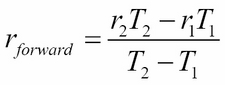

An investor who plans to invest at a later time might be curious to know what the future interest rate might look like, as implied by today's term structure of interest rates. For example, you might ask: What is the one-year spot rate one year from now? To answer this question, one can calculate forward rates for the period between ![]() and

and ![]() using this formula:

using this formula:

Here, ![]() and

and ![]() are the continuously compounded annual interest rates at time period

are the continuously compounded annual interest rates at time period ![]() and

and ![]() respectively.

respectively.

The following Python code helps us generate a list of forward rates from a list of spot rates:

"""

Get a list of forward rates

starting from the second time period

"""

class ForwardRates(object):

def __init__(self):

self.forward_rates = []

self.spot_rates = dict()

def add_spot_rate(self, T, spot_rate):

self.spot_rates[T] = spot_rate

def __calculate_forward_rate___(self, T1, T2):

R1 = self.spot_rates[T1]

R2 = self.spot_rates[T2]

forward_rate = (R2*T2 - R1*T1)/(T2 - T1)

return forward_rate

def get_forward_rates(self):

periods = sorted(self.spot_rates.keys())

for T2, T1 in zip(periods, periods[1:]):

forward_rate =

self.__calculate_forward_rate___(T1, T2)

self.forward_rates.append(forward_rate)

return self.forward_ratesUsing spot rates derived from our preceding yield curve, we get the following result:

>>> fr = ForwardRates() >>> fr.add_spot_rate(0.25, 10.127) >>> fr.add_spot_rate(0.50, 10.469) >>> fr.add_spot_rate(1.00, 10.536) >>> fr.add_spot_rate(1.50, 10.681) >>> fr.add_spot_rate(2.00, 10.808) >>> print fr.get_forward_rates() [10.810999999999998, 10.603, 10.971, 11.189]

Calling the get_forward_rates method of the ForwardRates class returns a list of forward rates, starting from the next time period.