OVERVIEW

Resources or assets of a business are financed either by the business's internal operations or by funds from entities external to the business. Two main external sources of funds are creditors, who are owed liabilities, and owners, who are contributors of equity capital. In this chapter, we begin our in-depth discussion of liabilities.

Due to the nature of business activities, it is common for goods and services to be received with the related payment to be made days or weeks later. Therefore, at a specific point in time, such as at a statement of financial position date, we may find that a business has obligations to pay for merchandise received from suppliers (accounts payable), salaries and wages incurred (salaries and wages payable), and interest incurred (interest payable). The business may also have obligations to remit amounts due to government agencies that are related to property tax incurred (property tax payable), sales tax charged to customers and not yet remitted to the government (sales tax payable), and other amounts due to government agencies in connection with employee compensation (such as withholding taxes payable). These current (short-term) liabilities are classified separately from non-current liabilities, in order to provide information about obligations that will place a demand on the business's current assets.

Non-financial liabilities are more difficult to account for, because there may be uncertainty regarding the existence of a liability and/or measurement amount. Non-financial liabilities, including decommissioning and restoration obligations, product guarantees and customer programs, and contingencies and uncertain commitments, require extensive analysis of relevant facts to determine the proper accounting treatment.

Accounting for current liabilities and non-financial liabilities is discussed in this chapter.

STUDY STEPS

Understanding the Nature of Liabilities

Liabilities

The current definition of a liability is “an obligation that arises from past transactions or events, which may result in a transfer of assets.” Current standards outline that liabilities have three essential characteristics:

- They embody a duty or responsibility.

- The entity has little or no discretion to avoid the duty. (For example, the company must pay vacation pay because an employee has earned it according to the law or the employment arrangement.)

- The transaction or event that obliges the entity has occurred. (For example, the act of the employee working causes the vacation pay obligation to arise.)

The proposed definition of a liability is “a present economic obligation for which the entity is the obligor.” The proposed definition outlines that liabilities have three essential characteristics:

- They exist at the present time (that is, at the statement of financial position date).

- They represent economic burdens or obligations.

- The obligations are enforceable on the obligor entity.

Under the proposed definition of a liability, the third characteristic of a liability requires that the obligation be enforceable on the obligor entity. Note that an obligation need not be legally enforceable to be considered enforceable and therefore a liability. Under the proposed definition, a liability may arise out of a moral, ethical, or constructive obligation. A constructive obligation is one that arises from past or present company practice that signals that the entity acknowledges a potential economic burden.

Under IFRS, a liability is classified as current when one of the following conditions is met:

- It is expected to be settled in the entity's normal operating cycle.

- It is held primarily for trading.

- It is due within 12 months from the end of the reporting period.

- The entity does not have an unconditional right to defer its settlement for at least 12 months after the statement of financial position date.

Under ASPE, the definition of a current liability is similar; however, there are differences in application, which will be highlighted in this chapter.

Financial versus non-financial liabilities

An important distinction is made between financial and non-financial liabilities. Under both IFRS and ASPE, a financial liability is a contractual obligation:

- To deliver cash or other financial assets to another entity, or

- To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity.

- A financial liability is both created by a contract and settled by delivery of cash or another financial asset or financial liability to another entity. Therefore, a key characteristic of a financial liability is the existence of a contract.

- Not all liabilities settled by delivery of cash, financial assets, or financial liabilities are considered financial liabilities. (For example, sales tax payable is a liability created by legislation, not a contract.)

A non-financial liability is often not payable in cash, but instead payable by delivery of goods or services (for example, dismantling and restoring an offshore oil drilling platform at the end of its useful life).

Due to the differing characteristics of financial and non-financial liabilities, measurement of non-financial liabilities is usually less certain than measurement of financial liabilities.

Understanding the Accounting Issues Related to Non-financial Liabilities

This chapter discusses various types of non-financial liabilities, including decommissioning and restoration obligations, unearned revenues, product guarantees and customer programs, contingencies and uncertain commitments, financial guarantees, and commitments.

Decommissioning and restoration obligations

Accounting standards require companies to recognize, in the period when the obligation is incurred (usually in the period of asset acquisition), a liability for future costs of retiring the asset, even though payment for these obligations may be years away. Examples include decommissioning and/or restoration of nuclear facilities, oil and gas properties, mines, and landfills. With these types of assets, at the end of the asset's useful life, the company usually has a legal or constructive obligation to restore the asset and its surrounding area to a certain condition. The best estimate of the present value of the expenditure required to settle the present obligation at the reporting date is included in the cost of the asset. This cost is then depreciated over the asset's useful life. The offsetting liability (asset retirement obligation) remains on the entity's books and is increased to its future value over the asset's useful life. This provides better matching of costs with expected benefits, as well as better predictability of the future obligation to be paid.

Under IFRS, recognition of an obligation related to decommissioning and restoration of a long-lived asset is consistent with the proposed definition of a liability outlined above. Specifically, IFRS requires that the present value cost of both legal and constructive obligations related to decommissioning and restoration be included in the related asset's recorded acquisition cost, with an offsetting credit entry to a liability account (such as Asset Retirement Obligation). Under IFRS, the subsequent costs of producing inventory from the long-lived asset are not included in the asset's capital asset account.

In contrast, under ASPE, only the present value cost of legal obligations related to decommissioning and restoration are included in the asset's recorded acquisition cost (with a similar offsetting credit entry to a liability account such as Asset Retirement Obligation). Under ASPE, the subsequent costs of producing inventory from the long-lived asset are included in the asset's capital asset account.

Product guarantees and warranty obligations

A warranty is a type of product guarantee used by a seller to promote sales. Under a warranty, the seller makes a promise to the buyer to correct certain problems experienced with the product after the point of sale. Because a warranty is a stand-ready obligation that will likely result in significant future costs, it is a liability that should be recorded.

Under the expense approach to recognition of a warranty obligation, all revenues related to the product are recognized in the period of sale, along with an estimated warranty expense and warranty liability. Under IFRS, the estimate is measured using a probability-weighted expected value. Under ASPE, the estimate is usually the value of the most likely estimate.

Under the revenue approach to recognition of a warranty obligation, revenue from sale of the product and related warranty is allocated between revenue recognized in the current period and unearned warranty revenue. Until the unearned warranty revenue is earned, the liability is reported at its sales or fair value on the statement of financial position. The unearned warranty revenue is gradually recorded as it is earned over the life of the warranty, and actual costs incurred to earn the warranty revenue are expensed in the future period(s) when they are incurred. This results in matching of warranty costs with warranty revenue.

More significantly, the revenue approach recognizes that the initial sale was made at the agreed-upon price, partially due to the seller's offer of warranty. Allocating part of the revenue collected upfront to an unearned warranty revenue account is representative of the economic substance of the transaction.

Customer loyalty programs

A customer loyalty program offers award credits to the buyer at the time of sale, redeemable in exchange for future awards or benefits. Under IFRS, the revenue from the original sale transaction should be allocated between the award credits and the other components of the sale, and at the time of sale, the fair value of the award credits should be recognized as unearned revenue. The unearned revenue should be recorded as earned when the award credits are exchanged for the promised awards. Customer loyalty programs are not explicitly addressed under ASPE; however, under ASPE, the revenue recognition criteria should be applied similarly “to the separately identifiable components of a single transaction in order to reflect the substance of the transaction.”

Contingencies and uncertain commitments

A contingency is “an existing condition or situation involving uncertainty as to possible gain or loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur. Resolution of the uncertainty may confirm the acquisition of an asset or the incurrence of a liability.” Contingent gains (gain contingencies or contingent assets) are not recorded.

Currently, both IFRS and ASPE require that only obligations of sufficient likelihood be measured and recorded. However, proposed revisions to the accounting standards for contingencies under IFRS favour recording of all events that represent unconditional obligations as liabilities (consistent with the definition of a liability), and incorporating uncertainty surrounding a particular liability in the measurement of the liability. See Illustration 13-1 for a chart summarizing accounting standards for contingencies and uncertain commitments.

Understanding How Liabilities Fit into the Financial Reporting Model

Financial statement analysis

Proper classification of liabilities between current and long-term is very important, as it impacts key ratios such as the current ratio and the quick (or acid-test) ratio. There may be a bias to show liabilities as long-term (for example, to falsely increase the current ratio).

Key ratios are:

If a company's current ratio exceeds 2:1, it is normally considered acceptable. However, care should be taken to analyze the individual assets and liabilities included in current assets and current liabilities, how quickly the current assets can be realized (or converted into cash), and how quickly the current liabilities will need to be paid. Referring to industry “standards” may also be useful in evaluating a company's ratios.

The quick (or acid-test) ratio benchmark is generally below 2:1 since, by definition, the formula focuses on more liquid assets only.

The current cash debt coverage ratio measures the company's ability to pay off its current liabilities in a specific year with cash provided by its operations.

TIPS ON CHAPTER TOPICS

- Current liabilities are often called short-term liabilities or short-term debt. Non-current liabilities are often called long-term liabilities or long-term debt.

- The key to analysis of a potential liability is analysis of the transaction or event that gives rise to the obligation. If the obligation is unconditional, promised, or required, or if the entity has a stand-ready responsibility to satisfy the obligation as at the statement of financial position date, a liability should be recorded. Any uncertainty about the amount to be paid should be taken into account in the measurement of the liability (for example, by calculating the liability amount as an expected value or probability-weighted average of the range of possible outcomes).

- Standards for classification of debt between current and long-term are more stringent under IFRS than ASPE. For example, if long-term debt becomes callable due to a violation of a debt agreement, IFRS requires that the debt be reclassified as current. In the same situation, under ASPE, the debt may remain classified as long-term under certain conditions. As a second example, if short-term debt is expected to be refinanced (on a long-term basis) after the statement of financial position date but before the financial statements are released, IFRS requires that the debt remain classified as current as at the statement of financial position date, unless at the statement of financial position date, the entity expects to refinance it or roll it over under an existing agreement for at least 12 months and the decision is solely at its discretion. Under ASPE, however, as long as the short-term debt expected to be refinanced is refinanced on a long-term basis before the financial statements are released, the debt can be reclassified to long-term as at the statement of financial position date. In general, regarding classification of debt, IFRS requires that the statement of financial position show conditions existing at the statement of financial position date.

- The difference in standards between IFRS and ASPE for classification of debt between current and long-term can impact key ratios significantly.

- In accounting for product guarantees and customer programs (such as warranties, customer loyalty programs, and premiums and rebates), current standards support a revenue approach. Under the traditional expense approach, the full amount of sales revenue is recognized in the period of the sale, and in the same period, an estimated expense and liability for the product guarantees or customer programs related to the sale are recognized. In contrast, the revenue approach focuses on the nature of the resulting asset and liability in the period of the sale, and therefore on the statement of financial position effect of the transaction. The revenue approach reflects that the original sale is for a bundle of goods and/or services, and that part of the original sale amount should be recorded as unearned if goods and/or services are to be delivered in the future. For example, under the revenue approach, a $10,000 bundled sale, including a warranty with a stand-alone value of $900, would be recorded as follows:

In the period of the sale, under the expense approach, the resulting liability is a warranty liability, whereas under the revenue approach, the resulting liability is an unearned warranty revenue. In subsequent periods, the unearned revenue is recorded as earned, perhaps on a straight-line basis over the service period, or as the goods and/or services are delivered.

- Under the revenue approach, the unearned revenue recorded (such as unearned warranty revenue) is measured at fair value, whereas under the expense approach, the liability recorded (such as estimated warranty liability) is measured at cost.

- Under ASPE, a contingent loss is accrued if both of the following conditions are met: (1) it is likely that a future event will confirm that an asset has been impaired or a liability has been incurred as at the date of the financial statements and (2) the loss amount can be reasonably estimated (measured). If the loss is likely but not reasonably estimable, or if the likelihood of a confirming future event cannot be determined, the item should be disclosed in the notes to the financial statements (but not accrued). If it is only unlikely that a liability has been incurred, no accrual or note disclosure is required.

- Under current IFRS requirements, a loss is accrued if it is probable (or more likely than not) that a liability has been incurred as at the statement of financial position date. If the amount cannot be measured reliably, no accrual is required; however, IFRS indicates that only in very rare circumstances would the amount not be reliably measurable.

- Under current IFRS requirements, the criterion for accrual of a liability related to a contingency (probable, or more likely than not) is a somewhat lower hurdle than the ASPE criterion for accrual of a contingent loss (likely). This may mean that a particular contingency may result in an accrued liability for an entity under IFRS, but not for an entity under ASPE.

PURPOSE: This exercise tests your ability to distinguish between current and non-current (long-term) liabilities.

Chalmers Corporation is a publicly accountable entity. Chalmers’ 2014 financial statements are issued on February 15, 2015.

Instructions

For each of the following items, indicate whether the liability would be reported as current or non-current on Chalmers’ statement of financial position as at December 31, 2014.

- Obligation to supplier for merchandise purchased on credit (terms 2/10, n/30).

- Note payable to bank maturing 90 days after statement of financial position date.

- Bonds payable due January 1, 2017.

- Property tax payable.

- Interest payable on long-term bonds payable.

- Income tax payable.

- Portion of lessee's lease obligations due in years 2016 through 2020.

- Revenue received in advance, to be earned over the next six months.

- Salaries and wages payable.

- Rent payable.

- Note payable to bank maturing six months after statement of financial position date. (Long-term refinancing of the note payable was completed under an agreement dated January 31, 2015.)

- Instalment loan payment due three months after statement of financial position date.

- Instalment loan payments due after one year.

- Portion of lessee's lease obligations due within a year after the December 31, 2014 statement of financial position date.

- Bank overdraft.

- Accrued officer bonus.

- Coupon offers outstanding.

- Cash dividends declared but not paid.

- Unearned rent revenue.

- Stock dividends distributable.

- Bonds payable due June 1, 2015.

- Bonds payable due July 1, 2015; by contract, the bonds payable will be retired using a sinking fund that has been accumulated for this purpose. The sinking fund is classified as a long-term investment.

- Discount to the bonds payable in item 3 above.

- Current maturities of long-term debt.

- Accrued interest on notes payable.

- Customer deposits.

- Sales tax payable.

- Employee payroll withholdings.

- Asset retirement obligation.

- Lawsuit liability (more likely than not, and measurable).

- Warranty liability.

- Unearned warranty revenue.

- Gift certificates outstanding.

- Loan from shareholder.

- Loan payable due on demand.

Solution to Exercise 13-1

Apply the criteria for classification of a liability as current. Recall that under IFRS, a liability is classified as current when one of the following conditions is met: (1) the liability is expected to be settled in the entity's normal operating cycle, (2) the liability is held primarily for trading, (3) the liability is due within 12 months from the end of the reporting period, or (4) the entity does not have an unconditional right to defer settlement of the liability for at least 12 months after the statement of financial position date. ASPE provides a similar definition; however, there are differences in application. ASPE suggests that current liabilities include amounts payable within one year from the balance sheet date or within the normal operating cycle, when that is longer than one year.

As a publicly accountable entity, Chalmers must follow IFRS.

- Current liability (called Accounts Payable).

- Current liability.

- Non-current liability.

- Current liability.

- Current liability; interest on bonds is usually due semi-annually or annually.

- Current liability.

- Non-current liability.

- Current liability.

- Current liability.

- Current liability.

- Current liability; the refinancing agreement did not exist at December 31, 2014 (the reporting date). Under IFRS, the short-term debt expected to be refinanced is reported as a current liability.

- Current liability.

- Non-current liability.

- Current liability.

- Current liability (assuming no other bank accounts with positive balances in the same bank and with a legal right to offset).

- Current liability.

- Current liability; may also classify a portion as non-current liability, if applicable.

- Current liability.

- Current liability or non-current liability, depending on when the revenue is expected to be earned.

- Does not meet the definition of a liability. Usually reported in shareholders’ equity.

- Current liability.

- Non-current liability; even though it is coming due within a year, it will not require the use of current assets to be liquidated.

- Contra non-current liability (deducted from the related bonds payable). Note that current practice also uses the net method of accounting for bonds payable (under which the initial bond payable is recorded at present value, rather than recording the maturity value of the bond in a bond payable account with a [contra] discount on bond payable account that together net to present value).

- Current liability.

- Current liability, generally; in rare cases may be non-current.

- Current liability or non-current liability, depending on the time remaining before they are to be returned or earned.

- Current liability.

- Current liability.

- Non-current liability, generally; current liability if it is coming due within a year.

- Current liability or non-current liability, depending on the date that settlement is expected.

- Current liability and/or non-current liability, depending on term of warranty. (This account title is used under the expense approach to accounting for warranties.)

- Current liability and/or non-current liability, depending on term of warranty. (This account title is used under the revenue approach to accounting for warranties.)

- Current liability, most likely; could have a portion as non-current liability.

- Current liability or non-current liability, depending on the due date of the loan; loans with related parties are required to be separately disclosed; if this loan is due on demand, it must be classified as a current liability.

- Current liability.

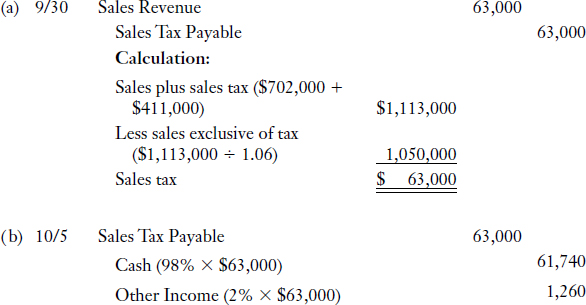

PURPOSE: This exercise provides an example of accounting for an obligation to a provincial or federal government agency for unremitted sales tax.

During the month of September, Rachida's Boutique had cash sales of $702,000 and credit sales of $411,000, both of which include the 6% sales tax that must be remitted to the provincial government by October 15. Sales tax on September sales was lumped with the sales price and recorded as a credit to the Sales Revenue account.

Instructions

(a) Prepare the adjusting entry that should be recorded to fairly present the financial statements at September 30.

(b) Prepare the entry to record the remittance of the sales tax on October 5 if a 2% discount is allowed for payments received by the provincial government by October 10.

Solution to Exercise 13-2

EXPLANATION: Sales tax on transfers of tangible personal property and on certain services must be collected from customers and remitted to the proper government authority. A liability account (Sales Tax Payable) is set up to provide for tax collected from customers but not yet remitted to the government. The Sales Tax Payable account should reflect the liability for sales tax due to the government.

PURPOSE: This exercise will provide you with two examples of accounting for short-term debt expected to be refinanced.

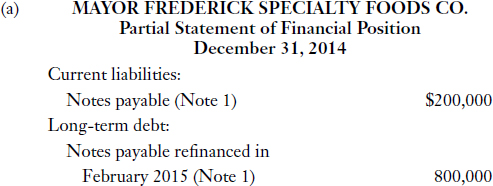

Situation 1

On December 31, 2014, Mayor Frederick Specialty Foods Company had $1 million of short-term debt in the form of notes payable due February 4, 2015. On January 22, 2015, the company issued 20,000 common shares for $41 per share, receiving $800,000 proceeds after brokerage fees and other costs of issuance. On February 4, 2015, the proceeds from the share sale, supplemented by an additional $200,000 cash, were used to liquidate the $1 million of short-term debt. The December 31, 2014 statement of financial position was issued on February 20, 2015.

Situation 2

Included in Hubbard Corporation's liability account balances on December 31, 2014, were the following:

Hubbard's December 31, 2014 financial statements were issued on March 31, 2015. On January 13, 2015, the entire $600,000 balance of the 16% note was refinanced by issuance of a long-term obligation payable in a lump sum. In addition, on March 8, 2015, Hubbard consummated a non-cancellable agreement with the lender to refinance the 14%, $500,000 note on a long-term basis, with readily determinable terms that have not yet been implemented. Both parties are financially capable of honouring the agreement, and there have been no violations of the agreement's provisions.

Instructions

(a) For situation 1, show how the $1 million of short-term debt would be presented on the December 31, 2014 balance sheet, including note disclosure, under ASPE.

(b) For situation 1, show how the $1 million of short-term debt would be presented on the December 31, 2014 statement of financial position, including note disclosure, under IFRS.

(c) For situation 2, explain how the liabilities should be classified on the December 31, 2014 balance sheet, under ASPE. How much should be classified as a current liability? Would classification differ under IFRS? If so, how?

Solution to Exercise 13-3

Note 1—Short-term debt refinanced

As at December 31, 2014, the Company had notes payable totalling $1 million due on February 4, 2015. On February 4, 2015, these notes were partially refinanced on a long-term basis using the $800,000 proceeds received from an issuance of common shares on January 22, 2015. The $200,000 notes payable balance was liquidated using current assets.

Note 1—Short-term debt refinanced

As at December 31, 2014, the Company had notes payable totalling $1 million due on February 4, 2015. On February 4, 2015, these notes were partially refinanced on a long-term basis using the $800,000 proceeds received from an issuance of common shares on January 22, 2015. The $200,000 notes payable balance was liquidated using current assets.

(c) Under ASPE, the entire $600,000 balance of the 16% note may be excluded from current liabilities as at the balance sheet date because it was refinanced on a long-term basis before financial statements were completed and issued. The $500,000 balance of the 14% note may also be excluded from current liabilities because as at the date financial statements were completed and issued, there was a non-cancellable agreement in place to refinance the note on a long-term basis with readily determinable terms, which both parties are capable of honouring.

Under IFRS, $200,000 of the $600,000 balance of the 16% note should be included in current liabilities, because long-term refinancing of this note was not firm as at the statement of financial position date. The $400,000 balance of the note would remain classified as a long-term liability. The $500,000 balance of the 14% note should be included in current liabilities as at the statement of financial position date, because the note did not have a firm long-term refinancing agreement in place as at the statement of financial position date.

APPROACH AND EXPLANATION: Review both ASPE and IFRS classification criteria for short-term debt expected to be refinanced, and apply the criteria to the situations at hand.

Under ASPE, an entity may exclude a short-term obligation from current liabilities if:

- the liability has been refinanced on a long-term basis before the financial statements are completed, or if

- before the financial statements are completed, there is a non-cancellable agreement in place to refinance the liability on a long-term basis, and nothing stands in the way of completing the refinancing.

Under IFRS, a short-term obligation must be included in current liabilities unless, as at the statement of financial position date, there is a firm and existing agreement in place to refinance, and the entity expects to refinance the liability under the agreement for at least 12 months, and the decision is solely at the entity's discretion. Under IFRS, even though the short-term liabilities in situation 2 were refinanced on a long-term basis before financial statements were issued, because the agreements were not entered into until after the statement of financial position date, the short-term liabilities should be classified as current.

Under both ASPE and IFRS, refinancing a short-term obligation on a long-term basis can be done by replacing the obligation with equity securities, as was done in situation 1. Whether refinanced by long-term debt or equity securities, the portion of the short-term obligation to be excluded from current liabilities may not exceed the proceeds from the new long-term debt or equity securities issued that are used to retire the short-term obligation. Similarly, if reclassification of a current liability to long-term is supported by the existence of a financing agreement, the amount of short-term debt that can be excluded from current liabilities cannot exceed the amount to be refinanced under the agreement.

IFRS criteria for long-term classification of short-term debt expected to be refinanced are more stringent than ASPE criteria. If the respective criteria are applied to the same case facts, there may be significantly different working capital and current ratio outcomes under IFRS versus ASPE.

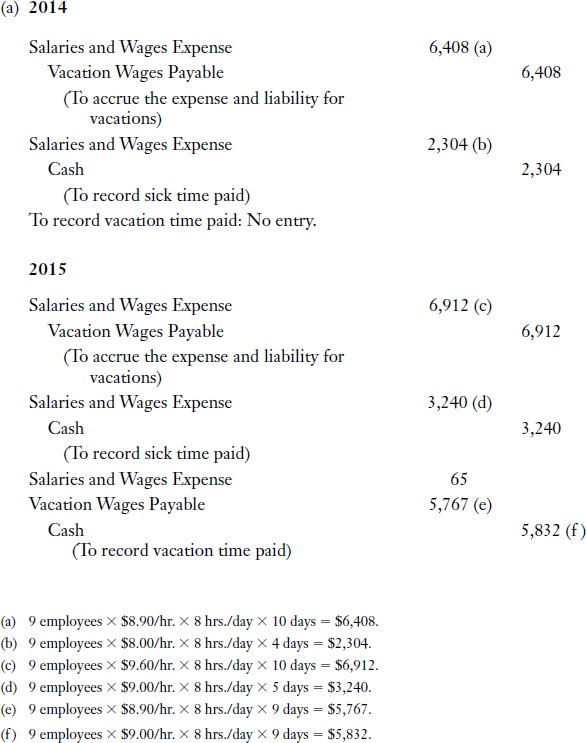

PURPOSE: This exercise will review accounting for compensated absences.

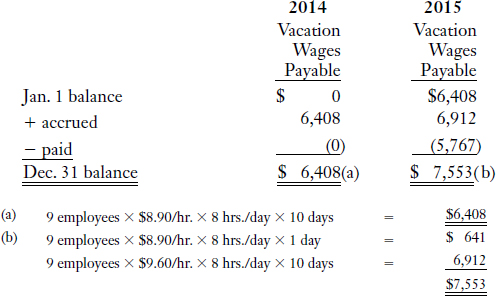

Marsha Diebler Company began operations on January 2, 2014. It employs nine individuals who work eight-hour days and are paid hourly. Each employee earns 10 paid vacation days and six paid sick days annually. Vacation days may be taken after January 15 of the year following the year in which they are earned. Sick days may be taken as soon as they are earned; unused sick days accumulate but do not vest. Additional information is as follows:

Marsha Diebler Company has chosen not to accrue paid sick leave until used, and to accrue paid vacation time at expected future rates of pay without discounting. The company used the following projected rates to accrue vacation time:

Instructions

(a) Prepare journal entries to record transactions related to compensated absences during 2014 and 2015.

(b) Calculate the amounts of any liability for compensated absences that should be reported on the statement of financial position at December 31, 2014 and 2015.

Solution to Exercise 13-4

(b) Accrued liability at year end:

The expense and related liability for compensated absences should be recognized in the year in which the employees earn the rights to those absences. Vacation and holiday pay must be accrued if it vests or accumulates. Sick pay must be accrued only if it vests.

Accounting Treatment of Loss Contingencies

PURPOSE: This exercise will enable you to practise analyzing situations to determine whether a liability should be reported, and if so, at what amount.

Cleese Inc., a publishing company, is preparing its December 31, 2014 financial statements and must determine the proper accounting treatment for each of the following situations:

- Cleese sells subscriptions to several magazines for a two- or three-year period. Cash receipts from subscribers are credited to Unearned Subscriptions Revenue. This account had a balance of $5.3 million at December 31, 2014, before adjustment. An analysis of outstanding subscriptions at December 31, 2014, shows that they expire as follows:

- On June 1, 2014, a suit for breach of contract against Cleese was filed by an author seeking damages of $1 million. The company's legal counsel believes that an unfavourable outcome is likely. A reasonable estimate of the court's award to the plaintiff is in the range between $200,000 and $800,000. The company's legal counsel believes the best estimate of potential damages is $350,000.

- On January 2, 2014, Cleese discontinued collision, fire, and theft coverage on its delivery vehicles and became self-insured for these risks. Actual losses of $40,000 during 2014 were charged to Delivery Expense. The 2013 premium for the discontinued coverage amounted to $75,000, and the controller wants to set up a reserve for self-insurance by a debit to Delivery Expense of $35,000 and a credit to Liability for Self-Insurance of $35,000.

- During December 2014, a competitor company filed suit against Cleese for copyright infringement, claiming $600,000 in damages. In the opinion of management and company counsel, it is possible that damages will be awarded to the plaintiff. The best estimate of potential damages is $175,000.

Instructions

For each of the situations above, prepare the journal entry that should be recorded as at December 31, 2014, under ASPE. Show supporting calculations in good form. Comment on how the liability would be accounted for under current IFRS standards, as well as proposed IFRS standards.

Solution to Exercise 13-5

This situation involves a contingent loss. Because it is likely that a liability has been incurred and the loss is reasonably estimable, a loss should be accrued. Under ASPE, when the expected loss amount is in a range of possible amounts, the best estimate within the range is accrued. If no amount within the range is a better estimate than any other amount, the dollar amount at the low end is accrued and the amount of the remaining exposure to possible loss is disclosed in the notes.

Under current IFRS standards, because an unfavourable outcome is probable (or more likely than not), and the amount is reliably measurable, a loss should also be accrued. However, under current IFRS standards, the accrual amount should be a probability-weighted expected value of the loss, or a sum of possible loss amounts, each multiplied by its probability of actually occurring. Thus, more information would be required to calculate the accrual amount under current IFRS standards.

Under proposed IFRS standards, because Cleese has a present obligation as a result of past events (past transactions with the author), this is an unconditional obligation and a loss should be accrued in the amount of the probability-weighted expected value of the loss. Note that under proposed IFRS standards, this obligation would not be termed a contingent liability; it would be considered an unconditional liability. (Note that the term “contingent liability” is eliminated from proposed IFRS standards.)

Under ASPE, current IFRS standards, and proposed IFRS standards, no entry should be made to accrue for this expense because absence of insurance coverage does not mean that an asset has been impaired or that a liability has been incurred as at the statement of financial position date. Cleese may, however, appropriate retained earnings for self-insurance as long as actual costs or losses are not charged against the appropriation of retained earnings, and no part of the appropriation is transferred to income. Appropriation of retained earnings and/or disclosure in notes to the financial statements is not required, but is recommended.

4. Under ASPE and current IFRS standards, because it is not likely or probable (respectively) that an asset has been impaired or that a liability has been incurred as at the statement of financial position date, no entry should be made for this loss contingency. Under ASPE, notes to the financial statements should include information about the nature of the contingency, the estimated amount of the contingent loss, and the extent of exposure to losses in excess of the estimated amount of loss. Under current IFRS standards, notes to the financial statements should also include an estimate of the loss, information about the uncertainties related to the amount or timing of any outflows, and whether any reimbursements are possible. Under proposed IFRS standards, because Cleese has a present obligation as a result of a past event (copyright infringement), it is an unconditional obligation as at the statement of financial position date, and an entry should be made to accrue the liability. Uncertainty about whether the plaintiff would be awarded any damages would be reflected in the measurement of the liability.

PURPOSE: This exercise will provide an example of accounting for premium claims outstanding.

Beiler Corporation includes one coupon in each box of cereal that it packs and 10 coupons are redeemable for a premium (a toy). In 2014, Beiler purchased 9,000 premiums at 90 cents each and sold 100,000 boxes of cereal at $3.00 per box. Five percent of the amount received from customers relates to the premiums to be awarded. In 2014, 40,000 coupons were presented for redemption. It is estimated that 60% of the coupons will eventually be presented for redemption. This is the first year of this premium offering.

Instructions

(a) Prepare all entries that would be made to record cereal sales as well as the premium plan in 2014, applying the expense approach.

(b) Prepare all entries that would be made to record cereal sales as well as the premium plan in 2014, applying the revenue approach.

Solution to Exercise 13-6

(a) Expense approach:

EXPLANATION: The first entry records the purchase of 9,000 toys that will be used as premiums. The second entry records the sale of cereal (100,000 boxes). The third entry records the redemption of 40,000 coupons, with customers receiving one premium for every 10 coupons. The cost of the 4,000 toys distributed to these customers is recorded by a debit to premium expense. The fourth entry is an adjusting entry at the end of the accounting period to accrue the cost of additional premiums included in boxes of cereal sold this period that are likely to be redeemed in future periods. This is an application of the matching principle and the expense approach to recording estimated premium liability.

(b) Revenue approach:

EXPLANATION: The first entry records the purchase of 9,000 toys that will be used as premiums. The second entry records the sale of cereal (100,000 boxes), and allocation of the sales amount between sales revenue earned and unearned sales revenue related to premiums to be awarded. The third entry records redemption of 40,000 coupons, with customers receiving one premium for every 10 coupons. The cost of the 4,000 toys distributed to these customers is recorded by a debit to premium expense. The fourth entry is an adjusting entry at the end of the accounting period to record sales revenue related to premiums awarded in the period. This is an application of the revenue approach to recording sales revenue related to premiums.

PURPOSE: This exercise will review the journal entries involved in accounting for a warranty that is included with the sale of a product (a bundled sale for which the warranty is not sold separately). Three methods are examined—the cash basis, the expense approach, and the revenue approach.

Colleen Mahla Corporation sells laptop computers under a two-year warranty contract that requires it to replace defective parts and provide necessary repair labour. During 2014, the corporation sold 400 computers for cash at a unit price of $2,000. Similar two-year warranty agreements are available separately and are estimated to have a stand-alone value of $250. On the basis of past experience, the per-unit, two-year warranty costs are estimated to be $90 for parts and $100 for labour. (For simplicity, assume that all sales occurred on December 31, 2014, rather than evenly throughout the year, and any warranty revenue is earned evenly over the two-year period.)

Instructions

(a) Record any necessary journal entries in 2014, applying the cash basis method.

(b) Record any necessary journal entries in 2014, applying the expense approach.

(c) Record any necessary journal entries in 2014, applying the revenue approach.

(d) Under each of the cash basis method, expense approach, and revenue approach, what liability relative to these transactions would appear on the December 31, 2014 statement of financial position and how would it be classified?

In 2015, actual warranty costs to Colleen Mahla Corporation are $14,800 for parts and $18,200 for labour.

(e) Record any necessary journal entries in 2015, applying the cash basis method.

(f) Record any necessary journal entries in 2015, applying the expense approach.

(g) Record any necessary journal entries in 2015, applying the revenue approach.

(h) Under what conditions is it acceptable to use the cash basis method? Explain.

Solution to Exercise 13-7

(d) No liability would be disclosed under the cash basis method of accounting for future costs due to warranties on past sales.

(h) The cash basis method is used mainly for income tax purposes. For financial reporting purposes, cash basis may be used only if warranty costs are immaterial or if the warranty period is relatively short. Usually, the expense approach or revenue approach to warranty recognition is applied, with financial accounting standards transitioning in favour of the revenue approach to recording warranties.

PURPOSE: This exercise will review the journal entries involved in accounting for a warranty that is sold separately from the related product.

Trent Company sells scanners for $800 each and offers each customer a three-year warranty contract for $90 that requires the company to perform periodic services and to replace defective parts. During 2014, the company sold 500 scanners and 400 warranty contracts for cash. It estimates per-unit costs of the three-year warranty to be $30 for parts and $50 for labour. Assume all sales occurred on December 31, 2014, and that revenue from the sale of warranties is recognized on a straight-line basis over the life of the contract.

Instructions

(a) Record any necessary journal entries in 2014.

(b) With respect to these transactions, what liability would appear on the December 31, 2014 statement of financial position and how would it be classified?

In 2015, actual warranty costs related to 2014 scanner warranty sales are $3,800 for parts and $6,000 for labour.

(c) Record any necessary journal entries in 2015 related to 2014 scanner warranties.

(d) With respect to the 2014 scanner warranties, what liability would appear on the December 31, 2015 statement of financial position and how would it be classified?

Solution to Exercise 13-8

The decision to use either the expense approach or the revenue approach to accounting for warranties applies if the warranty is bundled with the sale of the product (if the sale price of the product includes a warranty). If the warranty is sold separately, warranty revenue is initially recognized as unearned (a liability), and recognized as revenue over the period of the warranty contract.

PURPOSE: This exercise will show how to calculate a bonus under two different agreements.

Merry Rawls, president of the Merry Music Company, has a bonus arrangement with the company under which she receives 15% of net income (after deducting tax and bonus) each year. For the current year, income before deducting either the provision for income tax or the bonus is $719,400. The bonus is deductible for tax purposes, and the effective income tax rate is 30%.

Instructions

(a) Calculate the amount of Merry's bonus.

(b) Calculate the appropriate provision for federal income tax for the year.

(c) Recalculate the amount of Merry's bonus if the bonus is to be 15% of income after bonus but before tax (round to the nearest dollar).

Solution to Exercise 13-9

- Examine the equation to calculate the bonus. Make sure it is consistent with the wording of the agreement. For instance, if the bonus is based on net income after bonus and after tax, then income must be reduced by both bonus and tax in your formula (Net Income – B – T) (see part [a]). But if the bonus is based on income after bonus and before tax, then tax is not part of the formula (see part [c])

- Always “prove” the bonus figure calculated.

Proof—parts (a) and (b)

Proof—part (c)

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

1. A current liability is an obligation that:

- was paid during the current period.

- will be reported as an expense within the year or operating cycle that follows the statement of financial position date, whichever is longer.

- will be converted to a long-term liability within the next year.

- is due within 12 months from the end of the reporting period.

EXPLANATION: Before you read the answer selections, review the criteria for classification of a liability as a current liability, and compare each answer selection with the criteria. Under IFRS, a liability is classified as current when one of the following conditions is met: it is expected to be settled in the entity's normal operating cycle, it is held primarily for trading, it is due within 12 months from the end of the reporting period, or the entity does not have an unconditional right to defer its settlement for at least 12 months after the statement of financial position date. (Solution = d.)

Question

2. Reynolds Company borrowed money from Azdouz Company for nine months by issuing a zero-interest-bearing note payable with a face value of $106,000. The proceeds amounted to $100,000. In recording the issuance of this note, what account should Reynolds debit for $6,000?

- Interest Payable

- Interest Expense

- Prepaid Expenses

- Notes Payable

EXPLANATION: The excess of the face value of a zero-interest-bearing note payable and the proceeds collected upon its issuance is the cost of borrowing. This cost of borrowing (interest expense) should be recognized over the months the loan is outstanding. Therefore, the total interest ($6,000) is initially debited to the Notes Payable account. (In the initial entry to record the note, after a $106,000 credit and a $6,000 debit to the Notes Payable account, the Notes Payable account would have a net $100,000 credit balance.) The $6,000 debit included in the Notes Payable account is then amortized (allocated) to interest expense over the life of the note. (Solution = d.)

- A zero-interest-bearing note is often called a non-interest-bearing-note.

- Initially, the $6,000 amount may also be debited to a Notes Payable contra account called Discount on Notes Payable. However, current practice favours the net approach (described above).

Question

3. Martha's Boutique sells gift certificates. These gift certificates have no expiration date. Data for the current year are as follows:

At December 31, Martha should report unearned revenue of:

- $90,000.

- $126,000.

- $261,000.

- $315,000.

EXPLANATION: Draw a T account for the liability and enter the data given.

The gross profit percentage is not used in the calculation of unearned revenue. Revenue and unearned revenue are gross amounts, not net amounts.

Question

4. A local retailer is required to collect a 6% sales tax for the province's department of revenue, and to remit in the month that follows the sale. The retailer does not use a separate Sales Tax Payable account; rather, the sale prices of products sold and the related sales tax are all credited to Sales Revenue at the time of sale. During March 2014, credits totalling $25,440 were made to the Sales Revenue account. The amount to be remitted to the government in April for sales tax collected during the month of March:

- is $1,526.40.

- is $1,440.00.

- is $2,696.64.

- cannot be determined from the data given.

EXPLANATION: Set up a formula to relate the data given, and solve.

Question

5. Included in Arnold Howell Company's liability accounts at December 31, 2014, was the following:

![]()

On February 1, 2015, Arnold issued $5 million of five-year bonds with the intention of using part of the bond proceeds to liquidate the $2-million note payable maturing in May. On March 2, 2015, Arnold used $2 million of the bond proceeds to liquidate the note payable. Arnold's December 31, 2014 balance sheet is being issued on March 15, 2015. Under ASPE, how much of the $2-million note payable should be classified as a current liability on the December 31, 2014 balance sheet?

- $0

- $800,000

- $1,000,000

- $2,000,000

EXPLANATION: Review the definition of a current liability and the ASPE guidelines for classifying short-term debt expected to be refinanced. As at the date the balance sheet is being issued (March 15, 2015), the note payable was refinanced on a long-term basis (it was replaced with five-year bonds), and the proceeds from issuance of the five-year bonds exceeded the amount of the note. Therefore, the entire $2-million note payable should be classified as a long-term liability on the December 31, 2014 balance sheet. (Solution = a.)

Under IFRS, because there was no firm agreement in place to refinance the note on a long-term basis as at the statement of financial position date, the $2,000,000 note would be classified as a current liability on the December 31, 2014 financial statements.

Question

6. An employee's net (or take-home) pay is determined by gross earnings minus amounts for income tax withholdings and the employee's:

- portion of Employment Insurance premiums.

- and employer's portions of Employment Insurance premiums.

- portion of Employment Insurance premiums and Canada Pension Plan contributions.

- portion of Canada Pension Plan contributions.

EXPLANATION: Before you read the answer selections, write down the model for the calculation of net (take-home) pay. Then find the answer selection that agrees with your model.

The employer must also make Canada Pension Plan contributions and pay Employment Insurance premiums on behalf of each employee.

Question

7. An example of a contingent liability is:

- sales tax payable.

- accrued salaries.

- property tax payable.

- a pending lawsuit.

EXPLANATION: Review the definition of a contingent liability and think of some examples before you read the answer selections. Under current ASPE standards, the term “contingent liability” includes the whole population of existing or possible obligations that depend on the occurrence of one or more future events to confirm either their existence or the amount payable, or both. Under current IFRS standards, the term “contingent liability” is used only for those existing or possible obligations that are not recognized. Under proposed IFRS standards, the term “contingent liability” is eliminated. Sales tax payable, accrued salaries, and property tax payable are actual liabilities if they exist at the statement of financial position date. An example of a contingent liability is a pending or threatened lawsuit. (Solution = d.)

Question

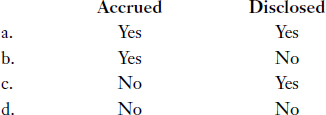

8. Under current IFRS standards, a contingency with an outcome that cannot be determined should be:

EXPLANATION: Under current IFRS standards, a contingency that is probable (or more likely than not) and reasonably measurable should be accrued. If outcomes and/or related probabilities cannot be determined, the contingency should not be accrued but should be disclosed in the notes to the financial statements. Note that under ASPE, a contingency related to an outcome that cannot be determined would also not be accrued, and would be disclosed in the notes to the financial statements. (Solution = c.)

Question

9. Mayberry Co. prepares financial statements in accordance with ASPE and has a contingent loss to accrue. The loss amount is determined to be within a range of possible amounts. No single amount within the range is a better estimate than any other amount within the range. The amount of loss to accrue should be:

- zero.

- the minimum of the range.

- the mean of the range.

- the maximum of the range.

EXPLANATION: Under ASPE, when the predicted loss amount is determined to be within a range of possible amounts, and a specific amount within the range is a better estimate than any other amount within the range, the specific amount (best estimate) is accrued. When no amount within the range is a better estimate than any other amount within the range, the minimum amount within the range is accrued. (Solution = b.)

Question

10. Scott Corporation began operations at the beginning of 2014. It provides a two-year warranty with the sale of its product. Scott estimates that warranty costs will equal 4% of the selling price the first year after sale and 6% of the selling price the second year after the sale. The following data are available:

Under the expense approach, the balance of the Warranty Liability account at December 31, 2015, should be:

- $12,000.

- $42,000.

- $44,000.

- $50,000.

EXPLANATION: Draw a T account, enter the amounts that would be reflected in the account, and determine its balance.

(1) $400,000 × (4% + 6%) = $40,000 expense for 2014. Under the expense approach, the estimated total warranty cost related to the products sold during 2014 should be recognized in the period of sale (2014).

(2) Given (actual expenditures during 2014).

(3) $500,000 × (4% + 6%) = $50,000 expense for 2015.

(4) Given (actual expenditures during 2015).

Because some items are sold near the end of the year and the warranty is for two years, a portion of the warranty liability should be classified as a current liability (the amount pertaining to the actual warranty expenditures estimated to occur in 2016), with the remainder classified as a long-term liability.

Question

11. Crazy Pete Theme Park is self-insured. Premiums for insurance used to cost $100,000 per year before Crazy Pete discontinued coverage. During 2014, Crazy Pete suffered losses of $39,000 that used to be (but are no longer) covered by insurance. Crazy Pete thinks this was a “light” year and that greater losses in future years will offset the lower amount paid in 2014. In order to avoid earnings volatility due to self-insurance, Crazy Pete wants to record a Liability for Self-Insurance. A reasonable estimate of losses to be incurred in 2015 is $120,000. The liability to be reported by Crazy Pete at December 31, 2014, is:

- $0.

- $61,000.

- $100,000.

- $120,000.

EXPLANATION: Even if the amount is estimable, future losses from self-insurance do not result in liabilities as at the statement of financial position date because the company does not have a present obligation as at the statement of financial position date (future losses will result from future events). It is not generally acceptable to accrue future losses from self-insurance. (Solution = a.)

Question

12. Powercell, a manufacturer of batteries, offers a cash rebate to buyers of its size D batteries. The rebate offer is good until June 30, 2014. Under the expense approach, at December 31, 2013, the statement of financial position should include an estimated liability for unredeemed rebates in order to comply with the:

- revenue recognition principle.

- full disclosure principle.

- matching principle.

- time-period assumption.

EXPLANATION: Premium, coupon, and rebate offers are made to stimulate sales, and under the expense approach, their costs should be charged to expense in the period of the sale that benefits from the premium plan. At the end of the accounting period, many of these rebate offers may be outstanding and must be redeemed when presented by customers in subsequent periods. Under the expense approach, the number of outstanding rebate offers to be presented for redemption must be estimated in order to reflect the existing current liability and to match expenses with revenues. An adjusting entry is made with a debit to Premium Expense and a credit to Premium Liability. (Solution = c.)

Current IFRS standards support the revenue approach to accounting for premiums and rebates, under which some of the consideration received from the sale transaction is allocated to unearned revenue. The unearned revenue (representing the consideration from the sale transaction that relates to the premiums or rebates to be awarded) is recorded as earned, in the period(s) in which the premiums or rebates are awarded or settled.

Question

13. The ratio of current assets to current liabilities is called the:

- current ratio.

- quick ratio.

- current asset turnover ratio.

- current liability turnover ratio.

EXPLANATION: Two major ratios used to measure an entity's liquidity are (1) the current ratio and (2) the quick (or acid-test) ratio. The current ratio is calculated by dividing current assets by current liabilities. The quick ratio is calculated by dividing quick assets (cash + marketable securities + net receivables) by current liabilities. Marketable securities in this context refer to short-term (trading) investments. The current ratio is sometimes called the working capital ratio; the quick ratio is often called the acid-test ratio. (Solution = a.)

Question

14. Gary Herlitz, a manager of a local business, is to receive an annual bonus equal to 10% of the company's income in excess of $100,000 before income tax, but after deduction of the bonus. If income before income tax and bonus is $820,000 and the tax rate is 30%, the amount of the bonus would be:

- $14,600.

- $43,091.

- $65,455.

- $72,000.

EXPLANATION: Carefully write an equation that expresses the calculation. Notice what should be deducted from income before the bonus percentage is applied—$100,000 and the bonus (but not tax). Solve for the bonus (B). Prove your answer.

Question

15. The three essential characteristics of a liability include all but which of the following?

- They embody a duty or responsibility.

- The entity has little or no discretion to avoid the duty.

- The obligation is legally enforceable.

- The transaction or event that obliges the entity has occurred.

EXPLANATION: Under current IFRS and ASPE standards, items a., b., and d. are included in the three essential characteristics of a liability. A transaction need not be legally enforceable to be a liability. (Solution = c.)

Question

16. It is important to present current liabilities separately from other liabilities for the following reason:

- When netted against current assets, it shows the working capital position of the company.

- It helps assess the company's liquidity since it shows the company's ability to realize its operating assets for payment of its operating liabilities.

- It helps users predict cash flow needs.

- All of the above.

EXPLANATION: Proper classification of current liabilities is very important for cash flow prediction, liquidity assessment, and assessment of working capital (defined as current assets minus current liabilities). (Solution = d.)

Question

17. Under ASPE, current debt that is expected to be refinanced through long-term debt may be classified as long-term as at the statement of financial position date, if which of the following sets of conditions holds?

- As at the financial statement issue date, there is a non-cancellable agreement in place with a financially solvent lender to refinance the current debt beyond one year, and the company is not in violation of any terms of the contract.

- The company fully intends to refinance the current debt and has contacted several interested parties, all of whom are financially solvent.

- There is a signed agreement to refinance the loan through a demand loan facility with a financially solvent lender, and the company is not in violation of any of the covenants under the agreement.

- The company fully intends to refinance and has a verbal agreement with a financially solvent party, the company is not in violation of any terms of the agreement, and under the terms of the contract, the company may cancel the agreement at any time.

EXPLANATION: The key in selecting the best answer is the concept of a non-cancellable agreement. Answer b. is based on intent and does not provide sufficient assurance; c. is a demand loan, which is technically another current liability; and d. allows the company to back out of the agreement. (Solution = a.)

Question

18. A company lacks fire insurance. Which of the following statements is true?

- This represents a contingent loss and should be accrued in the financial statements if estimable, and disclosed in the notes to the financial statements if not estimable.

- This results in uncertainty as to amounts and timing of losses; however, it should not be accrued since no asset has been impaired and no liability has been incurred prior to the event (the fire).

- This represents a contingent loss with an undeterminable outcome and therefore should be disclosed in the notes to the financial statements.

- This represents an uncertain situation that is unlikely to confirm that an asset has been impaired or that a liability has been incurred; however, disclosure in the notes to the financial statements is required.

EXPLANATION: Acts such as fires are random in occurrence and unpredictable. Since the event giving rise to a potential loss has not yet happened and may never happen, note disclosure is not required (although it may be desirable). Lack of insurance on key assets does represent a significant exposure that users may wish to be aware of (full disclosure principle). (Solution = b.)

Question

19. When analyzing a company's liquidity, which of the following statements is most true?

- The current ratio is the best measure and as long as it is greater than 2:1, the company is fine.

- The current ratio is a good measure of liquidity but it does not take into account the relative liquidity and illiquidity of the current assets.

- Ratios do not give useful information and users should focus on the cash flow statement instead.

- Ratios such as the current and quick ratios provide definitive quantitative information and therefore other information such as the nature of the business need not be considered.

EXPLANATION: The current ratio benchmark of 2:1 is often used; however, it is an incomplete benchmark when considered in isolation. Factors such as (1) the nature of the business, as well as (2) the company's stage of development (such as a start-up versus a mature company) should be considered, along with other factors. While the cash flow statement provides significant information, a better analysis would incorporate assessment of ratios as well as the factors noted above. The quick (or acid-test) ratio takes into account that some current assets are more liquid than others; it is therefore a more sensitive ratio. (Solution = b.)