Often, more detail relating to amounts shown in the financial statements is provided in the notes to the financial statements and/or other supplementary disclosures, in order to provide users with more useful information. Disclosure issues involving accounting policies, illegal acts, segmented reporting, and interim reporting are discussed in this chapter. Other measurement issues, including related-party transactions and subsequent events, are also discussed in this chapter. An overview of financial statement analysis techniques, including ratio analysis and percentage (common-size) analysis, is also provided in this chapter, with an emphasis on examining the relationships between items on the financial statements and identifying trends in these relationships.

STUDY STEPS

Understanding the Importance of Disclosures

The full disclosure principle requires that any financial facts that are significant enough to influence the judgement of an informed reader should be reported. This is a very broad guideline, and therefore professional judgement is required in applying it. More disclosure is generally better than less disclosure; for example, if the financial statements contain unexpected results or events, more disclosure of the related transactions is preferred. However, the full disclosure principle does provide that if a financial fact is not significant enough to influence the judgement of an informed reader, it need not be reported.

Disclosure requirements, especially for public companies, have increased substantially. Accounting standard-setting bodies have issued many disclosure-related standards in the recent past, due to the increasing complexity of business transactions and increasing necessity for timely information. As well, other regulatory bodies (such as securities exchange commissions) have become involved in financial reporting by mandating their own disclosures that must be included in the financial statements of any company whose shares are listed on a stock exchange.

A financial statement user should never analyze financial statements without reading the notes to the financial statements. The notes are considered part of a basic set of financial statements and often incorporate additional valuable information. However, it is important to note that note disclosure is not a substitute for proper financial statement presentation.

Accounting errors are unintentional mistakes, whereas irregularities are intentional misstatements of financial information. If errors or irregularities are discovered, they should be corrected in the financial statements. If irregularities and/or illegal acts are discovered, the accountant or auditor must also evaluate the adequacy of related disclosures in the financial statements and assess whether the related item(s) should be recognized in the statement of financial position and/or the income statement.

Accounting policies

A key financial statement note is the note disclosing the entity's accounting policies, which are the specific accounting principles and methods that are currently used and considered most appropriate to present the entity's financial statements fairly. All significant accounting policies should be disclosed in this note, especially those that were selected from among different policies. This note is usually the first note to the financial statements, and is sometimes presented before the financial statements to encourage users to read it first.

Segmented reporting

Segmented reporting is not addressed by ASPE. However, under IFRS, separate information is required to be presented for reportable segments including information about each segment's revenues, profits and loss, and assets and liabilities. A reportable segment is a significant operating segment. Operating segments and reportable segments, and their related disclosures, are discussed further in the Solution to Case 23-2. Segmented reporting is required under IFRS because different operating segments in an enterprise are often exposed to different business risks.

Interim reporting

Interim financial reports cover periods of less than one year. Interim reporting is also not addressed by ASPE, and IFRS does not mandate that entities should provide interim reports. However, IFRS does provide guidance for interim reporting, which entities are encouraged to follow if interim financial reports are prepared. In general, IFRS recommends that each interim period be considered a discrete (separate) period and that deferrals and accruals follow the same principles that are used for annual reports. Interim reporting is discussed further in the Solution to Case 23-3.

Understanding the Significance of Other Measurement Issues

Related-party transactions

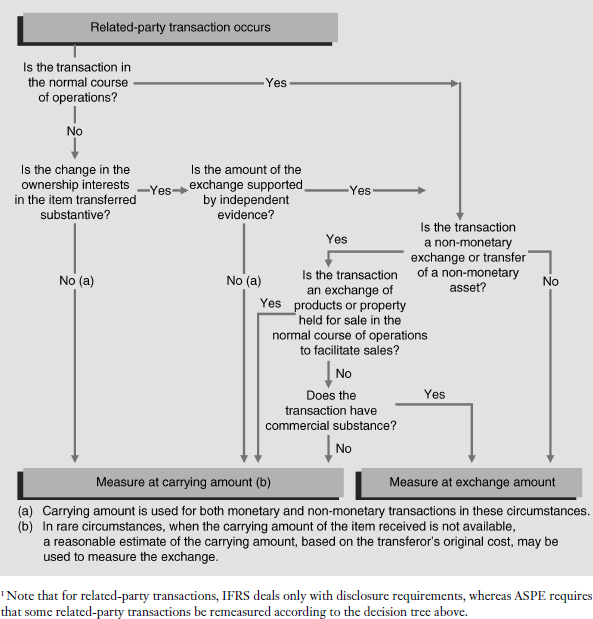

A related-party transaction arises when an enterprise engages in a transaction in which one of the transacting parties has the ability to significantly influence the policies of the other, or in which a non-transacting party has the ability to significantly influence the policies of the two transacting parties. Related-party transactions must be analyzed carefully because they are not necessarily based on arm's-length exchange values, terms, and/or conditions. Under both IFRS and ASPE, related-party transactions should be disclosed so that users are informed of the transactions, their accounting treatment, and their effect on the financial statements.

Under ASPE, certain related-party transactions that are (1) not in the normal course of business; (2) without substantive change in ownership; and/or (3) exchanged at an amount that is not supported by independent evidence, are remeasured to the carrying amount of the underlying assets or services that were exchanged. In recording these transactions at carrying amount (the amount of the item transferred as recorded on the books of the transferor), no gain or loss is recorded on the exchange, and any difference between the carrying amounts of the items exchanged is booked directly to equity.

The following disclosures are recommended for related-party transactions:

- the nature of the relationships involved

- a description of the transactions

- the recorded amounts of transactions

- the measurement basis that was used

- amounts due from or to related parties and the related terms and conditions

- contractual obligations with related parties

- contingencies involving related parties

- under IFRS, management compensation and the name of the entity's parent company as well as its ultimate controlling entity or individual

See Illustration 23-1 for a summary of measurement issues.

Subsequent events

Subsequent events occur after the statement of financial position date, but before the financial statements are complete. Under IFRS, the date the financial statements are complete is the date the financial statements are considered authorized for issue. Under ASPE, the date the financial statements are complete is a matter of professional judgement, taking into account management structure and procedures followed in completing the financial statements.

Subsequent events that provide additional evidence about conditions that existed at the statement of financial position date, and affect the estimates used in preparing financial statements, should be adjusted (reflected) in the financial statements.

Subsequent events that provide evidence about conditions that did not exist at the statement of financial position date but arose subsequent to that date do not require adjustment of the financial statements. However, they may have to be disclosed in order to prevent the financial statements from being misleading.

Understanding the Auditor's Report

An independent auditor is an accounting professional who conducts an independent examination of the accounting data presented by an entity, and expresses an opinion as to the fairness of the entity's financial statements in presenting the financial position, results of operations, and cash flows of the entity in accordance with generally accepted accounting principles.

In most cases, the auditor issues a standard unqualified (or clean) opinion. However, in some situations, the auditor is required to express a qualified opinion, which contains an exception to the standard unqualified opinion. A qualified opinion is issued in situations where, except for the effects of the matter related to the qualification, the financial statements present fairly, in all material respects, the financial position, results of operations, and cash flows in conformity with generally accepted accounting principles. The auditor is required to express an adverse opinion in situations where the exceptions to fair presentation in the financial statements are so pervasive that, in the independent auditor's judgement, a qualified opinion is not justified.

Overview of Financial Statement Analysis

Relationships between the amounts presented in financial statements may be analyzed to help identify strengths, weaknesses, and possible trends in the entity's financial position, results of operations, and cash flows.

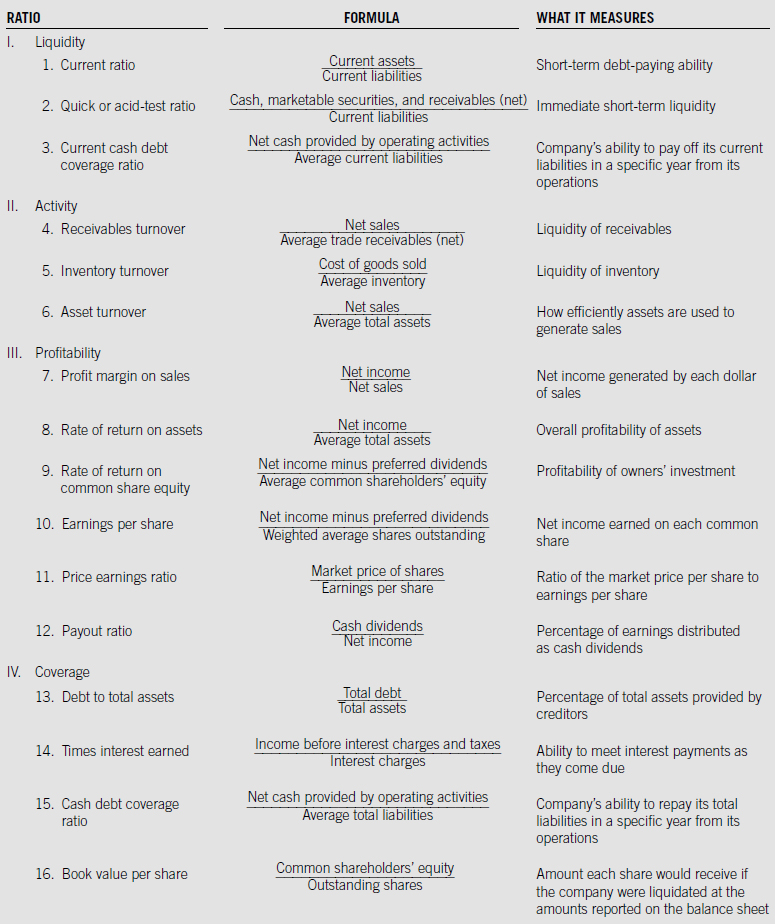

Ratio analysis begins with an expression of the relationship between two numbers from the financial statements, and facilitates a more in-depth analysis of the entity's financial position and performance, including comparison of the company's position and performance with those of its competitors in the same industry. Liquidity, activity, profitability, and coverage or solvency ratios are calculated to help analyze the entity's position and performance in each of these categories.

Percentage (common-size) analysis requires expression of each amount on a financial statement as a percentage of a particular base amount. For vertical percentage analysis, amounts on a statement of financial position are often expressed as a percentage of total assets, and amounts on an income statement are often expressed as a percentage of net sales. For horizontal percentage analysis, the change in an amount (the current year amount less the previous year amount) is expressed as a percentage of the previous year amount. Percentage (common-size) analysis facilitates analysis of the relative size of amounts in a given year's financial statement (vertical percentage analysis), and analysis of the entity's position and performance over time (horizontal percentage analysis).

TIPS ON CHAPTER TOPICS

- The first note to the financial statements should be a summary of significant accounting policies. This note disclosure should identify principles and methods applied by the entity that are: (1) selected from among different alternatives, (2) specific to the entity's industry, or (3) unusual or innovative applications. This note disclosure may precede the notes to the financial statements.

- Notes to the financial statements are an integral part of a set of basic financial statements.

- Related-party transactions require separate, detailed disclosures because transactions involving related parties cannot be presumed to be carried out on an arms'-length basis (because these transactions may not have been carried out under competitive, free-market conditions). The financial statements should reflect the economic substance of these transactions rather than the legal form.

- Subsequent events can be classified into two categories: those that provide additional evidence about conditions that existed at the statement of financial position date (commonly referred to as Type I subsequent events), and those that result from new information that financial statement users may find useful (commonly referred to as Type II subsequent events). Type I subsequent events require an adjustment to the financial statements, and Type II subsequent events would normally be disclosed in the notes to the financial statements. Note that some subsequent events may not fit into either category, and therefore would not be accrued or disclosed.

- In general, the same accounting principles used for the preparation of annual reports should be used in the preparation of interim reports. In preparing an interim report, an interim period is treated as a separate accounting period. Therefore, accruals and deferrals should follow the principles used for annual reports (accounting transactions should be recorded using accrual accounting).

- In preparing an interim report, income tax expense for the interim period is calculated using an annual estimated tax rate. Specifically, interim taxable income and temporary differences are estimated, and the estimated annual effective tax rate is applied, to arrive at an estimate of income tax expense for the interim period.

- Although ratio analysis and percentage (common-size) analysis are useful in helping to identify the strengths, weaknesses, and possible trends in the entity's position and performance, a deeper analysis of the entity's business environment, financial statements, and notes to the financial statements is required to better evaluate the entity's financial position, results of operations, and cash flows.

CASE 23-1

PURPOSE: This case will review the meaning or significance of a number of terms used in this chapter.

Instructions

Select the letter of the item that most directly relates to the numbered statements. Use the letter to identify your response.

(a) summary of significant accounting policies

(b) related-party transactions

(c) segmented reporting

(d) subsequent events

(e) errors

(f) interim reports

(g) full disclosure principle

(h) notes to the financial statements

(i) auditor's report

(j) management discussion and analysis

(k) financial statement analysis

(l) limitation of financial statement analysis

Solution to Case 23-1

- (g)

- (h)

- (a)

- (b)

- (e)

- (l)

- (c)

- (f)

- (j)

- (d)

- (i)

- (k)

CASE 23-2

PURPOSE: This case will review the tests applied in determining the reportable segments of an entity.

Diversified Galore Inc. has several reportable industry segments that account for 80% of its operations. Diversified Galore Inc. prepares financial statements in accordance with IFRS.

Instructions

(a) Explain the term “operating segment” as it applies to an entity diversified in its operations.

(b) Explain when information about two or more operating segments may be aggregated.

(c) Explain the criteria used to determine Diversified's reportable segments.

(d) Indicate what information is to be disclosed for each reportable segment.

Solution to Case 23-2

(a) An operating segment is a component of an enterprise that has all of the following characteristics:

- It engages in business activities from which it earns revenues and incurs expenses.

- Its operating results are regularly reviewed by the company's chief operating decision-maker to assess segment performance and allocate resources to the segment.

- There is discrete financial information is available for it.

(b) Information about two or more operating segments may only be aggregated if the segments have the same basic characteristics in all of the following areas:

- The nature of the products and services provided

- The nature of the production process

- The type or class of customer

- The methods of product or service distribution

- If applicable, the nature of the regulatory environment

(c) After an entity identifies its operating segments for possible disclosure, a quantitative materiality test is applied to determine whether each operating segment is significant enough to be a reportable segment (and therefore reported separately). An operating segment is regarded as significant, and therefore identified as reportable, if it satisfies one or more of the following quantitative thresholds:

- Its reporting revenue (including both sales to external customers and intersegment sales or transfers) is 10% or more of the combined revenue of all the enterprise's operating segments.

- The absolute amount of its reported profit or loss is 10% or more of the greater, in absolute amount, of:

- the combined operating profit of all operating segments that did not incur a loss, and

- the combined reported loss of all operating segments that did report a loss.

- Its assets are 10% or more of the combined assets of all operating segments.

In applying these tests, three additional factors must be considered:

- Segment data must explain a significant portion of the company's business. Specifically, the segmented results must equal or exceed 75% of the combined sales to unaffiliated customers for the entire enterprise. This test prevents a company from providing limited information on only a few segments and grouping the rest into one category.

- Entities are required to disclose at most 10 reportable segments.

- If an operating segment does not meet any of the tests but management believes separate information would be useful to users, then the segment may be presented separately.

(d) IFRS requires that an enterprise report the following:

- General information about its reportable segments. This includes factors that management considers most significant in determining the company's reportable segments, and the types of products and services from which each operating segment derives its revenues.

- Segment revenues, profit and loss, assets, liabilities, and related information for each reportable segment. In addition, the following specific information about each reportable segment must be reported if the amounts are regularly reviewed by management:

- revenues from external customers (revenues from customers attributed to individual material foreign countries should be separately disclosed)

- revenues from transactions with other operating segments of the same enterprise

- interest income

- interest expense

- depreciation and amortization

- unusual items

- equity in the net income of investees and joint ventures that are accounted for using the equity method

- income tax expense or benefit

- significant non-cash items other than depreciation and amortization expense

- Reconciliations. An enterprise must provide a reconciliation of the total of the segments' revenues to total revenues; a reconciliation of the total of the operating segments' profits and losses to its income before income taxes and discontinued operations; and a reconciliation of the total of the operating segments' assets and liabilities to total assets and liabilities. Reconciliations for other significant items that are disclosed should also be presented and all reconciling items should be separately identified and described for all of the above.

- Products and services. The amount of revenues from external customers.

- Geographic areas. Revenues from external customers (Canada versus foreign), and capital assets and goodwill (Canada versus foreign) should be stated. Foreign information must be disclosed by country if the amounts are material.

- Major customers. If 10% or more of the revenues are derived from a single customer, the enterprise must disclose the total amount of revenues from each of these customers by segment.

CASE 23-3

PURPOSE: This case will review the reporting requirements for interim financial statements.

Sally's Sweater Shop is located in Burnaby, B.C. It sells sweaters, jackets, and other related merchandise. Some shareholders have asked management to distribute quarterly financial statements to shareholders. Sally's Sweater Shop prepares financial statements in accordance with IFRS.

Instructions

(a) Discuss the accounting principles that should be used for interim reports.

(b) Indicate whether or not it is a requirement to include a statement of cash flows in an interim report. Also list the minimum data to be disclosed in an interim report.

Solution to Case 23-3

(a) IFRS indicates that the same accounting principles used for annual reports should be used for interim reports. Assets and liabilities should be recognized at the interim period reporting date on the same basis as they would be recognized at year end. Therefore, revenues and costs directly associated with revenues (product costs) such as materials, labour and related fringe benefits, and manufacturing overhead should be treated in the same manner for interim reports as they are for annual reports.

Generally, companies should use the same inventory pricing methods (FIFO, weighted average cost) for both interim reports and annual reports. However, an exception is provided for planned variances under a standard cost system that are expected to be absorbed by year end. These should ordinarily be deferred.

Costs and expenses other than product costs, often referred to as period costs, are often charged to the interim period as incurred. However, they may be allocated to interim periods based on estimated time to expiry, benefits received, or activities associated with each interim period.

(b) At a minimum, a condensed statement of financial position, statement of comprehensive income, statement of changes in equity, statement of cash flows, and notes to financial statements are required. Comparative financial statements are also required.

Regarding disclosure, the following interim data should be reported as a minimum:

- Whether the statements comply with IFRS

- A statement that the company follows the same accounting policies and methods as the most recent annual financial statements, including a description of new or changed policies

- A description of any seasonality or cyclicality of interim period operations

- The nature and amount of any unusual items

- The nature and amount of changes in estimates

- Issuances, repurchases, and repayments of debt and equity securities

- Dividends paid

- Information about reportable segments, including revenues from external customers, intersegment revenues, segment profit or loss, total assets for which there is a material change, a description of differences from the last annual statements in the basis of segmentation, and reconciliation of segment profit or loss to the entity's total profit or loss before taxes and discontinued operations

- Events subsequent to the interim period

- Specific information about changes in the composition of the entity

- Any other information that is required for fair presentation and/or is material to an understanding of the interim period

Related-Party Transactions—Decision Tree (ASPE)1

PURPOSE: This exercise will allow you to practise accounting for related-party transactions.

Ellis and Associates is a large multinational company with related companies all over the world. During 2014, De Melo Company (a subsidiary company fully owned by Ellis) sold a building to Trick Company (a different subsidiary company fully owned by Ellis). The building has a fair value of $100,000 and a net book value of $60,000. Trick Company paid De Melo Company $80,000 in cash for the building. You may assume that this transaction is outside the normal course of business. Both Trick Company and De Melo Company prepare financial statements in accordance with ASPE.

Instructions

Prepare the journal entries required for both Trick Company and De Melo Company for the above transaction.

Solution to Exercise 23-1

EXPLANATION: Review Illustration 23-1. Since this transaction is not in the normal course of business, we must consider if the change in the ownership interests in the item transferred is substantive. Since the same company (Ellis) controls the building, there has not been a substantive change in ownership interests, and therefore, the transaction is measured at carrying amount. Any difference between carrying amount and exchange amount is recorded in contributed surplus or another equity account. In this case, Trick debits Retained Earnings on the assumption there was no previous Contributed Surplus account balance to absorb the debit.

PURPOSE: This exercise will provide you with examples of Type I and Type II subsequent events.

Instructions

Analyze the following subsequent events and determine the correct accounting treatment.

(a) Fire destroys an office building that is fully covered by insurance.

(b) A significant customer declares bankruptcy.

(c) A major contract is lost.

(d) The union decides to go on strike.

(e) Fair value of FV-NI investments drops by a material amount.

(f) A new business segment is purchased.

(g) A lawsuit outstanding for two years is finally settled.

(h) The company issues new common shares.

(i) A new company president is appointed.

Solution to Exercise 23-2

(a) Since the condition did not exist at the statement of financial position date, this event would not require an adjustment to the financial statements. Whether or not to disclose the transaction would be a matter of professional judgement. Factors to consider would include the significance of the event to the overall operations.

(b) Assuming there is an amount owing at year end, this event would likely require an adjustment to the financial statements, because it provides additional evidence about conditions that existed at the statement of financial position date. A situation leading up to bankruptcy does not happen all of a sudden, but develops over a long period of time. The allowance for doubtful accounts on the year-end financial statements would be adjusted to take this into account.

(c) Loss of a major contract would likely be treated as an event of the subsequent year. It would be neither adjusted nor disclosed on the current year's financial statements. Instead, it would likely be communicated through the financial press.

(d) Since the condition did not exist at the statement of financial position date, there would be no adjustment to the financial statements. However, this too would be covered by the financial press.

(e) Similar to (a) above, with the decision based on the significance of the loss.

(f) Similar to (a) above, with the decision based on the significance of the transaction to its existing assets and liabilities and the company's future operations.

(g) As the lawsuit was outstanding at year end, the settlement provides additional evidence about conditions (the company's potential liability) that existed at the reporting date. The financial statements should be adjusted to reflect the settlement liability and loss amount.

(h) Similar to (a) above, with the decision based on the significance of the additional shares issued.

(i) Similar to (d) above.

A Summary of Financial Ratios

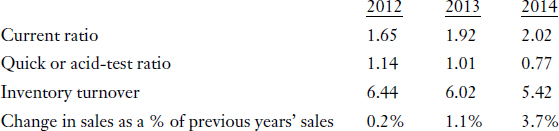

PURPOSE: This exercise will allow you to practise analyzing ratios and results of horizontal percentage analysis.

The following ratios and percentages were calculated using amounts from the 2012 to 2014 financial statements of Spring Corporation, as at and for the years ended December 31:

Instructions

Analyze the ratios and percentages provided, and comment on the financial position of Spring Corporation in the three-year period from 2012 to 2014.

Solution to Exercise 23-3

Spring Corporation's current ratio is increasing, while its quick or acid-test ratio is declining. The quick or acid-test ratio is the current ratio without including inventory and prepaid expenses in current assets (although prepaid expenses are generally insignificant relative to inventory). Any divergence in trend between these two ratios would therefore be explained by the inventory account. Inventory turnover has declined sharply in the three-year period, from 6.44 to 5.42. During the same period, total sales have continually increased. The decline in the inventory turnover is therefore not due to a decline in sales. Investment in inventory has increased at a faster rate than sales, and this has accounted for the divergence between the quick or acid-test and current ratios. These are signs that Spring Corporation's liquidity is deteriorating.

The ratios and percentages provided may be used to comment on the liquidity of Spring Corporation, one aspect of the company's overall financial position. To comment on the overall financial position and performance of Spring Corporation, additional activity ratios (such as receivables turnover and asset turnover), and coverage ratios (such as debt to total assets and cash debt coverage ratio) should be calculated and analyzed. As well, the company's financial position should be compared with the financial position of competitors in the same industry, and an in-depth analysis of the company's business environment and accounting policies and methods should be completed.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

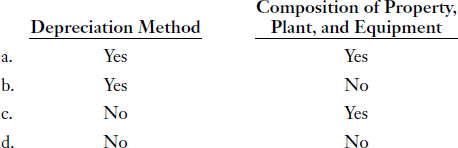

1. Which of the following should be disclosed in the summary of significant accounting policies?

EXPLANATION: The depreciation method for plant assets should be disclosed in the summary of significant accounting policies. Composition of plant assets should not be disclosed in the summary of significant accounting policies because that information is provided elsewhere in the notes to the financial statements. Disclosures in the summary of significant accounting policies should not duplicate information already presented.

Examples of accounting policies to be disclosed include:

- inventory pricing method

- depreciation and amortization methods

- revenue recognition policies (Solution = b.)

Question

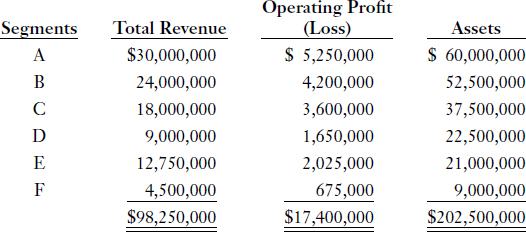

2. Kunita Corporation has six operating segments:

Under IFRS's quantitative guidelines, for which of the operating segments should separate information be presented?

EXPLANATION: An operating segment is regarded as significant and therefore identified as reportable if it satisfies one or more of the following quantitative thresholds:

- Its reporting revenue (including both sales to external customers and intersegment sales or transfers) is 10% or more of the combined revenue of all the enterprise's operating segments.

- The absolute amount of its reported profit or loss is 10% or more of the greater, in absolute amount, of:

- the combined operating profit of all operating segments that did not incur a loss, and

- the combined reported loss of all operating segments that did report a loss.

- Its assets are 10% or more of the combined assets of all operating segments.

Segments A, B, C, and E pass the revenue and operating profit tests, but A, B, C, D, and E pass the asset test. Since an operating segment need only pass one of the three 10% tests to be considered a reportable segment, Kunita Corporation has five reportable segments: A, B, C, D, and E. (Solution = c.)

Question

3. Which of the following does the IASB require an enterprise to report about its reportable segments?

- reconciliations including reconciliation of the segments' revenues to total revenues

- factors that management considers most significant in determining the company's reportable segments, and the types of products and services from which each operating segment derives its revenues

- information about major customers (if 10% or more of the revenues are derived from a single customer, the enterprise must disclose the total amount of revenues from each of these customers by segment)

- all of the above

EXPLANATION: The IASB requires that an enterprise report the following information about its reportable segments: general information about its reportable segments; segment revenues, profit and loss, assets, liabilities, and related information; reconciliations; products and services; geographic areas; and major customers. (Solution = d.)

Question

4. For interim reporting, a company's income tax expense for the second quarter should be calculated using the:

- statutory tax rate for the year

- effective tax rate expected to be applicable for the second quarter

- annual estimated tax rate estimated at the end of the first quarter

- annual estimated tax rate estimated at the end of the second quarter

EXPLANATION: In preparing an interim report, income tax expense for the interim period is calculated using an annual estimated tax rate. Specifically, interim taxable income and temporary differences are estimated, and the estimated annual effective tax rate is applied, to arrive at an estimate of income tax expense for the interim period. (Solution = d.)

Question

5. IFRS recommends that interim reporting be viewed as:

- reporting for a separate accounting period.

- reporting for an integral part of an annual period.

- a “special” type of reporting that need not conform to generally accepted accounting principles.

- requiring a cash basis approach.

EXPLANATION: Under IFRS, each interim period is considered a discrete (separate) period. Generally, preparation of interim reports should be based on the same accounting principles used in preparation of annual reports. However, certain principles and practices used in preparation of annual reports may require modification in preparation of interim reports. (Solution = a.)

Question

6. Events that occur after the December 31, 2014 statement of financial position date (but before the financial statements are completed) that provide additional evidence about conditions that existed at the statement of financial position date and affect the net realizable value of accounts receivable should be:

- discussed only in the MD&A (Management Discussion and Analysis) section of the annual report.

- disclosed only in the notes to the financial statements.

- used to record an adjustment to Bad Debt Expense for the year ended December 31, 2014.

- used to record an adjustment directly to the Retained Earnings account.

EXPLANATION: Notes to the financial statements should explain any significant financial events that took place after the statement of financial position date, but before the financial statements are issued. These events are referred to as subsequent events or events after the reporting period. Two types of events or transactions occurring after the statement of financial position date that may have a material effect on the financial statements, or may need to be considered to interpret the financial statements accurately, are as follows:

- events that provide additional evidence about conditions that existed at the statement of financial position date, which affect the estimates used in preparing the financial statements, and therefore require adjustment of the financial statements.

- events or information about conditions that did not exist at the statement of financial position date, but are significant enough to require disclosure.

The subsequent event described in the question provides additional evidence about conditions that existed at the statement of financial position date. This information would have been recorded in the accounts if it was known at the statement of financial position date. Therefore, this subsequent event requires adjustment of the financial statements before they are issued. (Solution = c.)

Question

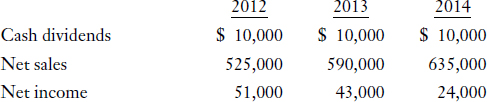

7. The following amounts are from the 2012 to 2014 financial statements of Parkville Corporation for the years ended December 31:

Which of the following statements is true?

- Parkville's payout ratio remained unchanged between 2012 and 2014.

- Parkville's payout ratio increased between 2012 and 2014.

- Parkville's profit margin on sales improved between 2012 and 2014.

- Parkville's profit margin on sales between 2012 and 2014 cannot be determined from the information given.

EXPLANATION: Payout ratio is calculated as cash dividends divided by net income, and profit margin on sales is calculated as net income divided by net sales. Parkville's profit margin on sales deteriorated between 2012 and 2014; however, Parkville's payout ratio increased between 2012 and 2014. (Solution = b.)

Question

8. Under ASPE, a related-party cash transaction in the normal course of business is measured at the following amount:

- exchange amount.

- fair value.

- carrying amount.

- replacement cost.

EXPLANATION: Refer to Illustration 23-1. Recall that related-party transactions can only be recorded at exchange value or carrying amount. If a related-party cash transaction is in the normal course of business, it is recorded at the exchange amount. (Solution = a.)

Question

9. Under ASPE, a related-party cash transaction that is not in the normal course of business, and is without a substantive change in ownership interests, is measured at the following amount:

- exchange amount.

- fair value.

- carrying amount.

- replacement cost.

EXPLANATION: Refer to Illustration 23-1. Recall that a related-party transaction can only be recorded at its exchange amount or carrying amount. If a related-party cash transaction is not in the normal course of business and there is no substantive change in ownership interests, it is recorded at the carrying amount of the assets exchanged. Any difference between the exchange amount and carrying amount is recorded in equity. (Solution = c.)

Question

10. Which of the following would not be considered a related party to A Company?

- B Company, where A Company controls B Company

- A major shareholder of A Company (owns 55%)

- Management of A Company

- C Company, where C Company is a 15% shareholder of A Company

EXPLANATION: Related parties include but are not limited to the following: (1) companies or individuals who control, or are controlled by, or are under common control with the reporting enterprise; (2) investors and investees where there is significant influence or joint control; (3) company management; (4) members of immediate family of the above; and (5) the other party when a management contract exists. (Solution = d.)

Question

11. Jutland Company is in the process of having its financial statements audited. The audit partner has called a meeting to discuss the fact that the company has not followed generally accepted accounting principles in accounting for advertising costs. The impact on net income is fairly significant but not so material that it renders the financial statements invalid as a whole. This situation, if not fixed, could result in which type of audit opinion?

- an unqualified opinion

- a qualified opinion

- an adverse opinion

- a denial of opinion

EXPLANATION: A qualified opinion would be issued because there is an exception to the standard opinion. The problem is not significant enough that it affects the usefulness of the rest of the financial statements taken as a whole. Therefore, an adverse opinion would not be issued, and a denial of opinion would not be issued. (Solution = b.)

Question

12. Jefferies Company is a clothing manufacturer in its fifth year of operations, and is seeking a short-term bank loan to fund planned expansion of its manufacturing operations in 2015. Sara Sherwin is a loan officer at Jefferies Company's bank, and is analyzing the company's financial statements for the years ended December 31, 2012, 2013, and 2014. In particular, Sara is concerned about Jefferies Company's short-term debt-paying ability. Which ratios should Sara calculate and consider in her assessment of Jefferies Company's liquidity?

- asset turnover

- quick or acid-test ratio

- times interest earned

- cash debt coverage ratio

EXPLANATION: Asset turnover is a measure of how efficiently assets are used to generate sales, and is not a measure of short-term debt-paying ability or liquidity. Times interest earned is a measure of the company's ability to meet interest payments as they come due, and cash debt coverage ratio is a measure of the company's ability to repay its total liabilities in a specific year from its operations. The times interest earned and cash debt coverage ratios are coverage ratios, and are not specific measures of short-term debt-paying ability or liquidity. The quick or acid-test ratio is a measure of immediate short-term liquidity. (Solution = b.)