In this section, we will implement a naive strategy based on the number of times a price increases or decreases. This strategy is based on the historical price momentum. Let's have a look at the code:

def naive_momentum_trading(financial_data, nb_conseq_days):

signals = pd.DataFrame(index=financial_data.index)

signals['orders'] = 0

cons_day=0

prior_price=0

init=True

for k in range(len(financial_data['Adj Close'])):

price=financial_data['Adj Close'][k]

if init:

prior_price=price

init=False

elif price>prior_price:

if cons_day<0:

cons_day=0

cons_day+=1

elif price<prior_price:

if cons_day>0:

cons_day=0

cons_day-=1

if cons_day==nb_conseq_days:

signals['orders'][k]=1

elif cons_day == -nb_conseq_days:

signals['orders'][k]=-1

return signals

ts=naive_momentum_trading(goog_data, 5)

In this code, the following applies:

- We count the number of times a price is improved.

- If the number is equal to a given threshold, we buy, assuming the price will keep rising.

- We will sell if we assume that the price will keep going down.

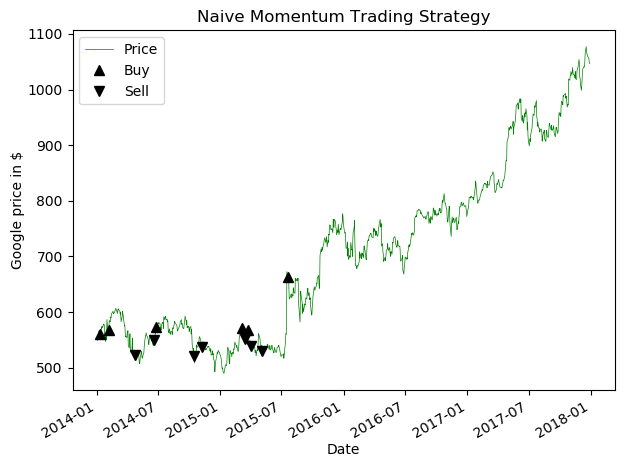

We will display the evolution of the trading strategy by using the following code:

fig = plt.figure()

ax1 = fig.add_subplot(111, ylabel='Google price in $')

goog_data["Adj Close"].plot(ax=ax1, color='g', lw=.5)

ax1.plot(ts.loc[ts.orders== 1.0].index,

goog_data["Adj Close"][ts.orders == 1],

'^', markersize=7, color='k')

ax1.plot(ts.loc[ts.orders== -1.0].index,

goog_data["Adj Close"][ts.orders == -1],

'v', markersize=7, color='k')

plt.legend(["Price","Buy","Sell"])

plt.title("Turtle Trading Strategy")

plt.show()

This code will return the following output. This curve represents the orders for the naive momentum trading strategy:

From this plot, the following can be observed:

- The naive trading strategy does not produce many orders.

- We can have a higher return if we have more orders. For that, we will use the following strategy to increase the number of orders.