APPENDIX I

Description of Bloomberg Screen CDSW

Screen CDSW on the BLOOMBERG PROFESSIONAL® service, an example of which was shown in Figure 1.7, is an implementation of the procedure for pricing a CDS described in Hull and White (2000). The input used in the model to price the CDS contract is one of the three described in Chapter 1. The Bloomberg links the market in CDS prices and the cash bond market with issuer default probabilities.

To calculate the present value of the CDS fee leg (premium leg), the Bloomberg uses the curve of probabilities of default of the reference entity. To calculate the expected present value of the CDS contingent leg, it requires additionally an assumption on the payoff in the case of default; for this, it uses [(par−R)+Accrued], where R is the recovery rate. The theoretical value of the CDS is then the difference in the expected present values of the two legs.

Calculating the Default Probability Curve

Given a curve of par CDS spreads (spreads of CDSs of various maturities, each with net present value of zero), the system calculates an implied default probability curve by using a bootstrap procedure. Thus, it finds a default probability curve such that all given CDS contracts have zero value. An alternative procedure is that, given a curve of risky par coupon rates (bond yields), the system calculates the default probability curve implied by this curve, again using a bootstrap process. The assumption is made that in the case of default of a bond, its value drops to a fraction R of par.

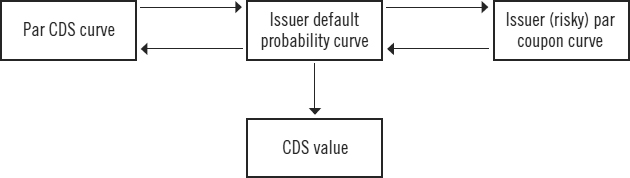

FIGURE AI.1 Transforming curves

Calculating an Implied Issuer Par Coupon Curve (the “Risky Curve”)

If a default probability curve is known, the system can compute a corresponding curve of par coupon rates, corresponding to the size of the coupons an issuer of bonds will have to pay, in order to compensate investors for the default risk they are taking on. In other words, given the par CDS curve, the issuer default probability curve, or the issuer (risky) par coupon curve, the system transforms it into the other two curves (see FIGURE AI.1).

Liquidity Premium

The observed spread between an issuer par curve and the risk-free par curve reflects a liquidity premium as well as default risk. The liquidity premium field is a flat spread and selected measure of liquidity. This spread is deducted from the spread between the risky and the risk-free curves before calculation of the default probabilities. A market convention for the liquidity premium is the spread between AAA rates and the interbank swap rate. This spread generally lies within a 0 to 25 basis-point magnitude. The screen defaults to 0 bps.

Issuer Spread-to-Fair Value

The Bloomberg assigns a relevant fair market curve to each bond in accordance with its currency, industry sector, and credit rating (for example, USD A-rated utilities). It also assigns an option-adjusted spread to each issuer, so that the default probability analysis becomes issuer-specific rather than industry-specific.1

References

Choudhry, M. 2001. The bond and money markets: Strategy, trading, analysis. Oxford: Butterworth-Heinemann.

Hull, J., and A. White. 2000. Valuing credit default swaps I: No counterparty default risk. Journal of Derivatives 8 (1) (Fall): 29–40.

1. See Choudhry (2001) for more information on option-adjusted spread.