Assurance Services and Auditing Research

LEARNING OBJECTIVES

After completing this chapter, you should understand:

- The types of assurance and consulting services and the applicable standards.

- The environment for the assurance services standard-setting process.

- Authoritative auditing support.

- The Public Company Accounting Oversight Board (PCAOB).

- How to utilize the AICPA's professional standards in research.

- The role of auditing in the public sector.

- The hierarchy of the AICPA Code of Professional Conduct.

- The role of professional judgment in the research process.

- International dimensions of auditing.

Because information technology has had a significant impact on the accounting profession and society in general, the public accounting profession has focused on its willingness and ability to design and offer additional value-added services, in addition to such traditional services as tax preparation and auditing. Technological changes have encouraged accounting professionals to transform from number crunchers and certifiers of information to decision support specialists and enhancers of information. Many professionals who keep abreast of the major changes in the profession and technology have adapted their practices and market orientation to these new value-added assurance services. Some practitioners are also expanding the area of consulting services offered to clients. As a result, the practitioner/researcher must become aware of these new assurance services and the related authoritative standards and restrictions that apply in offering these services.

ASSURANCE SERVICES

In order to focus on the needs of users of decision-making information and improve the related services that accountants provide, an AICPA committee conducted research that consisted of assessing customer needs, external factors, information technology, and needed competencies to offer these new value-added services. These services are referred to as assurance services, defined as follows:

Assurance Services are independent professional services that improve the quality of information, or its context, for decision makers.

Notice that this definition of assurance services implies that the service itself will add value to the user, not necessarily just the report. Additionally, an independent professional must offer the assurance services in order to improve the quality of the information or its context. Current examples of such assurance services proposed by the AICPA include CPA WebTrust, CPA ElderCare/Prime Plus, and CPA Performance View services.

QUICK FACTS

Assurance services add value by improving the quality of the information or its context for decision makers.

Therefore, assurance services are considered three-party contracts—involving the client, the assurer (that is, accountant), and the third party to whom the accountant is providing assurance. An example of an assurance service engagement is where Consumers Union tests a product and reports the results or ratings in Consumer Reports.

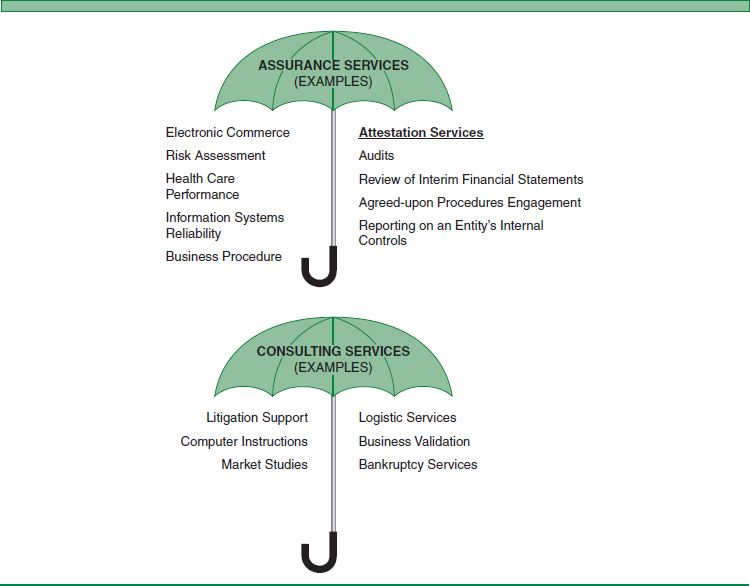

An overview of assurance services versus consulting services is presented in Figure 8-1. Specific details are provided in the following sections of this chapter. As depicted, the traditional audit service is an attestation function that falls under the broader term of assurance services. As a professional conducting research, one must recognize the professional standards for attestation and consulting engagements.

Consulting Services and Standards

Attestation and audit services are considered special types of assurance services. Consulting services do not fall under the umbrella of assurance services. Historically, consulting services offered to clients (two-party contracts) by CPAs were referred to as management consulting services or management advisory services. These services have generally evolved from accounting-related matters in connection with audits or tax engagements. In a consulting engagement, the CPA develops findings and conclusions, which are followed with recommendations for the benefit of the client. This is in contrast to an attest engagement (a three-party contract) whereby the CPA reports on the reliability of a written assertion that is the responsibility of a third party. Examples of consulting engagements include litigation support services, computer installation engagements, and various market studies for clients.

FIGURE 8-1 ASSURANCE AND CONSULTING SERVICES UMBRELLAS

The typical consulting engagement is quite similar to the research process presented in this text. The consulting engagement would normally include:

- Determination of the client's objectives

- Fact-finding

- Definition of the problem

- Evaluation of the alternatives

- Formulation of a proposed action

- Communication of the results

- Implementation and follow-up1

Professional standards for consulting services include general standards and specific consulting standards. In rendering professional services (including consulting), general standards of the profession are located in Rule 201 of the AICPA Code of Professional Conduct, as discussed later in this chapter. Additionally, the AICPA has issued Statements on Standards for Consulting Services (SSCS), which provide standards for the practitioner rendering consulting services. These standards are located in the AICPA's Professional Standards database, also discussed later in this chapter.

AUDITING STANDARD-SETTING ENVIRONMENT

Auditing is indispensable in a society where credit is extended widely and business failures regularly occur and where investors wish to study the financial statements of many enterprises. The purpose of the audit report is to add credibility to the financial information. The general environment for auditing is very dynamic and constantly evolving as various factors impact the audit process.

The independent auditor's role serves a secondary communication function; the audit opinion is expressed on the financial information reported by management. The auditor's primary concern is whether the client's financial statements are presented in accordance with GAAP. The auditor must conduct the audit in a manner that conforms to auditing standards and take actions that are guided by professional ethical standards. Additionally, in nonaudit engagements, the accountant must use relevant attestation standards and statements for compilation and review services, as well as standards for accountants' services on prospective financial information (that is, forecasts and projections).

Attestation Services and Standards

Society increasingly seeks attestation services (a subset of assurance services) from the accounting profession. In the past, attestation services were normally limited to audit opinions on historical financial statements based upon audits that followed generally accepted auditing standards (GAAS).

More recently, professional accountants render opinions on other representations, such as reporting on management's report as to the effectiveness of the entity's internal controls, as now required by the Sarbanes-Oxley Act of 2002. Accountants were concerned that existing standards or guidelines did not meet the demands of society. As a result, the AICPA developed attestation standards and related interpretations to provide a general framework for attest engagements.2

The term attest means to provide assurance as to the reliability of information. The AICPA has defined an attest engagement as follows:

An attest engagement is one in which a practitioner is engaged to issue or does issue a written communication that expresses a conclusion about the reliability of a written assertion that is the responsibility of another party.3

QUICK FACTS

Attestation services provide assurance as to the reliability of information.

Whether the attestation service is for the traditional audit of financial statements or reporting on an entity's internal control or prospective financial information, the professional accountant must follow certain guidelines and standards in rendering these attestation services. In conducting an attest engagement, the professional accountant reviews and conducts tests of the accounting records deemed necessary to obtain sufficient evidence to render an opinion. Choosing the accounting records and other information to review and deciding the extent to examine them are strictly matters of professional judgment, as many authoritative pronouncements emphasize.

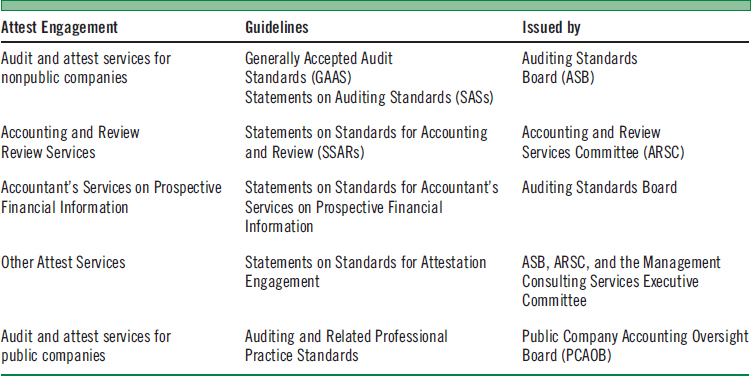

Figure 8-2 presents the major elements of the attestation environment that face accountants in conducting the research for an attest engagement. Figure 8-3 presents an overview of attest engagements and relevant guidelines. The following sections of this chapter provide an overview of the standard-setting environment for attestation services, the auditing standard-setting process, authoritative auditing pronouncements, and the role of professional judgment in the research process. The chapter also includes a discussion of how the researcher utilizes the AICPA's reSOURCE database in research, a summary of the attestation standards and compilation and review standards, as well as an overview of auditing in the public sector and the international dimensions of auditing. The appendix to this chapter presents examples of opening screen shots to the CPA exam that requires one to conduct auditing/attestation research utilizing the AICPA's Professional Standards.

FIGURE 8-2 ATTEST RESEARCH ENVIRONMENT

FIGURE 8-3 ATTEST ENGAGEMENTS AND GUIDELINES

During the past decade, as the range of attestation services has expanded, many CPAs have found it difficult to apply the basic concepts underlying GAAS or the standards of the Public Company Accounting Oversight Board (PCAOB) to various attestation services. Attestation services have also included the following examples: reporting to the client on which computer system is the cheapest or has the most capabilities, reporting on insurance claims data, and reporting on compliance with regulatory requirements. (In one instance, Wilson Sporting Goods requested an accounting firm to attest to the statement that Wilson's Ultra golf ball outdistance its competitors!)

Consequently, the AICPA has issued Statements on Standards for Attestation Engagements, Statements on Standards for Accounting and Review Services, and Statements on Standards for Accountants' Services on Prospective Financial Information to provide a general framework and set reasonable guidelines for an attest function. The desire is to respond to the changing environment and demands of society.

QUICK FACTS

AICPA has issued various authorities for different services.

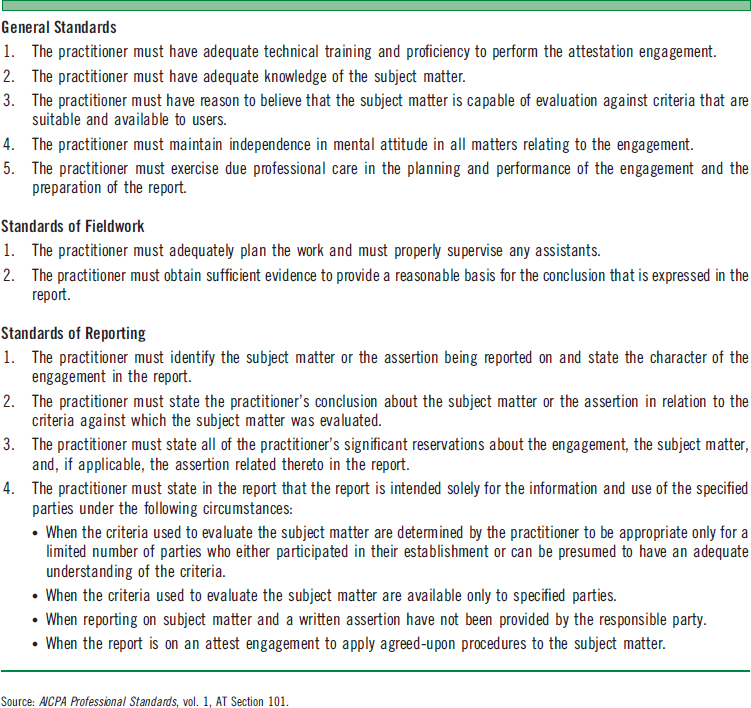

The broad guidelines for an attest engagement were issued by the AICPA's Auditing Standards Board (ASB) in conjunction with the Accounting and Review Services Committee and the Management Consulting Services Executive Committee. As listed in Figure 8-4, these attestation standards do not supersede any existing standards, but are considered a natural extension of the ten GAAS. The design of these attestation standards provides guidance to the professional to enhance both consistency and quality in the performance of attest services.

FIGURE 8-4 ATTESTATION STANDARDS

Auditing Standards

Auditing standards differ from audit procedures in that auditing standards provide measures of the quality of performance, whereas audit procedures refer to the specific acts or steps to perform in an audit engagement. Auditing standards do not vary; they remain identical for all audits. Audit procedures often change, depending on the nature and type of entity under audit and the complexity of the audit.

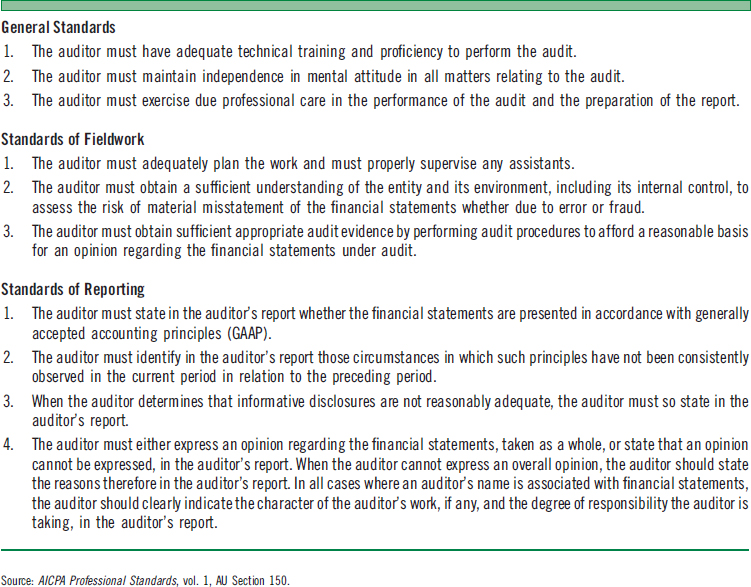

In contrast to GAAP, which is not identified with exactness, the AICPA has formally adopted ten broad requirements for auditors to follow in examining financial statements, classified as general standards, fieldwork standards, and reporting standards. These ten requirements, GAAS, are listed in Figure 8-5. In addition to the issuance of GAAS, the AICPA published a series of Statements on Auditing Standards (SASs).

FIGURE 8-5 GENERALLY ACCEPTED AUDITING STANDARDS

SASs supplement and interpret the ten GAAS by clarifying the audit procedures or prescribing the auditor's report in both form and content. SASs serve as the primary authoritative support in conducting an audit and are a major source of authoritative information when conducting auditing research. These SASs are incorporated into the AICPA's loose-leaf service and online Professional Standards, which provided a continuous codification of SASs.

Thus, the codification of auditing standards organizes logically the essence of the auditing standards. The prefix AU is used to refer to the codified auditing topic. If AU is followed by 2, this section interprets general standards on auditing. Thus, AU 210 addresses standards relating to training, AU 220 summarizes the standards relating to independence, and AU 230 addresses due professional care. If AU is followed by a 3, this section interprets fieldwork standards. Reporting standards are located in AU followed by a 4, 5, or 6. The PCAOB is currently using the codified version of the auditing standards as interim standards. The PCAOB is reviewing and updating audit standards for public companies, as discussed later in this chapter.

Various forms of GAAS are also recognized by governmental and internal auditors. The General Accountability Office (GAO), through the comptroller general of the United States, has issued Governmental Auditing Standards, often referred to as the Yellow Book. The Institute of Internal Auditors has also issued auditing standards, called the Standards for the Professional Practice of Internal Auditing, under which internal auditors operate. The comptroller general has established the U.S. Auditing Standards Coordinating Forum composed of members from the PCAOB, GAO, and the ASB, which meets several times during the year to facilitate coordination and constructive working relationships between the groups. The main focus of discussion is the convergence of auditing standards among the forum members.

AUDITING STANDARD-SETTING PROCESS

Concern has always existed as to who should set auditing standards for the independent auditor. Prior to establishment of the SEC, Congress debated having audits conducted by governmental auditors. However, the auditing standard-setting process remained in the private sector. SASs were created by the ASB as the AICPA's senior technical committee on auditing standards.

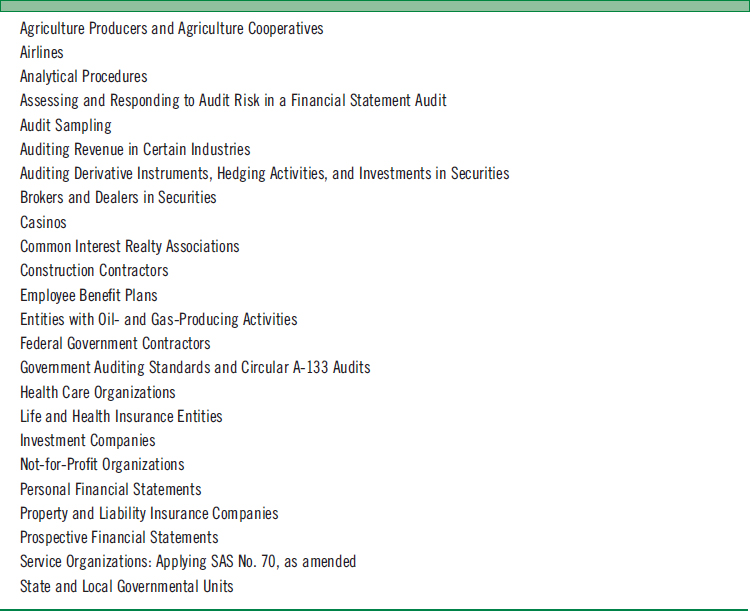

Auditing interpretations on the application of SASs are created by the staff of the Auditing Standards division of the AICPA. The interpretations are not considered as authoritative as SASs. However, auditors must justify any departure from an auditing interpretation issued by the Auditing Standards division of the AICPA. Other publications of the Auditing Standards division include a number of Industry Audit Guides (Figure 8-6) and SOPs.

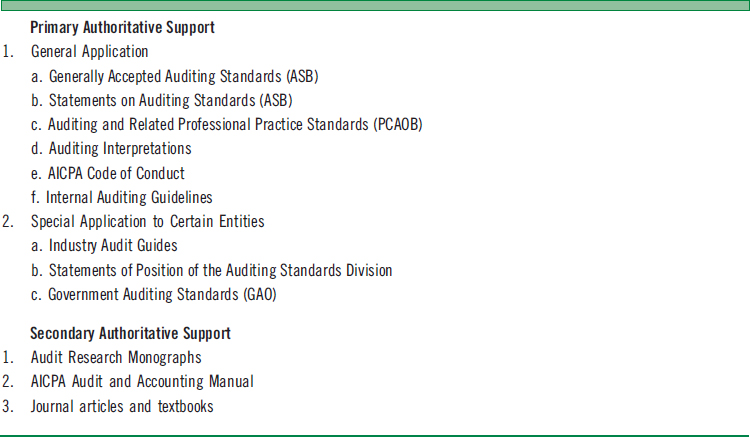

The Sarbanes-Oxley Act of 2002 transferred the responsibility for auditing and attestation standard setting for public companies to the PCAOB, as explained in the next section. An overview of the current hierarchy of authoritative auditing support is presented in Figure 8-7. The auditor needs to understand each of the sources listed, particularly the PCAOB's auditing standards and the predecessor SASs by the AICPA.

Unlike an audit that expresses whether the financial statements are in conformity with GAAP, the accountant's examination of prospective financial statements provides assurance only as to whether (1) the prospective financial statements conform to the AICPA's guidelines and (2) the assumptions used in the projections provide a reasonable basis for a forecast or projection. The accountant must provide a report on any attestation service provided, as described in the various attestation and auditing standards. (See Figures 8-4 and 8-5.)

Public Company Accounting Oversight Board (PCAOB)

The PCAOB has the legal responsibility under the Sarbanes-Oxley Act to establish GAAS, attestation, ethics, and quality control standards for those accounting firms auditing public companies. PCAOB has adopted a rule that requires all registered public accounting firms to adhere to the board's auditing and related practice standards in connection with the preparation or issuance of any audit report for an issuer and in their auditing and related attestation practices. Going forward, the board's new standards are called Auditing and Related Professional Practice Standards.

RESEARCH TIPS

Use the Public Company Accounting Oversight Board (PCAOB) authorities for auditing public companies.

Standards for auditors of nonpublic companies are currently within the domain of the AICPA. The reconstituted mission of the AICPA's ASB includes the following three main issues:

- To develop auditing, attestation, and quality control standards for non-issuer engagements, such as privately held commercial entities, nonprofit organizations, and governmental entities.

FIGURE 8-6 AICPA AUDIT AND ACCOUNTING GUIDES

- To contribute to the development and issuance of high-quality national and international auditing and assurance standards.

- To respond to the needs for practical guidance in implementing professional standards.

The PCAOB initially adopted as interim standards the AICPA's auditing, attestation, and quality control standards, as well as the AICPA's ethics and independence standards. Thus, the PCAOB uses the AICPA standards, as of April 2003, as the authoritative standards for public company audits until superseded or amended by the PCAOB.

AICPA reSOURCE Database

The AICPA reSOURCE database includes a comprehensive compendium of the AICPA literature consisting of Professional Standards, Accounting Trends and Techniques, Technical Practice Aids, Auditing and Accounting Guides, and Audit Alerts. The Professional Standards segment of this database is also utilized on the CPA exam in conducting auditing research.

FIGURE 8-7 AUDITING AUTHORITATIVE SUPPORT

RESEARCH TIPS

Access auditing standards in the AICPA reSOURCE database.

To conduct auditing research utilizing the AICPA's online reSOURCE database would consist of the following steps. The opening screen of the online version of the database appears in Figure 8-8. Clicking on the AICPA Professional Standards link provides the opening screen to the Professional Standards as depicted in Figure 8-9. The table of contents (TOC) appears on the left side of the screen. Clicking on the plus (+) box next to a phrase will expand the TOC section. Note the tabs across the top right of the screen.

RESEARCH TIPS

Keep track of the location of relevant literature on the AICPA reSOURCE database.

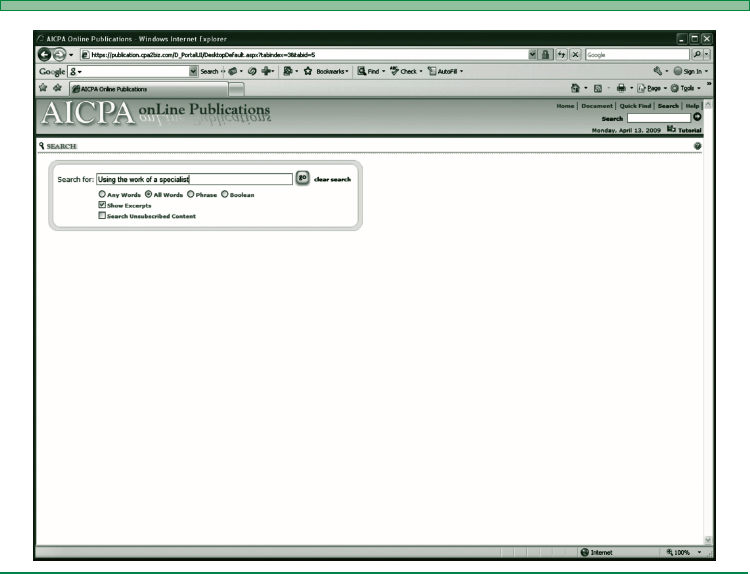

To conduct a specific search, click on the research tab, and the search screen appears, as in Figure 8-10. If one was searching for the guidance in using a specialist, the keywords would be inserted on this screen, resulting in the display of Figure 8-11.

AICPA CODE OF PROFESSIONAL CONDUCT

A distinguishing mark of any profession is the establishment and acceptance of a code of professional conduct. Such a code outlines a minimum level of conduct that is mandatory and enforceable upon its membership. A code of ethics emphasizes both the profession's responsibility to the public as well as to colleagues. Every CPA in the practice of public accounting has the responsibility to follow the AICPA Code of Professional Conduct and its applicability to audit, tax, and consulting services.

QUICK FACTS

The AICPA Code of Professional Conduct includes enforceable rules.

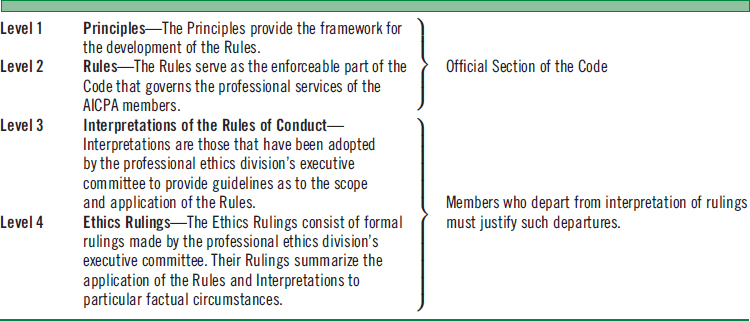

The AICPA Code of Professional Conduct consists of principles, rules, interpretations, and ethics rulings. The principles serve as the basic framework for the rules. The rules are mandatory and enforceable. Periodically, the Professional Ethics division of the AICPA issues ethics rulings and interpretations for the purpose of clarifying the Code. The interpretations render guidance to the accountant as to the scope and applicability of the rules. Ethics rulings help to clarify specific situations confronted by the accountant. The hierarchy of AICPA principles, rules, interpretations, and ethics rulings are depicted in Figure 8-12.

FIGURE 8-8 AICPA ONLINE PUBLICATIONS SCREEN

Departure from the rules may result in disciplinary action, unless the accountant can justify the departure under the circumstances. Disciplinary action may lead to suspension or termination of AICPA membership. Furthermore, a violation of professional conduct may result in revocation of a CPA certificate or license to practice by a state board of accountancy. In many cases, the revocation is also sanctioned by the SEC for auditors of public companies.

Although the AICPA Code of Professional Conduct applies to all members, certain rules are specifically applicable to the independent auditor. Rule 202 requires compliance with professional standards and is stated as follows:

Rule 202—Compliance with standards. A member who performs auditing, review, compilation, management consulting, tax, or other professional services shall comply with standards promulgated by bodies designated by Council.4

FIGURE 8-9 AICPA PROFESSIONAL STANDARDS SCREEN

Rule 203 generally prohibits the auditor from expressing an opinion that financial statements are in conformity with GAAP if the statements contain any departure from the official pronouncements of the FASB, its predecessors, the GASB, and the IASB for international accounting standards. Rule 203 is stated as follows:

Rule 203—Accounting principles. A member shall not (1) express an opinion or state affirmatively that the financial statements or other financial data of any entity are presented in conformity with generally accepted accounting principles or (2) state that he or she is not aware of any material modifications that should be made to such statements or data in order for them to be in conformity with generally accepted accounting principles, if such statements contain any departure from an accounting principle promulgated by bodies designated by Council to establish such principles that has a material effect on the statements taken as a whole. If, however, the statements or data contain such a departure and the member can demonstrate that due to unusual circumstances the financial statements would otherwise have been misleading, the member can comply with the rule by describing the departure, its approximate effects, if practicable, and the reasons why compliance with the principle would result in a misleading statement.5

As noted in the previous two rules, it is important to emphasize that the CPA must comply with GAAS or PCAOB standards and have familiarity with GAAP when expressing an audit opinion. Therefore, the practitioner should master the research methodology in order to determine if the audit is in compliance with GAAS and the entity is following GAAP.

QUICK FACTS

An audit opinion requires the CPA to comply with GAAS or PCAOB standards and review GAAP.

Rule 203 was clarified with the issuance of the following interpretations:

Interpretations under Rule 203—Accounting principles: 203-1—Departures from established accounting principles. Rule 203 was adopted to require compliance with accounting principles promulgated by the body designated by Council to establish such principles. There is a strong presumption that adherence to officially established accounting principles would in nearly all instances result in financial statements that are not misleading.

However, in the establishment of accounting principles, it is difficult to anticipate all of the circumstances to which such principles might be applied. This rule therefore recognizes that, upon occasion, there may be unusual circumstances where the literal application of pronouncements on accounting principles would have the effect of rendering financial statements misleading. In such cases, the proper accounting treatment is that which will render the financial statements not misleading.

QUICK FACTS

Interpretation of the AICPA Rules of Conduct provides guidelines as to the scope and application of the rules.

FIGURE 8-11 AICPA AUDITING STANDARDS SEARCH REQUEST

FIGURE 8-12 HIERARCHY OF THE AICPA CODE OF pROFESSIONAL CONDUCT

The question of what constitutes unusual circumstances as referred to in Rule 203 is a matter of professional judgment involving the ability to support the position that adherence to a promulgated principle would be regarded generally by reasonable men as producing a misleading result.

Examples of events that may justify departures from a principle are new legislation or the evolution of a new form of business transaction. An unusual degree of materiality or the existence of conflicting industry practices are examples of circumstances that do not ordinarily qualify as unusual in the context of Rule 203.

AUDITING STANDARDS IN THE PUBLIC SECTOR

Government officials and the general public are concerned about how the public's money was spent and whether government is achieving its goals funded by taxpayer dollars. Thus, to a large degree, the standards and guidelines used in a governmental audit are similar to auditing requirements in the corporate sector. Federal, state, and local governments have historically placed substantial reliance on the auditing requirements of the AICPA's Auditing Standards division. However, various governmental regulatory bodies have addressed specific governmental audit concerns.

The GAO's Government Auditing Standards (Yellow Book) are applicable to all governmental organizations, programs, activities, and functions. Government auditing standards have the objective of improving the quality of governmental audits at the federal, state, and local levels. These governmental standards were founded on the premise that governmental accountability should go beyond identifying the amount of funds spent in order to measure the manner and effectiveness of the expenditures. Therefore, these standards provide for an audit scope to include financial and compliance auditing as well as auditing for economy, efficiency, and effectiveness of program results. Under federal legislation, federal inspector generals must follow these GAO auditing standards. Also, these standards are audit criteria for federal executive departments and agencies.

QUICK FACTS

Use the Yellow Book to guide your governmental audits.

Currently, three audit levels affect governments. The first level consists of the GAAS issued by the AICPA. Building upon the AICPA standards are the Government Auditing Standards and federal audit requirements. The Government Auditing Standards, considered add-ons to GAAS, are also known as generally accepted government auditing standards (GAGAS), promulgated under the auspices of the GAO by the GASAB. The federal requirements are found in the OMB Circular A-133, Audits of States, Local Governments, and Nonprofit Organizations.

The GAO recognizes other sets of professional auditing standards under GAGAS § 1.15. AICPA fieldwork and reporting standards are incorporated by reference for financial statement audits. PCAOB and IAASB auditing standards are used in conjunction with GAGAS for financial statement audits. The Institute of Internal Auditors' standards are used in conjunction with GAGAS for performance audits.

Other major audit guidelines for nonprofit organizations are listed in Figure 8-13. The issuance of the Single Audit Act of 1984 (Public Law 98–502) was particularly important because it incorporated the concept of an entity-wide financial and compliance single audit. This act requires an annual audit of any state or local government unit that receives federal financial assistance. The single audit concept eliminated the need for separate financial and compliance audits conducted by the various federal agencies from whom the entity has received funding. By congressional directive, the director of the Office of Management and Budget (OMB) has the authority to establish policy, guidelines, and mechanisms to implement single, coordinated financial and compliance audits of government grant recipients.

QUICK FACTS

Three audit levels affecting government audits are from the GAO, OMB, and the AICPA.

FIGURE 8-13 MAJOR GUIDELINES FOR PUBLIC SECTOR AUDITING

INTERNATIONAL AUDITING STANDARDS

The International Federation of Accountants (IFAC) has had a broad objective to develop a worldwide accounting profession with harmonized standards. To meet the objective relating to auditing standards, the IFAC initially established the International Auditing Practices Committee to develop and issue International Standards on Auditing (ISA) on the form and content of audit reports.

The purpose of the ISA is to improve the uniformity of auditing practices throughout the world. Additionally, the IAPC issues International Auditing Practice Statements (IAPSs) that provide practical assistance in implementing the international standards, but do not have the authority of the international standards. In 2002, IFAC created a new International Auditing and Assurance Standards Board (IAASB) that now has the responsibility of developing international auditing standards. More recently, a Public Interest Oversight Board was created to review the IAASB.

The ISAs apply to every independent audit of financial information, regardless of the type or size of the entity under audit. However, within each country, local regulations govern. To the extent that the ISAs conform to the specific country's regulations, the audit will be considered in accordance with the standards. In the event that the regulations differ, the members of the IAASB will work toward the implementation of the ISAs, if practicable, within the specific country. These standards and other publications of the IAASB are available at www.ifac.org.

Moving forward with auditing standard setting, there exists a movement for standards convergence similar to the convergence to IFRS. The GAO's position on auditing standards convergence is that standard setters should work together to achieve core auditing standards that are universally accepted. Where there is a clear and compelling reason, the individual standard-setting bodies should develop additional standards necessary to meet the needs of their respective constituencies. The nature of any differences from core auditing standards and the basis for the differences also should be communicated. The GAO is working with the International Organization of Supreme Audit Institutions (INTOSAI) to advance government auditing standards in the international arena.

The official position of the ASB on convergence is that it will develop standards (SAS) using the ISAs as the base standard and modify the base standard only where modifications are deemed necessary to better serve the needs of U.S. users of audited financial statements of nonissuers. Currently, the ASB has a process to converge its standards with those of the IAASB and redraft them using a clarity convention.

COMPILATION AND REVIEW SERVICES

In response to the needs of nonpublic clients,6 regulatory agencies, and the investing public, the public accounting profession offers compilation or review services to clients rather than conducting a more expensive audit examination in accordance with GAAS. Compilation and review of financial statements are defined as follows:

Compilation: a service presenting, in the form of financial statements, information that is the representation of management without undertaking to express any assurance on the statements.

Review: a service performing inquiry and analytical procedures that provide the accountant with a reasonable basis for expressing limited assurance that there are no material modifications that should be made to the statements in order for them to be in conformity with GAAP or, if applicable, with another comprehensive basis of accounting.7

Therefore, the basic distinction between these two services is that a review service provides limited assurance about the reliability of unaudited financial data presented by management, whereas a compilation engagement provides no assurance as to the reliability of the data. In a compilation, the CPA prepares financial statements only from information supplied by management. The CPA in a compilation need not verify this information furnished by the client and therefore provides no assurance regarding the validity of this information.

The AICPA established guidance for the public accountant for compilation and review services with the issuance of Statements on Standards for Accounting and Review Services (SSARS). To date, the committee has issued seventeen statements.

QUICK FACTS

For reviews, use AICPA Statements on Standards for Accounting and Review Services.

ROLE OF JUDGMENT IN ACCOUNTING AND AUDITING

Accountants and auditors exercise professional judgment in considering whether the substance of business transactions differs from its form, in evaluating the adequacy of disclosure, in assessing the probable impact of future events, and in determining materiality limits. This informed judgment on the part of the practitioner is the foundation of the accounting profession. In providing an attest engagement, the result is often the rendering of a considered opinion or principled judgment. In effect, the auditor gathers relevant and reliable information, evaluates and judges its contents, and then formalizes an opinion on the financial information or statements.

A review of current authoritative literature reveals that certain pronouncements require disclosure on the applicable accounting principle for a given business transaction. Other pronouncements provide only general guidelines and, in some cases, suggest acceptable alternative principles. The process of applying professional judgment in choosing among alternatives is not carried out in isolation, but through consultation with other professionals knowledgeable in the area. In rendering professional judgment, the accountant/auditor must exercise critical thinking skills in the development of a solution or opinion.

QUICK FACTS

Disclosure of accountancy principles varies depending on the authority and accounting judgment.

Statement on Auditing Standards No. 5 makes the following point on the use of professional judgment in determining conformity with GAAP:

The auditor's opinion that financial statements present fairly an entity's financial position, results of operations, and changes in financial position in conformity with generally accepted accounting principles should be based on his judgment as to whether

(a) the accounting principles selected and applied have general acceptance;

(b) the accounting principles are appropriate in the circumstances;

(c) the financial statements, including the related notes, are informative of matters that may affect their use, understanding, and interpretation;

(d) the information presented in the financial statements is classified and summarized in a reasonable manner; that is, neither too detailed nor too condensed; and

(e) the financial statements reflect the underlying events and transactions in a manner that presents the financial position, results of operations, and changes in financial position stated within a range of acceptable limits; that is, limits that are reasonable and practicable to attain in financial statements.8

In order to render an opinion based upon professional judgment, the auditor often considers the opinions of other professionals. In such cases, the practitioner can use several published sources to determine how others have dealt with specific accounting and reporting applications of GAAP. The AICPA publishes Technical Practice Aids, which contains the Technical Information Service. This service consists of inquiries and replies that describe an actual problem that was encountered in practice and the interpretation and recommendations that were provided along with relevant standards and other authoritative sources.

ECONOMIC CONSEQUENCES

Because time is a scarce commodity, the auditor should weigh the cost-benefit trade-offs in extending the audit research process. The researcher should address the problem until eliminating all reasonable doubt relating to the issue, recognizing the hidden costs of making an improper audit decision.

Enforcement of professional audit work occurs at many levels. Quality control reviews are expected within a CPA firm. Peer reviews are conducted by other firms. The PCAOB conducts inspections of CPA firms. The inspections are generally used for the enhancement of the audit process, but also used for PCAOB enforcement sanctions. Audit quality has increased because of PCAOB inspection reports. The SEC can still issue an Accounting and Auditing Enforcement Release on a CPA firm. Litigation results in a review of audit quality. Besides the legal damages from an association with a negligent audit, the auditor can face criminal penalties; SEC, FTC, and other government sanctions; loss of reputation among the auditor's peers; and a significant loss of existing clients in a competitive environment.

If sloppy audit work is revealed to the public through failures of major corporations or investment vehicles, pressure is placed on Congress to change the audit environment, as happened under Sarbanes-Oxley. As congressional and other investigations continue in financial reform, only time will reveal the effects upon the audit environment.

SUMMARY

This chapter has presented an overview of assurance services, the auditing standard-setting environment, standards for international audits, compilation and review services, and professional ethics. Familiarity with this information, in particular the types of authoritative pronouncements that exist, will aid the practitioner in the research process.

In researching an accounting or assurance services issue, the practitioner must use professional judgment in the decision-making process. Experience is undoubtedly the primary factor in developing good professional judgment. However, this text presents a research methodology that should aid in the development and application of professional judgment.

DISCUSSION QUESTIONS

- What is an assurance service engagement?

- Define an attest engagement. Is an audit engagement an attest service?

- Identify three other attest services in addition to the normal financial statement audit.

- Differentiate between auditing standards and attestation standards.

- What guidelines exist for the performance of accounting and review services?

- Differentiate between auditing standards and auditing procedures.

- Discuss the relationship between GAAS and Statements on Auditing Standards (SAS).

- Discuss the applicability of the first and third general standards of GAAS to accounting and auditing research.

- What is the PCAOB? What standards does it issue?

- State the objective of the Single Audit Act. When is this act applicable?

- List the primary auditing guidelines for public sector auditing.

- Explain the importance of the Code of Professional Conduct in the performance of an audit.

- Explain the significance of Rules 202 and 203 of the AICPA Code of Professional Conduct.

- How may accounting or auditing research aid the practitioner in complying with Rules 202 and 203 of the Code of Professional Conduct?

- What role does professional judgment play in the daily activities of the accountant or auditor?

- What authoritative auditing literature that has general applicability in practice is considered primary authoritative support?

- What guidelines are available for the accountant in serving the needs of the nonpublic client?

- What authoritative body exists as to the development of international auditing standards?

EXERCISES

1. Access the International Federation of Accountants Web site (www.ifac.org) and briefly describe the following two International Auditing Standards: ISA 500 and ISA 505.

2. Utilizing Figure 2-3 (Universal Elements of Reasoning), identify the eight elements for the following: A prospective client has requested a report as to the reliability of its electronic commerce activities on the Internet. You are trying to decide the type of assurance service engagement this would involve.

3. Access the AICPA Professionals Standards and determine the AU section number that discusses the forms of confirmations.

4. Access the AICPA Professional Standards. In the By-laws section, determine the requirements for becoming a member of the AICPA.

5. Utilizing the AICPA Professional Standards database, conduct research to answer the following questions:

- In addition to completing the audit of Jack's Manufacturing, Inc., for the coming year, your firm has been requested to review the interim financial statements for the first three quarters of the year. The engagement partner has requested your assistance in preparing a draft of the appropriate report for the review. Locate and print out an example of an appropriate review report.

- You are the staff auditor for a large client that has two subsidiaries located in foreign countries. Because your firm does not have offices near these subsidiaries, your firm will be using other auditors to aid you in the audit of the parent company. The audit partner on the engagement has requested your assistance as to the type of audit report necessary in order to share responsibility with these other auditors. Identify the authoritative literature paragraph citation for a shared audit report and print out an example of the report for the partner.

6. Access the AICPA Web site (www.aicpa.org) and locate the ASB under auditing and attestation standards. Examine the approved highlights of the ASB. What were the last three auditing standards issued by the ASB?

7. Access the PCAOB Web site (www.pcaobus.org) and list two new or proposed auditing standards issued by the PCAOB.

AICPA reSOURCE Database

If you have access to the AICPA reSOURCE database, attempt to complete the following practice exercises. (Note: You can also complete these exercises with a hard copy of the AICPA Professional Standards.)

8. You have been requested by a potential client to conduct an agreed upon procedures engagement related to the client's pension plan. Access the AICPA database and determine what type of service this is: audit, attestation, or consulting engagement. Also identify the specific standard governing this type of service.

9. When is it appropriate to issue an adverse audit opinion? Cite the specific Professional Standard section used for your answer.

10. Utilize the AICPA database to answer the following issue brought to you by a co-worker. The co-worker believes that only the general standards of the AICPA Code of Professional Conduct apply to consulting engagements. Are there any other general standards that apply to a consulting engagement in addition to the general standards of the Code?

APPENDIX

CPA Exam Audit Simulation

As previously stated, the CPA exam has simulations in the auditing section of the exam. In conducting research in these simulations, one will be utilizing the AICPA Professional Standards, as depicted in Figure 8-9. A CPA candidate needs to be proficient in using this database. Figure 8-1A provides an example of a question in the opening screen of a sample simulation. Clicking on the research/authoritative literature tab will open up the Professional Standards to conduct your research.

FIGURE A8-1 SIMULATION RESEARCH SCREEN FOR AUDITING AND ATTESTATION

1 AICPA Professional Standards, vol. 2, Section CS-100.05.

2 AICPA Professional Standards, vol. 1, Section AT—Introduction.

3 AICPA Professional Standards, vol. 1, Section AT 100.01.

4 AICPA Professional Standards, vol. 2, Section ET-202.

5 AICPA Professional Standards, vol. 2, Section ET-203.

6 The distinction between a public versus nonpublic client is based on whether the entity's securities are traded publicly on a stock exchange or in the over-the-counter market.

7 AICPA, Accounting and Review Services Committee, Statement on Standards for Accounting and Review Services, No. 1, “Compilation and Review of Financial Statements” (1078).

8 AICPA Professional Standards, vol. 1, Section AU-411-04.