Chapter 4b

Accounting Process – Ledger

LEARNING OBJECTIVES

At the end of the chapter, you would be able to understand

Meaning of “Ledger”

Standard Form of Ledger and Its Contents

Meaning of “Posting”

The Procedure (Steps Involved) of Posting

Differences between “Journal” and “Ledger”

How to Post an “Opening Entry”

How to “Balance” an Account and Steps Involved in the Procedure for “Balancing”

OBJECTIVE 1: MEANING OF “LEDGER”

In the Journal, each transaction was dealt separately. They do not provide complete information at a glance. The net result of transactions relating to a particular account to be collected at one place, a separate book is to be maintained. This is the book, which we call “ledger.”

A ledger is a book, which contains all the accounts in a summarised and classified form. A ledger is a permanent record of all business transactions transferred from Journal or other books of original entry.

According to L.C. Cropper, “the book which contains a classified and permanent record of all the transactions of a business is called the ledger.”

The Ledger is also referred to as the “Book of Final Entry.” It serves as a destination of all transactions relating to all accounts (whether we follow conventional rules with regard to Personal, Real and Nominal accounts or Accounting Equation (American procedure) Approach in terms of increases or decreases relating to Assets Account, Liabilities Account, Capital Account, Income and Gains Account and Losses and Expenses Account) to which transactions recorded in the books of original entry are transferred.

OBJECTIVE 2: STANDARD FORM OF LEDGER AND ITS CONTENTS

A ledger, in the traditional way, is normally kept in the form of bound note books. In bigger business enterprises, it is not easy to maintain a large and variety of transactions in a singe book.

To overcome this difficulty, loose leaf sheets take the place of bound books. Under Loose-Leaf Ledger, appropriate sheets (ledger format in individual papers) are introduced. Additional pages may be added to any extent, completed accounts may be removed to reduce volume, any accounts may be rearranged so as to suit the needs of the enterprises. This mode of maintaining ledger in the form of loose sheets is called Loose-Leaf Ledger.

Of late, in an electronic era, ledgers are kept in the form of floppy diskettes or CDs or RCDs or DBDs, Pen or Desk Drives or any other electronic device.

Ledger Folio No.……….

2.1 Explanation of Ledger Account Format

- Each ledger account starts with the name of the account. The name of the account is shown in the top (middle or centre) of the account.

- Ledger account is divided into two parts. It is divided into two equal sides by a dark vertical line as shown in the format.

- The left-hand side is called the Debit side (written in the abbreviated form “Dr.”) and the right-hand side is called the Credit side (“Cr.”) Accordingly, the words Dr. and Cr. are written at the top of left and right-hand corners of the columns.

- The columns on both sides (left-hand side – Debit and right-hand side – Credit) are similar.

- The date of transactions is to be recorded in the “Date Column.”

- Amounts to be recorded into the left-hand side are called debits and amounts to be recorded into the right hand side are called credits.

- In the Particulars Column, the source of transaction is recorded. The entry in the debit side begins with the words “To,” that is, “To” is used before the name of the account and “By” is used before the name of an account to be recorded in the credit side.

- The page number of the Journal or Subsidiary Book from which that particular entry is transferred, is to be recorded in the Folio Column.

- The amount pertaining to the account, is recorded in the “Amount Column.”

OBJECTIVE 3: MEANING OF POSTING

Business transactions are usually first recorded in the books of original entry or subsidiary books. Only then they are transferred to the ledger. This process of transferring from the books of original entry in the concerned accounts to the ledger is called “Posting.”The main object of “Posting” is to make classified and summarised record of various transactions during a specified period on a particular account. Net effect of transactions can be had from the ledger at a glance. It is prepared periodically (daily, weekly, fortnightly, monthly, quarterly), depending upon the needs and requirements of the respective business concerns.

OBJECTIVE 4: PROCEDURE OF POSTING

Step 1: Open the account for items of transactions in their respective name, write that account title in BOLD letters at the top, centre portion of the ledger account.

Example: Transaction: Goods sold for cash Rs 1,001.

Journal entry: |

Cash A/c |

Dr. 1,001 |

|

To Sales A/c |

1,001 |

Two ledger accounts have to be opened:

- Cash Account

- Sales Account

Write CASH ACCOUNT in the middle at the top of the ledger.

Like that SALES ACCOUNT for another ledger.

Important Note:

- Once a particular account is opened in the ledger, for example, Sales Account, the same account with the same account title IS NEVER TO BE OPENED again in the same accounting period.

- Each transaction in the Journal is to be considered separately for posting process.

Step 2: For items which have been debited in the Journal Entry:

- Locate in the ledger, the account to be debited. Then enter the date of transaction in the “Date Column” on the debit side.

- Record the name of the account CREDITED IN THE JOURNAL in the “Particulars Column” on the debit side as “To …….. (name of the account credited)……”

- Record the page number of the Journal in the ledger. (Now in the Journal, write the page number of the ledger now recorded.) (Remember in recording the process of journalising transactions, this column was not filled up at that time. It was left blank, being filled up now.)

- Enter the relevant amount in the “Amount Column” on the debit side.

Step 3: For items which have been debited in the Journal Entry:

- Locate in the ledger, the account to be credited and enter the date of transaction in the “Date Column” on the credit side.

- Record the name of the account DEBITED IN THE JOURNAL in the “Particulars Column” on the credit side of the ledger as “By …(name of the account debited) ….”

- Record the page number of the Journal in the “Folio Column” on the credit side of the ledger. Then write this page number of the ledger in the Journal “L.F. Column.”

- Record the relevant amount in the “Amount Column” on the credit side of credit side of the ledger.

Procedure of Posting: Illustrated:

Transaction: Feb 25, 2009: Goods sold for cash Rs 25,000.

Journal entry for this transaction would be:

| Cash A/c | Dr. 25,000 | |||

| To Sales A/c | 25,000 | |||

| (Goods purchased for cash.) | ||||

For posting in the ledger:

- Identify the account: In this transaction two accounts are involved.

- Cash Account

- Sales Account

- First, open “Cash Account”

- Draw the journal of ledger

- Record as “Cash Account” in the top-middle of the note. Cash Account is debited in the journal entry as such, for this, left-hand side of this Cash Account has to be recorded. (For this transaction, now, credit side is ignored.)

- Enter the date Feb 25 2009 in the “Date Column” on the debit side of the ledger.

- Go to the Particulars Column and enter the word “To” (and write the name of the account in the journal entry associated with credit aspect) Sales A/c.

CAUTION: ONE SHOULD NOT WRITE (as in this case) the name of the Cash account in the Particulars column as Cash Account.

- Record the amount Rs 25,000 in the Amount Column on the debit side.

Cash Account

Now, for the item which has been credited in the journal entry, that is, Sales Account Rs 25,000.

- Draw the format of the ledger.

- Enter the name of the account as SALES ACCOUNT on the top-middle in bold letters.

- As the transaction is related to credit aspect, go to the credit side of the ledger and enter the date in the “Date Column.”

- Go to the “Particulars Column,” write the word “By” (followed by the name of the account debited in journal) Cash Account.

Note: One should not write “By Sales Account” in the Particulars Column (of this Sales Account). Only the name of the other account, which is associated with this transaction, that is, Cash Account has to be recorded.

- Record the amount Rs 25,000 in the “Amount Column” on the credit side.

Sales Account

As no information regarding folio number is given, that column can be left blank.

OBJECTIVE 5: DISTINCTION BETWEEN JOURNAL AND LEDGER

Books of Original Entry (Journal) and Ledger may be distinguished as follows:

| Basis of Distinction | Journal | Ledger |

|---|---|---|

1. Recording the transactions |

All the transactions have to be recorded first in this book. |

Transactions that are recorded in Journal are transferred to this book. |

2. Book |

Book of Original Entry It is a subsidiary book. |

This is a book of second entry. It is a principal book of account. |

3. Order of recording transactions |

Transactions are recorded in chronological order. |

Transactions relating to a particular account are recorded at one place. |

4. Variety of transactions |

Transactions relating to a person or property or expense, all categories are recorded. |

Transactions relating to a particular account, only one category, one account is recorded on a particular page. |

5. Unit of classification |

The unit of classification of data in the Journal is “transaction.” |

The unit of classification here is “account.” |

6. Name of the process |

The process of recording transaction is called “journalising.” |

Recording transaction is called “posting.” |

7. Net-effect |

The final position of a particular account cannot be found. |

The final position of a particular account can be found at a glance. |

8. Next stage |

Entries are transferred to ledger. |

From the ledger, Trial Balance is prepared. |

9. Tax-Assessment |

Tax authorities do not rely on Journals. |

They rely on ledger for assessment purpose. |

Illustration: 1

Jan 15, 2009 Cash sales Rs 50,000; Cash received from Babu Rs 10,000; Commission earned Rs 5,000.

You are required to journalise the above transaction and post it into the ledger.

Solution

Stage 1: First, Journal is prepared

- Cash sales – Cash A/c – Real A/c – Cash comes in – Debit what comes in.

- Sales – Real A/c – Goods go out – Credit what goes out.

- Babu –Personal A/c – Giver – Credit the Giver.

- Commission earned – Nominal A/c – Income – Credit all income and gains.

Journal

Stage 2: Posting to Ledger

In the above transaction, there is only one debit aspect ”Cash Account and three Credit aspects “Sales Account, Babu Account and Commission Account.

As such four ledger accounts have to be prepared.

First: Preparation of Cash Account.

- Draw the format.

- As Cash A/c relates to debit aspect, posting has to be done on the debit side.

- Enter the date in the “Date Column.”

- Write “To” followed by (corresponding credit accounts in the Journal), that is, Sales Account, Babu Account, and Commission Account, in the “Particulars Column” on the debit side of this account.

- Enter the amount in the “Amount Column” for each account separately.

Note: While posting in the Cash account, three corresponding accounts have to be recorded.

Cash Account

All the other three accounts, which have been credited in the transaction are prepared as follows:

Sales Account

Babu Account

Commission Account

Note: One Debit account: Cash A/c: Amount (Value): Rs 65,000.

Three Credit accounts: Sales A/c: Rs 50,000; Babu A/c: Rs 10,000; Commission A/c: Rs 5,000; Total: Rs 65,000.

OBJECTIVE 6: POSTING OF AN OPENING ENTRY

The opening entry is passed to open the books of accounts for the new accounting year. The closing balances of the previous year (the same is the opening balance of the new year – current accounting period) are incorporated in the new ledger by posting from the Journal paper.

But strictly speaking, opening entry is not posted in the ledger, but the accounts are merely incorporated in the ledger.

An account, which has a debit balance, the words “To Balance b/d” are written on the debit side of the ledger in the “Particulars Column.” Similarly, an account which has a credit balance, the words “By Balance b/d” are written in the “Particulars Column” on the credit side.

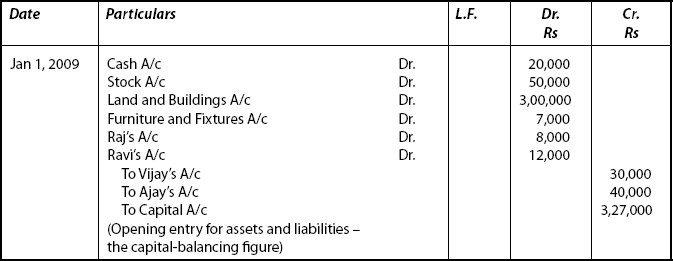

Illustration: 2

From the following particulars, pass the opening entry and post them to ledger.

A trader has the following balances on Jan 1, 2009, the beginning of the new accounting period:

Assets: Cash-in-hand: Rs 20,000; Stock: Rs 50,000;

Land and Buildings: Rs 3,00,000; Furniture and Fixtures: Rs 7,000; Raj: Rs 8,000;

Ravi: Rs 12,000 Liabilities: Vijay: Rs 30,000; Ajay: Rs 40,000

Solution

First opening entries have to be passed.

Journal

Ledger

Cash Account

Stock Account

Land And Building Account

Furniture and Fixtures Account

Raj’s Account

Ravi’s Account

Vijay’s Account

Ajay’s Account

Capital Account

Illustration: 3

Journalise the following transactions and post them into their respective accounts.

2009 |

|

Feb 2 |

Received for cash sales: Rs 27,500; From Yadav: Rs 7,500; Commission: Rs 1,000; |

Feb 5 |

Paid for rent: Rs 2,400; Medicines: Rs 600. |

Solution

Journal Entries

Cash Account

Sales Account

Yadav’s Account

Commission Account

Rent Account

Medicines Account

OBJECTIVE 7: BALANCING AN ACCOUNT AND PROCEDURE FOR BALANCING

Balance of an account is the difference between the total of debits and total of credits appearing in an account when the posting process is completed, ledger accounts have entries on their debit side as well as credit side. The net result of all such debits and credits in an account is termed as “balance.” At times, the total of debit entries and the total of credit sides will be equal. If one side has the greater amount than the other side, such difference is called “balance.”

Balancing means the writing of difference between the amount columns of the debit side and credit side, so as to make the grand totals of the two sides equal.

There are three possible situations while balancing an account during a given period. The net effect of all transactions will result in Debit balance or Credit balance or Nil balance.

- Debit balance: If the total amount on the debit side is more than the total amount on the credit side, such difference is referred to as “debit balance.”

- Credit balance: If the total amount on the credit side is greater than the total amount on the debit side, such difference in the amount itself is called as “credit balance.”

- Nil balance: If the total of the debits and credits are equal, it indicates “nil balance.” It is a closed account, as it has no balance.

7.1 Balancing of Different Accounts

As explained earlier, balancing is the process of equalising the two sides of an account. Before explaining the procedure for balancing a ledger account, we have to look into the types of accounts and their relationship with the “balance” of an account.

- Personal accounts: A personal account may have a debit balance or a credit balance or nil balance. When a personal account has a debit balance, such person is referred to as “debtor.” But when a personal account has a credit balance, such person is termed as “creditor.” In case of nil balance, such persons are neither debtors nor creditors.

- Real accounts: Generally, these accounts are balanced at the end of an accounting period. A debit balance indicates the value of assets owned by the business. These accounts may have a debit balance or nil balance. But these accounts will NEVER have a CREDIT BALANCE.

Balance of these two accounts, that is, Personal accounts and Real accounts are shown in the Balance Sheet.

- Nominal accounts: Generally, nominal accounts are not balanced, as these accounts are concerned with incomes earned or expenses incurred. In case when they are balanced, a debit balance indicates a loss or expense while a credit balance indicates an income or gain. At the end of accounting year, these accounts are closed by transferring direct to either Trading Account or Profit and Loss Account.

7.2 Procedure for Balancing

Procedure for balancing is same for all categories of accounts whether they belong to Personal accounts or Real accounts or Nominal accounts. Steps involved in the procedure for balancing are as follows:

Step 1: |

Total the “Amount Column” on the debit side. Then total the “Amount Column” on the credit side. Ascertain the difference in the total amount. |

Step 2: |

If the debit side total exceeds the credit side total, enter the difference amount in the “Amount Column” of the credit side. Write the date on which balancing is done in the “Date Column.” Then write the words “By Balance c/d” in the “Particulars Column” (c/d means carried down). |

If the credit side total exceeds the debit side total, write the difference amount in the “Amount Column” of the debit side. Write the date on which balance is done in the “Date Column.” Then write the words, “To Balance c/d” in the “Particulars Column.”

Step 3: |

Again total both “Debit Amount Column” and “Credit Amount Column.” Put the total on both the sides and draw a line above and another line below the totals. |

In case, if it is a debit balance, bring down the debit balance on the debit side. Write the words “To Balance b/d” (b/d means brought down) in the “Particulars Column” on the debit side. Write the date of the beginning of next period in the “Date Column.”Write the amount in the “Amount Column”on the debit side. |

If it is a credit balance, bring down the credit balance on the credit side. Write down the words “By Balance b/d” in the “Particulars Column” on the credit side. Write the date of the beginning of next period in the “Date Column.” Write the amount in the a Amount Column” on the credit side.

[In practise, some accountants may use c/f or c/o and b/f or b/o in the place of c/d and b/d. c/f means carried forward, c/o means carried over, b/f means brought forward and b/o denotes brought over. But, in general, when the balance is carried down in the same page the words c/d and b/d are used. But when balance is carried over to the next page, the words c/o and b/o are used. If the balance is carried forward to some other page, the words c/f and b/f are used.]

| Note: | The balancing of the figures is not “posting.” There is no opposite entry in any other account. In such opposite entries, c/d or b/d should be made in the account itself. |

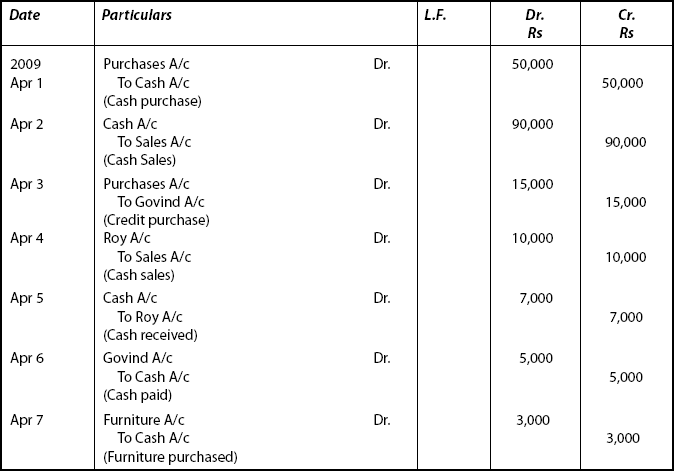

Illustration: 4

Journalise the following transactions in the books of Praveen and post them in the ledger and balance them.

|

Apr 2009 |

1 |

Bought goods for cash Rs 50,000. |

|

|

2 |

Sold goods for cash Rs 90,000. |

|

|

3 |

Bought goods for credit from Govind Rs 15,000. |

|

|

4 |

Sold goods on credit to Roy Rs 10,000. |

|

|

5 |

Received from Roy Rs 7,000. |

|

|

6 |

Paid to Govind Rs 5,000. |

|

|

7 |

Bought furniture for cash Rs 3,000. |

Solution

Journal of Praveen

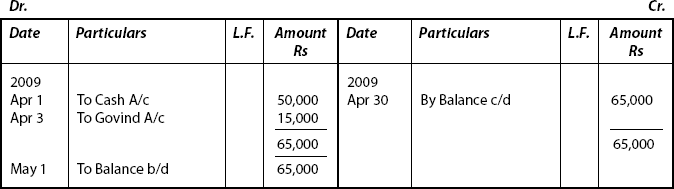

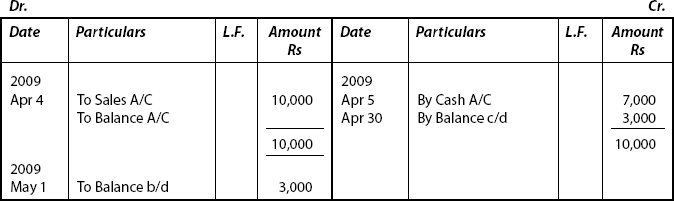

Next, post these journal entries in the ledger. After posting is done, each account is balanced according to the steps explained earlier.

(i) Cash Account

Notes:

- Total of Debit Column: Rs 97,000.

- Total of Credit Column: Rs 58,000.

- Difference: Rs 39,000 (Debit is greater than Credit.)

- It is recorded with words “By Balance c/d” on the credit side.

- This is further brought down to the beginning of next period and the date is written as May 1 in this case and recorded as “To Balance b/d” in the Particulars Column.

- This is called Debit balance, as the excess of debit total over credit total occurs in this case as Rs 39,000.

The procedure explained above is adopted in the following after posting is done.

(ii) Purchases Account

Here, total Debit Column = Rs 65,000

Total Credit Column = 0

As such the entire amount has to be written as “By Balance c/d.”

Other steps remain the same, as explained previously.

(iii) Sales Account

(iv) Furniture Account

(v) Govind’s Account

(vi) Roy’s Account

Note: In case, Nominal accounts are provided, such accounts need not be balanced.

Summary

- Ledger is “a book which contains a classified and permanent record of all the transactions of a business.” A book of original entry.

- Ledger is normally kept in the form of bound note books. Loose Leaf-Ledger in the form of loose sheets – ledger format in individual papers are being maintained.

- The process of transferring from the books of original entry in the concerned accounts in the ledger is referred to as “posting.”

- Distinction between journal and ledger: (Refer: Text)

- Opening Entry: Opening entry is passed to open the books and not posted in the ledger, but the accounts are merely incorporated in the ledger. Debit balance is to be written as “To Balance b/d” and Credit balance is to be written as “By Balance b/d” on the debit and credit side of the ledger respectively.

- Balancing means the writing of the difference between the amount columns of the debit side and credit side, so as to make the end totals of the two sides equal.

- Procedure for balancing (Refer: The Main Part).

A Objective-type Questions

I. State whether the following statements are True or False

- All the transactions relating to a particular account and collected at one place in a book is called the ledger.

- Instead of a single bound note book, loose-sheets may be used.

- Ledger is also called the “Book of Original Entry.”

- The process of transferring the entries recorded in the Journal to the respective accounts opened in the ledger is called “Posting.”

- Balance is the difference between the total debits and total credits of an account.

- The excess of debit total over the credit total is called the debit balance.

- The excess of credit total over the debit total is called the credit balance.

- There is no amount either in the debit column or in the credit column, that is, not even a single transaction is called the nil balance.

- Personal accounts, when balanced, enable one to know the amount due to others or due from others.

- Assets account always show credit balance

- A debit balance in a nominal account indicates that it is an income or gain.

- Nominal accounts, normally, are not balanced.

- All balances in personal and real accounts are to be shown in the Balance Sheet.

- Nominal account balances are not taken to final accounts.

- The closing balance becomes the opening balance in the next accounting year.

Answers

1. True |

2. True |

3. False |

4. True |

5. True |

6. True |

7. True |

8. False |

9. True |

10. False |

11. False |

12. True |

13. True |

14. False |

15. True |

B Multiple-choice Questions

I. Choose the Correct Answer

- Ledger is a book of:

- journalizing

- original entry

- secondary

- all credit transaction

- L.F. column in the Journal is to be entered at the time of:

- journalising

- casting

- balancing

- posting

- The process of transferring the transactions relating to changes in a particular item at one place in the form of an account is called:

- posting

- balancing

- journalizing

- none of the above

- The process of recording a transaction in the journal is called:

- posting

- journalising

- balancing

- none of the above

- The words “To Balance b/f, By Balance b/d are recorded in the “Particular Column” of the ledger book: at the time of

- opening entry

- closing entry

- simple entry

- compound entry

- Personal and real accounts are:

- at sometimes balance

- always balance

- closed

- closed and transferred

- The column of ledger which links the entry with journal is:

- L.F. Column

- J.F. Column

- Amount Column

- Date Column

- Real accounts always show:

- debit balance

- credit balance

- nil balance

- cannot be balanced

- Nominal account having credit balance represents:

- income and gain

- expense or loss

- assets

- liabilities

- Nominal account having debit balance represents:

- assets

- liabilities

- expense or loss

- income or gain

- When the total of the debits and the total of the credits are equal, it represents:

- nil balance

- debit balance

- credit balance

- none of the above

- Account having credit balance is closed by writing:

- To Balance c/d

- By Balance b/d

- To Balance b/d

- By balance b/f

- The balances of personal and real accounts are shown in the:

- Balance Sheet

- Profit and Loss Account

- both

- none of the above

- The nominal accounts are closed by transferring to:

- Balance Sheet

- Profit and Loss Account

- both

- none of the above

- In general, the following accounts are balanced:

- real accounts and nominal accounts

- personal accounts and real accounts

- personal accounts and nominal accounts

- none of the above

Answers

- (c)

- (d)

- (a)

- (b)

- (a)

- (b)

- (b)

- (a)

- (a)

- (c)

- (a)

- (a)

- (a)

- (b)

- (b)

C Short Answer-type Questions

- What is a ledger?

- “Ledger is the book of final entry.” Why?

- Explain the utilities of a ledger

- What is “posting”?

- Mention the different forms in which a ledger may be kept.

- What are the utilities of ledger?

- Explain the meaning of balancing in account.

- Explain the significance of balancing.

- What is debit balance?

- What is credit balance?

- Indicate the nature of balance in the following accounts

- Cash

- Debtors

- Creditors

- Capital

- Purchases

- Sales

- Wages Paid

- Interest Received

- Rent Paid

- Computer

- Distinguish Journal with Ledger.

D Essay-type Questions

- Explain the steps involved in “posting”.

- Explain the procedure for balancing a ledger account.

- Explain the significance of debit and credit balances of various types of accounts with examples.

E Exercises

- Journalise the following transactions in the books of Dev. Post them in the ledger and balance the various accounts opened in the ledger.

2009

Mar 1

Ramkumar commenced business with cash Rs 1,00,000.

Mar 2

Paid into the Bank Rs 60,000.

Mar 5

Purchased goods for cash Rs 70,000.

Mar 7

Sold goods for cash Rs 1,00,000.

Mar 9

Purchased goods from Tiwari Rs 60,000.

Mar 10

Sold goods to Diraj Rs 90,000.

Mar 15

Withdraw cash for personal use Rs 2,000.

Mar 17

Paid travelling charges Rs 1,800.

Mar 20

Paid electric charges Rs 700.

Mar 23

Draw cash from Bank for office purpose Rs 10,000.

Mar 30

Paid salaries to staff Rs 9,000.

- Journalise the following transaction in the books of Govind. Post them in the ledger and balance the various accounts opened in the ledger.

2009

Apr 1

Govind commenced business with the following assets and liabilities.

Cash

Rs 1,00,000

Stock

Rs 75,000

Machinery

Rs 90,000

Furniture

Rs 5,000

Creditors

Rs 1,00,000

Sold goods to Kamal Rs 1,15,000.

Apr 7

Bought goods from Ajay Rs 75,000.

Apr 9

Paid to Ajay Rs 50,000 on account.

Apr 11

Withdraw cash for personal use Rs 3,500.

Apr 13

Received Commission Rs 6,000.

Apr 15

Furniture purchased Rs 9,000.

Apr 17

Brought in additional capital Rs 25,000.

Apr 18

Issued a cheque for rent Rs 6,000.

Apr 19

Drew from bank for personal use Rs 4,000.

Apr 21

Paid life insurance premium Rs 1,327.

- On 1, Apr 2009, the following were the ledger balance of Vasant.

Cash-in-hand – Rs 5,000.

Cash at Bank – Rs 60,000.

Bills-Payable – Rs 7,000.

Stock – Rs 30,000.

Mr. A – Rs 7,000 (Dr.).

Mr. B – Rs 15,000; (Cr).

Mr. C. –Rs 9,000 (Dr.).

Mr. D – Rs 4,300 (Cr).

Other transactions

Apr 2 Bought goods from Mr. B – Rs 7,500. Apr 4 Sold goods to Mr. B – Rs 6,000. Apr 6 Bought goods from Mr. D – Rs 7,000. Apr 8

Sold to Mr. A – Rs 4,000.

Apr 10

Paid to Mr. by cheque – Rs 9,000.

Apr 12

Received from Mr. C – Rs 10,000.

Allowed him discount – Rs 100.

Apr 14

Accepted Mr. D‘s bills at 2 months Rs 5,000.

Apr 15

Sold goods to Mr. C – Rs 6,500.

Apr 17

Paid rent by cheque – Rs 2,300.

Apr 20

Sold to Mr. A – Rs 8,000.

Apr 22

Paid salaries by cheque – Rs 4,800.

Make journal entries and post them to ledger and balance them.

- Prepare Ajay’s account as it would appear in the books of Vijay.

- Prepare Krishna’s account in the books of Venkat and Venkat’s account in the ledger of Krishna.

- Record the following transactions in the journal of Anand and open only personal account in the ledger and balance them.

2009

May 1

Anand

started business with Rs 1,00,000.

May 2

Purchased goods from Sachin Rs 25,000.

May 7

Purchased furniture Rs 12,000 from King Enterprises.

May 9

Goods returned to Sachin – Rs 650.

May 13

Goods sold to Gopi for Rs 9,000.

May 15

Paid to Sachin Rs 19,500 and discount received Rs 500.

May 17

Goods returned by Gopi Rs 350.

May 25

Cash returned from Gopi – Rs 7,000.

May 27

Paid rent by cheque to the landlord Rs 5,000.

May 30

Paid to Sachin Rs 2,000.