “The concept of business income is a matter of matching revenue with related cost or expense, that is, if revenue is deferred because it is regarded as not yet earned, all elements of expenses related to such deferred revenue must be deferred also in order to achieve a matching of revenue which is essential to a proper determination of income.” Expenses that are directly associated with a particular type of revenue are recognised expenses in the period in which the revenues are recognised. Expenses that are not directly associated with revenues are treated as expenses of the period in which they are recognised.

The matching of incomes and expenses method is practiced widely due to the reason the elements which are entered into Profit and Loss Account (Income Statement) can be verified with objective evidence. Incomes consist of revenues and gains and expenses consist of expenses and losses as well.

5.1 Incomes and Expenses

“Incomes and expenses” are explained as follows with examples:

- Income is a measure of inflow of assets that result in increase of equity.

- Income in the form of inflows – sales and other incomes, such as interest, commission and fees received.

- Enhancement of assets – increase in the value of assets.

- Decrease in liabilities – discounts received in the settlement of liabilities.

The above elements result in the increase of equity, but the additional capital introduced also results in increase of equity, which is not treated as an income.

- Expenses are a measure of outflows that result in decrease of equity.

- Expenses in the form of outflows – payment for materials, components, wages, salaries, salesmen and so on.

- Depletion of assets – depreciation on assets put into use and consumption of loose tools.

- Liabilities incurred on tax payments, audit fees and outstanding expenses.

These elements “incomes and expenses” are directly related to measure profit.

OBJECTIVE 6: COMPARISON OF “NET WORTH METHOD” AND “MATCHING COSTS AGAINST REVENUE METHOD”

- The Net Worth Method of measuring business income emphasises the importance of Balance Sheet, while the method of matching costs against revenues gives much importance to Profit and Loss Account (Income Statement).

- Under the Net Worth Method, the focus is on the net worth at two points in time, whereas in the latter method the focus is on explanation of changes which took place in the net worth.

- Elements that constitute the income statement can be verified with objective evidence under the second method, whereas these cannot be verifiable under net worth method.

OBJECTIVE 7: PROCEDURE FOR MEASUREMENT OF BUSINESS INCOME

The procedure for measurement of business income to be followed is explained step by step as follows:

Step 1: |

Determination of accounting period. First, the accounting period has to be determined for computing the business income. A pre-determined and specified period of time is the basic need for the measurement of business income. Generally, the accounting period is of 12 months, i.e. one year. The financial statement should be prepared on a periodic basis. The notion of realisation, matching and accounting are interrelated and better results cannot be obtained in the absence of any of the three. Once the date is determined, expenses can be matched with revenues, relating to the specified period. A calendar year is the accounting period which begins on Jan 1 and ends on Dec 31, whereas a financial year begins from Apr 1 and ends on Mar 31. |

Step 2: |

Identification of revenues. The next step in the process to ascertain business income is the proper identification of revenues relating to the accounting period, as determined in Step 1. Revenue recognition may easily be carried on by applying realisation concept. In a trading concern, revenue is generated mainly from sale of goods and/or services. Value of stock in hand is not treated as an item of revenue under this concept. Such unrealised gains/incomes are not recognised. But in certain circumstances, this realisation concept is relegated to background and unrealised income is recognised for the determination of business income. Long-term business contract is a typical example for unrealised income. |

Step 3: |

Identification of costs. Costs incurred to earn revenue in that specified accounting period have to be identified. Only these costs/expenses which have been associated with that part of revenue earned will have to be taken into account. For example, depreciation (expired cost of an asset) and at times unexpired costs are also treated as assets. Prepaid expense is an example for such unexpired costs (treated as assets). |

Step 4: |

After ascertaining all revenues (as in Step 2) and expenses (as in Step 3) incurred to earn revenues, business income is calculated by preparing Income Statement (Profit and Loss Account) for the accounting period. |

OBJECTIVE 8: SALIENT FEATURES OF BUSINESS INCOME

Some of the special features of business income are detailed as follows:

1. Accounting period convention: The very first step in the computation of business income is the determination of accounting period. So, business income is based on the accounting period convention. It reflects the financial position of the business entities for a specified accounting period.

2. Revenue principles: Business income is also based on the revenue principles, as the computation of business income requires the definition, measurement and recognition of revenue.

3. Realisation concept: This concept plays a vital role in revenue recognition. Realisation concept is another important feature of business income.

4. Objective evidence: All transactions relating to measurement of business income are based on objective evidence. They are verifiable; thereby depicting a true and accurate figure on net income arrived at. Only the actual transactions which occurred in the specified accounting period are taken into account.

5. Historical cost: Business income measures expenses in terms of historical costs.

6. Matching principle: Matching revenue with related cost or expense, i.e. matching principle is applied for the business income measurement.

7. Ex-post income: Ex-post income represents the excess of the capital of the accounting year over that of the previous year. Future expected returns are based on current period income. Business income is an ex-post income viewed from this angle.

8. Unrealised profits and losses: Business income ignores unrealised profits and losses. It is based on the realisation concept. Realisation concept gives importance to realised gains only. Unrealised profit/loss arises on the holding of fixed assets. This is ignored in the determination of business income.

OBJECTIVE 9: MEANING OF ECONOMIC CONCEPT OF INCOME

So far we have explained the accounting concept of income. Now, some of the important characteristics of the economic concepts of income are explained.

Economic income results from consumption in a specified period plus changes in the value of capital. This means that the economic income arises from the changes in the “value of assets” and “capital.” According to eminent economists, the income refers to the periodic benefits derived from the use of capital. Unlike business income, which is based on the principle of matching of revenues and expenses, economic income is measured in real terms by taking into account both the changes in the value of assets and the capital (i.e., value of consumption is taken into account).

OBJECTIVE 10: SALIENT FEATURES OF ECONOMIC CONCEPT OF INCOME

1. Current values: Economic concept of income is based on current values. Unlike the accounting concept of income, it gives emphasis only on current values and not on historical cost.

2. Unrealised gains/losses: Unrealised gains/losses are taken into account in the value of fixed assets.

3. Consumption: Under economic concept of income, only income is available for consumption. Value of consumption is the main criterion in the economic concept of income.

4. Comparison of capitals: Income is measured by comparing the value of capital at two different dates.

5. Ex-ante income: Income is an ex-ante income. It refers to excess of value of capital for the current period over that of the previous period with reference to the present value of the future expected returns on the previous year basis.

6. Value of capital and asset: Value of capital is derived from the value of income, whereas the value of asset refers to the present value of all future benefits that the asset can provide.

OBJECTIVE 11: PROCEDURE TO MEASURE ECONOMIC INCOME

In practice, there are two different income concepts, ex-ante income and ex-post income.

- The difference between the value of capital at the end of the year and the value of capital at the beginning of the year is determined which represents “economic income.”

- Value of capital at the beginning of the year (A) is based on the future cash flows expected to be generated from the assets, estimated at the beginning of the year.

- Value of the capital at the end of the year (B) is based on the revised future cash flows expected to be generated from the assets, estimated at the end of the year.

- Economic income is based on the present value of cash flows.

- Ex-ante income is calculated with reference to present value at the beginning of the year (X level)

Ex-ante income: BX − AX

- Ex-post income is calculated with reference to present value at the end of the year (Y level)

Ex-post income: BY − AY

Illustration: 1

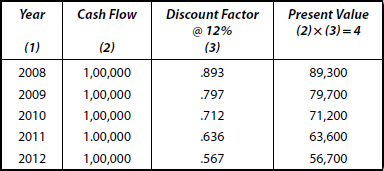

On Jan 1, 2008, Raj purchased an asset for Rs 3,50,000 and anticipated an annual cash flow of Rs 1,00,000 at the end of each year for the next 5 years. On Dec 31, 2008, he actually earned Rs 1,20,000 during 2008 (it was ascertained from his financial records) and anticipated an annual cash flow of Rs 1,50,000 at the end of each year for the next 4 years. The discount factors at 12% discount rate are given as follows:

Compute ex-ante income of Mr Raj.

Solution

Step 1: |

Estimated annual cash flow at the beginning of the year (Jan 2008) is Rs 1,00,000–(A) (given) |

Step 2: |

The present value of future cash flow has to be calculated. Discount (present value) factor is given in the present value table. Multiply this factor with the estimated cash flow at the beginning of the year (Rs 1,00,000). As the factor varies from year to year, multiply with that factor for each year for the remaining 4 years and sum up the present value. This is shown in the following table. |

AX = 3,60,500

Step 3: |

Revised expected cash flow at the end of the year has to be taken into account as given in the question. |

Step 4: |

Present value of revised future cash flows rate at the beginning of the year is calculated as follows: |

BX = 5,13,960

Step 5: |

Ex-ante income = BX – AX |

|

Substituting the values in the equation: |

|

= Rs 5,13,960 – 3,60,500 |

|

= Rs 1,53,460 |

Illustration: 2

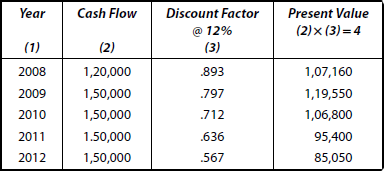

Compute the ex-post income of Mr Raj based on the figures from Illustration 1.

Solution

Step 1: |

Cash flows expected to be generated at the beginning of year (Jan 1, 2008) is given as Rs 1,00,000 taken into account. |

Step 2: |

Compute the present value at the end of the year (AY) |

AY = 4,03,800

Step 3: |

Revised cash flows (anticipated) are taken into account. |

Step 4: |

Compute the present value of revised future cash flow at the end of the year (BY) as follows. |

BY = 5,75,700

Step 5: |

Ex-post income = BY – AY |

|

Substituting the values in the equation: |

|

= Rs 5,75,700 – 4,03,800 |

|

= Rs 1,71,900 |

Illustration: 3

Mr Vas started a business with a capital of Rs 5,00,000. The following information is extracted from his books of account for the year 2009:

Purchases |

Cash: |

Rs 1,50,000 |

|

Credit: |

Rs 2,50,000 |

Sales |

Cash: |

Rs 4,00,000 |

|

Credit: |

Rs 6,00,000 |

Payment to Suppliers |

|

Rs 1,50,000 |

Expenses |

Paid |

Rs 40,000 |

|

Outstanding |

Rs 60,000 |

Closing Stock |

|

Rs 50,000 |

Fixed Assets |

|

Rs 1,50,000 |

Depreciation on Fixed Assets : 10% |

|

|

Collection from Customers |

|

Rs 4,00,000 |

You are requested to compute the accounting income of Mr Vas.

Solution

Notes

- Accounting income and business income are synonyms.

- Both accrual basis and net worth methods are used to explain how business income is measured.

- First, measurement of business income on accrual basis is computed as follows (Profit and Loss Account).

Step 1: |

Revenue Recognised |

Rs |

Rs |

|

(i) (sales) Cash Received |

4,00,000 |

|

|

(ii) Add: Credit Sales |

6,00,000 |

10,00,000 |

Step 2: |

Less: Costs Recognised |

|

|

|

(i) Cost of Goods Sold |

|

|

|

Cash Purchases + Credit |

|

|

|

Purchases: Rs 1,50,000 + 2,50,000 = |

4,00,000 |

|

|

(ii) Less : Closing stock |

50,000 |

3,50,000 |

Step 3: |

Gross Profi t (Step 1 − Step 2) |

|

6,50,000 |

Step 4: |

Less: Other Costs Recognised |

|

|

|

(i) Expenses (paid + outstanding) |

|

|

|

(Rs 40,000 + 60,000) |

1,00,000 |

|

|

(ii) Depreciation (10% of Rs 1,50,000) = |

15,000 |

1,15,000 |

Step 5: |

Accounting Income |

|

5,35,000 |

Note

- As the students may not be able to understand the actual accounting method of preparing Income Statement (Profit and Loss Account) at this stage, it is worked out in the form of a statement.

- Also, actual accounting method of preparing a balance sheet is not followed. Simply, assets on the credit side and liabilities on the debit side are shown to compute capital at the end of the period to employ the net worth method.

Preparation of Profit and Loss Account and preparation of Balance Sheet are explained in detail in Chapter 5.

Now, compare the value of capital at the end of the year with the beginning of the year.

|

|

|

Rs |

Step 1: |

Capital at the end of the year: |

= |

10,35,000 |

Step 2: |

Less: Capital at the beginning of the year |

= |

5,00,000 |

|

(given in the question) |

|

______ |

Step 3: |

Accounting Income (1 − 2) |

= |

5,35,000 |

Note The accounting income computed under two different methods are same, i.e. Rs 5,35,000.

- Income may be defined as the maximum value which a man can consume during a week and still expect to be “as well off” at the end of the week as he was at the beginning.

- Income may be defined as money or money equivalent earned or accrued during an accounting period, increasing the total of previously existing net assets, and arising from sales and renewals of any type of goods or services, commissions, interest, gifts, recoveries from damage and windfall from any outside source.

- Revenues may be measured by the inflow of assets.

- Expenses may be measured by the outflow of assets.

- Measurement of net income: Net worth method [net worth = total assets – total liabilities (owing to outsiders)]. Matching of incomes and expenses is another approach.

- Procedure for measurement of business income: (i) determination of accounting period, (ii) identification of revenues, (iii) identification of costs and (iv) preparation of income statement.

- Salient features of business income are based on (i) accounting period convention and revenue principles, (ii) realisation concept, (iii) objective evidence, historical cost and matching principle, (iv) ex-post income and (v) unrealised profits and losses are ignored.

- Economic concept of income: Economic income results from consumption in a specified period plus changes in the value of capital.

- Economic income is measured by taking into account both the changes in the value of assets as well as capital (i.e., value of consumption).

- Salient features of economic concept of income: (i) based on current values, (ii) unrealised gains/losses are taken into account, (iii) concept of consumption, (iv) determination of income by comparison of capitals, (v) ex-ante income and (vi) value of capital and asset.

- Procedure to measure economic income: Two different income concepts are used: (i) ex-ante income is computed with reference to present value at the beginning of the year and (ii) ex-post income is computed with reference to present value at the end of the year (based on future cash flows – value of capital).

Key Terms

Business income: Denotes the income in net assets determined by the excess of revenues over expenses. It is the net increase in the owner’s capital that results from operating activities of the enterprise.

Inflation: The situation of rising prices is called inflation. In such situation, the purchasing power of monetary unit will decline.

Income − Economic concept of: “The amount which a man can consume during a period and still remain as well off at the end of the period as he was at the beginning.” It is determined from the changes in the value of assets and capital at the beginning and at the end of an accounting period.

Matching principle: According to the principle, the expenses incurred in an accounting period are matched with the revenue earned during the same accounting period.

Reference

Anthony, R.N. and J.S. Reecee. “Accounting Principles,” Richard D Irwin Inc.

A Objective-type Questions

I. State whether the following statements are true or false:

- Revenues are a measure of inflow of assets.

- Business income is the net increase in the owner’s capital.

- Accounting income is not necessarily a business income.

- The terms net profit and net income are synonyms in the measurement of business income.

- Business income is based on the actual transactions.

- Business income need not be based on the revenue principle.

- Business income is an ex-post income.

- Business income ignores the unrelated profits and losses resulting from the holding of fixed assets.

- Business income ignores historical cost concept.

- No standardised procedure exists for the measurement of business income.

- The doctrine of going concern (entity) is essential for the measurement of business income.

- Accounting period is not very essential for measurement of business income.

- The matching concept is an important basis for the computation of business income.

- Business income is based on purchasing power of the rupee.

- Economic income is consumption in the given period plus changes in the value of capital

Answers

1. True |

2. True |

3. False |

4. True |

5. True |

6. False |

7. True |

8. True |

9. False |

10. True |

11. True |

12. False |

13. True |

14. False |

15. True |

II. Fill in the blanks with appropriate word(s):

- Business income is defined as the increase in _______ measured by the excess of revenue over expenses.

- Revenues are a measure of _______ of assets.

- Expenses are a measure of _______ of assets.

- Net income is measured by comparing _______ _______ and _______.

- Business income is the net increase in _______.

- Revenue recognition is possible with the help of _______ concept.

- Unexpired costs are treated as _________.

- Business income also means _______ income.

- According to matching concept, all revenues and expenses (incurred to earn revenue) must belong to the same _______ period.

- Business income requires the measurement of expenses in terms of _______ cost.

- Business income is an _______ income.

- Business income is based on _______ transaction.

- Business income ignores unrealised _______ and _______.

- The doctrine of _______ states that the business will continue its operations for the foreseeable future.

- The accrual process aims to match _______ and _______ with a definite accounting period.

Answers

- net assets

- inflow

- outflow

- revenue and costs

- owner’s capital

- realisation

- assets

- accounting income

- accounting

- historical

- ex-post

- actual

- profit; loss

- entity or going concern

- revenues; expenses

B Short Answer-type Questions

- Define business income.

- What do you mean by “matching principle”?

- What is “realisation concept”?

- Explain the term “accounting period.”

- Explain “doctrine of entity.”

- Mention the general rules followed in accrual basis of timing and measurement of business income.

- What do you mean by economic concept of income?

- “Inflation affects the measurement of business income”–do you agree?

C Essay-type Questions

- Explain the procedure for measurement of business income.

- Explain the salient features of business income.

- What are the advantages and disadvantages of business income?

- What are the objectives of income measurement?