In this more advanced trading strategy, we are going to create a long signal when the price reaches the highest price for the last window_size days (in this example, we will choose 50):

- We will create a short signal when the price reaches its lowest point. We will get out of a position by having the price crossing the moving average of the last window_size days. This code starts the turtle_trading function by creating a column to store the highs, the lows, and the average with a rolling window window_size:

def turtle_trading(financial_data, window_size):

signals = pd.DataFrame(index=financial_data.index)

signals['orders'] = 0

# window_size-days high

signals['high'] = financial_data['Adj Close'].shift(1).

rolling(window=window_size).max()

# window_size-days low

signals['low'] = financial_data['Adj Close'].shift(1).

rolling(window=window_size).min()

# window_size-days mean

signals['avg'] = financial_data['Adj Close'].shift(1).

rolling(window=window_size).mean()

- We will write the code that creates two new columns specifying the rules to place an order:

- The entry rule is stock price > the highest value for the window_size day.

- Stock price < the lowest value for the window_size day:

signals['long_entry'] = financial_data['Adj Close'] > signals.high

signals['short_entry'] = financial_data['Adj Close'] < signals.low

- The exit rule (when placing an order to get out of a position) will be when the stock price crosses the mean of past window_size days:

signals['long_exit'] = financial_data['Adj Close'] < signals.avg

signals['short_exit'] = financial_data['Adj Close'] > signals.avg

- To draw the chart representing the orders, as shown in the code, we will give the values 1 when we enter a long position, -1 when we enter a short position, and 0 for not changing anything:

init=True

position=0

for k in range(len(signals)):

if signals['long_entry'][k] and position==0:

signals.orders.values[k] = 1

position=1

elif signals['short_entry'][k] and position==0:

signals.orders.values[k] = -1

position=-1

elif signals['short_exit'][k] and position>0:

signals.orders.values[k] = -1

position = 0

elif signals['long_exit'][k] and position < 0:

signals.orders.values[k] = 1

position = 0

else:

signals.orders.values[k] = 0

return signals

ts=turtle_trading(goog_data, 50)

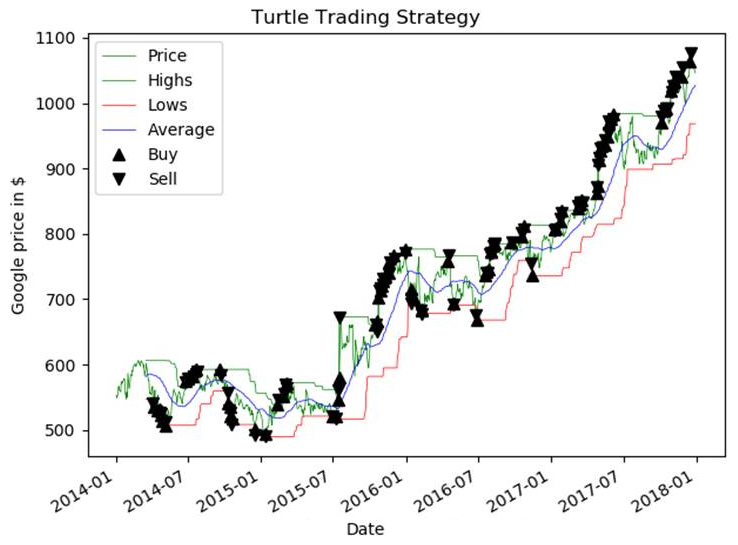

The turtle_trading function from the code will display the plot that describes how the strategy behaves:

From the plot, the following can be observed:

- The number of orders between the naive momentum strategy and the turtle trading strategy.

- On account of a higher number of orders, this strategy offers more potential of returns than the previous one.