Chapter 8

The Statement of Cash Flows

In This Chapter

![]() Exploring the statement of cash flows

Exploring the statement of cash flows

![]() Understanding operating activities

Understanding operating activities

![]() Getting a grip on investments

Getting a grip on investments

![]() Figuring out the financing section

Figuring out the financing section

![]() Looking at other line items

Looking at other line items

![]() Finding net cash from all company activities

Finding net cash from all company activities

Cash is a company's lifeblood. If a company expects to manage its assets and liabilities and to pay its obligations, it has to know the amount of cash flowing into and out of the business, which isn't always easy to figure out when using accrual accounting. (You can find out more about accrual accounting in Chapter 4.)

The reason accrual accounting makes it hard to figure out how much cash a company actually holds is that cash doesn't have to change hands for the company to record a transaction. The statement of cash flows is the financial statement that helps the financial report reader understand a company's cash position by adjusting for differences between cash and accruals. (See Chapter 4 for more information on cash and accruals.) This statement tracks the cash that flows into and out of a business during a specified period of time and lays out the sources of that cash. In this chapter, I explore the basic parts of the statement of cash flows.

Digging into the Statement of Cash Flows

Basically, a statement of cash flows gives the financial report reader a map of the cash receipts, cash payments, and changes in cash that a company holds, minus the expenses that arise from operating the company. In addition, the statement looks at money that flows into or out of the firm through investing and financing activities. As with the income statement (see Chapter 7), companies provide three years’ worth of information on the statement of cash flows.

When reading the statement of cash flows, you need to be looking for answers to these three questions:

When reading the statement of cash flows, you need to be looking for answers to these three questions:

- Where did the company get the cash needed for operations during the period shown on the statement — from revenue generated, funds borrowed, or stock sold?

- What cash did the company actually spend during the period shown on the statement?

- What was the change in the cash balance during each of the years shown on the statement?

Knowing the answers to these questions helps you determine whether the company is thriving and has the cash needed to continue to grow its operations or the company appears to have a cash-flow problem and may be nearing a point of fiscal disaster. In this section, I show you how to use the statement of cash flows to find the answers to these questions.

The parts

Transactions shown on the statement of cash flows are grouped in three parts:

- Operating activities: This part includes revenue the company takes in through sales of its products or services and expenses the company pays out to carry out its operations.

- Investing activities: This part includes the purchase or sale of the company's investments and can include the purchase or sale of long-term assets, such as a building or a company division. Spending on capital improvements (upgrades to assets the company holds, such as the renovation of a building) also fits into this category, as does any buying or selling of short-term invested funds.

- Financing activities: This part involves raising cash through long-term debt or by issuing new stock. It also includes using cash to pay down debt or buy back stock. Companies include any dividends paid in this section.

Operating activities is the most important section of the statement of cash flows. In reading this section, you can determine whether the company's operations are generating enough cash to keep the business viable. I discuss how to analyze this statement and make these determinations in Chapter 12.

Operating activities is the most important section of the statement of cash flows. In reading this section, you can determine whether the company's operations are generating enough cash to keep the business viable. I discuss how to analyze this statement and make these determinations in Chapter 12.

The formats

Companies can choose between two different formats when preparing their statement of cash flows. Both arrive at the same total but provide different information to get there:

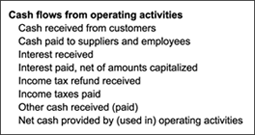

- Direct method: The Financial Accounting Standards Board (FASB; see Chapter 18) prefers the direct method, which groups major classes of cash receipts and cash payments. For example, cash collected from customers is grouped separately from cash received on interest-earning savings accounts or from dividends paid on stock the company owns. Major groups of cash payments include cash paid to buy inventory, cash disbursed to pay salaries, cash paid for taxes, and cash paid to cover interest on loans. Figure 8-1 shows you the direct method.

- Indirect method: Most companies (90 percent) use the indirect method, which focuses on the differences between net income and net cash flow from operations, and allows firms to reveal less than the direct method, leaving their competitors guessing. The indirect method is easier to prepare. Figure 8-2 shows you the indirect method.

The direct and indirect methods differ only in the operating activities section of the report. The investing activities and financing activities sections are the same.

Figure 8-1: The direct method.

Figure 8-2: The indirect method.

Using the indirect method, you just need the information from two years’ worth of balance sheets and income statements to make calculations. For example, you can calculate changes in accounts receivable, inventories, prepaid expenses, current assets, accounts payable, and current liabilities by comparing the totals shown on the balance sheet for the current year and the previous year. If a company shows $1.5 million in inventory in 2011 and $1 million in 2012, the change in inventory using the indirect method is shown easily: “Decrease in Inventory — $500,000.” The statement of cash flows for the indirect method summarizes information already given in a different way, but it doesn't reveal any new information.

With the direct method, the company has to reveal the actual cash it receives from customers, the cash it pays to suppliers and employees, and the income tax refund it receives. Someone reading the balance sheet and income statement won't find these numbers in other parts of the financial report.

In addition to having to reveal details about the actual cash received or paid to customers, suppliers, employees, and the government, companies that use the direct method must prepare a schedule similar to one used in the indirect method for operating activities to meet FASB requirements. Essentially, companies save no time, must reveal more detail, and must still present the indirect method. Why bother? You can see why you'll most likely see the indirect method used in the vast majority of financial reports you read.

The investing activities and financing activities sections for both the direct and indirect methods look something like Figure 8-3 and Figure 8-4, both of which show the basic line items. Read on to find out what each of these line items includes. If you're interested in finding out about line items that make their way onto the statement only in special circumstances, see “Recognizing the Special Line Items,” later in the chapter.

Figure 8-3: The investing activities section.

Figure 8-4: The financing activities section.

Checking Out Operating Activities

The operating activities section is where you find a summary of how much cash flowed into and out of the company during the day-to-day operations of the business.

Operating activities is the most important section of the statement of cash flows. If a company isn't generating enough cash from its operations, it isn't going to be in business long. Although new companies often don't generate a lot of cash in their early years, they can't survive that way for long before going bust.

The primary purpose of the operating activities section is to adjust the net income by adding or subtracting entries that were made in order to abide by the rules of accrual accounting that don't actually require the use of cash. In this section, I describe several of the accounts in the operating activities section of the statement and explain how they're impacted by the changes required to revert accrual accounting entries to actual cash flow.

Depreciation

A company that buys a lot of new equipment or builds new facilities has high depreciation expenses that lower its net income. This fact is particularly true for many high-tech businesses that must always upgrade their equipment and facilities to keep up with their competitors.

The bottom line may not look good, but all those depreciation expenses don't represent the use of cash. In reality, no cash changes hands to pay depreciation expenses. These expenses are actually added back into the equation when you look at whether the company is generating enough cash from its operations because the company didn't actually lay out cash to pay for these expenses.

For example, if the company's net income is $200,000 for the year and its depreciation expenses are $50,000, the $50,000 is added back in to find the net cash from operations, which totals $250,000. Essentially, the firm is in better shape than it looked to be before the depreciation expenses because of this noncash transaction.

Inventory

Another adjustment on the statement of cash flows that usually adds cash to the mix is a decrease in inventory. If a company's inventory on hand is less in the current year than in the previous year, the company bought some of the inventory sold with cash in the previous year.

On the other hand, if the company's inventory increases from the previous year, then it spent more money on inventory in the current year, and it subtracts the difference from the net income to find its current cash holdings. For example, if inventory decreases by $10,000, the company adds that amount to net income on the statement of cash flows.

Accounts receivable

Accounts receivable is the summary of accounts of customers who buy their goods or services on direct credit from the company. Customers who buy their goods by using credit cards from banks or other financial institutions aren't included in accounts receivable. Payments by outside credit sources are instead counted as cash because the company receives cash from the bank or financial institution. The bank or financial institution collects from those customers, so the company that sells the good or service doesn't have to worry about collecting the cash.

When accounts receivable increase during the year, the company sells more products or services on credit than it collects in actual cash from customers. In this case, an increase in accounts receivable means a decrease in cash available.

The opposite is true if accounts receivable are lower during the current year than the previous year. In this case, the company collects more cash than it adds credit to customers’ credit accounts. In this situation, a decrease in accounts receivable results in more cash received, which adds to the net income.

Accounts payable

Accounts payable is the summary of accounts of bills due that haven't yet been paid, which means the company must still lay out cash in a future accounting period to pay those bills.

When accounts payable increase, a company uses less cash to pay bills in the current year than it did in the previous one, so more cash is on hand. This has a positive effect on the cash situation. Expenses incurred are shown on the income statement, which means net income is lower. But in reality, the company hasn't yet laid out the cash to pay those expenses, so an increase is added to net income to find out how much cash is actually on hand.

Conversely, if accounts payable decrease, the company pays out more cash for this liability. A decrease in accounts payable means the company has less cash on hand, and it subtracts this number from net income.

The cash flow from activities section, summed up

To give you a taste of what all these line items look like in the statement of cash flows, see Table 8-1, where I roll together the information from the previous sections.

Table 8-1 Cash Flows from Operating Activities

|

Line Item |

Cash Received or Spent |

|

Net income |

$200,000 |

|

Depreciation |

50,000 |

|

Increase in accounts receivable |

(20,000) |

|

Decrease in inventories |

10,000 |

|

Decrease in accounts payable |

(10,000) |

|

Net cash provided by (used in) operating activities |

$230,000 |

In Table 8-1, the company has $30,000 more in cash from operations than it reported on the income statement, so the company actually generated more cash than you may have thought if you just looked at net income.

If you compare the statements for the toy companies Mattel and Hasbro in 2012 (you can download them at www.mattel.com and www.hasbro.com), you can see that Mattel's net cash flow totaled $1,276 million after adjustments on $777 million net income, whereas Hasbro's net cash was $535 million on $336 million of net income. For Hasbro, depreciation and amortization adjustments added $100 million to the company's net cash position. Mattel added $157 million to its net cash with depreciation and amortization. Mattel increased accounts payable, accrued liabilities, and income taxes by $312 million to hold on to cash. Hasbro decreased its cash with a $22 million decrease in accrued liabilities and accounts payable. It also used $59 million in cash to pay for production costs.

If you compare the statements for the toy companies Mattel and Hasbro in 2012 (you can download them at www.mattel.com and www.hasbro.com), you can see that Mattel's net cash flow totaled $1,276 million after adjustments on $777 million net income, whereas Hasbro's net cash was $535 million on $336 million of net income. For Hasbro, depreciation and amortization adjustments added $100 million to the company's net cash position. Mattel added $157 million to its net cash with depreciation and amortization. Mattel increased accounts payable, accrued liabilities, and income taxes by $312 million to hold on to cash. Hasbro decreased its cash with a $22 million decrease in accrued liabilities and accounts payable. It also used $59 million in cash to pay for production costs.

Investigating Investing Activities

The investment activities section of the statement of cash flows, which looks at the purchase or sale of major new assets, is usually a drainer of cash. Consider what this section typically lists:

- Purchases of new buildings, land, and major equipment

- Mergers or acquisitions

- Major improvements to existing buildings

- Major upgrades to existing factories and equipment

- Purchases of new marketable securities, such as bonds or stock

The sale of buildings, land, major equipment, and marketable securities also appears in the investment activities section. When any of these major assets are sold, they're shown as cash generators rather than as cash drainers.

The primary reason to check out the investments section is to see how the company is managing its capital expenditures (money spent to buy or upgrade assets) and how much cash it's using for these expenditures. If the company shows large investments in this area, be sure to look for explanations in the management's discussion and analysis and the notes to the financial statements (see Chapter 9) to get more details about the reasons for the expenditures.

If you believe that the firm is making the right choices to grow the business and improve profits, investing in its stock may be worthwhile. If the company is making most of its capital expenditures to keep old factories operating as long as possible, that may be a sign that it isn't keeping up with new technology.

Compare companies in the same industry to see what type of expenditures each lists in investment activities and the explanations for those expenditures in the notes to the financial statements. Comparing a company with one of its peers helps you determine whether the company is budgeting its capital expenditures wisely.

In comparing the statements of Hasbro and Mattel, you can see that Mattel spent more on purchases of tools, dies, molds, property, plant, and equipment. Mattel's spending totaled more than $219 million, whereas Hasbro spent about $112 million.

Understanding Financing Activities

Companies can't always raise all the cash they need from their day-to-day operations. Financing activities are another means of generating cash. Any cash raised through activities that don't include day-to-day operations appears in the financing section of the statement of cash flows.

Issuing stock

When a company first sells its shares of stock, it shows the money it raises in the financing section of the statement of cash flows. The first time a company sells shares of stock to the general public, this sale is called an initial public offering (IPO; see Chapter 3 for more information). Whenever a company decides to sell additional shares to raise capital, all additional sales of stock are called secondary public offerings.

Usually, when companies decide to do a secondary public offering, they do so to raise cash for a specific project or group of projects that they can't fund by ongoing operations. The financial department must determine whether it wants to raise funds for these new projects by borrowing money (new debt) or by issuing stock (new equity). If the company already has a great deal of debt and finds that borrowing more is difficult, it may try to sell additional shares to cover the shortfall. I talk more about debt versus equity in Chapter 12.

Buying back stock

Sometimes you see a line item in the financing section indicating that a company has bought back its stock. Most often, companies that announce a stock buyback are trying to accomplish one of two goals:

- Increase the market price of their stock. (If companies buy back their stock, fewer shares remain on the market, thus raising the value of shares still available for purchase.)

- Meet internal obligations regarding employee stock options, which guarantee employees the opportunity to buy shares of stock at a price that's usually below the price outsiders must pay for the stock.

Sometimes a company buys back stock with the intention of going private (see Chapter 3). In this case, company executives and the board of directors decide that they no longer want to operate under the watchful eyes of investors and the government. Instead, they prefer to operate under a veil of privacy and not to have to worry about satisfying so many company outsiders. I discuss the advantages and disadvantages of staying private in Chapter 3.

For many firms, an announcement that they're buying back stock is an indication that they're doing well financially and that the executives believe in their company's growth prospects for the future. Because buybacks reduce the number of outstanding shares, a company can make its per-share numbers look better even though a fundamental change hasn't occurred in the business's operations.

If you see a big jump in earnings per share, look for an indication of stock buyback in the financing activities section of the statement of cash flows.

Paying dividends

Whenever a company pays dividends, it shows the amount paid to shareholders in the financing activities section. Companies aren't required to pay dividends each year, but they rarely stop paying dividends after the shareholders have gotten used to their dividend checks.

If a company retrenches on its decision to pay dividends, the market price of the stock is sure to tumble. The company's decision not to pay dividends after paying them in the previous quarter or previous year usually indicates that it's having problems, and it raises a huge red flag on Wall Street.

If a company retrenches on its decision to pay dividends, the market price of the stock is sure to tumble. The company's decision not to pay dividends after paying them in the previous quarter or previous year usually indicates that it's having problems, and it raises a huge red flag on Wall Street.

Incurring new debt

When a company borrows money for the long term, this new debt also appears in the financing activities section. This type of new debt includes the issuance of bonds, notes, or other forms of long-term financing, such as a mortgage on a building.

When you read the statement of cash flows and see that the company has taken on new debt, be sure to look for explanations in the management's discussion and analysis and the notes to the financial statements about how the company is using this debt (see Chapter 9).

Paying off debt

Debt payoff is usually a good sign, often indicating that the company is doing well. However, it may also be an indication that the company is simply rolling over existing debt into another type of debt instrument.

If you see that the company paid off one debt and took on another debt that costs about the same amount of money, it likely indicates that the firm simply refinanced the original debt. Ideally, that refinancing involves lowering the company's interest expenses. Look for a full explanation of the debt payoff in the notes to the financial statements.

If you compare the financing activities of Mattel and Hasbro, you see that Mattel paid off long-term debt, bought back stock, and paid dividends to deplete its cash holdings. Hasbro also paid dividends and purchased common stock, but it raised cash by taking on short-term borrowings and collecting cash from stock option transactions. Mattel used $410 million of its cash for its financing activities, while Hasbro used $219 million.

When you look at the financing activities on a statement of cash flows for younger companies, you usually see financing activities that raise capital. Their statements include funds borrowed or stock issued to raise cash. Older, more established companies begin paying off their debt and buying back stock when they've generated enough cash from operations.

Recognizing the Special Line Items

Sometimes you see line items on the statement of cash flows that appear unique to a specific company. Businesses use these line items in special circumstances, such as the discontinuation of operations. Companies that have international operations use a line item that relates to exchanging cash among different countries, which is called foreign exchange.

Discontinued operations

If a company discontinues operations (stops the activities of a part of its business), you usually see a special line item on the statement of cash flows that shows whether the discontinued operations have increased or decreased the amount of cash the company takes in or distributes. Sometimes discontinued operations increase cash because the firm no longer has to pay the salaries and other costs related to that operation.

Other times, discontinued operations can be a one-time hit to profits because the company has to make significant severance payments to laid-off employees and has to continue paying manufacturing and other fixed costs related to those operations. For example, if a company leases space for the discontinued operations, it's contractually obligated to continue paying for that space until the contract is up or the company finds someone to sublease the space.

Foreign currency exchange

Whenever a company has global operations, it's certain to have some costs related to moving currency from one country to another. The U.S. dollar, as well as currencies from other countries, experiences changes in currency exchange rates — sometimes 100 times a day or more.

Each time the dollar exchange rate between two countries changes, moving currency between those countries can result in a loss or a gain. Any losses or gains related to foreign currency exchanges appear on a special line item on the statement of cash flows called Effect of currency exchange rate changes on cash. Both Mattel and Hasbro show the effects of currency exchange on their statements in 2007 — Hasbro's net cash decreased by $1 million, and Mattel's increased by $2 million.

Adding It All Up

This is the big one, the highlight, the bottom line: Cash and short-term investments at end of year. This number shows you how much cash or cash equivalents a company has on hand for continuing operations the next year.

Cash equivalents are any holdings that the company can easily change to cash, such as cash, cash in checking and savings accounts, certificates of deposit that are redeemable in less than 90 days, money-market funds, and stocks sold on the major exchanges that can be easily converted to cash.

The top line of the statement starts with net income. Adjustments are made to show the impact on cash from operations, investing activities, and financing. These adjustments convert that net income figure to actual cash available for continuing operations. Remember that this is the cash on hand that the company can use to continue its activities the next year.

If you look at the statement of cash flows for Mattel and Hasbro, you can see that Mattel had about $1,336 million on hand at the end of December 2012 on net earnings of $777 million. Hasbro had about $850 million in cash and cash equivalents at the end of December 2012 on net earnings of $336 million. Mattel's cash on hand was down slightly from 2011, while Hasbro increased its cash holdings.

In Part III, I delve more deeply into how the cash results of these two companies differ. I also show you how you can use the figures on the statement of cash flows and other statements in the financial reports to analyze the results and make judgments about a company's financial position.