Chapter 9. Estimating Financial Risk through Monte Carlo Simulation

If you want to understand geology, study earthquakes. If you want to understand the economy, study the Depression.

Ben Bernanke

Under reasonable circumstances, how much can you expect to lose? This is the quantity that the financial statistic Value at Risk (VaR) seeks to measure. Since its development soon after the stock market crash of 1987, VaR has seen widespread use across financial services organizations. The statistic plays a vital role in the management of these institutions—it helps determine how much cash they must hold to meet the credit ratings that they seek. In addition, some use it to more broadly understand the risk characteristics of large portfolios, and others compute it before executing trades to help inform immediate decisions.

Many of the most sophisticated approaches to estimating this statistic rely on computationally intensive simulation of markets under random conditions. The technique behind these approaches, called Monte Carlo simulation, involves posing thousands or millions of random market scenarios and observing how they tend to affect a portfolio. Spark is an ideal tool for Monte Carlo simulation, because the technique is naturally massively parallelizable. Spark can leverage thousands of cores to run random trials and aggregate their results. As a general-purpose data transformation engine, it is also adept at performing the pre- and post-processing steps that surround the simulations. It can transform the raw financial data into the model parameters needed to carry out the simulations, as well as support ad-hoc analysis of the results. Its simple programming model can drastically reduce development time compared to more traditional approaches that use HPC environments.

Let’s define “how much can you expect to lose” a little more rigorously. VaR is a simple measure of investment risk that tries to provide a reasonable estimate of the maximum probable loss in value of an investment portfolio over the particular time period. A VaR statistic depends on three parameters: a portfolio, a time period, and a p-value. A VaR of 1 million dollars with a 5% p-value and two weeks indicates the belief that the portfolio stands only a 5% chance of losing more than 1 million dollars over two weeks.

We’ll also discuss how to compute a related statistic called Conditional Value at Risk (CVaR), sometimes known as Expected Shortfall, which the Basel Committee on Banking Supervision has recently proposed as a better risk measure than VaR. A CVaR statistic has the same three parameters as a VaR statistic, but considers the expected loss instead of the cutoff value. A CVaR of 5 million dollars with a 5% q-value and two weeks indicates the belief that the average loss in the worst 5% of outcomes is 5 million dollars.

In service of modeling VaR, we’ll introduce a few different concepts, approaches, and packages. We’ll cover kernel density estimation and plotting with the breeze-viz package, sampling from the multivariate normal distribution, and statistics functions from the Apache Commons Math package.

Terminology

This chapter makes use of a set of terms specific to the finance domain. We’ll briefly define them here:

- Instrument

-

A tradable asset, such as a bond, loan, option, or stock investment. At any particular time, an instrument is considered to have a value, which is the price for which it could be sold.

- Portfolio

-

A collection of instruments owned by a financial institution.

- Return

-

The change in an instrument or portfolio’s value over a time period.

- Loss

-

A negative return.

- Index

-

An imaginary portfolio of instruments. For example, the NASDAQ Composite index includes about 3,000 stocks and similar instruments for major US and international companies.

- Market factor

-

A value that can be used as an indicator of macro aspects of the financial climate at a particular time—for example, the value of an index, the Gross Domestic Product of the United States, or the exchange rate between the dollar and the euro. We will often refer to market factors as just factors.

Methods for Calculating VaR

So far, our definition of VaR has been fairly open ended. Estimating this statistic requires proposing a model for how a portfolio functions and choosing the probability distribution its returns are likely to take. Institutions employ a variety of approaches for calculating VaR, all of which tend to fall under a few general methods.

Historical Simulation

Historical Simulation extrapolates risk from historical data by using its distribution directly instead of relying on summary statistics. For example, to determine a 95% VaR for a portfolio, it might look at that portfolio’s performance for the last hundred days and estimate the statistic as its value on the fifth-worst day. A drawback of this method is that historical data can be limited and fails to include “what-ifs.” The history we have for the instruments in our portfolio may lack market collapses, but we might wish to model what happens to our portfolio in these situations. Techniques exist for making historical simulation robust to these issues, such as introducing “shocks” into the data, but we won’t cover them here.

Monte Carlo Simulation

Monte Carlo Simulation, which the rest of this chapter will focus on, tries weakening the assumptions in the previous methods by simulating the portfolio under random conditions. When we can’t derive a closed form for a probability distribution analytically, we can often estimate its density function (PDF) by repeatedly sampling simpler random variables that it depends on and seeing how it plays out in aggregate. In its most general form, this method:

-

Defines a relationship between market conditions and each instrument’s returns. This relationship takes the form of a model fitted to historical data.

-

Defines distributions for the market conditions that are straightforward to sample from. These distributions are fitted to historical data.

-

Poses trials consisting of random market conditions.

-

Calculates the total portfolio loss for each trial, and uses these losses to define an empirical distribution over losses. This means that, if we run 100 trials and want to estimate the 5% VaR, we would choose it as the loss from the trial with the fifth-greatest loss. To calculate the 5% CVaR, we would find the average loss over the five worst trials.

Of course, the Monte Carlo method isn’t perfect either. The models for generating trial conditions and for inferring instrument performance from them must make simplifying assumptions, and the distribution that comes out won’t be more accurate than the models and historical data going in.

Our Model

A Monte Carlo risk model typically phrases each instrument’s return in terms of a set of market factors. Common market factors might be the value of indexes like the S&P 500, the US GDP, or currency exchange rates. We then need a model that predicts the return of each instrument based on these market conditions. In our simulation, we’ll use a simple linear model. By our previous definition of return, a factor return is a change in the value of a market factor over a particular time. For example, if the value of the S&P 500 moves from 2,000 to 2,100 over a time interval, its return would be 100. We’ll derive a set of features from simple transformations of the factor returns. That is, the market factor vector mt for a trial t is transformed by some function φ to produce a feature vector of possible different length ft:

For each instrument, we’ll train a model that assigns a weight to each feature. To calculate rit, the return of instrument i in trial t, we use ci, the intercept term for the instrument; wij, the regression weight for feature j on instrument i; and ftj, the randomly generated value of feature j in trial t:

This means that the return of each instrument is calculated as the sum of the returns of the market factor features multiplied by their weights for that instrument. We can fit the linear model for each instrument using historical data (also known as doing linear regression). If the horizon of the VaR calculation is two weeks, the regression treats every (overlapping) two-week interval in history as a labeled point.

It’s also worth mentioning that we could have chosen a more complicated model. For example, the model need not be linear: it could be a regression tree or explicitly incorporate domain-specific knowledge.

Now that we have our model for calculating instrument losses from market factors, we need a process for simulating the behavior of market factors. A simple assumption is that each market factor return follows a normal distribution. To capture the fact that market factors are often correlated—when NASDAQ is down, the Dow is likely to be suffering as well—we can use a multivariate normal distribution with a non-diagonal covariance matrix:

where μ is a vector of the empirical means of the returns of the factors and Σ is the empirical covariance matrix of the returns of the factors.

As before, we could have chosen a more complicated method of simulating the market or assumed a different type of distribution for each market factor, perhaps using distributions with fatter tails.

Getting the Data

It can be difficult to find large volumes of nicely formatted historical price data, but Yahoo! has a variety of stock data available for download in CSV format. The following script, located in the risk/data directory of the repo, will make a series of REST calls to download histories for all the stocks included in the NASDAQ index and place them in a stocks/ directory:

$ ./download-all-symbols.sh

We also need historical data for our risk factors. For our factors, we’ll use the values of the S&P 500 and NASDAQ indexes, as well as the prices of 30-year treasury bonds and crude oil. The indexes can be downloaded from Yahoo! as well:

$ mkdir factors/ $ ./download-symbol.sh SNP factors $ ./download-symbol.sh NDX factors

The treasury bonds and crude oil must be copy/pasted from Investing.com.

Preprocessing

At this point, we have data from different sources in different formats. For example, the first few rows of the Yahoo!-formatted data for GOOGL looks like:

Date,Open,High,Low,Close,Volume,Adj Close 2014-10-24,554.98,555.00,545.16,548.90,2175400,548.90 2014-10-23,548.28,557.40,545.50,553.65,2151300,553.65 2014-10-22,541.05,550.76,540.23,542.69,2973700,542.69 2014-10-21,537.27,538.77,530.20,538.03,2459500,538.03 2014-10-20,520.45,533.16,519.14,532.38,2748200,532.38

And the Investing.com history for crude oil price looks like:

Oct 24, 2014 81.01 81.95 81.95 80.36 272.51K -1.32% Oct 23, 2014 82.09 80.42 82.37 80.05 354.84K 1.95% Oct 22, 2014 80.52 82.55 83.15 80.22 352.22K -2.39% Oct 21, 2014 82.49 81.86 83.26 81.57 297.52K 0.71% Oct 20, 2014 81.91 82.39 82.73 80.78 301.04K -0.93% Oct 19, 2014 82.67 82.39 82.72 82.39 - 0.75%

From each source, for each instrument and factor, we want to derive a list of (date, closing price) tuples. Using Java’s SimpleDateFormat, we can parse dates in the Investing.com format:

importjava.text.SimpleDateFormatvalformat=newSimpleDateFormat("MMM d, yyyy")format.parse("Oct 24, 2014")res0:java.util.Date=FriOct2400:00:00PDT201

The 3,000-instrument histories and 4-factor histories are small enough to read and process locally. This remains the case even for larger simulations with hundreds of thousands of instruments and thousands of factors. The need for a distributed system like Spark comes in when we’re actually running the simulations, which can require massive amounts of computation on each instrument.

To read a full Investing.com history from local disk:

importcom.github.nscala_time.time.Imports._importjava.io.Fileimportscala.io.SourcedefreadInvestingDotComHistory(file:File):Array[(DateTime,Double)]={valformat=newSimpleDateFormat("MMM d, yyyy")vallines=Source.fromFile(file).getLines().toSeqlines.map(line=>{valcols=line.split(' ')valdate=newDateTime(format.parse(cols(0)))valvalue=cols(1).toDouble(date,value)}).reverse.toArray}

As in Chapter 8, we use JodaTime and its Scala wrapper NScalaTime to represent our dates, wrapping the Date output of SimpleDateFormat in a JodaTime DateTime.

To read a full Yahoo! history:

defreadYahooHistory(file:File):Array[(DateTime,Double)]={valformat=newSimpleDateFormat("yyyy-MM-dd")vallines=Source.fromFile(file).getLines().toSeqlines.tail.map(line=>{valcols=line.split(',')valdate=newDateTime(format.parse(cols(0)))valvalue=cols(1).toDouble(date,value)}).reverse.toArray}

Notice that lines.tail is useful for excluding the header row. We load all the data and filter out instruments with less than five years of history:

valstart=newDateTime(2009,10,23,0,0)valend=newDateTime(2014,10,23,0,0)valfiles=newFile("data/stocks/").listFiles()valrawStocks:Seq[Array[(DateTime,Double)]]=files.flatMap(file=>{try{Some(readYahooHistory(file))}catch{casee:Exception=>None}}).filter(_.size>=260*5+10)valfactorsPrefix="data/factors/"valfactors1:Seq[Array[(DateTime,Double)]]=Array("crudeoil.tsv","us30yeartreasurybonds.tsv").map(x=>newFile(factorsPrefix+x)).map(readInvestingDotComHistory)valfactors2:Seq[Array[(DateTime,Double)]]=Array("SNP.csv","NDX.csv").map(x=>newFile(factorsPrefix+x)).map(readYahooHistory)

Different types of instruments may trade on different days, or the data may have missing values for other reasons, so it is important to make sure that our different histories align. First, we need to trim all of our time series to the same region in time. Then, we need to fill in missing values. To deal with time series that are missing values at the start and end dates in the time region, we simply fill in those dates with nearby values in the time region:

deftrimToRegion(history:Array[(DateTime,Double)],start:DateTime,end:DateTime):Array[(DateTime,Double)]={vartrimmed=history.dropWhile(_._1<start).takeWhile(_._1<=end)

if(trimmed.head._1!=start){trimmed=Array((start,trimmed.head._2))++trimmed}if(trimmed.last._1!=end){trimmed=trimmed++Array((end,trimmed.last._2))}trimmed}

Implicitly takes advantage of the NScalaTime operator overloading for comparing dates

To deal with missing values within a time series, we use a simple imputation strategy that fills in an instrument’s price as its most recent closing price before that day. Unfortunately, there is no pretty Scala collections method that can do this for us, so we need to write our own:

importscala.collection.mutable.ArrayBufferdeffillInHistory(history:Array[(DateTime,Double)],start:DateTime,end:DateTime):Array[(DateTime,Double)]={varcur=historyvalfilled=newArrayBuffer[(DateTime,Double)]()varcurDate=startwhile(curDate<end){if(cur.tail.nonEmpty&&cur.tail.head._1==curDate){cur=cur.tail}filled+=((curDate,cur.head._2))curDate+=1.days// Skip weekendsif(curDate.dayOfWeek().get>5)curDate+=2.days}filled.toArray}

We apply trimToRegion and fillInHistory to the data:

valstocks:Seq[Array[Double]]=rawStocks.map(trimToRegion(_,start,end)).map(fillInHistory(_,start,end))valfactors:Seq[Array[Double]=(factors1++factors2).map(trimToRegion(_,start,end)).map(fillInHistory(_,start,end))

Each element of stocks is an array of values at different time points for a particular stock. factors has the same structure. All these arrays should have equal length, which we can verify with:

(stocks++factors).forall(_.size==stocks(0).size)res17:Boolean=true

Determining the Factor Weights

Recall that Value at Risk deals with losses over a particular time horizon. We are not concerned with the absolute prices of instruments, but how those prices move over a given length of time. In our calculation, we will set that length to two weeks. The following function makes use of the Scala collections’ sliding method to transform time series of prices into an overlapping sequence of price movements over two-week intervals. Note that we use 10 instead of 14 to define the window because financial data does not include weekends:

deftwoWeekReturns(history:Array[(DateTime,Double)]):Array[Double]={history.sliding(10).map(window=>window.last._2-window.head._2).toArray}valstocksReturns=stocks.map(twoWeekReturns)valfactorsReturns=factors.map(twoWeekReturns)

With these return histories in hand, we can turn to our goal of training predictive models for the instrument returns. For each instrument, we want a model that predicts its two-week return based on the returns of the factors over the same time period. For simplicity, we will use a linear regression model.

To model the fact that instrument returns may be nonlinear functions of the factor returns, we can include some additional features in our model that we derive from nonlinear transformations of the factor returns. We will try adding two additional features for each factor return: its square and its square root. Our model is still a linear model in the sense that the response variable is a linear function of the features. Some of the features just happen to be determined by nonlinear functions of the factor returns. Keep in mind that this particular feature transformation is meant to demonstrate some of the options available—it shouldn’t be perceived as a state-of-the-art practice in predictive financial modeling.

While we will be carrying out many regressions—one for each instrument—the number of features and data points in each regression is small, meaning that we don’t need to make use of Spark’s distributed linear modeling capabilities. Instead, we’ll use the ordinary least squares regression offered by the Apache Commons Math package. While our factor data is currently a Seq of histories (each an array of (DateTime, Double) tuples), OLSMultipleLinearRegression expects data as an array of sample points (in our case a two-week interval), so we need to transpose our factor matrix:

deffactorMatrix(histories:Seq[Array[Double]]):Array[Array[Double]]={valmat=newArray[Array[Double]](histories.head.length)for(i<-0untilhistories.head.length){mat(i)=histories.map(_(i)).toArray}mat}valfactorMat=factorMatrix(factorsReturns)

Then we can tack on our additional features:

deffeaturize(factorReturns:Array[Double]):Array[Double]={valsquaredReturns=factorReturns.map(x=>math.signum(x)*x*x)valsquareRootedReturns=factorReturns.map(x=>math.signum(x)*math.sqrt(math.abs(x)))squaredReturns++squareRootedReturns++factorReturns}valfactorFeatures=factorMat.map(featurize)

And then fit the linear models:

importorg.apache.commons.math3.stat.regression.OLSMultipleLinearRegressiondeflinearModel(instrument:Array[Double],factorMatrix:Array[Array[Double]]):OLSMultipleLinearRegression={valregression=newOLSMultipleLinearRegression()regression.newSampleData(instrument,factorMatrix)regression}valmodels=stocksReturns.map(linearModel(_,factorFeatures))

We will elide this analysis for brevity, but at this point in any real-world pipeline, it would be useful to understand how well these models fit the data. Because the data points are drawn from time series, and especially because the time intervals are overlapping, it is very likely that the samples are autocorrelated. This means that common measures like R2 are likely to overestimate how well the models fit the data. The Breusch-Godfrey test is a standard test for assessing these effects. One quick way to evaluate a model is to separate a time series into two sets, leaving out enough data points in the middle so that the last points in the earlier set are not autocorrelated with the first points in the later set. Then train the model on one set and look at its error on the other.

To find the model parameters for each instrument, we can use OLSMultipleLinearRegression’s estimateRegressionParameters method:

valfactorWeights=models.map(_.estimateRegressionParameters()).toArray

We now have a 1,867-×-8 matrix where each row is the set of model parameters (coefficients, weights, covariants, regressors, whatever you wish to call them) for an instrument.

Sampling

With our models that map factor returns to instrument returns in hand, we now need a procedure for simulating market conditions by generating random factor returns. That is, we need to decide on a probability distribution over factor return vectors and sample from it. What distribution does the data actually take? It can often be useful to start answering this kind of question visually. A nice way to visualize a probability distribution over continuous data is a density plot that plots the distribution’s domain versus its PDF. Because we don’t know the distribution that governs the data, we don’t have an equation that can give us its density at an arbitrary point, but we can approximate it through a technique called kernel density estimation. In a loose way, kernel density estimation is a way of smoothing out a histogram. It centers a probability distribution (usually a normal distribution) at each data point. So a set of two-week-return samples would result in 200 normal distributions, each with a different mean. To estimate the probability density at a given point, it evaluates the PDFs of all the normal distributions at that point and takes their average. The smoothness of a kernel density plot depends on its bandwidth, the standard deviation of each of the normal distributions. The GitHub repository comes with a kernel density implementation that works both over RDDs and local collections. For brevity, it is elided here.

breeze-viz is a Scala library that makes it easy to draw simple plots. The following snippet creates a density plot from a set of samples:

importcom.cloudera.datascience.risk.KernelDensityimportbreeze.plot._defplotDistribution(samples:Array[Double]){valmin=samples.minvalmax=samples.maxvaldomain=Range.Double(min,max,(max-min)/100).toList.toArrayvaldensities=KernelDensity.estimate(samples,domain)valf=Figure()valp=f.subplot(0)p+=plot(domain,densities)p.xlabel="Two Week Return ($)"p.ylabel="Density"}plotDistribution(factorReturns(0))plotDistribution(factorReturns(1))

Figure 9-1 shows the distribution (probability density function) of two-week returns for the bonds in our history.

Figure 9-1. Two-week bond returns distribution

Figure 9-2 shows the same for two-week returns of crude oil.

Figure 9-2. Two-week crude oil returns distribution

We will fit a normal distribution to the returns of each factor. Looking for a more exotic distribution, perhaps with fatter tails, that more closely fits the data is often worthwhile. However, for the sake of simplicity, we will avoid tuning our simulation in this way.

The simplest way to sample factors’ returns would be to fit a normal distribution to each of the factors and sample from these distributions independently. However, this ignores the fact that market factors are often correlated. If S&P is down, the Dow is likely to be down as well. Failing to take these correlations into account can give us a much rosier picture of our risk profile than its reality. Are the returns of our factors correlated? The Pearson’s correlation implementation from Commons Math can help us find out:

importorg.apache.commons.math3.stat.correlation.PearsonsCorrelationvalfactorCor=newPearsonsCorrelation(factorMat).getCorrelationMatrix().getData()println(factorCor.map(_.mkString(" ")).mkString(" "))1.0-0.34830.23390.3975-0.34831.0-0.2198-0.44290.2339-0.21981.00.33490.3975-0.44290.33491.0

Digits truncated to fit between the margins

Because we have nonzero elements off the diagonals, it doesn’t look like it.

The Multivariate Normal Distribution

The multivariate normal distribution can help here by taking the correlation information between the factors into account. Each sample from a multivariate normal is a vector. Given values for all of the dimensions but one, the distribution of values along that dimension is normal. But, in their joint distribution, the variables are not independent.

The multivariate normal is parameterized with a mean along each dimension and a matrix describing the covariances between each pair of dimensions. With N dimensions, the covariance matrix is N by N, because we want to capture the covariances between each pair of dimensions. When the covariance matrix is diagonal, the multivariate normal reduces to sampling along each dimension independently, but placing nonzero values in the off-diagonals helps capture the relationships between variables.

The Value at Risk literature often describes a step in which the factor weights are transformed (decorrelated) so that sampling can proceed. This is normally accomplished with a Cholesky Decomposition or Eigendecomposition. The Apache Commons Math MultivariateNormalDistribution takes care of this step for us under the covers using an Eigendecomposition.

To fit a multivariate normal distribution to our data, first we need to find its sample means and covariances:

importorg.apache.commons.math3.stat.correlation.CovariancevalfactorCov=newCovariance(factorMat).getCovarianceMatrix().getData()valfactorMeans=factorsReturns.map(factor=>factor.sum/factor.size).toArray

Then, we can simply create a distribution parameterized with them:

importorg.apache.commons.math3.distribution.MultivariateNormalDistributionvalfactorsDist=newMultivariateNormalDistribution(factorMeans,factorCov)

To sample a set of market conditions from it:

factorsDist.sample()res1:Array[Double]=Array(2.6166887901169384,2.596221643793665,1.4224088720128492,55.00874247284987)factorsDist.sample()res2:Array[Double]=Array(-8.622095499198096,-2.5552498805628256,2.3006882454319686,-75.4850042214693)

Running the Trials

With the per-instrument models and a procedure for sampling factor returns, we now have the pieces we need to run the actual trials. Because running the trials is very computationally intensive, we will finally turn to Spark to help us parallelize them. In each trial, we want to sample a set of risk factors, use them to predict the return of each instrument, and sum all those returns to find the full trial loss. To achieve a representative distribution, we want to run thousands or millions of these trials.

We have a few choices in how to parallelize the simulation. We can parallelize along trials, instruments, or both. To parallelize along both, we would create an RDD of instruments and an RDD of trial parameters, and then use the cartesian transformation to generate an RDD of all the pairs. This is the most general approach, but it has a couple of disadvantages. First, it requires explicitly creating an RDD of trial parameters, which we can avoid by using some tricks with random seeds. Second, it requires a shuffle operation.

Partitioning along instruments would look something like this:

valrandomSeed=1496valinstrumentsRdd=...deftrialLossesForInstrument(seed:Long,instrument:Array[Double]):Array[(Int,Double)]={...}instrumentsRdd.flatMap(trialLossesForInstrument(randomSeed,_)).reduceByKey(_+_)

With this approach, the data is partitioned across an RDD of instruments, and, for each instrument a flatMap transformation computes and yields the loss against every trial. Using the same random seed across all tasks means that we will generate the same sequence of trials. A reduceByKey sums together all the losses corresponding to the same trials. A disadvantage of this approach is that it still requires shuffling O(|instruments| * |trials|) data.

Our model data for our few thousand instruments data is small enough to fit in memory on every executor, and some back-of-the-envelope calculations reveal that this is probably still the case even with a million or so instruments and hundreds of factors. A million instruments times five hundred factors times the eight bytes needed for the double that stores each factor weight equals roughly 4 GB, small enough to fit in each executor on most modern-day cluster machines. This means that a good option is to distribute the instrument data in a broadcast variable. The advantage of each executor having a full copy of the instrument data is that total loss for each trial can be computed on a single machine. No aggregation is necessary.

With the partition-by-trials approach (which we will use), we start out with an RDD of seeds. We want a different seed in each partition so that each partition generates different trials:

valparallelism=1000valbaseSeed=1496valseeds=(baseSeeduntilbaseSeed+parallelism)valseedRdd=sc.parallelize(seeds,parallelism)

Random number generation is a time-consuming and CPU-intensive process. While we don’t employ this trick here, it can often be useful to generate a set of random numbers in advance and use it across multiple jobs. The same random numbers should not be used within a single job, because this would violate the Monte Carlo assumption that the random values are independently distributed. If we were to go this route, we would replace parallelize with textFile and load a randomNumbersRdd.

For each seed, we want to generate a set of trial parameters and observe the effects of these parameters on all the instruments. Let’s start from the ground up by writing a function that calculates the return of a single instrument underneath a single trial. We simply apply the linear model that we trained earlier for that instrument. The length of the instrument array of regression parameters is one greater than the length of the trial array, because the first element of the instrument array contains the intercept term:

definstrumentTrialReturn(instrument:Array[Double],trial:Array[Double]):Double={varinstrumentTrialReturn=instrument(0)vari=0while(i<trial.length){instrumentTrialReturn+=trial(i)*instrument(i+1)i+=1}instrumentTrialReturn}

We use a

whileloop here instead of a more functional Scala construct because this is a performance-critical region

Then, to calculate the full return for a single trial, we simply sum over the returns of all the instruments:

deftrialReturn(trial:Array[Double],instruments:Seq[Array[Double]]):Double={vartotalReturn=0.0for(instrument<-instruments){totalReturn+=instrumentTrialReturn(instrument,trial)}totalReturn}

Lastly, we need to generate a bunch of trials in each task. Because choosing random numbers is a big part of the process, it is important to use a strong random number generator that will take a very long time to repeat itself. Commons Math includes a Mersenne twister implementation that is good for this. We use it to sample from a multivariate normal distribution as described previously. Note that we are applying the featurize method that we defined before on the generated factor returns in order to transform them into the feature representation used in our models:

importorg.apache.commons.math3.random.MersenneTwisterdeftrialReturns(seed:Long,numTrials:Int,instruments:Seq[Array[Double]],factorMeans:Array[Double],factorCovariances:Array[Array[Double]]):Seq[Double]={valrand=newMersenneTwister(seed)valmultivariateNormal=newMultivariateNormalDistribution(rand,factorMeans,factorCovariances)valtrialReturns=newArray[Double](numTrials)for(i<-0untilnumTrials){valtrialFactorReturns=multivariateNormal.sample()valtrialFeatures=featurize(trialFactorReturns)trialReturns(i)=trialReturn(trialFeatures,instruments)}trialReturns}

With our scaffolding complete, we can use it to compute an RDD where each element is the total return from a single trial. Because the instrument data (matrix including a weight on each factor feature for each instrument) is large, we use a broadcast variable for it. This ensures that it only needs to be deserialized once per executor:

valnumTrials=10000000valbFactorWeights=sc.broadcast(factorWeights)valtrials=seedRdd.flatMap(trialReturns(_,numTrials/parallelism,bFactorWeights.value,factorMeans,factorCov))

If you recall, the whole reason we’ve been messing around with all these numbers was to calculate VaR. trials now forms an empirical distribution over portfolio returns. To calculate 5% VaR, we need to find a return that we expect to underperform 5% of the time, and a return that we expect to outperform 5% of the time. With our empirical distribution, this is as simple as finding the value that 5% of trials are worse than and 95% of trials are better than. We can accomplish this using the takeOrdered action to pull the worst 5% of trials into the driver. Our VaR is the return of the best trial in this subset:

deffivePercentVaR(trials:RDD[Double]):Double={valtopLosses=trials.takeOrdered(math.max(trials.count().toInt/20,1))topLosses.last}valvalueAtRisk=fivePercentVaR(trials)valueAtRisk:Double=-1752.8675055209305

We can find the CVaR with a nearly identical approach. Instead of taking the best trial return from the worst 5% of trials, we take the average return from that set of trials:

deffivePercentCVaR(trials:RDD[Double]):Double={valtopLosses=trials.takeOrdered(math.max(trials.count().toInt/20,1))topLosses.sum/topLosses.length}valconditionalValueAtRisk=fivePercentVaR(trials)conditionalValueAtRisk:Double=-2353.5692728118033

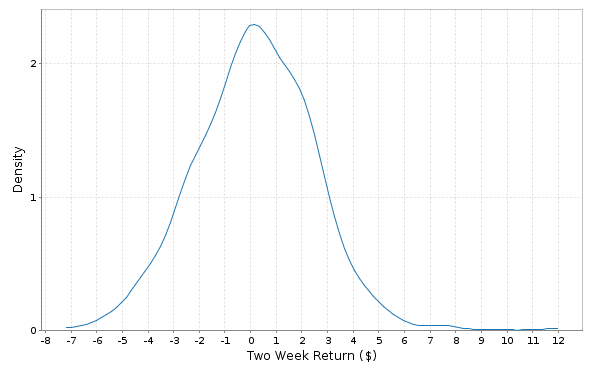

Visualizing the Distribution of Returns

In addition to calculating VaR at a particular confidence level, it can be useful to look at a fuller picture of the distribution of returns. Are they normally distributed? Do they spike at the extremities? As we did for the individual factors, we can plot an estimate of the probability density function for the joint probability distribution using kernel density estimation (see Figure 9-3). Again, the supporting code for calculating the density estimates in a distributed fashion (over RDDs) is included in the GitHub repository accompanying this book:

defplotDistribution(samples:RDD[Double]){valstats=samples.stats()valmin=stats.minvalmax=stats.maxvaldomain=Range.Double(min,max,(max-min)/100).toList.toArrayvaldensities=KernelDensity.estimate(samples,domain)valf=Figure()valp=f.subplot(0)p+=plot(domain,densities)p.xlabel="Two Week Return ($)"p.ylabel="Density"}plotDistribution(trials)

Figure 9-3. Two-week returns distribution

Evaluating Our Results

How do we know whether our estimate is a good estimate? How do we know whether we should simulate with a larger number of trials? In general, the error in a Monte Carlo simulation should be proportional to ![]() . This means that, in general, quadrupling the number of trials should approximately cut the error in half.

. This means that, in general, quadrupling the number of trials should approximately cut the error in half.

A nice way to get a confidence interval on our VaR statistic is through bootstrapping. We achieve a bootstrap distribution over the VaR by repeatedly sampling with replacement from the set of portfolio returns that are the results of our trials. Each time, we take a number of samples equal to the full size of the trials set and compute a VaR from those samples. The set of VaRs computed from all the times form an empirical distribution, and we can get our confidence interval by simply looking at its quantiles.

The following is a function that will compute a bootstrapped confidence interval for any statistic (given by the computeStatistic argument) of an RDD. Notice its use of Spark’s sample where we pass true for its first argument withReplacement, and 1.0 for its second argument to collect a number of samples equal to the full size of the data set:

defbootstrappedConfidenceInterval(trials:RDD[Double],computeStatistic:RDD[Double]=>Double,numResamples:Int,pValue:Double):(Double,Double)={valstats=(0untilnumResamples).map{i=>valresample=trials.sample(true,1.0)computeStatistic(resample)}.sortedvallowerIndex=(numResamples*pValue/2).toIntvalupperIndex=(numResamples*(1-pValue/2)).toInt(stats(lowerIndex),stats(upperIndex))}

Then we call this function, passing in the fivePercentVaR function we defined earlier that computes the VaR from an RDD of trials:

bootstrappedConfidenceInterval(trials,fivePercentVaR,100,.05)(-1754.9059171183192,-1751.0657037512767)

We can bootstrap the CVaR as well:

bootstrappedConfidenceInterval(trials,fivePercentCVaR,100,.05)(-2356.2872000503235,-2351.231980404269)

The confidence interval helps us understand how confident our model is in its result, but it does little to help us understand how well our model matches reality. Backtesting on historical data is a good way to check the quality of a result. One common test for VaR is Kupiec’s proportion-of-failures (POF) test. It considers how the portfolio performed at many historical time intervals and counts the number of times that the losses exceeded the VaR. The null hypothesis is that the VaR is reasonable, and a sufficiently extreme test statistic means that the VaR estimate does not accurately describe the data. The test statistic, which relies on p, the confidence level parameter of the VaR calculation; x, the number of historical intervals over which the losses exceeded the VaR; and T, the total number of historical intervals considered, is computed as:

The following computes the test statistic on our historical data. We expand out the logs for better numerical stability:

varfailures=0for(i<-0untilstocksReturns(0).size){valloss=stocksReturns.map(_(i)).sumif(loss<valueAtRisk){failures+=1}}failures...155valfailureRatio=failures.toDouble/totalvallogNumer=(total-failures)*math.log1p(-confidenceLevel)+failures*math.log(confidenceLevel)vallogDenom=(total-failures)*math.log1p(-failureRatio)+failures*math.log(failureRatio)valtestStatistic=-2*(logNumer-logDenom)...96.88510361007025

If we assume the null hypothesis that the VaR is reasonable, then this test statistic is drawn from a chi-squared distribution with a single degree of freedom. We can use the Commons Math ChiSquaredDistribution to find the p-value accompanying our test statistic value:

importorg.apache.commons.math3.distribution.ChiSquaredDistribution1-newChiSquaredDistribution(1.0).cumulativeProbability(testStatistic)

This gives us a tiny p-value, meaning we do have sufficient evidence to reject the null hypothesis that the model is reasonable. Looks like we need to improve it a little…

Where to Go from Here

The model laid out in this exercise is a very rough first cut of what would be used in an actual financial institution. In building an accurate VaR model, a few steps that we glossed over are very important. Curating the set of market factors can make or break a model, and it is not uncommon for financial institutions to incorporate hundreds of factors in their simulations. Picking these factors requires both running numerous experiments on historical data and a heavy dose of creativity. Choosing the predictive model that maps market factors to instrument returns is also important. Although we used a simple linear model, many calculations use nonlinear functions or simulate the path over time with Brownian motion. Lastly, it is worth putting care into the distribution used to simulate the factor returns. Kolmogorov-Smirnoff tests and chi-squared tests are useful for testing an empirical distribution’s normality. Q-Q plots are useful for comparing distributions visually. Usually, financial risk is better mirrored by a distribution with fatter tails than the normal that we used. Mixtures of normal distributions is one good way to achieve these fatter tails. “Financial Economics, Fat-tailed Distributions”, an article by Markus Haas and Christian Pigorsch, provides a nice reference on some of the other fat-tailed distributions out there.

Banks use Spark and large-scale data processing frameworks for calculating VaR with historical methods as well. “Evaluation of Value-at-Risk Models Using Historical Data”, by Darryll Hendricks, provides a good overview and performance comparison of historical VaR methods.

Monte Carlo risk simulations can be used for more than calculating a single statistic. The results can be used to proactively reduce the risk of a portfolio by shaping investment decisions. For example, if, in the trials with the poorest returns, a particular set of instruments tends to come up losing money repeatedly, we might consider dropping those instruments from the portfolio or adding instruments that tend to move in the opposite direction from them.