Duration is a sensitivity measure of bond prices to yield changes. Some duration measures are: effective duration, Macaulay duration, and modified duration. The type of duration that we will discuss is modified duration, which measures the percentage change in bond price with respect to a percentage change in yield (typically 1 percent or 100 basis points (bps)).

The higher the duration of a bond, the more sensitive it is to yield changes. Conversely, the lower the duration of a bond, the less sensitive it is to yield changes.

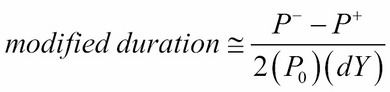

The modified duration of a bond can be thought of as the first derivative of the relationship between price and yield:

Here, dy is the given change in yield, ![]() is the price of the bond from a decrease in yield by dy,

is the price of the bond from a decrease in yield by dy, ![]() is the price of the bond from an increase in yield by dy, and

is the price of the bond from an increase in yield by dy, and ![]() is the initial price of the bond.

is the initial price of the bond.

It should be noted that the duration describes the linear price-yield relationship for a small change in Y. Because the yield curve is not linear, using a large value of dy does not approximate the duration measure well.

The implementation of the modified duration calculator is given in the following Python code. The bond_mod_duration function uses the bond_ytm function as discussed earlier in this chapter to determine the yield of the bond with the given initial value. Also, it uses the bond_price function to determine the price of the bond with the given change in yield:

""" Calculate modified duration of a bond """

from bond_ytm import bond_ytm

from bond_price import bond_price

def bond_mod_duration(price, par, T, coup, freq, dy=0.01):

ytm = bond_ytm(price, par, T, coup, freq)

ytm_minus = ytm - dy

price_minus = bond_price(par, T, ytm_minus, coup, freq)

ytm_plus = ytm + dy

price_plus = bond_price(par, T, ytm_plus, coup, freq)

mduration = (price_minus-price_plus)/(2*price*dy)

return mduration We can find out the modified duration of the 5.75 percent bond discussed earlier that will mature in 1.5 years with a par value of 100 and a bond price of 95.0428:

>>> from bond_mod_duration import bond_mod_duration >>> print bond_mod_duration(95.04, 100, 1.5, 5.75, 2, 0.01) 1.392

The modified duration of the bond is 1.392 years.