Chapter 16

Examining Cash Inflow and Outflow

In This Chapter

![]() Discovering the ins and outs of accounts receivable

Discovering the ins and outs of accounts receivable

![]() Considering the nuts and bolts of accounts payable

Considering the nuts and bolts of accounts payable

![]() Digging into discount offers

Digging into discount offers

Is the money flowing? That's the million-dollar, and sometimes multimillion-dollar, question. Measuring how well a company manages its inflow and outflow of cash is crucial to being able to stay in business. Cash is king in business — without it, you can't pay the bills.

In this chapter, I review the key ratios for gauging cash flow and show you how to calculate them. In addition, I explore how companies use their internal financial reporting to monitor slow-paying customers, and I discuss whether paying bills early or on time is better — and how you can test that issue.

Assessing Accounts Receivable Turnover

Sales are great, but if customers don't pay on time, the sales aren't worth much to a business. In fact, someone who doesn't pay for the products he takes is no better for business than a thief. When you're assessing a company's future prospects, one of the best ways to judge how well it's managing its cash flow is to calculate the accounts receivable turnover ratio.

A balance sheet lists customer credit accounts under the line item Accounts receivable. Any company that sells its goods on credit to customers must keep track of whom it extends credit to and whether those customers pay their bills.

Financial transactions involving credit card sales aren't figured into accounts receivable, but are handled like cash. The type of credit I'm referring to here is in-store credit. In this case, the bill the customer receives comes directly from the store or company where the customer purchased the item.

Financial transactions involving credit card sales aren't figured into accounts receivable, but are handled like cash. The type of credit I'm referring to here is in-store credit. In this case, the bill the customer receives comes directly from the store or company where the customer purchased the item.

When a store makes a sale on credit, it enters the purchase on the customer's credit account. At the end of each billing period, the store or company sends the customer a bill for the purchases she made on credit. The customer usually has between 10 and 30 days from the billing date to pay the bill. When you calculate the accounts receivable turnover ratio, you're seeing how fast the customers are actually paying those bills.

Calculating accounts receivable turnover

Here's the three-step formula for testing accounts receivable turnover:

- Calculate the average accounts receivable:

-

Find the accounts receivable turnover ratio:

-

Net sales ÷ Average accounts receivable = Accounts receivable turnover ratio

-

-

Find the average sales credit period (the time it takes customers to pay their bills):

-

52 weeks ÷ Accounts receivable turnover ratio = Average sales credit period

-

If you work inside the company, an even better test is to use annual credit sales instead of net sales because net sales include both cash and credit sales. But if you're an outsider reading the financial statements, you can't find out the credit sales number.

If you work inside the company, an even better test is to use annual credit sales instead of net sales because net sales include both cash and credit sales. But if you're an outsider reading the financial statements, you can't find out the credit sales number.

I show you how to test accounts receivable turnover by using Mattel's and Hasbro's 2012 income statements and balance sheets.

I show you how to test accounts receivable turnover by using Mattel's and Hasbro's 2012 income statements and balance sheets.

Mattel

-

Calculate the average accounts receivable:

-

($1,226,833,000 + $1,029,959,000) ÷ 2 = $1,236,760,000

-

-

Find Mattel's accounts receivable turnover ratio for 2012:

-

$6,420,881,000 (Net sales) ÷ $1,236,760,000 (Average accounts receivable) = 5.19 times

-

-

Find the average credit collection period:

-

52 weeks ÷ 5.19 (Accounts receivable turnover ratio) = 10.02 weeks

-

Mattel's customers averaged about 10.2 weeks to pay their bills.

Comparing this data with the previous year's is a good way to see whether the situation is getting better or worse. If you use the same process to calculate Mattel's 2011 average credit collection period, you find that the answer is 5.07 weeks, meaning that the company took slightly longer in 2011 to collect than it did in 2012. To understand the significance of this, look at what's happening with similar companies, as well as what's happening within the industry as a whole. It may be an internal company problem, or it may be an industry-wide problem related to changes in the economic situation.

Hasbro

-

Calculate Hasbro's average accounts receivable:

-

($1,029,959,000 + $1,034,580,000)/2 = $1,032,270,000

-

-

Calculate Hasbro's accounts receivable turnover ratio for 2012:

-

$4,088,983,000 (Net sales) ÷ $1,032,270,000 (Average accounts receivable) = 3.96 times

-

-

Calculate the average sales credit period:

-

52 weeks ÷ 3.96 (Accounts receivable turnover ratio) = 13.13 weeks

-

Hasbro's accounts receivable turned over at a rate slower than Mattel's.

Is that an improvement or a step backward for Hasbro? Using the 2011 numbers, you find that Hasbro took 12.52 weeks to collect from its customers. So the company experienced deterioration in its accounts receivable collection.

What do the numbers mean?

The higher an accounts receivable turnover ratio is, the faster a company's customers are paying their bills. Most times, the accounts receivable collection is directly related to the credit policies that the company sets. For example, a high turnover ratio may look very good, but that ratio may also mean that the company's credit policies are too strict and that it's losing sales because few customers qualify for credit. A low accounts receivable turnover ratio usually means that a company's credit policies are too loose, and the company may not be doing a good job of collecting on its accounts. In the case of Mattel and Hasbro, the slow pay rates may be indicative of the economic environment in the toy industry since the 2008 bubble burst, not a major problem with their credit approval processes.

Hasbro's customers took an average of 13.13 weeks to pay their bills in 2012. Mattel's customers paid quicker, at 10.02 weeks. Both companies waited more than two months to get paid. The amount sitting in accounts receivable for Mattel decreased by about $20 million between 2011and 2012. Hasbro also experienced a decrease in accounts receivable of almost $5 million.

Both companies seem to be improving their collections after what was one of the most severe downturns in the economy since the Great Depression.

Taking a Close Look at Customer Accounts

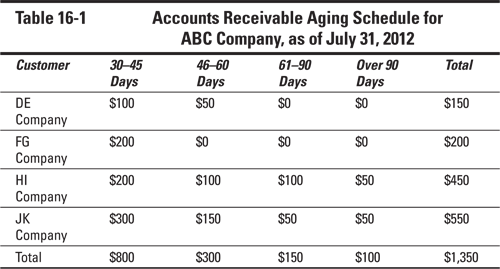

If you work inside a company and have responsibility for customer accounts, you get an internal financial report called the accounts receivable aging schedule. This schedule summarizes the customers with outstanding accounts, the amounts they have outstanding, and the number of days that their bills are outstanding. Each company designs its own report, so they don't all look the same. Check out Table 16-1 to see an example of an accounts receivable aging schedule.

Looking at the aging schedule, you can quickly see which companies are significantly past due in their payments. Many firms begin cutting off customers whose accounts are more than 60 or 90 days past due. Other firms cut off customers when they're more than 120 days past due. No set accounting rule dictates when to cut off customers who haven't paid their bills; this decision depends on the accounting policies the company sets.

In the aging schedule example for ABC Company, the JK Company looks like its account needs some investigating. Although a company can carry past-due payments because of a dispute about a bill, after that dispute goes beyond 90 days, the company awaiting payment may put restrictions on the other company's future purchases until its account gets cleaned up. HI Company seems to be another slow-paying company that may need a call from the accounts receivable manager or collections department.

Many times, a company salesperson makes the first contact with the customer. If the salesperson is unsuccessful, the business initiates more severe collection methods, with the highest level being an outside collection agency. Companies with strong collection practices place a gentle reminder call when an account is more than 30 days late and push harder as the account goes more past due.

When a business decides that it probably will never collect on an account, it writes off the account as a bad debt in the Allowance for Bad Debt Account. Each company sets its own policies about how quickly it writes off a bad debt. A company usually reviews its accounts for possible write-offs at the end of each accounting period. I talk more about accounts receivable and their impact on cash flow in Chapter 17.

Finding the Accounts Payable Ratio

A company's reputation for paying its bills is just as important as its ability to collect from its own customers. If a company develops the reputation of being a slow payer, it can have a hard time buying on credit. The situation can get even more serious if a company is late paying on its loans. In that case, the business can end up with increased interest rates while its credit rating drops lower and lower. I discuss the importance of a good credit rating in Chapter 21.

You can test a company's bill-paying record with the accounts payable turnover ratio. In addition, you can check how many days a company takes to pay its bills by using the days in accounts payable ratio. Keep reading to find out how to calculate these ratios.

Calculating the ratio

The accounts payable turnover ratio measures how quickly a company pays its bills. You calculate this ratio by dividing the cost of goods sold (you find this figure on the income statement) by the average accounts payable (you find the accounts payable figures on the balance sheet).

Here's the formula for the accounts payable turnover ratio:

Cost of goods sold ÷ Average accounts payable = Accounts payable turnover ratio

I use Mattel's and Hasbro's income statements and balance sheets for 2012 to compare their accounts payable turnover ratios.

Mattel

-

Find the average accounts payable:

-

$334,999,000 (2011 accounts payable) + $385,375,000 (2012 accounts payable) ÷ 2 = $360,187,000 (Average accounts payable)

-

-

Use that number to calculate Mattel's accounts payable turnover ratio:

-

$3,011,684 (Cost of goods sold) ÷ $360,187,000 (Average accounts payable) = 8.4 times

-

Mattel turns over its accounts payable 8.4 times per year.

Hasbro

-

Find the average accounts payable:

-

$134,864,000 (2011 accounts payable) + $139,906,000 (2012 accounts payable) ÷ 2 = $137,385,000 (Average accounts payable)

-

-

Calculate Hasbro's accounts payable turnover ratio:

-

$1,671,980 (Cost of goods sold) ÷ $137,385,000 (Average accounts payable) = 12.7 times

-

Hasbro turns over its accounts payable 12.7 times per year, which is faster than Mattel.

What do the numbers mean?

The higher the accounts payable turnover ratio, the shorter the time between purchase and payment. A low turnover ratio may indicate that a company has a cash-flow problem. Hasbro is paying its bills more rapidly than Mattel.

Each industry has its own set of ratios. The only way to accurately judge how a company is doing paying its bills is to compare it with similar companies and the industry.

Determining the Number of Days in Accounts Payable

The number of days in accounts payable ratio lets you see the average length of time a company takes to pay its bills.

If a company is taking longer to pay its bills each year, or if it pays its bills over a longer time period than other companies in its industry, it may be having a cash-flow problem. Similarly, if a company pays its bills slower than other companies in the same industry, that could be a problem, too.

Calculating the ratio

Use the following formula to calculate the number of days in accounts payable:

- Average accounts payable ÷ Cost of goods sold × 360 days = Days in accounts payable

Note: The industry uses 360 days rather than a full year's 365 to make this calculation based on an average 30-day month (30 × 12 = 360).

I use Mattel's and Hasbro's balance sheets and income statements to find the number of days in accounts payable ratio. I don't have to calculate average accounts payable because I already did so when I calculated the accounts payable turnover ratio (see the section “Finding the Accounts Payable Ratio,” earlier in this chapter).

Mattel

- $360,187,000 (Average accounts payable) ÷ $3,011,684,000 (Cost of goods sold) × 360 = 43.1 days

Mattel takes about 43.1 days to pay its bills, or about 6.2 weeks, which is about 4 weeks less than it takes Mattel to collect from its customers — 10.02 weeks, as the accounts receivable turnover ratio shows. Therefore, Mattel is receiving cash from its customers at a slower rate than it's paying out in cash to its vendors and suppliers. This issue may be a factor in the need for short-term borrowings of $9,844 million, as the balance sheet shows.

Hasbro

- $137,385,000 (Average accounts payable) ÷ $1,671,980,000 (Cost of goods sold) × 360 = 29.6 days

Hasbro takes about 29.6 days, or 4.2 weeks, to pay its bills. Hasbro's accounts receivable turnover ratio shows that its customers take slightly more than 13.12 weeks to pay their bills. Therefore, Hasbro must pay its bills more quickly than its customers pay theirs, which could cause a cash-flow problem.

What do the numbers mean?

If the number of days a company takes to pay its bills increases from year to year, it may be a red flag indicating a possible cash-flow problem. To know for certain what's happening, compare the company with similar companies and the industry averages.

If the number of days a company takes to pay its bills increases from year to year, it may be a red flag indicating a possible cash-flow problem. To know for certain what's happening, compare the company with similar companies and the industry averages.

Just as accounts receivable prepares an aging schedule for customer accounts, companies prepare internal financial reports for accounts payable that show which companies they owe money to, the amount they owe, and the number of days for which they've owed that amount.

Deciding Whether Discount Offers Make Good Financial Sense

One common way companies encourage their customers to pay early is to offer them a discount. When a discount is offered, a customer (in this case, the company that must pay the bill) may see a term such as “2/10 net 30” or “3/10 net 60” at the top of its bill. “2/10 net 30” means that the customer can take a 2 percent discount if it pays the bill within 10 days; otherwise, it must pay the bill in full within 30 days. “3/10 net 60” means that if the customer pays the bill within 10 days, it can take a 3 percent discount; otherwise, it must pay the bill in full within 60 days.

Taking advantage of this discount saves customers money, but if a customer doesn't have enough cash to take advantage of the discount, it needs to decide whether to use its credit line to do so. Comparing the interest saved by taking the discount with the interest a company must pay to borrow money to pay the bills early can help the company decide whether using credit to get the discount is a wise decision.

Calculating the annual interest rate

The formula for calculating the annual interest rate is:

- ([% discount] ÷ [100 – % discount]) × (360 ÷ Number of days paid early) = Annual interest rate

I calculate the interest rate based on the early payment terms I stated earlier.

For terms of 2/10 net 30

You first must calculate the number of days that the company would be paying the bill early. In this case, it's paying the bill in 10 days instead of 30, which means it's paying the bill 20 days earlier than the terms require. Now calculate the interest rate, using the annual interest rate formula:

- (2 [% discount] ÷ 98 [100 – 2]) × (360 ÷ 20 [Number of days paid early]) = 36.73%

That percentage is much higher than the interest rate the company may have to pay if it needs to use a credit line to meet cash-flow requirements, so taking advantage of the discount makes sense. For example, if a company has a bill for $100,000 and takes advantage of a 2 percent discount, it has to pay only $98,000, and it saves $2,000. Even if it must borrow the $98,000 at an annual rate of 10 percent, which would cost about $544 for 20 days, it still saves money.

For terms of 3/10 net 60

First, find the number of days the company would be paying the bill early. In this case, it's paying the bill within 10 days, which means it's paying 50 days earlier than the terms require. Next, calculate the interest rate, using this formula:

- (3 [% discount] ÷ 97 [100 – 3]) × (360 ÷ 50 [Number of days paid early]) = 22.27%

Paying 50 days earlier gives the company an annual interest rate of 22.27 percent, which is likely higher than the interest rate it would have to pay if it needed to use a credit line to meet cash-flow requirements. But the interest rate isn't nearly as good as the terms of 2/10 net 30. A company with 3/10 net 60 terms will probably still choose to take the discount, as long as the cost of its credit lines carries an interest rate that's lower than the rate that's available with these terms.

What do the numbers mean?

For most companies, taking advantage of these discounts makes sense as long as the annual interest rate calculated using this formula is higher than the one they must pay if they borrow money to pay the bill early. This becomes a big issue for companies because, unless their inventory turns over very rapidly, 10 days probably isn't enough time to sell all the inventory purchased before they must pay the bill early. Their cash would come not from sales but, more likely, from borrowing.

If cash flow is tight, a company has to borrow funds using its credit line to take advantage of the discount. For example, if the company buys $100,000 in goods to be sold at terms of 2/10 net 30, it can save $2,000 by paying within 10 days. If the company hasn't sold all the goods, it has to borrow the $100,000 for 20 days, which wouldn't be necessary if it didn't try to take advantage of the discount. I assume that the annual interest on the company's credit line is 9 percent. Does it make sense to borrow the money?

The company would need to pay the additional interest on the amount borrowed only for 20 additional days (because that's the number of days the company must pay the bill early). Calculating the annual interest of 9 percent of $100,000 equals $9,000, or $25 per day. Borrowing that money would cost an additional $500 ($25 times 20 days). So even though the company must borrow the money to pay the bill early, the $2,000 discount would still save it $1,500 more than the $500 interest cost involved in borrowing the money.