Chapter 9

Recording Receipts and Sales

In This Chapter

Recording sales and customer payments — different strokes for different folks

Doing the books for other kinds of income

Staying wise to who owes what

Triumphing over tricky situations

Everyone loves to receive money. I know I do. And so the part of bookkeeping where you get to catalogue sales and match up customer payments is kind of fun.

As a bookkeeper, keeping tabs on how much customers owe is life-and-death stuff. If a business doesn’t chase customers for overdue accounts or extends too much credit without realising, the consequences can get pretty dire. As a bookkeeper, your job is to make sure the books are accurate and up to date, and to keep on the back of recalcitrant payers.

In this chapter, I explain how to keep a simple cash receipts register, and I also explain how to record customer invoices, match payments against invoices, and record other kinds of income, such as bank interest or capital contributions. I also show no fear and delve into the lonely corridors of customer credits and discounts, refunds and rebates, and last but not least, the sad act of writing off bad debts.

Tailoring for the Perfect Fit

A bookkeeper can keep track of income in many different ways. What works best depends on the size of the business that you’re doing books for, your budget and what you’re most familiar with. Here are just a few possible approaches:

If you prefer to do books by hand, the simplest method is to write up a receipts journal that lists all money received in date order, and includes columns for the date, customer name, amount, payment method and GST. See ‘Writing up sales by hand’ later in this chapter for more details.

You can create a receipts journal in the same way using a spreadsheet, although you may prefer to combine payments and receipts on a single worksheet. See ‘Working up a sweat with spreadsheets’ later in this chapter for more details.

![]() You can use accounting software not only to record customer payments, but also to generate sales invoices. See ‘Recording sales using accounting software’ and ‘Recording customer payments using accounting software’ later in this chapter for more details.

You can use accounting software not only to record customer payments, but also to generate sales invoices. See ‘Recording sales using accounting software’ and ‘Recording customer payments using accounting software’ later in this chapter for more details.

The principles of bookkeeping stay constant whatever method you use, and in this chapter I don’t attempt to cast judgement about the pros and cons of handwritten books versus spreadsheets, or spreadsheets versus accounting software. I leave that job to Chapter 5. Instead I explore all three methods, outlining a strategy for each one.

![]() I don’t give detailed step-by-step guides when explaining how to perform tasks using accounting software because this kind of instruction depends on the software you’re using. However, if you need more specific info for either MYOB or QuickBooks software, check out the companion titles MYOB Software For Dummies and QuickBooks QBi For Dummies, both written by yours truly and published by Wiley Australia.

I don’t give detailed step-by-step guides when explaining how to perform tasks using accounting software because this kind of instruction depends on the software you’re using. However, if you need more specific info for either MYOB or QuickBooks software, check out the companion titles MYOB Software For Dummies and QuickBooks QBi For Dummies, both written by yours truly and published by Wiley Australia.

Writing up sales by hand

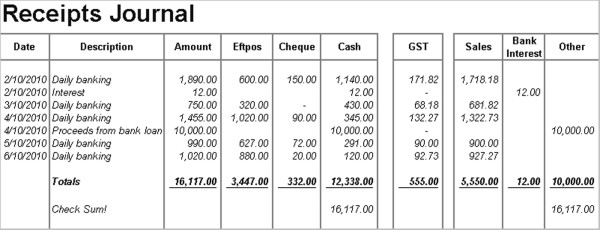

In Figure 9-1 you can see a typical handwritten receipts journal, a term that bookkeepers use to describe a journal that records all transactions relating to business income. This journal lists transactions in date order, showing the amount, including GST, the payment method, the amount of tax and the net value of each sale.

Figure 9-1: A typical handwritten receipts journal.

You can probably make a stab at doing a receipts journal just by buying a ledger book from the newsagent and copying this format, but I’ll chuck a few comments into the mix to help you along:

1. List all transactions in date order.

Work directly from your bank statement, listing each deposit on a separate line. Remember to include miscellaneous income such as bank interest.

2. Show GST in a separate column.

![]() Figure 9-1 shows GST as one-eleventh but if you’re on the east side of the Tasman, then GST works out as one-ninth.

Figure 9-1 shows GST as one-eleventh but if you’re on the east side of the Tasman, then GST works out as one-ninth.

3. Write the net value of each receipt in the relevant income column.

By net, I mean the value before GST. For example, the first line of Figure 9-1 shows daily banking of $1,890. I write $1,890 in the Amount column, $171.82 in the GST column and $1717.18 in the Sales column. On the second line, I write $12 in the Amount column, nothing in the GST column and $12 in the Bank Interest column. If you make any GST-free sales (Australia) or zero-rated sales (New Zealand), create an additional column for these sales.

4. Add any transactions where you didn’t bank the cash.

![]() If you sometimes receive cash and don’t bank it, show these sales in a separate column called ‘Cash Not Banked’ and change the name of the ‘Cash’ column to become ‘Cash Banked’.

If you sometimes receive cash and don’t bank it, show these sales in a separate column called ‘Cash Not Banked’ and change the name of the ‘Cash’ column to become ‘Cash Banked’.

5. Double-check that the bank statement accurately reflects ‘source’ records such as deposit books and EFTPOS merchant totals.

Get the deposit book and make sure that for every page in the deposit book, a matching amount shows up on the bank statement (this process guards against money going missing or getting banked into the wrong bank account, or the bank making mistakes). Similarly, if match daily EFTPOS merchant totals against daily deposits on the bank statement.

6. Grab your calculator and total each column.

7. Double-check that the totals match.

Add up the total of the GST column and all the columns to the right of that column, and write this total on the bottom line in the far-right column (in Figure 9-1, this total equals $16,117). Compare this total to the total of the Amount column. The two figures should match! In addition, add up the total of each payment method column (in Figure 9-1, I add up the columns for EFTPOS, cheque and cash). I can sleep easy tonight, knowing that this grand total also equals $16,117.

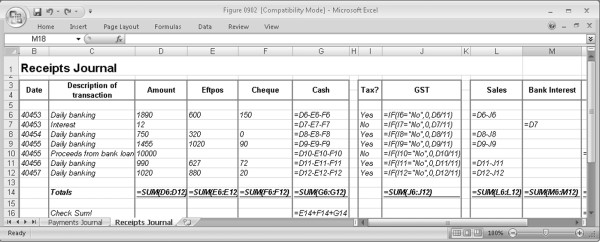

Working up a sweat with spreadsheets

Back in Chapter 8, I talk about writing up payments and receipts using a spreadsheet; and in Figure 8-2, I show a journal with both types of transactions, along with a column that tracks the running balance. I favour this method for small businesses with a limited number of payments and receipts.

However, if you do a lot of income analysis, or if you have a mixture of taxable and non-taxable sales, you may prefer to mimic traditional bookkeeping and maintain one spreadsheet for cash payments and another spreadsheet for cash receipts.

In Figure 9-2, you can see a cash receipts spreadsheet that’s pretty much the exact mirror of the handwritten transactions in Figure 9-1. The beauty of spreadsheets is that they do all the adding automatically, so long as you insert a few simple formulas. In Figure 9-2, I’ve changed the view settings so you can see what formulas I’ve used.

Figure 9-2: Using formulas in spreadsheets makes doing your books much quicker.

![]() By the way, I find that spreadsheets work well for recording customer receipts but aren’t ideal for tracking how much customers owe you. However, a small owner-operated business can get away with generating invoices using a word processor, filing invoice copies in a folder and marking each invoice when payment is received. Alternatively, you can keep things real simple, writing invoices by hand using a carbon-copy invoice book and marking each invoice copy when you receive payment.

By the way, I find that spreadsheets work well for recording customer receipts but aren’t ideal for tracking how much customers owe you. However, a small owner-operated business can get away with generating invoices using a word processor, filing invoice copies in a folder and marking each invoice when payment is received. Alternatively, you can keep things real simple, writing invoices by hand using a carbon-copy invoice book and marking each invoice copy when you receive payment.

Recording sales using accounting software

![]() When you record income from customers using accounting software, you don’t simply record the receipt of money. Instead, you use the accounting software to first record the sale and then later, when you receive money from the customer, to record the payment.

When you record income from customers using accounting software, you don’t simply record the receipt of money. Instead, you use the accounting software to first record the sale and then later, when you receive money from the customer, to record the payment.

I explain in Chapter 3 the difference between cash and accrual accounting. When you beaver away using a receipts journal — which is what I talk about in the earlier sections ‘Writing up sales by hand’ and ‘Working up a sweat with spreadsheets’ — you work on a cash basis. On the other hand, when you record sales and then payments — which is what happens when you use accounting software — you work on an accrual basis.

Although the precise details of how to record sales using accounting software vary, depending on what software you use, here are some general tips to bear in mind:

Cash or credit? Some accounting software differentiates between cash sales and sales on credit, using different screens for each type of sale.

![]() How is GST calculated? With accounting software, instead of entering the dollar amount of GST, you usually enter a tax code and the software calculates GST automatically. For this reason, setting up tax codes properly is absolutely vital (refer to Chapter 7 for more about this topic). Remember that most software lets you toggle between entering transactions inclusive, or exclusive, of GST.

How is GST calculated? With accounting software, instead of entering the dollar amount of GST, you usually enter a tax code and the software calculates GST automatically. For this reason, setting up tax codes properly is absolutely vital (refer to Chapter 7 for more about this topic). Remember that most software lets you toggle between entering transactions inclusive, or exclusive, of GST.

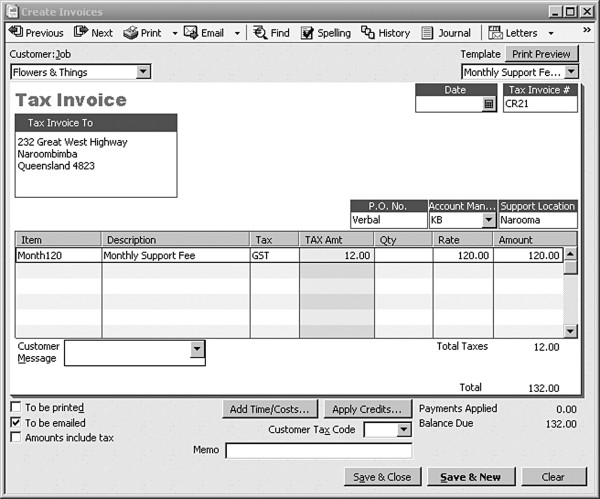

Is it best to set up items, even for services? Most accounting software lets you set up ‘items’ for billing. Items can be for services, not just products. I often set up things such as hourly rates as individual ‘items’, making for swift and accurate billing. You can see how this works in Figure 9-3.

What account do you want to allocate this sale to? I like to provide business owners with as much information about their business performance as possible, and so I like to split income into a few different categories, creating a different account for each one. For example, I split my own income into consulting income, freelance writing income and royalty income.

What’s the best layout? Spend time thinking about how you want your invoice to look, and take care to customise the layout (also sometimes called ‘forms’ or ‘templates’). Sure, your main responsibility is probably to produce a clean set of books, but the invoices that customers receive should look smart and professional.

![]() What other info do you want to include? The neat thing about accounting software is that you can record a lot of extra information about each transaction, coding transactions according to individual projects, locations, salespeople, shipping details or promised delivery date. Ask yourself, what additional info could you record about each sale that may be useful for this business?

What other info do you want to include? The neat thing about accounting software is that you can record a lot of extra information about each transaction, coding transactions according to individual projects, locations, salespeople, shipping details or promised delivery date. Ask yourself, what additional info could you record about each sale that may be useful for this business?

Figure 9-3: Entering a sale in QuickBooks.

Copyright © 2010 Intuit Inc. All rights reserved

Recording customer payments using accounting software

![]() I can’t be that specific about how to record customer payments using accounting software because I don’t know what software you’re using, but I can provide a few general tips:

I can’t be that specific about how to record customer payments using accounting software because I don’t know what software you’re using, but I can provide a few general tips:

Cultivate your inner pedant: Be careful when recording dates. If you’re imprecise about the date, you make life much harder for yourself when it comes to reconciling bank accounts later on.

Decide whether you want to batch payments together: You can usually choose between depositing customer payments into your bank account or grouping customer payments in an undeposited funds account. If you bank several payments in a batch each day, I recommend you use an undeposited funds account; otherwise, simply select the bank account into which you’ll bank this payment.

File remittance advices: When customers send remittance advices, file them carefully in date order.

Pick the payment method with precision: The method a customer chooses to pay affects when the money appears in your account. For example, EFTPOS, Visa and MasterCard transactions usually appear as a single batch the day after the transaction; cheques appear in your bank account when you slog up to the bank to deposit them; and cash may get banked or it may get spent. Diners Club and American Express appear in separate batches some days later.

![]() Play the matchmaking game with care: When you record a customer payment, you usually have to match this payment against specific invoices. Sounds easy, but sometimes a customer overpays, underpays or pays a recent invoice and forgets an older one. Sometimes the customer deducts a credit that they think you owe them, or sometimes a customer pays a totally weird amount altogether. As a bookkeeper extraordinaire, try to figure out exactly what the customer is paying and if they make a mistake, waste no time communicating with the customer to get the problem fixed.

Play the matchmaking game with care: When you record a customer payment, you usually have to match this payment against specific invoices. Sounds easy, but sometimes a customer overpays, underpays or pays a recent invoice and forgets an older one. Sometimes the customer deducts a credit that they think you owe them, or sometimes a customer pays a totally weird amount altogether. As a bookkeeper extraordinaire, try to figure out exactly what the customer is paying and if they make a mistake, waste no time communicating with the customer to get the problem fixed.

Stay alert for customer credits: With most accounting software, applying credits against invoices is a manual (rather than an automatic) process. Figure out the inner workings of the software and get on top of credits . . . before they get on top of you.

![]() Debits and credits unplugged

Debits and credits unplugged

Want to understand the debits and credits behind cash sales and credit sales? Here goes:

Imagine I make a cash sale for $100, with $10 GST. The journal behind this transaction is:

|

Debit |

Credit |

|

|

Cash at Bank GST Collected Income from Sales |

$110.00 |

$10.00 $100.00 |

Now imagine I make a credit sale for $100, with $10 GST. The journal behind this transaction is:

|

Debit |

Credit |

|

|

Accounts Receivable GST Collected Income from Sales |

$110.00 |

$10.00 $100.00 |

And then when the payment is made, the journal looks like this:

|

Debit |

Credit |

|

|

Cash at Bank |

$110.00 |

|

|

Accounts Receivable |

$110.00 |

|

Bookkeeping for Other Kinds of Income

Sometimes you receive money from sources other than your customers. Perhaps you receive a refund from a cancelled insurance policy, the bank pays you some interest or you receive a loan from Great-Aunt Thelma. You still have to record this money in your books; the burning question is, how?

Recording miscellaneous receipts

If you do books by hand, you record miscellaneous receipts in your receipts journal, mixed up with regular income from sales. You can see how this works in Figure 9-1, where I record not only sales receipts in my journal, but bank interest and a new bank loan also.

The same principle goes for a spreadsheet: You record miscellaneous receipts in the same way as you record any other income. Just be careful that you separate these receipts from regular sales using a different column, adding a comments column if necessary.

![]() With accounting software, things get a little different. With most software you record sales in a specific menu, and customer payments in another menu that’s designed specifically for matching up payments against invoices. When it comes to miscellaneous receipts, you don’t usually record these as sales, but instead as a bank deposit or supplier refund.

With accounting software, things get a little different. With most software you record sales in a specific menu, and customer payments in another menu that’s designed specifically for matching up payments against invoices. When it comes to miscellaneous receipts, you don’t usually record these as sales, but instead as a bank deposit or supplier refund.

For example, in MYOB software, you record miscellaneous receipts in the Receive Money window in the Banking command centre (whereas you record customer payments in the Receive Payments window in the Sales command centre). Similarly, with QuickBooks, the method depends on the kind of receipt: You record supplier refunds using supplier credit notes; interest is entered via cash receipts; and you record new loans via the Record Deposits menu.

Dazzling everyone with your brilliance

Whether you do your books by hand, with a spreadsheet or using accounting software, what transforms an ordinary bookkeeper into a killer bookkeeper (asides from accuracy) is the ability to choose the correct account for each transaction.

In Chapter 2, I talk about setting up your chart of accounts and customising this chart to suit your business. I can’t provide you hard-and-fast rules about what income accounts to use when allocating transactions because every business is unique, but in Table 9-1, I point out the tricky transactions which catch many a bookkeeper unaware.

|

Table 9-1 Matchmaking Receipts and Accounts |

||

|

Type of Income Payment |

Comments |

Use This Account |

|

Regular sales |

For most businesses, I recommend you allocate sales into a few different categories, depending on your business. |

Income from Service Sales; Income from Product Sales and so on |

|

Bank interest |

Always distinguish between interest income (money the bank gives you) and interest expense (money you pay the bank). |

Interest Income |

|

Dividends |

Remember to account for any imputation credits on dividends (see Chapter 14 for details). |

Dividend Income |

|

Insurance claims |

Be sure to check the GST status of any payments received from insurance claims. |

Insurance Recovery |

|

Receipt of bank loans |

Whatever you do, don’t allocate money coming in from a bank loan to income. It’s not! Create a new liability account for each new bank loan. |

Loan from Bank (liability account) |

|

Receipt of personal funds (sole trader or partnership) |

For small amounts, allocate as a credit to the Drawings account. For large amounts, create a new equity account called Owner’s Contributions or Partner’s Contributions. |

Owner’s Drawings Partner’s Drawings Owner’s Contributions Partner’s Contributions |

|

Receipt of personal funds (via a company director or shareholder) |

Allocate to a Directors’/Shareholders’ Loan account. |

Directors’/Shareholders’ Loan (liability account) |

|

Rental income |

Unless the core focus of a business concerns property investment, separate rental income from regular income so that the income doesn’t affect gross profit. |

Rental Income |

|

Sale of equipment or motor vehicles |

Ask the company accountant how best to record this transaction and check the GST status of this income (see Chapter 13 for more info). |

Sale of Assets Profit & Loss on Asset Disposal |

|

Supplier refunds |

Allocate the supplier refund against whatever expense account you allocated the original payment to. |

Purchases Insurance Expense Telephone Expense |

|

Tax refunds |

For sole traders or partnerships, allocate to a Drawings account. For companies, allocate to Provision for Company Tax. |

Owner’s Drawings Partner’s Drawings Provision for Company Tax |

![]() If you get a bank loan, that’s not income. If your secret lover has a heart attack and leaves you everything in the final will, that’s not income. If you deposit your life’s savings into your new entrepreneurial venture exporting sheep to New Zealand (oh no, please don’t), that’s not income. Income is only income when you earn it. Simple as that.

If you get a bank loan, that’s not income. If your secret lover has a heart attack and leaves you everything in the final will, that’s not income. If you deposit your life’s savings into your new entrepreneurial venture exporting sheep to New Zealand (oh no, please don’t), that’s not income. Income is only income when you earn it. Simple as that.

Keeping Track of Who Owes You What

One of the most important parts of a bookkeeper’s job is to keep track of how much customers owe the business. I talk more about the art of debt collection in Chapter 20, but in this chapter I focus on how to generate a report showing how much customers owe you.

All accounting software includes as standard an Aged Receivables report, a report that lists how much each customer owes, sorted in columns according to how old the debt is. Figure 9-4 shows a typical report.

Figure 9-4: An Aged Receivables report shows how much customers owe you.

Copyright © 2010 Intuit Inc. All rights reserved

Keep this report sweet by taking a few tips on board:

As your business grows, review your Aged Receivables report every week. Make sure that the percentage of accounts that are overdue doesn’t increase month after month, and don’t wait until you’re already strapped for cash before asking customers to cough up.

![]() As a conscientious bookkeeper, if amounts appear on this report that you don’t understand — for example, a customer shows as owing money but you’re positive they paid — then figure out why the report is wrong, and fix it!

As a conscientious bookkeeper, if amounts appear on this report that you don’t understand — for example, a customer shows as owing money but you’re positive they paid — then figure out why the report is wrong, and fix it!

With most software, you can double-click on any amount to see the individual invoices that make up a customer’s debt, or you can print a detailed Aged Receivables report that lists every invoice outstanding, sorted by customer.

![]() The older an account is, the less likely the customer is to pay. So beware!

The older an account is, the less likely the customer is to pay. So beware!

If you bill customers weekly or fortnightly, you’re best to see whether you can modify this report to specify either 7 or 14 days as the number of days per ageing period.

Dealing with Tricky Situations

If only life were as easy as graduating from high school, finding a gorgeous partner, bringing a few children into the world and living happily ever after. No getting expelled, getting divorced, getting sacked or getting sick. And if only bookkeeping were as simple as recording a few sales, matching up a few payments and printing up some insightful reports. No yucky sales returns, weird discounts, miscellaneous credits or unexpected bad debts.

Sadly, bookkeeping — like life — throws you a few googlies, so the rest of this chapter focuses on dealing with odd bookkeeping problems that come your way.

Dishing out discounts

Some businesses offer discounts for prompt payment. You know the kind of thing: Pay within 14 days and you get 5 per cent discount. Sounds fine, but how do you do the books?

![]() If you use accounting software, you can usually allocate the discount at the time you receive the payment, by entering this amount into a discount column. For example, in Figure 9-5, I show a payment for $104.50 with a discount of $5.50, settling an invoice for $110. I’m using MYOB software in this example, but most other software works in a similar way.

If you use accounting software, you can usually allocate the discount at the time you receive the payment, by entering this amount into a discount column. For example, in Figure 9-5, I show a payment for $104.50 with a discount of $5.50, settling an invoice for $110. I’m using MYOB software in this example, but most other software works in a similar way.

Figure 9-5: Applying settlement discounts to invoices.

![]() Be careful that you — or your accounting software — calculate GST on settlement discounts correctly. For example, if an invoice is for $110 with a 5 per cent discount, the discount is worth $5.50. If this invoice includes 10 per cent GST, then this $5.50 includes 50 cents of GST. However, if an invoice is a combination of taxable and non-taxable goods (something that often happens in Australia, but never happens in New Zealand), GST applies to the discount in the same proportions as GST applies to the original invoice. For example, if this $110 invoice includes 10 per cent GST on $25 worth of items only and you offer a 5 per cent discount, the discount is still $5.50, but the GST on this discount is only 11 cents.

Be careful that you — or your accounting software — calculate GST on settlement discounts correctly. For example, if an invoice is for $110 with a 5 per cent discount, the discount is worth $5.50. If this invoice includes 10 per cent GST, then this $5.50 includes 50 cents of GST. However, if an invoice is a combination of taxable and non-taxable goods (something that often happens in Australia, but never happens in New Zealand), GST applies to the discount in the same proportions as GST applies to the original invoice. For example, if this $110 invoice includes 10 per cent GST on $25 worth of items only and you offer a 5 per cent discount, the discount is still $5.50, but the GST on this discount is only 11 cents.

By the way, the jury is out about the best account to choose for settlement discounts. Some accountants like to have a contra income account called ‘Less Settlement Discounts’ (a contra account is an account which offsets another account). Other accountants prefer to create a new cost of sales or expense account called ‘Discounts Given’. I don’t mind which way the cake gets cut, but I do suggest you ask the company accountant what they prefer.

Giving credits or refunds

Bookkeeping for customer credits or refunds is a tricky business, and the correct procedure depends on what kind of books you keep. Here are some general tips to help you find your way:

If you do your books on a cash basis, only recording sales when you receive payments from customers, then you don’t have to change anything in your receipts journal.

![]() If you use accounting software, you usually raise a credit note either by recording a minus sale (the MYOB strategy) or going to a special menu for creating adjustment notes and credit notes (the QuickBooks strategy).

If you use accounting software, you usually raise a credit note either by recording a minus sale (the MYOB strategy) or going to a special menu for creating adjustment notes and credit notes (the QuickBooks strategy).

An adjustment note is just a fancy word for credit note.

![]() Don’t ever allocate refunds to an expense account called Refunds (something I’ve seen happen more often than I care to remember). Always allocate refunds to whatever income account the original sale went to. For example, if a pet shop makes a sale and allocates this income to Puppy Dog Sales, and then the puppy dog behaves like a wild child (biting my toes as my puppy is doing as I write this very paragraph) and the owner takes it back to the pet shop and gets a refund (I promise I won’t), then the pet shop’s bookkeeper allocates this refund as a debit against Puppy Dog Sales.

Don’t ever allocate refunds to an expense account called Refunds (something I’ve seen happen more often than I care to remember). Always allocate refunds to whatever income account the original sale went to. For example, if a pet shop makes a sale and allocates this income to Puppy Dog Sales, and then the puppy dog behaves like a wild child (biting my toes as my puppy is doing as I write this very paragraph) and the owner takes it back to the pet shop and gets a refund (I promise I won’t), then the pet shop’s bookkeeper allocates this refund as a debit against Puppy Dog Sales.

If you use accounting software, make sure you use the correct command to record customer refunds (usually hidden away in the deepest, darkest reaches of the software), and don’t record refunds using the regular spend money, pay money or write cheques commands. Why? Because the refund needs to be matched against the customer credit, otherwise the credit stays sitting on the customer’s account forever.

Writing off bad debts

Writing off a bad debt, although an extremely sad and regretful event, is not rocket science. Although the precise mechanics vary depending on what accounting software you use, the essential principle is that you generate a credit note for this customer (using whatever procedure you normally use to generate credit notes) but instead of allocating this credit to an income account, you allocate this credit to an expense account called Bad Debt Expense.

In accounting software where every sale requires an ‘item’ (such as QuickBooks), create a new sales item that links to Bad Debt Expense.

If you’re doing books by hand and you only write up income as you receive payments, you don’t need to record bad debts in your books because, guess what? That payment ain’t never going to arrive.

![]() Be mindful of GST on this transaction: If the original sale included GST, then the credit note allocated to Bad Debt Expense needs to include GST also.

Be mindful of GST on this transaction: If the original sale included GST, then the credit note allocated to Bad Debt Expense needs to include GST also.

Include a memo on the credit note that refers to the original invoice number and write a brief description of why you’re writing off this debt.

Avoid using the discount feature as a way to write off a bad debt (a method sometimes recommended in software user guides). You want to report for this expense correctly as a bad debt in the Profit & Loss report, which is quite different from reporting this expense as a discount.

![]() Never simply delete the original invoice. A complete set of books maintains a record of both the original sale and the write-off.

Never simply delete the original invoice. A complete set of books maintains a record of both the original sale and the write-off.

Add a warning to the customer’s record, maybe adding the words ‘Do Not Use’ to the end of the customer’s name and setting their credit limit to 10 cents (it’s often unwise to set the credit limit to zero, as the software interprets this as meaning there is no credit limit). This way, salespeople won’t accidentally make another sale to this customer in the future. Alternatively, some software lets you put customers on ‘Stop Credit’, preventing operators from recording sales to that customer.

If your chart of accounts includes a balance in a Provision for Doubtful Debts account (this scenario usually only crops up with larger businesses) and this account has a balance that isn’t zero, ask the company accountant whether you should allocate the bad debt to Bad Debt Expense or Provision for Doubtful Debts.

![]() You can’t claim a bad debt as a tax deduction unless you have already declared the original invoice as income.

You can’t claim a bad debt as a tax deduction unless you have already declared the original invoice as income.