118 EMPIRICAL RESULTS

10

0

10

4

10

8

10

12

10

16

0 0.25

(a)

0.5

α

0.75 1

Total wealth achieved

OLMAR Market

BCRP

10

0

10

3

10

6

10

9

0

(b)

0.50.25 0.75 1

Total wealth achieved

α

OLMAR

Market

BCRP

10

0

10

1

10

2

10

3

0 0.25 0.5

(c)

0.75 1

Total wealth achieved

α

OLMAR Market

BCRP

OLMAR Market

BCRP

1

25

5

0

(d)

0.50.25 0.75 1

Total wealth achieved

α

00.25

(e)

α

0.5 0.75 1

OLMAR Market

BCRP

25

5

Total wealth achieved

1

1

2

3

0

(f)

0.25 0.5 0.75 1

Total wealth achieved

α

OLMAR Market

BCRP

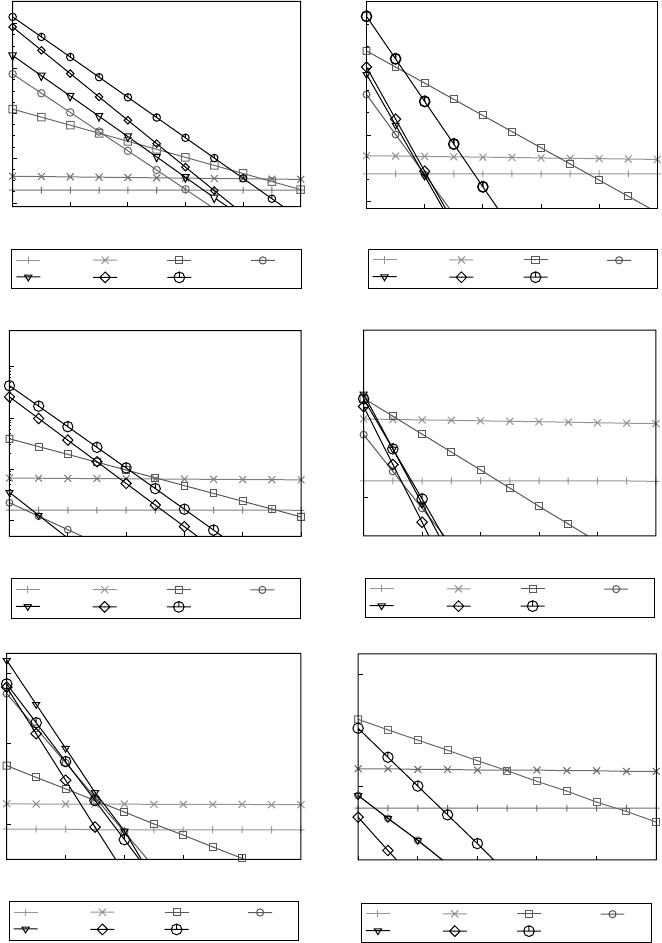

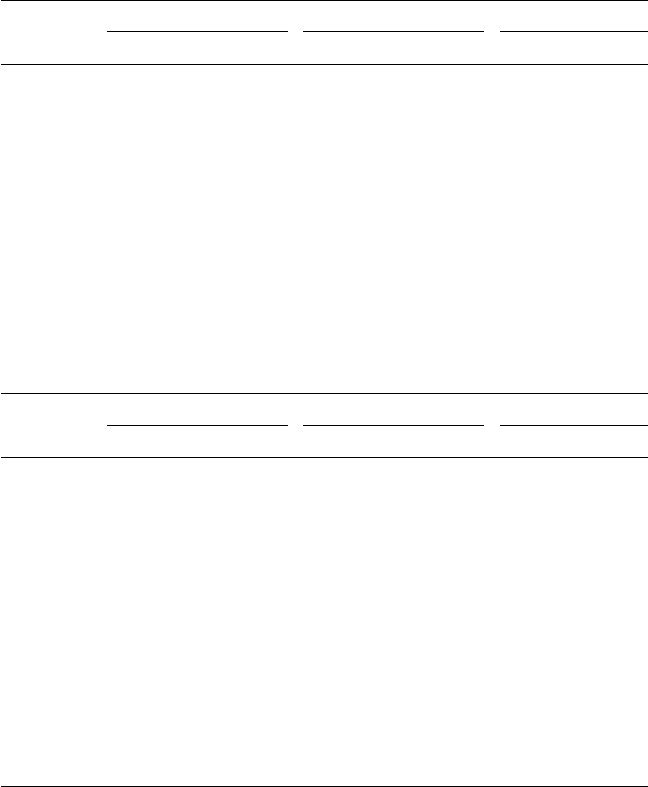

Figure 13.10 Parameter sensitivity of OLMAR-2 with respect to α with fixed ( = 10):

(a) NYSE (O); (b) NYSE (N); (c) TSE; (d) SP500; (e) MSCI; and (f) DJIA.

First, the transaction cost is an important and unavoidable issue that should be

addressed in practice. To test the effects of transaction cost on the proposed strategies,

we adopt the proportional transaction cost model stated in Section 2.2. Figure 13.11

depicts the effects of proportional transaction cost when the algorithms are applied

on the six datasets, where the transaction cost rate γ varies from 0% to 1%. We

present only the results achieved by three representative algorithms (CORN, PAMR,

T&F Cat #K23731 — K23731_C013 — page 118 — 9/28/2015 — 21:35

EXPERIMENT 4 119

10

0

10

4

10

8

10

12

10

16

0 0.2 0.4 0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

(a)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

10

9

10

6

10

3

10

0

0 0.2 0.4 0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

(b)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

10

3

10

2

10

1

10

0

0 0.2 0.4 0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

(c)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

1

5

20

0

0.2 0.4

(d)

0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

1

5

20

0 0.2 0.4 0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

(e)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

1

2

4

0 0.2 0.4

(f)

0.6 0.8 1

Total wealth achieved

Transaction costs (γ%)

Β

ΝΝ

Market

CORN

BCRP

PAMR

Anticor

OLMAR

Figure 13.11 Scalability of the proposed strategies with respect to the transaction cost rate (γ):

(a) NYSE (O); (b) NYSE (N); (c) TSE; (d) SP500; (e) MSCI; and (f) DJIA.

T&F Cat #K23731 — K23731_C013 — page 119 — 9/28/2015 — 21:35

120 EMPIRICAL RESULTS

and OLMAR) and ignore the results of CWMR, whose curves often overlap that

of PAMR. For comparison, we also plot the results achieved by two state-of-the-art

strategies (Anticor and B

NN

) and two benchmarks (BCRP and Market). Since most

follow the winner approaches try to approach BCRP, we ignore their figures.

From the figures, we can observe that the proposed algorithms can withstand

reasonable transaction cost rates, on most datasets. For example, the break-even rates

with respect to the market index vary from 0.2% to 0.8%, except DJIA, on which only

OLMAR can withstand around 0.3%. As CORN and PAMR/CWMR fail to beat the

markets on the DJIA dataset without transaction costs, their failures with transaction

costs can be naturally expected. On the other hand, the behaviors of the proposed

algorithms diverge. With a similar pattern-matching principle, CORN often performs

similar to B

NN

, while both of them generally underperform the mean reversion algo-

rithms. Since the three mean reversion algorithms (PAMR, CWMR, and OLMAR)

revert to the mean more actively than Anticor and thus result in more drastic portfolio

rebalances, they surpass Anticor with low or medium transaction costs and underper-

form Anticor with high transaction costs. Note that the transaction cost rate in the

real market is low

∗

; thus, the results clearly indicate the practical applicability of the

proposed strategies even when we consider reasonable transaction costs.

Second, margin buying is another practical concern for a real-world portfo-

lio selection task. To evaluate the impact of margin buying, we adopt the model

described in Section 2.2 and present the cumulative wealth achieved by the com-

peting approaches with or without margin buying in Table 13.3. The results clearly

show that if margin buying is allowed, the profitability of the proposed algorithms

on most datasets increases. Similar to the results without margin buying, certain pro-

posed algorithms often achieve the best results with margin buying. In summary, the

proposed strategies can be extended to handle the margin-buying issue and benefit

from it, and thus are practically applicable.

13.5 Experiment 5: Evaluation of Computational Time

Our next experiment is to evaluate the computational time costs of different

approaches, which is also an important issue in developing a practical trading strategy.

As previously analyzed, CORN has a batch-learning step on each period and is time

consuming in both its sample selection step and portfolio optimization step,

†

while

PAMR, CWMR, and OLMAR are online learning algorithms and cost linear time

per iteration. Table 13.4 presents the computational time cost (in seconds) of three

performance-comparable approaches (Anticor, B

K

, and B

NN

) on the six datasets. All

the experiments were conducted on an Intel Core 2 Quad 2.66 GHz processor with

4 GB RAM, using MATLAB

2009b on Windows XP.

‡

∗

For example, without considering taxesand bid–ask, Interactive Broker(www.interactivebrokers.com)

charges $0.005 per share. Since the average price of Dow Jones Composites is around $50.00 (as of June

2011), the transaction cost rate is about 0.01%.

†

In its MATLAB implementation, the latter step costs more than 80% of the total time.

‡

We use MATLAB function tic/toc to measure the time. There are preprocessing (such as data loader,

variable initialization, etc.) and postprocessing (such as result analysis, etc.), whose time is all excluded

from the time statistics in Table 13.4.

T&F Cat #K23731 — K23731_C013 — page 120 — 9/28/2015 — 21:35

EXPERIMENT 5 121

Table 13.3 Cumulative wealth achieved by various strategies on the six datasets without and

with margin loans (MLs)

NYSE (O) NYSE (N) TSE

Algorithms No ML With ML No ML With ML No ML With ML

Market 14.50 15.75 18.06 17.68 1.61 1.71

Best-stock 54.14 54.14 83.51 173.18 6.28 10.53

BCRP 250.6 3755.09 120.32 893.63 6.78 21.23

UP 27.41 62.99 31.49 57.03 1.60 1.69

EG 27.09 63.28 31.00 55.55 1.59 1.68

ONS 109.19 517.21 21.59 228.37 1.62 0.88

Anticor 2.41E+08 1.05E+15 6.21E+06 5.41E+09 39.36 18.69

B

K

1.08E+09 6.29E+15 4.64E+03 3.72E+06 1.62 1.53

B

NN

3.35E+11 3.17E+20 6.80E+04 5.58E+07 2.27 2.17

CORN 1.48E+13 6.59E+25 5.37E+05 7.31E+07 3.56 5.00

PAMR 5.14+15 5.57E+25 1.25E+06 1.12E+09 264.86 720.42

CWMR 6.49E+15 6.59E+25 1.41E+06 7.31E+07 332.62 172.36

OLMAR 3.68E+16 5.67E+30 2.54E+08 1.73E+12 424.80 31.63

SP500 MSCI DJIA

Algorithms No ML With ML No ML With ML No ML With ML

Market 1.34 1.03 0.91 0.69 0.76 0.59

Best-stock 3.78 3.78 1.50 1.50 1.19 1.19

BCRP 4.07 6.48 1.51 1.54 1.24 1.24

UP 1.62 1.75 0.92 0.71 0.81 0.66

EG 1.63 1.70 0.93 0.72 0.81 0.65

ONS 3.34 7.76 0.86 0.33 1.53 2.21

Anticor 5.89 10.73 3.22 3.40 2.29 2.89

B

K

2.24 1.88 2.64 6.56 0.68 0.56

B

NN

3.07 3.29 14.47 150.49 0.88 0.67

CORN 6.35 14.59 26.10 835.08 0.84 0.55

PAMR 5.09 15.91 15.23 68.83 0.68 0.84

CWMR 5.90 23.50 17.28 76.29 0.68 0.88

OLMAR 5.83 5.60 16.39 57.79 2.12 1.46

From the results, we can clearly see that CORN and the state-of-the-art algorithms

have high costs, and in all cases the proposed PAMR, CWMR, and OLMAR take

significantly less computational time than others. Even though the computational

time in daily back-tests, especially per trading day, is small, it is important in certain

scenarios such as high-frequency trading (Aldridge 2010), where transactions may

occur in fractions of a second. Nevertheless, the results obviously demonstrate the

computational efficiency of three proposed mean reversion strategies, which further

enhances their real-world large-scale applicability.

T&F Cat #K23731 — K23731_C013 — page 121 — 9/28/2015 — 21:35

122 EMPIRICAL RESULTS

Table 13.4 Computational time cost (in seconds) on the six real datasets

Algorithms NYSE (O) NYSE (N) TSE SP500 MSCI DJIA

Anticor 2.57E+03 1.93E+03 2.15E+03 387 306 175

B

K

7.89E+04 5.78E+04 6.35E+03 1.95E+03 2.60E+03 802

B

NN

4.93E+04 3.39E+04 1.32E+03 2.91E+03 2.55E+03 1.28E+03

CORN 8.78E+03 1.03E+04 1.59E+03 563 444 172

PAMR 8 7 2 1.1 1.0 0.3

CWMR 12 11 3 1.4 1.3 0.5

OLMAR 4 3 0.7 0.6 0.5 0.3

13.6 Experiment 6: Descriptive Analysis of Assets and Portfolios

Existing experiments on related studies (refer to Experiments 1 to 5) focus on com-

paring different algorithms based on various preceding aspects. In this section, we

perform a preliminary analysis of the behaviors of asset returns and portfolios, which

may reflect some insights into future study. While the analysis on different datasets is

similar, we focus on the standard benchmark dataset, NYSE (O) (Cover 1991).

∗

We

also append the data statistics and top five average allocations of our strategies and

the state-of-the-art algorithms on other datasets,

†

such as Appendix C.

Before analyzing their portfolios, we list some descriptive statistics on NYSE (O),

including each asset’s cumulative return over the whole periods, their (arithmetic)

return mean and standard deviation, and their autocorrelation with lag 1, in Table 13.5.

Then, we plot some representative approaches’ mean weights and standard devi-

ations in Figure 13.12, and list the top five average weights in Table 13.6. First, let

us analyze the BCRP strategy, whose portfolio has the same weights for every period

and thus has zero standard deviation. BCRP is essentially different from the best stock

strategy (asset #30), as the weight on the stock is zero. Interestingly, BCRP focuses

on the five most volatile stocks (refer to the highest Std values in Table 13.5), which

means that the portfolio selections are undiversified and verifies the “volatility pump-

ing” (Luenberger 1998) nature. Even though asset #23 does not perform as good as

most assets, its high volatility makes it the second weighted asset. This shows that

exploiting volatile stocks, even though some of them may perform poorly, can give

good performance.

For both EG and ONS, their portfolios have much lower volatility than other

strategies. In particular, EG’s portfolios always slightly drift around the initial uni-

form portfolio (for NYSE (O),

1

36

1). Such a phenomenon can be explained by its

learning rate (λ > 0), which has to be small such that the algorithm is universal.

However, decreasing the learning rate (λ → 0) ultimately approaches the algorithm

to uniform CRP.

‡

Our observation on EG’s portfolios verifies the previous analysis

on its parameter, in Section 4.2.

∗

Due to the table constraints, we use indices to represent individual assets, whose symbols are available

at http://stevenhoi.org/olps

†

We ignore TSE, which has too much assets (m =88) to show.

‡

Uniform CRP will be constant at uniform portfolio. This is approachable but not achievable as λ > 0.

T&F Cat #K23731 — K23731_C013 — page 122 — 9/28/2015 — 21:35

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.