Chapter 10

Paying Employees

In This Chapter

Working through your payroll checklist

Signing up new employees

Paying employees their dues, one by one by one

Chucking a sickie, heading for Bali, rostering days off, and more

Keeping a set of immaculate records (why not?)

Working with payroll, especially if you’re managing the payroll for any more than a handful of employees, is one of the more demanding roles for a bookkeeper. Not only is the bookkeeping itself very technical, but figuring out minimum pay and conditions for each employee makes organising high school reunions look easy.

But hey, there’s an upside. A bookkeeper who’s skilled in payroll can earn big bucks. And deciding who gets paid and who doesn’t each week is a deliciously powerful feeling (just kidding).

So in this chapter, I provide a straightforward introduction to payroll, talking up the business of taking on new employees, processing pay, calculating leave entitlements and keeping good records. If you feel yourself flagging, just take a moment to reflect on how I must feel having to write this stuff. And remember, your value as a bookkeeper is building dollar by dollar with every page you read.

Staying Squeaky Clean

A payroll officer is responsible for all aspects of payroll management: Calculating pay, deducting tax, paying superannuation and keeping abreast of office affairs. (No, not that kind of affair. After all, the heading of this section is about staying squeaky clean.)

In Figure 10-1, I show a simple employment checklist. As you can see, the obligations of managing payroll don’t just relate to calculating

Figure 10-1: Taking on a new employee? Your payroll checklist.

|

Payroll Checklist |

|

|

Australia only |

|

|

⇒ |

Have all employees completed a tax file number (TFN) declaration? |

|

⇒ |

Is the business complying with all relevant awards and standards as regards employee pay and conditions, or is there some other kind of employment contract or official workplace agreement in place? (Don’t forget — employment contracts can’t undercut the award.) |

|

⇒ |

Have you supplied all new employees with a Fair Work Information Statement? |

|

⇒ |

Do you have a copy of all relevant awards or agreements at your workplace available for employees to read? |

|

⇒ |

Do you provide payslips with every employee pay that includes all the necessary information such as employer name, date and period of payment, any deductions and superannuation payments? |

|

⇒ |

Are you aware of the payroll tax threshold for your state, and are you paying this tax if you exceed this threshold? |

|

⇒ |

Have you supplied all eligible employees with a Standard choice form for superannuation? |

|

⇒ |

Do you have a workers compensation policy so that all employees are insured in the event that they have an accident? |

|

New Zealand only |

|

|

⇒ |

Have all employees completed a tax code declaration (IR330) form? |

|

⇒ |

Has the employer sent a covering letter with the employee’s initial offer of employment, and has the employee signed this covering letter to say that they accept the offer as well as the conditions in the employment agreement? |

|

⇒ |

Is there a written employment agreement in place for every employee? |

|

⇒ |

Is the business paying the minimum wage or above for all employees? |

|

⇒ |

Do you have copies of the KiwiSaver information pack (KS3) to give to new employees, and have you provided Inland Revenue with details of any employees who are registered? |

|

⇒ |

Have you supplied a KiwiSaver deduction form (KS2) to employees joining for the first time? |

|

Both countries |

|

|

⇒ |

Have you — or the business owner — double-checked with the company accountant whether any subcontractors should really be considered employees for taxation, superannuation and/or workers compensation purposes? |

|

⇒ |

Do you understand how to calculate employee tax (called PAYG tax in Australia, or PAYE tax in New Zealand) and superannuation (called KiwiSaver in New Zealand)? |

|

⇒ |

Do you maintain and keep all necessary employment records, which, most often, include wage rates, leave history, superannuation details, nature of the employment (for example, full-time, part-time or casual) and hours worked? |

pay transactions, and at some point you arrive at a grey area between the responsibilities of a business owner and the responsibilities of a bookkeeper. For example, a bookkeeper isn’t legally responsible for making sure that employment agreements are in place or that employees are paid at least the minimum according to the law — this responsibility falls to the owner. However, an experienced bookkeeper on top of their game knows to check through employment agreements (in New Zealand) or industrial awards (in Australia), and become familiar with these documents.

Unless you’re the business owner as well as the bookkeeper, you won’t personally be responsible for all items on this checklist. However, you can use this list to have a conversation with the business owner about what you’re responsible for, and what you’re not. (And, if you end up being responsible for the whole box and dice, then why not ask for a pay rise?)

Hiring a New Employee

So you’re about to organise the paperwork for a new employee? Don’t think that life is so simple as a handshake agreement and an envelope of cash at the end of a working week. No, you have to fight your way out of a mound of paperwork as high as Mount Everest before you can even say ‘boo’. Not that saying ‘boo’ is quite how you greet a new employee, but never mind.

Getting the paperwork in order

The first step with every new employee is to get them to fill in a form outlining their personal details. No, not that personal, just a bit personal:

1. On the employee’s first day (or before), present them with either a tax file number (TFN) declaration (Australia) or a tax code declaration IR330 (New Zealand).

In Australia, you can pick up this form from most newsagencies or order some by phoning 1300 720 092. In New Zealand, www.ird.govt.nz is the spot to go.

2. Ensure the employee completes this declaration before the first payday.

I suggest you provide an incentive: Say ‘No form — no pay.’ Why? Because if an employee doesn’t give you a completed declaration by the time payday comes around, you have to deduct tax at a rate of 46.5 per cent (Australia) or 46.7 per cent (New Zealand).

3. If the employee is entitled to any tax rebates, provide a Withholding declaration form (Australia only).

Some employees claim reduced tax rates by anticipating an entitlement for zone rebates, dependent spouse rebates and so on. However, if someone doesn’t complete a Withholding declaration, and you deduct tax at the standard rate, the employee gets a refund at tax return time.

4. ![]() Post or electronically lodge the tax file number declaration to the Tax Office within 14 days of the employee completing the form (Australia only).

Post or electronically lodge the tax file number declaration to the Tax Office within 14 days of the employee completing the form (Australia only).

You have no idea how often bookkeepers forget to send off these forms. So dare to be different, and get your form(s) to the Tax Office without delay. (In New Zealand, you don’t need to post these forms, just keep ’em in a safe place.)

5. Store your copy of each employee’s tax declaration in a private place.

No, I don’t mean your undies drawer. Rather, store employee declarations in a place where other employees can’t find them, preferably in a file you keep for each employee.

Covering against mishaps

I was having a drink the other night at our local hotel when I overheard one guy say to the other, ‘What’s happened to Harry; did he win Lotto or something?’ ‘Nah’, his mate replied, ‘the lucky bastard injured himself at work.’

![]() In Australia, whatever your personal feelings, no employer can afford to ignore workers comp insurance. The idea behind workers comp is that all employers pay insurance to cover for the event of an employee getting injured at the workplace. This insurance means the employee receives compensation if unable to work. I list the contact details for the government regulators of workers comp in each Aussie state in Table 10-1.

In Australia, whatever your personal feelings, no employer can afford to ignore workers comp insurance. The idea behind workers comp is that all employers pay insurance to cover for the event of an employee getting injured at the workplace. This insurance means the employee receives compensation if unable to work. I list the contact details for the government regulators of workers comp in each Aussie state in Table 10-1.

If you’re simply a bookkeeper (rather than a business owner), you’re not usually responsible for ensuring that your employer has workers comp insurance in place, but you may sometimes be expected to assist with the annual insurance declarations. I cover this topic in Chapter 12.

In New Zealand, workplace accident cover is automatic, because when a business registers as an employer, Inland Revenue automatically informs the Accident Compensation Corporation (ACC), which in turn sets about contacting the business owner. (To contact the ACC for more details, visit www.acc.co.nz.)

Employees (not employers) pay an additional levy to the ACC (which is added onto the PAYE rates in the tax tables). This levy provides insurance for accidents that happen outside of work, such as being mashed in a collapsing scrum on the rugby field or falling into the gooseberry bush and breaking your arm.

|

Table 10-1 Workers Compensation — Australia |

|||

|

State |

Authority |

Phone |

Website |

|

ACT |

ACT WorkCover |

02 6207 3000 |

|

|

NSW |

WorkCover NSW |

13 10 50 |

|

|

NT |

NT WorkSafe |

1800 019 115 |

|

|

QLD |

WorkCover Queensland |

1300 362 128 |

|

|

SA |

WorkCover SA |

13 18 55 |

|

|

TAS |

WorkCover Tasmania |

1300 366 322 |

|

|

VIC |

WorkSafe Victoria |

1800 136 089 |

|

|

WA |

WorkCover WA |

1300 794 744 |

|

Subscribing to super (Australia only)

The whole superannuation rigmarole gets a little overwhelming. To keep up to date (after all, this information that I write here could have changed by dinner time, let alone by the time you’re reading this), I suggest you visit www.ato.gov.au/businesses and make your way to the Superannuation page. However, at the moment, the superannuation samba steps go like this:

1. Figure out whether you need to worry about super at all.

If a business has any employees who earn more than $450 a month (in any one month of the year), or pays contractors for work that is primarily for labour, then super comes into the picture.

2. Double-check employment awards, agreements or contracts for any differences in super calculation methods.

A handful of awards and agreements have weird differences when it comes to super, such as having to pay 5 per cent if an employee earns between $350 and $450 a month.

3. Get super fund details for each employee.

By super funds details, I mean the name of the fund and that employee’s membership number. If an employee doesn’t already belong to a fund, sign them up for your default super fund.

4. If necessary, supply everyone with a Standard choice form.

Depending on the award, agreement or other arrangement under which they are employed, some employees may be eligible to choose their superannuation fund. In this case, you need to provide them with a Standard choice form within 28 days of starting employment.

5. For each employee, inform their superannuation fund of the employee’s tax file number.

Get this together within 14 days of receiving an employee’s tax file number declaration form.

6. Every month or quarter, figure out how much you owe.

Not sure how? See the section later in the chapter ‘Calculating superannuation (Australia only)’ for more details.

7. ![]() Pay up.

Pay up.

You’re obliged to pay superannuation on the 28th day after the end of each month or quarter (the minimum frequency is per quarter, but some super funds specify that you have to pay monthly). Of course, if a business has a lot of employees, you’re likely going to pay super into several different funds. (I talk more about paying superannuation obligations in Chapter 12.)

Submitting to KiwiSaver (New Zealand only)

KiwiSaver is a voluntary, long-term savings plan initiated by the New Zealand government in the hope of getting folks to save. (Employees who sign up get heaps of benefits, including a $1,000 kick-start bonus and member tax credits of up to $20 a week.)

I don’t have space here to detail every itsy-bit about how KiwiSaver works, and for the 100-page low-down, you need to head to www.ird.govt.nz/kiwisaver. In the meantime, here’s your quick-and-dirty guide:

1. Check whether new employees are eligible to join KiwiSaver.

KiwiSaver is open to all New Zealand citizens (or people entitled to be in New Zealand indefinitely) who are under the age of 65. Some employees are exempt, such as casuals on temporary employment of 28 days or less, or employees not required to have PAYE deductions from their wages. (See www.ird.govt.nz/kiwisaver for details.)

![]() 2. Check whether new employees should be automatically enrolled.

2. Check whether new employees should be automatically enrolled.

All businesses must enrol eligible new employees, unless they provide access to another registered superannuation scheme.

3. Give each new employee a KiwiSaver employee information pack (KS3) and KiwiSaver deduction form (KS2) within seven days.

New employees complete the KiwiSaver deduction form (KS2), to let you know whether they want 2, 4 or 8 per cent of their pay deducted. (Existing employees who want to opt in or change their contribution rate can also complete and sign these forms.)

By the way, employees can choose to opt out from the scheme after two weeks. However, right now you only have to worry about them signing up!

4. Tell Inland Revenue all about it.

Send Inland Revenue the full names, IRD numbers and addresses of any employees you’re enrolling using the KiwiSaver employee details form (KS1). (You don’t need to send this info if the employee was already a KiwiSaver member.)

5. Deduct the right amount from the employee’s pay.

If an employee has completed a deduction form, deduct whatever was agreed on that form. If an employee gives you diddly-squat, then deduct 2 per cent from their pay.

6. Calculate the compulsory contribution.

You have to make a compulsory contribution for every employee enrolled in KiwiSaver. The minimum employer contribution is 2 per cent, but some employers may give more. You calculate KiwiSaver on any employee payments that are subject to PAYE tax. Don’t include any non-cash benefits or non-taxable allowances that are essentially reimbursements in nature.

7. Send the money you deduct to Inland Revenue, along with your PAYE payments.

That sexy Employer deductions form takes some beating as far as government forms go. Confused? Ask the company accountant to give you a hand.

![]() By the way, existing employees can also choose to opt in to the KiwiSaver scheme. If they do, supply them with the necessary forms and follow the same procedures as for new employees.

By the way, existing employees can also choose to opt in to the KiwiSaver scheme. If they do, supply them with the necessary forms and follow the same procedures as for new employees.

Doling Out the Cash on Pay Day

Paying employees is a job that’s not without pressure. If you goof up and underpay someone, chances are you’ll get an earful from a disgruntled employee the next morning. If you overpay someone, you may be blessed with an eerie silence for days, weeks or even months, but you’re back in the dungeon if your employer finds out.

To cope with the pressure, I suggest you devote your full attention to getting everything just right. Now is the ideal opportunity for your inner pedant to blossom. Out go the silk stockings, on go the horn-rimmed spectacles. Out go the plunging necklines, on goes the cashmere twinset. Payroll is a serious business, and you’re just the (wo)man for the job. (No, I’m not displaying any gender bias here — a bloke in a cashmere twinset and silk stockings is just fine by me.)

Paying folks their dues

So you’re new on the job and doing payroll for the first time. You pick up the first timesheet in the pile. According to what’s written, this employee seems to arrive just before nine, leaves at five, and takes an hour for her lunch. Although you can’t see any breaks marked on her timesheet, you know that almost all employees take a break of 10 minutes every morning and afternoon. You can also see that this dedicated staff member rang in sick on Wednesday (no medical certificate), arrived late on Thursday because her cat had kittens and took a day’s holiday on the Friday. You, lucky bunny, have to calculate her pay. Where do you start?

Always check that employees have enough leave accruals before paying leave: For example, if an employee chucks a sickie, you need to check that they have enough sick leave available. If not, talk to your employer who may decide to let this employee have sick leave in advance, take a day’s leave unpaid or take a day’s annual leave.

Be clear about which breaks are paid, and which are unpaid: When calculating total hours worked, look up the award (Oz) or employment agreement (NZ) to figure out which breaks are paid, and which are unpaid. (Typically, most awards/employment agreements allow for one or two paid coffee breaks per day, usually 10 minutes each, but lunch is an unpaid break.)

![]() Don’t be tricked by fractions: Remember to calculate hours as decimals, not minutes. For example, if an employee works 8 hours and 15 minutes, this actually means they worked eight and a quarter hours, so key in 8.25 hours, not 8.15 hours. (Maybe now you’ll regret all those times when you went surfin’ instead of going to maths class . . .)

Don’t be tricked by fractions: Remember to calculate hours as decimals, not minutes. For example, if an employee works 8 hours and 15 minutes, this actually means they worked eight and a quarter hours, so key in 8.25 hours, not 8.15 hours. (Maybe now you’ll regret all those times when you went surfin’ instead of going to maths class . . .)

![]() Don’t forget allowances: Stay alert for any allowances due to employees such as weekend loadings, uniform allowance, vehicle allowance or first aid allowance. (Note: Employee allowances are much more common in Australia than they are in New Zealand.) Some allowances are paid for every shift (such as a Saturday loading), some allowances are paid weekly (such as a uniform allowance) and some allowances are paid monthly (such as motor vehicle allowance).

Don’t forget allowances: Stay alert for any allowances due to employees such as weekend loadings, uniform allowance, vehicle allowance or first aid allowance. (Note: Employee allowances are much more common in Australia than they are in New Zealand.) Some allowances are paid for every shift (such as a Saturday loading), some allowances are paid weekly (such as a uniform allowance) and some allowances are paid monthly (such as motor vehicle allowance).

Find out the rules about medical certificates: In Australia, some workplaces demand medical certificates before granting sick leave; other workplaces only demand medical certificates for sick leave of three days or more. In New Zealand, an employee must provide a medical certificate if they are sick for three days or more, but the employer can demand a medical certificate for a shorter time if they suspect the employee is fudging it. In this case the employer must pay for the doctor’s visit.

Get the rate right! If you’re new to the job, the pay rates are probably correct at the moment. However, part of a payroll officer’s job often includes staying tuned to pay increases and changes to industrial relations legislation. See Chapter 12 for more details.

If you record wages using accounting software, here are a few other points to bear in mind:

![]() Set up employees so that pays calculate automatically: Set up each employee with standard pay details so that pay is calculated automatically. This way you only need to adjust an employee’s pay if anything is different from normal (such as commission paid, holiday or sick pay).

Set up employees so that pays calculate automatically: Set up each employee with standard pay details so that pay is calculated automatically. This way you only need to adjust an employee’s pay if anything is different from normal (such as commission paid, holiday or sick pay).

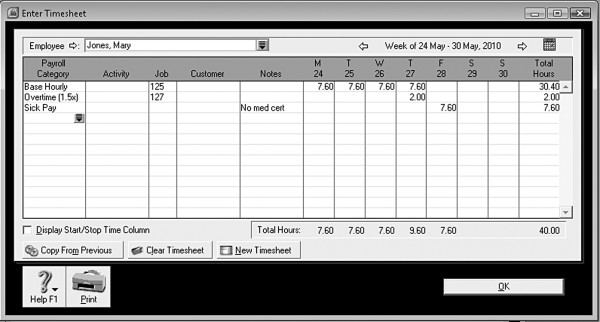

Speed your work with timesheet features: Some accounting software has timesheet features, so you can record start and finish times and send this information through to weekly payroll. I like working in this way because not only do you meet all your record-keeping obligations (some awards specify that you keep track of start and finish times), but you use the accounting software to calculate total hours, all in the one go. Figure 10-2 shows a typical timesheet record.

Use different pay categories to record leave: Remember that when an employee takes leave, even though they get the same pay, you reduce the hours you allocate to Hourly Pay or Base Hourly and increase the hours you allocate to Holiday Pay or Sick Pay.

Figure 10-2: If the feature exists, try using the timesheets feature in your accounting software.

Taxing pay (no mercy shown)

![]() You can find out how much tax to deduct from employees’ pay in three different ways:

You can find out how much tax to deduct from employees’ pay in three different ways:

In Australia, use the tax calculator at www.ato.gov.au (available from the Pay Staff page in the Business section). In New Zealand, use the tax calculator at www.ird.govt.nz/calculators/keyword/paye.

Pick up a set of printed tax tables from your local newsagent (Australia) or, in New Zealand, print a copy from the IRD’s website (the IRD no longer distributes hard copies).

Use accounting/payroll software.

With this info close to hand, you still need to make sure that you select the right level of tax for each employee. Grab the employee’s newly completed tax file number declaration (Australia) or tax code declaration (New Zealand) form, and check the following:

![]() Is this employee a resident of this fair country? In Australia non-residents have a different tax scale because they don’t receive the tax-free threshold and they don’t pay the Medicare levy. In New Zealand, you must deduct PAYE and ACC (accident compensation) from wages paid to non-resident employees in the same way as for resident employees. However, a non-resident may be entitled to an exemption from New Zealand tax under either a double taxation agreement or the 92-day rule (check with the IRD if you think this may apply).

Is this employee a resident of this fair country? In Australia non-residents have a different tax scale because they don’t receive the tax-free threshold and they don’t pay the Medicare levy. In New Zealand, you must deduct PAYE and ACC (accident compensation) from wages paid to non-resident employees in the same way as for resident employees. However, a non-resident may be entitled to an exemption from New Zealand tax under either a double taxation agreement or the 92-day rule (check with the IRD if you think this may apply).

Does this employee have a tax file/IRD number? If an employee doesn’t provide a tax file/IRD number, you have to deduct tax at the top marginal rate (also called the non-declaration rate), which is currently 46.5 per cent in Oz, and 46.7 per cent in NZ.

Does this employee have a uni debt or student loan? If so, this employee has to pay extra tax if they earn over a certain amount per week.

Does this employee have a second job? If an employee has two or more jobs, make sure to select the correct tax scale (you tax second jobs at a higher rate).

Is this employee claiming a Medicare exemption (Australia only)? If so, ask the employee to provide you with a Medicare Variation Form.

Phew! Even with the answers to these questions in hand, you still have a few other things to consider before you tax each employee within an inch of their life:

Are tax tables up to date? Tax tables tend to change every year on 1 July in Australia, or 1 April in New Zealand.

What is the pay frequency? For example, if you pay employees fortnightly, don’t select a weekly tax scale (or you will be overtaxing an employee).

Is tax calculated before or after deductions? If you make any deductions from employee pay (such as child support, loan repayments or union fees), consult the company accountant about whether you calculate tax before or after this deduction. (Sadly, nearly all deductions are made after tax is deducted!)

Does this employee receive leave loading when they go on holiday? In Australia, employers aren’t meant to tax the first $320 of an employee’s leave loading, so tax scales differentiate between those who receive leave loading and those who don’t. (Leave loading is a bonus 17.5 per cent payment that employees receive on top of regular holiday pay, in order that the holiday can be that little bit more special.)

![]() Is this employee receiving a one-off payment? Remember that tax on irregular payments such as bonuses and termination or redundancy pay has different calculation rules.

Is this employee receiving a one-off payment? Remember that tax on irregular payments such as bonuses and termination or redundancy pay has different calculation rules.

Dealing with deductions

If you take money from an employee’s pay, chances are that it’s a deduction. The most common deductions include child support, additional superannuation (or KiwiSaver in New Zealand) and union fees; other deductions include repayments of employee advances and loans, health insurance, salary packaging, social club membership and workplace giving programs.

The most important point to consider about any deduction category is how it shows up in your accounts. Just think: If you deduct an amount from an employee’s pay, the inevitable consequence is that you have to pay this money to someone else, whether this payment is due to a union, a finance company or the Child Support Agency. You mustn’t forget that you owe this money!

![]() Every payroll deduction creates a liability. If you use accounting software, make sure that every payroll deduction category links back to a specific liability account in your chart of accounts. If you use a spreadsheet or do books by hand, you must track this liability and make sure that every month, you pay out exactly the same amount as you deducted from employee pay.

Every payroll deduction creates a liability. If you use accounting software, make sure that every payroll deduction category links back to a specific liability account in your chart of accounts. If you use a spreadsheet or do books by hand, you must track this liability and make sure that every month, you pay out exactly the same amount as you deducted from employee pay.

![]() Get smart

Get smart

I remember my first payroll job. With no training, no understanding of industrial relations and little previous employment, I was suddenly in charge of a payroll for 14 staff. I muddled along doing my best, but the more I learned, the more I realised how many mistakes I’d been making along the way (some of which cost my employer a fair bit of dough).

In Bookkeeping For Dummies, I only touch on the topic of payroll (covering day-to-day transactions in this chapter, and reporting obligations in Chapter 12). After all, to cover payroll in full detail warrants a book in itself. If you find yourself responsible for payroll, don’t underestimate the challenge involved, and seek advice whenever a transaction is out of the ordinary. For example, you may be confident about how to look up the amount of tax to deduct from an employee’s wages, but if you do a final pay for an employee, you need to calculate tax differently.

If you’re responsible for payroll and you don’t have any formal training, then I suggest you ask your employer if they can send you on a course. In Australia, your best bet is probably the Association of Payroll Specialists (TAPS), which runs regular courses in the capital cities and some distance education courses as well (see www.payroll.com.au for more details). In New Zealand, the New Zealand Payroll Practitioners’ Association is a similar kind of organisation (visit www.nzppa.co.nz for more details). Alternatively, if you use computerised payroll, then check with your software provider for courses.

Calculating superannuation (Australia only)

In Australia, superannuation is a handsome 9 per cent of ordinary time earnings. Ordinary time earnings includes all regular wages, but doesn’t include irregular payments such as annual holiday leave loading, one-off bonuses, overtime and so on. I provide a summary of the definition of ordinary time earnings in Table 10-2.

|

Table 10-2 When You Have to Pay Super (and When You Don’t) |

|

|

You Must Pay Super on . . . |

You Don’t Have to Pay Super on . . . |

|

Non-expense allowances |

Expense allowances (such as motor vehicle) |

|

Bonuses |

Annual holiday leave loading |

|

Casual loadings |

Benefits subject to FBT |

|

Payments in lieu of notice |

Accrued leave on termination |

|

Government wage subsidies |

Maternity or paternity leave |

|

Holiday pay |

Overtime payments |

|

Long service leave |

Top-up payments (when on jury duty) |

|

Sick pay |

Redundancy payouts |

|

Regular wages |

Reimbursement of expenses |

|

Shift loadings |

Workers compensation payments |

So for example, if you pay an employee $500 a week, you pay an additional $45 a week (which is $500 multiplied by 9 per cent) into a complying superannuation fund on the employee’s behalf.

Sounds simple? Pretty much, but you do get a few exceptions to this flat 9 per cent rule:

The most common exception is for casual employees who earn less than $450 in a single month. If casuals earn less than $450 in a single month, you don’t have to pay a cent.

You don’t have to pay super to employees under 18 who work 30 hours a week or less.

Some domestic workers such as nannies and housekeepers are exempt if they work fewer than 30 hours a week. (Why housekeepers, who are saints sent from heaven as far as I’m concerned, should be a unique category deprived of super beats me, but there you go.)

![]() Stay clear of heavy fines and pay super for everyone who’s entitled to it, even if an employee is hired and fired by the time you come to pay super.

Stay clear of heavy fines and pay super for everyone who’s entitled to it, even if an employee is hired and fired by the time you come to pay super.

Taking Leave in the Land of Oz

Tracking employee holiday and sick leave is tricky. You’ve got to figure out what kind of leave employees are entitled to receive, how much leave each employee gets each year and how much leave you owe at any one time.

You can calculate leave entitlements using either a fixed number of hours per pay period or a percentage calculation. A fixed number of hours per pay period tends to work best for full-time salaried employees whose hours stay constant from week to week. Percentage calculations work well for part-timers, especially for part-timers whose hours vary from week to week.

![]() Don’t ever pay anybody a cent’s leave without first reading every single last line of their industrial award. Different employee awards stipulate different amounts of holiday and sick leave per year, and calculation methods often vary for shift workers or permanent employees working irregular hours.

Don’t ever pay anybody a cent’s leave without first reading every single last line of their industrial award. Different employee awards stipulate different amounts of holiday and sick leave per year, and calculation methods often vary for shift workers or permanent employees working irregular hours.

Calculating leave on a percentage basis

If you employ a lot of part-timers who work different numbers of hours, calculating entitlements on a percentage basis is the way to go. Check out how to calculate the correct percentage by absorbing the following examples:

Annual leave: If an employee receives 20 days holiday per year and there are 260 working days in the year (that’s 52 × 5), then the sum for calculating annual leave equals 20 divided by 260. Multiply this by 100 to equal 7.6923 per cent.

Sick leave: If an employee receives 10 days sick leave per year and there are 260 working days in the year (that’s 52 × 5), then the sum for calculating annual leave equals 10 divided by 260. Multiply this by 100 to equal 3.8461 per cent.

![]() Different accounting software packages take different approaches to calculating entitlements. Table 10-3 shows a quick reference for different calculation methods, regardless of how many hours are in a working week.

Different accounting software packages take different approaches to calculating entitlements. Table 10-3 shows a quick reference for different calculation methods, regardless of how many hours are in a working week.

|

Table 10-3 Calculating Leave Entitlements |

|||

|

Amount of Leave Per Year |

Hours Accrued Per Hour Paid |

Percentage Calculation |

Time Accrued for Every Hour Worked |

|

5 days |

0.019214 |

1.9214% |

1 min 9 secs |

|

8 days |

0.30786 |

3.0786% |

1 min 50 secs |

|

10 days |

0.038464 |

3.8464% |

2 mins 18 secs |

|

20 days |

0.076929 |

7.6923% |

4 mins 36 secs |

![]() If you calculate leave entitlements on a percentage basis, make sure that you don’t calculate leave entitlements on anything other than regular pay (you don’t want an employee to receive extra holiday leave just because they work overtime or receive a tool allowance). In other words, you accrue leave entitlements on base salary, base hourly pay, holiday pay and sick pay. You don’t accrue leave entitlements on allowances, holiday leave loading and overtime.

If you calculate leave entitlements on a percentage basis, make sure that you don’t calculate leave entitlements on anything other than regular pay (you don’t want an employee to receive extra holiday leave just because they work overtime or receive a tool allowance). In other words, you accrue leave entitlements on base salary, base hourly pay, holiday pay and sick pay. You don’t accrue leave entitlements on allowances, holiday leave loading and overtime.

Calculating hours per pay period

If you employ mostly full-time salaried employees whose hours stay fairly constant, you’re usually best to calculate employee entitlements as a fixed number of hours per pay period. This begs the question: How do you calculate how many hours an employee accrues per pay period?

1. Confirm how many weeks’ leave each employee is entitled to per year.

For example, an employee may be entitled to four weeks’ holiday, two weeks’ sick leave and one week long service leave per annum.

2. Multiply the number of hours in the employee’s working week by the number of weeks’ entitlement.

For example, if an employee is entitled to four weeks’ holiday leave per year and they work a 38-hour week, then they are entitled to 152 (that’s 4 × 38) hours holiday per year.

3. Divide the total number of hours leave per year by the number of pay periods per year.

For example, if an employee is entitled to 152 hours holiday per year and they get paid once a fortnight, then this converts to 5.846 hours leave per fortnight (that’s 152 divided by 26).

4. Double-check that your figures make sense.

Table 10-4 provides a quick guide to help you figure out how many hours to accrue per pay period for standard working weeks and common leave amounts. For example, if you give an employee 20 days holiday leave per year and they work a 38-hour week, this equates to 2.923 hours (which equals 2 hours 55 minutes) per week.

![]() If you use Table 10-4 as your reference, remember to multiply these figures by two if you pay fortnightly, not weekly.

If you use Table 10-4 as your reference, remember to multiply these figures by two if you pay fortnightly, not weekly.

|

Table 10-4 Converting Leave Entitlements to Hours Accrued |

||||

|

Days |

28-hour Week |

35-hour Week |

38-hour Week |

40-hour Week |

|

5 days |

0.538 |

0.673 |

0.731 |

0.769 |

|

8 days |

0.862 |

1.077 |

1.169 |

1.231 |

|

10 days |

1.077 |

1.346 |

1.462 |

1.538 |

|

20 days |

2.154 |

2.692 |

2.923 |

3.077 |

Taking Leave in New Zealand

Tracking employee holiday and sick leave is tricky. You’ve got to figure out what kind of leave employees are entitled to receive, what pay rate to use, how much leave each employee gets each year, and how much leave you owe at any one time. You’re best to use a payroll program to help here, as working out average weekly earnings manually is so complex that even maths graduates quail at the thought. (Hopefully the Holiday Pay Act 2003 will be simplified in the not too distant future.)

Calculating annual leave for full-timers and part-timers

In New Zealand, you work out an employee’s leave entitlement according to the length of their working week. For example, if an employee works a three-day week and they take a week’s holiday, you pay them for three days.

All employees are entitled to a minimum of four week’s annual holidays after the first year of employment. The calculation for annual holiday is the higher of ordinary weekly pay versus average weekly earnings.

Ordinary weekly pay is everything an employee normally receives weekly, including

Regular allowances, such as a shift allowance

Regular productivity or incentive-based payments (including commission or piece rates)

Regular overtime

The cash value of board or lodgings

On the other hand, you calculate average weekly earnings by getting the total gross earnings an employee received over the 12 months before the annual holiday, and divide this total by 52 (weeks). Gross earnings include all regular payments, allowances and bonuses received during this time.

You can see how different ordinary weekly pay and average weekly earnings can be in Figure 10-3, where ordinary weekly pay comes out at $919.23, but average weekly earnings is a handsome $976.92.

![]() If an employee resigns, you calculate their final holiday pay at a flat rate of 8 per cent of gross earnings from their last anniversary date to their termination date, plus leave owing from their last leave year.

If an employee resigns, you calculate their final holiday pay at a flat rate of 8 per cent of gross earnings from their last anniversary date to their termination date, plus leave owing from their last leave year.

Figure 10-3: Calculating ordinary weekly pay and average weekly earnings.

You calculate annual leave for casuals on a straight 8 per cent of gross earnings, either in the form of pay-as-you-go holiday pay or as a lump sum on termination. (Make sure that any pay-as-you-go holiday payments for casuals are agreed and signed off in the employee’s employment contract.)

![]() If you process pay manually or use a spreadsheet, I can recommend the IRD’s handy holiday pay calculator (called Calculate tax on holiday pay) found at www.ird.govt.nz/calculators.

If you process pay manually or use a spreadsheet, I can recommend the IRD’s handy holiday pay calculator (called Calculate tax on holiday pay) found at www.ird.govt.nz/calculators.

Calculating other kinds of leave

As if calculating holiday pay wasn’t bad enough, you also need to calculate pay for other kinds of leave such as alternative holidays (days in lieu for working public holidays), bereavement leave, public holidays and sick leave. You calculate pay for other kinds of leave using a sexy little figure called relevant daily pay.

Calculating relevant daily pay is a piece of cake: Simply work out the amount of pay that the employee would have received had they worked on the day concerned, remembering to include things like commission, overtime or the cash value of any board or lodgings.

More handy points to bear in mind regarding other kinds of leave include:

Alternative holidays: If an employee works on a public holiday and this day is normally a working day, they are entitled to time and a half for the day they work plus a whole day’s alternative holiday at a later stage. This provision includes shift-workers and, in some cases, employees on call. (Both types of employees get a full day off later, even if they work for only a small part of the public holiday.)

Casual employees: Casual employees earn holiday pay at the minimum rate of 8 per cent but, due to the nature of the work, aren’t generally entitled to sick or bereavement leave.

Relevant daily pay when hours fluctuate: If an employee works different hours from one week to the next, you calculate relevant daily pay based on the last four weeks earnings. For example, imagine an employee has an attack of Mondayitis (a common work-related illness that hits employees on a Monday), and in the last four Mondays they worked four hours, then six hours, then five hours and finally eight hours. To calculate a day’s leave for this employee, you simply take an average over four weeks, paying 5.75 hours in total.

Sick leave: After six months employment, employees are entitled to five day’s sick leave on full pay, plus a further five days of sick leave for every 12 months of employment after that. You pay employees what they would have been paid had they actually worked on the day and weren’t sick. Employees can carry over up to 15 days of unused sick leave from one year to the next, accumulating to a maximum of 20 days over four years. Part-time employees receive the same entitlements as full-time employees, but they only receive sick leave if they are sick on a normal working day.

Employees can take sick leave if they are sick or injured, their spouse is sick or injured, or someone who depends on them is sick or injured.

Maintaining Proper Records

In the last few pages of this chapter, I explain how important it is to keep records regarding employee details, employee pay and employee leave. You can keep these records either electronically (using payroll software or a spreadsheet) or by hand.

![]() Sounds okay, but here’s the rub: You have to keep these records accessible for seven whole years. You can store handwritten records in archive boxes or somewhere in the office; but for computerised records, you’re best to archive data onto a CD, with a separate CD for every payroll year.

Sounds okay, but here’s the rub: You have to keep these records accessible for seven whole years. You can store handwritten records in archive boxes or somewhere in the office; but for computerised records, you’re best to archive data onto a CD, with a separate CD for every payroll year.

Sounds easy, but don’t stop reading yet. Recently, when a client of mine received an audit notice and the rather earnest, bespectacled auditor turned up at her office, she proudly produced her pile of CDs (and even one, ancient floppy disk!) for the last six years. She restored her data without a hitch, but then the problem hit. Some years earlier my client had changed the password she used to view her accounting data. And try as hard as she could (pets, children, ex-lovers, favourite food and more), she couldn’t remember what on earth that password was.

The moral of my story? Store your payroll archives in a safe place and, if these records are computerised, store the password somewhere safe too.

Keeping records of what’s due

Probably the most important thing about paying holiday or sick leave is maintaining proper records. If you’re using accounting software, this can sometimes be tricky, because some software applications purge data every time you start a new payroll year. It can be a real pain if an employee queries their leave entitlements, because you often have to travel back in time to when this employee first started employment — which could be several years ago — in order to justify their current balance.

You’re the only person who knows what method is going to work best for you. Some people like to keep handwritten cards for each employee, logging all leave taken; others make sure to print leave reports for each employee at the end of each year; another approach is simply to be meticulous about retaining payroll backups on CD, year after year. Whatever your preferred poison, choose a method and stick to it.

Figure 10-4 shows a possible format for documenting leave taken in Australia (to download this template, go to Employment Leave Records at www.fairwork.gov.au). Alternatively, you can find a good New Zealand template at www.ema.co.nz/holiday_leave_record.pdf. However, these formats are very time-consuming to maintain and so if you have more than a few employees, your best approach is to figure out how to get your accounting or payroll software to provide this information.

![]() Whatever record-keeping system you use, I suggest you generate a report at the end of each payroll year for each employee that shows the amount of leave accrued during the year, the amount taken and the balance due. Make two copies, giving one copy to each employee and keeping the second copy for yourself. This way, if an employee disagrees about leave calculations, you can figure out who’s wrong before the events fade into ancient history.

Whatever record-keeping system you use, I suggest you generate a report at the end of each payroll year for each employee that shows the amount of leave accrued during the year, the amount taken and the balance due. Make two copies, giving one copy to each employee and keeping the second copy for yourself. This way, if an employee disagrees about leave calculations, you can figure out who’s wrong before the events fade into ancient history.

Figure 10-4: Keep a detailed record of all leave taken.

Keeping tabs on employee details

For every employee, you need to record the date they started employment, whether the employee is full-time, part-time or casual, whether the employee is permanent or temporary and the rate of pay. The easiest and clearest method of recording this information is to provide the employee with a formal letter of offer or agreement when they begin employment (supplying a written agreement is a legal obligation in New Zealand, but not in Australia).

If an employee decides to go their own way — or you give them their marching orders — then you also have to record who terminated the employment (did they jump or were they pushed?), and how the termination took place. Did both parties agree, did the employer give notice, or was this a case of summary (instant) dismissal?

![]() Again, the clearest way of recording information about employee terminations is to get things in writing: If an employee resigns, ask them to provide you with a letter; if you give notice to an employee, then provide confirmation in writing also.

Again, the clearest way of recording information about employee terminations is to get things in writing: If an employee resigns, ask them to provide you with a letter; if you give notice to an employee, then provide confirmation in writing also.

Writing up pay correctly

![]() If you use payroll or accounting software, don’t worry too much about what information you need to record concerning employee pay, because the very process of using software almost always ensures you capture the essentials. The only thing to remember is that some accounting software applications prompt you to enter only total hours, rather than start and finish times. If an employee is paid by the hour, working casual or irregular part-time hours, then you need to store start and finish info separately.

If you use payroll or accounting software, don’t worry too much about what information you need to record concerning employee pay, because the very process of using software almost always ensures you capture the essentials. The only thing to remember is that some accounting software applications prompt you to enter only total hours, rather than start and finish times. If an employee is paid by the hour, working casual or irregular part-time hours, then you need to store start and finish info separately.

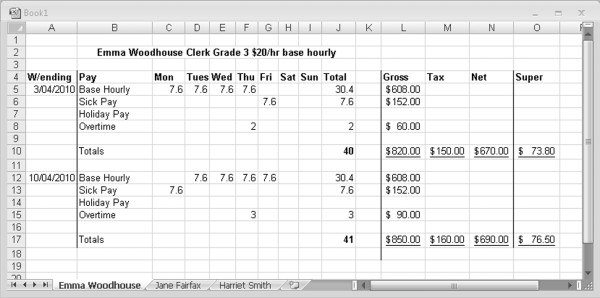

If you record pay by hand or using a spreadsheet, a simple rule of thumb is to write down every bit of info you use in order to calculate someone’s pay. In other words, if an employee works overtime and gets paid a higher rate during this time, ensure your workings show these calculations. You also need to keep a record of daily start and finish times for casual or irregular part-time employees. See Figure 10-5 for a simple spreadsheet adapted from one of my clients. (For privacy purposes, I’ve changed her employees’ names to characters from one of my favourite novels — can you guess which one?)

Figure 10-5: A simple spreadsheet showing pay calculations.

Issuing legit pay slips

In Australia, every time you pay an employee, you must provide them with a pay slip within one working day of the payday. Every pay slip has to include a surprising amount of detail, similar to what you can see in Figure 10-6. (By the way, although full pay slips aren’t a legal requirement in New Zealand, I do recommend you supply all employees with pay slips so that employees can check their pay and pick up on any mistakes before too much time slips by.)

Figure 10-6: Make sure you include enough detail on every pay slip.

Pay slips must include

The name of the employer and the ABN

The employee’s name

The date of payment and the pay period (for example, 24/3/10 to 30/3/10)

The gross and the net amount of pay (that is, the amount before tax and the amount after tax)

Any allowances, bonuses, commissions, loadings or penalty rates, or details of holiday or sick pay paid

If the employee is paid hourly, the hourly rate of pay and the number of hours worked at that rate. Or, if the employee is paid a salary, the annual salary

Any deductions made from the employee’s pay, including the amount and details of each deduction

All superannuation contributions due for that pay, including the name of the superannuation fund that contributions get paid into

![]() If you don’t have accounting software that includes payroll features, you can find a pay slip template at the Fact Sheets & Tools template of the Employers section at the Fair Work website (www.fairwork.gov.au).

If you don’t have accounting software that includes payroll features, you can find a pay slip template at the Fact Sheets & Tools template of the Employers section at the Fair Work website (www.fairwork.gov.au).