4

Overheads Classification, Distribution and Control

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Understand the term “overheads”.

Classify the overheads into different categories.

Understand the constituents of factory overeads, office overheads, and selling and distribution overheads.

Segregate costs into fixed and variable kinds.

Ascertain semi-variable overheads by various methods.

Understand the term “allocation” and “apportionment” of overheads and the basis of apportionment of overheads.

Understand “inter-service distribution” and different methods of apportionment of overheads.

Appraise the various methods involved in absorption of factory overheads.

Distinguish between the actual overhead rate and pre-determined overhead rate.

Apply different methods for dealing with under- and over-absorption overheads.

Explain the meaning of certain important terms.

There are certain costs which belong to more than one cost unit. It is not easy to identify then to a specific cost unit. Nowadays, overheads constitute a major portion of the total cost in any organization, particularly industrial organizations. The terminology and the use of overheads vary widely. In this chapter, the meaning of overheads, its classification, method of apportioning them, the accounting treatment of the different items of overheads in cost accounts and how can it be controlled are all explained in detail.

4.1 MEANING AND DEFINITION OF OVERHEADS

The terminology of CIMA defines overheads as “the total cost of indirect materials, indirect labour and indirect expenses”.

Some costs in an organization are indirect in nature. They cannot be allocated easily to the product, job or process. Besides this, some expenses that are incurred on material labour cannot be economically identified with specific saleable units. Such costs are referred to as “overhead costs”. These overhead costs are also known as “convenience costs”.

Overheads include the following:

- indirect materials.

- indirect labour.

- all indirect expenses that cannot be charged to a product or job or process. For example, expenses incurred for maintenance, supervision, rent, rates and taxes, lubricants and cleaning materials, personnel department and sales department which cannot be easily identified with the cost units produced.

4.2 CLASSIFICATION OF OVERHEADS

Classification is the process of grouping costs depending upon their common characteristics. Overheads have to be classified in order to ascertain cost, product pricing, planning and control.

Classification may be defined as, “the arrangement of items in logical groups having regard to their nature (subjective classification) or the purpose to be fulfilled (objective classification)”.

Overhead costs may be classified as follows:

- Functional classification.

- Element-wise classification.

- Behaviour-wise classification.

4.2.1 Functional Classification

Under this method, the classification of overheads is based according to the functions of an organization. Some important functional classifications of overheads of an organization are as follows:

- Production overhead:

- It is also known as factory overhead, manufacturing overhead, or works overhead.

- It is the aggregate of indirect material cost, indirect wages, and indirect expenses incurred with respect to the manufacturing activity.

- The manufacturing activity begins with the supply of materials and ends with the primary packing of products.

Production overhead includes carriage inwards, consumable stores, rent, rates and taxes of a factory: Wages, salaries and other expenses incurred in a factory for stores personnel; design-and-drawing office staff; quality-control personnel; staff-maintenance records; insurance premium for the factory buildings, plant, machinery and equipments, and furniture and fixtures; depreciation for factory buildings, furniture and fixtures, and plant machinery and equipments; and idle-time wages, welfare-expenses stationery and communication expenses incurred in a factory.

- Administration overhead: It is the aggregate of indirect material, indirect wages and indirect expenses incurred with respect to administration of an organization.

Examples: Salary of administrative-office personnel, rent, taxes of general office, remuneration and sitting fees of directors, lighting, heating and other expenses of general office; all stationery and communication of expenses of office, audit fees, legal fees, insurance premium of office buildings, furnitures and fixtures and their respective depreciation and bank charges.

- Research and development overhead: This is the aggregate of indirect material, indirect wages and indirect expenses incurred on the research and development (R&D) activities of an organization.

Examples: Salaries of R&D personnel, patent changes, cost of maintenance of R&D office, insurance premium, depreciation and repair and maintenance expenses with respect to R&D office buildings, equipments, lab, furniture and fixtures, materials used in research, contributions made to research institutions, periodicals and books relating to R&D.

- Selling overhead: This is the aggregate of indirect materials, indirect wages and all indirect expenses which are incurred for creating and stimulating demand for a firm’s products.

Examples: Salary and all incentives offered for sales personnel, travelling expenses of sales personnel, rebates and discounts in the cost of price list, brochures, samples, collection costs for debts, repair and maintenance, insurance premium paid and depreciation with respect to sales office building, sales office equipments, furnitures and fixtures.

- Distribution overhead: This is the aggregate of indirect materials, indirect wages and indirect expenses incurred for making a firm’s products available to customers.

Examples: Carriage outwards, expenses on the delivery vehicles, delivery and packing expenses, salary and wages of godown keeper, drivers, packers, delivery personnel, rent, rates, taxes on the finished goods, repairs and maintenance costs, insurance premium, depreciation with respect to godown and distribution outlets.

4.2.2 Element-Wise Classification

Under this classification, the overhead is split into the following elements:

- Indirect materials.

- Indirect expenses.

- Indirect labour.

- Indirect materials: Indirect materials are those which cannot be identified with specific products. They cannot be measured in any standardized physical units. But they are essential for the smooth running of the manufacturing process.

Examples: Cotton waste used for cleaning plant and machinery consumable stores, industrial lubricants, coolants, printing and stationery and so on.

- Indirect labour: Costs that cannot be conveniently identified with a product are known as “indirect labour costs”. Indirect labour in no way alters the construction or composition of a product.

Examples: Wages and salaries relating to supervisors, management personnel, stores personnel, production personnel, security personnel, administrative personnel, secretarial and accounts personnel and so on.

- Indirect expenses: Indirect expenses are those which cannot be easily identifiable with a product or a job or a process. These cannot be directly allocated to cost units. These expenses are common to all the products, processes or jobs and are incurred for carrying out all business activities in toto.

Examples: Rent, rates, taxes, postage, telegram, fax, e-mail expenses, insurance premium, lighting and heating.

4.2.3 Behaviour-Wise Classification

Overheads exhibit different characteristics (in the short term) with respect to the volume of production and sales. This is known as the “behaviour of overheads”. The behaviour-wise classification clarifies overheads in accordance with their behaviour. They are:

- Variable overhead: Variable-overhead costs change in the same ratio in which the output changes (volume of output). But it remains constant per unit.

Examples: Power consumption, selling commission, consumption of stores and consumables and so on.

- Fixed overheads: The fixed costs remain unaffected by the change in the volume of output. Costs are fixed for a given period over a relevant range of output.

Examples: Insurance premium and depreciation with respect to fixed assets, rent, rates and taxes. Fixed cost is also known as “period cost”.

- Semi-variable overhead: This is also called “semi-fixed overhead”. These costs are partly fixed and partly variable. Some overheads possess characteristics of both fixed and variable costs. These costs do not change in the same ratio in which the output changes.

Examples: Maintenance expenses, telephone expenses and stationery expenses.

Importance and the need of classifying overheads into fixed and variable kinds are as follows:

- Flexible budgeting: The gap between the expected results and the achieved ones will vary. To make meaningful comparisons between the budgeted and the actual performance, it is necessary to prepare budgets for different volumes of output. This is known as “flexible budget”. Unless and until the total costs are divided into variable and fixed, it will not be easy to prepare such flexible budgets.

- Decision-making: The classification of costs into fixed and variable elements facilitates the management to comprehend how costs change with changes in the volume of activity. This helps the management in assessing the accurate projections of the expected changes in the total costs with the changes in the volume. It helps the management to a great extent in the decision-making process.

- Cost control: Effective cost control can be achieved only if which costs are to be controlled and who is responsible to control those costs are planned in advance. The segregation of costs into fixed and variable kinds will serve the purpose. Variable costs can be controlled by the persons who are at the lower level of management. Fixed costs can be controlled by the top-level management.

- Cost–volume–profit analysis and Marginal-costing techniques: The management relies to a greater extent on the techniques of cost–volume–profit analysis and marginal costing for the purpose of decision-making. These techniques are based on the principle of segregation of costs into fixed and variable elements.

4.3 METHODS OF SEGREGATING SEMI-VARIABLE COSTS INTO FIXED AND VARIABLE COSTS

The identification of costs into variable and fixed categories can be made easy for any item of cost. But the real problem arises when semi-variable costs are identified. In order to separate the semi-variable overheads into fixed and variable, the techniques are most-widely applied as discussed in the following:

4.3.1 Method 1: (Technique 1) Levels of Output Compared with the Levels of Expenses Method

Under this method, as the very name implies, the output at two different levels is compared with the corresponding levels of expenses. As the fixed expenses remain constant, the variable overheads are ascertained by the ratio of change in expenses to the change in output.

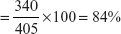

Illustration 4.1

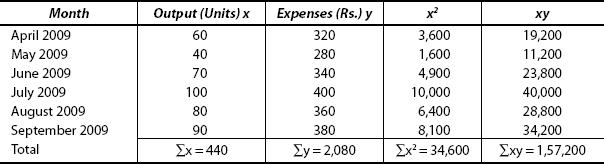

From the following data, you are required to compute the amount of fixed, variable and total semi-variable expenses for the month of October 2009, where the production is 50 units.

| Month | Production (Units) | Semi-Variable Expenses (Rs.) |

|---|---|---|

April 2009 |

60 |

320 |

May 2009 |

40 |

280 |

June 2009 |

70 |

340 |

July 2009 |

100 |

400 |

August 2009 |

80 |

360 |

September 2009 |

90 |

380 |

Solution

Step 1: Take the figures for any two months:

For instance, take April and August.

Month |

Production (Units) |

Semi-Variable Expenses (Rs.) |

April 2009 |

60 |

320 |

August 2009 |

80 |

360 |

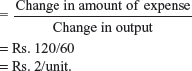

Step 2: Compare the difference between these two levels: 20 40

Step 3: Variable part

Step 4: Now calculate the variable overhead for April:

Step 5: Therefore, fixed costs for April = Rs. 320 – Rs. 120 = Rs. 200.

Step 6: Similarly, for August = 80 × Rs. 2 = Rs. 160.

Therefore, Fixed costs = (Rs. 360 – Rs. 160) = Rs. 200.

Step 7: Variable costs for October 2009:

(i) |

Variable costs = No. of units × Rs. 2 = 50 × Rs. 2 |

= Rs. 100. |

(ii) |

Fixed overheads (Ref Step 4 & 6) (It remains constant) |

= Rs. 200. |

(iii) |

∴ Total semi-variable overheads (Add i + ii) |

|

4.3.2 Method 2: High- and Low-Point Method: (or) Range Method

Although this method is similar to the previous method it differs by taking into account only the highest and lowest volumes of production and cost. The procedure is the same as follows: The difference between the outputs and costs (highest and lowest levels of output) are determined. The incremental cost is divided by the incremental output to ascertain the variable cost per unit. Then multiply this variable cost per unit with either the highest or level output to find out the total variable cost. To ascertain the fixed cost, the total variable cost is deducted from the total cost (at the same level of output). This is explained in the following illustration.

Illustration 4.2

Ref: Illustration 4.1.

Solution

Step 1: The highest production is in the month of July, which is 100 units. The lowest production is in the month of May where the corresponding semi-variable expenses are taken and the differences are computed.

Step 2:

| Month | Units | Semi-Variable Expenses (Rs.) |

|---|---|---|

May |

40 |

280 |

July |

100 |

400 |

Differences |

60 |

120 |

Step 3: Variable cost per unit

Step 4: |

Variable overheads for May: 40 × Rs. 2 |

= Rs. 80. |

Step 5: |

Therefore, fixed overheads for May = Rs. 280 – 80 |

= Rs. 200. |

Step 6: |

Similarly, variable overheads for July = 100 × Rs. 2 |

= Rs. 200. |

Step 7: |

Therefore, fixed overhead for July: Rs. 400 – Rs. 200 |

= Rs. 200. |

Step 8: |

October 2009: |

(i) |

Variable costs = No. of units × Rs. 2 = 50 × 2 |

= Rs. 100. |

(ii) |

Fixed overheads (Ref Step 6 & 7) |

= Rs. 200. |

(iii) |

Total semi-variable overheads |

= Rs. 300. |

4.3.3 Method 3: Degree of Variability Method

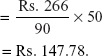

Under this method, the degree of variability has to be assigned for each item of semi-variable expenses. Variability percentage ranges normally from 30% to 70% depending on the nature of items. In this method, the determination of the degree of variability is arbitrary and no accuracy can be possible.

Illustration 4.3

Same illustration no. 4.1.

Solution

Step 1: |

→ |

Assume that the degree of variability is 70% of the total semi-variable expenses. Take the month of September. |

Step 2: |

→ |

Variable element = 70% of Rs. 380 = 266.00. |

Step 3: |

→ |

Fixed element: Rs. 380–Rs. 266 = Rs. 114. |

Step 4: |

→ |

For the month of October: |

- For 90 units, variable expenses = Rs. 266.

(Ref: Step 2)

- ∴ for 50 units, variable expenses

- Total variable expenses for October 2009 = Rs. 266 + Rs. 147.78

= Rs. 413.78

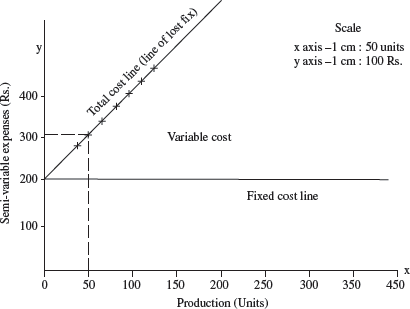

4.3.4 Method 4: Scattergraph Method

Under this method, the given data are plotted on a graph paper and the line of best fit (total cost line) and the variable cost at any level may be determined by the quantum of difference between the fixed cost line and the total cost line. This method is explained by way of an illustration as follows:

Illustration 4.4

Take the same figures as given in illustration no. 4.1.

Solution

Step 1: Take a graph paper.

Step 2: On the horizontal axis (x axis), volume of production or sales (output, here) is plotted on a predetermined suitable scale, say 1 cm = 50 units.

Step 3: On the vertical axis (y axis), the costs corresponding to volume are plotted on a predetermined suitable scale, say 1cm = 100 Rs.

Step 4: A straight line is drawn connecting the points plotted on the graph. This line is known as the line of best fit or total cost line.

Step 5: The point, where this total cost line cuts the y axis represents the fixed (costs) element.

Step 6: A line is drawn parallel to the x axis, from the point where the total cost line (line of best fit) intersects the y axis. This is the fixed cost line.

Step 7: The variable element at any level may be determined by the difference between the fixed cost and the total cost lines.

Production (units)

Graph shows fixed expenses are Rs. 200.

For the months of October 2009:

For 50 units, the total semi-variable costs are Rs. 300 (shown in …lines).

Therefore, variable expenses = Rs. 300 – Rs. 200 = Rs. 100.

Like this, for any level of output, the results can be read from the graph at a glance.

4.3.5 Method 5: Method of Least Squares

This method segregates the cost into variable and fixed elements and determines their relationship to the changes in volume. In this method, we select one variable as a dependant variable and another as an independent variable to study the relationship between the cause and effect. Regression is the measure of the average relationship between two or more variables in terms of the original units of data. This method is also known as “simple linear regression analysis method”. The regression line can be used to determine the values of the dependent variable where two variables possess a linear relationship. The linear equation may be assumed as:

|

y |

= |

a + bx; |

where |

y |

= |

total cost, |

|

a |

= |

fi xed proportion of total cost, |

|

b |

= |

variable component and |

|

x |

= |

number of units. |

Illustration 4.5

Ref: Illustration 4.1.

Solution

Based on the figures in illustration 4.1, a linear equation is obtained from the following values shown in the tabular column:

Take two sub-equations.

|

Σy = Σa + bΣx2 |

(1) |

|

Σxy = aΣx + bΣx2 |

(2) |

Substituting the values in the equations, we get:

|

2,080 = 6 × a + 440 b |

(3) |

|

1,57,200 = 440 a + 34,600 b |

(4) |

Multiplying (2) by 440 and (3) by 6, we get

2,080 × 440 |

= |

(6a + 440b) × 440 |

(5) |

1,57,200 × 6 |

= |

(440a × 34,600b) × 6 |

(6) |

9,15,200 |

= |

2640a + 440 × 440b (1,93600 b) |

(7) |

9,43,200 |

= |

2640a + 6 × 34600b (2,07,600b) |

(8) |

|

28,000 |

= |

0 + 14,000b |

|

14,000 b |

= |

28,000 |

|

b |

= |

28,000/14,000 = 2. |

Substituting the value of b in equation (3), we get

|

2,080 |

= |

6 × a + 440 × 2 |

|

2,080 |

= |

6a + 880 |

|

2,080–880 |

= |

6a |

|

1200 |

= |

6a. |

|

a |

= |

1200/6 = 200 |

|

a |

= |

fixed cost = Rs. 200 |

|

b |

= |

variable cost = Rs. 2. |

For the month of October 2009, we get:

Total semi-variable overhead for 50 units:

Variable cost@ Rs. 2/unit (a) |

= Rs. 100 |

Fixed cost (b) |

= Rs. 200 |

∴ Total semi-variable overheads: |

|

4.4 CODIFICATION OF OVERHEADS

Costs have to be collected on a systematic basis under properly defined accounting headings. The account heads have to be defined well. Adequate number of account heads has to be selected to avoid confusion. The terminology of CIMA defines coding as “a system of symbols designed to be applied to a classified set of items, to give a brief accurate reference facilitating entry, collection and analysis”. It involves a system of allotment of code numbers to individual head, sub-head and group of expense.

A code number is allotted to each account code and individual cost centres. Code numbers allotted to factory expenses and code numbers that are allotted to administration, selling and distribution expenses are known by different names.

“Standard order numbers” is the name christened to codes allotted to factory expenses. “Cost-account numbers” is the name given to administration, selling and distribution expenses.

The methods used to allot symbols or code numbers are as follows:

4.4.1 Numeric or Numerical or Straight-Number Coding

In this method, each type of expenditure is allotted a fixed number.

For instance,

S. No. |

28 |

Indirect material |

S. No. |

108 |

Indirect labour |

Numbers are allotted an each heading and sub-heading of an expense like:

Item |

Depreciation -1 |

Code No. |

|

Plant |

11 |

|

Land and Building |

12 |

|

Furniture and Fixtures |

13 |

Repairs 2 - |

|

|

|

Plant |

21 |

|

Land and Building |

22 |

|

Furniture and Fixtures |

23 |

4.4.2 Alphabetical or Mnemonic Method

In this method, alphabets are used for identifying the expenses of cost centres:

Example:

|

AC |

Assembly cost |

|

MC |

Maintenance cost |

|

AD |

Administration |

4.4.3 Alphabetical Cum Numerical Method

Under this method, both alphabetical as well as numerical numbers are used. Alphabet to denote the main expenditure and the numerals to represent its subdivision.

Example:

M1, M2, M3…

Where M denotes maintenance, M1 denotes maintenance of plant, M2 maintenance of building and M3 maintenance of machinery and so on.

4.4.4 Decimal Method

In this method, the whole number is allotted for the head of the expenditure on master group whereas decimals are allotted to primary or secondary items.

Example:

1. |

Factory overheads: |

1.1. |

Indirect materials |

1.1.1 |

Cotton waste |

1.1.2. |

Spare parts |

1.2. |

Indirect labour |

1.2.1. |

Stores |

1.2.2. |

Inspection and so on. |

4.4.5 Field Method

In this method, the codes used are numeric. Each code number consists of 9 digits. For example:

Code 20 120 01 05

- First 2 digits denote – variable cost – 20.

- The next 3 digits denote – idle time – 120.

- The next 2 digits denote – power failure – 01.

- The last 2 digits denote – the particular machinery – 05.

In order to facilitate the collection of overhead, it should be ensured that all source documents must have the correct cost-centre number and the correct standing-order number or cost-account number. If the account headings are properly defined, it is easy to estimate the overheads properly. These figures are the base for determining the predetermined overhead rates.

4.4.6 Advantages of Codification of Accounts

- As homogeneous items are grouped, they serve as a proper basis for apportionment of expenses.

- It saves much time as account headings need not be written on all documents.

- Codification is essential for computerization.

4.5 DISTRIBUTION OF OVERHEADS

Distribution of overheads is the division of total overheads in an equitable manner to each unit of the cost object. The cost object may be a process, a unit of production, a production order and so on. The distribution of overheads is a three-stage process, as explained in the following:

4.5.1 Stage I: Allocation of Overheads

- Allocation involves the identification of overheads with a given cost centre.

- Cost allocation may be defined as “the charging of discrete, identifiable items of costs to cost centres or cost units. Where a cost can be clearly identified with a cost centre or cost unit, then it can be allocated to that particular cost centre or cost unit”.

- An organization must try to allocate as many items as possible.

- Estimation of the benefits received by each cost centre is essential for the apportionment of overheads.

- The cost centres should be mentioned on the documents that are used to collect overheads, which is essential for correct allocation of factory overheads.

4.5.2 Stage II: Apportionment of Overheads

- The terminology of CIMA defines apportionment as, “the allotment of two or more cost centres of proportions of the common items of cost and the estimated basis of benefits received”.

- Some overheads are common to more than one cost centre or department. Such overheads are to be apportioned to various cost centres or departments.

- A proper assessment of the benefits which different cost centres or departments have received from each head of expense is the proper basis for the apportionment of the common overheads.

- The measurement of benefits must be assessed properly for each expense head.

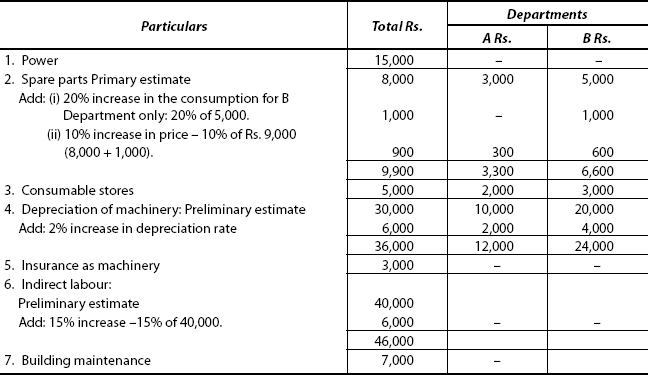

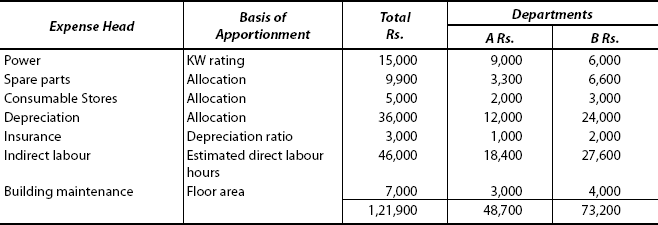

Some common overheads and their basis of apportionment are as follows:

| Overhead | Basis of Apportionment |

|---|---|

1. Depreciation, repairs and maintenance of of plant machinery and other production Activities like insurance premium on assets |

Capital values (original cost or book value of assets) |

2. Depreciation, rent, heating, lighting rates and taxes, maintenance of building and other expenses with respect to the premises and fire-protection services. |

Floor area |

3. Electric power |

Machine horse power + Operating time |

4. Water, steam |

Technical estimates |

5. Store expenses |

Value of materials issued |

6. Any expense related to workers such as supervision, canteen expenses, dispensary expenses and recreational expenses |

Number of workers |

7. Other general overhead expenses |

Machine hours or labour hours |

8. Delivery expenses |

Weight, volume etc |

9. Audit fees |

Sales or total cost |

At times, other than proportionate benefit, secondary criteria are used for apportionment of overheads which are:

- incentives or efficiency: a pre-determined activity level is used for apportionment of overhead and

- ability to pay: apportionment of costs is based on their ability to bear the costs.

Distribution of overhead consists of allocation and apportionment of overhead costs to the different departments or cost centres on a suitable basis. The distribution is to be followed by redistribution of the costs assigned to certain departments. The distribution may be classified into two types: primary distribution and secondary distribution.

4.5.2.1 (Stage I) Primary Distribution of Overheads

Primary distribution of overheads is the process of allocating and apportioning the overhead costs to all the departments or cost centres. This is done on a suitable and equitable basis. While primary distribution is done, no distinction is made whether it is production department or service department. This is done to all the departments.

Bases of apportionment: To ascertain the correct cost of cost centres and cost units, suitable bases have to be adopted for allocation and apportionment of overhead expenses.

Following are the some of the bases used for apportionment of manufacturing overheads:

- Direct allocation: If overheads are traceable, they may be directly allocated to a particular job or department. E.g., power.

- Labour hours: Wherever direct labour hours are shown distinctly, overheads should be apportioned on the basis of direct labour hours for different departments.

- Machine hours: Where activities are entirely dependent on machineries, overheads are distributed on the basis of machine hours.

- Direct Materials: Indirect materials, material-handling charges and the like are apportioned on the basis of the value of direct materials consumed.

- Direct wages: Indirect wages and general overheads are apportioned on the basis of direct wages.

- Number of staff: Number of employees in each department is used as a basis for apportioning overhead costs that are incurred for the welfare of workers.

- Floor area: The area occupied by different departments is taken as the basis for apportioning expenses such as rent, tax, lighting and building-maintenance expenses.

- Capital value: Depreciation, insurance premium, repairs and maintenance, etc., would be apportioned on the basis of the capital value of assets.

- Light points: The light points in various departments serve as the basis for apportioning lighting expenses.

- Kilowatt hours: Power expenses are to be apportioned on the basis of kilowatt hour (KWH).

Primary distribution (apportionment) of overhead expenses can be best understood from the following illustration:

Illustration 4.6

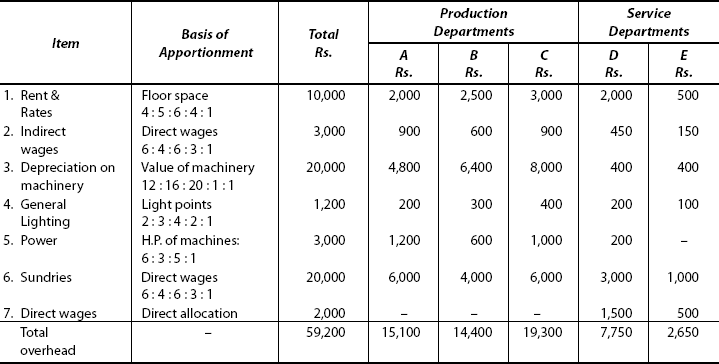

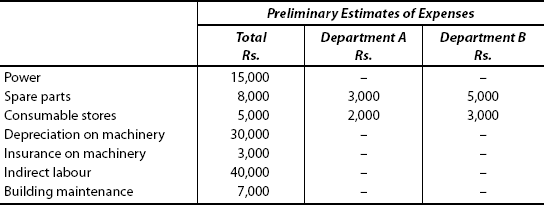

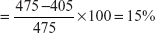

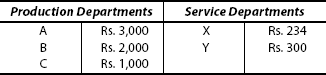

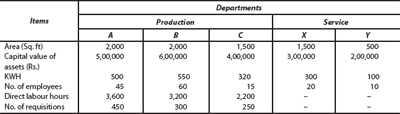

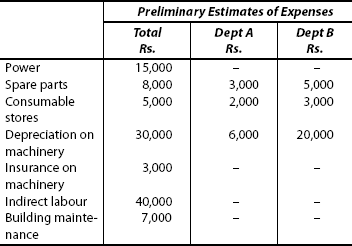

X Ltd has three production departments A, B and C and two service departments D and E. The following figures are extracted from the records of the company:

| Rs. | |

|---|---|

Rent and rates |

10,000 |

Indirect wages |

3,000 |

Depreciation of machinery |

20,000 |

General lighting |

1,200 |

Power |

3,000 |

Sundries |

20,000 |

The following further details are available:

You are required to apportion the costs to various departments on the most equitable basis by preparing a primary distribution summary.

[Delhi – B.Com – Modified]

Solution

NOTE: |

Apportionment means nothing but distribution. Distribution of costs has to be made on a basis. Every expense is to be distributed properly which is explained in the following steps: |

Step 1: Expense given: Rent and Rates: Rs. 10,000.

- Now, refer to further details in the table.

- From among the items, choose the appropriate basis for distributing this expense.

- Floor space is the suitable basis for apportionment of this type of expense.

- Floor space is given as 10,000 sq ft. (in Total column)

- It is shown in different values for different departments.

- Based on these figures, a ratio is determined, i.e., 2,000 for A, 2,500 for B, 3,000 for C, 2,000 for D and 500 sq. ft. for E.

Based on their ratio, Rent & Rates Rs. 10,000 will be found out as:

For Department A: Ratio × Total rent and rates: 4/20 × 10,000 = Rs. 2,000.

For Department B: 5/20 × 10,000 = Rs. 2,500.

For Department C: 6/20 × 10,000 = Rs. 3,000.

For Department D: 4/20 × 10,000 = Rs. 2,000.

For Department E: 1/20 × 10,000 = Rs. 500.

Step 2:

- Indirect wages: Rs. 3,000.

- Suitable basis: Direct wages (Ref: Table).

- Ratio determination:

- Apportionment:

For Department A:

For Department B:

For Department C:

For Department D:

For Department E:

Step 3:

- Item of expense: Depreciation: Rs. 20,000.

- Suitable basis: Value of machinery (Ref. Table).

- Ratio determination:

- Apportionment:

For Department A =

For Department B =

For Department C =

For Department D =

For Department E =

Step 4:

- Item of expense: General lighting: Rs. 1,200.

- Suitable basis: Light points (Ref: Table)

- Ratio determination:

- Apportionment:

For Department A =

For Department B =

For Department C =

For Department D =

For Department E =

Step 5:

- Item of expense: Power (Rs. 3,000).

- Suitable basis: H.P. of machines (Ref. Table)

- Ratio determination:

- Apportionment:

For Department A =

For Department B =

For Department C =

For Department D =

For Department E = — = Nil.

Step 6:

- Item of expense: Sundry expenses (Rs. 20,000).

- Suitable basis: Direct wages (Same as in Step 2).

- Ratio : 6 : 4 : 6 : 3 : 1

- Apportionment:

For Department A =

For Department B =

For Department C =

For Department D =

For Department E =

Step 7:

- Item of expense: Direct wages (Ref: Table).

- Basis: Direct allocation – It means expenses are allocated directly.

- Ratio: The same amount shown in the table to be taken into account.

- Apportionment: Only for service departments:

Important Note

Direct wages of service departments are to be included.

Step 8: These figures are transfered to the table as follows:

Secondary distribution of overheads is explained in Stage III as follows:

(Stage III) Re-apportionment of service-cost-centre overheads or Secondary distribution of overheads

- The overheads of service-cost centres are reapportioned to the production departments only. The reason is that the service-cost centres provide services to the production department. The process of redistribution of service-cost-centre costs to production department is called “reapportionment”. This is also known as “secondary distribution of overheads”.

- The proportionate benefit received by the other cost centres forms the basic criterion for reapportioning the overheads relating to the service-cost centres.

- The methods that are used for the reapportionment of service-cost centre overheads are:

- Direct redistribution method.

- Step distribution method.

-

- Reciprocal method – Simultaneous equation method.

- Reciprocal method – Repeated distribution method.

- Trial-and-Error method

4.5.2.2 Direct Redistribution Method

This method is based on the assumption that service-cost centres provide services to production departments only. The overheads of service cost centres are reapportioned to the production-cost centres. This is done on the basis of the proportion of benefits received by the production departments.

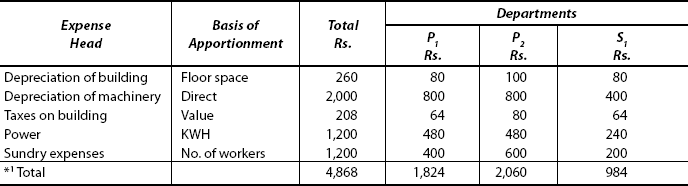

Illustration 4.7

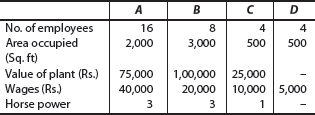

You are required to apportion and reapportion the service department costs to production departments using direct distribution method.

The expenses of the service department are shared between P1 and P2 in the ratio of 1:2. The total direct labour hours per month are estimated to be 4,304 and 6,790 for P1 and P2, respectively.

Solution

Basic calculations needed for each item of expense are determined as follows:

- Depreciation of building:

- Taxes on building:

- Formula:

- Substituting the figures, we get

- Formula:

- Power:

- Formula:

-

- Formula:

- Sundry expenses:

- Formula

-

- Formula

Now Departmental Distribution Summary (Primary Distribution) is to be prepared as follows:

Secondary Distribution

*2S1 – 984 in the ratio of 1:2.

P1 = 984 × ![]() = Rs. 328

= Rs. 328

P2 = 984 × ![]() = Rs. 656

= Rs. 656

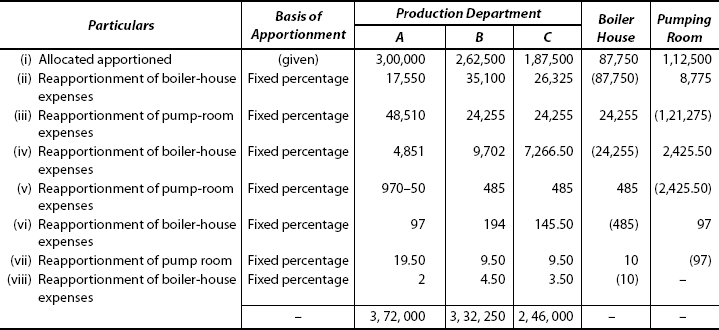

4.5.2.3 Step-distribution Method

- Under this method, limited consideration is made of the services provided by the service departments to other service departments. Hence, a series (sequence) of reapportionments are made.

- The sequence begins with the department that has the largest amount of overhead or provides the highest percentage of its total services to other service departments.

- The sequence continues in step-by-step manner and ends with the reapportionment of the costs of the service department that has the lowest amount of overhead or the lowest percentage of its total services to other service departments.

- It is important to note that once a service department’s costs are reapportioned, no further reapportionment of costs is made to it.

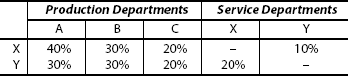

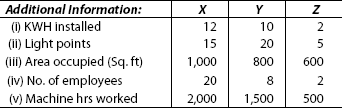

Illustration 4.8

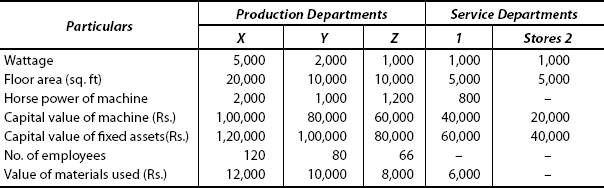

XYZ Ltd. has three production departments and two service departments. The estimated figures for a certain period are as follows:

| Rs. | |

|---|---|

Lighting & Electricity |

20,000 |

Rent, rates and taxes |

1, 00,000 |

Power |

10,000 |

Wages of store staff |

20,000 |

Depreciation of machinery |

30,000 |

Insurance premium |

20,000 |

|

2, 00,000 |

Further details:

You are required to apportion the cost to production-cost centres using the step method.

Solution

For each item, expenses have to be apportioned as follows:

- Item of expense: Lighting and Electricity.

- Basis for apportionment, i.e., Formula

-

- X =

× Rs. 20,000 = Rs. 10,000

× Rs. 20,000 = Rs. 10,000 - Y =

× Rs. 20,000 = Rs. 4,000

× Rs. 20,000 = Rs. 4,000 - Z =

× Rs. 20,000 = Rs. 2,000

× Rs. 20,000 = Rs. 2,000 - S1 =

× Rs. 20,000 = Rs. 2,000

× Rs. 20,000 = Rs. 2,000 - S2 =

× Rs. 20,000 = Rs. 2,000

× Rs. 20,000 = Rs. 2,000

- X =

- Basis for apportionment, i.e., Formula

- Item of expense: Rent, Rates and Taxes.

- Formula

-

- X =

× Rs. 1,00,000 = Rs. 40,000

× Rs. 1,00,000 = Rs. 40,000 - Y =

× Rs. 1,00,000 = Rs. 20,000

× Rs. 1,00,000 = Rs. 20,000 - Z =

× Rs. 1,00,000 = Rs. 20,000

× Rs. 1,00,000 = Rs. 20,000 - S1 =

× Rs. 1,00,000 = Rs. 10,000

× Rs. 1,00,000 = Rs. 10,000 - S2 =

× Rs. 1,00,000 = Rs. 10,000

× Rs. 1,00,000 = Rs. 10,000

- X =

- Formula

- Item of expense: Power

- Formula

-

- X =

× Rs. 10,000 = Rs. 4,000

× Rs. 10,000 = Rs. 4,000 - Y =

× Rs. 10,000 = Rs. 2,000

× Rs. 10,000 = Rs. 2,000 - Z =

× Rs. 10,000 = Rs. 2,000

× Rs. 10,000 = Rs. 2,000 - S1 =

× Rs. 10,000 = Rs. 1,000

× Rs. 10,000 = Rs. 1,000

- X =

- Formula

- Item of expense: Depreciation of Machinery

- Formula

-

- X =

× Rs. 30,000 = Rs. 10,000

× Rs. 30,000 = Rs. 10,000 - Y =

× Rs. 30,000 = Rs. 8,000

× Rs. 30,000 = Rs. 8,000 - Z =

× Rs. 30,000 = Rs. 6,000

× Rs. 30,000 = Rs. 6,000 - S1 =

× Rs. 30,000 = Rs. 4,000

× Rs. 30,000 = Rs. 4,000 - S2 =

× Rs. 30,000 = Rs. 2,000

× Rs. 30,000 = Rs. 2,000

- X =

- Formula

- Item of expense: Insurance Premium

- Formula

-

- X:

× Rs. 20,000 = Rs. 6,000

× Rs. 20,000 = Rs. 6,000 - Y:

× Rs. 20,000 = Rs. 5,000

× Rs. 20,000 = Rs. 5,000 - Z:

× Rs. 20,000 = Rs. 4,000

× Rs. 20,000 = Rs. 4,000 - S1:

× Rs. 20,000 = Rs. 3,000

× Rs. 20,000 = Rs. 3,000 - S2:

× Rs. 20,000 = Rs. 2,000

× Rs. 20,000 = Rs. 2,000

- X:

- Formula

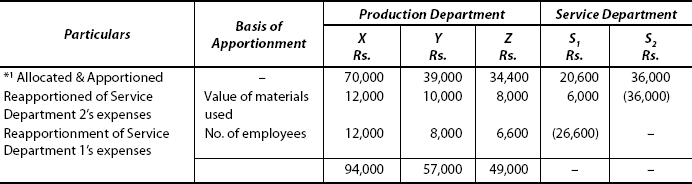

- For secondary distribution of overheads, reapportionment of service departments 2 and 1’s items of expenses are to be calculated in a similar way.

- Wages of store staff—as it is identified with stores department, they are allocated to that department only directly.

NOTE:

- S-2 has the highest amount of overhead. So, it is to be reapportioned first in the ratio of materials used as follows:

- Then, S1—the total amount of overhead is Rs. 26,600. This amount has to be reapportioned on the basis of the number of workers.

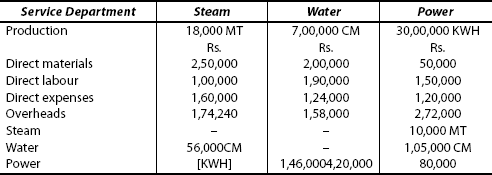

4.5.2.4 Reciprocal Method

This method reapportions the costs by explicitly including the mutual services provided among departments. This method is used when the service department provides services to another reciprocally. For instance, the stores department provides service to the repairs and maintenance department while the stores department receives some services from the repairs and maintenance department. That is why it is termed as “reciprocal”.

*There are two approaches under this method:

- Simultaneous equation method.

- Repeated distribution method.

4.5.2.5 Simultaneous Equation Method

In this approach, the overheads of service-cost centres are first determined using simultaneous equations. Then, based on the given predetermined percentages, they are to be reapportioned to production-cost centres.

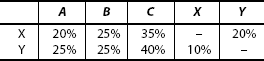

Illustration 4.9

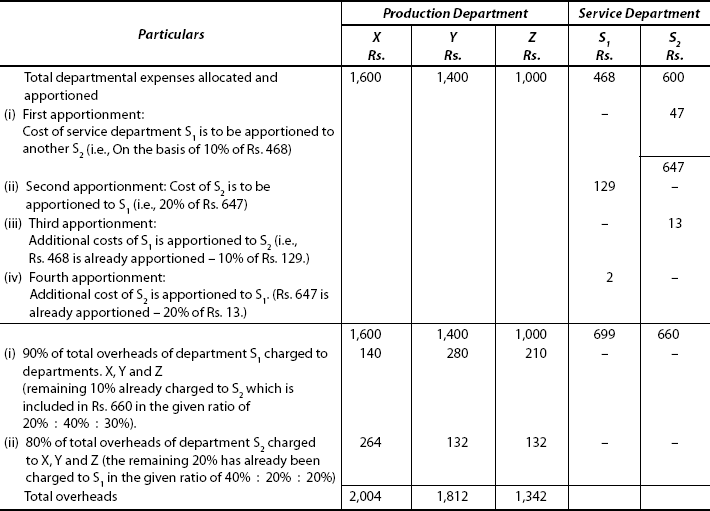

The total departmental expenses of ABC Co. Ltd are as follows:

You are required to prepare a statement showing the distribution of service department cost to production departments using the simultaneous equation method.

Solution

Step 1 → Let x represents the total overhead of Service Department 1.

Let y represents the total overhead of Service Department 2.

Step 2 → (i) x = 468 + 20% of y |

(1) |

y = 600 + 10% of x |

(2) |

(Simultaneous equations are formed as above with the figures available to find the total overhead cost.)

|

(ii) (or) x = |

|

|

y = |

|

|

(iii) (or) x = 468 + 0.2y |

(5) |

|

y = 600 + 0.1x |

(6) |

|

(iv) (or) x − 0.2y = 468 |

(7) |

|

y − 0.1x = 600 |

(8) |

Step 3 → Multiplying (7) and (8) by 10 to remove decimal, we get

|

10x − 2y = 4680 |

(9) |

|

10y − x = 6000 |

(10) |

Step 4 → Multiplying (9) by 5, we get

|

5 × 10x − 2y × 5 = 4680 × 5 |

|

|

50x − 10y = 23,400 |

(11) |

|

−x + 10y = 6,000 |

(12) |

Step 5 → Add (11) + (12): 49x + 0 = 29,400

Step 6 → Substituting the value of x in equation (12) we get,

Step 7 →

Now, based on these values, reapportionment of service-department expenses are to be ascertained.

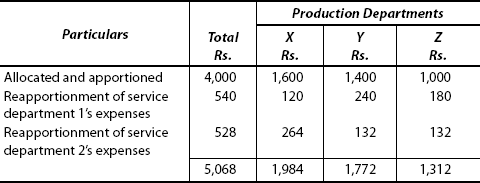

(a) For service department S1:

- X = 20% of Rs. 600; Y = 40% of 600; Z = 30% of 600

= Rs. 120; = Rs. 240; = Rs. 180.

Step 8 →

(b) Reapportionment of service department 2 ’s expenses:

- X = 40% of Rs. 660; Y = 20% of Rs. 660; Z = 20% of Rs. 660

= Rs. 264; Y = Rs. 132; = Rs. 132

Step 9 → Departmental Distribution Summary

4.5.2.6 Repeated Distribution Method

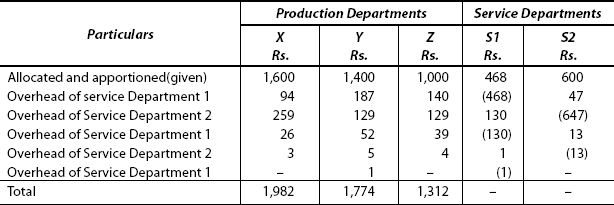

Under this method, the predetermined percentages are used for the reapportion of service-cost centre’s costs to production-cost centres and the other service departments. The redistribution goes on till the accounts in the service-cost-centre columns become “zero” or “too small value”.

Illustration 4.10

Same as the previous illustration no. 4.9.

Solution

NOTE 1:

The percentage given in the problem is the basis for the reapportionment of service department overheads to the other departments.

S1’s expense is reapportioned as follows:

S1’s expense = Rs. 468.

X = 20% (Given) Rs. 468 × ![]() = 93.6 or 94 (approx)

= 93.6 or 94 (approx)

Y = 40% (Given) Rs. 468 × ![]() = 187.2 or 187 (approx)

= 187.2 or 187 (approx)

Z = 30% (Given) Rs. 468 × ![]() = 140.4 or 140 (approx)

= 140.4 or 140 (approx)

S1 = 10% (Given) Rs. 468 × ![]() = 46.8 or 47 (approx)

= 46.8 or 47 (approx)

In a similar manner, the service departments are to be reapportioned and tabulated as follows:

NOTE:

The results under both these methods will be the same. (Variation of 1 or 2 may be due to round-off of fractions.)

4.5.2.7 Trial-and-Error Method

Under this method, the cost of one service department is apportioned to another service department. The cost of another service department PLUS the share received from the first cost centre is again apportioned to the first service department. This process is continued till the amount to be apportioned becomes “nil” or “too small value”.

Illustration 4.11

[As same illustration No. 4.9]

Solution

Take the same figures as in the previous illustration. The cost of one service-cost centre is apportioned to another in the following way:

4.6 ABSORPTION OF FACTORY OVERHEAD

Absorption of overheads means charging of overheads to individual products or jobs. The terminology of CIMA defines the absorption of overhead as “the process of absorbing all overhead costs allocated or apportioned over a particular cost centre or production department by the units produced”. A fair proportion of the total factory overhead should be assigned to each unit of production. This requires the identification of the main factor which causes the overhead to be incurred and then measuring the production in terms of that factor. Overhead absorption rates are applied for the absorption of overhead to individual jobs, processes or products. The factors that should be considered for the choice of proper overhead absorption rate are as follows:

- Base to be used.

- Actual or predetermined overhead rate to be used.

- Activity level to be used.

- Length of the period for accounting of overheads.

- The use of single blanket or multiple overhead rates

Actual or pre-determined overhead rate: The overhead absorption rate may be ascertained either based on the actual cost or on the estimated cost. Formulae for computing the overhead rates are as follows:

- Actual overhead rate:

Formula for computing the actual overhead rate is:

Actual overhead rate

- Predetermined overhead rate:

Pre - determined overhead rate

- Blanket overhead rate:

Blanket overhead rate

- Multiple overhead rate

4.6.1 Methods of Overhead Absorption

The overhead costs should be properly applied to the production units. Several factors should be considered for selecting a proper method to charge the overheads to jobs or products. Some of them are as follows:

- Factors mainly responsible for the incurrence of overhead.

- Nature of the product passing through the specific cost centre.

- Differences in the time taken by various products.

- Clerical costs.

- Selection of a suitable base.

- Neither over-recovery nor under-recovery of overheads.

- Amount charged should be equitable.

A suitable base is said to be the one which is economical, common to all products produced and distributes overhead in an equitable manner.

4.6.1.1 Method 1: Units of Production: (Rate Per Unit of Production)

Under this method, the charge per unit is computed by dividing the total estimated factory overhead by the total estimated units. The overhead absorption rate is calculated as follows:

This method is suitable when an organization produces only one product. In case an organization produces more than one product and they are similar too (differs only in volume and weight), then this method can be used by the conversion of physical units into equivalent units, which is done by using “points” or “weights”.

Illustration 4.12

From the following data, you are required to calculate the overhead absorption rate per unit:

Products produced |

A |

B |

Normal capacity (units) |

45,000 |

55,000 |

The estimated factory overhead for the budget period is Rs. 2,00,000.

Solution

- Formula:

Overhead absorption rate

- Substituting the figures in the above formula, we get:

Illustration 4.13

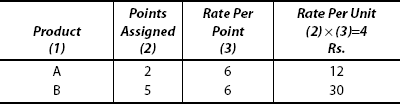

ABC Co. Ltd is a manufacturing company. It produces two products A and B. It has assigned 2 and 5 points to A and B, respectively, in order to compensate for the basic differences in products. The estimated factory overhead for the budget period is Rs. 2, 40,000. The normal capacity is:

|

A |

5,000 units |

|

B |

6,000 units |

You are required to calculate the overhead absorption rate.

Solution

- Total points for the normal capacity are to be calculated.

- Estimated overhead is to be divided by these total points to arrive at the overhead absorption rate (rate per point).

- Finally, this rate per point is to be multiplied by the points assigned to arrive at the rate per unit.

Overhead absorption rate per unit = ![]()

(rate per point) = Rs. 6.

Next, this rate per point is converted into rate per unit as follows:

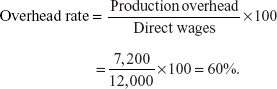

4.6.1.2 Method 2: Direct Material Cost

Under this method, the cost of direct materials is used as the base in the absorption of factory overheads. This is determined by expressing the estimated factory overhead as a percentage of direct material cost. The over head rate is calculated by using the formula:

Merits of this method:

- This method is simple to understand and easy to apply.

- When the prices of materials are stable, this method will be a more suitable one.

- Overhead cost relating to up-keep and handling of materials are absorbed equitably by this method.

Demerits:

- Most of the overheads accrue on the basis of time. This method ignores this factor.

- During the fluctuation of prices, this method will not at all be suitable as the factory overhead will not respond to such price-level changes.

4.6.1.3 Method 3: Direct Wages

In this method, the factory overhead expenses are charged as a percentage of direct wages incurred on jobs. The overhead rate is computed by dividing the estimated factory overhead by direct wages. The formula is as follows:

Merits:

- This method is easy as the needed information is readily available.

- This method considers the time factor.

- Change in the wage rate will not occur frequently. As such, the overhead rate is stable.

Demerits:

- The wage structure varies among the workers. So, it is not a suitable basis.

- The payment of overtime may create further complications.

- No distinction is made between jobs done by manual labour and those done by machines.

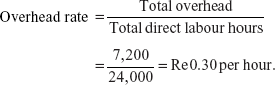

4.6.1.4 Method 4: Direct Labour Hours

This is a variation of direct wages method. In this method, the overhead rate is computed by dividing the factory overhead expenses by the direct labour hours. Formula is as follows:

The direct labour hours are estimated by taking into account the leave with wages, holidays and all normal wastage of time.

Merits:

- In case the labour operations dominate the manufacturing process, this is the most suitable method.

- This method recognizes the time factor.

Demerits:

- This is not suitable if cost centres mainly rely on machines.

- This method does not recognize the skill of workers.

4.6.1.5 Method 5: Prime Cost

Under this method, the overhead rate is determined by expressing the estimated factory overhead as a percentage of the estimated prime cost, where prime cost = direct material + direct labour. The prime cost method may be said to be a combination of two methods namely direct material method and direct wage method. The overhead rate is calculated as follows:

Merits:

- It is simple and easy to calculate.

- This method is suitable where the uniform labour hours and the uniform quality of materials are required in the manufacturing process.

Demerits:

- This method does not recognize the time factor. Overheads vary with time whereas both the material costs and labour costs do not vary with time as they do not bear any direct relationship with time.

- As the material prices are subject to frequent fluctuations, the amount of manufacturing overheads recovered would also fluctuate widely.

- This method does not recognize the skill of the workers.

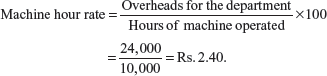

4.6.1.6 Method 6: Machine Hours

This method is based on the time required by machines. Under this method, the factory overheads are charged to production on the basis of the number of hours a machine was put to use. This is similar to direct labour hours method. This is calculated as follows:

- This method requires accumulation of machine hours used for each job or production unit.

- In case the operations are highly mechanized, the major portion of overheads is dependant upon the machines. For example, power, depreciation, machine oil, repairs and maintenance, insurance and so on. That is, only indirect expenses that are immediately connected with the operation of machine should be taken into account.

- Besides the expenses mentioned above, there are still some other manufacturing expenses like supervision charges, consumable stores, shop general labour, rent and taxes. These expenses are not charged to any machine. Hence, a proportionate amount of such expenses have to be added.

- Rate for charging the general departmental expenses to production has to be calculated separately on the basis of the direct labour hours. To arrive at an accurate result, both machine hour as well as labour hour rates must be applied.

ADVANTAGES:

- This method is suitable where machinery is the prime factor in production.

- This method is suitable where one operator uses many machines or several operators involve in one machine.

- This method recognizes the time factor, as a major portion of overheads vary with time.

DISADVANTAGES:

- The method is not suitable for labour-intensive cost centres.

- Additional work is involved in computing separate machine hour rate for each machine.

- Maintenance of operating time of machines may not be easy as it involves much time and additional labour.

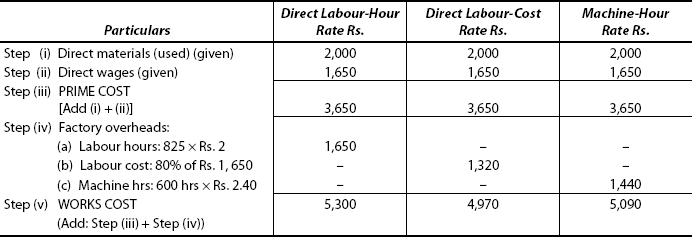

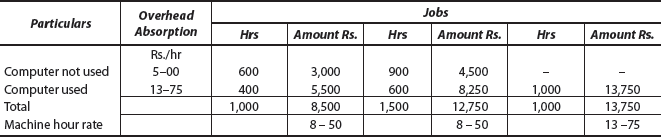

Illustration 4.14

Model: Combination of Labour hour and Machine hour methods

The following information relates to the activities of a production department for a certain period in a factor:

| Rs. | ||

|---|---|---|

Materials used |

|

36,000 |

Direct wages |

|

30,000 |

Hours of machine operation |

10,000 |

|

Labour hours worked |

12,000 |

|

Overheads chargeable to the department |

|

24,000 |

On one order carried out in the department during the period, the relevant data collected were as follows:

| Rs. | ||

|---|---|---|

Materials used |

|

2,000 |

Direct wages |

|

1,650 |

Labour hours |

825 |

|

Machine hours |

600 |

|

You are required to prepare a comparative statement of cost of this order by using the following three methods of recovery of overheads:

- Direct labour-hour-rate method

- Direct labour-cost-rate method

- Machine-hour-rate method.

[B.Com., Hons. (Delhi) – Modified]

Solution

(i) Direct labour hour rate; (ii) Direct labour cost %; and (iii) Machine hour rate will be calculated as follows:

Step 1: Calculation of direct labour-hour rate:

- Formula:

- Substituting the values in the formula, we get:

Step 2: Calculation of direct labour cost:

- Formula:

Step 3: Calculation of machine hour:

- Formula:

Step 4: Preparation of comparative statement of cost:

Illustration 4.15

Model: Plant-wise and departmental rates based on direct labour hours.

Trichy manufacturing company produces several product lines which are processed through these production departments – A, B and C.

The information concerning the relevant data for a year is as follows:

Production records at the end of the year indicated the following for the product line XX′.

You are required to:

- Calculate the departmental and plant-wise overhead rates based on direct labour hours.

- Compare the cost of XX′ line for the year using (i) plant-wise rate and (ii) departmental rates.

- Comment on the results

[B.Com – (Hons) – Modified]

Solution

- Departmental overhead rates are calculated on the basis of direct hours as follows:

- Department

- Department

- Department

- Department

- Plant-wise overhead is to be calculated on the basis of total factory overheads and total direct labour hours for all the three departments:

- Computation of the cost of XX′ line using departmental rates.

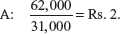

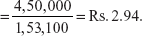

- Computation of cost of XX′ line using plant-wise rate.

Rs. (i) Prime cost (Total of A, B & C)

1,20,000

(ii) Add: Factory overheads: (5,000 + 6,000 + 9,000) × Rs. 2.94

58,800

(iii) FACTORY COST

1,78,800

Illustration 4.16

Model: Machine hour rate

A machine is purchased for cash at Rs. 18,400. Its working life is estimated to be 36,000 hours after which its scrap value is estimated at Rs. 400. It is assumed from the past experience that:

- the machine will work for 3,600 hours annually.

- the repair charges will be Rs. 2,160 during the whole period of life of the machine.

- the power consumption will be 10 units per hour at Re 0.10 per unit.

- other annual standing charges are estimated to be:

Rs.

(a) Rent of department

1,560(b) Light (24 points in the departments – 4 points engaged in the machine)

576

(c) Foreman’s salary

12,000

(d) Insurance premium for machinery

72

(e) Cotton waste

120

You are required to compute the machine hour rate on the basis of the above data for allocation of work expenses to all jobs for which the machine is used.

[M.Com – University of Madras – Modified]

Solution

| Particulars | Per Annum Rs. | Per Hour Rs. |

|---|---|---|

(a) Machine-running costs: |

|

|

Step 1: Depreciation: |

1,800, |

0.50 |

Step 2: Repairs & Maintenance: |

216 |

0.06 |

Step 3: Power: (10 units/hr × Re 0.10 × 3, 600 hrs) |

3,600 |

1.00 |

|

|

1.56 |

(b) Other overheads: |

|

|

(a) Rent |

312 |

0.09 |

(b) Lighting: |

96 |

0.03 |

(c) Insurance premium |

72 |

0.02 |

(d) Cotton waste |

120 |

0.03 |

(e) Foreman’s salary |

3,000 |

0.83 |

|

3,600 |

1.00 |

Total A + B |

|

2.56 |

Illustration 4.17

Model: Machine hour rate

You are required to calculate the machine hour rate from the following:

|

Rs. |

Cost of machine |

40,000 |

Cost of installation |

4,000 |

Scrap value after 10 years |

4,000 |

Rates and rents for a quarter of the shop: |

1,200 |

General lighting |

400 p.m. |

Shop supervisor’s salary per quarter |

12,000 |

Insurance premium for a machine |

240 p.a. |

Repairs (estimated) |

400 p.a. |

Power 3 units per hour @ Rs. 200 per 100 units |

|

Estimated working hours |

4000 p.a. |

The machine occupies 1/4 th of the total area of the shop. The supervisor is expected to devote 1/6 th of his time for supervising the machine. General lighting expenses are to be apportioned on the basis of floor area.

[C.S. – Inter – Modified]

Solution

| Particulars | Per Year Rs. | Per Year Rs. |

|---|---|---|

(a) Machine-running costs: |

|

|

(i) Cost of the machine: 40,000 |

|

|

Add: Installation 4,000 |

|

|

44,000 |

|

|

Less scrap 4,000 |

|

|

(Rs. 40, 000 ÷ 10 yrs: 4000 ÷ 4,000) = 40,000 ÷ 4,000 ÷ 10 yr. |

|

1.00 |

(ii) Repairs − Rs. 400 ÷ 4,000 hrs = |

|

0.10 |

(iii) Power units: 3 units @ Rs. 2 per units |

|

6.00 |

|

|

7.10 |

(b) Other overheads: |

|

|

(i) Rent and rates |

1,200 |

|

(ii) General lighting as per floor area: |

1,200 |

|

(iii) Supervisor’s salary |

8,000 |

|

(iv) Insurance premium |

240 |

|

Total |

10,640 |

|

(v) Hourly rate: Rs. 10,640 ÷ 4,000 hrs |

|

2.66 |

(a) + (b) → Machine hour rate |

|

9.76 |

Illustration 4.18

Model: Determination of selling price

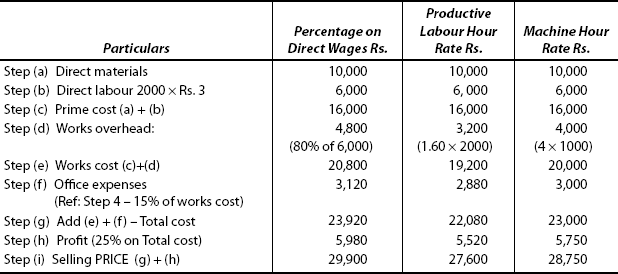

The following information relates to the cost records of a company.

| Rs. | |

|---|---|

Direct materials |

1,25,000 |

Direct labour |

1,00,000 |

Direct expenses |

10,000 |

Work overheads |

80.000 |

Office expenses |

47,250 |

The total number of direct labour hours were 50,000 involving 20,000 machine hours. What should be the price quoted for a job involving 2,000 labour hours@ Rs. 3 per hour, 1000 machine hours and Rs. 10,000 in direct materials if the profit desired is 20% on the selling price?

Solution

Apportionment of production overheads is computed as follows:

Step 1. Percentage on direct workers

Step 2. Productive labour hour rate

Step 3. Machine hour rate

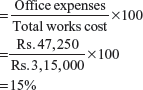

Step 4. Percentage of offi ce expenses to works cost:

Step 5. Statement of cost is to be prepared as follows:

Illustration 4.19

Model: Machine-hour-rate determination

Calculate the machine hour rate for recovery of overheads for a group of four machines from the following data:

Original cost of four machines Rs. 1,53,600.

Depreciation@ 10% per annum – straight line method.

Maintenance cost – average Rs. 16 per day of 8 hours for the group of machines.

Power – 50 paise per running hour per machine.

Supervision for the machine group – Rs. 1,280 per month.

Allocation of building depreciation for the four machines on a floor area basis@ Rs. 160 per month.

Share of manufacturing overheads – Rs. 480 per month for the group.

Normal working days in a year – 300 days.

Normal idle time – 20%.

Normal running – 1 shift of 8 hours.

[M.Com; Madras University – Modified]

Solution

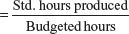

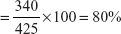

Step 1: Effective running hours per year:

= No of days × Hours per day × Productive hours

= 300 × 8 × (100% − 20% idle time) 80%

= 300 × 8 × ![]() = 1,920 hours.

= 1,920 hours.

Step 2: Machinery-running expenses: |

Per Hour |

|

(Rs.) |

(i) Power |

0.50 |

(ii) Depreciation: |

|

(iii) Maintenance |

|

|

|

Step 3: Other overheads (fixed)

|

|

Per Annum |

Per Hour |

|

|

Rs. |

Rs. |

(i) |

Supervision: |

3,840 |

|

(ii) |

Building depreciation: |

480 |

|

(iii) |

Manufacturing overhead: |

1,440 |

|

|

|

5,760 ÷ 1,920 |

= 3.00 |

|

|

|

|

Step 4: Machine hour rate (Step 2 + Step 3)

Illustration 4.20

Model: Absorption of factory overheads

The following figures have been extracted from the cost records of a manufacturing company. All jobs pass through the company’s two departments:

| Working Department Rs. | Finishing Department Rs. | |

|---|---|---|

Materials used |

24,000 |

2,000 |

Direct wages |

12,000 |

6,000 |

Production overhead |

7,200 |

4,800 |

Direct labour hours |

24,000 |

10,000 |

Machine hours |

20,000 |

4,000 |

The following information relates to Job No. J 115.

| Working Department Rs. | Finishing Department Rs. | |

|---|---|---|

Materials used |

480 |

40 |

Direct wages |

260 |

100 |

Direct labour hours |

520 |

140 |

Machine hours |

500 |

50 |

You are required to:

- Enumerate four methods of absorbing factory overheads by jobs showing the rates for each department under the methods quoted.

- Prepare a statement showing the different cost results for Job J 115 under any of the two methods referred to.

[M.Com; Madras University]

Solution

(a) Absorption of factory overheads is to be calculated under four different methods as follows:

STAGE I:

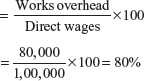

Method 1: Percentage on a direct material cost

- (Working department) Overhead rat =

- Finishing department overhead rate

STAGE II:

Method 2: Percentage on direct wages

- Working department:

- Finishing department:

STAGE III:

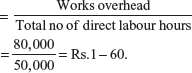

Method 3: Labour hour rate

- Working department:

- Finishing department

STAGE IV:

Method 4: Machine hour rate:

- Workingdept

- Finishing department

(b) Now, going to the second part of the question, the cost of production for Job No. 115 has to be computed.

I: “Percentage on direct wages” method is used for overhead absorption.

II: “Machine hour rate method” is used for overhead absorption:

Illustration 4.21

Model: Machine hour rate

The following annual charges are incurred in respect of a machine shop where the manual labour is almost nil.

There are five identical machines in the shop.

(i) |

Cost of each machine is Rs. 32,000 and the residual value after the expiry of the useful life of 10 years is |

Rs. 8,000 |

(ii) |

Power consumption p.a. as per metre reading (each machine uses 10 units of power@ 0.50 paise per unit) |

Rs. 30,000 |

(iii) |

Repairs and maintenance for 5 machines p.a |

Rs. 6,000 |

(iv) |

Rent and rates for the shop p.a. |

Rs. 24,000 |

(v) |

Electricity and lighting for the shop |

Rs. 2,400 |

(vi) |

Supervision: Two supervisors for the shop salary being Rs. 100 p.m. each. |

|

(vii) |

Sundry supplies such as lubricating oil, cotton waste, etc., for the shop |

Rs. 2,000 |

(viii) |

Canteen expenses for the shop p.a. |

Rs. 1,200 |

(ix) |

Hire-purchase annual instalment payable for the machines including Rs. 600 as interest |

Rs. 2,500 |

You are required to compute the machine hour rate for a machine.

[M.Com; Bharathidasan University]

Solution

First, the machine-running hours are calculated as follows:

Step 1. Value of power consumed: |

Rs. 30, 000. |

Step 2. Rate per unit: |

Re 0.50. |

|

|

|

|

Step 5. No. of units used/hour: |

10. |

|

|

Next, machine hour rate is to be computed as follows:

| Particulars | Per Annum Rs. | Per Hour Rs. |

|---|---|---|

(a): Machine-running expenses (variable) |

|

|

Step1: Depreciation: [Rs. 32, 000 – Rs. 8, 000 (residue) ÷ 10 years] |

2,400 |

2.00 |

Step 2: Power (10 units × 0.50 per unit) |

– |

5.00 |

Step 3: Repairs and maintenance |

1,200 |

1.00 |

Step 4 Sundry expenses (2, 000 ÷ 5) |

400 |

0.33 |

|

|

8.33 |

(b) Other overheads (fixed): |

|

|

Step 5: Rent and rates (24, 000 ÷ 5) |

4,800 |

4.00 |

Step 6: Electricity & Lighting (24,00 ÷ 5) |

480 |

.40 |

Step 7: Supervision: (Rs. 100 × 12 × 2 ÷ 5) |

480 |

.40 |

Step 8: Canteen (Rs. 1, 200 ÷ 5) |

240 |

.20 |

Step 9: HP interest (Rs. 600 ÷ 5) |

120 |

.10 |

|

|

5.10 |

(c): Step 10: MACHINE HOUR RATE – (A) + (B) |

|

13.43 |

4.7 OVER ABSORPTION OR UNDER ABSORPTION

In case of factories, the overhead expenses are based on predetermined rates. In practice, the amount of expenses incurred will vary from the predetermined expenses. Some differences persist. In case the actual overhead incurred is higher than the overhead absorbed (applied), it is known as “under-absorption of overhead”. But if the overhead absorbed is higher than the actual overhead incurred, it is known as “over-absorption of overhead”. This kind of over- or under-absorption of overhead is termed as “overhead variance”. The amount of over-absorption is represented by the credit balance on the variance account. The amount of under-absorption is represented by a debit balance on the variance account. The organization should analyse such under- or over-absorption of overheads and find out the causes responsible for such overhead variance.

4.7.1 Reasons for Under-Absorption of Overheads

- It may be caused due to idle capacity.

- There may not be a proper basis for predetermining the overhead rates.

- Failure to consider all vital factors may lead to errors in determining the estimates.

4.7.2 Reasons for Over-Absorption of Overheads

- When the actual level of operations exceed the normal level.

- Errors made in determining the overhead rates without considering factors like correct estimation of normal production level, methods of production, etc.

4.7.3 Accounting Treatment of Over- or Under-Absorbed Overheads

The under- or over-absorbed overheads must be disposed. When the product cost gets distorted due to overhead variances it has to be rectified. The important methods followed for the disposal of under- or over-absorbed overheads are as follows:

Method 1: Use of supplementary rates:

- The cost of a product may be adjusted by using supplementary rates. This is used when the difference is high and it is caused by errors in determining the overhead rates.

- This supplementary rate is calculated by dividing the amount of variance (over- or under-absorption) by the base which was used for absorption.

- In case of under-absorption, the respective amount is set right by a negative rate while doing adjustment.

- At the end of the accounting period, over- or under-absorption amount is adjusted in work-in-progress (WIP), finished stock, the cost of sales in proportion to direct labour hours or machine hours or the value of the balances of such accounts by use of a supplementary rate. The amount so adjusted will be shown in the balance sheet as deductions from the WIP or finished goods, as the case may be.

Method 2: Transfer to overhead reserve or suspense account:

- This method is used in two different situations. First, in the case of new organizations, when the difference arises to non-utilization of 100% of capacity, in the initial years. Second, when the difference arises due to seasonal fluctuations and the business cycle is a prolonged one.

- Overhead difference is transferred to either the overhead reserve or suspense account.

- In case of under-absorption, this amount is carried forward to subsequent accounting periods and written off as a deferred charge.

- In case of over-absorption, it is carried forward and credited as a deferred credit.

Method 3: Written off to costing and profit-and-loss account:

- In the case of under absorption, the difference is debited to the costing and profit-and-loss account (P&L A/c).

- In the case of over absorption, the difference is credited to the costing and P&L A/c.

Illustration 4.22

Model: Over- or Under-absorption

The budgeted activity and cost data for each half year of XY Ltd were as follows:

|

Rs. |

Direct labour hours |

34,000 |

Direct wages |

21,250 |

Overhead: |

18,700 |

Fixed variable |

32,300 |

During the first six months, the following actual results were achieved:

Direct labour hours incurred |

32,500 |

Direct wages |

42,750 |

Overhead: |

19,350 |

Fixed variable |

32,900 |

The existing method of absorbing overhead is by a direct-wage percentage rate. A proposal has been made to change the overhead absorption to a direct labour-hour rate analysed into fixed and variable overhead.

You are required to calculate under the new proposal (i.e., using direct labour-hour rates of absorption) for the first six months period:

- The budget of direct labour-hour rates of overhead absorption for fixed and variable overheads.

- The absorbed overhead.

- The over- or under-absorbed overhead.

[B.Com. (Hons) – Delhi – Modified]

Solution

Step 1: Write the formula for computing the overhead rates.

Overhead absorption rate (Based on direct labour hours) ![]()

|

|

|

|

Step 4: Total (Step 2 + step 3) |

|

Step 5: Absorbed overheads = Total rate × Direct labour hour

Step 6: Actual overheads = Rs. 19, 350 + Rs. 32, 900 = Rs. 52,250.

Step 7: Absorbed overheads is less than actual overheads.

Hence, it is under-absorption.

Under-absorption |

= |

Actual overheads − Absorbed overheads |

|

= |

Rs. 52, 250 − Rs. 48, 750 |

|

= |

Rs. 3, 500. |

Illustration 4.23

Model: Treatment of under-recovery

In a manufacturing unit, the overhead was recovered at a predetermined rate of Rs. 30 per man-day. The total factory overhead expenses incurred and the man-days actually worked were Rs. 65 lakhs and 2 lakhs days, respectively.

Out of the 60,000 units produced during a period, 40,000 units were sold. On analysing the reasons, it was found that 60% of the unabsorbed overheads were due to defective planning and the rest were attributable to the increase in the overhead costs. How would the unabsorbed overheads be treated in cost accounts?

[B.Com – Delhi – Modified]

Solution

Step 1: Recovered overheads |

= |

Rate × actual man-days |

|

= |

Rs. 30 × 2 lakhs |

|

= |

Rs. 60 lakhs. |

Step 2: Under-recovery of overheads |

= |

Actual overheads − Recovered overhead |

|

= |

Rs. 65 lakhs − Rs. 60 lakhs |

|

= |

Rs. 5 lakhs. |

Step 3: Reasons for under-recovery:

- Defective planning = 60% of Rs. 5 lakhs

- Increase in overhead costs = 40% of Rs. 5 lakhs

Step 4: Treatment of under-recovery:

- Under-recovery of Rs. 3 lakhs due to a defective planning would be charged to costing P&L A/c, as it is an abnormal occurrence.

- Under-recovery of Rs. 2 lakhs due to an increase in the overhead rates would be recovered from the cost of sales account and the finished goods stock in the ratio of *2:1.

- A positive supplementary rate is charged.

Step 5: Amount to be charged:

- Cost of sales A/c: Rs. 2 lakhs ×

= Rs.1.33 lakhs.

= Rs.1.33 lakhs. - Finished goods stock A/c: Rs.2 lakhs ×

= Rs. 0.67 lakhs.

= Rs. 0.67 lakhs.

*NOTE: Ratio between the cost of sales and finished goods stock is:

40,000 units sold : 20,000 not sold (finished stock)

Illustration 4.24

Model: Unabsorbed overheads and Supplementary rate

The total overhead expenses of a factory are Rs. 4,50,000. Taking into account the normal working of the factory, the overhead was recovered from production at Rs.1.40 per hour. The actual hours worked were 2,80,000. How would you proceed to close the books of accounts, assuming that besides the 4,500 units that were produced of which 3,800 were sold, there were 500 equivalent units in WIP. On investigation, it was found that 50% of the unabsorbed overhead was on account of increase in the cost of indirect material and indirect labour and the other 50% was due to the factory’s inefficiency.

[B.Com (Hon) – Delhi – Material]

Solution

- First, the unabsorbed overheads are to be ascertained.

- Then, 50% of the unabsorbed is to be taken to find the supplementary rate.

- Finally, it has to be apportioned between the cost of sales, finished goods and WIP.

STAGE I: Computation of unabsorbed overheads:

|

|

Rs. |

Step 1: |

Overheads recovered (2,50,000 hrs × Rs. 1.40) |

= 3,92,000 |

Step 2: |

Actual overheads |

= 4,50,000 |

Step 3: |

Unabsorbed overheads (3 − 2) |

= 58,000 |

STAGE II: Calculation of supplementary rate:

Out of the total unabsorbed overheads of Rs. 58,000, 50% was due to an increase in the cost of indirect material and indirect labour. Hence, this 50% amount, that is, Rs. 29,000 has to be charged to units produced by “supplementary rate”, which is calculated as follows:

|

|

Rs. |

Step 4: |

Unabsorbed overheads on account of increase in the cost of indirect material and indirect labour |

= 29,000 |

Step 5: |

Units produced: (Produced + WIP = 4,500 + 500) |

= 5000 units. |

|

|

|

|

|

= Rs. 5.80 per unit. |

STAGE III : |

The amount of overheads of Rs. 29,000 has to be apportioned between the cost of sales, finished goods and WIP as follows: |

|

|

Rs. |

Step 7: |

Cost of sales account: (No. of units sold × Supplementary rate) |

|

|

(3,800 × Rs. 5.80) |

= 22,040. |

Step 8: |

Finished goods A/c (No. of units × Supplementary rate) |

|

|

(5000 – (3,800 + 500)) = (5000 – 4300) = 700 × Rs. 5.80 |

= 4,060 |

Step 9: |

WIP A/c (500 units × Rs. 5.80) |

= 2,900 |

|

|

|

Step 10: |

The remaining balance 50% of Rs. 29,000 should be transferred to costing P&L A/c—because this part of the unabsorbed overhead is due to the factory’s inefficiency—an abnormal factor. |

FOR PROFESSIONAL COURSES

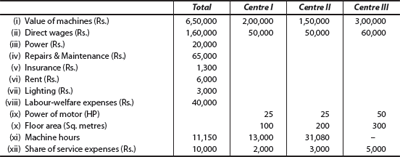

Illustration 4.25

Model: Comprehensive hour rate

A machine shop has eight identical handling machines manned by six operators. The machines cannot be worked without an operator wholly engaged to it. The original cost of all these 8 machines works out to Rs. 8 lakhs.

These particulars are furnished for a six-month period:

Normal available hours per month |

= 208 |

Absenteeism (without pay) hours |

= 18 |

Leave (with pay) hours |

= 20 |

Normal and idle unavoidable hours |

= 10 |

Average rate of wages per day of 8 hours |

= Rs. 20 |

Production bonus estimated |

= 15% on wages |

Value of power consumed |

= Rs. 8,050 |

Supervision and indirect labour |

= Rs. 3,300 |

Lighting & Electricity |

= Rs. 1,200 |

These particulars are for a year: |

|

Repairs & Maintenance including consumables |

= 3% on value |

Insurance |

= Rs. 50,000 |

Other sundry-work expenses |

= Rs. 15,000 |

General-management expenses allocated |

= Rs. 60,000. |

You are required to work out a comprehensive machine hour rate for the machine shop.

[C.A. (Inter) – Adapted & Modified]