OVERVIEW

Employee future benefits discussed in this chapter include (1) post-retirement plans, such as pensions, that provide benefits after an employee's retirement; (2) post-employment plans that provide benefits after an employee's employment but before retirement; and (3) plans covering accumulating and vested compensated absences. Employee future benefit plans are generally either defined contribution plans or defined benefit plans. Under a defined contribution plan, the employer's obligation is limited to amounts to be contributed according to the plan. Under a defined benefit plan, the benefits to be received by the employee in the future or the method of determining those benefits is specified in the benefit plan, and the benefits often vest after the employee has worked a specified number of years. As such, the employer's obligation to pay benefits in the future on account of services provided by its employees up to the statement of financial position date must be estimated (by an actuary). Recognition and measurement of the employer's defined benefit obligation (or accrued benefit obligation) and the plan assets under a defined benefit plan is complex, with specific recognition and measurement requirements under IFRS, and different recognition and measurement options available under ASPE. In this chapter, accounting for defined benefit plans is discussed extensively, with a focus on defined benefit pension plans.

STUDY STEPS

Understanding the Nature of Employee Future Benefit Plans

What is a benefit plan?

A benefit plan is any arrangement between an entity and its employees whereby, as part of the compensation to its employees, the entity is obligated to provide benefits after an employee's retirement (a post-retirement benefit plan), after an employee's employment but before retirement (a post-employment benefit plan), or during an employee's absence from work (a plan covering accumulating and vested compensated absences).

The employer contributes funds to the benefit plan each year based on one of two options. In the case of a defined contribution plan, the required payments are stated in the benefit plan. In the case of a defined benefit plan, contributions are based on an established funding pattern calculated by an actuary to ensure that enough funds will be available to provide the benefits that have been promised. The benefit plan is often a separate legal entity administered by an independent third party or trustee that is also responsible for investment of the benefit plan assets and distribution of those assets (for example, to retirees in the case of a pension plan).

In summary, in the case of a pension plan, the employee earns future benefits during his or her period of employment with the employer, and is paid these benefits during his or her period of retirement. The employer contributes funds to the benefit plan during the employee's period of employment, and the benefit plan pays the employee benefits during his or her period of retirement.

The parties involved in a benefit plan

Often, a benefit plan has a trustee (such as a trust company) that administers the plan, invests the plan assets, and distributes the plan assets to the participating employees. The trustee retains the plan assets, which include securities held as the plan's investments and amounts in the plan's bank account, to which employer contributions are paid.

An actuary calculates an appropriate funding (contribution) pattern to ensure that enough funds will be available to provide the future benefits that have been promised. The actuary also calculates various amounts used in accounting for the plan, including the defined benefit obligation (or accrued benefit obligation), annual cost of servicing the plan, and cost of amendments to the plan. The actuary incorporates many assumptions in his or her calculations, including discount rates, rates of return on assets, and mortality rates. The actuary may use conservative assumptions since the employer is relying on the actuary's calculations to determine its funding (contribution) pattern, and the employer is ultimately responsible for providing the future benefits that have been promised.

Most pension plans require a specific minimum number of years of service to the employer before the employee's future benefits vest. That is, most future benefits vest after an employee has worked for the employer for a certain pre-specified amount of time. Vesting occurs when an employee becomes legally entitled to future benefits even if the employee leaves and no longer works for the employer. If the employee leaves the employer prior to the vesting date, he or she forfeits the right to any future benefits. As long as the employee remains with the employer until the vesting date, he or she is entitled to receive the full amount of accumulated benefits in future.

Defined contribution plans versus defined benefit plans

There are two types of benefit plans: defined contribution and defined benefit. Under defined contribution plans, the employer only promises to contribute a certain amount to the benefit plan each year; the employer does not agree to pay a certain amount of benefits in the future. In contrast, under defined benefit plans, the employer promises to pay a certain amount of benefits in the future, and therefore assumes the economic risks involved in meeting the obligation, including changes in plan costs and fluctuations in investment returns on plan assets.

An example of a defined benefit pension plan benefit formula is as follows: 2% of the employee's best year of salary (of the years that the employee worked for the employer) multiplied by the number of years worked for the employer. Therefore, if the best year of salary is estimated to be $40,000 and the employee has worked 10 years to date, he or she will be entitled to a payout on retirement of:

![]()

This chapter focuses mainly on accounting for defined benefit plans since accounting for defined contribution plans is relatively straightforward.

The benefit plan itself has assets and a defined benefit obligation. The plan assets are accumulated contributions from the employer and investment returns on plan assets up to the statement of financial position date minus benefits paid to retirees. The defined benefit obligation (DBO) is estimated future benefits earned by employees up to the statement of financial position date. The benefit plan's assets and defined benefit obligation are not recognized in the employer's financial statements, but are tracked by the employer in off–balance sheet or memo accounts.

Recognition and measurement differences: IFRS and ASPE

The employer (or benefit plan sponsor) records an annual pension expense and a net defined benefit liability/asset. The amount of annual pension expense and the amount of net defined benefit liability/asset are affected by (1) the accounting approach used (either the immediate recognition approach required under IFRS and permitted under ASPE or the deferral and amortization approach permitted under ASPE); (2) application of optional recognition and measurement rules available under ASPE; (3) changes in the benefit plan's plan assets and defined benefit obligation; and (4) estimated inputs such as discount rate.

Under the immediate recognition approach, past service costs are recognized immediately in pension expense and net defined benefit liability/asset, along with current service cost, interest cost, and actual return on plan assets. When applying the immediate recognition approach under ASPE, the accrued benefit obligation is based on an actuarial valuation of the obligation used for funding purposes, and represents the present obligation at the balance sheet date. Under IFRS, a form of the immediate recognition approach is applied.

When applying the immediate recognition approach under ASPE, the actual return on plan assets is used in the calculation of pension expense and is included in net income. When applying the immediate recognition approach under IFRS, the expected return on plan assets (using the same discount rate used in calculating the DBO) is used in the calculation of pension expense that is included in net income. The difference between the actual and expected return on plan assets is an asset actuarial gain or loss and it is included as a remeasurement gain or loss in other comprehensive income (OCI).

In addition, when applying the immediate recognition approach under ASPE, actuarial gains and losses on the defined/accrued benefit obligation are recognized as a component of pension expense and included in net income in the same period they are incurred. When applying the immediate recognition approach under IFRS, actuarial gains and losses on the defined/accrued benefit obligation are recorded in OCI as remeasurement gains or losses in the same period they are incurred.

When applying the ASPE deferral and amortization approach, the accrued benefit obligation is based on the projected benefit obligation, or present value of vested and non-vested benefits earned up to the balance sheet date, with the benefits measured using employees' future salary levels. Under the deferral and amortization approach, past service costs and actuarial gains and losses may be deferred and amortized and therefore recognized in pension expense and net defined benefit liability/asset over more than one period.

Other employee future benefit plans

Other employee future benefit plans include plans that provide health care or life insurance benefits, service-related long-term disability benefits, and unrestricted sabbaticals. In general, employers do not contribute to post-employment benefit plans other than pensions in advance of benefit payments, and benefits related to these plans are more difficult to measure. Under IFRS, the same accounting standards that apply to defined benefit pension plans apply only to other long-term benefit plans. Under ASPE, the same accounting standards that apply to defined benefit pension plans also apply to other post-employment benefit plans that vest or accumulate.

Under both IFRS and ASPE, if a benefit plan does not vest or accumulate, no accrued cost or liability is recorded; instead, costs and liabilities are recorded when incurred, or when an obligating event occurs.

Becoming Proficient in Related Calculations: The Work Sheet/Spreadsheet

Accounting for pensions and other employee future benefits is theoretically and technically complex. Therefore, a significant amount of time should be devoted to studying the exercises and illustrations in this chapter, and understanding the related calculations.

The work sheet approach (shown in the text) is an excellent tool for analysis of a defined benefit pension plan in a given year, and for calculation of the annual journal entry amounts. Therefore, you should familiarize yourself with it as soon as possible.

Remember that an objective of the work sheet is to calculate the costs associated with the employee future benefits plan. This is in order to accrue pension expense in the periods in which the employees provide services to earn the future benefits, and thus match pension expense with revenues generated by the employees in those periods. The end result of the work sheet is the following:

- calculation of pension expense for the year (recorded with a debit to Pension Expense, and a credit to Net Defined Benefit Liability/Asset);

- calculation of the remeasurement gain or loss reported in OCI under IFRS (recorded with a debit to Remeasurement Loss (OCI) or credit to Remeasurement Gain (OCI), and a credit or debit to Net Defined Benefit Liability/Asset); and

- recording of contributions to the plan (with a debit to Net Defined Benefit Liability/Asset and a credit to Cash).

Thus, under IFRS the net defined benefit liability/asset changes by the difference between the amount of pension expense and remeasurement gain or loss included in OCI for the year, and the cash contributions paid into the plan in the year.

The work sheet is needed only for defined benefit plans. It is not necessary for defined contribution plans because they do not have similar complications.

Compare a work sheet prepared under the immediate recognition approach with a work sheet prepared under the deferral and amortization approach to review the differences between the two approaches.

- Under both IFRS and ASPE, the immediate recognition approach requires that past service costs be included in pension expense immediately (in the year of plan initiation or amendment). Under the ASPE deferral and amortization approach, past service costs may be deferred and amortized over more than one period. Under the ASPE deferral and amortization approach, past service costs are amortized over the period that the employer will benefit from the plan initiation or amendment. This is usually the expected period until the employees are eligible for the plan's full benefits, but may be shorter. Unrecognized past service costs are recorded off–balance sheet in a memo account.

- Under the IFRS immediate recognition approach, pension expense is reduced by the expected return on plan assets, using the same discount rate as is used to calculate interest cost. The asset actuarial gain or loss (the difference between actual and expected return on plan assets) is included in the remeasurement gain or loss reported in OCI. Under the ASPE immediate recognition approach, pension expense is decreased (usually) by the actual return on plan assets. Under the ASPE deferral and amortization approach, pension expense is decreased by the expected return on plan assets, using an actuary-determined long-run rate of return. The asset actuarial gain or loss—the difference between expected and actual return on plan assets—is recorded off–balance sheet in a memo account and included in unrecognized actuarial gain or loss.

- Under the IFRS immediate recognition approach, liability actuarial gains and losses (differences between the actuary's assumptions and actual experience, and resulting from changes in the assumptions that are used by the actuary in calculating the defined benefit obligation) are included in the remeasurement gain or loss reported in OCI. Under the ASPE immediate recognition approach, liability actuarial gains and losses are recognized in pension expense immediately. Under the ASPE deferral and amortization approach, liability actuarial gains and losses are recorded off–balance sheet in a memo account and included in unrecognized actuarial gain or loss.

- Under the ASPE deferral and amortization approach, amortization of the net accumulated actuarial gain or loss is recorded in pension expense if the net accumulated unrecognized actuarial gain or loss at the beginning of the year exceeds the corridor, which is 10% of the larger of the accrued benefit obligation and the fair value of the plan assets at the beginning of the year. If the corridor is exceeded, the minimum amortization is the net accumulated unrecognized actuarial gain or loss at the beginning of the year less the corridor amount, divided by the expected average remaining service life (EARSL) of the employee group that is covered by the plan.

TIPS ON CHAPTER TOPICS

- The defined benefit obligation (DBO) (referred to as accrued benefit obligation (ABO) under ASPE) is a measure of the pension obligation at the statement of financial position date. The DBO (or ABO) is based on the projected benefit obligation, or present value of vested and non-vested benefits earned up to the statement of financial position date, with the benefits measured using employees' future salary levels. Under the ASPE immediate recognition approach, the ABO is based on actuarial valuation for funding purposes, and represents the present obligation at the balance sheet date. Notice whether the beginning-of-period or end-of-period balance of DBO (or ABO) is required for a particular calculation, for example:

- The beginning balance of DBO (or ABO) is used to calculate the interest cost included in pension expense for the period, assuming that all other transactions that affect DBO (or ABO) take place at the end of the year.

- The ending balance of DBO (or ABO) is used to reconcile the funded status of the plan with the net defined benefit liability/asset reported on the employer's statement of financial position.

- Under the ASPE deferral and amortization approach, the greater of the beginning balance of the ABO or the beginning balance of the fair value of plan assets is used to calculate the 10% corridor in determining whether or not any net accumulated unrecognized actuarial gain or loss should be amortized.

- Under IFRS, interest cost on the DBO must be calculated using a current market rate (for example, the current yield on high-quality debt instruments such as high-quality corporate bonds). Under ASPE, interest cost on the ABO can be calculated using a current market rate (for example, the current yield on high-quality debt instruments such as high-quality corporate bonds) or a current settlement rate (for example, the rate implied in an insurance contract that could be purchased to effectively settle the pension obligation).

- Under IFRS, the same discount rate is used to calculate interest cost on the DBO and the expected return on plan assets. Under the ASPE deferral and amortization approach, the discount rate used to calculate interest cost on the ABO is usually different from the rate used to calculate expected return on plan assets.

- Actual return on plan assets is the income generated on plan assets, from interest, dividends, and realized and unrealized changes in fair value of the plan assets. Actual return on plan assets can be calculated by (1) calculating the change in fair value of plan assets, (2) deducting contributions, and (3) adding benefits paid. Under the IFRS immediate recognition approach, asset actuarial gain or loss (the difference between expected return on plan assets and actual return on plan assets) is included in the remeasurement gain or loss in OCI. Under the ASPE deferral and amortization approach, the asset actuarial gain or loss is recorded off–balance sheet, with the net accumulated unrecognized actuarial gain or loss, and is subject to the corridor approach for amortization purposes.

- Under the IFRS immediate recognition approach, liability actuarial gains and losses (differences between the actuary's assumptions and actual experience, and resulting from changes in the assumptions that are used by the actuary in calculating the defined benefit obligation) are included in the remeasurement gain or loss reported in OCI. Under the ASPE deferral and amortization approach, liability actuarial gains and losses (differences between the actuary's assumptions and actual experience, and resulting from changes in the assumptions that are used by the actuary in calculating the accrued benefit obligation) are included in the net accumulated unrecognized actuarial gain or loss and corridor approach calculations, along with the asset actuarial gain or loss. Under the corridor approach, the net accumulated actuarial gain or loss is amortized when it exceeds 10% of the larger of the beginning balances of ABO or fair value of the plan assets.

- Under the corridor approach, the minimum amount of net accumulated actuarial gain or loss to be amortized in a year equals net accumulated actuarial gain or loss in excess of the corridor amount divided by the expected average remaining service life (EARSL) of the employee group. A larger amount can be amortized, even to the extent of full immediate recognition.

- Plan adoptions or amendments often include provisions to increase future benefits based on employee services provided in prior years. Under both IFRS and ASPE, the immediate recognition approach requires that these past service costs be included in pension expense immediately (in the year of plan initiation or amendment). Under the ASPE deferral and amortization approach, these costs are amortized to pension expense over more than one period, starting in the period of plan adoption or amendment.

- The balances of DBO (or ABO), plan assets, unrecognized past service cost (under ASPE's deferral and amortization approach), and unrecognized actuarial gain or loss (under ASPE's deferral and amortization approach) do not appear on the employer's statement of financial position. However, they have an impact on the calculation of amounts that appear on the employer's statement of comprehensive income (or income statement), statement of financial position, and notes to financial statements.

- A pension work sheet calculates amounts for both formal journal entries and memo journal entries. The journal entry to record pension expense is a debit to Pension Expense for the amount calculated on the pension work sheet, a debit to Remeasurement Loss (OCI) or a credit to Remeasurement Gain (OCI) for the amount calculated on the pension work sheet under the IFRS immediate recognition approach, and a debit or a credit to Net Defined Benefit Liability/Asset for the difference. The entry to record the contributions to the fund include a credit to Cash for the amount contributed for the period, and a debit to Net Defined Benefit Liability/Asset.

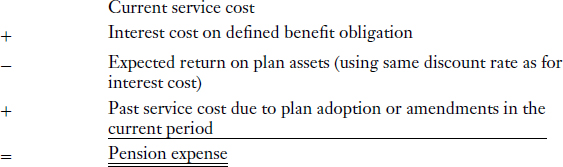

Components of Pension Expense

Calculation of Pension Expense—IFRS Immediate Recognition Approach

Calculation of Pension Expense—ASPE Immediate Recognition Approach

Calculation of Pension Expense—Deferral and Amortization Approach (ASPE)

Description of components:

Current service cost: This is the cost of the benefits that are to be provided in the future in exchange for the services that the employees provided in the current period. The actuary calculates current service cost as present value of the additional benefits earned by employees in the current year.

Interest cost on defined benefit obligation (or accrued benefit obligation): Because a pension is a deferred compensation arrangement, the time value of money is a factor. Defined benefit obligation (or accrued benefit obligation) is recorded at present value, and interest accrues each year on the defined benefit obligation (or accrued benefit obligation), just as it would on any other discounted debt.

Actual return on plan assets: This is income generated on plan assets (from interest, dividends, and realized and unrealized changes in fair value of the plan assets).

Expected return on plan assets: For ASPE, this is the return expected to be earned in the period by the accumulated pension fund assets, calculated based on the expected long-term rate of return on plan assets, and applied to the fair value of plan assets. Under the IFRS immediate recognition approach, the expected rate is the same rate as the discount rate used to determine interest costs for the period. The asset actuarial gain or loss (the difference between expected return on plan assets and actual return on plan assets) is included in the remeasurement gain or loss reported in OCI. Under the ASPE deferral and amortization approach, any asset actuarial gain or loss is included in the net accumulated unrecognized actuarial gain or loss, and in corridor approach calculations.

Past service cost: This is the cost of additional future benefits (or in rare cases, the decrease in future benefits) based on employee services provided in prior years, as a result of pension plan adoption or amendments. Under both IFRS and ASPE, the immediate recognition approach requires that past service costs be included in pension expense immediately in the period of plan initiation or amendment.

Amortization of unrecognized past service cost: Under the ASPE deferral and amortization approach, past service cost may be deferred and amortized over the period when the employer will benefit from the plan initiation or amendment.

Liability actuarial gain/loss: This is what arises from differences between the actuary's assumptions and actual experience, and from changes in the assumptions that are used by the actuary in calculating the defined benefit obligation (or accrued benefit obligation). Under the IFRS immediate recognition approach, the liability actuarial gain/loss is included in the remeasurement gain or loss recognized in OCI. Under the ASPE deferral and amortization approach, the liability actuarial gain/loss is included in net accumulated unrecognized actuarial gain or loss, and in corridor approach calculations, along with any asset actuarial gain or loss.

Amortization of unrecognized actuarial gain or loss: Actuarial gains or losses include both asset actuarial (experience) gains/losses (the difference between expected and actual return on plan assets), and liability actuarial (experience) gains or losses (differences between the actuary's assumptions and actual experience, and resulting from changes in the assumptions that are used by the actuary in calculating the accrued benefit obligation). Under the ASPE deferral and amortization approach, amortization of unrecognized actuarial gain or loss is subject to the corridor approach.

PURPOSE: This exercise will enable you to practise calculating pension expense based on the immediate recognition approach.

The following data relate to Safety Company's pension plan for the year 2014:

Instructions

(a) Calculate pension expense to be included in net income for 2014 based on the IFRS immediate recognition approach.

(b) Calculate pension expense to be included in net income for 2014 based on the ASPE immediate recognition approach.

Solution to Exercise 19-1

(a) IFRS immediate recognition approach

APPROACH: When calculating pension expense, refer to Illustration 19-1.

Interest cost may also be calculated on a weighted average basis. In the text and in this chapter, it is assumed, unless otherwise stated, that current service cost, contributions to the fund, and benefits paid to retirees are end-of-year cash flows, and that a separate weighted average calculation of defined/accrued benefit obligation is not required before calculating interest cost.

PURPOSE: This exercise will enable you to practise calculating pension expense based on the ASPE deferral and amortization approach.

The following data relate to Kleen Company's pension plan for the year 2014:

Instructions

Calculate pension expense for 2014 based on the ASPE deferral and amortization approach.

Solution to Exercise 19-2

APPROACH: When calculating pension expense, refer to Illustration 19-1.

- Under the deferral and amortization approach, the corridor approach is applied for amortization of unrecognized actuarial gains or losses. Under the corridor approach, if the unrecognized actuarial gain or loss (beginning balance) exceeds the corridor amount (10% of the larger of the beginning balance of the accrued benefit obligation and the beginning balance of the fair value of plan assets), then the unrecognized actuarial gain or loss is considered too high and must be amortized. The minimum current year amortization of the unrecognized actuarial gain or loss is the unrecognized actuarial gain or loss in excess of the corridor amount, divided by the expected average remaining service life (EARSL) of the employee group. In this exercise, under the corridor approach, no amortization of the unrecognized actuarial gain or loss is required in 2014:

- Because the actual return on plan assets equals the expected return on plan assets for 2014, there is no asset actuarial (experience) gain or loss for 2014 to include in the unrecognized actuarial gain or loss, which would be subject to the corridor approach in the following year.

Components of Defined Benefit Obligation (or Accrued Benefit Obligation) and Plan Assets

Calculation of Defined Benefit Obligation (or Accrued Benefit Obligation)

Calculation of Plan Assets

- Calculation of the defined/accrued benefit obligation and plan assets is the same under both the immediate recognition approach and the ASPE deferral and amortization approach.

- It is helpful to know the various components of the defined/accrued benefit obligation and plan assets. If you are given the amounts contributed by the employer during the year, the benefits paid to employees and retirees from the pension fund during the year, and the net increase in the fair value of plan assets for the year, you can solve for the actual return on plan assets for the year.

- Although the balance of the defined/accrued benefit obligation and the balance of plan assets are not reported on the employer's statement of financial position, they have an impact on the calculation of amounts that appear on the employer's statement of comprehensive income (or income statement), statement of financial position, and notes to financial statements.

- One of the components of the defined/accrued benefit obligation is the liability actuarial (experience) gain or loss for the period, which may be due to differences between the actuary's assumptions and actual experience, or changes in the assumptions that are used by the actuary in calculating the defined/accrued benefit obligation. Liability actuarial gains reduce the defined/accrued benefit obligation, whereas liability actuarial losses increase the defined/accrued benefit obligation.

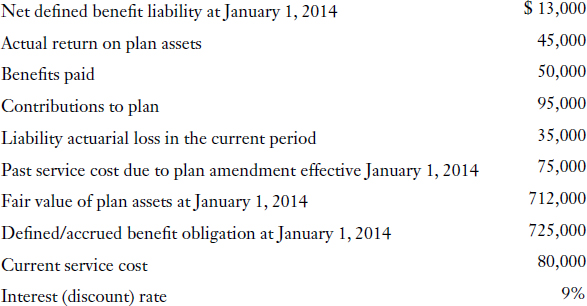

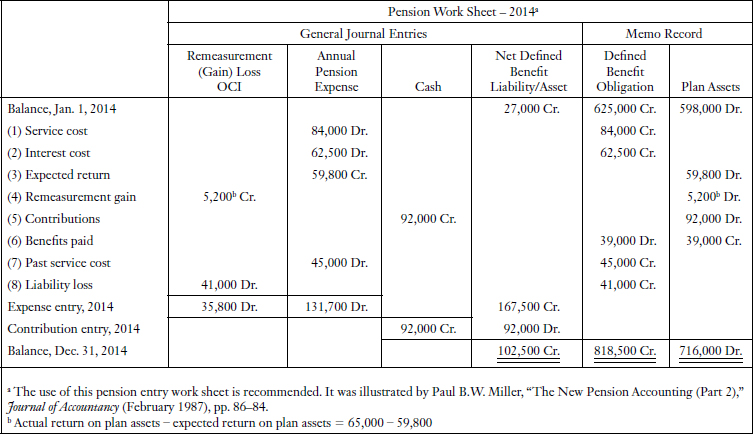

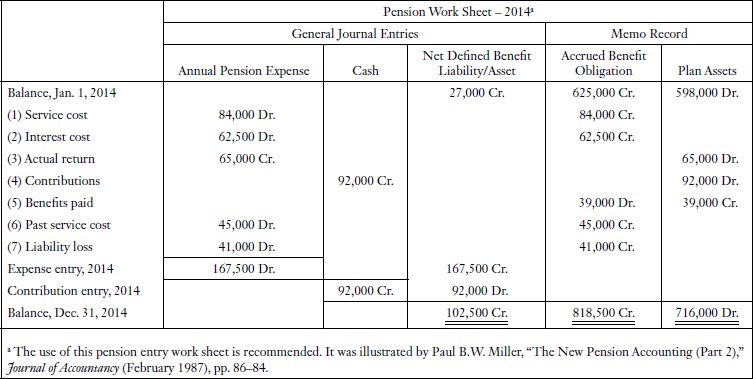

PURPOSE: This exercise will illustrate the mechanics of the pension work sheet.

The following data relate to Lambda Company's pension plan for the year 2014:

Instructions

(a) Prepare a pension work sheet for 2014 based on the IFRS immediate recognition approach. Show the journal entries for pension expense and contribution for 2014.

(b) Prepare a pension work sheet for 2014 based on the ASPE immediate recognition approach. Show the journal entries for pension expense and contribution for 2014.

Solution to Exercise 19-3

(a) IFRS immediate recognition approach

(b) ASPE immediate recognition approach

- In the pension work sheet, the balance of net defined benefit liability/asset equals the net of the balances in the (off–balance sheet) memo accounts. If the memo accounts net to a credit balance, a net defined benefit liability is reported on the statement of financial position. If the memo accounts net to a debit balance, a net defined benefit asset is reported on the statement of financial position.

PURPOSE: This exercise will illustrate the calculation of the actual return on plan assets.

Instructions

Calculate actual return on plan assets during 2014.

Solution to Exercise 19-4

APPROACH: Write down the formula for reconciling the beginning and ending balance of plan assets at fair value (see Illustration 19-2). Enter the data given. Solve for the unknown.

PURPOSE: This exercise will illustrate the calculation of the expected return on plan assets and discuss the effect of the expected return on plan assets in calculation of pension expense.

Assume that Milette Company (from Exercise 19-4) also reports:

| Expected return on plan assets | 10% |

Instructions

(a) Calculate the expected return on plan assets during 2014 and the remeasurement gain or loss under the IFRS immediate recognition approach.

(b) Explain how the expected return on plan assets and remeasurement gain or loss enter into the calculation of pension expense under the IFRS immediate recognition approach.

(c) Explain how the expected return on plan assets and remeasurement gain or loss enter into the calculation of pension expense under the ASPE immediate recognition approach.

Solution to Exercise 19-5

(a) 10% × $3,200,000 fair value of plan assets at January 1, 2014 = $320,000 expected return on plan assets.

(b) Under the IFRS immediate recognition approach, the expected return on plan assets of $320,000 is included in the calculation of current pension expense, reducing the expense by this amount. The difference between the expected and actual return on assets is included in OCI as a remeasurement loss.

(c) Under the ASPE immediate recognition approach, pension expense is reduced directly by the actual return of $220,000. The expected return on plan assets of $320,000 and asset actuarial (experience) loss of $100,000 net to the actual return on plan assets of $220,000, but are not calculated separately.

EXPLANATION: In parts (a) and (b) of this exercise, the expected return on plan assets is calculated by multiplying the fair value of the plan assets (beginning balance) by the same discount rate used to calculate the interest cost. It is assumed that contributions to the plan and benefits paid from the plan took place at the end of the year. However, if a contribution to the plan was made at the beginning of the year, the calculation shown in this exercise would not reflect the economic reality that more assets were available for investing than were used in the calculation of expected return. Therefore, if there were contributions to the plan and benefits paid from the plan throughout the year, the expected return on plan assets is calculated using a weighted average balance of fair value of plan assets.

PURPOSE: This exercise will illustrate accounting for post-retirement benefits other than pensions.

Handy Company reports the following data related to post-retirement benefits for 2014:

Handy follows IFRS and accounts for post-retirement benefit expense based on the immediate recognition approach.

Instructions

(a) Calculate post-retirement benefit expense for 2014.

(b) Prepare the journal entries to record post-retirement benefit expense and Handy's contribution for 2014.

(c) Calculate the defined benefit obligation at December 31, 2014.

Solution to Exercise 19-6

(a)

EXPLANATION: The components used to calculate post-retirement benefit expense are the same as the components used to calculate pension expense.

- Current service cost is the cost of the benefits that are to be provided in the future in exchange for the services that the employees provided in the current period.

- Interest cost is the discount rate multiplied by the defined benefit obligation at the beginning of the year. However, interest cost may also be calculated using a weighted average amount of defined benefit obligation. See discussions above regarding calculation of interest cost and expected return on plan assets for pensions.

(b)

EXPLANATION: The journal entries to record post-retirement benefit expense are similar to the entries to record pension expense.

(c)

EXPLANATION: Similar to the defined benefit obligation for pension benefits, the defined benefit obligation for post-retirement benefits increases by current service cost and interest cost, and decreases by the amount of benefits paid during the period. A liability actuarial (experience) gain or loss for the period would also affect the balance of the defined benefit obligation for post-retirement benefits.

PURPOSE: This exercise will illustrate reconciliation of the funded status of a pension plan to the net defined benefit liability/asset reported on the statement of financial position, under the ASPE deferral and amortization approach.

Steele Company provided the following data related to its pension plan at December 31, 2014:

![]()

Instructions

Present a schedule showing a reconciliation of the funded status of the pension plan to the net defined benefit liability/asset reported on the statement of financial position, under the ASPE deferral and amortization approach.

Solution to Exercise 19-7

APPROACH AND EXPLANATION: This plan is clearly underfunded, since the fair value of plan assets is less than the accrued benefit obligation. The funded status is reconciled to the net defined benefit liability reported on the statement of financial position by including the effect of unrecognized liabilities, gains, and losses, which have not been recognized on the employer's financial statements, but which have been recognized in the memo accounts and records of the pension plan.

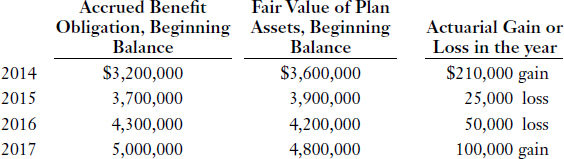

PURPOSE: This exercise will illustrate the use of the corridor approach to amortizing unrecognized actuarial gains and losses, under the ASPE deferral and amortization approach.

The following information is available for Shi Company's pension plan:

The net accumulated unrecognized actuarial gain is $300,000 as at January 1, 2014. Expected average remaining service life of the employee group is 12 years in 2014 and 2015, and 15 years in 2016 and 2017.

Instructions

Set up a schedule to calculate the amount of actuarial gain or loss to be amortized to pension expense each year using the ASPE corridor approach.

Solution to Exercise 19-8

(1) 10% of the greater of accrued benefit obligation and fair value of plan assets at the beginning of the year.

(2) ($510,000 − $390,000) ÷ 12 = $10,000.

(3) $510,000 − $10,000 net gain amortized − $25,000 loss = $475,000.

(4) ($475,000 − $430,000) ÷ 15 = $3,000.

(5) $475,000 − $3,000 net gain amortized − $50,000 loss = $422,000.

If the balance of Net Accumulated Unrecognized Actuarial Gain or Loss stays within the upper and lower limits of the corridor, no amortization of actuarial gain or loss is required. (The unrecognized actuarial gain or loss is carried forward unchanged.) If amortization of actuarial gain or loss is required, the minimum amount of amortization for the year is the excess of net accumulated unrecognized actuarial gain or loss above the corridor amount divided by the expected average remaining service life of the employee group.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

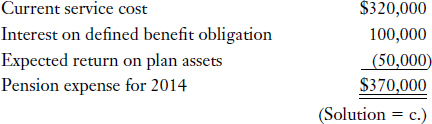

1. The Minnow Corp. has a defined benefit pension plan. Information for the plan for 2014 is as follows:

Based on the IFRS immediate recognition approach, what amount should Minnow report as pension expense on its statement of comprehensive income for 2014?

- $270,000

- $350,000

- $370,000

- $420,000

EXPLANATION: Pension expense is calculated as follows:

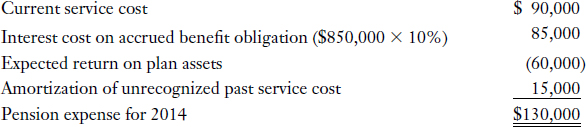

Question

2. Which of the following items should be included in the calculation of net pension expense under the ASPE immediate recognition approach to accounting for defined benefit plans?

EXPLANATION: Review the components of pension expense (refer to Illustration 19-1). Under both IFRS and ASPE, the immediate recognition approach requires that past service costs be included in pension expense immediately (in the year of plan initiation or amendment). While actual return on plan assets is a component of pension expense under the ASPE immediate recognition approach, fair value of the plan assets is not. (Solution = c.)

Question

3. The following information relates to the pension plan of Jay, Inc. for 2014:

Under the ASPE deferral and amortization approach, pension expense for 2014 is:

- $400,000.

- $412,000.

- $466,000.

- $478,000.

EXPLANATION: Current service cost and interest cost increase pension expense. Expected return on plan assets reduces pension expense. Amortization of unrecognized net actuarial gain reduces pension expense. Amortization of unrecognized past service cost increases pension expense. Calculation of pension expense is as follows:

Question

4. The following information relates to the pension plan of Surnoskie Company, which is accounted for based on the IFRS immediate recognition approach:

In 2014, Surnoskie's contribution was $420,000, and benefits paid totalled $375,000. Actual return on plan assets for 2014 is:

- $255,000.

- $300,000.

- $345,000.

- $955,000.

EXPLANATION: Recall that actual return on plan assets can be determined by (1) calculating the change in plan assets (at fair value), (2) deducting contributions during the year, and (3) adding benefits paid during the year:

Question

5. Refer to the data for Surnoskie Company in Question 4. Knowing that the actual return on plan assets is $255,000 in 2014, the asset remeasurement gain or loss recognized in OCI for 2014 is:

- $24,000 gain.

- $45,000 gain.

- $57,600 gain.

- $59,000 gain.

EXPLANATION: Expected return on plan assets is calculated as expected rate of return multiplied by plan assets (at fair value) at the beginning of the year. For 2014, expected return on plan assets is $210,000 (7% × $3 million). Since the actual return on plan assets is $255,000, there is an asset remeasurement gain of $45,000 ($255,000 − $210,000) for 2014. (Solution = b.)

Question

6. Refer to the data for Surnoskie Company in Question 4. The net remeasurement gain or loss reported in OCI for 2014 is:

- $500,000 gain.

- $500,000 loss.

- $455,000 gain.

- $455,000 loss.

EXPLANATION: The net remeasurement gain or loss reported in OCI in 2014 includes both the asset actuarial gain or loss (the difference between expected return on plan assets and actual return on plan assets), and the liability actuarial gain or loss. Therefore, Surnoskie's net remeasurement gain or loss reported in OCI in 2014 is a $455,000 loss ($45,000 asset gain − $500,000 liability loss). (Solution = d.)

Question

7. Refer to the data for Surnoskie Company in Question 4. The service cost for 2014 is:

- $579,000.

- $704,000.

- $900,000.

- $1,079,000.

EXPLANATION: Service cost can be determined by (1) calculating change in defined benefit obligation (at fair value), (2) deducting interest cost, (3) adding benefits paid during the year, and (4) deducting liability actuarial loss:

Question

8. The Greenberg Corporation has a defined benefit plan. Under the immediate recognition approach, a net defined benefit liability will result at the end of the first year of the plan if:

- the defined benefit obligation exceeds the fair value of the plan assets.

- the fair value of the plan assets exceeds the defined benefit obligation.

- the amount of employer contributions exceeds the net periodic pension expense.

- None of the above.

EXPLANATION: Under the immediate recognition approach, a net defined benefit liability will result at the end of the first year of the plan if the defined benefit obligation exceeds the fair value of the plan assets. (Solution = a.)

Question

9. Kent Company has the following information related to its pension plan as at December 31, 2014:

Under the ASPE immediate recognition approach, the amount to be reported as net defined benefit liability on the December 31, 2014 balance sheet is:

- $1,860,000.

- $1,500,000.

- $1,460,000.

- $1,100,000.

EXPLANATION:

Question

10. Sampat Corp. has a defined benefit plan for its employees, and prepares financial statements in accordance with IFRS. All of the following must be disclosed, either in the body of the financial statements or in the notes, except:

- the characteristics of the defined benefit plans and risks associated with them.

- a schedule showing changes in employees covered by the plan.

- the amounts in the financial statements arising from the plans.

- reconciliations of the opening to closing balances of the net defined benefit liability/asset, plan assets, and the defined benefit obligation.

EXPLANATION: The disclosure requirements for pensions are extensive. Under IFRS, information is disclosed, either in the body of the financial statements, or in the notes to the financial statements, that:

- Explain the characteristics of the defined benefit plans and risks associated with them.

- Identify and explain the amounts in the financial statements arising from the plans.

- Explain how the defined benefit plans may affect the amounts, timing, and likelihood of the cash flows that are associated with future benefits.

- Reconcile the opening to closing balances of the net defined benefit liability/asset, plan assets, and the defined benefit obligation.

- Show the amounts included in periodic net income, including the amounts included in expense, such as current service cost, interest cost, and expected return on plan assets, along with amounts recognized in OCI.

- Show the sensitivity information for each significant actuarial assumption, including the impact on the defined benefit obligation.

(Solution = b.)

Question

11. The following information relates to the Boyd Company's post-retirement benefit plan for 2014:

Under the ASPE immediate recognition approach, the amount of post-retirement benefit expense for 2014 is:

- $82,000.

- $89,000.

- $93,000.

- $97,000.

EXPLANATION: Recall that post-retirement benefit expense is similar to pension expense and, under the ASPE immediate recognition approach, includes current and past service cost, interest cost, a reduction (usually) for the actual return on plan assets, and an adjustment for any liability actuarial gain or loss. Interest cost is the discount rate multiplied by the accrued benefit obligation at the beginning of the year. Therefore, the calculation of post-retirement benefit expense for 2014, under the ASPE immediate recognition approach, is:

Question

12. Assumptions incorporated in the calculation of pension expense should reflect best estimates regarding the effect of future events on the actuarial present value of net defined benefit liability/asset. These assumptions should take into account the following:

- recognition of the past history of the plan; actual experience.

- recognition of the long-term nature of the plan; expected long-term future events.

- recognition of the fact that best estimates are made at a point in time; recent experience.

- All of the above.

EXPLANATION: Assumptions are a matter of professional judgement and should take into account all of the factors listed above. (Solution = d.)

Question

13. Which of the following would not be considered a defined benefit plan?

- Benefit is fixed and based on number of service years.

- Benefit is based on number of service years and returns earned on plan assets up to date of retirement.

- Benefit is based on number of service years and compensation earned by the employee over the entire service period.

- Benefit is based on number of service years and compensation earned by the employee over a specified number of years in the service period.

EXPLANATION: Under a defined benefit plan, the benefit is fixed, and usually calculated by a formula. The answer selections are all formulas (versus exact dollar amounts), but selection “b” has an element of benefit uncertainty related to investment returns. If the benefit is based on number of service years and returns earned on plan assets, economic risk is transferred to the employee, which is the essence of a defined contribution plan. (Solution = b.)