APPENDIX TO CHAPTER 2

Swap, Spot, and Forward Rates

A2.1 CONTINUOUS COMPOUNDING

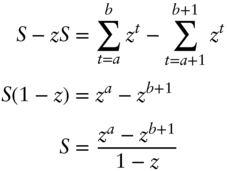

Equation (2.7) gives the proceeds of investing ![]() for

for ![]() periods at the rate

periods at the rate ![]() , which is compounded

, which is compounded ![]() times per year. By the definition of

times per year. By the definition of ![]() , there are

, there are ![]() periods over

periods over ![]() years. Therefore, with

years. Therefore, with ![]() , (2.7) becomes,

, (2.7) becomes,

Under continuous compounding, interest is paid every instant, so that the proceeds of an investment that is continuously compounded over ![]() years grows to the limit of Equation (A2.1) as

years grows to the limit of Equation (A2.1) as ![]() approaches infinity. Taking the logarithm of (A2.1) and rearranging terms,

approaches infinity. Taking the logarithm of (A2.1) and rearranging terms,

Using l'Hôpital's rule, the limit of the right‐hand side of (A2.2) as ![]() becomes large is

becomes large is ![]() . Hence, the limit of (A2.1) is

. Hence, the limit of (A2.1) is ![]() , where

, where ![]() is the base of the natural logarithm. Therefore, if interest is continuously compounded at the rate

is the base of the natural logarithm. Therefore, if interest is continuously compounded at the rate ![]() , an investment of one unit of currency will grow after

, an investment of one unit of currency will grow after ![]() years to,

years to,

Equivalently, the present value of one unit of currency to be received in ![]() years is,

years is,

This section now defines discount factors, spot rates, and forward rates under continuous compounding. Let ![]() be the

be the ![]() ‐year continuously compounded spot rate. Let

‐year continuously compounded spot rate. Let ![]() be the forward rate from

be the forward rate from ![]() to

to ![]() , and define

, and define ![]() to be the continuously compounded forward rate at time

to be the continuously compounded forward rate at time ![]() , that is, the limit of

, that is, the limit of ![]() as

as ![]() approaches zero.

approaches zero.

By Equation (A2.4), spot rates and discount factors are related such that,

Linking forward rates and spot rates is the continuously compounded analog of Equation (2.21),

To link forward rates and discount factors, note that the continuously compounded analogue of Equation (2.20) is,

Then substitute from Equation (A2.5) for each of the two spot rates and rearrange terms to get,

Then take the natural logarithm of both sides and rearrange terms,

Finally, take the limit of both sides of this equation, recognizing that the limit of the right‐hand side is the derivative of ![]() , to obtain,

, to obtain,

where ![]() is the derivative of the discount function with respect to term.

is the derivative of the discount function with respect to term.

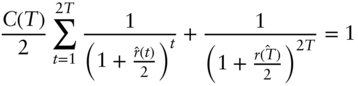

A2.2 RELATIONSHIPS BETWEEN SWAP OR PAR, SPOT, AND FORWARD RATES

This section will work with semiannually compounded rates, though it could easily be cast in terms of other compounding intervals.

Approximation: The ![]() ‐year spot rate is approximately equal to the average of all forward rates to year

‐year spot rate is approximately equal to the average of all forward rates to year ![]() .

.

Start from Equation (2.21), noting that, because interest rates themselves are small numbers, the product of two or more interest rates is particularly small. To illustrate, take the case of the one‐year spot rate, though the argument generalizes easily to longer‐term rates,

where the approximation from (A2.14) to (A2.15) comes from dropping the terms that multiply two rates.

Proposition 1:

Proof: Define ![]() as the left‐hand side of (A2.16). Then,

as the left‐hand side of (A2.16). Then,

and it follows that,

as was to be shown.

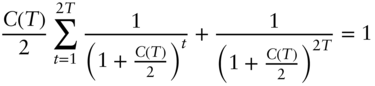

Proposition 2: If the term structure of spot rates is flat, then the term structure of par rates is flat at that same rate.

Proof: Denote the semiannually compounded par rate of maturity ![]() as

as ![]() . If spot rates are flat at the rate

. If spot rates are flat at the rate ![]() , then, by definition of

, then, by definition of ![]() ,

,

Applying Equation (A2.16) of Proposition 1 with ![]() ,

,

But solving (A2.18) for ![]() shows that

shows that ![]() . Hence, the term structure of par rates is flat at

. Hence, the term structure of par rates is flat at ![]() , as was to be shown.

, as was to be shown.

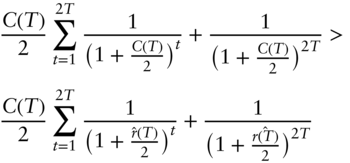

Proposition 3: ![]() if and only if

if and only if ![]() .

.

Proof: The condition ![]() is equivalent to,

is equivalent to,

But, using Equation (2.20) to rewrite the left‐hand side of (A2.19),

as was to be shown.

Proposition 4: ![]() if and only if

if and only if ![]() .

.

Proof: Reverse the inequalities in the proof of Proposition 3.

Proposition 5: If ![]() , then

, then ![]() .

.

Proof: By the definition of the par rate, ![]() ,

,

It is easy to show from Equation (A2.16), setting ![]() , that,

, that,

And, because the term structure of spot rates is assumed to be increasing,

Note that the spot rates in the summation on the top line are ![]() , while those in the summation in the bottom line are all

, while those in the summation in the bottom line are all ![]() .

.

Now, because the left‐hand sides of Equations (A2.22), (A2.23), and (A2.24) are all equal to one, the left‐hand side of (A2.23) can replace the left‐hand side of (A2.24), that is,

which implies that ![]() , which was to be proved.

, which was to be proved.

Proposition 6: If ![]() , then

, then ![]() .

.

Proof: Reverse the inequalities of Equations (A2.24) and (A2.25) in the previous proof to conclude that ![]() , as was to be proved.

, as was to be proved.