1

Cost Accounting—An Overview (General Principles)

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Understand the evolution and scope of cost accounting.

Explain the meaning of cost accounting.

State the objectives of cost accounting.

Know the significance of cost accounting.

Differentiate cost accounting from financial accounting.

Distinguish cost accounting from management accounting.

Understand the concepts of cost.

Classify cost concepts.

Explain the different elements of costs and their components.

Understand the meaning of cost unit and cost centre.

Recognize the items to be excluded from costs.

Appraise the installation of costing system.

Explain the different methods of costing.

Prepare a cost sheet.

Appreciate the role of a cost accountant in an organisation.

Explain the meaning of important terms associated with this chapter.

With the advent of Industrial Revolution followed by Technological revolution, many manufacturing industries have come into existence across the world. Entrepreneurs face cut-throat competition for their survival. Cost factor is a crucial factor for any industrialist. It is natural that a manufacturer has to plan and control cost factor relating to the entire operations. This cost-consciousness necessitated the accountants to devise a new technique of accounting which resulted in the birth of cost accounting. Cost accounting is a branch of accounting which is designed to measure the economic resources consumed in producing goods or providing services. Of late, cost accounting has come to occupy an important and inherent part of economy. Cost accounting is vital and indispensable to modern management for product costing, operational planning and control decisions.

1.1 MEANING OF COST ACCOUNTING

Costing is “the technique and process of ascertaining costs”. These costing techniques comprise principles and rules to ascertain cost of products or services. The techniques vary from industry to industry. According to the definition in the Cost and Financial Accounting Terminology, published by Chartered Institute of Management Accountants (CIMA), London, “It involves the classification, recording and appropriate allocation of expenditure for the determination of the costs of products or services; the relation of these costs to sales values; and the ascertainment of profit ability.” Ascertainment of costs may be done by one of the following ways:

Historical costing: It refers to the ascertainment of costs after they are incurred actually. Cost of a product is determined after production. It is useful for ascertaining costs and not for exercising any control over them.

Standard costing: Here, costs are predetermined. Actual costs are compared with predetermined standard costs and variances are analysed to obtain maximum efficiency.

Marginal costing: It refers to the segregation of costs into fixed and variable. Only variable costs are charged to products or services. Fixed costs are charged to profit and loss account.

Cost accounting differs from costing; however, both are used interchangeably. Cost accounting is a specialised branch of accounting which involves classification, recording, analysing, standardising, comparing, reporting and recommending. The terminology of CIMA defines cost accounting as “the establishment of budgets, standard costs, and actual costs of operations, processes, activities or products; and the analysis of variances, profitability or the social use of funds”.

1.2 OBJECTIVES OF COST ACCOUNTING

The main objectives of cost accounting are:

To determine the cost of a product, process or service

To analyse, classify and record all expenditures with respect to the cost of product, process or service in order to determine its cost

To provide necessary information to the management in time

To provide data needed for periodical preparation of profit and loss account and balance sheets

To serve as a guide by providing actual data for comparison

To facilitate price fixation and offering quotations

To assist budgetary control

To assist cost control and cost reduction

To record the relative production results in each unit of plant to examine efficiency

To provide the basis for production planning and for avoiding wastages of materials and stores

To provide data for different periods and various volumes of output for effective planning and future expansion of business

To provide the basis for making decisions such as:

- To shut down or operate

- To make or buy

- To continue with existing plant/machinery or to replace it

- To determine cost–volume–profit relationship

To assist the management in devising suitable policy decisions in other key areas

1.3 ADVANTAGES OF COST ACCOUNTING

Helps in adverse periods: Cost accounting helps in the periods of economic recession, trade depression and trade competition. In such periods, the management should concentrate on measures to be taken to minimize loss. While taking decision during such periods, cost accounting extends a helping hand to the management to resolve crisis.

Price fixation, Floating tenders, Quotations etc.: Cost records play a vital role in fixing the price of a product, service or process. Cost accounting facilitates such task.

Makes estimates: Proper cost-accounting records provide the basis to prepare estimates and tenders.

Eliminates wastages: Cost of the article or process at each and every stage can be determined with the help of cost records, thereby minimizing wastages that occur.

Maximizes profit: Cost accounting helps in maximizing profit, choosing apt approach for its production. Non-profitable lines may be avoided.

Facilitates comparison: Cost records provide data to compare different periods, which in turn helps the management to take future course of action promptly.

Preparation of final accounts: Cost records provide the necessary accounting information for the preparation of profit and loss account and balance sheet at specified periods promptly.

Inventory control: Costing helps to a great extent with respect to control of stock of raw materials, work-in-progress and finished goods.

Increasing productivity: Productivity of material and labour is inevitable for any organization to attain growth and expansion. Costing helps in these areas to increase productivity.

Enhancing efficiency: As costs are determined at each stage, wastages can be detected and remedial measures can be taken without delay; efficiency of an organization is enhanced, which in turn maximizes the profitability.

Boon to creditors: Costing records serve as a reliable and authentic document by which creditors (investors, banks and money-lending institutions etc.) can repose faith on business organizations and extend advances without any hesitation and with confidence.

Beneficial to employees: Costing records are easily accessible and transparent to employees because of which they are benefitted monetarily by way of incentive, bonus etc. This strengthens the cordial relationship between the employer and employee, and industrial peace environment prevails.

Boost to national economy: Prosperity in industrial sector will reflect in the general economy of any nation by way of increased revenue to the government. Better system of cost accounting paves the way to achieve higher GDP growth of the nation.

1.4 COST ACCOUNTING AND OTHER BRANCHES OF ACCOUNTING

Accounting is classified into:

Financial accounting and

Management accounting

First, we shall look into the relationship between cost accounting and financial accounting. Notwithstanding the fact that both are concerned with systematic recording and presentation of data based on the same records and on the same principles of debit and credit rules, they differ widely in the aspects shown in Table 1.1.

Table 1.1 Differences between Financial Accounting and Cost Accounting

| Basis of Distinction | Financial Accounting | Cost Accounting |

|---|---|---|

1. Aim |

Financial accounting aims at strengthening the interests of the business, proprietors and all others associated with it. |

Cost accounting aims at strengthening the management for proper planning, operation, control and decision-making. |

2. Statutory requirement |

These accounts have to comply with statutory requirements such as company act and income tax act. |

Cost accounts have to comply with the requirements of management. Of late, certain industries have to meet the requirements of company act (only obligatory). |

3. Emphasis |

This emphasizes the measurement of profitability. |

Cost accounting emphasizes ascertainment of costs. |

4. Profit analysis |

This analyses accounts and discloses the profit of the firm as a whole. |

This discloses profit made on each product, process, job or service. |

5. Nature of recording transactions |

Transactions are recorded, classified and analysed in a subject manner, i.e., according to the nature of expenditure. |

Transactions are recorded and analysed in an objective manner, i.e., according to the purpose for which costs are incurred. |

6. Facts and estimates |

Financial accounts deal mainly with facts and figures only. |

Cost accounting deals with facts and figures besides estimates. |

7. Valuation of stock |

Stocks are valued at cost or market price whichever is less. |

Stocks are valued at cost price. |

8. Nature of report of costs |

Costs are reported in aggregate in financial accounts. |

Costs are broken into unit basis in cost accounting. |

9. Relative efficiency |

This does not provide information on the relative efficiency of workers, plant, machinery etc. |

Cost accounting provides information on relative efficiency of workers, plant and machinery. |

10. Type of transactions and basis |

Financial accounts are concerned with external transactions, which form the basis of payment or receipt of cash. |

Cost accounts are concerned with internal transactions, which do not form the basis of payment or receipt of cash. |

11. Periodicity of report |

Financial statements are prepared and reported only at specified period, usually once in a year. |

Cost reports are prepared and reported most frequently, whenever management requires it. |

12. Degree of accuracy |

Financial statements are more accurate as they are subject to scrutiny by statutory authorities. |

These are comparatively less accurate as they are intended mainly for the management. |

13. Classification |

Financial accounts do not classify accounts, expenses etc. |

In cost accounting, they are classified properly and analysed perfectly. |

14. Information |

Proper and adequate information on each aspect of business is not provided to outsiders, though it extends information to outsiders. |

Proper and adequate information on each and every aspect of business is provided to outsiders. |

1.4.1 Cost Accounting and Management Accounting

Some accounting professionals are of the view that cost accounting is a branch of management accounting. Such a close relationship exists between the two categories of accounting. Both are internal to the organization. Both have the same objectives—for instance, both assist management in its functions of planning, controlling and decision-making. Both use more or less similar techniques such as marginal costing and budgetary control. But cost accounting and management accounting differ in certain areas. The main points of distinction between cost accounting and management accounting are shown in Table 1.2.

Table 1.2 Difference between Cost Accounting and Management Accounting

| Basis of Distinction | Cost Accounting | Management Accounting |

|---|---|---|

1. Objective |

Cost accounting is concerned with the ascertainment, allocation, distribution and accounting aspects of costs. |

This is mainly concerned with (i) the impact (ii) effect aspects of costs. |

2. Hierarchy level |

In an organization, cost accountant is placed at a lower hierarchy level than management accountant. |

Management accountant is placed at a higher hierarchy level than cost accountant. |

3. Accounting data |

Cost accounting data are generally derived by using management accounting techniques. |

Management accounting data are derived from cost accounts and financial accounts. |

4. Relevance and objectivity |

Relevance and objectivity of data is not higher in cost accounting compared to management accounting. |

Relevance and objectivity of data is higher than cost accounting. |

5. Usage of tools and techniques |

Tools and techniques used in cost accounting are limited such as standard costing, budgetary control, break-even analysis. |

A wide range of tools and techniques are used such as ratio analysis, cash flow in addition to tools and techniques used in cost accounting. |

6. Period of planning |

Cost account is generally concerned with short-term planning. |

Management account is concerned both with short-term and with long-term planning. |

7. Evaluation of performance |

It is mainly concerned with assisting in management functions and in the evaluation of performance. |

It is concerned with both assisting management in its functions and in evaluating the performance of the management. |

8. Approach |

Cost accounting is generally historical in its approach. It projects the past. |

It is generally futuristic in its approach. |

9. Inclusion of other branches of accounting. |

Cost accounting does not include financial accounting and tax accounting. |

It includes cost accounting as well as tax accounting. |

1.5 CONCEPTS OF COST

It is difficult to define the term “cost”. The term “cost” is ambiguous and uncertain. In general, cost means the amount of resource used in exchange for goods or services. The resources used shall be money or money’s worth, which is usually expressed in monetary units. The terminology of CIMA defines cost as “the amount of expenditure (actual or motional) incurred on, or attributable to, a specified thing or activity”. It may also be defined as Cost is a foregoing, measured in monetary terms, incurred or potentially to be incurred to achieve a specific objective. A cost has to be looked in relation to (i) the nature of business (ii) purpose, (iii) different conditions and (iv) the context in which it is used.

As already said, cost is measured in terms of money. However, costs which do not give rise to actual cash outlay, namely, imputed (actual) or notional cost, are to be considered while decision-making. But these are not available from accounting records—for instance, interest on capital invested by the owner in the firm in notional cost.

Nature of business: A cost has to be studied in relation to its nature of business. For example, a manufacturing organization is interested in knowing the cost per unit of its product, whereas the organizations rendering services such as electricity and transport are interested in ascertaining The costs of services they undertook. The cost per unit can be easily ascertained by dividing the total expenditure by number of units produced or quantum of services rendered. This is relatively easy if the organization produces only a single product. But if more than one product is produced, other factors have to be considered for determining the cost.

Purpose: A cost has to be studied in relation to its purpose. For example, the purpose is fixation of selling price cost. All items of expenditure relating to production, administration and selling will have to be included. But if the purpose is valuation of inventories, only cost of production will have to be taken into account. Hence, the concept of cost varies according to the purpose. It differs from purpose to purpose and has different denotations.

Conditions: A cost has to be ascertained under different conditions also. For instance, while dealing with inventory, work-in-progress is valued at factory cost, whereas stock of finished goods is valued at production cost. Different conditions lead to different modes of valuation of cost. Concept of cost varies thus.

Context: The term “cost” may not stand on its own and has to be qualified. It is a generic term. It is generally used to include all the various types of costs. However, when the term is used specifically, it is always modified with reference to the context costed by such descriptions as prime cost, fixed cost, variable cost, opportunity cost and sunk cost. Each such modification implies a certain attribute which is important in computing and measuring the cost.

Concept of cost is not precise and cannot be pinpointed. It is ever-widening. It has its own terminology. Hence, different costs are to be used for different purposes.

1.6 CLASSIFICATION OF COSTS

Costs may be classified on different bases. They can be classified as follows:

By time (historical, predetermined)

By nature of elements (material, labour, overhead)

By association (product or period)

By traceability (direct, indirect)

By changes in activities or volume (fixed, variable, semi-variable)

By function (manufacturing, administration, selling, research and development)

Controllability (controllable, non-controllable)

Analytical and decision-making (marginal, uniform, opportunity, sunk, differential etc.)

By nature of expense (capital, revenue)

Miscellaneous (conversion, traceable, normal, total)

1.6.1 Classification on the Basis of Time

Costs can be classified into historical costs and predetermined costs.

Historical costs: Historical costs are determined after they are incurred actually. When production is completed, i.e., products reached their final stage of finished status, costs are available and on that basis costs are ascertained. Only on the basis of actual operations, costs are accumulated. Hence they are objective in nature.

Predetermined costs: Costs are calculated before they are incurred, i.e., before the production process is completed.

These predetermined costs may further be classified into estimated costs and standard costs

Estimated costs: Costs are estimated before goods are produced. As these are purely estimates, they lack accuracy.

Standard costs: These costs are also predetermined. But certain factors are analysed with care before setting up costs. Standard cost is not only a concept of cost but a technique or method of costing also.

1.6.2 Classification by Nature or Elements

Elements of costs may be broadly divided into material, labour and expenses.

Direct costs: In general, production is carried on in different cost centres. Costs which can be directly identifiable with cost centres, processes or production units are known as direct costs.

Indirect costs: If costs cannot be identifiable with cost centres or cost units, they are termed as “indirect costs”. Such costs that cannot be easily identifiable with cost centres have to be apportioned on some equitable basis. These terms should be understood properly, as the same will be applied in case of materials, labour and wages.

1.6.2.1 Material Costs

Commodities or substances from which products are produced are called materials. They may be further divided into direct and indirect. The term “direct” means that which can be identified with and allocated to cost centres and cost units. The term “indirect” means that which cannot be allocated but can be apportioned to, or absorbed by, cost centres and cost units.

Direct materials: Direct materials are those materials which enter into and form part of the product, e.g., wood in furniture, chemicals in drugs, leather in shoes. Direct materials include:

All materials specially purchased or requisitioned for a particular process or job or order

All components—purchased or produced

All materials passing from one process to another

All primary packing materials

Indirect materials: Materials which cannot be traced as part of the product are known as indirect materials. Indirect materials include:

Fuel, lubricating oil, grease etc. (for maintenance of plant and machinery)

Tools of small value for general use

Consumable stores

Printing and stationery materials

Stores of small value used

1.6.2.2 Labour Costs

Labour costs can also be classified into direct labour and indirect labour.

Direct labour: Where employees are employed directly in making the product and their work can be easily identified in the process of conversion of raw materials into finished goods, such labour is called direct labour. The cost incurred on direct labour is called direct wages. Example: Wages paid to the driver of a bus in a transport service.

Indirect labour: Labour employed in the works on factory which is ancillary to production is known as indirect labour. The cost incurred on indirect labour is called indirect wages. These costs may not be traced to specific units of output. Wages which cannot be directly identified with a job or process are treated as indirect wages. Example: wages of store keepers, time keepers, supervisors etc.

1.6.2.3 Expenses Costs

Expenses also can be direct and indirect.

Direct expenses: Direct expenses do not include direct material cost and direct labour cost. These expenses are incurred in respect of a specific product. Example: cost of special pattern, drawing or layout; secret formula, hire charges of machinery to execute an order, consultancy fees to a specific job. The latest trend in cost accounting is that these expenses are not taken into account. The terminology of CIMA is also of this view. Generally, direct expenses form a small part of total cost.

Indirect expenses: Expenses which cannot be charged to production directly and which are neither indirect material cost nor indirect wages cost are treated as indirect expenses. Examples: Rent, rates, taxes, power, insurance, depreciation.

1.6.3 Overheads

Overheads include the cost of indirect material, indirect labour and indirect expenses. Overheads may be classified into (i) production or manufacturing overheads, (ii) administrative overheads), (iii) selling overheads and (iv) distribution overheads.

Production or factory overhead: It is the aggregate of indirect material cost, indirect wages and indirect expenses incurred in respect of manufacturing activity. It commences with the supply of raw materials and ends with the primary packing of finished goods.

Administration overhead: It is the aggregate of indirect material cost, indirect wages and indirect expenses incurred for policy formulation, control and administration. Example: Directors’ remuneration.

Selling overhead: It is the cost of creating sales and retaining customers. It is the aggregate of all indirect material costs, indirect wages and indirect expenses incurred in creating and stimulating demand for a firm’s products and securing orders. Example: advertisement, publicity expenses.

Distribution overhead: It is the aggregate of indirect material cost, indirect wages and indirect expenses incurred in preparing the packed products for despatch and making them available to customers. Example: rates and taxes for finished goods, godown expenses.

Various elements of cost are illustrated in Figure 1.1.

Figure 1.1 Various elements of cost

1.6.4 Association with the Product (Costs in Their Relation to Product)

Prime cost: Prime cost is the aggregate of direct material cost, direct wages and direct expenses.

Conversion cost: Conversion cost is the aggregate of direct wages and factory overhead. It is the cost incurred in the factory for the conversion of raw materials into finished goods.

Product costs: Costs included in inventory values are called product costs. In manufacturing organizations, raw material costs and cost incurred in the conversion of raw materials into finished products are called product cost or inventoriable cost. For trading organizations, the cost of goods purchased, and expenses incurred in bringing them to their existing location and in saleable condition are product costs. Product cost is a full factory cost. This is shown as asset in the balance sheet till they are sold off. Product costs are included in the cost of the product. It will not affect the income till it is sold.

Period costs: Period costs are costs that are charged against the revenue of a period of time in which they are incurred. Period costs are incurred on the basis of time like rent and salaries. Period costs include selling and distribution costs and administration costs. Since they are not directly associated with the product, they are not assigned to the product. They are charged to the period in which they are incurred and are to be treated as expenses. In this context, one has to distinguish between expense and expenditure. Expense is nothing but expired cost or expenditure. An organization incurs expenditure in order to acquire goods and services. The same can be said to have expired when consumption takes place, meaning thereby that it has given the intended benefit. Thus, the cost of acquisition of goods for re-sale is an expenditure. But it becomes an expense when the goods are sold and is shown in the profit and loss account.

Direct costs and indirect costs: Already explained in the heading “Direct Materials”.

Joint costs: Joint costs arise when two or more products are processed at the same time or in a single operation or from a common material. To apportion joint costs among products is not an easy affair. If two or more products are produced from the same raw materials (e.g., petrol, diesel, kerosene), joint costs are incurred up to the point of separation.

1.6.5 Accounting Period-Wise Classification of Costs

Capital expenditure: It may be defined as expenditure which results in the acquisition of or increase in an asset, or pertains to the extension or enhancement of earning capacity at a smaller cost. A capital expenditure is intended to benefit future periods. It is classified as a fixed asset. Example: Costs of acquiring land, building and machinery.

Revenue expenditure: This expenditure occurs for the maintenance of assets in working condition and not intended for increasing the revenue-earning capacity. A revenue expenditure benefits the current accounting period. It is treated as an expense.

For matching of costs and revenues, the distinction between capital expenditure and revenue expenditure is inevitable.

1.6.6 Behaviour-Wise Classification of Costs

1.6.6.1 Variable Cost

The terminology of CIMA defines variable cost as “a cost which tends to follow (in the short-term) the level of activity”. Variable costs are also known as marginal costs. Variable costs vary directly and proportionally with the output. Variable cost per unit is constant but the total costs change corresponding to the levels of output. Variable cost is expressed in terms of units only. Variable costs are synonymous with engineered costs. Example: Materials used to manufacture a product, wages of workers in a manufacturing process. To illustrate, let direct material cost to produce one unit of a product be Rs. 25. The existing volume of production is 10,000 units per annum, then the existing direct material cost is 10,000 units × Rs. 25 = Rs. 2,50,000. In case, if the production increases to 20,000 units, the direct material cost would be Rs. 25 × 20,000 units = Rs. 5,00,000. This shows that the direct material cost per unit remains constant but total material cost rises with an increase in activity level. Figure 1.2 depicts the behaviour of variable costs.

Figure 1.2A Total variable cost

Note:

- Figures are not drawn to scale.

- Figures are not based on any figures. (They are only a rough sketch to show the behaviour of variable cost.)

1.6.6.2 Fixed Cost

The terminology of CIMA defines fixed cost as “the cost which accrues in relation to the passage of time and which, within certain limits, tends to be unaffected by fluctuations in the level of activity”.

A going business should have physical facilities and an organization for use. These things provide the capacity to manufacture and sell. The continuing costs of having capacity incurred in anticipation of future activity are termed as “capacity costs”. In case capacity is utilized, additional costs are incurred. Such additional costs of manufacturing and selling are controllable with current activity, while capacity costs tend to continue regardless of the current rate of activity as long as the same capacity is maintained.

Fixed costs are those which are not expected to change in total within the current budget year, irrespective of variations in the volume of activity. Such costs are fixed for a given period over a relevant range of output, on the assumption that technology and methods of manufacturing remain unchanged.

For the purpose of cost analysis, fixed costs may be classified as follows:

Committed Costs: These costs cannot be eliminated instantly. These costs are incurred to maintain basic facilities. Example: Rent, rates, taxes, insurance.

Policy and managed costs: Policy costs are incurred in enforcing management policies. Example: Housing scheme for employees. Managed costs are incurred to ensure the operating existence of the company. Example: Staff services.

Discretionary costs: These are not related to operations. These can be controlled by the management. These occur at the discretion of the management.

To illustrate, a factory manufacturing CDs incurs a fixed cost of Rs. 1,00,000 per annum (which includes rent, depreciation of plant and machinery, insurance of all fixed assets, salaries of staff). The existing volume of production is 10,000 CDs per annum. If the production increases to 20,000 CDs, the total fixed cost remains the same i.e., Rs. 1,00,000 only. But the average fixed cost per unit will come down from (Rs. 1,00,000 ÷ 10,000) Rs. 10 to (Rs. 1,00,000 ÷ 20,000) Rs. 5 per unit. Figure 1.3A and B depict the nature of fixed costs.

1.6.6.3 Semi-Variable Costs

The terminology of CIMA defines semi-variable cost as “a cost containing both fixed and variable elements which is thus partly affected by fluctuations in levels of activity” Semi-variable costs consist of features of both fixed and variable costs. These costs vary in total with changes in the level of activity—not in direct proportion. Due to the fixed part of the element, they do not change in direct proportion to output. Due to the variable part of the element, they tend to change with volume. Semi-variable costs change in the same direction of output but not in the same proportion. Example: electricity charges, stationery, telephone expenses. To illustrate, telephone expenses is a semi-variable cost. Annual rental is Rs.1000. For every call used the charge per call is Re. 1. Here the annual rental is the fixed part of the element—remains unchanged—whereas the call made forms the variable element. It varies as per usage. Figure 1.4 shows the behaviour of semi-variable costs.

Figure 1.3A Total fixed cost

Figure 1.3B Fixed cost per unit

1.6.6.4 Step Cost

Step costs remain unchanged (constant) for a given level of output and then increase by a fixed amount at higher level of output, i.e., from one level of output to another higher level. Example: Salary of supervisors in a factory.

Figure 1.4 Semi-variable cost

Assume that a supervisor can supervise effectively 10 workers, a second supervisor would be needed if workers exceed 10, and a third supervisor if workers exceed 20 and so on. There would be a sudden increase in the salary of the supervisors, if the activity level increases from one range to next.

Depending upon the period up to which an expense can be kept up to a certain level in spite of increase in activity, the height and width of steps vary. In case, if the steps are small and narrow, the behaviour of cost is like that of “pure variable cost”. This is called “step variable cost”. In case, if the steps are wider, cost is like that of “fixed cost”. This is called “step fixed cost”. Figure 1.5A and B show the behaviour of step fixed costs and step variable costs.

Figure 1.5A Step fixed costs

Figure 1.5B Step variable costs

1.6.6.5 Relevant Range

A relevant range is said to be a band of activity (volume) in which a specific form of budgeted sales and cost (expense) relationship will be valid. A fixed cost is regarded as fixed only in relation to a given relevant range and a given time (budget period). Example: (in the fixed cost example) A fixed cost level of Rs.1,00,000 may be valid up to a relevant range i.e., production value of 20,000 CDs per year. Beyond this volume of production, fixed costs would increase as additional capacity has to be increased.

Figure 1.6 shows the behaviour of all three types of costs, viz., fixed costs, variable cost and semi-variable costs.

Figure 1.6 Behaviour of costs

1.6.7 Functional Classification of Costs

Production costs: They are the cost of operating a production department in which manual and machine operations are performed directly upon any part of product manufactured. This includes the cost of direct materials, direct labour, direct expenses, primary packing expenses and all overhead expenses pertaining to production.

Administration costs: These expenses include all indirect expenses incurred in formulating the policy, directing the organization and controlling the operation of a concern. The expenses relating to selling and distribution, production, development and research functions are not to be included under this head.

Selling and distribution costs: These expenses include all expenses incurred with selling and distribution functions.

Research and development costs: These include the cost of discovering new ideas, processes or products by research and the cost of implementation of such results on a commercial basis.

Preproduction costs: when a new manufacturing unit is started or a new product is launched, certain expenses are incurred. There would be trial runs. All such costs are called preproduction costs. They are charged to the cost of future production because they are treated as deferred revenue expenditure.

1.6.8 Costs for Planning and Control

Controllable cost: The terminology of CIMA defines controllable cost as “a cost which can be influenced by the action of specified member of an undertaking”. It refers to those costs which may be regulated at a specified level of authority (management) within a specified time period. The term “controllable costs” means variable costs. Cost-control factor depends on time factor and level of managerial authority. If the time period is sufficiently long, cost can be well controlled. Proper delegation of authority with responsibility facilitates the task of control of costs.

Uncontrollable costs: Uncontrollable cost is defined as the “cost which cannot be influenced by the action of a specified member of an undertaking”. This cost is not subject to control at any level.

The difference between the terms is important for the purpose of cost control, and responsibility accounting costs which are not subject to the control of a person should not be charged to that person. For instance, a foreman should not be charged with the plant superintendent salary. The foreman should be charged only with such items as usage of materials, direct labour, supplies. Further, it must be noted that the distinction between controllable and uncontrollable cost is not absolute. It is made in relation to a given member of an organization. A cost which is considered uncontrollable by a manager can be controlled by a higher official. Examples of uncontrollable cost: rent, salary of staff, depreciation.

Budget: A budget is a plan for a future period. It is expressed in monetary terms. The terminology of CIMA defines a budget as “ a plan quantified in monetary terms, prepared and approved prior to a defined period of time usually showing planned income to be generated and/or expenditure to be incurred during that period and the capital to be employed to attain a given objective”. It is also a tool of control.

Standard costs: Standard costs are closely related to budgets, and both are said to be complementary to each other. It is a basic accounting tool. A standard cost is a predetermined calculation of how much costs should be under specific working conditions. It is built up from an assessment of the value of cost elements and correlates technical specifications and quantification of material, labour and other costs to the prices and/or wage raves expected to apply during the period in which standard cost is intended to be used. Its main purposes are to provide bases for control through variance accounting, for valuation of stock, and work-in-progress and in some cases, for fixing selling prices.

1.6.9 Costs for Analytical and Decision-Making Purposes

Imputed costs: Imputed costs do not involve actual cash outlay (cash payment). They are not recorded in the books of accounts. They are not measurable accurately. However, imputed costs are useful while taking decisions. Imputed costs can be estimated from similar situations. Imputed costs can be estimated from similar situations outside the organization. Although these are hypothetical costs, in making comparison, in performance evaluation, in making decision, the inclusion of imputed costs is inevitable. Examples: Interest on invested capital, rental value of company-owned building, salaries of owner-directors of sole proprietorship firms.

Sunk costs: Sunk cost is invested cost or recorded cost. A sunk cost is one which has been incurred already and cannot be avoided by decision taken in future. Sunk cost may be defined as “an expenditure for equipment or productive resources which has no economic relevance to the present decision-making process”. Sunk cost is a past cost which cannot be taken into account in decision making. Sunk cost may also be defined as the difference between the purchase price of an asset and its salvage value. Non-incremental costs (i.e., cost which do not increase) are also, at times, termed as sunk costs (one specific group of non-incremental costs).

Differential costs: Differential costs arise on account of the change in total costs associated with each alternative. In the language of the AAA committee, “it is the increase or decrease in total costs, or the changes in the specific elements of cost that results from any variation in operation.” Differential cost consists of both variable and fixed costs. The differential cost between any two levels of production is (i) the difference between two marginal costs (variable cost) at these two levels and (ii) the increase or decrease in fixed costs. A distinction has to be understood between differential cost and incremental cost. Incremental cost applies to increase in production and restricted to cost only, whereas differential cost confines to both increase or decrease in output.

Differential cost is of much use in decision-making process, especially in choosing the best alternative and in ascertaining profit where additional investments are introduced in the business.

Opportunity costs: Opportunity costs are the economic resources which have been foregone as the result of choosing one alternative instead of another. The unique feature of an opportunity cost is that no cash has changed hands. There is no exchange of economic resources. It results from sacrificing some action. They are never shown in regular cost accounting records.

Example:

Some amount—say, Rs. 5,00,000—in the purchase of one modern equipment which is necessary to run the business. This amount, as present, cannot be invested in equity shares of dividends. The loss of interest that would have been earned from this type of investment (shares and debentures) is the opportunity cost. One alternative—investing in equipment—is chosen over another alternative (investing in shares and debentures is sacrificed). The economic resources—interest from debentures—have been foregone, which is termed as opportunity cost. Its role is important in decision-making process.

Postponable costs: These are costs which may be postponed to the future with little or no effect on current operations. Actually it means deferring the expenditure to some future date. It does not mean that the cost is avoided and rejected summarily. Example: Repairs and maintenance.

Avoidable costs: By choosing one alternative, costs may be saved. That means by avoiding one, and choosing another, costs can be saved. Example: By not manufacturing a new product, the appropriate direct material, labour and variable costs can be avoided.

Out-of-pocket costs: Out-of-pocket cost means those elements of cost which warrant cash payment in the period under consideration. This is helpful in deciding whether a particular venture will at least return the cash expenditure caused by the expected project. Example: Taxes, insurance premium, salaries of supervisory staff, etc.

Relevant costs: Relevant costs are those expected future costs that differ between alternatives. It is a cost affected by a decision at hand. Historical costs are irrelevant to a decision. It is reasonable because it helps to ascertain whether the costs are relevant to a particular decision at the present condition. In general, variable costs are affected by a decision and so they are considered relevant.

Uniform costs: Generally they are not distinct costs as such. According to this, common costing principles and procedures are being adopted by a number of firms. These costs are mainly intended for inter-firm comparison.

Marginal costs: It is the aggregate of variable costs. It is useful in various ways for the management.

Common costs: Common costs are those costs which are incurred for more than one produce, job territory or any other specific costing object. The National Association of Accountants defines common costs as “the cost of services employed in the creation of two or more outputs, which is not allocable to those outputs on a clearly justified basis”.

1.6.10 Other Costs

Normal cost: This cost is incurred at a given level of output in the conditions that level of output is achieved.

Traceable cost: This cost can be easily identified with a product or job or process.

Total costs: It denotes the sum of all costs in respect of a particular process or unit or job or department or even the entire organization.

1.7 COST OBJECTS

Cost object is anything in respect of which a separate measurement of cost is desirable. There are several purposes of cost accumulation. Keeping in view the objectives of cost accumulation, the objects for which costs are computed are to be identified. These are known as cost objects. To illustrate, when it is shown that the cost of production centre is Rs. 1,00,000, it means that the cost centre is the production centre whose cost is Rs. 1,00,000. Cost objects are of the following types: cost unit and cost centre.

1.7.1 Cost Unit

The terminology of CIMA defines cost unit as “a quantitative unit of product or service in relation to which costs are ascertained”. It refers to a unit of product or service or time or combination of these which are to be used for the purpose of ascertainment of cost through the process of allocation, apportionment or absorption. The definition of cost unit varies from industry to industry. The forms of measurement are the units of physical measurements such as weight, number, value, time, length and weight. Examples are given in Table 1.3.

Table 1.3 Examples of Cost Unit

| Industry/Product/Service | Cost Unit |

|---|---|

Bricks |

Per 1000 bricks |

Cement, steel, sugar |

Per tonne |

Hospital |

Per patient day |

Consultancy |

Per consulting hour |

Transport |

Per passenger. Km |

Drugs |

Per batch |

Chemicals |

Per litre, tonne |

While selecting a cost unit, the following factors have to be considered:

Nature of business

Organization of factory

Management policy

Availability of information

Relevancy of purpose for which it is needed

Costing system in vogue in the entity

1.7.2 Cost Centre

Costs are to be ascertained by cost centre or cost unit or by both. The terminology of CIMA defines a cost centre as “a location, function, items of equipment in respect of which costs may be ascertained and related to cost units for control purposes”. To control costs effectively, the factory has to be divided into a number of departments. It will be not only unwieldy, but it loses its essence and effectiveness if whole factory is treated as a single unit. Hence subdivision of factory into a number of departments is essential. Further, these departments can be subdivided into various cost centres based on their activities. Costs collected such centre-wise may be compared with standards, budgets or estimates for the purpose of control and fixing responsibility. Examples of cost centres: work office, quality control department, sales office, milling machines.

1.7.2.1 Type of Cost Centres

Cost centres may be categorized into (1) personal and (2) impersonal.

Personal cost centre: It is composed of a person or group of persons in relation to which costs are ascertained and used for the purpose of control. Examples: Factory manager, sales manager.

Impersonal cost centre: A cost centre which consists of a location, department, plant or items of equipment is referred to as impersonal cost centre. Examples: Machine shop, milling machines.

However, the cost accountant classifies cost centres into the following categories:

Production cost centre: Cost centres which are involved in production activity are known as production cost centres. They are involved in the conversion of raw material input into finished goods.

Process cost centre: A process cost centre is an organizational unit. A given process or a continuous sequence of operation is carried on in that unit. For instance, fermentation process in a brewery is a process cost centre.

Service cost centre: A cost centre which provides service to other departments is called service cost centre.

Example:

Tool room in a factory, boiler house.

The proper selection of a suitable cost centre is vital for the ascertainment and control of cost.

1.7.3 Profit Centre

If the performance in a responsibility centre is measured in terms of both the revenue it earns and the cost it incurs, it is known as profit centre. Differences between profit centre and cost centre are shown in Table 1.4:

Table 1.4 Differences between Profit Centre and Cost Centre

| Basis of Distinction | Cost Centre | Profit Centre |

|---|---|---|

1. Objective |

Cost centres are created to ascertain costs and control costs. |

Profit centre is created to delegate authority and fix responsibility to individual to measure performance. |

2. Autonomous |

Cost centres are not autonomous |

Profit centres are autonomous |

3. Target |

Cost centres do not have target costs. |

Profit centres have a profit target. |

4. Numbers |

Cost centres are large in numbers. |

Profit centres are less in number mostly department wise created. |

5. Coverage |

Cost centre is the smallest unit of activity where costs are collected and revenues are ignored. |

Profit centre is a big unit which is responsible for both revenues and costs. |

1.8 METHODS OF COSTING

The methods used for the calculation of cost per unit of output are known as costing methods. Different methods are available for the calculation of the cost per unit of output. The choice of a specified method depends on the manufacturing process. According to the terminology of CIMA, there are two generic classes of costing methods:

Specific order costing

Process costing

Specific order costing: This is also known as job costing or terminal costing. This category of costing method is suitable for the work (job, batch, contract) of separate identity in nature which is mostly authorized by a specific order. Under this category, job costing, batch costing, contract costing are included.

Process costing: This is also known as operation costing or period costing. This category of costing method is suitable for industries manufacturing goods using a series of continuous or repetitive processes or operations. Under this category, operation costing (single unit or output and multiple), process costing, and some times batch costing are included.

These methods are discussed briefly.

1.8.1 Process Costing

Process costing: This is suitable for industries manufacturing goods using a series of continuous or repetitive processes or operations. Many units of the same product are manufactured during a period. Examples: paper, soap, paint, textiles and chemicals. Under this method, costs are assigned to each process and the product cost assigned on an average basis.

Operation costing (One operation costing): This is also known as unit or output costing. This is suitable for industries where manufacture is continuous and units are identical. Example: brick kilns, paper mills. Under this method, the entire production cycle is costed and the total accumulated cost is divided by the number of units produced to ascertain cost per unit.

Operation costing (Multiple operation costing): This method of manufacture consists of a number of distinct operations. Usually this method refers to conversion cost—the cost of converting raw materials into finished goods. Input units and cost are determined after taking into account the rejections in each operation. The cost per unit is ascertained with reference to final output.

Multiple costing: This is also known as composite costing. This is suitable for industries where a number of component parts are produced separately but all are assembled in the final product. In such industries (e.g., cycle, radio, automobile), a combination of different costing methods are used. This method is not included in the terminology of CIMA, of late.

Service costing: This is also known as operating costing. This is suitable for concerns which render services. Examples: transport, power, hospitals, canteens. This method is applied to ascertain the cost of services rendered. This is usually expressed in compound units.

Examples:

Transport → Tonne, kilometres

Power supply → Kilowatt-hour

Hospital → Patient day

1.8.2 Specific Order Costing

Job costing: In this method, costs are accumulated for each job. Each job is distinctly identifiable. This method is suitable for industries like printing, foundries. A job card is to be prepared for each job for cost accumulation.

Contract costing: This is a variation of job costing. This method is used when the job is spread over more than one accounting period. This method is suitable for industries involved in building construction and civil engineering. In this method, costs which are found to be common to different contracts and cannot be identified in an economical manner with individual contracts are assigned on an equitable basis to each contract.

Batch costing: This is another variation of job costing. This method is used where similar or identical items are manufactured as a batch in large quantities. This method is suitable for industries manufacturing general-purpose machine tools, bakeries, garments, spare parts, accessories. In this method, the accumulation of costs is done for each specific batch. The cost per unit is ascertained by dividing the cost of the batch by the number of units produced in a batch.

Cost units and methods of costing for different industries are depicted in Table 1.5 in the summarized form.

Table 1.5 Cost Units and Methods of Costing for Different Industries

| Industry | Cost Unit | Method of Costing |

|---|---|---|

1. Sugar |

Quintal |

Process |

2. Chemicals |

Kilogram |

Process |

3. Cement |

Kg; tonne |

Process |

4. Timber |

Cubic foot |

Process |

5. Confectionery |

Kilogram |

Process |

6. Automobile |

Number |

Process |

7. Soft drinks |

Per bottle |

Process |

8. Oil Refinery |

Per tonne—quintal |

Process |

9. Bicycle |

Number |

Multiple |

10. Hospital |

Per bed /per day or number of patients (OP) |

Service |

11. Transport |

Tonne—km or Passenger km |

Service |

12. Advertising |

Per ad |

Job |

13. Interior Decoration |

Per job |

Job |

14. Garments |

Number |

Batch |

15. Pharmaceutical |

Per number |

Batch |

1.9 TECHNIQUES OF COSTING

The way in which cost information is presented to the level of authority in an organization is referred to as costing techniques. Though there are a wide variety of techniques, the following are the widely used techniques for ascertainment of costs:

Historical costing: It is a technique of costing for the ascertainment of costs after they are incurred. Comparison of costs for different periods may be possible by the results obtained under this technique. It is of limited use because of the historical nature.

Marginal costing: In this technique, costs are segregated into fixed and variable. It is employed to determine the effect of changes in volume or type of output on profit. This is used for making cost-based short-term tactical decisions to maximize the profit of an organization with available resources.

Cost–volume–profit analysis: This technique is employed to analyse the pattern of cost behaviour and cost–volume–profit relationship in order to assist in short-term profit planning.

Budgetary control: This technique is used as a tool for planning and control.

Standard costing and variance analysis: Under this technique, a comparison is made of the actual cost incurred and the standard cost predetermined. Any variance is analysed by causes. Suitable corrective action is taken by the management by investigating the causes for such variances.

Direct costing: All direct costs are charged (variable and fixed in respect of products). All the other costs are to be written off against profits.

Absorption costing: All costs are charged, irrespective of fixed or variable, to operations, processes or products.

Uniform costing: Same costing procedure is applied by several undertakings for common control. It may also be used for the purpose of comparison of costs.

1.10 ELEMENTS OF COST

The principal constituents of elements of cost are material, labour and expenses.

1.10.1 Material

Elements of cost has already been discussed under the heading “Classification of costs by nature or elements of cost” in the earlier part of this chapter.

Now, computation of total costs of elements is explained as follows.

1.10.1.1 Components of Total Cost

Prime cost: It is the aggregate of direct material cost, direct labour cost and direct expenses.

Factory cost: It is the aggregate of prime cost and factory overheads. Factory cost is also termed as “works cost” or “production cost” or “manufacturing cost”.

Office cost: It is the aggregate of factory cost and office and administration overheads. This is also known as administrative cost or total cost of production.

Total cost: It is the aggregate of office cost and selling and distribution overheads. This is also called cost of sales

In the determination of different components of cost, certain adjustments have to be carried out for inventories of raw materials, work-in-progress and finished goods as follows:

Consumption of raw material (or) material used:

Work-in-progress: It has to be adjusted with works cost (i.e., after computation of prime cost but before determining works cost)

Finished goods: It has to be adjusted with cost of production (i.e., after computation of works cost but before determining cost of production)

Cost of production of goods sold or cost of goods sold

= Cost of production + Opening stock of finished goods − Closing stock of finished goods

1.10.1.2 Analysis of the Components of Total Cost

An analysis of the total cost of production and cost of sales is carried out by preparing “Cost sheet”. A Cost sheet is an important document prepared by the costing department. Cost sheet is prepared to analyse the components of total cost, thereby determining (i) prime cost, (ii) works cost, (iii) cost of production, (iv) cost of sales and (v) profit. All aspects discussed are presented in the format or specimen of a cost sheet which is shown in Table 1.6:

Table 1.6 Specimen of Cost Sheet

| Particulars | Amount (Rs.) |

|---|---|

1. Direct Material |

– |

2. Direct Labour |

– |

*13. Direct Expenses |

– |

4. PRIME COST (Add 1 + 2 + 3) |

×× |

5. Add: Factory overhead |

– |

6. WORKS COST (or) FACTORY COST {Add 4 + 5} |

×× |

*27. Add: Administration overhead |

– |

8. COST OF PRODUCTION (6 + 7) |

×× |

9. Add: Selling and distribution overhead |

– |

10. TOTAL COST (or) COST OF SALES |

×× |

11. PROFIT |

– |

12. SALES |

×× |

Cost Sheet Depicting Components of Total Cost

NOTES:

As per the Terminology of CIMA, direct expenses are not included in prime cost.

Office cost is not added separately to works cost, but added along with selling and distribution overhead with works cost to arrive at total cost. Further, they prefer “Administration” instead of “Office”.

Adjustments for Opening and closing stock of (i) raw materials, (ii) work-in-progress and (iii) finished goods have to be carried out with respective items, as discussed earlier.

Illustration 1.1

You are required to calculate (i) prime cost, (ii) works cost, (iii) total cost of production and (iv) cost of sales, from the following particulars:

| Rs. | |

|---|---|

Raw materials consumed |

30,000 |

Wages paid to labourers |

12,000 |

Chargeable expenses—Direct |

1,000 |

Wages of foreman |

2.000 |

Wages of store keeper |

1,000 |

Electricity : Factory |

2,500 |

Office |

500 |

Rent : Factory |

1,500 |

Office |

500 |

Depreciation: Plant and machinery |

600 |

Office furniture |

200 |

Consumable stores |

1,000 |

Manager’s salary |

3,000 |

Office printing and stationery |

500 |

500 |

|

Salesmen’s salary and commission |

1,500 |

Travelling expenses |

300 |

Carriage outward |

100 |

Advertising |

300 |

Warehouse charges |

200 |

Solution

Illustration 1.2

From the following particulars, calculate:

Cost of raw-materials consumed

Prime cost

Works/manufacturing cost

Cost of Goods sold

Total cost of production

Total cost and

Profit

| Rs. | |

|---|---|

Opening stock |

|

Raw materials |

10,000 |

Finished goods |

5,000 |

Raw material purchased |

60,000 |

Wages paid to labourers |

25,000 |

Directly chargeable expenses |

3,000 |

Rent, rates and taxes |

4,000 |

Power |

2,500 |

Factory heating and lighting |

2,000 |

Factory insurance |

1,000 |

Sale of wastage of materials |

500 |

Office management salaries |

5,000 |

Office printing and stationery |

300 |

Salesmen salary |

3,000 |

Travelling expenses |

1,200 |

SALES |

1,75,000 |

Closing stock |

|

Raw materials |

7,000 |

Finished Goods |

10,000 |

Solution

Adjustment for raw materials opening stock and closing stock is to be made before determining the prime cost as illustrated above.

Any sale value realized by way of wastage of materials has to be deducted to arrive at cost of raw materials consumed.

Adjustment for finished stock-opening and closing stock is to be made before arriving at cost of production of goods sold as illustrated above.

Illustration 1.3

The following inventory data relate to XL Ltd:

| Inventories | |||

|---|---|---|---|

Beginning (Rs.) |

Ending (Rs.) |

||

Raw materials |

72,000 |

80,000 |

|

Work-in-progress |

75,000 |

90,000 |

|

Finished goods |

1,20,000 |

1,00,000 |

|

| Additional Information | (Rs.) |

||

| Cost of goods available for sale | 7,15,000 |

||

| Total goods processed during the period | 6,75,000 |

||

| Factory overheads | 1,21,000 |

||

| Direct materials used | 1,64,000 |

||

You are required to determine:

Raw material purchased

Direct labour cost incurred

Cost of Goods sold.

[B.Com (Hons) Delhi. Modified]

Solution

Determination of raw material used

Step 1: Formula:

Raw materials used = Opening stock + Purchases − Closing stock

or Purchases = Raw materials used − Opening stock + Closing stock.

Step 2: Now, substituting the given values in the above formula, we get

Purchases

=

Rs. 1,64,000 − Rs. 72,000 + 80,000

=

Rs. 1,72,000

Determination of direct labour cost

Procedure:

First, determine Prime cost from cost of goods processed, by deducting opening work-in-progress and factory overheads.

Then, from prime cost deduct the cost of raw material used to arrive at direct labour cost.

Determination of Cost of Goods sold

Formula:

=

Cost of Goods Sold = Cost of goods available for sale − Closing stock of finished Goods

=

Rs. 7,15,000 − Rs. 1,00,000

=

Rs. 6,15,000.

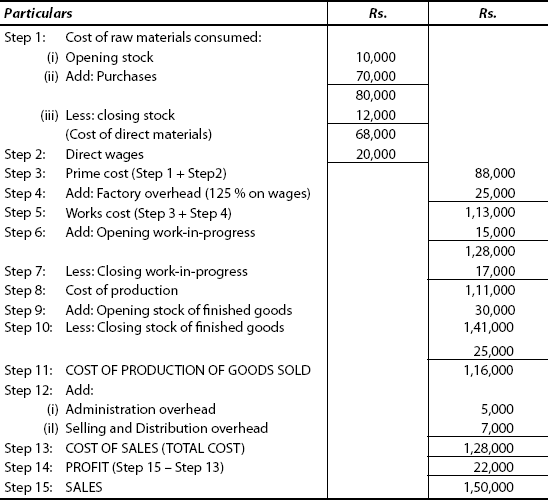

Illustration 1.4

ABC Co Ltd. is engaged in the manufacture of product “P”. Its records reveal the following data for 31 March 2010:

Direct Wages: Rs. 20,000

Factory overhead: 125% of direct wages

| 31 March 2009 Rs. | 31 March 2010 Rs. | |

|---|---|---|

Raw Materials |

10,000 |

12,000 |

Work-in-progress |

15,000 |

17,000 |

Finished goods |

30,000 |

25,000 |

Administration overhead |

|

5,000 |

Purchases |

|

70,000 |

Selling overhead |

|

7,000 |

Sales for the year |

|

1,50,000 |

Prepare a cost statement.

Solution

NOTE: Cost statement is prepared on the basis of present concept of product cost. Administration overhead is excluded from the cost of production and treated as period cost and charged against the revenue for the period.

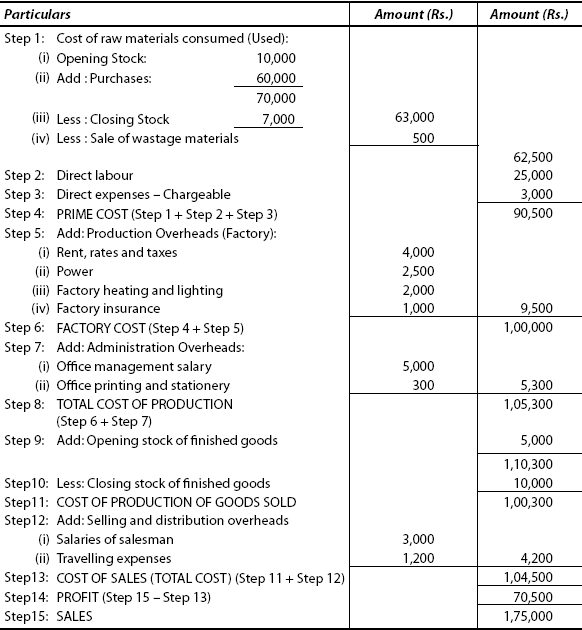

Illustration 1.5

The books and records of Good Luck Manufacturing Co. present the following data for the month of January 2010:

Direct labour cost: Rs. 32,000 (160% of factory overhead)

Cost of goods sold: Rs. 1,12,000

Inventory accounts showed these opening and closing balances:

|

January 1 |

January 31 |

|

Rs. |

Rs. |

Raw material |

16,000 |

17,200 |

Work-in-progress |

16,000 |

24,000 |

Finished goods |

28,000 |

36,000 |

Other data:

Selling expenses |

6,800 |

General and administration expenses |

5,200 |

Sales for the month |

1,50,000 |

You are required to prepare a statement showing cost of goods manufactured and sold and profit earned.

[C.A. (Inter) and B.Com (Hons) − Delhi. Modified]

Solution

Cost of material consumed is to be ascertained as follows:

NOTE: In this problem, General and administration overheads are included in cost of production. Students should be able to understand both the concepts: (i) Exclusion of administration expenses from cost of production (as shown in Illustration 1.4) and (ii) Inclusion of administration expenses (overhead) in cost of production as is explained in this illustration.

Based on this, cost of raw material is determined thus: cost of goods sold and cost of production of goods sold are treated alike.

Step 1 → Cost of goods sold |

|

1,12,000 |

Step 2 → Add: Closing stock of finished goods |

|

36,000 |

|

|

1,48,000 |

Step 3 → Less: Opening stock of finished goods |

|

28,000 |

|

|

1,20,000 |

Step 4 → Add: Closing stock of work-in-progress |

|

24,000 |

|

|

1,44,000 |

Step 5 → Less: Opening stock of work-in-progress |

|

16,000 |

Step 6 → Cost of production |

|

1,28,000 |

|

Rs. |

|

Step 7 → Less: Direct labour |

32,000 |

|

Factory overhead: |

20,000 |

|

Administration overhead: |

5,200 |

|

Step 8 → |

|

57,200 |

*1 Cost of raw materials consumed = |

|

70,800 |

Now, statement of cost of goods manufactured and sold and profit earned for the month of January is prepared as follows:

*2 Purchases |

= |

Raw materials used + Opening stock − Closing stock |

|

= |

Rs. 70,800 − 16,000 + 17,200 |

|

= |

Rs. 72,000 |

| Particulars | Rs. | Rs. |

|---|---|---|

Step 1: Raw materials consumed: |

|

|

(i) Opening stock |

16,000 |

|

*2(ii) Purchases (Balancing figure) |

72,000 |

|

|

88,000 |

|

(iii) Less: Closing stock |

17,200 |

70,800 |

Step 2: Direct labour |

|

32,000 |

Step 3: Prime cost (Step 1 + Step 2) |

|

1,02,800 |

Step 4: Factory overheads |

|

20,000 |

Step 5: Gross works cost |

|

1,22,800 |

Step 6: Add: Opening work-in-progress |

|

16,000 |

|

|

1,38,000 |

Step 7: Less: Closing work-in-progress |

|

24,000 |

Step 8: Works cost |

|

1,14,800 |

Step 9: Add: General and administration expenses |

|

5,200 |

Step 10: Cost of production (of goods manufactured) |

|

1,20,000 |

Step 11: Add: Opening stock of finished goods |

|

28,000 |

|

|

1,48,000 |

Step 12: Less: Closing stock of finished goods |

|

36,000 |

Step 13: COST OF PRODUCTION OF GOODS SOLD |

|

1,12,000 |

Step 14: Add Selling Expenses |

|

6,800 |

Step 15: COST OF SALES (Total cost) |

|

1,18,800 |

Step 16: PROFIT (Step 17 − Step 15) |

|

31,200 |

Step 17: SALES |

|

1,50,000 |

1.11 INSTALLATION OF A COSTING SYSTEM

Any system should be devised to suit the needs of an organization. A cost accounting system may be said to be a system which (i) accumulates costs, (ii) assigns them to cost objectives and (iii) reports cost information. Further, it ascertains product profitability. Above all, the system helps the management in planning and controlling activities of the organization. Costing system may be employed in manufacturing industries (including mining, construction, etc.) or in service organizations.

The design and installation of a Costing system is a difficult task. The following are some of the factors that should be taken into consideration while designing a costing system:

Objectives of the system

Objectives of the management

Nature of business

Nature of product

Organizational structure of business

Business situation

Manufacturing process

Types of cost information desired and required by the management

Elasticity

Accuracy of data

Existing accounting policies and procedures

Key personnel and employees of the organization

Availability of qualified technical personnel

Materiality of cost items

Deployment of works to facilitate the implementation of costing system

Need to maintain uniformity

Impact of computerization

Choice of cost centre and degree of delegation of authority and fixing responsibility

Selection of a suitable unit of cost

Statutory and other legal provisions to be complied with

1.11.1 Practical Difficulties in Installing a Costing System

Lack of support from top management: The costing system is introduced either by the managing director or chairman of the organization without consulting the departmental heads in all the functional areas. They resist because they construe it as an interference to their duties. They do not want to have a check on their activities.

Inadequate trained personnel: Costing is a specialized branch of accounting. To carry out the work of cost analysis, cost control and cost reduction, there may not be adequate cost accountants. Such work cannot be taken by the existing personnel, who may perhaps be dealing with financial accounts only.

Heavy costs: The costing system involves high costs, as the existing units are not suitably designed to meet specific requirements.

Resistance from the staff: The existing financial accounting staff may resist the introduction of costing system for the reason that they may be declared redundant under the new system.

Non-co-operation at other levels of organization: The foreman, supervisor and other staff may also be averse to the system because it involves additional paper work. Basic data have to be provided to the cost accountants periodically. Above all, they do not want to interfere in their activities by such accounting professionals.

1.11.2 Measures to Overcome Difficulties

The following measures may be taken to overcome these difficulties in introducing the costing system:

The top management should be taken into confidence before the installation of a costing by appraising them of the salient features of the system and its imperative need in organizations.

The existing accounting staff should be impressed in such way that the new system is not competitive but complementary to the existing system.

The management should allay the fear of staff that they would not be replaced from the organization.

The existing staff in accounting department should be trained in cost accounting methods and techniques.

To avoid excess costs, a costing system should be installed and operated to meet the requirements of a specific case.

There should be proper supervision and review by the cost accountant to make the system successful.

1.12 ROLE OF A COST ACCOUNTANT IN AN ORGANIZATION

The cost accountant is an important person in an organization—especially manufacturing organization. The responsibility of discharging the cost accounting functions of the organization lies on the cost accountants’ shoulders. Their role has attained a significant position, now. They are a part of senior management team. The role of a cost accountant can be understood from the following important functions to be performed by them.

Maintenance of records: The basic function is to maintain cost accounting records as per section 209(1)(d) of the Companies Act 1956. In pursuance of this provision, the Government of India has notified Cost Accounting Record Rules for more than 40 industries. These rules prescribe the manner in which cost accounting records have to be maintained. They specify the particulars that should be entered in the books of accounts. Some of the records are to be maintained under the following heads: Stores and raw materials; salaries and wages; overheads; work-in-progress; production (finished goods) sales; depreciation. These records should be kept in such a way so as to reveal the business operations and valuation of stocks are determined accurately. Reconciliation of the results from these cost records should be made with those of financial accounts. In case, if the firms are not governed by the statutory provision, the cost accountant himself has to maintain records in such a way that they are useful to the management for taking decisions.

Financial planning: The cost accountant’s role in financial planning cannot be minimized. The cost accountant assists the line and staff managers in the preparation of budgets, making changes as and when necessary, ensuring consistency, and final compilation of the budget and master budget.

Product pricing: This is an important function to be performed by a cost accountant. The cost accountant assists the management in pricing a product by providing valid information after analysing and interpreting various cost data relating to fixing the price of a product.

Cost ascertainment: Ascertainment of the cost of a product or service is another important function of a cost accountant.

Cost control: Controlling the costs of business operations is the prime function of a cost accountant. Cost accountants have to exercise cost control by using a variety of techniques such as budgetary control, standard costing, quality control. They have to assist the management by submitting periodical reports to facilitate cost-control function. For example, statement of inventory valuation with relevant ratios will help the management to appraise the level of stock.

Cost reduction: This is another important area in which a cost accountant’s role has gained much importance. Manufacturing quality goods and rendering prompt services at the minimum cost is the goal of any organization. The cost accountant aims at achieving reduction on the unit cost of goods produced or services rendered and at the same time maintaining quality.

Evaluation of performance: The cost accountant compares the actual results with the budget, and variances are ascertained. Variances are analysed by causes and responsibility centres and communicated to appropriate level for corrective action. The performance of the responsibility centre is evaluated constantly which enhances the efficiency of an organization.

Management decision: One more important function of a cost accountant is to adopt as well as adapt cost accounting tools and techniques for management decision analysis such as make or buy, to continue or shut down operation, to accept an order, to quote a price, to choose alternative proposal etc. and various problem-solving situations.

Communication: The cost accountant discloses the needed financial information to all needed centres.

Coordinator: The cost accountants’ role of coordination with other departments cannot be underestimated. Their constant flow of cost information with production department, purchase department, personnel department, finance and accounts department, marketing department is essential for the successful functioning of an organization. They coordinate the activities of all the departments by way of exercising cost control and cost reduction.

Reliable tax basis: As costs are ascertained precisely and profits shown in cost records are reliable and accurate, it facilitates the tax-levying authorities to assess the tax without great difficulty. So, the role of the cost accountant gains greater responsibility.

Customer relationship management: CRM initiatives use technology to coordinate all customer-facing activities (such as marketing, sales calls, distribution and post-sales support) and the design and production activities necessary to get products to customers.

*1 “Cost Accountants track the costs incurred in each value-chain category (research and development, design of products, services or processes, production, marketing distribution and customer service). Their goal is to reduce costs in each category and to improve efficiency.”

Cost Accounting: A Managerial Emphasis. Charles T. Horn green, Srikant M. Dattar and George Foster, Pearson Education; 2008.

Wilmot has summarized the role of a cost accountant as that of “a historian, a news agent and prophet. As a historian he must be meticulously accurate and sedulously impartial. As a news agent he must be up-to-date, selective and pithy. As a prophet he must combine knowledge and experience with foresight and courage.”*2

*2 “The Cost Accountant’s Place in Management,” Wilmot; The Cost Accountant; October 1936.

Key Terms

Cost Accounting: A system that measures and reports financial as well as non-financial information about the cost of products of services being produced or sold.

Cost Object: It represents anything in respect of which a separate measurement of cost is desirable

Cost Centre: A location, function, items of equipment in respect of which costs may be ascertained and related to cost units for control purposes.

Cost Unit: A quantitative unit of product or service in relation to which costs are ascertained.

Cost Sheet: A document that depicts the components of cost in detail—an analysis of total cost of production and cost of sales.

Cost Driver: A variable (level of activity, volume etc) that casually affects over a given time span)

Direct Material: Directly identifiable with the product and forms part of the product.

Direct Labour: Employees employed directly in making the product.

Prime Cost: Aggregate of direct material cost, direct wages and direct expenses.

Fixed Cost: A cost which remains unaffected in a given period of time, by fluctuations in the level of activity.

Variable Cost: A cost which tends to follow (in the short-term) the level of activity.

Semi-variable Cost: A cost containing both fixed and variable elements which would be partly affected by fluctuations in the levels of activity.

Profit Centre: A responsibility centre in which performance is measured in terms of both the revenue it earns and the cost it incurs.

QUESTION BANK