Chapter 5

The Remarkable Notions of the Remarkable Notions Man

We all have to make decisions on the basis of limited data. One sip, even a sniff, of wine determines whether the whole bottle is drinkable. Courtship with a future spouse is shorter than the lifetime that lies ahead. A few drops of blood may evidence patterns of DNA that will either convict or acquit an accused murderer. Public-opinion pollsters interview 2,000 people to ascertain the entire nation’s state of mind. The Dow Jones Industrial Average consists of just thirty stocks, but we use it to measure changes in trillions of dollars of wealth owned by millions of families and thousands of major financial institutions. George Bush needed just a few bites of broccoli to decide that that stuff was not for him.

Most critical decisions would be impossible without sampling. By the time you have drunk a whole bottle of wine, it is a little late to announce that it is or is not drinkable. The doctor cannot draw all your blood before deciding what medicine to prescribe or before checking out your DNA. The president cannot take referendums of 100% of all the voters every month before deciding what the electorate wants—nor can he eat all the broccoli in the world before expressing his distaste for it.

Sampling is essential to risk-taking. We constantly use samples of the present and the past to guess about the future. “On the average” is a familiar phrase. But how reliable is the average to which we refer? How representative is the sample on which we base our judgment? What is “normal,” anyway? Statisticians joke about the man with his feet in the oven and his head in the refrigerator: on the average he feels pretty good. The fable about the blind men and the elephant is famous precisely because each man had taken such a tiny sample of the entire animal.

![]()

Statistical sampling has had a long history, and twentieth-century techniques are far advanced over the primitive methods of earlier times. The most interesting early use of sampling was conducted by the King of England, or by his appointed proxies, in a ceremony known as the Trial of the Pyx and was well established by 1279 when Edward I proclaimed the procedure to be followed.1

The purpose of the trial was to assure that the coinage minted by the Royal Mint met the standards of gold or silver content as defined by the Mint’s statement of standards. The strange word “pyx” derives from the Greek word for box and refers to the container that held the coins that were to be sampled. Those coins were selected, presumably at random, from the output of the Mint; at the trial, they would be compared to a plate of the King’s gold that had been stored in a thrice-locked treasury room called the Chapel of the Pyx in Westminster Abbey. The procedure permitted a specifically defined variance from the standard, as not every coin could be expected to match precisely the gold to which it was being compared.

A more ambitious and influential effort to use the statistical process of sampling was reported in 1662, eight years after the correspondence between Pascal and Fermat (and the year in which Pascal finally discovered for himself whether God is or God is not). The work in question was a small book published in London and titled Natural and Political Observations made upon the Bills Of Mortality. The book contained a compilation of births and deaths in London from 1604 to 1661, along with an extended commentary interpreting the data. In the annals of statistical and sociological research, this little book was a stunning breakthrough, a daring leap into the use of sampling methods and the calculation of probabilities—the raw material of every method of risk management, from insurance and the measurement of environmental risks to the design of the most complex derivatives.

The author, John Graunt, was neither a statistician nor a demographer—at that point there was no such thing as either.2 Nor was he a mathematician, an actuary, a scientist, a university don, or a politician. Graunt, then 42 years old, had spent his entire adult life as a merchant of “notions,” such as buttons and needles.

Graunt must have been a keen businessman. He made enough money to be able to pursue interests less mundane than purveying merchandise that holds clothing together. According to John Aubrey, a contemporary biographer, Graunt was “a very ingenious and studious person . . . [who] rose early in the morning to his Study before shop-time . . . . [V]ery facetious and fluent in his conversation.”3 He became close friends with some of the most distinguished intellectuals of his age, including William Petty, who helped Graunt with some of the complexities of his work with the population statistics.

Petty was a remarkable man. Originally a physician, his career included service as Surveyor of Ireland and Professor of Anatomy and Music. He accumulated a substantial fortune as a profiteer during the wars in Ireland and was the author of a book called Political Arithmetic!?, which has earned him the title of founder of modern economics.4

Graunt’s book went through at least five editions and attracted a following outside as well as inside England. Petty’s review in the Parisian Journal des Sçavans in 1666 inspired the French to undertake a similar survey in 1667. And Graunt’s achievements attracted sufficient public notice for Charles II to propose him for membership in the newly formed Royal Society. The members of the Society were not exactly enthusiastic over the prospect of admitting a mere tradesman, but the King advised them that, “if they found any more such Tradesmen, they should be sure to admit them all, without any more ado.” Graunt made the grade.

The Royal Society owes its origins to a man named John Wilkins (1617–1672), who had formed a select club of brilliant acquaintances that met in his rooms in Wadham College.5 The club was a clone of Abbé Mersenne’s group in Paris. Wilkins subsequently transformed these informal meetings into the first, and the most distinguished, of the scientific academies that were launched toward the end of the seventeenth century; the French Académie des Sciences was founded shortly after, with the Royal Society as its model.

Wilkins later became Bishop of Chichester, but he is more interesting as an early author of science fiction embellished with references to probability. One of his works carried the entrancing tide of The Discovery of a World in the Moone or a discourse tending to prove that ’tis probable there may be another habitable world in that planet, published in 1640. Anticipating Jules Verne, Wilkins also worked on designs for a submarine to be sent under the Arctic Ocean.

![]()

We do not know what inspired Graunt to undertake his compilation of births and deaths in London, but he admits to having found “much pleasure in deducing so many abstruse, and unexpected inferences out of these poor despised Bills of Mortality . . . . And there is pleasure in doing something new, though never so little.”6 But he had a serious objective, too: “[T]o know how many people there be of each Sex, State, Age, Religious, Trade, Rank, or Degree, &c. by the knowing whereof Trade and Government may be made more certain, and Regular; for, if men know the People as aforesaid, they might know the consumption they would make, so as Trade might not be hoped for where it is impossible.”7 He may very well have invented the concept of market research, and he surely gave the government its first estimate of the number of people available for military service.

Information about births and deaths had long been available in parish churches, and the City of London itself had started keeping weekly tallies from 1603 onward. Additional data were available in Holland, where the towns were financing themselves with life annuities—policies purchased for a lump sum that would pay an income for life to the owner of the policy, and occasionally to survivors. Churches in France also kept records of christenings and deaths.

Hacking reports that Graunt and Petty had no knowledge of Pascal or Huygens, but, “Whether motivated by God, or by gaming, or by commerce, or by the law, the same kind of ideas emerged simultaneously in many minds.”8 Clearly Graunt had chosen a propitious moment for publishing and analyzing important information about the population of England.

Graunt was hardly aware that he was the innovator of sampling theory. In fact, he worked with the complete set of the bills of mortality rather than with a sample. But he reasoned systematically about raw data in ways that no one had ever tried before. The manner in which he analyzed the data laid the foundation for the science of statistics.9 The word “statistics” is derived from the analysis of quantitative facts about the state. Graunt and Petty may be considered the co-fathers of this important field of study.

Graunt did his work at a time when the primarily agricultural society of England was being transformed into an increasingly sophisticated society with possessions and business ventures across the seas. Hacking points out that so long as taxation was based on land and tillage nobody much cared about how many people there were. For example, William the Conqueror’s survey known as the Domesday Book of 1085 included cadasters—registers of ownership and value of real property—but paid no heed to the number of human beings involved.

As more and more people came to live in towns and cities, however, headcounts began to matter. Petty mentions the importance of population statistics in estimating the number of men of military age and the potential for tax revenues. But for Graunt, who appears to have been a tradesman first, at a time of rising prosperity, political considerations were of less interest.

There was another factor at work. Two years before the publication of Graunt’s Observations, Charles II had been recalled from exile in Holland. With the Restoration in full sway, the English were finally rid of the intellectual repression that the Puritans had imposed on the nation. The death of absolutism and Republicanism led to a new sense of freedom and progress throughout the country. Great wealth was beginning to arrive from the colonies across the Atlantic and from Africa and Asia as well. Isaac Newton, now 28 years old, was leading people to think in new ways about the planet on which they lived. Charles II himself was a free soul, a Merry Monarch who offered no apologies for enjoying the good things of life.

It was time to stand up and look around. John Graunt did, and began counting.

![]()

Although Graunt’s book offers interesting bits for students of sociology, medicine, political science, and history, its greatest novelty is in its use of sampling. Graunt realized that the statistics available to him represented only a fraction of all the births and deaths that had ever occurred in London, but that failed to deter him from drawing broad conclusions from what he had. His line of analysis is known today as “statistical inference”—inferring a global estimate from a sample of data; subsequent statisticans would figure out how to calculate the probable error between the estimate and the true values. With his ground-breaking effort, Graunt transformed the simple process of gathering information into a powerful, complex instrument for interpreting the world—and the skies—around us.

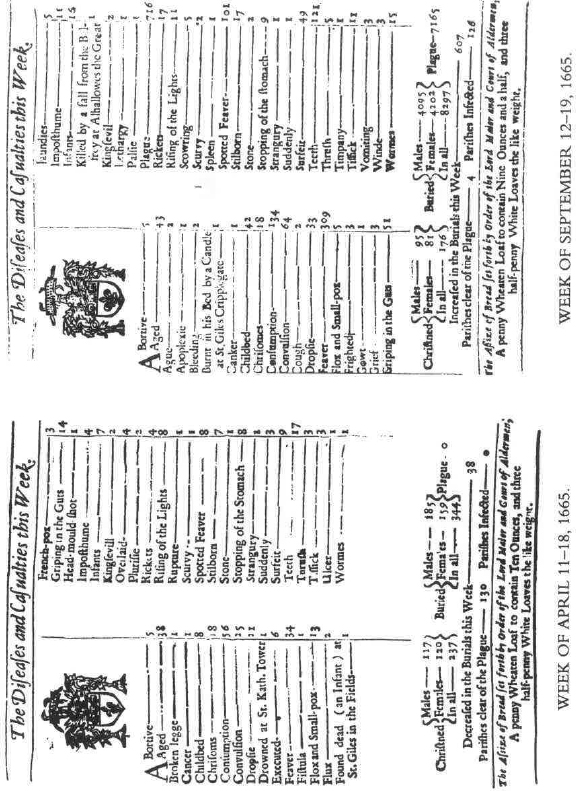

The raw material that Graunt gathered was contained in “Bills of Mortality” that the City of London had started collecting in 1603. That was only incidentally the year in which Queen Elizabeth died; it was also the year in which London suffered one of the worst infestations of the plague. Accurate knowledge of what was going on in the field of public health was becoming increasingly important.10

The bills of mortality revealed the causes of death as well as the number of deaths and also listed the number of children christened each week. The accompanying illustration shows the documents for two weeks in the year 1665.a There were 7,165 deaths from plague in just the one week of September 12–19, and only four of 130 parishes were free of the disease.11

Graunt was particularly interested in the causes of death, especially “that extraordinary and grand Casualty” the plague, and in the way people lived under the constant threat of devastating epidemic. For the year 1632, for example, he listed nearly sixty different causes of death, with 628 deaths coming under the heading of “aged.” The others range from “affrighted” and “bit with mad dog” (one each) to “worms,” “quinsie,” and “starved at nurse.” There were only seven “murthers” in 1632 and just 15 suicides.

(Reproduction courtesy of Stephen Stigler.)

In observing that “but few are Murthered . . . whereas in Paris few nights came without their Tragedie,” Graunt credits the government and the citizen guard of the City of London. He also credits “the natural, and customary, abhorrence of that inhumane Crime, and all Bloodshed by most Englishmen,” remarking that even “Usurpers” during English revolutions executed only a few of their countrymen.

Graunt gives the number of deaths from plague for certain years; one of the worst was in 1603, when 82% of the burials were of plague victims. From 1604 to 1624, he calculated that 229,250 people had died of all diseases and “casualties,” about a third of which were from children’s diseases. Figuring that children accounted for half the deaths from other diseases, he concluded that “about thirty six per centum of all quick conceptions died before six years old.” Fewer than 4,000 died of “outward Griefs, as of Cancers, Fistulaes, Sores, Ulcers, broken and bruised Limbs, Impostumes, King’s evil, Loprosie, Scald-head, Swinepox, Wens, &c.”

Graunt suggests that the prevalence of acute and epidemical diseases might give “a measure of the state, and disposition of this Climate, and Air . . . as well as its food.” He goes on to observe that few are starved, and that the beggars, “swarming up and down upon this City . . . seem to be most of them healthy and strong.” He recommends that the state “keep” them and that they be taught to work “each according to his condition and capacity.”

After commenting on the incidence of accidents—most of which he asserts are occupation-related—Graunt refers to “one Casualty in our Bills, of which though there be daily talk, [but] little effect.” This casualty is the French-Pox—a kind of syphilis—”gotten for the most part, not so much by the intemperate use of Venery (which rather causes the Gowt) as of many common Women.”b Graunt wonders why the records show that so few died of it, as “a great part of men have, at one time or another, had some species of this disease.” He concludes that most of the deaths from ulcers and sores were in fact caused by venereal disease, the recorded diagnoses serving as euphemisms. According to Graunt, a person had to be pretty far gone before the authorities acknowledged the true cause of death: “onely hated persons, and such, whose very Noses were eaten of, were reported . . . to have died of this too frequent Maladie.”

Although the bills of mortality provided a rich body of facts, Graunt was well aware of the shortcomings in the data he was working with. Medical diagnosis was uncertain: “For the wisest person in the parish would be able to find out very few distempers from a bare inspection of the dead body,” Graunt warned. Moreover, only Church of England christenings were tabulated, which meant that Dissenters and Catholics were excluded.

![]()

Graunt’s accomplishment was truly impressive. As he put it himself, having found “some Truths, and not commonly believed Opinions, to arise from my Meditations upon these neglected Papers, I proceeded further, to consider what benefit the knowledge of the same would bring to the world.” His analysis included a record of the varying incidence of different diseases from year to year, movements of population in and out of London “in times of fever,” and the ratio of males to females.

Among his more ambitious efforts, Graunt made the first reasoned estimate of the population of London and pointed out the importance of demographic data for determining whether London’s population was rising or falling and whether it “be grown big enough, or too big.” He also recognized that an estimate of the total population would help to reveal the likelihood that any individual might succumb to the plague. And he tried several estimating methods in order to check on the reliability of his results.

One of his methods began with the assumption that the number of fertile women was double the number of births, as “such women . . . have scarce more than one child in two years.”12 On average, yearly burials were running about 13,000—about the same as the annual non-plague deaths each year. Noting that births were usually fewer in number than burials, he arbitrarily picked 12,000 as the average number of births, which in turn indicated that there were 24,000 “teeming women.” He estimated “family” members, including servants and lodgers, at eight per household, and he estimated that the total number of households was about twice the number of households containing a woman of child-bearing age. Thus, eight members of 48,000 families yielded an estimated 384,000 people for the total population of London. This figure may be too low, but it was probably closer to the mark than the common assumption at the time that two million people were living in London.

Another of Graunt’s methods began with an examination of a 1658 map of London and a guess that 54 families lived in each 100 square yards—about 200 persons per acre. That assumption produced an estimate of 11,880 families living within London’s walls. The bills of mortality showed that 3,200 of the 13,000 deaths occurred within the walls, a ratio of 1:4. Four times 11,880 produces an estimate of 47,520 families. Might Graunt have been figuring backwards from the estimate produced by his first method? We will never know.

![]()

Graunt does not use the word “probability” at any point, but he was apparently well aware of the concept. By coincidence, he echoed the comment in the Port-Royal Logic about abnormal fears of thunderstorms:

Whereas many persons live in great fear and apprehension of some of the more formidable and notorious diseases, I shall set down how many died of each: that the respective numbers, being compared with the total 229,520 [the mortality over twenty years], those persons may the better understand the hazard they are in.

Elsewhere he comments, “Considering that it is esteemed an even lay, whether any man lives ten years longer, I supposed it was the same, that one of any ten might die within one year.”13 No one had ever proposed this problem in this fashion, as a case in probability. Having promised “succinct paragraphs, without any long series of multiloquious deductions,” Graunt does not elaborate on his reasoning. But his purpose here was strikingly original. He was attempting to estimate average expected ages at death, data that the bills of mortality did not provide.

Using his assessment that “about thirty six per centum of all quick conceptions died before six years old” and a guess that most people die before 75, Graunt created a table showing the number of survivors from ages 6 to 76 out of a group of 100; for purposes of comparison, the right-hand column of the accompanying table shows the data for the United States as of 1993 for the same age levels.

| Age | Graunt | 1993 |

| 0 | 100 | 100 |

| 6 | 64 | 99 |

| 16 | 40 | 99 |

| 26 | 25 | 98 |

| 36 | 16 | 97 |

| 46 | 10 | 95 |

| 56 | 6 | 92 |

| 66 | 3 | 84 |

| 76 | 1 | 70 |

Sources: For Graunt, Hacking, 1975, p. 108; for 1993, “This Is Your Life Table,” American Demographics, February 1995, p. 1.

No one is quite sure how Graunt concocted his table, but his estimates circulated widely and ultimately turned out to be good guesses. They provided an inspiration for Petty’s insistence that the government set up a central statistical office.

Petty himself took a shot at estimating average life expectancy at birth, though complaining that “I have had only a common knife and a clout, instead of the many more helps which such a work requires.”14 Using the word “likelihood” without any apparent need to explain what he was talking about, Petty based his estimate on the information for a single parish in Ireland. In 1674, he reported to the Royal Society that life expectancy at birth was 18; Graunt’s estimate had been 16.15

The facts Graunt assembled changed people’s perceptions of what the country they lived in was really like. In the process, he set forth the agenda for research into the country’s social problems and what could be done to make things better.

Graunt’s pioneering work suggested the key theoretical concepts that are needed for making decisions under conditions of uncertainty. Sampling, averages, and notions of what is normal make up the structure that would in time house the science of statistical analysis, putting information into the service of decision-making and influencing the degrees of belief we hold about the probabilities of future events.

![]()

Some thirty years after the publication of Graunt’s Natural and Political Observations, another work appeared that was similar to Graunt’s but even more important to the history of risk management. The author of this work, Edmund Halley, was a scientist of high repute who was familiar with Graunt’s work and was able to carry his analysis further. Without Graunt’s first effort, however, the idea of such a study might never have occurred to Halley.

Although Halley was English, the data he used came from the Silesian town of Breslau—Breslaw, as it was spelled in those days—located in the easternmost part of Germany; since the Second World War the town has been part of Poland and is now known as Wrozlaw. The town fathers of Breslaw had a long-standing practice of keeping a meticulous record of annual births and deaths.

In 1690 a local scientist and clergyman named Caspar Naumann went through the Breslaw records with a view to “disproving certain current superstitions with regard to the effect of the phases of the moon and the so-called ‘climacteric’ years on health.” Naumann sent the results of his study to Leibniz, who in turn sent them on to the Royal Society in London.16

Naumann’s data soon attracted the attention of Halley. Halley was then only 35 years old but already one of England’s most distinguished astronomers. Indeed, he was responsible for persuading Isaac Newton in 1684 to publish his Principia, the work in which Newton first set forth the laws of gravity. Halley paid all the costs of publication out of his own modest resources, corrected the page proofs, and put his own work aside until the job was done. The historian James Newman conjectures that the Principia might never have appeared without Halley’s efforts.

Widely recognized as a child genius in astronomy, Halley carried his 24-inch telescope with him when he arrived as an undergraduate at Queen’s College, Oxford. He left Oxford without receiving a degree, however, and set off to study the heavens in the southern hemisphere; the results of that study established his reputation before he was even 20 years old. By the age of 22, he was already a member of the Royal Society. Oxford turned him down for a professorship in 1691 because he held “materialistic views” that did not match the religious orthodoxy of Oxford. But the dons relented in 1703 and gave him the job. In 1721, he became Royal Astronomer at Greenwich. Meanwhile, he had received his degree by the King’s command.

Halley would live to the age of 86. He appears to have been a jolly man, with an “uncommon degree of sprightliness and vivacity,” and had many warm friendships that included Peter the Great of Russia. In 1705, in his pathbreaking work on the orbits of comets, Halley identified a total of 24 comets that had appeared between the years 1337 and 1698. Three seemed to be so similar that he concluded that all three were a single comet that had appeared in 1531, 1607, and 1682. Observations of this comet had been reported as far back as 240 BC. Halley’s prediction that the comet would reappear in 1758 electrified the world when the comet arrived right on schedule. Halley’s name is celebrated every 76 years as his comet sweeps across the skies.

The Breslaw records were not exactly in Halley’s main line of work, but he had promised the Royal Society a series of papers for its newly established scholarly journal, Transactions, and he had been scouting around for something unusual to write about. He was aware of certain flaws in Graunt’s work, flaws that Graunt himself had acknowledged, and he decided to take the occasion to prepare a paper for Transactions on the Breslaw data by trying his hand at the analysis of social rather than heavenly statistics for a change.

Graunt, lacking any reliable figure for the total population of London, had had to estimate it on the basis of fragmentary information. He had numbers and causes of deaths but lacked complete records of the ages at which people had died. Given the constant movement of people into and out of London over the years, the reliability of Graunt’s estimate was now open to question.

The data delivered by Leibniz to the Royal Society contained monthly data for Breslaw for the years 1687 through 1691, “seeming to be done,” according to Halley, “with all the Exactness and Sincerity possible”; the data included age and sex for all deaths and the number of births each year. Breslaw, he pointed out, was far from the sea, so that the “Confluence of Strangers is but small.” Births exceeded the “Funerals” by only a small amount and the population was much more stable than London’s. All that was lacking was a number for the total population. Halley was convinced that the figures for mortality and birth were sufficiently accurate for him to come up with a reliable estimate of the total.

He found an average of 1,238 births and 1,174 deaths a year over the five-year period, for an annual excess of about 64, which number, he surmised, “may perhaps be balanced by the Levies for the Emperor’s Service in his Wars.” Directing his attention to the 1,238 annual births and examining the age distribution of those who died, Halley calculated that “but 692 of the Persons born do survive Six whole Years,” a much smaller proportion than Graunt’s estimate that 64% of all births survived beyond six years. About a dozen of the deaths in Breslaw, on the other hand, occurred between the ages of 81 and 100. Combining a variety of estimates of the percentage of each age group who die each year, Halley worked back from the age distribution of the people dying annually to a grand estimate of 34,000 for the town’s total population.

The next step was to devise a table breaking down the population into an age distribution, “from birth to extream Old Age.” This table, Halley asserts, offered manifold uses and gave “a more just Idea of the State and condition of Mankind, than any thing yet extant that I know of.” For example, the table provided useful information on how many men were of the right age for military service—9,000—and Halley suggested that this estimate of 9/34ths of the population could “pass for a Rule for other places.”

Halley’s entire analysis embodies the concept of probability and ultimately moves into risk management. Halley demonstrates that his table “shews the odds” that a “Party” of any given age “does not die in a Year.” As an illustration, he offers the 25-year age group, which numbered 567, while the 26-year age group numbered 560. The difference of only 7 between the two age groups meant that the probability that a 25-year-old would die in any one year was 7/567, or odds of 80-to-l that a 25-year-old would make it to 26. Using the same procedure of subtraction between a later age and a given age, and taking the given age as the base, the table could also show the odds that a man of 40 would live to 47; the answer in this instance worked out to odds of 5 1/2-to-l.

Halley carried the analysis further: “[I]f it be enquired at what number Years, it is an even Lay that a Person of any Age shall die, this Table readily performs it.” For instance, there were 531 people aged 30, and half that number is 265. One could then look through the table for the age group numbering 265, which appeared to be between 57 and 58. Hence, it would be “an even Wager that. . . a Man of 30 may reasonably expect to live between 27 and 28 years.”

The next level of Halley’s analysis was the most important of all. The table could be used to reckon the price of insuring lives at different ages, “it being 100 to 1 that a man of 20 dies not in a year, and but 38 to 1 for a Man of 50 Years of Age.” On the basis of the odds of dying in each year, the table furnished the necessary information for calculating the value of annuities. At this point Halley launches into a detailed mathematical analysis of the valuation of annuities, including annuities covering two and three lives as well as one. He offers at the same time to provide a table of logarithms to reduce the “Vulgar Arithmetick” imposed by the mass of necessary calculations.

This was a piece of work that was long overdue. The first record we have of the concept of annuities dates back to 225 AD, when an authoritative set of tables of life expectancies was developed by a leading Roman jurist named Ulpian. Ulpian’s tables were the last word for over 1400 years!

Halley’s work subsequently inspired important efforts in calculating life expectancies on the Continent, but his own government paid no attention to his life tables at the time. Taking their cue from the Dutch use of annuities as a financing device, the English government had attempted to raise a million pounds by selling annuities that would pay back the original purchase price to the buyer over a period of 14 years—but the contract was the same for everyone, regardless of their age! The result was an extremely costly piece of finance for the government. Yet the policy of selling annuities at the same price to everyone continued in England until 1789. The assumption that the average life expectancy at birth was about 14 years was at least an improvement over earlier assumptions: in 1540, the English government had sold annuities that repaid their purchase price in seven years without regard to the age of the buyer.17

After the publication of Halley’s life tables in Transactions in 1693, a century would pass before governments and insurance companies would take probability-based life expectancies into account. Like his comet, Halley’s tables turned out to be more than a flash in the sky that appears once in a lifetime: his manipulation of simple numbers formed the basis on which the life-insurance industry built up the data base it uses today.

![]()

One afternoon in 1637, when Graunt was just seventeen years old and Halley had not yet been born, a Cretan scholar named Canopius sat down in his chambers at Balliol College, Oxford, and made himself a cup of strong coffee. Canopius’s brew is believed to mark the first time coffee was drunk in-England; it proved so popular when it was offered to the public that hundreds of coffee houses were soon in operation all over London.

What does Canopius’s coffee have to do with Graunt or Halley or with the concept of risk? Simply that a coffee house was the birthplace of Lloyd’s of London, which for more than two centuries was the most famous of all insurance companies.18 Insurance is a business that is totally dependent on the process of sampling, averages, independence of observations, and the notion of normal that motivated Graunt’s research into London’s population and Halley’s into Breslaw’s. The rapid development of the insurance business at about the time Graunt and Halley published their research is no coincidence. It was a sign of the times, when innovations in business and finance were flourishing.

The English word for stockbroker—stock jobber—first appeared around 1688, a hundred years before people started trading stocks around the Buttonwood tree on Wall Street, New York. Corporations of all kinds suddenly appeared on the scene, many with curious names like the Lute-String Company, the Tapestry Company, and the Diving Company. There was even a Royal Academies Company that promised to hire the greatest scholars of the age to teach the 2,000 winners of a huge lottery a subject of their own choosing.

The second half of the seventeenth century was also an era of burgeoning trade. The Dutch were the predominant commercial power of the time, and England was their main rival. Ships arrived daily from colonies and suppliers around the globe to unload a profusion of products that had once been scarce or unknown luxuries—sugar and spice, coffee and tea, raw cotton and fine porcelain. Wealth was no longer something that had to be inherited from preceding generations: now it could be earned, discovered, accumulated, invested—and protected from loss.

Moreover, toward the end of the century the English had to finance the sequence of costly wars with the French that had begun with Louis XIV’s abortive invasion of England in May 1692 and ended with the English victory at Blenheim and the signing of the Treaty of Utrecht in 1713. On December 15, 1693, the House of Commons established the English national debt with the issue of the million pounds of annuities mentioned above. In 1849, Thomas Babington Macaulay, the great English historian, characterized that momentous event with these resounding words: “Such was the origin of that debt which has since become the greatest prodigy that ever perplexed the sagacity and confounded the pride of statesmen and philosophers.”19

This was a time for London to take stock of itself and its role in the world. It was also a time to apply the techniques of financial sophistication demanded by war, a rapidly growing wealthy class, and rising overseas trade. Information from remote areas of the world was now of crucial importance to the domestic economy. With the volume of shipping constantly expanding, there was a lively demand for current information with which to estimate sailing times between destinations, weather patterns, and the risks lurking in unfamiliar seas.

In the absence of mass media, the coffee houses emerged as the primary source of news and rumor. In 1675, Charles II, suspicious as many rulers are of places where the public trades information, shut the coffee houses down, but the uproar was so great that he had to reverse himself sixteen days later. Samuel Pepys frequented a coffee house to get news of the arrival of ships he was interested in; he deemed the news he received there to be more reliable than what he learned at his job at the Admiralty.

The coffee house that Edward Lloyd opened in 1687 near the Thames on Tower Street was a favorite haunt of men from the ships that moored at London’s docks. The house was “spacious . . . well-built and inhabited by able tradesmen,” according to a contemporary publication. It grew so popular that in 1691 Lloyd moved it to much larger and more luxurious quarters on Lombard Street. Nat Ward, a publican whom Alexander Pope accused of trading vile rhymes for tobacco, reported that the tables in the new house were “very Neat and shined with Rubbing.” A staff of five served tea and sherbet as well as coffee.

Lloyd had grown up under Oliver Cromwell and he had lived through plague, fire, the Dutch invasion up the Thames in 1667, and the Glorious Revolution of 1688. He was a lot more than a skilled coffee-house host. Recognizing the value of his customer base and responding to the insistent demand for information, he launched “Lloyd’s List” in 1696 and filled it with information on the arrivals and departures of ships and intelligence on conditions abroad and at sea. That information was provided by a network of correspondents in major ports on the Continent and in England. Ship auctions took place regularly on the premises, and Lloyd obligingly furnished the paper and ink needed to record the transactions. One corner was reserved for ships’ captains where they could compare notes on the hazards of all the new routes that were opening up—routes that led them farther east, farther south, and farther west than ever before. Lloyd’s establishment was open almost around the clock and was always crowded.

Then as now, anyone who was seeking insurance would go to a broker, who would then hawk the risk to the individual risk-takers who gathered in the coffee houses or in the precincts of the Royal Exchange. When a deal was closed, the risk-taker would confirm his agreement to cover the loss in return for a specified premium by writing his name under the terms of the contract; soon these one-man insurance operators came to be known as “underwriters.”

The gambling spirit of that prosperous era fostered rapid innovation in the London insurance industry. Underwriters were willing to write insurance policies against almost any kind of risk, including, according to one history, house-breaking, highway robbery, death by gin-drinking, the death of horses, and “assurance of female chastity”—of which all but the last are still insurable.20 On a more serious basis, the demand for fire insurance had expanded rapidly after the great fire of London in 1666.

Lloyd’s coffee house served from the start as the headquarters for marine underwriters, in large part because of its excellent mercantile and shipping connections. “Lloyd’s List” was eventually enlarged to provide daily news on stock prices, foreign markets, and high-water times at London Bridge, along with the usual notices of ship arrivals and departures and reports of accidents and sinkings.c This publication was so well known that its correspondents sent their messages to the post office addressed simply “Lloyd’s.” The government even used “Lloyd’s List” to publish the latest news of battles at sea.

In 1720, reputedly succumbing to a bribe of £300,000, King George I consented to the establishment of the Royal Exchange Assurance Corporation and the London Assurance Corporation, the first two insurance companies in England, setting them up “exclusive of all other corporations and societies.” Although the granting of this monopoly did prevent the establishment of any other insurance company, “private and particular persons” were still allowed to operate as underwriters. In fact, the corporations were constantly in difficulty because of their inability to persuade experienced underwriters to join them.

In 1771, nearly a hundred years after Edward Lloyd opened his coffee house on Tower Street, seventy-nine of the underwriters who did business at Lloyd’s subscribed £100 each and joined together in the Society of Lloyd’s, an unincorporated group of individual entrepreneurs operating under a self-regulated code of behavior. These were the original Members of Lloyd’s; later, members came to be known as “Names.” The Names committed all their worldly possessions and all their financial capital to secure their promise to make good on their customers’ losses. That commitment was one of the principal reasons for the rapid growth of business underwritten at Lloyd’s over the years. And thus did Canopius’s cup of coffee lead to the establishment of the most famous insurance company in history.

By the 1770s an insurance industry had emerged in the American colonies as well, though most large policies were still being written in England. Benjamin Franklin had set up a fire-insurance company called First American in 1752; the first life insurance was written by the Presbyterian Ministers’ Fund, established in 1759. Then, when the Revolution broke out, the Americans, deprived of Lloyd’s services, had no choice but to form more insurance companies of their own. The first company to be owned by stockholders was the Insurance Company of North America in Philadelphia, which wrote policies on fire and marine insurance and issued the first life-insurance policies in America—six-term policies on sea captains.d21

![]()

Insurance achieved its full development as a commercial concept only in the eighteenth century, but the business of insurance dates back beyond the eighteenth century BC. The Code of Hammurabi, which appeared about 1800 BC, devoted 282 clauses to the subject of “bottomry.” Bottomry was a loan or a mortgage taken out by the owner of a ship to finance the ship’s voyage. No premium as we know it was paid. If the ship was lost, the loan did not have to be repaid.e This early version of marine insurance was still in use up to the Roman era, when underwriting began to make an appearance. The Emperor Claudius (10 BC-AD 54), eager to boost the corn trade, made himself a one-man, premium-free insurance company by taking personal responsibility for storm losses incurred by Roman merchants, not unlike the way governments today provide aid to areas hit by earthquakes, hurricanes, or floods.

Occupational guilds in both Greece and Rome maintained cooperatives whose members paid money into a pool that would take care of a family if the head of the household met with premature death. This practice persisted into the time of Edward Lloyd, when “friendly societies” still provided this simple form of life insurance.f

The rise of trade during the Middle Ages accelerated the growth of finance and insurance. Major financial centers grew up in Amsterdam, Augsburg, Antwerp, Frankfurt, Lyons, and Venice; Bruges established a Chamber of Assurance in 1310. Not all of these cities were seaports; most trade still traveled over land. New instruments such as bills of exchange came into use to facilitate the transfer of money from customer to shipper, from lender to borrower and from borrower to lender, and, in huge sums, from the Church’s widespread domain to Rome.

Quite aside from financial forms of risk management, merchants learned early on to employ diversification to spread their risks. Antonio, Shakespeare’s merchant of Venice, followed this practice:

My ventures are not in one bottom trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year;

Therefore, my merchandise makes me not sad.

(Act I, Scene 1)

The use of insurance was by no means limited to shipments of goods. Farmers, for example, are so completely dependent on nature that their fortunes are peculiarly vulnerable to unpredictable but devastating disasters such as drought, flood, or pestilence. As these events are essentially independent of one another and hardly under the influence of the farmer, they provide a perfect environment for insurance. In Italy, for example, farmers set up agricultural cooperatives to insure one another against bad weather; farmers in areas with a good growing season would agree to compensate those whose weather had been less favorable. The Monte dei Paschi, which became one of the largest banks in Italy, was established in Siena in 1473 to serve as an intermediary for such arrangements.22 Similar arrangements exist today in less-developed countries that are heavily dependent on agriculture.23

Although these are all cases in which one group agrees to indemnify another group against losses, the insurance process as a whole functions in precisely the same manner. Insurance companies use the premiums paid by people who have not sustained losses to pay off people who have. The same holds true of gambling casinos, which pay off the winners from the pot that is constantly being replenished by the losers. Because of the anonymity provided by the insurance company or the gambling casino that acts as intermediary, the actual exchange is less visible. And yet the most elaborate insurance and gambling schemes are merely variations on the Monte dei Paschi theme.

The underwriters active in Italy during the fourteenth century did not always perform to the satisfaction of their customers, and the complaints are familiar. A Florentine merchant named Francesco di Marco Datini, who did business as far away as Barcelona and Southampton, wrote his wife a letter complaining about his underwriters. “For whom they insure,” he wrote, “it is sweet to them to take the monies; but when disaster comes, it is otherwise, and each man draws his rump back and strives not to pay.”24 Francesco knew what he was talking about, for he left four hundred marine insurance policies in his estate when he died.

Rembrandt’s Storm on the Sea of Galilee.

(Reproduction courtesy of the Isabella Stewart Gardner Museum, Boston.)

My ventures are not in one bottom trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year;

Therefore, my merchandise makes me not sad.

(Act I, Scene 1)

Activity in the insurance business gained momentum around 1600. The term “policy,” which was already in general use by then, comes from the Italian “polizza,” which meant a promise or an undertaking. In 1601, Francis Bacon introduced a bill in Parliament to regulate insurance policies, which were “tyme out of mynde an usage amonste merchants, both of this realm and of forraine nacyons.”

![]()

The profit on an investment in goods that must be shipped over long distances before they reach their market depends on more than just the weather. It also depends on informed judgments about consumer needs, pricing levels, and fashions at the time of the cargo’s arrival, to say nothing of the cost of financing the goods until they are delivered, sold, and paid for. As a result, forecasting—long denigrated as a waste of time at best and a sin at worst—became an absolute necessity in the course of the seventeenth century for adventuresome entrepreneurs who were willing to take the risk of shaping the future according to their own design.

Commonplace as it seems today, the development of business forecasting in the late seventeenth century was a major innovation. As long as mathematicians had excluded commercial applications from their theoretical innovations, advances toward a science of risk management had to wait until someone asked new questions, questions that, like Graunt’s, required lifting one’s nose beyond the confines of balla and dice. Even Halley’s bold contribution to calculations of life expectancies was to him only a sociological study or a game with arithmetic played out for the amusement of his scientific colleagues; his failure to make any reference to Pascal’s theoretical work on probability thirty years earlier is revealing.

An enormous conceptual hurdle had to be overcome before the shift could be made from identifying inexorably determined mathematical odds to estimating the probability of uncertain outcomes, to turn from collecting raw data to deciding what to do with them once they were in hand. The intellectual advances from this point forward are in many ways more astonishing than the advances we have witnessed so far.

Some of the innovators drew their inspiration by looking up at the stars, others by manipulating the concept of probabiliry in ways th at Pascal and Fermat had never dreamed of But the next figure we meet was the most originalofall: he directed his attention to the question of wealth. We draw on his answers almost every day of our lives.

a The information on the quantity of bread a penny could buy provided a standard for estimating the cost of living. In our own times, a package of goods and services is used as the standard.

b The word “venery” descends from the Middle-French word vena, to hunt (from which also comes the word “venison”) and from Venus (from which comes the word “venereal).” A venerable word indeed!

c Lloyd’s, in short, is the ancestor of the huge Bloomberg business news network of our own time.

d The trust business in Boston was founded by Nathaniel Bowditch in the 1810s to serve the same market.

e This principle applied to life insurance as well. The debts of a soldier who died in battle were forgiven and did not have to be repaid.

f In the United States it survived into the twentieth century. Here it was known as “industrial insurance” and usually covered only funeral expenses. My father-in-law had a little book in which he kept a record of the weekly premiums he paid into such a policy.

Notes

1. I am grateful to Stigler (1977) for this description and to Stephen Stigler personally for drawing the Trial of the Pyx to my attention.

2. The background material on Graunt is from Muir, 1961; David, 1962; and Newman, 1988g. (Direct quotations from Natural and Political Obligations are primarily from Newman.)

3. Newman, 1988g, p. 1394.

4. The background material on Petty is from Hacking, 1975, pp. 102–105.

5. The material about Wilkins and the Royal Society is from Hacking, 1975, pp. 169–171.

6. Graunt, p. 1401.

7. Ibid, p. 1401.

8. Hacking, 1975, p. 103.

9. I am grateful to Stephen Stigler for making this point clear to me.

10. See Hacking, 1975, pp. 103–105.

11. The illustration is from Stigler, 1996.

12. David, 1962, p. 107. An extended explanation of Graunt’s calculations and estimating procedure appears on pp. 107–109.

13. Hacking, 1975, p. 107.

14. Ibid., p. 110.

15. See discussion in Hacking, 1975, pp. 105–110.

16. The background material on Naumann and Halley and the quotations from Halley are primarily from Newman, 1988g, pp. 1393–1396 and 1414–1432.

17. See discussion in Hacking, 1975, pp. 111–121.

18. The material that follows on the history of insurance in general and Lloyd’s in particular is from Flower and Jones, 1974; also Hodgson, 1984.

19. Macaulay, 1848, p. 494. For Macaulay’s full and fascinating story of the English national debt, see the entire chapter that runs from p. 487 to p. 498.

20. Flower and Jones, 1974.

21. American Academy of Actuaries, 1994, and Moorehead, 1989.

22. Interesting background material on the role of the Monte dei Paschi may be found in Chichilnisky and Heal, 1993.

23. See, in particular, Townsend, 1995, and Besley, 1995.

24. Flower and Jones, 1974, p. 13.