Chapter 11

Testing the Profits and Market Value

In This Chapter

![]() Getting a handle on the price/earnings ratio

Getting a handle on the price/earnings ratio

![]() Diving into the dividend payout ratio

Diving into the dividend payout ratio

![]() Examining return on sales

Examining return on sales

![]() Reviewing return on assets

Reviewing return on assets

![]() Understanding return on equity

Understanding return on equity

![]() Working with margins

Working with margins

Well, did the company make any money? Everyone, and I mean everyone with a financial stake in the company — executives, investors, debtors, employees — wants the answer to that question. Investors especially want to know whether the company's stock is worth the price they have to pay.

You may think the answer is a simple yes or no, but the answer always depends on many factors. How well did the business make use of its resources in order to make a profit? Was that profit high enough based on the resources the firm had on hand and compared with that of similar companies? Did the company pay out a fair share of its earnings to its investors? Did it reinvest the right amount of money in its coffers for future growth?

In this chapter, I show you how to answer these key questions with calculations that help you test a company's profitability and market value: price/earnings ratio (P/E), dividend payout ratio, return on sales (ROS), return on assets (ROA), and return on equity (ROE). I also review how to calculate the profit margins — both the operating margin and the net margin.

To help you understand the validity of these profitability tests, I compare the results of the two leading toy companies, Mattel and Hasbro, and I compare their results with those of the toy industry in general. If you want to follow along, you need the financial statements of Mattel (http://investor.shareholder.com/mattel/financials.cfm) and Hasbro (http://investor.hasbro.com/annuals.cfm). You can download those at each of the company's websites, or you can order an annual report by calling the company's investor relations office.

The Price/Earnings Ratio

The profit number you hear discussed most often in the financial news is the price/earnings ratio, or the P/E ratio. Basically, the P/E ratio looks at the price of the stock versus its earnings. For example, a P/E ratio of 10 means that, for every $1 in company earnings per share, people are willing to pay $10 per share to buy the stock. If the P/E is 20, then people are willing to pay $20 per share for each $1 of company earnings.

Why are people willing to pay more per dollar of earnings on some stock? Because the people who buy the more expensive stock believe the stock has greater potential for growth. This ratio is used when valuing stocks and is one of the oldest measurements in the world of stock exchanges.

On its own, the P/E ratio means little, but as part of an overall evaluation of a company, the P/E ratio helps you interpret earnings results. Never make a decision on whether to buy or sell a stock based solely on the P/E ratio. Nonetheless, a negative P/E or a P/E of zero is a major trouble sign, indicating that a company isn't profitable.

On its own, the P/E ratio means little, but as part of an overall evaluation of a company, the P/E ratio helps you interpret earnings results. Never make a decision on whether to buy or sell a stock based solely on the P/E ratio. Nonetheless, a negative P/E or a P/E of zero is a major trouble sign, indicating that a company isn't profitable.

Figuring out earnings per share

Earnings per share represents the amount of income a company earns per share of stock on the stock market. The firm calculates the earnings per share (EPS) by dividing the total earnings by the number of shares outstanding. Companies often use a weighted average of the number of shares outstanding during the reporting period because the number of shares outstanding can change as the company sells new shares to outside investors or company employees. In addition, companies sometimes buy back shares from existing shareholders, reducing the number of shares available to the general public.

A weighted average is calculated by totaling the number of shares available during a certain period of time and dividing that number by the number of periods included. For example, if the weighted average is based on a monthly average, the number of shares outstanding on the stock market at the end of each month is totaled and divided by 12 to find the weighted average. This calculation can also be done with a weekly or daily figure. If weekly stock totals are used, the total of these periods is divided by 52. If daily numbers are used, the total is divided by 365.

Calculating the P/E ratio

To get the P/E ratio, divide the market value per share of stock by earnings per share of stock:

- Market value per share of stock ÷ Earnings per share of stock = P/E ratio

Many websites help you find the market value per share of stock. Yahoo! Finance (finance.yahoo.com) is one of my favorites for easily finding historical stock data.

Many websites help you find the market value per share of stock. Yahoo! Finance (finance.yahoo.com) is one of my favorites for easily finding historical stock data.

The P/E formula comes in three flavors, which vary according to how earnings per share is calculated: trailing, current, and forward earnings.

- Trailing P/E: You calculate a trailing P/E by using earnings per share from the last four quarters, or 12 months of earnings. This number gives you a view of a company's earnings ratios based on accurate historical data.

-

Leading or projected P/Es: The other two types of P/E ratios are calculated using analysts’ expectations, so they're sometimes called leading or projected P/Es.

- The current P/E ratio is calculated using earnings that analysts expect during the current year.

- A forward P/E ratio is based on analysts’ projections for the next year.

Any P/E ratio that uses future projected results is only as good as the analyst making those projections. So be careful when you see the terms leading, projected, current, or forward P/E.

Any type of P/E ratio is just one of many profitability ratios to consider. This ratio gives you a good idea of what the public is willing to pay per share of stock based on the company's historical earnings (trailing P/E) or what the analysts project you can consider paying per share of stock based on future earnings (current P/E or forward P/E). It gives you no guarantee of what the company will earn or what the stock price will be in the future.

Any type of P/E ratio is just one of many profitability ratios to consider. This ratio gives you a good idea of what the public is willing to pay per share of stock based on the company's historical earnings (trailing P/E) or what the analysts project you can consider paying per share of stock based on future earnings (current P/E or forward P/E). It gives you no guarantee of what the company will earn or what the stock price will be in the future.

Practicing the P/E ratio calculation

Now that you understand the basics behind the P/E ratio, I show you how to calculate it using real-world numbers from Hasbro and Mattel. As I mention earlier in this chapter, the company calculates earnings per share, which represents the total earnings divided by the number of shares outstanding. Remember that the number of shares outstanding can change as the company sells new shares to investors or buys them back from existing shareholders.

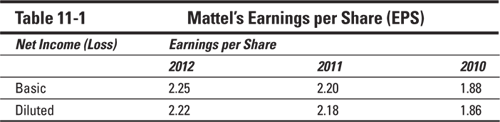

When a company reports its earnings per share, it usually shows two numbers: basic and diluted. The firm calculates the basic EPS using a weighted average of all shares currently on the market. The diluted EPS takes into consideration all future obligations to sell stock. For example, this number takes into account employees who have stock options to buy stock in the future, or bondholders who hold bonds that are convertible to stock.

To practice using the formula to calculate P/E ratios, I use numbers from Mattel's and Hasbro's income statements. Table 11-1 shows Mattel's basic and diluted EPS for 2012, 2011, and 2010. Table 11-2 shows the same information for Hasbro.

To practice using the formula to calculate P/E ratios, I use numbers from Mattel's and Hasbro's income statements. Table 11-1 shows Mattel's basic and diluted EPS for 2012, 2011, and 2010. Table 11-2 shows the same information for Hasbro.

In the following examples, to calculate how the public valued the results for Mattel and Hasbro at the end of June 2013 using the 2012 annual report, I use the stock price at the time the market closed on June 20, 2013. I also use the diluted earnings per share, which more accurately represents the company's outstanding shareholder obligations.

Mattel closed at $44.02, and Hasbro closed at $43.81. Even though Mattel's diluted earnings per share were 36 cents per share lower than Hasbro, Hasbro's stock sold for slightly less than Mattel, by 21 cents per share.

Here's Mattel's P/E ratio:

- $44.02 (Market value) ÷ $2.22 (2012 Diluted EPS) = 19.90 (P/E ratio)

Note that the P/E ratio is shown without a dollar sign. P/E is not a dollar value, but instead shows the number of times the price outweighs the earnings of the company.

So Mattel investors were willing to pay $19.90 for every $1 of earnings by Mattel in 2013. Following is Hasbro's P/E ratio:

- $43.81 (Market value) ÷ $ 2.55 (2007 Diluted EPS) = 17.18 (P/E ratio)

Hasbro investors were willing to pay $17.18 for every $1 of earnings by Hasbro in 2013.

These numbers show a dramatic improvement for Mattel over its results five years ago, after the scandal involving toy recalls from China in 2007. At that time, Mattel's P/E ratio was just $13.08, whereas Hasbro's was $18.40. In 2013, the tables turned: Investors were willing to pay more per dollar of earnings for Mattel stock.

Using the P/E ratio to judge company market value (stock price)

In comparing Mattel's and Hasbro's P/E ratios, you can conclude that, on June 20, 2013, investors believed that Mattel had better chances of improving its earnings performance than Hasbro and, therefore, were willing to pay a higher price for each share of Mattel's stock. You must dig deeper into the numbers, the quarterly reports for the first half of 2013, and general financial press coverage to determine why investors were more bullish on Mattel than Hasbro. But this one quick calculation lets you know which stock investors favor.

How do you know what a reasonable P/E ratio is for a company? Historically, the average P/E ratio for stock falls between 15 and 25. This ratio depends on economic conditions and the industry the company's in. Some industries, such as technology, regularly maintain higher P/E ratios in the range of 30 to 40.

In addition to comparing two companies, you need to compare the P/E calculation to the industry of the companies. Doing so allows you to gauge stock price or market value not only for the companies whose annual reports you're analyzing, but also for other companies in the same business.

One way you can find out the average industry P/E is to look up a company on Yahoo! Finance (finance.yahoo.com). On its home page, you see a link for industry information. Toy companies fall into the Toys & Games industry category. In June 2013, Mattel and Hasbro beat out all other industry players by a significant margin. The next-closest toy and games company was Gaming Partners International Corporation, with a P/E of 12.15.

The P/E is a good quick ratio for picking potential investment candidates, but you don't want to use this ratio alone to make a buying or selling decision. After you pick your targets, read and analyze the annual reports and other information about the company before making a decision to invest.

If you want to start your research on potential investment opportunities based on leaders or laggards in an industry, you can find a summary for all industry statistics at http://biz.yahoo.com/ic/index.html. You may wonder why someone would even consider laggards as investment opportunities. Well, you can sometimes find a company that many investors think is a dog but is actually terribly undervalued and doing the right things to recover from its current slump. This style of investing is called value investing.

When investors are bullish, they tend to bid up the price of stock and end up paying higher prices for the stock than it may actually be worth. This price-bidding war also drives up the P/E ratio.

The market sets stock prices based solely on the price at which someone is willing to sell a stock and the price at which someone is willing to buy a stock.

During the Internet and technology stock bubble of the late 1990s and early 2000s, P/E ratios hit highs in the hundreds and tumbled dramatically after the bubble burst. Even big names, such as Microsoft, had P/E ratios over 100 that dropped back to realistic levels when the bubble burst. In July 2004, Microsoft's P/E was 41.37, so you can see that investors can seriously overbid even a top company. By June 2008, Microsoft's P/E had dropped dramatically to 16.14. In 2013, Microsoft still carried a much lower P/E than in 2004. In June 2013, the P/E was 17.11. Its new operating system, Windows 8 didn't do as well as expected, and the losses in the European courts hurt the company's future earnings potential. Investors are no longer willing to overpay for its stock.

Be careful when you see P/Es creeping above their historical averages. Usually you're encountering a sign that a correction is looming on the horizon and will bring stock prices down to realistic levels. Do your homework while you wait for the correction, and be ready to jump in after the correction and pick up the stocks you want on sale.

Understanding variation among ratios

You'll probably find varying P/E ratios for the same company because the number used for EPS can vary depending on which method the company chooses for calculating EPS. The diluted EPS is the one you generally want to use. This figure is based on the current number of shares on the market, as well as shares promised to employees for purchase in the future and shares promised to creditors who may decide to convert a debt into a stockholding (if that's part of the debt agreement). So diluted earnings gives you the most accurate picture of the actual earnings per share of stock now available on the market or committed for sale in the future.

But when companies put out a press release, they tend to use whatever EPS looks most favorable for them. Companies can choose among four basic ways to calculate EPS:

- Reported EPS: Companies calculate this EPS number by using general accounting principles and report it on the financial statements. They show it in two formats: basic and diluted. Most times, the diluted EPS number is the best one to use, but it's sometimes distorted by one-time events, such as the sale of a division or a one-time charge for discontinued operations. Be sure to read the notes to the financial statements to determine whether you need to adjust the EPS figure for unusual events. Chapter 9 discusses the notes to the financial statements in great detail.

-

Pro forma EPS: You almost always find this EPS in a company's press release because it makes the company look the best. In most cases, this figure excludes some of the expenses or income the firm uses in the official financial reports. The company adjusts these official numbers to take out income that won't recur, such as a one-time gain on the sale of marketable securities, or expenses that won't recur, such as the closing of a large division.

When a company mentions pro forma EPS or statements in its press release, be sure that you compare these numbers with what the company develops using generally accepted accounting principles (GAAP) and reports in the financial statements filed with the Securities and Exchange Commission (SEC).

- Headline EPS: This EPS is the one you hear about on TV and read about in the newspapers. The earnings per share numbers used may be basic EPS, diluted EPS, pro forma EPS, or some other EPS that's calculated based on analysts’ projections, so you have absolutely no idea what's behind the numbers or the P/E ratio calculated using it. It's likely the most unreliable EPS, and you don't want to use it for your evaluation.

- Cash EPS: Companies calculate this EPS by using operating cash flow (cash generated by business operations to produce and sell its products). Operating cash can't be manipulated by accounting rules as easily as net income, so some analysts believe this EPS is the purest. When you see this number, be sure that it's based on operating cash and isn't just a fancy way of saying EBITDA (earnings before interest, taxes, depreciation, and amortization). You can judge this by calculating the cash EPS using the EBITDA reported on the financial statements and the net cash from operations reported on the statement of cash flows. Only the net cash figure gives you a true picture of cash flow.

The P/E ratio is an ever-changing number based on the day's market price. It's also a number that's hard to depend on unless you know the calculations behind it. Companies can calculate the earnings per share in many different ways — using basic EPS, diluted EPS, pro forma EPS, cash EPS, headline EPS, and projected or leading EPS. Reading the financial reports and checking the calculation for yourself is the only way you can truly determine a company's P/E and what's included in its calculation.

The Dividend Payout Ratio

The dividend payout ratio looks at the amount of a firm's earnings that it pays out to investors. Using this ratio, you can determine the actual cash return you'll get by buying and holding a share of stock.

Some companies pay a portion of their earnings directly to their shareholders using dividends. Growth companies, which reinvest all their profits, rarely pay out dividends, but older, mature companies usually do. Older companies that no longer need to reinvest large sums in growing their businesses pay out the highest dividends.

To determine how well investors did with their stock holding, you can calculate the dividend payout ratio.

Determining dividend payout

To find the dividend payout ratio, divide yearly dividend per share (the total amount per share paid out to investors during the year in dividends) by earnings per share:

- Yearly dividend per share ÷ Earnings per share = Dividend payout ratio

You can use numbers from Mattel's 2012 income statement to practice calculating the dividend payout ratio:

- $1.24 (Dividends per share) ÷ $2.22 (Diluted EPS) = 55.86% (Dividend payout ratio)

Mattel paid out 55.86 percent of its diluted earnings per share to investors in 2012. If you subtract this percentage from 100 percent, you can find how much the company plowed back into its operations toward future growth. In Mattel's case, it reinvested 44.1 percent of its earnings in the growth of the company. You can find the earnings reinvested in the company over the years in the retained earnings line in the shareholders’ equity section of the balance sheet. (See Chapter 6 for a more detailed discussion of shareholders’ equity.) Each year, any additional retained earnings are added to this line item. Mattel's retained earnings were more than $3,5 billion during its lifespan, according to the 2012 balance sheet.

Following are numbers from Hasbro's 2007 income statement. You can use them to calculate the dividend payout ratio.

- $1.44 (Dividends per share) ÷ $2.55 (Diluted EPS) = 56.5% (Dividend payout ratio)

Hasbro paid out 56.5 percent of its diluted earnings per share to investors and plowed 43.5 percent (subtract 56.5 from 100) back into the company to use for future growth. Hasbro's retained earnings on its 2012 balance sheet were more than $3.3 billion.

Digging into companies’ profits with dividends

Should the dividend payout ratio make a difference to you? In the past, investors expected dividend payouts. In fact, dividends made up as much as 40 percent of most investors’ portfolio returns about 20 years ago. But investors’ priorities have changed in the past 20 years. Today investors look toward capital gains, which are the profits investors make when selling a share of stock for more than they paid for that stock, for portfolio growth.

The big question is what better serves the investor and the company: immediate cash payouts of dividends or long-term growth resulting from reinvesting profits each year? The answer to this question isn't an easy one. Younger companies rarely pay dividends because they need the money for growth, but as companies mature, the correct answer is more difficult to determine. For example, Microsoft held billions in cash and refused to pay dividends for years, claiming that it may need the cash for growth. Not until investors screamed long and loud did Microsoft finally pay its first dividend in 2003: only 8¢ per share, or a total of about $857 million! In 2012, Microsoft paid 92 cents per share in dividends. Microsoft held $73.79 billion in cash and short-term investments at the end of June 2012.

Definitely check how the dividend payout ratio compares with that of similar companies. If the dividend payout ratio is considerably smaller than that of other similar companies, be sure you understand what the company does with the money and whether it's making good use of the funds it's reinvesting. If the company pays out a significantly larger portion of earnings to investors than most other companies in the industry, it may not have any good ideas for growth and is therefore just milking the cash cow, which may eventually run dry.

High dividend payout ratios may be a sign that a decrease in profits is on the way. If a company continually increases its dividend payout ratio even as profits fall, you've encountered a warning sign that future trouble is brewing.

If the dividend payout ratio looks extremely high or extremely low, look at the financial statements before you get too concerned. Did some extraordinary event, such as a significant loss from a plant closing or the sale or purchase of a subsidiary, dramatically impact net income? A one-time event that impacts net income can explain an unusually high or low dividend payout ratio and needn't raise a red flag for investors.

Return on Sales

You can test how efficiently a company runs its operations (that is, the making and selling of its products) by calculating its return on sales (ROS). This ratio measures how much profit the company is producing per dollar of sales. By analyzing the numbers in the income statement using ROS, you can get a picture of the company's profit per dollar of sales and gauge how much extra cash the company is bringing in per sale.

Remember that the firm needs that cash to cover its expenses, develop new products, and keep itself competitive. Investors also hope that, at some point in the future, they may even be paid some dividends. At the very least, investors want to be sure the company is generating enough cash from sales to keep itself competitive in the market through advertising, new product development, and new market development.

Figuring out ROS

To calculate ROS, divide the net income before taxes by sales. You can find both numbers on the income statement. Net sales (sometimes called net revenue) is the top number on the income statement. Net income before taxes is in the expense section of the income statement, just before tax expenses are reported.

- Net income before taxes ÷ Sales = Return on sales

You can calculate Mattel's ROS based on information in its income statement for 2012:

- $776,464,000 (Net income before taxes) ÷ $6,420,881,000 (Sales) = 12.1% (ROS)

Mattel made 12.1 percent on each dollar of sales. Compare that number with Hasbro's ROS using numbers on its income statement for 2012:

- $335,999,000 (Net income before taxes) ÷ $4,088,983 (Sales) = 8.2% (ROS)

Hasbro made 8.2 percent on each dollar of sales.

Investors can use the ROS ratio to determine how much profit a company is making on a dollar of sales. In comparing Mattel and Hasbro, you can see why Mattel's P/E is higher: Mattel is getting considerably better return on sales than Hasbro.

Reaching the truth about profits with ROS

In reading analysts’ reports on Mattel and Hasbro, I found that Hasbro's historical ROS has been about 7 percent, so the results for Hasbro in the preceding section show minimal improvement. Mattel is stagnating with its efforts to improve operating income. Its ROS in 2001 was 12.5 percent, and it dropped to 11.8 percent in 2007, but that percentage was headed in the right direction in 2012, at 12.1 percent. Mattel wants to get back to its previous historical average of about 15 to 16 percent.

ROS is just one part of the puzzle. You need to fully analyze the information you see in the annual reports to find all the pieces and make a determination about whether to invest in a company. This chapter focuses on profitability. You also need to analyze a company's liquidity, which I discuss in Chapter 12, and its cash flow, which I discuss in Chapter 13.

Return on Assets

You can judge how well a company uses its assets by calculating the return on assets (ROA). If the ROA is a high percentage, the company is likely managing its assets well. As an investor, that consideration is important because your shares of stock represent a claim on those assets. You want to be sure that the company is using your claim wisely. If you haven't invested yet, be sure your investment will go toward stock in a company that invests its assets well. As with all ratios, you need to compare results with those of similar companies in an industry for the numbers to mean anything.

To calculate ROA, divide net income by total assets. You can find net income at the bottom of the income statement, and you can find total assets at the bottom of the assets section of the balance sheet.

- Net income ÷ Total assets = Return on assets

Doing some dividing to get ROA

Using the numbers from Mattel's income statement and balance sheet, you can determine its ROA:

- $776,464,000 (Net income) ÷ $6,526,785(Total assets) = 11.9% (ROA)

So Mattel made 11.9 percent on each dollar of assets. Compare this number with Hasbro's ROA:

- $335,999,000 (Net income) ÷ $4,325,387 (Total assets) = 7.8% (ROA)

Hasbro made 7.8 percent on each dollar of assets. Mattel earned about 4 percent more than Hasbro on each dollar of assets.

Ranking companies with the help of ROA

The ROA ratio shows you how much a company earns from its assets or capital invested. This ratio gives investors and debtors a clear view of how well a company's management uses its assets to generate a profit. Both shareholders’ equity (claims on assets by shareholders) and debt funding (claims on assets by creditors) factor into this calculation, meaning that the ratio looks at the income generated using money raised by borrowing funds from creditors and selling stock to shareholders.

ROA can vary significantly, depending on the type of industry. Companies that must use their capital to maintain manufacturing operations with factories and expensive machinery have a much lower ROA than companies that don't require heavy manufacturing, like service companies. Businesses with low asset requirements average an ROA of 20 percent or higher, whereas companies that require a large investment in assets can have ROAs below 5 percent.

Return on Equity

Return on equity (ROE) measures how well a company does earning money for its investors. In fact, you'll probably find it easier to determine an ROE for a company than an ROA. Although the ROE is an excellent measure of how profitable the company is in comparison with other companies in the industry, you want to examine the ROA as well because that ratio looks at returns for both investors and creditors.

Calculating ROE

You calculate ROE by dividing net income the company earned (which you find at the bottom of the income statement) by the total shareholders’ equity (which you find at the bottom of the equity section of the balance sheet):

- Net income ÷ Shareholders’ equity = Return on equity

You can figure out Mattel's ROE based on its 2012 income statements and balance sheets:

- $776,464,000 (Net income) ÷ $3,067,044 (Shareholders’ equity) = 25.3% (ROE)

Mattel made 26 percent on each dollar of shareholders’ equity. Following is Hasbro's ROE, also based on 2012 income statements and balance sheets:

- $335,999,000 (Net income) ÷ $1,507,379 (Shareholders’ equity) = 22.3% (ROE)

Hasbro made 22.3 percent on each dollar of assets. Comparing Mattel and Hasbro, you can see that Mattel generated more than Hasbro on its shareholders’ equity. It's another reason investors pay more for Mattel stock.

Reacting to companies with ROEs assistance

Investors most often cite the ROE ratio when they want to see how well a company is doing for them. Looking at that ratio can be a huge mistake because ROE ignores the impact of debt on profitability and thus doesn't give investors the full picture of a company's financial position. ROE doesn't consider the impact of a company's debt position on its future earnings potential.

Comparing ROE to ROA for Mattel and Hasbro, you can see that both companies’ ROEs look better than their ROAs:

|

|

ROA |

ROE |

|

Mattel |

11.9% |

25.3% |

|

Hasbro |

7.8% |

22.3% |

The primary reason ROE often looks better than ROA is that ROE doesn't include debt.

When you see comparisons of company statistics, you frequently find an ROE but see no mention of an ROA. Many companies believe that ROA is primarily a statistic to be used by management and the company's debtors. Take the extra time to determine the company's ROA and compare it with the ROA of other firms in the industry. You get a much better idea of how well the company generates its profit when you take both debt and equity into consideration.

The Big Three: Margins

You need to investigate three types of margins when you evaluate a company based on its financial reports. Margins show you how much financial safety the company has after its costs and expenses. Each of the three margins I discuss — gross margin, operating margin, and net profit margin — shows what the company has left to work with at various stages of the profit calculation.

Dissecting gross margin

Gross margin looks at the profit margin based solely on sales and the cost of producing those sales. It gives you a picture of how much revenue is left after subtracting all the direct costs of producing and selling the product. These costs can include discounts offered, returns, allowances, production costs, and purchases. I talk about these costs in greater detail in Chapter 7.

To calculate gross margin, divide gross profit by net sales or revenues:

- Gross profit ÷ Net sales or revenues = Gross margin

You can find gross profit at the bottom of the sales or revenue section of the income statement. Net sales are at the top of the same section.

Using numbers from Mattel's income statement, you can calculate its gross margin:

- $3,409,197 (Gross profit) ÷ $6,420,881 (Net sales) = 53.1% (Gross margin)

Mattel made a gross profit of 46.5 percent on each dollar of sales. Compare this number with Hasbro's gross margin (using numbers from its income statement). Hasbro doesn't show gross profit, so you must calculate it first by subtracting cost of goods sold ($1,671,980) from net revenues:

- $2,417,003 (Gross profit) ÷ $4,088,983 (Net sales) = 59.1% (Gross margin)

Hasbro has about 6 percent more revenue left after it subtracts its direct costs than Mattel has, which shows that Hasbro has better cost controls on the purchase or production of the toys it's selling.

Investigating operating margin

The operating margin takes the financial report reader one step further in the process of finding what's left over for future use and looks at how well a company controls costs, factoring in any expenses not directly related to the production and sales of a particular product. These costs include advertising, selling (sales staff, sales offices, sales materials, and other items directly related to the selling process), distribution, administration, research and development, royalties, and other expenses.

Selling and advertising expenses aren't factored into the cost of goods sold, which were subtracted out before calculating gross margin, because these expenses usually involve the sale of a number of products or even product lines. These expenses can rarely be matched to a specific sale of a specific product in the same way that the cost of actually manufacturing or purchasing that product can be matched.

Divide operating profit by net sales or revenues to calculate the operating margin:

- Operating profit ÷ Net sales or revenues = Operating margin

You can find net sales or revenues at the top of the income statement and find the operating profit at the bottom of the expenses-from-operations section on the income statement.

Using numbers from Mattel's income statement, you can calculate the operating margin:

- $1,021,015 (Operating profit) ÷ $6,420,881 (Net sales) = 15.9% (Operating margin)

Mattel made an operating margin of 15.9 percent on each dollar of sales. Compare this number with Hasbro's operating margin (using numbers from its income statement):

- $551,785,000 (Operating profit) ÷ $4,088,983 (Net sales) = 13.5% (Operating margin)

Hasbro made an operating profit of 13.5 percent on each dollar of sales.

You can see that the tables have turned. Now that all indirect expenses are factored into the equation, you can see that Hasbro lost its big advantage over Mattel on costs. Hasbro's operating profit is 2.4 percent lower than Mattel's.

One key expense factor that hurts Hasbro is that its royalty expenses (more than $302 million) are much higher than Mattel's. Hasbro buys the rights to toys instead of developing them in-house, so it must pay royalties on its toys.

Mattel traditionally develops more of its toys in-house and has much lower royalty payments. In fact, when you look at Mattel's income statement, you don't even see royalties separated out from other selling and administrative expenses.

Companies with an operating margin that's higher than the industry average usually can better hold down their cost of goods sold and operating expenses. Maintaining a higher operating margin means the company has more price flexibility during hard times. If a company with a higher operating margin must lower prices to stay competitive, more room is available to continue earning profits even when they must sell products for less.

Catching the leftover money: Net profit margin

The net profit margin looks at a company's bottom line. This calculation shows you how much money the company has left after it has deducted all expenses — whether from operations related to the production and selling of the company's products or from nonoperating expenses or revenue not related to the company's sales of products or services.

For example, one nonoperating revenue item is interest earned on a company's bond holdings. That money isn't generated by operations but is still considered earnings for the company. After the operating income line on the income statement, you most likely see a line for interest expense. This line represents the interest the company paid out on corporate debt. You also see income taxes expense, which indicates the amount the company paid in taxes. These items are two of the biggest charges left to subtract from operating income. The only exception to this rule is if a large extraordinary charge from a special event, such as discontinued operations or the purchase or sale of a division, appears on the income statement. Any extraordinary charges also appear on the income statement after the operating income line.

To find net profit margin, divide net profit by net sales or revenues:

- Net profit ÷ Net sales or revenues = Net profit margin

You find the net profit at the bottom line of the income statement; it may also be called net income or net loss. Net sales or revenue is on the top line of the income statement.

You can calculate the net profit margin using numbers from Mattel's income statement:

- $776,464,000 (Net profit) ÷ $6,420,881,000 (Net sales) = 12.1% (Net profit margin)

Mattel made a net profit of 10.05 percent on each dollar of sales. Now calculate Hasbro's net profit margin using numbers from its income statement:

- $335,999,000 (Net profit) ÷ $4,088,983 (Net sales) = 8.2% (Net profit margin)

Hasbro made a net profit of 8.2 percent on each dollar of sales. Comparing Mattel's and Hasbro's net profit margins, Mattel appears to be more successful than Hasbro at generating a net profit per dollar of sales. The key question investors must then ask is whether Mattel will perform as well in the future.