Chapter 10

Considering Consolidated Financial Statements

In This Chapter

![]() Understanding consolidation

Understanding consolidation

![]() Seeing how companies buy companies

Seeing how companies buy companies

![]() Exploring consolidated financial statements

Exploring consolidated financial statements

![]() Turning to the notes for details

Turning to the notes for details

Like couples who marry and work to combine two incomes, two sets of financial obligations, and two ways of managing money, situations get complicated when companies decide to join forces or buy other companies and combine their financial statements. This new arrangement can make it much harder for you to find out how each piece of this new entity performs financially. In this chapter, I discuss how to read the more complex financial reports that arise when companies consolidate.

Getting a Grip on Consolidation

One of the ways businesses grow is buying or merging with other companies. When a company buys another, it gobbles up the new one, which loses its identity. But when firms decide to merge, they usually decide jointly how the new company will operate and how to present the financial statements.

Major corporations that own more than 50 percent of a company create financial reports for each division. These entities include subsidiaries, joint ventures, and associates. Here's how they stack up:

- Subsidiaries are entities that a larger entity, usually a corporation, controls. The corporation controlling the subsidiary is called the parent company. I discuss the various ways a company can become a subsidiary in the next section, “Looking at Methods of Buying up Companies.”

- Joint ventures are entities in which venturers (usually two or more corporations) share joint control over the economic activity.

- Associates are entities over which the parent company has significant influence, but not the level of control it has over a subsidiary.

If a company's financial report mentions these entities in any detail, you find it in the notes to the financial statements. Most times, you know only that a company has subsidiaries or associates, or participates in joint ventures, if you see “Consolidated” noted at the top of the page on the balance sheet (see Chapter 6) or income statement (see Chapter 7).

If a company's financial report mentions these entities in any detail, you find it in the notes to the financial statements. Most times, you know only that a company has subsidiaries or associates, or participates in joint ventures, if you see “Consolidated” noted at the top of the page on the balance sheet (see Chapter 6) or income statement (see Chapter 7).

If you look at Mattel's or Hasbro's statements online (http://investor.shareholder.com/mattel/financials.cfm; http://investor.hasbro.com/annuals.cfm), you see that each statement indicates that it represents the financial results of the parent company and its subsidiaries. However, you don't see any listing on the balance sheet or income statement of what those subsidiaries are. In fact, unless a company discusses a merger, acquisition, or sale of a subsidiary, associate, or joint venture in the notes to the financial statements, you probably won't see them mentioned individually in the current year's financial report. If no financial transactions occur in the year being reported, the company may only highlight some of its subsidiaries’ successes in the narrative pages in the front of the financial report.

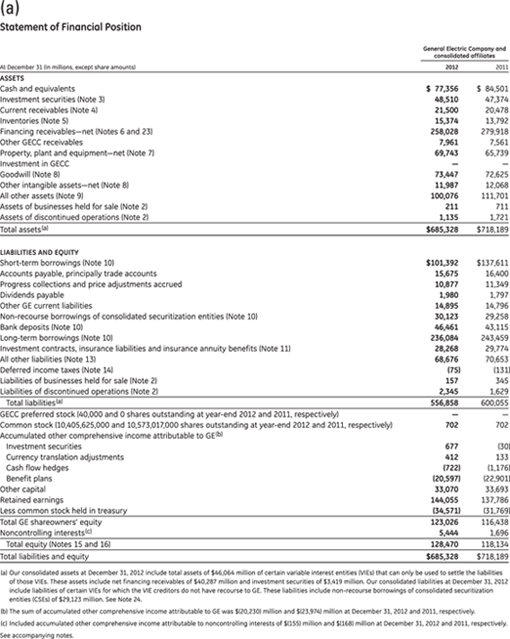

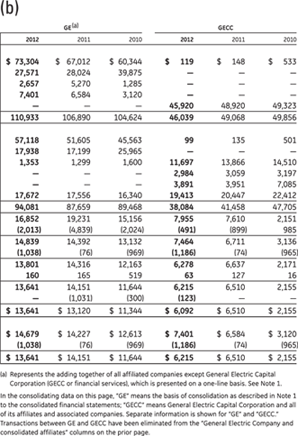

General Electric's consolidated statements are among the easier to navigate because almost every line item of the financial statements indicates which note to look for in the notes to the financial statements for more details about that line item. The Association for Investment Management and Research (AIMR) has cited GE as having one of the best practices for presenting financial information. See Figures 10-1 and 10-2.

General Electric's consolidated statements are among the easier to navigate because almost every line item of the financial statements indicates which note to look for in the notes to the financial statements for more details about that line item. The Association for Investment Management and Research (AIMR) has cited GE as having one of the best practices for presenting financial information. See Figures 10-1 and 10-2.

You can see GE's complete annual report online at www.ge.com/ar2012/.

Most companies play a game of cat-and-mouse, hiding relevant data in the notes to the financial statements, hoping that you won't take the time to find it in the small print. Look at the statements for Hasbro and Mattel on their websites. Neither statement mentions which notes are relevant to the line items on their balance sheets or income statements. You have to scour the notes to find out which material is relevant to which parts of each of their financial statements.

Figure 10-1: GE balance sheet.

Figure 10-1: GE balance sheet.

Figure 10-2: GE income statement.

Figure 10-2: GE income statement.

Looking at Methods of Buying up Companies

One of the most common ways companies grow is to buy up smaller companies. Either these smaller companies get completely gobbled up, with no outward sign that they ever existed, or they become subsidiaries operating under the umbrella of the firm that bought them.

A company can take control over another company by using any of three different methods: statutory merger, statutory consolidation, or stock acquisition. Only when a company buys another using the stock acquisition method does it become a subsidiary. Here's a brief overview of the ways one company can buy another:

- Statutory merger: This merger occurs when one company acquires all the assets of another and accepts the responsibilities of all its liabilities. The company that's taken over goes out of business and is no longer a separate legal entity. The financial results of the business that disappeared become part of the consolidated financial results of the company that remains.

- Statutory consolidation: In this situation, two companies agree to combine to form one new entity; one company does not take over the other. When the transaction is complete, only one legal entity survives, either under one of the original names of the two companies or under a completely new name. Their financial results are combined in a consolidated financial statement.

-

Stock acquisition: In this case, two companies combine, but both remain separate legal entities after the transaction. The company that buys the stock emerges as the parent firm, and the other company becomes the subsidiary. The parent company takes on all the subsidiary's responsibilities and liabilities, and the financial statements of the two are consolidated into the parent company's financial statements.

Two types of stock acquisition exist:

Two types of stock acquisition exist:- Majority interest: When a company buys more than 50 percent of another company's stock, this represents a majority interest. When a company buys 100 percent of another company's stock, but the two businesses don't merge, the subsidiary is called a wholly owned subsidiary.

- Minority interest: When a company or individual owns less than 50 percent of a corporation's voting stock, that's a minority interest. A consolidated balance sheet that indicates minority interest shows the interests of minority shareholders as a liability, an equity, or between the liabilities and equities sections.

Subsidiaries are the entities left in place after a company acquires another company using the stock acquisition method. If you were a shareholder in the subsidiary before it was bought out, you won't find tracking the company that you originally owned easy. Instead, you'll find that most of the financial detail is now just part of the consolidated financial statements of the larger firm.

Stock acquisition is the most common method for taking control of another company because it's cheaper than paying for all the company's assets. To control another company, a parent company needs to buy more than 50 percent of its stock. This type of acquisition doesn't require the difficult and more time-consuming negotiations that are necessary to take control of 100 percent of a company. Sometimes after a parent company takes control of another business, it continues buying stock over the next few years until it owns 100 percent of the stock.

Stock acquisition is the most common method for taking control of another company because it's cheaper than paying for all the company's assets. To control another company, a parent company needs to buy more than 50 percent of its stock. This type of acquisition doesn't require the difficult and more time-consuming negotiations that are necessary to take control of 100 percent of a company. Sometimes after a parent company takes control of another business, it continues buying stock over the next few years until it owns 100 percent of the stock.

Acquiring a company through stock acquisition is also easier than using the other takeover methods because the company's shares are sold on the open market. One company can take over another simply by buying up those open-market shares.

Reading Consolidated Financial Statements

Most major corporations are made up of numerous companies bought along the way to create their empires. The financial statement for such a corporation reflects the financial results for all these entities it bought, as well as the original assets of the company.

After a stock acquisition by the parent company, the subsidiary continues to maintain separate accounting records. But in reality, the parent company controls the subsidiary, so it no longer operates completely independently. By accounting rules, the parent company must present its subsidiary's and its own financial operations in a consolidated manner (even though the two companies may be separate legal entities). The parent company does so by publishing consolidated financial statements, which combine the assets, liabilities, revenue, and expenses of the parent company with those of its affiliates (that is, its subsidiaries, associates, and joint ventures).

If you hold a minority interest (see the previous section for more information on minority interest) in the subsidiary of a parent company, the consolidated financial statements don't give you the information you need to make decisions about your holdings. But in addition to having its report included in the consolidated financial statements, a subsidiary with minority shareholders must report its financial results separately from its parent company.

If you hold a minority interest (see the previous section for more information on minority interest) in the subsidiary of a parent company, the consolidated financial statements don't give you the information you need to make decisions about your holdings. But in addition to having its report included in the consolidated financial statements, a subsidiary with minority shareholders must report its financial results separately from its parent company.

When a company owns all the common stock of its subsidiaries, it doesn't need to publish reports about the subsidiaries’ individual results for the general public to peruse. Shareholders don't even need to know the results of these subsidiaries.

In preparing consolidated financial statements, the parent company must eliminate numerous transactions between itself and its affiliates before presenting the statements to the public.

For example, the parent company must eliminate such transactions for accounts receivable and accounts payable, to avoid counting revenue twice and giving the financial report reader the impression that the consolidated entity has more profits or owes more money than it actually does. Other key transactions that a parent company must eliminate when preparing consolidated financial statements include the following:

- Investments in the subsidiary: The parent company's books show its investments in a subsidiary as an asset account. The subsidiary's books show the stock that the parent company holds as shareholders’ equity. Instead of double-counting this type of transaction, the parent company eliminates it on the consolidated statements by writing off one transaction.

- Advances to the subsidiary: If a parent company advances money to a subsidiary or a subsidiary advances money to its parent company, both entities carry the opposite side of this transaction on their books (that is, one entity gains money while the other one loses it, or vice versa). Again, companies avoid the double transaction on the consolidated statements by getting rid of one transaction.

- Interest revenue and expenses: Sometimes a parent company loans money to a subsidiary, or a subsidiary loans money to a parent company; in these business transactions, one company may charge the other one interest on the loan. On the consolidated statements, any interest revenue or expenses that these loans generate must be eliminated.

- Dividend revenue and expenses: If a subsidiary declares a dividend, the parent company receives some of these dividends as revenue from the subsidiary. Anytime a parent company records revenue from its subsidiaries on its books, the parent company must eliminate any dividend expenses that the subsidiary recorded on its books.

- Management fees: Sometimes a subsidiary pays its parent company a management fee for the administrative services it provides. These fees are recorded as revenue on the parent company's books and as expenses on the subsidiary's books.

-

Sales and purchases: Parent companies frequently buy products or materials from their subsidiaries, and their subsidiaries buy products or materials from them. In fact, most companies that buy other companies do so within the same industry as a means of getting control of a product line, a customer base, or some other aspect of that company's operations.

However, the consolidated income statements can't show these sales as revenue and can't show the purchases as expenses. Otherwise, the company is double-counting the transaction. Accounting rules require that parent companies eliminate these types of transactions.

As you can see, these major transactions are all critical for determining whether a company made a profit or loss from its activities. Eliminating assets, liabilities, revenue, and expenses from public view makes determining a subsidiary's financial results nearly impossible for shareholders or creditors. But if these transactions are included, the value of the parent company's stock is distorted because the transactions are counted twice. The shareholders of the parent company can't know the true value of the company's assets and liabilities in such a case; the income statement doesn't reflect the company's true revenues and expenses.

The Securities and Exchange Commission (SEC) and Financial Accounting Standards Board (FASB) tried to address the problem that shareholders and creditors of a subsidiary face by requiring parent companies to provide segment reporting (reporting about subsidiaries, business units, and divisions of the company), which you also find in the notes to the financial statements.

Looking to the Notes

The eliminations to adjust for reporting subsidiary results mentioned in the previous section don't show up in the parent company's financial reports unless some portion of the stock acquisition takes place in the year that's being reported. When the acquisition or some financial impact of that acquisition does take place in the year that's being reported, you need to look to the notes to the financial statements to get details about any financial impacts.

In the first note to the consolidated financial statement, the company indicates that the financial statements represent the results of the parent company, not its affiliates. The company also includes some statement about the eliminated transactions. Just to give you an example of how this is worded, here's the information from GE's notes.

Here, verbatim, is how GE explains its presentation of the number in its financial statements:

- Financial data and related measurements are presented in the following categories:

- GE: This represents the adding together of all affiliates other than General Electric Capital Corporation (GECC), whose continuing operations are presented on a one-line basis, giving effect to the elimination of transactions among such affiliates.

- GECC: This represents the adding together of all affiliates of GECC, giving effect to the elimination of transactions among such affiliates.

- Consolidated: This represents the adding together of GE and GECC, giving effect to the elimination of transactions between GE and GECC.

- Operating Segments: These comprise our eight businesses, focused on the broad markets they serve: Power & Water, Oil & Gas, Energy Management, Aviation, Healthcare, Transportation, Home & Business Solutions and GE Capital.

- Prior-period information has been reclassified to be consistent with how we managed our businesses in 2012.

Note that you don't find out what subsidiaries fall under GE in this explanation. You don't find that detail in Mattel's or Hasbro's notes, either, as I discuss in Chapter 9. Few companies provide that detail. Sound like a confusing house of cards? Yep, it sure is, which is what makes reading consolidated financial statements so difficult!

Mergers and acquisitions

If a company completes a merger or acquisition in the year that's reported on the consolidated financial statement, you find a special note in the notes to the financial statements. Otherwise, if you want to find out any details about how the mergers and acquisitions may still be impacting the company financially, you have to start digging.

For example, if a company issues additional shares of stock to buy a subsidiary, the value of the stock held by shareholders before the acquisition is diluted, which means that the same earnings or assets must be divided among a greater number of pieces. To see how this works, imagine an example involving 100 shares of stock and a company profit of $100. In this scenario, each share of stock claims $1 of earnings. If, after the acquisition, 150 shares of stock are outstanding, each share of stock can claim only 67 cents of the $100 of earnings. This diluted ownership impacts the amount of dividends or the portion of ownership you have in the company for the rest of the time you own that stock.

You can see how you need to play a game of cat-and-mouse to find all the little pieces of cheese laid out in the financial statements. Companies don't make information easily accessible, and they often hide the financial impact of an acquisition or merger on the value of your shares by writing the notes to the financial statements in such a convoluted way that you have to be a detective to sort out the relevant details.

Goodwill

Another important note you can check out to find the impact of mergers and acquisitions on the consolidated financial statements is the note that explains goodwill. Goodwill is the amount of money a company pays in excess of the value of the assets when it buys another company (see Chapters 4 and 6 for more details). For example, suppose a company has $100 million in assets, and another company offers to buy it for $150 million. The extra $50 million doesn't represent tangible assets like inventory or property; it represents extra value because of customer loyalty, store locations, or other factors that add value. Goodwill is a factor only in the case of a merger or acquisition that involves acquiring 100 percent of the subsidiary or other affiliate.

Liquidations or discontinued operations

Whenever a company sells a subsidiary or other affiliate or discontinues its operations, a note to the financial statements regarding this transaction appears in the year in which the transaction first occurred. After the first year, any impact that a sale or a discontinuance of operations has on a company's operating results is usually buried in other notes. Just like with mergers and acquisitions, you have to play detective to find out any ongoing impact that these changes have had on the company.

The company includes information in the notes about any profits or losses related to the liquidation of an asset or discontinued operations. Because these transactions can impact financial statements over a number of years, the fine print includes financial impacts for the years prior to the year being reported, as well as anticipated future impacts.

When reading the consolidated financial statements and their related notes, be sure you look for any mention of the impact of previous mergers or acquisitions of affiliates and how those transactions may still be impacting the financial statements.

You may find notes related to impacts on the balance sheet, income statement, shareholders’ equity, or cash flows. Transactions involving affiliates can impact any of these statements.