3

Direct Labour and Direct Expenses

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Understand the meaning of direct labour and indirect labour.

Explain the terms: time-study, motion study, job analysis and job evaluation.

Know the various records that are in use for recording attendance and time of workers.

Account for holiday pay, idle time and overtime in cost accounts.

Understand the factors associated with labour turnover.

Appraise the different methods of wage payment.

Understand the salient features of different incentive plans.

Ascertain the wage payable to workers under different methods of wage payment.

Understand the meaning of direct expenses.

Know the characteristics of direct expenses

Explain the meaning of certain important key terms.

Another important element of cost is “labour”. Labour may be said to be the key stone of an industrial concern. A reduction in labour cost would make any organization competitive. Till the advent of technological advancement, labour cost constituted the major portion of the total production cost. With the increase in mechanization, automation and the like, the importance of labour is not yet minimized. Indeed, mechanization also depends on highly-skilled labour. However, whatever may be the situation, the study on all related factors regarding labour has gained much importance because the productivity of all other resources depend to a greater extent on the productivity of an employee. Further, in our country, all SMEs (small- and medium-sized enterprises) are dependent upon labour alone for their entire operations. In this chapter, we are going to discuss the meaning of direct labour, accounting and controlling of the labour costs, labour turnover and all related factors on labour in detail.

3.1 MEANING AND DEFINITION OF LABOUR COST

The term “labour cost” represents wages paid to the workers employed in business organizations for producing goods or rendering services. It also represents the various payments made to an employee (worker), which are as follows:

- Immediate monetary benefits:

- Basic wages

- Dearness allowance (DA)

- Production bonus

- Deferred monetary benefits:

- Employer’s contribution to Provident Fund (PF)

- Employer’s contribution to Employees’ State Insurance Corporation (ESIC)

- Retirement benefit like gratuity

- Profit bonus

- Fringe benefits:

Free or subsidized food, housing, transport to office, medical facilities, canteen, recreational activities and the like. Fringe benefits categorized under ‘c’ are generally treated as manufacturing overheads. The labour cost may be classified into:

Direct labour costs and

Indirect labour costs

3.1.1 Direct Labour Cost

Direct labour is “where employees are employed directly in making the product and their work can be readily identified in the process of conversion of raw materials into finished goods”.

The cost incurred on direct labour is known as “direct labour cost”. Direct labour is the time spent by workers in making the product. Their work can be readily identified in the process of conversion of raw materials into finished goods. All other labour is “indirect labour”. Direct labour can be easily identified and charged to a single costing unit.

3.1.2 Indirect Labour Cost

This refers to the labour expended that does not alter the construction, composition or the condition of the product. Wages which cannot be readily identifiable with a job, process or operation are called “indirect labour cost”.

Examples:

General indirect labour like inspectors, supervisors, wages for maintenance workers, idle-time wages, overtime and the like.

Indirect labour is treated as part of the factory overhead. For the purpose of cost analysis and cost control, the need arises to distinguish between direct labour cost and indirect labour cost. The distinction should be made for:

- Ascertaining accurate labour cost which provides a basis for proper control.

- Computing labour efficiency.

- Allocating overheads.

- Ascertaining total labour costs.

- Introducing new incentive schemes.

3.2 TIME-RECORDING

Recording of time involves two purposes, namely, “time-keeping” and “time-booking”. It is essential for any type of workers–direct, indirect, casual, hired and outworkers.

Time-keeping is necessary to:

- Record attendance and time.

- Calculate wages.

Time-booking is necessary for

- Cost analysis and

- Cost apportionment

When time-keeping and time-booking tally, record keeping will be perfect and accurate.

3.2.1 Time-Keeping

When a worker enters a factory, his attendance is recorded at the factory entrance. This function is performed by a person known as the “time-keeper” and at the place called “time-office”. The date and time of arrival are noted. This process of making the attendance of workers, the time of arrival and departure is known as “time-keeping”. The methods employed for time-keeping are clock card, check or disc.

3.2.1.1 Purposes of Time-Keeping

As already explained, the underlying purpose of keeping time-records is to provide the necessary basic data for the payroll department to compute and prepare the pay roll. Time-keeping has the following aims:

- Payroll purposes:

To show the number of hours worked.

To disclose absence or tardiness.

To measure overtime and calculate extra pay.

To provide evidence of compliance with legal requirements.

- Cost Purposes

To know the quantity of work done on each job

To know the cost of work done.

Wages paid on the piece-rate basis, for casual-labour-hired workers and the like would also require that attendance be recorded for the following reasons:

Recording of attendance is essential for ascertaining cost.

To compute overhead rates based on the labour rates.

To ensure discipline among the workers.

To avoid or reduce idle time.

To comply with the production schedule.

To calculate any financial benefits such as overtime, DA, bonus, PF, pension and the like.

To provide statistical data.

3.2.2 Time-Booking

Workers may be deputed on different operations or jobs or processes. Time spent by each worker in activities entrusted with them, is an important factor. The process of recording the time spent in a working day on various operations, jobs or processes is known as “Time-Keeping”. Job cards, piece-work tickets, time-tickets are used for marking the time-in and the time-out in each activity where a worker works.

Objectives underlying time-booking are:

To ascertain the labour cost of various products and jobs.

To evaluate the labour performance.

To ascertain the time spent on each job.

To analyse idle time.

To apportion overheads.

To determine the overhead rates of absorbing the overhead expenses as per the labour-hour and machine-hour methods.

3.3 LABOUR TIME-RECORDS

Maintenance of Labour Time-Records.

It is necessary to maintain the following records in a factory for the purpose of attendance, time spent on jobs, and the output of a worker:

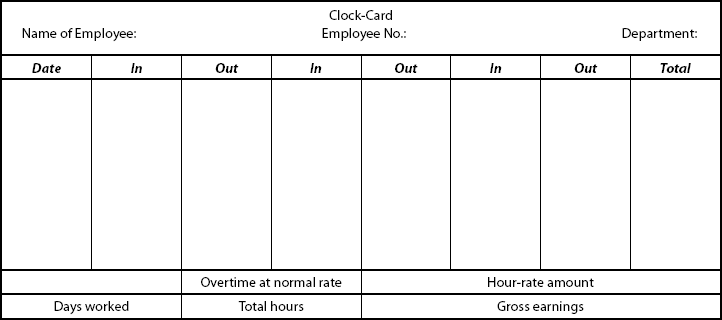

3.3.1 Clock-Card

This is used for recording the date and time of entry and departure of workers. Each worker is given a clock-card. At the time of entry or departure, this card is inserted in a specific place in the time-recording clock and the date and time of entry and departure would be punched on it. Now a days, time-clocks are connected to main-frame computers. This provides input data to the computer for preparation of daily attendance reports and payroll at the end of the wage period.

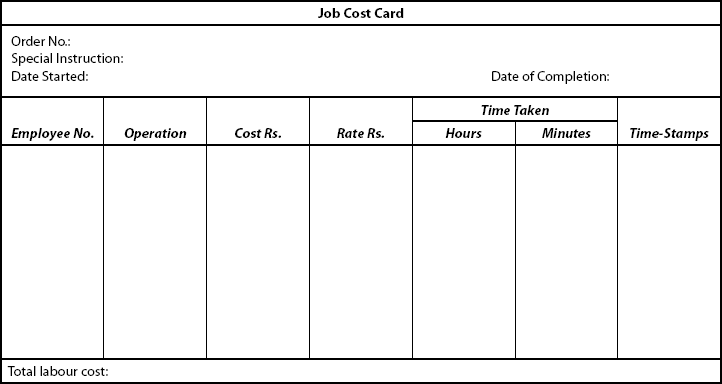

3.3.2 Job Cards

This document is used for recording the time spent by various workers on each job. When a job is commenced, a job number is allotted to it. The job card moves along with the job. The starting date and time of each operation is entered in it. When the job is completed, the total time spent by the worker is calculated. Materials consumed for each operation is entered in the job card (on the reverse side). It is also called “labour-cost card”.

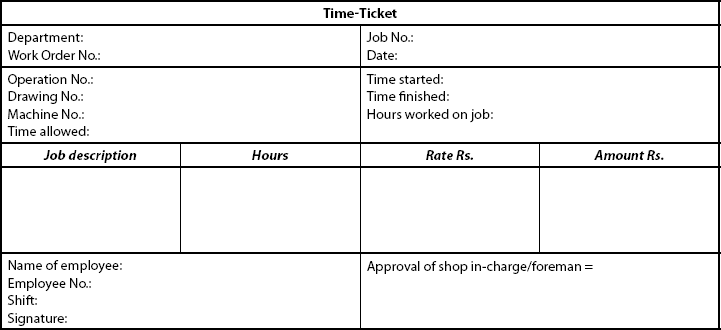

3.3.3 Time-Ticket

This is used for recording the time spent by each worker in the factory. Where workers are to be paid on the basis of time, time-ticket will be much useful.

3.3.4 Piece-Work Tickets

Payments to workers may be made either on the basis of time spent in the factory or on the number of units produced. Payment on the basis of time is known as ‘time rate’ whereas payment on the basis of number of units produced is known as “piece rate”.

When piece rate is adopted, a piece-work card is necessary. It shows the number of units produced each day by a worker. At the same time, it is also necessary to maintain time-ticket also in order to (i) apportion the overheads based on the time worked on each job and (ii) when payment of bonus or premium is made on the basis of the time saved, both the time taken and number of units produced are required.

Piece-work card has to be reconciled with the payroll on a continuous basis.

3.3.5 The Check or Disc Method

Metal discs are used. In metal discs, a worker’s employment number is inscribed. At the factory entrance gate, these discs are placed on a board. When a worker enters the factory, he picks up his disc and leaves it in a box kept exclusively for this. When the reporting time is over, the box will be removed. Workers arriving late have to put their discs in a separate box. After half-an-hour intervals the foreman replaces the boxes with the new ones. This is done in order to deduct the wages on a uniform basis for each step of half an hour.

Reconciliation of time-paid for as per time-keeping records and time-booked:

The time recorded at the factory gates with the time booked on jobs must be reconciled. If the time shown in the clock-card exceeds the time booked on different jobs, the difference is reported as “idle time.” On the other hand, if the total time booked exceeds the time recorded on the clock card, the difference is reported as “error”. This has to be corrected.

Reconciliation serves two purposes:

- To exercise control over wastage of labour time and

- To prevent dummy workers’ inclusion in payroll.

3.4 ACCOUNTING OF LABOUR COST

The payments made to labour have to be properly accounted for as it constitutes a significant portion of the total cost. Sufficient care to be taken from the stage of recruitment till they leave the firms. Proper care of labour will reduce the cost of production. Hence, the labour cost has to be controlled effectively for which the following departments will assist the task. They are:

- Personnel department

- Time-keeping department

- Engineering and work-study department

- Payroll department

- Cost Accounting department

Before dealing with the accounting of labour cost, one has to understand that the cost incurred on workers consists of a numbers of items. These may be broadly grouped into the following three heads:

- Monetary benefits

- Non-monetary benefits (or) Fringe benefits

- Deferred monetary benefits (or) Terminal benefits

3.4.1 Monetary Benefits

The following items are included in this category:

- Basic wages: This is the basic rate of pay. It is fixed on the taking into account the employee’s position (hierarchy level) in a firm.

- Dearness allowance: The payment of dearness allowance (DA) is usually linked with the cost of living index. This is paid in order to compensate a rise in the cost of living. This amount is fixed on basic wages by way of certain percentage on it.

- House rent allowance: This is another constituent of wage. As firms could not provide house for each worker, HRA is awarded.

- Overtime pay: This is paid for the extra hours they worked.

- Profit-sharing bonus: This is a scheme of sharing profit between the employer and the employee. It is governed by the payment of Bonus Act, 1965. Minimum bonus is 8.33%. The maximum bonus is 20%.

- Incentive bonus: This is otherwise known as production bonus. Employees are rewarded with this type of bonus for their efficiency which exceeds the standard. This varies from firm to firm.

- Contribution to PF: Any organization has to contribute 10% of the worker’s pay (Basic wages + DA) to PF compulsorily. A similar amount of contribution comes from the worker. This scheme is governed by the Employees Provident Funds Act, 1952.

- Contributions under ESIC: It is compulsory for any organization to contribute a certain percentage of monthly wages (Basic pay + DA) of employees to Employees’ State Insurance Corporation (ESIC). This scheme is governed by the Act.

- Contribution of superanuation/pension fund

- Holiday pay

- Special incentives

- Special allowances–night shift, children’s educational allowance and so on.

3.4.2 Non-Monetary Benefits

In this category, the employer does not pay any money to its employees but extends benefits such as hospital facilities, subsidized food, subsidized or free transport and recreational facilities to employees. The employer bears the cost.

3.4.3 Deferred Monetary Benefits or Terminal Benefits

The benefits under this category are not paid each month but in future. For example, pension, gratuity, and so on.

3.4.4 Accounting of Labour Cost

Any payments made to both direct labour and indirect labour should be accounted for. For Direct labour (or direct workers), the following two different ways of accounting for labour cost are followed:

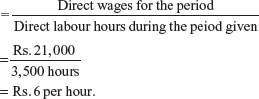

- Only two items as described in the previous paragraph, that is, basic wages and DA are charged to jobs or units produced by using an hourly rate while the remaining monetary benefits and the cost of non-monetary benefits are treated as an overhead. The formula for computing the rate per hour is as under:

- The other method involves the charging of monetary as well as the cost of non-benefits to jobs or units produced by using an hourly rate as follows:

For Indirect Labour (Indirect Workers), both the costs of monetary as well as non-monetary benefits are charged to overheads.

Illustrations

Illustration 3.1

Model: Ascertainment of labour cost

From the following particulars, you are required to prepare a statement of labour cost showing the cost per day of 8 hours:

- Monthly salary Rs. = 5,000.

- Leave salary = 10% of salary.

- Employer’s contribution to PF = 10% of (a) & (b).

- Employer’s contribution to ESI = 2% of (a) & (b).

- Pro-rata expenditure on amenities to labour = Rs. 20–50 per worker, per month.

- No. of working hours in a month = 200.

Solution

Step 1: All costs (monetary & non-monetary benefits) of items are to be added (i.e., (a) to (d)).

Step 2: The sum of costs will be the total cost.

Step 3: The sum total arrived at Step 2 is to be divided by no. of working hours (i.e., (f) 200 hrs).

Step 4: Labour cost per hour as calculated in Step 2 is to be multiplied by the no. of hours (i.e., 8) to determine the labour cost per day.

Statement of Labour Cost per month

Step 1: Add all the items: |

Rs. |

(a) Salary = |

5,000 |

(b) Leave salary (10% of Rs. 5,000) = |

500 |

(c) Employer’s contribution to PF – 10% on (a) + (b) i.e., 10% of (Rs. 5000 + Rs. 500) = |

550 |

(d) Employer’s contribution to ESI – 2% on (a) and (b) i.e., 2% (Rs. 5,000 + Rs. 500) = |

110 |

(e) Pro-rate expenses on the amenities to labour = |

20.50 |

Step 2: Total labour for the month (200 hrs) (Add Step 1 (a) to (e)) = |

6,180.50 |

Step 3: Labour cost per hour (Step 2 ÷ 200 hours Rs. 6,180 – 50 ÷ 200) = |

30.90 |

Step 4: Labour cost per day for 8 hrs: 8 hrs × Rs. 30.90 (as in Step3) = |

247.20. |

Illustration 3.2

Model: Labour cost to employer

- Monthly salary (Basic wages) = Rs. 6,000.

- DA = 10% of (a).

- Leave salary payable to workman = 15% of (a) and (b).

- Employee’s contribution to PF = 8% of (a) and (b).

- Employer’s contribution to ESI = 5% of (a) & (b).

- Employee’s contribution to ESI – same as (e).

- Pro-rata expenditure on amenities to labour = Rs. 50 per head per month.

- No. of working hours in a month = 200 hours.

From the above data, prepare a statement showing the cost per day of 8 hours of engaging a particular type of labour.

Solution

Labour cost per day to the employer is to be calculated.

Important Note

Employee’s contribution to PF or ESIC should not be taken into account for computation of labour cost.

Step 1: Basic calculation to be done:

In this problem, the calculation of working days in a month is to be calculated as under:

No. of working hours in a month (given in the problem) = 200 hours.

Working hours per day (given) = 8 hours.

Working days in a month (i) ÷ (ii) (200 ÷ 8 hrs) = 25 days.

Step 2: Preparation of statement of labour cost

| Particulars | Rs. | Paise |

|---|---|---|

(i) Step (a) Basic wages per day: |

240 |

– |

Step (b) DA: per month: per day: Rs.10% of 6,000 |

24 |

– |

Step (c) Leave salary: (15% of 240+24) (15% of 6,000+600÷25). |

39 |

60 |

Step (d) Employer’s contribution to ESIC: (5% of 6,000+600÷25). |

13 |

20 |

Step (e) Amenities to labour: (Rs. 50÷25days). |

2 |

00 |

(ii) Add I (a) to (e): Cost per man day |

318 |

80 |

Illustration 3.3

Model: Cash needed for wage payment

From the following particulars, find the amount required for cash payment of wages in a factory for a particular month:

| Rs. | |

|---|---|

Wages for normal hours worked |

3,00,000 |

Wages for overtime worked |

10,000 |

Leave wages |

8,000 |

Deduction for ESI |

6,000 |

Employee’s contribution to PF |

30,000 |

House rent to be recovered from 50 employees at Rs.100 per month. Employer also contributes an equal amount towards PF and ESIC.

Solution

Important Note

Employee’s contribution to PF and ESIC should not be taken into account while computing wages. First, the gross wages payable is determined. Then, from this, the employee’s contribution to PF, ESI and HRA to be recovered are to be deducted because such expenditure is not needed now by the management. That is, there is no actual disbursement.

The statement showing wages payable in cash is as follows:

| Particulars | Rs. | Rs. |

|---|---|---|

Step 1: (ADD:) |

|

|

Wages for normal working hours |

|

3,00,000 |

Wages for overtime worked |

|

10,000 |

Leave wages |

|

8,000 |

Step 2: Gross wages payable |

|

3,18,000 |

(Add : Step (i) to (iii)) |

|

|

Step 3: (Deductions:) |

|

|

Employee’s contribution to ESIC |

6,000 |

|

Employee’s contribution to PF |

30,000 |

|

House rent to be recovered from 50 employees @ Rs.100 p.m. |

5,000 |

41,000 |

Step 4: Amount required for cash payment of wages for a particular month Step 2 – Step (i + ii + iii) |

– |

2,77,000 |

Illustration 3.4

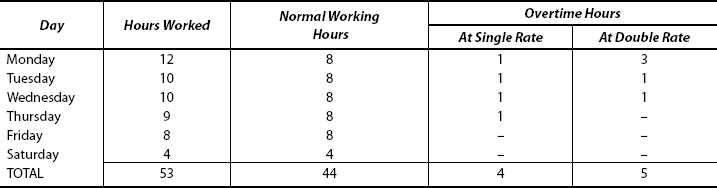

Model: Computation of normal and overtime wages

Calculate the normal wages and overtime wages payable to a workman from the following data:

| Days | Hours Worked |

|---|---|

Monday |

12 |

Tuesday |

10 |

Wednesday |

10 |

Thursday |

9 |

Friday |

8 |

Saturday |

4 |

|

53 |

Normal working hours: 8 hours per day.

On Saturday: 4 hours per day.

Normal rate: Rs. 2 per hour.

Overtime rate: Up to 9 hours in a day at single rate and over 9 hours a day at double rate

(or)

Up to 48 hours in a week at single rate and over 48 hours at double rate whichever is more beneficial to the workers.

[Madras University B.Com (modified)]

Solution

Following steps are to be followed:

- Normal working hours.

- Overtime working hours at single rate.

- Overtime working hours at double rate have to be determined for each day and for the week as well.

Next, computation of total wages to be made:

- On day’s work basis.

- On week’s work basis.

STAGE I: Preparation of statement showing normal and overtime hours and wages

Out of 53 hours worked in a week:

44 hours are normal working hours

4 hours are overtime at single rate

5 hours are overtime at double rate

STAGE II: Computation of total wages on a day’s work basis

|

Rs. |

Step 1: Wages for normal working hours – (44 hours × Rs. 2) – |

88 |

Step 2: Wages for overtime wages: |

|

(i) At single rate: 4 hrs × Rs. 2: |

8 |

(ii) At Double rate: 5 hrs × Rs. 4: |

20 |

Step 3: Total Wages (Add 1 and 2 (i) & (ii)) |

116 |

STAGE III: Computation of total wages on a week’s work basis.

Step 1: Normal rare wages (44 + 4 hours) 48 hours × Rs. 2 = |

96 |

Step 2: Overtime wages: 5 hours × Rs. 4 = |

20 |

Step 3: Total wages (Add 1 and 2) |

116 |

Step 4: |

|

Decision: Total wages under both the approaches are same, that is, Rs. 116.

Hence, both methods are equally beneficial to the worker.

Illustration 3.5

Model: Allocation of wages

Rajeev, a worker in a manufacturing unit, is paid at the rate of Rs. 20 per hour. His working hours constitute 48 hours over 6 days a week. Time allowed per day as approved absence for personal needs and so on is 20 minutes.

Rajeev’s card for the week ended in a particular month shows that his time during the week is chargeable as follows:

Job No. X: 25 hours

Job No. Y: 15 hours

Job No. Z: 3 hours

The time unaccounted for is due to a power failure. You are required to show Rajeev’s wages for the week and how they would be dealt with in Cost Accounts?

Solution

STAGE I: Basic calculations:

Step 1: Computation of normal idle time:

Normal idle time: 6 days × 20 minutes each day

= 120 minutes

= 2 hours.

Step 2: Computation of abnormal idle time:

Abnormal idle time |

= |

Working hours in a week – Hours actually spent |

|

= |

48 hours – (X: 25 hrs + Y: 15 hrs + Z: 3 hrs + 2 hrs (normal idle time) |

|

= |

48 hrs – 45 hrs |

|

= |

3 hrs. |

Step 3: Normal idle-time (i.e., wages for approved absence) wages to be recovered as factory overhead:

Step 4: Abnormal idle time wages have to be treated as abnormal loss and charged to costing P&L A/c:

Wages for abnormal idle time:

STAGE II: Preparation of a statement showing allocation of worker’s wages

Illustration 3.6

Model: Worker’s earnings – Labour cost and its allocation to jobs

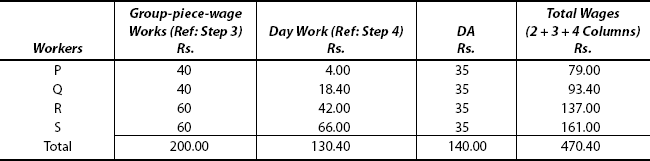

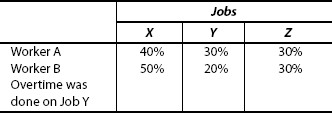

Calculate the earnings of worker P and Q for a month and allocate the earnings of each to job X, Y and Z.

| P | Q | |

|---|---|---|

(i) Basic wages |

Rs. 400 |

600 |

(ii) DA |

50% |

50% |

(iii) PF (on basic wages) |

10% |

10% |

(iv) ESI (on basic wages) |

2% |

2% |

(v) Overtime |

10 hrs |

– |

(vi) Idle time and leave |

– |

16 hrs |

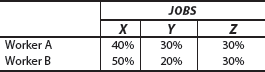

The normal working hours for the month are 200 hrs. Overtime is paid at double the normal rate of wages plus DA. Employer’s contribution to ESIC and PF are at equal rate with an employee’s contribution. The month contains 25 working days and one paid holiday. Two workers were employed on Jobs X, Y and Z in the following proportions:

Overtime was done on Job Y.

[C.A. – (Inter) Modified]

Solution

STAGE I: Statement showing wages to be prepared:

Statement showing wages of workers P and Q

Particulars |

Workers | |

|---|---|---|

| P Rs. | Q Rs. | |

Step 1: Basic wages |

400 |

600 |

Step 2: DA (50% of basic) |

200 |

300 |

Step 3: Overtime: |

|

|

Step 4: Gross wages (1 + 2 + 3) |

690 |

900 |

Step 5: Deductions: (i) Employee’s contribution to PF is10% on basic wages |

|

|

Step 6: Net Wages Payable |

642 |

828 |

STAGE II: Computation of labour cost of workers

| Particulars | P Rs. | Q Rs. |

|---|---|---|

Step 1: Gross wages (Excluding overtime) |

600 |

900 |

Step 2: Employee’s contribution to PF is 10% on basic wages |

40 |

60 |

Step 3: Employee’s contribution to ESIC is 2% |

8 |

12 |

Step 4: Labour cost to employer (Add 1+ 2 + 3) |

648 |

972 |

Step 5: Normal working hours pm |

200 |

200 |

Step 6: Labour cost per hour (Step 4 ÷ Step 5) |

Rs. 3.24 |

Rs. 4.86 |

STAGE III: A statement showing allocation of labour cost to jobs

3.5 TYPES OF WORKERS

3.5.1 Casual Workers

These type of workers are employed in the place of workers who are absent. To cope up with the production, some big firms employ such labour on a temporary basis. Usually, casual workers are employed by the personnel department who maintains a panel of casual workers. These workers should follow the same procedure that is adopted for regular workers. But their names are not entered in the pay roll of the firm. They are paid preferably on a daily basis. They are not entitled to any other benefit.

3.5.2 Outworkers

These workers perform work in their own premises. They use their own tools and implements. Payment is based on the work done. No other formalities are observed for them, that is, no system of time-keeping, time-booking and so on. They are not entered in the payroll of the firm. However, materials are issued from stores to such workers, for which a proper maintenance of records by the firms is essential.

3.5.3 Hired Workers

Firms hire workers through contractors. Proper time-keeping records are maintained for them, for those engaged in the production directly. The firms make payment to the contractors, who, in turn, pay wages to the hired workers. To avoid overbilling by the contractors, the contractors’ bills are subject to verification by the firm and spot checking is usually carried out.

3.6 WORK STUDY

Meaning of Work Study

Work study is the study of work, namely human work. It consists of work measurement and method study. It is a technique for the improvement of productivity, where productivity is the relationship between output and input—usually expressed in quantitative terms. The end result of productivity improvement is lower unit cost.

Work study involves a systematic analysis of human work and the work of machines.

Objectives of work study are as follows:

- The most effective use of human (resources) effort.

- The most effective use of plant and equipment.

- The evaluation of human work.

Work study involves:

- Motion study

- Time study

- Method study

3.6.1 Motion Study

To quote Benjamin W. Niebel, “Motion study is the study of body motions used in performing an operation, with the thought of improving the operation, by eliminating unnecessary motions and simplifying necessary motions and then establishing the most favourable motion sequence for maximum efficiency”.

3.6.1.1 Advantages

- It enables the operations to be scientifically planned.

- It facilitates working in a faster and improved manner.

- It leads to an increase in production.

- It results in reduction in costs.

- It helps in improving the arrangement of work place; tools, implements and plans; and proper distribution of work among the employees.

3.6.1.2 Disadvantages

- It is a costly exercise.

- To enforce motions in performing an operation is very difficult as it varies from worker to worker.

- It takes a lot of time to set right the motions as per the desired expectations.

- It creates distrust and frustration among workers.

- Each worker’s skill is curtailed under this study.

- Workers are deprived of freedom.

3.6.2 Time Study

According to Benjamin W. Niebel, “Time study involves the technique of establishing an allowed time standard to perform a given task, based upon measurement of the work content of the prescribed method, with due allowance for fatigue and for personal and unavoidable delay”.

Time study determines

- the standard time

- needed by an average work

- working under normal conditions

- to carry out a given task.

3.6.2.1 Advantages

- It facilitates the calculation of the cost of production.

- It helps to implement an incentive wage-payment scheme.

- It facilitates budgeting, manning and production scheduling.

- Quotas can be fixed for hourly-rated workers.

- Standard labour cost can be easily established.

3.6.2.2 Disadvantages

- It cannot be used for non-repetitive jobs.

- Quality is sacrificed at the cost of quantity.

- Splitting-up of a task into different elements is a complex process.

- Subjective elements dominate the scheme.

- Its mathematical accuracy is not to be relied upon.

The following are the important steps involved in time and motion study:

Step 1 → Split the task into its elements.

Step 2 → Consult the basic time which has been previously set in respect of each element.

Step 3 → Conduct time and motion study where element-wise basic time does not exist.

Step 4 → A relaxation allowance is made at a certain percentage and added to the basic times, either individually or in totality. (This gives the work content of a job.)

Step 5 → Collect the technical data and values of human work, and then analyse and calculate the standard time for the task.

3.6.3 Method Study

Method study is the systematic recording, analysing and examining the methods and movements involved in the performance of a task. Its aim is to improve efficiency in performing the task by getting rid of the unnecessary work, avoidable delays and other forms of waste.

Steps involved in method study are as follows:

Step 1 → Definition of area of study

Step 2 → Collection of information

Step 3 → Alternative methods—Consideration

Step 4 → Choosing best alternatives—Decision

Step 5 → Getting feedback and monitoring the progress

3.7 JOB EVALUATION AND MERIT RATING

An organization requires people of different skills, grades, educational qualifications and experience to work in various levels. Due to these factors, the remuneration also has to vary from one level to another. Job evaluation is one of the solutions to this problem. But job analysis has to be carried out before job evaluation. Job analysis involves a proper appraisal of all jobs in an organization. Job analysis has been defined as,

“Job analysis is the process of determining, by observations and study, and reporting pertinent information relating to the nature of a specific job. It is the determination of the tasks which comprise the job and the skills, knowledge, abilities and responsibilities required of the workers for successful performance and which differentiates the job from all others”.

Obtaining detailed information from job analysis, job evaluation is carried out.

3.7.1 Job Evaluation

Job evaluation is a technique that equitably measures the relative worth of a job in a firm. It ranks jobs in a formal manner, measures the worth of a job and determines the remuneration that is suitable for each job. Using this technique, a wage structure is framed. This technique is used for determining the relative worth of a job.

One of the requirements of job evaluation is that a written description of the work operations in each job has to be done in a detailed manner.

3.7.2 Methods of Job Evaluation

3.7.2.1 Factor-Comparison Method

There are a number of factors involved in each job. Some important factors are: (1) Skill; (2) Working conditions; (3) Responsibility; (4) Mental requirements; and (5) Physical requirements. Using this method, selection of few key jobs is done and a rating scale is made on the basis of evaluating and ranking of these jobs in accordance with these factors.

3.7.2.2 Ranking Method

Under this method, job descriptions and specifications are recorded. Different jobs are compared after considering the educational requirements, skills, and so on. Jobs are ranked by comparing the said job with the same components of another job and placed in the ranked scale of jobs. It results in an arrangement of jobs in an hierarchical manner.

3.7.2.3 Paint-Rating Method

Splitting up of a job into various component factors like experience, physical requirements, skill and so on is the method. Points are allotted based on the relative weightage of these factors. Based on the points scored, the jobs are ranked. Finally, they are placed in a number of pre-determined grades. The relative worth of various jobs is determined by the comparison of point values. These point values are used for the fixation of scales of pay for each grade.

3.7.2.4 Classification Method (or) Grading Method

This is an improvement over the ranking method. Under this method, each grade has to be properly described. Based on the skill, educational qualifications, experience, type of work, responsibilities and so on, grades are fixed in advance. After establishing grades, a study is made for each job.

3.7.2.5 Merit Rating

This is a technique used for determining each worker’s fair wages on the basis of his ability and performance. An employee is evaluated individually using factors such as skill, intelligence, discipline, integrity, responsibilities, personality, sense of judgement and so on.

Merit rating may be defined “as the systematic process of performance of an employee on the job in terms of job requirements”. The main object of merit rating is to rate the performance of an employee, for promotion, award of merit and so on.

This method of evaluation is carried on a systematic basis. The performance of an individual is assessed on the job on the basis of requirements of each job.

3.7.2.6 Differences Between Job Evaluation and Merit Rating

| Basis of Distinction | Job Evaluation | Merit Rating |

|---|---|---|

1. Objective |

To set up a rational wage and salary structure. |

To provide a scientific basis for determining fair wages for each worker. |

2. Rating |

It rates the jobs. |

It rates the employees. |

3. Assessment |

It is the assessment of the relative worth of jobs. |

It is the assessment of the relative worth of a man behind the jobs. |

4. Underlying purpose |

It simplifies the wage administration by evolving uniformity in the wages. |

It determines the fair rate of pay to the workers based on their ability & performance |

3.8 LABOUR REMUNERATION

3.8.1 Principles of Labour Remuneration

Remuneration has been defined as the reward for labour and services rendered. All business organizations should have a proper method of remuneration for their employees. The management’s aim should be to achieve high productivity. So, it has to devise a method of remuneration in such a way that it promotes goodwill and satisfaction among the labourers and at the same time, increasing the efficiency, economy, and productivity of firms too.

The principles underlying the selection of a remuneration method are:

- The method has to ensure that fair wages are paid for a fair day’s work.

- It should be simple to understand and easy to practice.

- The workers should accept the method.

- It should be comparable with the wages adopted in other similar industries, in a particular geographical area.

- It should guarantee a minimum standard wage.

- The wages should have a direct relationship with their output.

- The skill and effort of the worker have to be duly recognized while devising a wage system.

- It should minimize labour turnover.

- It should be flexible to adapt itself to changes in skills, job content, method and technology.

- The quality of product is to be considered.

- The method should discourage absenteeism among workers.

- It should motivate the workers.

- The method should have inbuilt incentives.

- The administration of the method should be capable of being carried out with ease and economy.

- Last but not the least, a mutual trust and goodwill should be established between the employer and the employees.

3.8.2 Methods of Remuneration

3.8.2.1 Straight Piece-Rate Method

This method rewards employees based on their output. This method is based on the principle “payment by results”. This is a method of paying wages which depends on the output or units produced by the worker. A fixed rate of wage is paid for each unit produced or number of operations completed or the job completed. Time taken to complete the work is immaterial, under this method.

The wage is calculated as under:

Wage = Number of units produced × Rate per unit.

There is generally a guaranteed hourly rates for workers who will not be able to attain the standard. It is necessary to pay minimum “day wages” in compliance with the statutory provisions of the Minimum Wages Act, 1948. This method of remuneration is suitable in the following cases:

- Where the production is of a repetitive nature.

- Where the quantity of output does not require any specialized skill.

- Where there is flow of work without any interruption.

- Where the price rate can be fixed easily.

ADVANTAGES:

- It promotes efficiency among workers.

- It reduces costs.

- Idle time is controlled.

- It leads to higher production.

- A fall in labour cost until the standard is reached.

- It reduces the need and the cost of supervision.

- As the cost per unit is known in advance, quotations can be made on a competitive basis.

DISADVANTAGES:

- This method may result in higher scrap, spoilage and waste because workers are interested in producing more units.

- Stricter quality control is needed to maintain the required quality of the product.

- Machineries may get the stage of obsolescence soon because of workers’ carelessness in handling them to maximize the output.

- Workforce will suffer in case of power failure, breakdown of machine, and so on.

- Determination of piece rate is not easy in practice.

3.8.2.2 Flat Time-Rate Method

This method is used on the basis of the attendance of workers. A fixed rate of wage is paid hourly or daily or weekly on the basis of time spent on the shop floor (in production).

Under this method, the wage is calculated as follows:

Wage = Hourly rate × No. of hours (spent)

(or)

Daily wage rate × No. of days.

This method is suitable in the following cases:

- Where individual skills of workers are involved.

- Where quality of work is the main criterion.

- Where work is non-repetitive in nature.

- Where the output of a worker cannot be measured and not under his control.

- Where the work can be closely monitored.

ADVANTAGES:

- As the workers are not in a hurry to produce more number of units, scrap and spoilage, defectives may be minimized to a great extent.

- Output confirms to the firm’s specified standards of quality.

- Quality inspection costs are minimized.

- Interests of workers are safeguarded in case of breakdown of machinery, power cut, and so on.

- As all workers are paid alike, labour unions welcome this method.

DISADVANTAGES:

- It is not easy to set standards for labour.

- Labour cost may increase.

- There will be a decrease in the productivity.

- This cannot be used for a quotation purpose.

- It induces more idle time.

- Finally, it may result in inefficiency.

3.8.2.3 Incentive Wage Plans

The motivation, the productivity and the satisfaction of workers are dependent upon the reward system. The incentive plans provide the needed reward to the workers directly in proportion to the work done. This reward induces him to earn more by producing more. Higher production reduces the unit cost of production. Incentive wage plans (incentive schemes) may be classified as follows:

- Direct financial plans.

- Indirect financial plans.

- Other than financial plans.

Pre-Requisites of a Sound Incentive Scheme: A good incentive scheme should fulfil the following requirements:

- Easy to understand: The scheme should be understood by the workers easily. They themselves should calculate their earnings.

- Motivation: The scheme should be so devised that it can motivate their workers to raise production.

- Savings in production cost: The plan should result in savings in the cost of production.

- Less supervision: It should be made in such a way that it can result in minimum supervision.

- Reward for good production: The scheme should discourage spoilage and defective work and reward good production.

- Comply with statutory guidelines: It should guarantee the minimum days’ wages as per the Minimum Wages Act.

- Time lag: The time lag between the effort and the reward should be kept a minimum.

- Inexpensive: The scheme should be administered with minimum expense.

- Labour turnover: The scheme should be so attractive that workers remain in the organization for a longer period.

- Equal opportunity: All workers should be provided equal opportunity to earn more. There should be no room for any nested interest

- Uniformity: The scheme should be devised in such a way that there should be uniformity of reward for the same amount of effort.

- Complementary to other control systems: The plan should facilitate the other control systems such as budgetary control and standard cost systems.

- Continuity and permanency: This should be based on a permanent basis and continued for a long period.

- Flexibility: It should be so flexible that it can accommodate any changes in future.

- Coverage: Indirect workers also should be covered under this scheme.

ADVANTAGES:

- Reduction in cost per unit: Increase in productivity will result in reduction in cost per unit.

- Increase in productivity: Because of incentive schemes, the work force may try to boost up production.

- Estimation of labour cost: Labour cost can be estimated in advance which facilitates the control of labour cost.

- Utilization of resources: There will be a maximum utilization of resources.

- Supervision: Less supervision is required.

DISADVANTAGES:

- Clerical work: More calculations are needed and clerks would be overburdened with such work.

- Deterioration of quality: By aiming an increased output, quality may not be maintained.

- Discontent among workers: As the rates are not uniform, it creates unrest and discontent among the workforce.

- Disparity among the workers: Even semi-skilled workers may earn more than the skilled labourers.

- Rate cutting: There may be apprehensions regarding rate cutting.

3.8.2.4 Differential Piece Rate

Under differential piece-rate method, more than one piece rate is determined. This method rewards workers on the basis of the output. Standards are set for each job. There are two piece rates. One is in respect of an average worker and another for an efficient worker. Efficient and inefficient workers are distinguished. There are many differential price-rate methods in vogue. Some are discussed as follows:

3.8.3 Taylor’s Differential Piece-Rate Method

F.W. Taylor invented this scheme. Under this method, the standard output is determined on the basis of time and motion studies. No minimum wage is guaranteed. There is a wide gap between the higher piece rate and lower piece rate. Generous reward is given to workers who produce in excess of standard. Whereas, the workers who were unable to attain the standard set are penalized.

Time factor may also be taken into account. The efficiency of the worker is determined either (1) by comparing the standard time and the actually taken time or (2) by comparing the actual output and the standard output.

ADVANTAGE: Workers are motivated to increase production.

DISADVANTAGE: Calculations are complicated.

How this method operates?

- The lower rate is based on 83% of the day-wage rate.

- The higher rate is based on 175% of the day rate + an incentive of the 50% of the day rate.

Wages are determined by applying the above criteria.

Illustration 3.7

The wage rate is Rs. 0.80 per unit. You are required to determine: (i) the low piece rate and (ii) the high piece rate by using Taylor’s differential piece-rate method.

Solution

- The low piece rate is based on 83% of the day wage rate.

∴ Low piece rate = 83% × 0.80 (day wage rate: given)

= Re. 0.664 per unit.

- High piece rate = 175% of day rate + 50% of day rate

= 175% × 0.80 + 50% × 0.80

= Rs. 1.40 + 0.40

= Rs. 1.80 per unit

3.8.4 Merrick’s Differential Rate Scheme (or) Multiple Piece-Rate System

This is a modification of Taylor’s scheme. Three gradual rates are determined instead of two levels in Taylor’s method. This method does not guarantee time rate. Each worker is paid according to his efficiency.

Efficiency level Piece rate

Up to 83% → Normal rate

83% to 100% → 110% of normal rate

Above 100% → 120% of normal rate

The worker who has performed below standard will not be penalized.

Illustration 3.8

Three workers A, B and C work in a factory. The following particulars apply to them:

Normal rate per hour |

= Re. 0.90. |

Piece rate |

= Re. 0.60 per unit. |

Standard |

= 4 units per hour. |

In a 40-hour week, the production of workers is as follows:

A: 100 units

B: 160 units

C: 240 units

You are required to calculate earning of workers as follows:

- Taylor’s differential piece-rate system

- Merrick’s differential piece-rate system.

Solution

First, efficiency in terms of percentage is calculated for each worker as follows:

STAGE I: This may be computed in the following method.

Standard time (hours) is taken as a base

Standard: 4 units per hour

For Worker A: 100 units produced.

Time taken to produce ![]() hours (for 100 units).

hours (for 100 units).

For Worker ![]() hours (to produce 160 units).

hours (to produce 160 units).

For Worker ![]() hours (to produce 200 units).

hours (to produce 200 units).

Normal working hours = 40 hours/week (given).

A’s efficiency ![]()

B’s efficiency ![]() .

.

C’s efficiency ![]() .

.

On the basis of efficiency level, piece rate is to be determined for these two methods.

STAGE II:

I: Taylor’s System:

Under this system,

Step (i) Low piece rate = 83% of 0.60 = 0.50 (approx.)

Step (ii) High piece rate = 175% of 0.60 = 1.05.

Step (iii) For Worker A:

Output is 100 units – Efficiency is 62.5% – Hence, wages are to be calculated under low piece rate, that is, 0.50/unit.

∴ Wages = 100 units × 0.50 = Rs. 50.

Step (iv) For Worker B:

Output is 160 units – Efficiency is 100% – Hence, wages @ Rs. 1.05 is to be calculated.

∴ Wages = 160 units × Re. 1.05 = Rs. 168.

Step (v) For Worker C:

Output is 240 units - Efficiency is 150% - Hence, wages @ Rs. 1.05/unit is to be calculated.

∴ Wages = 240 units × Rs. 1.05 = Rs. 252.

STAGE II:

Merrick System:

Under this system, wages are calculated as follows:

Step 1 |

Efficiency level |

Piece rate |

|

Up to 83% |

Normal rate: 0.60/unit |

|

83% to 100% |

110% of normal rate: 110% of 0.60 = 0.66. |

|

Above 100% |

120% of normal rate: 120% of 0.60 = 0.72. |

Step 2 Wages for Worker A (efficiency 62.5%): 100 units × Normal rate = 100 × 0.60 = Rs. 60.

Step 3 Wages for Worker B (efficiency 100%): 160 units × 110% of Normal rate = 160 × 0.66 = Rs. 105.60.

Step 4 Wages for Worker C (efficiency 150%): 240 units × 120% of Normal rate = 240 × 0.72 = Rs. 172.80.

3.8.5 Gantt’s Task and Bonus Plan

Under this method, time wages are guaranteed to every worker. Standards are set. Bonus is allowed up to 20% at 100% efficiency. (Standard Time → 100% efficiency). If a worker takes the standard time to perform the task, he is given wages for standard time and bonus of 20% on wages earned. If the worker completes the task in less than the standard time, he is given wages for the actual output and a bonus of 20% of the wages for standard time.

Illustration 3.9

You are required to compute the earnings of workers and labour cost per unit under Gantt Task Bonus Wage System from the following data:

Standard output – 20 units per hour

No. of hours in day – 8

Time rate – Rs. 10 per hour

Output of workers:

X – 120 units

Y – 180 units

Z – 220 units

Standard output per day – 160 units

Solution

First wage rate per unit (piece) is to be calculated.

Standard output = 20 units/hour

Time rate = Rs. 10/hour

*1∴ Wage rate per unit = ![]()

As per Gantt’s Task Bonus Plan,

*2Higher wage rate |

= |

(Lower) Standard rate + 20% Bonus |

|

= |

Re. 0.50 + 20% of 0.50 = Re. 0.60. |

Higher wage rate is allowed if the worker’s output exceeds the standard output, that is, 160 units.

Answers are shown in the following table:

Statement showing wages earned by the workers and the unit cost

Important Note

- Till the productivity reaches the standard level, the labour cost per unit would be less.

- Thereafter, the labour cost per unit will remain constant. (Now, refer the table and compare the results there of.)

3.8.6 Baum’s Differential Scheme (or) Milwakee Scheme

This method is a combination of Taylor’s differential piece-rate system and Halsey plan, where as time rate is guaranteed under Halsey plan alone. This system provides incentives at different levels of efficiency.

3.9 PREMIUM BONUS PLANS

Generally, under a piece-rate system, it is the workers who gain or lose. But under the time-rate system, the employer will be benefited by the gains of efficient workers and the losses of inefficient workers.

Under the Premium Bonus Plans, the gains will be shared by the employer and the employees in agreed proportions. In addition to the minimum guaranteed wages, the efficient workers are rewarded bonus which is related to the time saved. Some of the important premium bonus plans are discussed as follows:

3.9.1 Emerson’s Efficiency System (or) Empiric System

Main features of the system are as follows:

- Minimum day wages are guaranteed.

- Efficiency is rewarded by way of bonus

- A standard time is set for each job or operation. Or sometimes, the volume of output is taken as the standard.

- Standard is set on the time and motion study.

- Level of efficiency and piece rate is determined as follows:

Levels of efficiency

Piece rate

Up to

→

Guaranteed time rateFrom 66⅔% to 90%

→

Time rate + 10% as Bonus

From 90% to 100%

→

Time rate + 20% as Bonus

Above 100%

→

Time rate + 20% as Bonus + Additional bonus of 1% for every increase of 1% beyond 100% efficiency.

- Efficiency for this purpose is to be calculated as follows:

- On Time basis:

- On Production basis:

ADVANTAGES:

- Under this plan, slow workers are encouraged and an account of this slow work is avoided.

- ‘Payment by results’ principle dominates the scheme.

- Work is done at a uniform rate.

DISADVANTAGES: Incentive allowed beyond the standard is not encouraging the efficient workers.

Illustration 3.10

From the following information, you are required to calculate the bonus and earnings under Emerson’s efficiency bonus plan:

Standard output in 10 hours: 50 units.

Actual output in 10 hours: 40 units.

Time rate: Re. 0.80 per hour.

If the actual output is 60 units, what will be the amount of bonus and earnings?

Solution

Step 1 → The formula to compute earnings under Emerson’s plan = Earnings = T×R + P (T× R).

Step 2 → Bonus under this scheme varies as follows:

- Up to

efficiency – Time wages only.

efficiency – Time wages only. - From

to 100% – A bonus increasing from 0.01% to 20% above the basic wages on 100% 3 efficiency.

to 100% – A bonus increasing from 0.01% to 20% above the basic wages on 100% 3 efficiency. - Above 100% – A bonus of 20% above basic wages + 1% for each 1% increase in efficiency.

Step 3 → Efficiency is to be computed.

|

|

|

|

Illustration 3.11

ABC Ltd is engaged in the manufacture of a particular product. The guaranteed daily wage rate is Rs. 12. The standard output fixed for the month is 600 units which represents 100% efficiency. Workers whose efficiency is below ![]() will not be paid any bonus. Bonus is payable in a graded scale after this level of efficiency as follows:

will not be paid any bonus. Bonus is payable in a graded scale after this level of efficiency as follows:

Efficiency |

Bonus |

90% |

10% |

100% |

20% |

There are two workers X and Y who have worked for 25 days in a month, and their output is 360 units and 600 units, respectively. You are required to compute the earnings of workers under Emerson’s plan.

Solution

| Worker X | Worker Y | |

|---|---|---|

|

|

|

Step 2 → Earnings |

|

Bonus has to be computed |

|

No Bonus 25 days × Rs. 12 =Rs. 300 |

|

|

|

= 300+60=360 |

|

|

|

Result: Labour cost per unit falls from Re. 0.833 to Re 0.60 per unit, as the productivity increases from 360 units to 600 units.

3.9.2 Bedauxe Scheme or Points Scheme

This system requires a very accurate time study and work study. Time wages are guaranteed. Under this scheme, each minute of standard time is called the Bedauxe Point or “B”. Each operation to be performed can be expressed as being so many B’s and the payment is made on the basis of number of B’s. Standing in the credit of the workers, to put in other words, ‘B’ means a standard work performed in a standard minute. One ‘B’ unit represents the amount of work—an average worker will do under normal level. Bonus is rewarded at 75% of B’s saved.

If the bonus is given to the extent of the value of the entire time saved, then this plan is known as 100% Bedauxe plan. If nothing is mentioned, it is 75% known as 75% Bedauxe plan.

ADVANTAGES:

- A healthy competition motivates higher productivity.

- It serves as a tool of managerial control.

DISADVANTAGES:

- Material costs cannot be controlled.

- Increase in cost due to additional clerical work.

Illustration 3.12

The following are the particulars with respect to a job. You are required to calculate bonus and earnings under Bedaux Point Premium System.

Allowed time for the job: 720 B’s

Time taken: 600 B’s

Rate – Re 0.90 per hour.

Solution

- Formula:

T: Time Taken:

=

10hrR: Rate

=

0.90/hr

P = 720 − 600

=

120 B−s.

Substituting the values in the formula we get,

- When 100% scheme is operated:

Earnings

=

=10 × 0.90 +

× 0.90

× 0.90=

Rs. 9 + 1.80

=

Rs. 10.80.

3.9.3 Barth Scheme

Under this scheme, the day wages are not guaranteed. Wages are calculated by the formula:

ADVANTAGE:

This scheme is suitable for less-efficient people.

DISADVANTAGE:

Efficiency is not encouraged.

Illustration 3.13

Hourly rate = Rs. 3.

Time allowed for a job = 10 hours.

Actual time taken by a worker:

A – 8 hours

B – 10 hours

C – 12 hours

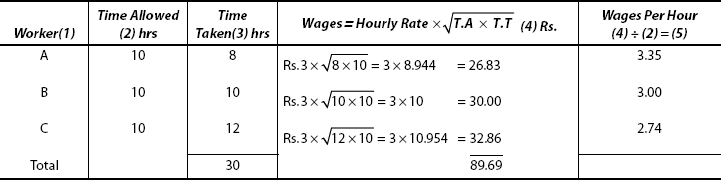

You are required to calculate the wages of workers under Barth Premium Scheme and ascertain the labour cost per hour.

Solution

Substituting the values, we get the earnings for different workers, which is tabulated as follows:

Labour cost per hour is calculated as follows:

Total wages paid |

= Rs. 89.69. |

Total number of hours worked |

= 30. |

|

|

|

= Rs.2.989. |

3.9.4 Halsey Scheme

Main features are as follows:

- Standard time is fixed for each job.

- Time rate is guaranteed and, hence, the worker will receive the guaranteed wages and it is immaterial whether he completes the work within the time allowed or not.

- In case, if a job is completed within the time allowed, such worker will be paid a bonus of 50% of the time saved.

Earnings = Time taken × Hourly rate +

of Time saved × Hourly rate

of Time saved × Hourly rate

ADVANTAGES:

- Since day wages are guaranteed, the interests of workers are safeguarded.

- It is easy to operate.

DISADVANTAGES:

- 50% of bonus is shared by the employer.

- Quantum of incentive offered is insufficient.

Illustration 3.14

Normal hour rate |

: Rs. 5. |

Time allowed for a job |

: 8 hours. |

Time taken |

: 6 hours. |

You are required to compute the total earnings under Halsey Scheme.

Solution

Formula:

|

|

Time taken × Hourly rate + |

|

|

(6 × Rs. 5) + |

|

|

Rs. 30 + |

|

= |

Rs. 30 + 5 |

|

= |

Rs. 35 |

3.9.5 Halsey–Weir Scheme

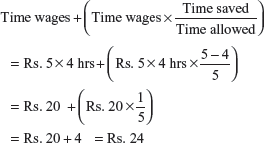

Under this scheme, the bonus will be ![]() of the standard time saved, whereas it is 50% under Halsey plan. Except this, all the other aspects of these schemes Halsey and Halsey–Wair are similar to each other.

of the standard time saved, whereas it is 50% under Halsey plan. Except this, all the other aspects of these schemes Halsey and Halsey–Wair are similar to each other.

Total wages = Time taken × Hourly rate + ![]() (Time saved) × Hourly rate.

(Time saved) × Hourly rate.

Illustration 3.15

Based on the same figures as in the previous illustration, calculate wages under the Halsey-Weir scheme.

Solution

Total wages = Time taken × Hourly rate + ![]() (Time saved) × Hourly rate

(Time saved) × Hourly rate

3.9.6 Rowan Scheme

David Rowan introduced this scheme in 1901. Bonus is paid on the basis of time saved. Unlike a fixed percentage as in the schemes of Halsey and Halsey–Weir, proportionate basis is adopted under this scheme.

Formula:

In this method, the bonus may be calculated in two ways:

- By adding bonus to the normal time wages.

- By adjusting the hourly rate.

Irrespective of the way to be adopted, the result will be the same under both the following approaches:

Approach 1 : ![]()

Approach 2: ![]()

Illustration 3.16

Time Taken: 4 hours.

Time allowed: 5 hours.

Rate per hour: Rs. 5.

You are required to calculate total earnings under Rowan scheme.

Solution

Approach 1:

Formula:

Approach 2:

Illustration 3.17

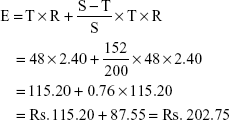

In a factory, guaranteed wages at the rate of Rs. 2.40 per hour are paid in a 48-hour week. By time and motion study, it is estimated that to manufacture one unit of a particular product 40 minutes are taken. The time allowed is increased by 25%. During one week, a worker produced 240 units of a product. Calculate his wages under each of the following methods:

- Time rate.

- Piece rate with guaranteed weekly wage.

- Halsey Premium Bonus.

- Rowan Premium Bonus.

Solution

- Time rate:

Earnings

=

Total hours × Rate per hour

=

48 × Rs. 2.40

=

Rs. 115.20.

- Piece rate:

1. Earnings = No. of units produced × Rate per unit

Rate per unit is to be calculated as follows:

Step (i) Time taken = 40 minutes.

Step (ii) Incentive allowance at ![]()

Step (iii) Standard time to produce one unit, Add (i) + (ii) = 50 minutes.

Step (iv) Rate per minute ![]()

Step (v) Rate per unit = 50 × 0.04 = Rs. 2.

(Step (iii) and Step (iv))

Step (vi) Now substitute the values in the formula (i)

Earnings = 240 units × Rs. 2 = Rs. 480

3.9.6.1 Halsey Premium Bonus Plan

Formula: ![]()

where |

T |

= |

Total hours in a week; R = Rate per hour. |

|

S |

= |

Standard Time; T = Actual time taken. |

Standard time is calculated as follows:

Time taken to produce one unit = 50 minutes (Ref (b) – Step (iii))

Time taken to produce 240 units = 240 × 50 = 12,000 minutes

Or

Now, substituting the values in the formula, we get,

(iii) Rowan Premium Plan:

3.9.6.2 Accelerating Premium Bonus Scheme

Under this method, workers are rewarded on the basis of their output. It is based on the principle: “Payment by Results Scheme”. The bonus offered in this scheme rises at a rapid rate. This scheme offers a high incentive. This scheme is suitable for supervisors.

There is no standard formula for this scheme. It varies from one industry to another. To understand the scheme, the graph of the function y = 0.8x2 may be used, where y = wages and ![]() , as follows:

, as follows:

3.10 GROUP-BONUS PLANS OR SCHEMES

This method of remuneration is used where the production system requires collective efforts, preferably by a group of workers. As such, individual efforts cannot be measured. Under this scheme, payment is made by results to all the workers in the group. In the initial stages, the production of group of employees is measured and the total bonus is calculated. After a certain period, the bonus is distributed equally or on the basis of an agreed proportion among the workers belonging to the group. The proportions are based on time rates or some previously agreed ratios.

ADVANTAGES:

- This scheme fosters team spirit among workers.

- Self-discipline is developed.

- Each and every worker is totally involved in the output and due to this, the production is increased.

- Cost of production decreases.

- Supervision may be reduced to a minimum level.

- Spoiled and defective goods can be brought down to a greater extent.

DISADVANTAGES:

- The quantum of incentive is very meagre.

- Efficient workers are not distinguished from inefficient workers. They are treated at par.

- Time lag between effort and reward is too much.

Some of the group-incentive plans are as follows:

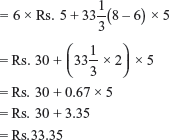

3.10.1 Priestman’s Production Bonus Plan

Standard output is established to be attained for each department. This is stated in points or units. When the workers produce in excess of the standard, they are paid bonus in proportion with the increase. For instance, if the standard output is 50 units and the actual output is 70 units, the workers would receive a bonus equal to 40% of their basic wages (70 units ÷50 units × 100 = 140%). This is over and above their basic wages.

3.10.2 Rucker’s Plan

This is also known as “cost-saving–sharing plan”. In this method, the bonus to be paid to the workers is linked to the value added. Value added is the excess of sales value over the cost of purchase of materials and services. It includes the profit. Bonus will be a fixed proportion of the value added, which is calculated on a monthly basis.

Only two-thirds of the bonus earned is distributed. The remaining one-third is transferred to the reserve fund. When the actual performance falls below the standard, the amount kept in reserve fund is utilized. The standards are set on the basis of past trends.

3.10.3 Scalon Plan

This is similar to Rucker’s plan. The main difference is that it uses the ratio of direct labour cost of the sales value of production to compute the bonus.

3.10.4 Towne’s Gain-Sharing Plan

Under this method, bonus depends on the reduction in labour cost when compared with the standard set. Bonus is computed as follows: Bonus is based on the 50% of direct labour costs saved. For example, if time allowed is 8 hours, time taken is 5 hours and base rate is Rs. 30 per hour, then the bonus will be = 50% × (8–5hrs) × Rs. 30 = Rs. 45.

3.10.5 Budgeted Expenses Bonus

Under this scheme, the bonus is linked with the savings in the expenses. The actual expenses are compared in total with the budgeted expenses in order to ascertain the savings in the expenses. By using a pre-determined percentage, the bonus is computed by multiplying the pre-determined percentage with the savings achieved actually.

3.11 INCENTIVE PLANS FOR INDIRECT WORKERS

Indirect workers should not be neglected for providing incentives. Their role is also equally important in enhancing the productivity. To attain the maximum efficiency, enlisting the cooperation of indirect workers is essential. But devising an incentive scheme for indirect workers is not easy. The main reason is that the output of indirect workers cannot be quantified accurately. Their contribution to attain a higher level of performance cannot be underestimated.

3.11.1 Principles Governing the Incentive Plan for Indirect Workers are

- Establish standards for repetitive activities: Repetitive activities can be measured to a certain extent. Such measurable repetitive activities are loading, unloading, packing of standard products, bill processing and so on. Standards may be set in respect of such activities. Incentives can be rewarded when the actual performance is higher than the standard.

- Forming a part of the collective plan: Indirect workers should be included in the collective plan with the direct workers. Incentive payment should be made to them proportionate to the total incentive earnings of the direct workers.

- Provision for linking incentive with the direct workers: In certain circumstances, the efficiency of direct workers is dependant upon the quality of work rendered by the indirect workers. The incentive paid to the indirect workers must be linked to the incentive earned by the direct group of workers.

- Reward and efforts: The scheme should be devised in such a way that rewards should be related to the efforts of the indirect workers.

- Regular intervals: The bonus is to be payable at regular intervals without much time lag between effort and reward.

Besides these basic principles, incentive plan should be devised for certain category of indirect workers. They are:

- Material-handling staff: Important elements involved in material handling are loading, unloading, movement from stores to production department and the like. In such cases, an overall group-incentive scheme may be envisaged.

- Office staff: Office staff also should get motivated by way of incentive schemes. Incentive paid to direct workers may serve as a basis for computing bonus for the office staff.

- Inspection staff: Same basis may be adopted as in the case of office staff for rewarding the inspection staff

- Maintenance staff: Standards can be set with respect to routine maintenance staff. Incentives should be linked to such standards. If it is not possible, a group-bonus plan may be envisaged.

3.11.2 Indirect Monetary Incentive Schemes

Besides direct incentives, workers are given some indirect incentives to attain the maximum productivity. Indirect incentives are of two categories: (i) Monetary incentives and (ii) Non-monetary incentives.

- Monetary incentives: Incentives that are given in terms of money are known as “monetary incentives”. For example, monetary incentives include profit sharing, co-partnership and so on.

- Non-monetary incentives: Incentives which are given in kind (other than money) are known as “non-monetary incentives”. They include canteen facilities, medical facilities, leave-travel concession, free uniforms and the like.

3.11.3 Monetary (Indirect) Schemes

3.11.3.1 Profit Sharing

Profit sharing has been defined as, “an agreement freely entered into, by which an employee receives a share, fixed in advance, of the profits”. Or it may be said, “where an employer rewards its employees with special current or deferred sums on the basis of overall prosperity of the business – it is known as profit sharing”. Such amount would be paid over and above his regular pay. The profit percentage is predetermined. Profit-sharing scheme should comply with the statutory provisions envisaged in the payment of Bonus Act, 1935. Profit-sharing plans may be classified under the following categories:

- Cash plans: Employees are rewarded with a certain amount of cash periodically. The quantum of amount depends on the overall profit of the business. Such amount is an extra reward to the workers in recognition of their high performance.

- Deferred credit plans: Under this scheme, the firm invests a part of the profit on a periodic basis. On the date of retirement or resignation of an employee, he will be paid that amount. As the time lag is wide between the effort and reward, the workforce will not accept this plan wholeheartedly.

- Combined plan: This plan is a combination of the above two methods. A certain percentage of the share of the profit is invested and the remaining part is paid in cash.

ADVANTAGES:

- Employer–employee relationship: This method is based on the assumption that profit is shared by all the employees, irrespective of their efficiency. This results in a better employer–employee relationship.

- Industrial peace: Workers and the management in unison try to maximize the productivity. Profit-sharing motive causes less friction between the two. Hence, there may not be any room for industrial unrest.

- Low labour turnover: As every worker gets his share of profit in addition to wages, periodically, labour-turnover ratio would be low.

- Enhancement of labour morale: The workforce may concentrate mainly in productivity which in turn enhances their morale.

- Team spirit: Better cooperation and high team spirit will prevail.

- Effort and reward: There exists a better relativity between effort and reward, as every worker is motivated in such a way to maximize his efficiency, which in turn is rewarded by a share in profits.

- Sense of belonging: Psychologically, every worker feels that he is a part and parcel of the firm. Each one shows his maximum talent, handles materials and machinery carefully, exercises his role to control the activities and the like factors to develop a sense of belonging to the firm.

- Efficient work force: This scheme attracts the efficient workers. Qualified and skilled workers are not only encouraged to join the firm but they are retained for a relatively longer period.

DISADVANTAGES:

- Basis of distribution of profit: Sometimes, the management may not adopt a suitable basis for apportionment of profit among the workers, which may result in distrust with the management.

- Role of labour unions: On account of this scheme, each labourer is concentrated on his own work. This attitude alienates the workers from unions. Hence, labour unions may oppose vehemently.

- Uncertainty: As profits depend on many factors, which are in fact not within the control of the workers, profit is not an assured factor. In the absence of profit, effort of workers may not be rewarded suitably.

- Non-recognition of efficient workers: This scheme fails to distinguish between the efficient and inefficient workers. This will have an impact on the efficient workers.

- Fluctuations in bonus: This scheme cannot pre-determine the quantum of amount. Profits may fluctuate and sometimes loss will also arise. In such situations, the workforce may get dejected and indulge in unfair activities.

- Time lag between effort and reward: Workers have to wait till the end of the year and this wide gap between effort and reward may dampen their enthusiasm.

3.12 CO-PARTNENSHIP

Instead of cash, labour will be given a share of profit in the form of shares. This type of profit sharing is known as “co-partnership”. Under this scheme, the workers of the firm will get a part of the capital and profits accruing. But these shares may or may not carry the voting rights. In case they do not have such rights, employees may feel inscure because of the restrictions imposed on them.

ADVANTAGES:

- Owners of the firm: Employees have a share in the capital. They attain the status of owners of the firm.

- Low labour turnover: As workers are made as co-partners in the company, labour-turnover ratio will be low.

- Cooperation and team spirit: There will be greater cooperation between workers and a good team spirit will be developed among them.

DISADVANTAGES:

- Time lag between effort and reward: The underlying factor behind the incentive itself is negated as the date of the actual payment of the incentive is far away.

- No distinction between efficient and inefficient workers: This scheme does not distinguish between efficient and inefficient workers.

- Distrust: As employees are not in a position to verify such allotment of shares, distrust and ill-will will develop between the employer and employee.

3.12.1 Other Non-Monetary Incentive Schemes

This type of incentive is given to all employees. These are provided entirely at the cost of the management (free) or the employees may be asked to contribute towards such incentives at a very low margin. In fact, some of the incentives are rewarded to comply with the statutory regulations. Strictly speaking, these incentives are not provided for any kind of super performance of the workers. Some of such incentives are: (i) PF contribution; (ii) Gratuity; (iii) Pension; (iv) Protective measures to workers; (v) Medical facilities; (vi) Subsidized services; (vii) Leave-travel concessions; (viii) all welfare measures; (ix) housing facilities; and so on.

ADVANTAGES:

- As these incentives are labour oriented (management is not benefited), workers welcome such incentives

- Employees feel secured on account of incentives like PF, Pension and Gratuity.

- Labour-turnover ratio gets reduced.

- A good reputation of the company emerges.

- Workers feel contended by such incentive schemes.

3.13 LABOUR TURNOVER

Employees may join and leave an organization for a change in job for any of the following reasons:

- For personal betterment.

- When new opportunities are available.

- Due to present firm’s decision.

- For any other compulsion.

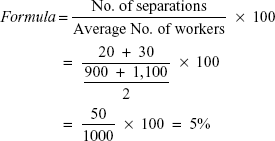

In such cases, the leavers have to be replaced by new employees. Due to this, there is a change in the composition of labour force. Labour turnover may be defined as the rate of change in the labour force in an organization during the specified period. The change in the composition of labour force may also arise on account of death, retirement, resignation, and so on. This is measured by dividing the number of workers leaving during the period by the average total number of employees.

Example:

50 employees leave an organization in a year and the average total number of employees is 500. Then the

Here, the average figure means simple average. Simple average is the average of the number of employees at the beginning and at the end of the specified period.

3.13.1 Causes of Labour Turnover

Various causes of labour turnover may be grouped under two heads:

- Avoidable causes.

- Unavoidable causes

3.13.2 Avoidable Causes

These causes can be avoided. The management may take proper measures to minimize or eliminate these causes to avoid the labour turnover. The management has to undertake cost–benefit analysis.

Avoidable causes include the following:

- Unsatisfactory working conditions.

- Lack of job satisfaction.

- Low wages and benefits.

- Lay-offs, overtime and inconvenient working hours.

- Lack of basic amenities—transport, medical reimbursement, etc.

- Relationship with superiors.

- Relationship with fellow workers.

- Lack of incentives and promotion.

- No proper placement of job.

- Lack of training.

3.13.3 Unavoidable Causes

Under this category, the causes for labour turnover cannot be minimized or eliminated by the management. These include:

- Personal betterment.

- Marriage, in case of women workers.

- Retirement.

- Death.

- Health grounds.

- Dismissed by management for genuine reasons.

- Redundancy.

- Family circumstances.

- Disability.

3.13.4 Effects of Labour Turnover

Labour turnover results in an increased cost of production which is due to the following reasons:

(x) |

Increased cost of selection, training and so on of new workers. |

(xi) |

Increase in cost of scrap and defectives. |

(xii) |

Decrease in the overall production on account of time lost between turnover and recruitment. |

(xiii) |

Increase in the cost of plant maintenance due to mishandling of equipments by new workers. |

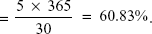

3.13.5 Measurement of Labour Turnover

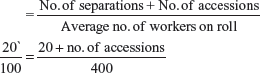

There are various methods in use for measuring the labour turnover. They are as follows:

- Accession method:

(Accession = Nos. at the end of period - Nos. at the beginning + Nos. that have left during the period)

- Separation-rate method:

Formula:

- Replacement method

or

Net labour-turnover-rate method:

Formula:

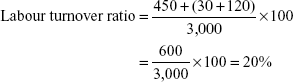

- Flux method:

Formula: