Major Issues in Chinese Cross-Border Mergers and Acquisitions

This chapter deals with China’s rules and regulations governing the conduct of Chinese enterprises that aim to acquire foreign-owned enterprises abroad. We further discuss the accounting method for business combinations in China, review postmerger difficulties as well as integration challenges of the Chinese enterprises that invested abroad, and examine policies of the United States and Australia with respect to China’s direct investment in those countries.

An Overview of Merger and Acquisition Process in China

Chinese enterprises that aim to acquire target companies abroad must comply with certain rules and regulations in China to obtain license from China’s government for the acquisition. In the following, we discuss the main government agencies that are responsible for management of cross-border acquisitions by Chinese enterprises.

Rules for Overseas Acquisitions by Chinese Enterprises

Chinese regulations require that four different agencies approve each overseas acquisition. These agencies include: State Council, the National Development and Reform Commission (NDRC), the Ministry of Commerce (MOFCOM), and the State Administration of Foreign Exchange Control (SAFE).

In certain cases, permission for financial and banking investment from sector-specific regulators such as the China Banking Regulatory Commission and the China Insurance Regulatory Commission is also required. Outbound investments by state-owned enterprises (SOEs) require approval by the State-owned Assets Supervision and Administration Commission of the State Council (SASAC), which at its central level supervises 117 SOEs.1 In some cases, review by the People’s Republic of China’s (PRC) antitrust regulators may also be required.

If extra financing or a fast approval process in certain sectors (such as clean energy) is required, then the approval of the Ministry of Industry and Information Technology is also needed.

The Measures for the Administration of Outbound Investments (the Outbound Investment Measures), which became effective on May 1, 2009, defines an outbound investment as any transaction that establishes “a new overseas enterprise, the merger with or acquisition of an existing overseas enterprise, or obtaining control rights or business management rights thereof” (Wang et al. 2009).

State Council

The State Council of the PRC, which is also known as the Central People’s Government, is the highest executive authority and state administration of the country. The State Council, among its other administrative duties, mandates the NDRC, which relies on its Department of Foreign Capital and Overseas Investment, for “….examining and approving key foreign-invested projects, major resources related overseas investment projects and projects that consume substantial amount of foreign currency” (NDRC 2014).

The Role of National Development and Reform Commission (NDRC)

The NDRC is the main government agency that designs, regulates, and coordinates national economic development and industrial policy of the PRC. In addition to overseeing government investments in the domestic economy of China, the Department of Foreign Capital and Overseas Investment of NDRC adopts “strategies, goals and policies to balance and optimize China’s overseas investments” (Wenbin and Wilkes 2011, 4).

Any outbound investment by Chinese enterprises must first be reviewed by NDRC. Before any overseas acquisitions, a Chinese private or state-owned enterprise must obtain a letter of approval to be submitted to the other state agencies that are responsible for management and control of foreign direct investment (FDI) of China’s enterprises. In general, based on Administrative Measures for Examination and Approval of Overseas Investment Projects, which was published on August 16, 2012, the NDRC and its offices are responsible for reviewing all investment projects that fall into the following two categories:

1.Outlays exceeding $300 million in resource-based sectors

2.Outlays exceeding $100 million in nonresource-based sectors

Review of investment less than the above stated minimum threshold is the responsibility of NDRC’s local offices.

Nonetheless, on December 2, 2013, the Chinese central government (State Council) announced that only investments over $1 billion or investments involving sensitive countries, regions, or industries will require NDRC approval, even though all investments between $300 million and $1 billion are required to be filed with NDRC in all cases (Xiong, Schroder, and Tudor 2014). Contrary to the final project approval regime by the NDRC process, filing an investment in sensitive countries and industries does not require an in-depth review of the project, and is considered “preliminary review”.

Overseas investment projects must meet a number of conditions including compliance with the laws and regulations of China; compliance with the sustainable development of the economy; promotion of exports of technology, products, and services; and compliance with national capital projects and foreign loans. The applicants must also demonstrate their financial capability to invest in the proposed project.

Before a formal review process, a prereview examination of the project is required by NDRC. All Chinese enterprises wishing to invest overseas are required to receive a confirmation letter from the NDRC by submitting a report to NDRC describing the project before any executable binding agreements, proposing binding offers, applying to the foreign government authorities, and launching official bids.

The authority of the NDRC applies not only to direct foreign investment, but also to indirect foreign investment, in the form of providing financing or guarantees to another entity or for the benefit of the offshore affiliates of Chinese enterprises.

Ministry of Commerce (MOFCOM)

MOFCOM oversees the establishment of newly formed enterprises that were acquired through cross-border mergers and acquisitions (M&As). The supervision includes reviewing major agreements, contracts, and documents, for example, review of articles of association of the enterprises to be established. After approving an application for cross-border M&A, the ministry issues the Certificate of Enterprises’ Outbound Investment to the applicant.

The following categories of cross-border investment require approval by the MOFCOM.

•Investments in countries that have no diplomatic relationships with China

•Investments in certain countries, which may involve “political sensitivity,” require review by MOFCOM and the Ministry of Foreign Affairs

•Investments in excess of $100 million

•Investments involving more than one country or region

•Investments involving the establishment of overseas special purpose vehicles (SPVs)

State Administration of Foreign Exchange (SAFE)

SAFE is the Chinese government agency that is responsible for controlling China’s foreign exchange transactions. After the approval of an application for a cross-border investment by NDRC and MOFCOM, another application must be filed with the SAFE for a Foreign Exchange Registration Certificate of Outbound Direct Investment. In the past, this step also involved another review and approval; however, in recent years, this application is a mere registration requirement.

Recent Developments in China’s Outbound Investment Policy Regarding SOEs

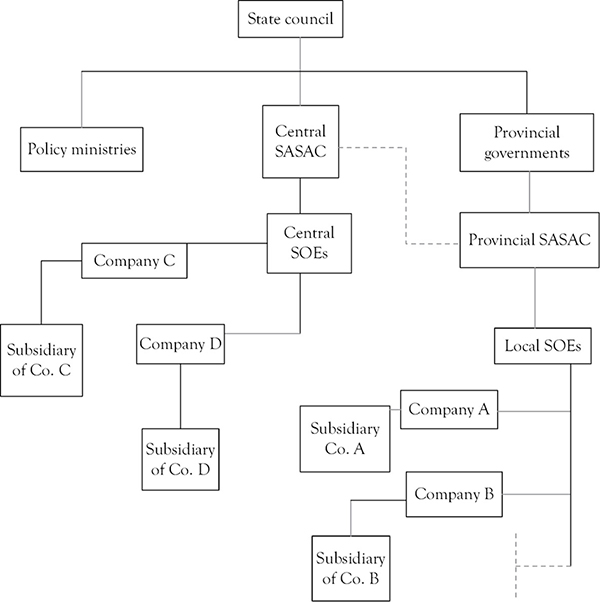

The SASAC is a government agency that is in charge of management of Chinese SOEs. SASAC “…performs investor’s responsibilities, supervises and manages the state-owned assets of the enterprises under the supervision of the Central Government (excluding financial enterprises), and enhances the management of the state-owned assets” (SASAC 2014). Created in 2003, SASAC manages nonfinancial SOEs according to the principle of separation of government administration from enterprise management, by separating management and ownership of the enterprises.

Both the national government and the provincial governments manage SOEs through SASACs. The national government has 117 central SASACs and the provincial SOEs are managed by Provincial SASAC. The organizational flowchart of SOEs in China appears in Figure 15.1.

Figure 15.1 Organizational flowchart of central and provincial SASAC and SOEs

Source: Larum and Qian ( 2012).

As depicted in the flowchart the Central SASAC directly reports to State Council, and the government exercises its ownership control of SOEs by appointment of board members and approval of appointment of senior executives of the enterprises. Moreover, the Organization Department of Communist Party of China plays a role in the management of central SOEs by influencing the appointment of senior management of the enterprises.

Finally, central and provincial SOEs can have wholly, partially owned subsidiaries, or both as well as can enter into joint ventures with foreign or private domestic enterprises (Larum and Qian 2012).

In 2011, the SASAC published two new rules that were to govern the conduct of SOEs or their subsidiaries in outbound investment activities. The first rule is called Interim measures for the supervision and administration of overseas State-owned assets of central State-owned Enterprises (Rule 26). The second rule is Interim measures for the administration of overseas property rights of State-owned Enterprises (Rule 27). These rules became effective on July 1, 2011. Additionally Circular 114, which further recognized and enhanced SOE’s overseas property rights, was issued by the SASAC and became effective on September 29, 2011. The rules and circular were applicable to enterprises under the jurisdiction of the central-level SASAC; however, the provincial-level SASAC has followed suit. Approval of the SASAC is required only in cases where overseas investment falls outside of the primary business of the acquiring SOE, even though approval from NDRC, MOFCOM, and SAFE for these SOEs is required (Norton Rose Fulbright 2014).

We discuss the requirements of the rules next.2

Approval and Filing Requirements

According to Article 7 of Rule 26, merger or acquisition of an overseas listed company, or any “material” overseas investment by a central SOE or its major subsidiary, must be filed with or receive approval from the SASAC. The filing should include information on the size of overall investment, source and composition of funds used on offshore investments. Moreover, the filing should include information regarding the investment projects, containing data such as, the background of investment, description of the investment project, capital structure, investment location and size, financing plan, the implementing terms, risk analysis, and investment cash flows.

Due Diligence

Article 8 of Rule 26 requires due diligence for all overseas investments.

Valuation

Article 9 of Rule 27 requires that in all cases where an SOE intends to use onshore state-owned assets for overseas investments, or transfer the sum of money equal to the appraised asset value to another entity, the appraisal must be conducted by a domestic valuation institution. The appraisal must be filed at the SASAC for approval .

Article 6 of Circular 114 mandates an appraisal of the value of overseas assets to be purchased or sold by a central SOE by a professional appraisal institution with the necessary qualification and good reputation as well as expertise. Article 6 of Circular 114 is applicable to those investments by noncash asset means of payment or changes in holding of shares in nonlisted companies by central SOEs and their subsidiaries.

Article 10, Rule 27, requires that central SOE file appraisal and obtain approval from the SASAC in the event of any transactions by the SOE, which could result in a reduction of state ownership.

All transactions must be based on the appraised value of the assets.

Financing

Article 22, Rule 26, prohibits offshore SOEs and their subsidiaries, with the exception of offshore state-owned financial institutions, from providing financing of any kind to any individual or entity that is not a member of the same group.

Registration and Monitoring of Overseas State-Owned Assets

Article 8, Rule 27, mandates that any overseas acquired state-owned assets and any change in overseas state-owned assets should be registered with the SASAC. Furthermore, Article 4, Circular 114, requires that annual report covering the administration of overseas state-owned properties be submitted to the SASAC by April 30 each year.

Special Purpose Vehicles

Article 11, Rule 26, pertains to registration and approval of SPVs3, and sale of offshore state-owned assets. According to the article, the decision to set up an offshore SPV by the central SOE must be reported to the SASAC in writing. Any SPVs that do not perform useful function must be dissolved. If the payment for the sale of offshore assets is not to be received in one lump sum, the buyer must provide security guaranteeing the outstanding payments.

Recent Development of Chinese Government Regulation of Outbound Investment of China’s Enterprises

Given the growing interest on the part of China’s enterprises for outbound acquisitions, the PRC MOFCOM, as the leading market regulatory agency of China, issued three administrative provisions, guidelines, and policies relating to cross-border M&A activities of China’s enterprises in late March and early April of 2013. These measures encourage outbound acquisitions by Chinese enterprises so long as the investments meet the principles of equity, fairness, and generally acceptable commercial practices. The MOFCOM directives promote fair competition and prohibit unfair business practices, require adoption of environment-friendly policies of acquiring companies, and set standard practices to be used by the ministry’s units and functionaries as well as for Chamber of Commerce and other organizations that are concerned with FDI.

The MOFCOM defines unfair competition to mean any of the following forms of conduct: acquiring business opportunities by bribery; adopting unfair, cut-throat pricing policies; engaging in collusive agreements; damaging the business reputation of a competitor; having false claims to achievements of one’s own enterprise; false advertising, and other activities which are considered unfair competition in law.

To ensure accountability on the part of outbound investors regarding their business conduct, the MOFCOM intends to establish a “bad credit filing system” of overseas investment. The system will aim to record the unfair and anticompetitive conduct of Chinese enterprises that invest abroad and report any misbehavior by these entities to the relevant authorities and institutions. All Chinese enterprises with a bad credit record will be excluded from receiving any policy support from the government of the PRC for 3 years.

The content of the guidelines spells out the social responsibility of enterprises, and makes implementation of the responsibility mandatory for China’s enterprises that invest overseas. These responsibilities include: adopting environment- friendly policies by observing the environmental laws and regulations of the host country as well as standards and practices adopted by international organizations; showing sensitivity to and paying respect to religious beliefs and customs of host countries; and protecting the rights and interests of local workers.

Finally the internal standard practices recommended by MOFCOM aim at the establishment of efficient, transparent corporate governance of Chinese overseas’ enterprises by the mechanism of increased inspection of these enterprises. These measures should be similar to those policies adopted by developed countries, countries that were successful in preventing commercial bribery and in promoting efficient, transparent corporate governance. Furthermore, the standards aim to create corporate culture within Chinese enterprises abroad; promote the public image of Chinese companies; strengthen regulation of overseas Chinese enterprises; and insist on the implementation of the Regulation on the Administration of Foreign Labor Cooperation (Wu 2013).

Accounting Method for Business Combinations in China

Accounting for the proposed M&A constitutes an important part of financial analysis in M&A decision making. In China, the rules for Generally Accepted Accounting Practices, PRC GAAP, were issued by Ministry of Finance under Accounting Standard for Business Combination, No. 20, in 2006.

Accounting Standards for Enterprises No. 20—Business Combinations defines business combination as follows: “The term ‘business combinations’ refers to a transaction or event bringing together two or more separate enterprises into one reporting entity. Business combinations are classified into the business combinations under the same control and the business combinations not under the same control.” Moreover, business combination under the same control is defined as “…. a business combination in which all of the combining enterprises are ultimately controlled by the same party” (Kuai 2006). Accordingly, one can construe a business combination of two or more entities that are under the same control as an M&A.

This rule essentially converges with international business combination standards. The rule requires the use of the “pooling-of-interest method” for business combinations involving entities under common control.

Postmerger Integration Experiences of Chinese Enterprises

In Chapter 13, we discussed postmerger integration processes of private enterprises in great detail. However, discussing whether Chinese enterprises follow the same practices as described in that chapter would be insightful. We will discuss postmerger integration practices of Chinese acquiring firms by reviewing some of China’s FDI post merger practices in Australia and by examining two case studies of Chinese acquisitions in Italy and the United States. Selection of the Australian experiences is motivated by the rising Chinese FDI in that country, which has caused a surge in Australian nationalistic reactions to Chinese investments, restrictions on Chinese FDI in the country, and complaints of Australian discriminatory practices against Chinese firms by China (Mendelshon and Fels 2013). The case in the United States exemplifies inadequate legal due diligences, and the Italian case demonstrates insufficient post-merger integration.

Overseas Investment Performances of Chinese State-Owned Enterprises

Observations of cross-border, postmerger experiences of many Chinese firms indicate that Chinese enterprises operating abroad have not been very effective in adopting new technology, in creating new brands, in investing in marketing and intangible assets, and in adopting Western management practices and corporate governance standards and regulations (Spigarelli, Alon, and Mucelli 2013). Studies have shown that “….in the past 20 years, 67% of China’s cross-border M&A have not been successful and almost all of the country’s technology-seeking M&A have failed” (Chen and Wang 2012, 282).

Factors that contribute to postmerger failure of newly formed enterprises include, but are not limited to (Deloitte 2011; Chen and Wang 2012):

1.Changing market conditions

2.Optimistic view of the market size

3.Selecting an unsuitable partner or having incorrect focus

4.Cultural differences

5.Poor leadership

6.Acquiring an enterprise that is too far removed from the core competency of the acquiring firm

In what follows, we aim to identify additional factors that might be contributing to the not too successful outcomes by case studies.

Due Diligence and Chinese Acquisitions in Australia, Italy and the United States

Anecdotal experiences of Chinese acquiring companies in Australia and the United States, which we discussed earlier in the book confirm the difficulties Chinese entities face in the due diligence stage of acquiring companies abroad. The problems faced by CITIC Pacific and Ralls Corporation, which were discussed in case studies in Chapter 5, are notable examples that may have resulted from inadequate due diligence. In the CITIC Pacific case, even though the initial investment in acquiring the target was $4.2 billion, by the time of production of the output in July 2011, the total investment by CITIC was estimated to have reached $5.2 billion (Sun, Zhang, Chen, 2013; Huang and Austin 2011). In the Ralls Corporation case, the company was forced to cease construction and operating activities and was forbidden to divest without permission of CFIUS. In what follows we will examine two additional cases , which involve Chinese acquisitions in Italy and the United States. The new case studies allow drawing important lessons for appreciation of importance of sufficient legal and cultural due diligences in M&A’s.

China’s Acquisitions in Australia

The pattern of postacquisition integration processes of Chinese acquiring companies in seven acquisitions in Australia indicates a mixed approach in terms of retaining or dismissing the top executives of the acquired companies. The experiences of Chinese acquisitions in Australia show that transferring executives from the acquiring companies to the target depends on the international experiences of the acquiring companies: The higher the international experience of the acquirer, the higher the likelihood of replacing the top management of the target with the executives of the acquiring firm. For example, both Sinosteel and CITIC Pacific appointed their managing director and executive chairman to their Australian subsidiaries, Sinosteel Midwest Corporation and CITIC Pacific Mining, respectively. However, the Chinese enterprises with less international experience retained the executives of the acquired Australian firms and also transferred some of their own executives to the target companies (Huang and Austin 2011).

China’s Acquisition in Italy

Case Study: Qianjiang Motors Acquires Benelli Motorcycles

We use a case study presented by Spigarelli, Alon, and Mucelli (2013) to illustrate the cultural challenges faced in postacquisition integration process by a Chinese acquirer.

Qianjiang Motors, a Chinese SOE, which is located in Zhejiang province in Southeast China, is a manufacturer of motorcycles and engine parts among other products. The company has 7 percent of the market share in China and exports to more than 110 countries. The target company, Benelli Motorcycles, is a small, family-owned Italian manufacturer of motorcycles and scooters that was established in 1911. The Italian company was started as a repair shop for automobile and motorcycles, which also manufactured automobile parts. Having acquired technical know-how, the firm introduced one of its manufactured motorcycles at the Third International Bicycle and Motorcycle Exhibition in Milan in 1921. Winning many national and international awards for manufacturing and design excellence, the firm became very successful in the European market. However, the success of the company ended in the 1960s when Japanese-manufactured motorcycles entered the European and world markets. By 2005, the company had to cease production because of loss of the market share and massive financial losses. The company went bankrupt in 2005.

The Chinese SOE acquired the Italian firm in September 2005, and the combined operations began a month later in October. Given the technical know-how and advanced design skills of the Italian firm, the Chinese company’s goal to acquire it was based on its strategic move to access the technical capabilities of the target. Additionally, the Italian company enjoyed a reputable brand name. The acquirer’s strategy was to combine the technical and marketing capabilities of the Italian company with its own favorable cost of production so that it could compete with the Japanese producers of motorcycles globally.

The location of Benelli Motorcycles is in a province in Italy where the local government and trade unions are very involved in economic activities, and they played an important role in completing the deal.

In the postacquisition phase, the Chinese acquiring company restructured the production processes to increase efficiency, raise production capacity, and by doing so lowered the costs of production. The new entity planned to double the workforce and introduce six products within 2 years. However, no major change in administration was planned. Only the sales director, the part quality manager, and the managing director were relocated from China to Italy. Despite the minimal changes in the management of the target firm, several postmerger integration issues including national cultural differences with respect to attitudes, lifestyles, and approaches to business management appeared.

Using the sales revenues as a measure of postmerger performance of the new company shows that acquisition was not totally successful. In spite of more or less steady sales of the rivals, the new company’s products sold in Italy dropped from 848 in 2008 to 163 in 2009. Specifically, the total value of production of the acquired company dropped from 13.972 million euros in 2006 (the year after acquisition) to 7.747 million euros in 2010. Nevertheless, while both the debts and assets of the company decreased, its equity increased between 2006 and 2010 (Spigarelli, Alon, and Mucelli 2013).

Moreover, difficulties in coordination of human resources mostly in the form of communication because of languages, cultural background, and work habits delayed the development of new products. English was used as a language of communication, but neither side was proficient in English. The Chinese would speak in Mandarin during official meetings on occasions where the two sides disagreed on certain issues. In such conditions, building trust became very challenging.

The differences between Chinese and Italians on the issue of belonging and work habits created another challenge. The Chinese showed a strong commitment to the success of the company, and were willing to work at evenings and weekends; the Italians found such work habits unacceptable, even under urgent situations.

Differences between Chinese and Italian executives on policies such as expenditure of resources for image of the firm, advertising, and customer cares also created friction. The Chinese did not place these items on the top of the priority list, while the Italian executives considered them to be very important. Moreover, persistent efforts on the part of Chinese executives to reduce costs resulted in delays in investments.

The accounting and management information systems of the two companies were not integrated. Finally, the hierarchy, line of command, and responsibility of human resources were not well-defined, and the power was mostly at the disposal of the managing director.

China’s Acquisitions in the United States

Case Study: Lenovo Acquires IBM’s PC Division

In 2005, Lenovo, a Chinese computer company, acquired IBM’s personal-computer division. Lenovo’s strategy for the acquisition of IBM PC division, as stated by Liu Chuanzhi, the founder and chairman of Legend Holding Ltd was capturing synergies from “…leveraging Lenovo’s strength in China and IBM PCs strength in advanced countries, integrating procurement capabilities, optimizing supply relationships, and streamlining end-to-end processes from order taking through fulfillment, all contributing to become more efficient” (Rui and Yip 2008, 220). The motive for Lenovo’s globalization efforts in spite of its preeminence in China’s personal computer (PC) market, which emerged from the company’s competitive advantages such as its technological advantage in China’s niche PC market over its foreign competitors, its large market share, and its profitability in China is based on the potential threat the foreign competitors posed for Lenovo. Both Dell and Hewlett Packard were acquiring more knowledge of the Chinese local market.4

Qiao Song, Lenovo’s senior vice president and chief procurement officer, was assigned the task of the rapid integration of the purchasing departments of IBM PC division and Lenovo, departments that had different processes, management systems, and cultures. Three months before the closing date, the top management of Lenovo also mandated that Mr. Qiao Song save the merged companies over $150 million in direct spending on materials and show an overall annual saving of $300 million within 18 months after closing. Mr. Song met and exceeded the target cost reduction by creating a general-procurement function for the company that was responsible for managing overheads, expenditure such as travels and office supplies. How did Mr. Qiao Song achieve his goal?

In an interview given to McKinsey & Company in May 2008, Mr. Qiao Song (Hexter 2008) stated that in spite of vast differences between the two purchasing departments, the purchasing teams of both companies considered full integration of the purchasing departments to be a top priority because of the sum of money that was to be saved. The managers of the purchasing departments realized that the system differences included processes, information technology (IT), management systems, key performance indicators, and cultures. Given such incongruities, the first set of tasks was determining the production costs for each company, identifying the immediate saving opportunities after closing, and integrating the purchasing departments.

One of the first tasks was identification of costs of the companies. Due to legal restrictions during the negotiations, direct comparison of costs was not permitted. The companies had to select certain members from both purchasing departments so that they could review and analyze cost data for both companies. During these review sessions, the combined team was able to identify common supply categories where Lenovo could share supplies with IBM. Next, synergies from Lenovo’s newly found global access to supplies were realized.

The third source of cost saving was reduction of material costs by redesigning products or eliminating internal items in the products that were not valued by customers. Cost structures of all products of the new company were analyzed. The idea behind such examination was to determine whether a new product design was required or in some cases whether the excessive specifications for a product, for example, internal items that customers could not see, value, or were willing to pay were to be eliminated. Moreover, the process allowed standardization of products, which allowed the company to realize synergy from economies of scale by increasing the volume of purchases from some suppliers.

The net effect of these per-closing costs of production analyses was that the new Lenovo company had a clear understanding of the savings they needed to get, the methods they had to adopt to get them, and the time it required to obtain the savings.

Mr. Qiao Song described the cultural differences between IBM and Lenovo by stating that Lenovo had an entrepreneurial culture, while IBM’s culture was very systematic and analytical. Moreover, on the issue of overcoming cultural differences between the management teams of IBM and Lenovo, Mr. Song indicated that the balance between flexibility in dealing with the senior executives who had difficulties adapting to change during the initial adjustment period and firmness on the performance results was the key to success. He stated that accommodating the senior executives during the adjustment period was fruitful and resulted in complete acculturation and fine performance of those executives. He went on to say that he was focused on results and after the closing of the deal he had a bimonthly review for each product. He required the team members to report on their cost saving efforts. One of the areas that Mr. Song found great resistance from IBM executives was air travel expenses that they thought were very personal. Mr. Song solved the travel expenditure issue by relying on credible insiders who were very familiar with the issue rather than relying on outside consultants to remedy the problem.

Further examination of Lenovo Group’s culture is helpful in developing an understanding of how cultural differences in cross-border M&As could pose difficulties in integration processes.

It is instructive to discuss the pivotal role Mr. Yang Yuanqing played in the development of Lenovo. Mr. Yang, an engineer by training, is the chief executive officer of Lenovo Group, a company that had a humble beginning in 1984. Mr. Yang is described to have a “forceful personality” and is an unrepentant believer in discipline and centralized decision making (Stahl and Köster 2013). Following his disciplinarian instinct, President Yang required that all employees of the company abide by the following company rules:

1.Treat customers and suppliers with care and respect

2.Be frugal: “save money, save energy, save time”

3.Concentrate on the fundamental leadership tasks: build the management team, develop strategy, and lead the employees

4.Do not abuse your position to benefit yourself

5.Do not accept bribes

6.Do not take second employment

7.Do not share information about your salary with your coworkers

8.All employees had to use time clock to check in and out

9.Employees who were tardy to meetings had to stand behind their chair for one minute

10.All employees who were found outside the office building without a reasonable explanation received pay dock5

One could easily imagine that enforcing these rules in Lenovo operations in the United States or other Western countries would pose formidable challenges for the management, because workers in Western countries are resistant to a rigid work environment.

Lenovo is a global player in the IT industry and has become the number one producer of PCs globally. We present the following interesting stories about the company to learn about some recent developments pertaining to Lenovo, and its strategy to become a global entity through M&As.

Bloomberg Technology reported on September 2, 2013, that Chief Executive Officer Yang Yuanqing will share $3.25 million of his bonus with workers for a second year. Lenovo’s staff totaling 10,000 workers in 20 countries received payments in September 2013, in recognition of their contributions to the company. About 85 percent of the recipients are in China (Bloomberg 2013).

Benevolence of Lenovo’s chief executive in contrast to practices of some executives of U.S. companies demanding wage and benefit concessions from employees in the midst of high profitability, while at the same time awarding themselves hefty salary raises and bonuses (Greenhouse 2012) is another clear evidence of the cultural differences between the companies.

On January 20, 2014, Bloomberg Businessweek (Culpan 2014) reported that Lenovo Business Group Ltd is in serious negotiations in acquiring IBM’s low-end server division. The report indicates that Lenovo has completed due diligence and trying to diversify into the server business because of falling demand for PCs. IBM plans to spin off the unit because of its lower profit margin.

According to an e-mail message received by one of the authors from Thomas F. Looney, vice president and general manager, Lenovo North America, Lenovo will acquire:

•IBM’s x86 product lines (including towers, racks, blades, and high-density systems)

•All blade networking technology products

•Solutions and converged systems tied to the previously-mentioned products

•All associated intellectual property (IP)

•IBM’s x86 sales force, research and development teams, quality and product assurance engineers, key labs and other facilities supporting these products

On January 29, 2014, it was announced that Lenovo is in negotiations with Google to acquire Motorola Mobility smartphone business for an initial negotiating price offer of $2.91 billion. With a fast growing smartphone business, the acquisition if completed will give Lenovo a strong position in North and Latin Americas, and a stepping stone into Western Europe. These new markets would complement Lenovo’s smartphone business in the emerging markets. According to the proposed offer, Lenovo will pay $1.41 billion, consisting of $660 million in cash and $750 million in Lenovo’s common stocks, at closing. The remaining balance of $1.5 billion will be paid by a 3-year promissory note (Lenovo 2014).

Policies of Governments of the Host Countries Toward Chinese Outbound Direct Investment

The experiences of many Chinese companies in acquiring companies in North America and Australia have not always been pleasant and positive. In fact, due to the inexperience of many Chinese enterprises in conduct of international business, particularly in M&As, the outbound investing Chinese enterprises have paid heavily for their mistakes. Due to the importance of these experiences for future outbound direct investment including M&A activities of Chinese firms, we will discuss governmental policies and Chinese investment practices in Australia and the United States next.

United States’ Policy Toward Foreign Acquisitions of American Companies and Chinese Experiences of Acquisitions in the United States

The policy of the U.S. government concerning foreign acquisitions of enterprises in the United States is governed by Foreign Investment and National Security Act of 2007. The law defines “covered transaction” to mean “…any merger, acquisition, or takeover that is proposed or pending after August 23, 1988, by or with any foreign person which could result in foreign control of any person engaged in interstate commerce in the United States.” Furthermore, “the term ‘foreign government-controlled transaction’ means any covered transaction that could result in the control of any person engaged in interstate commerce in the United States by a foreign government or an entity controlled by or acting on behalf of a foreign government” (United States of America 2007, 246–247).

In the United States, the trigger for review of the proposed merger is set in motion if the proposed acquisition is in high technology firms, in sectors of critical infrastructure, or if it may result in significant outsourcing of jobs.

The critical infrastructure sectors of the economy include most of the major sectors of the economy including the following: chemical; communication; commercial facilities; critical manufacturing; dams; defense industrial base; emergency services; energy; financial services; food and agriculture; government facilities; healthcare; public health; IT; nuclear reactors, materials, and waste; transportation systems; and water and waste water systems (Department of Homeland Security 2013).

It should be noted that other advanced industrial countries have a similar set of policies concerning foreign acquisitions of domestic enterprises, particularly acquisitions of firms in the critical infrastructure sectors. For discussions of how different countries define critical infrastructure and a short history of the development of laws for control of FDI in the United States, see Masters (2013).

Committee on Foreign Investment in the United States (CFIUS)

As discussed in previous chapters, the Committee on Foreign Investment in the United States (CFIUS) has the responsibility of reviewing M&As of foreign enterprises in the United States, and report to the president of the United States those mergers or acquisitions that are potential threats to the national security of the United States (see Chapter 5 for the case study involving Ralls Corporation and CFIUS). The CFIUS must issue an annual report to the U.S. Congress on the number of notices submitted by foreign enterprises that planned to acquire American companies, the number of filings that were investigated, and the number of filings that were withdrawn.

According to the 2012 Annual Report issued by CFIUS (2014), there were 23 filings by Chinese acquiring companies in 2012, which showed a dramatic rise in such filings by Chinese entities. This number compares to 10 filings in 2011 and 6 filings in 2010. According to this report, Chinese investors had the highest number of filings among 21 foreign investors who filed with CFIUS to declare their intention to acquire companies in the United States. The top five foreign investors were from China (23), United Kingdom (17), Canada (13), Japan (9), and France (8). In addition to China, three were from BRICS (Brazil, Russia, India, China, South Africa) countries including India (4), Brazil (2), and Russian Federation (2).

The committee reports that 45 out of 114 filers in 2012 were investigated; however, it does not publicly report the nationality of the applicants who were investigated. Nevertheless, the published data show that in spite of a 26 percent decline in the number of companies filing for authorization to acquire a target company in the United States, the number and percentage of the applications that were investigated by CFIUS are on the rise (see Table 15.1).

Table 15.1 Total filing, number, and percentage of investigations by CFIUS

|

Year |

Number of notices |

Number of investigations |

Percentage of investigations |

|

2008 |

155 |

23 |

15.00 |

|

2009 |

65 |

25 |

38.00 |

|

2010 |

93 |

35 |

38.00 |

|

2011 |

111 |

40 |

36.00 |

|

2012 |

114 |

45 |

39.00 |

Source: CFIUS (2014).

Does CFIUS Place Chinese Acquiring Companies Under Special Scrutiny?

Given that the data for the number of investigations by nationality of applicants are not publicly available, one cannot make a factual statement about whether CFIUS places the Chinese filers under special scrutiny. Nonetheless, the CFIUS went on record stating in its 2011 Annual Report that “Based on its assessment of transactions identified by CFIUS for purposes of this report, the U.S. Intelligence Community (USIC) judges with moderate confidence that there is likely a coordinated strategy among one or more foreign governments or companies to acquire U.S. companies involved in research, development, or production of critical technologies for which the United States is a leading producer” (CFIUS 2012, 23). Even though the CFIUS did not report a “coordinated strategy” by any government or company owned by a foreign government to acquire company with a “critical technology” during 2012, there is circumstantial evidence that CFIUS views investors from countries that are not allies of the United States with caution.

In addition to the data on a simultaneous rise in the number of filings by investors from BRICS countries and an increase in the number of cases CFIUS reviewed,6 we present the view of a U.S. law firm that specializes in representing companies in M&A matters. In support of the presence of the cautionary approach by CFIUS in dealing with foreign acquisitions from the BRICS countries, particularly from China, we cite a commentary by a U.S. law firm, which states that “…our observation of CFIUS reactions to China-related cases continues to suggest that CFIUS views China and countries that are known to have close economic and military ties to China with heightened suspicion in terms of their potential to execute coordinated strategies to acquire leading-edge U.S. technologies. CFIUS is likely to be particularly sensitive with respect to transactions involving Chinese government-owned or affiliated acquirers. However, even where subjected to heightened scrutiny, China-related transactions have continued to be approved by CFIUS” (Latham & Watkins 2014, 2). Moreover, the 2012 Annual Report stated a number of factors it considered in its review of covered transactions. We quote these considerations from the 2012 Annual Report.

Foreign control of U.S. businesses that:

•Provide products and services to an agency or agencies of the U.S. government, or state and local authorities that have functions that are relevant to national security

•Provide products or services that could expose national security vulnerabilities, including potential cyber security concerns, or create vulnerability to sabotage or espionage. This includes consideration of whether the covered transaction will increase the risk of exploitation of the particular U.S. business’s position in the supply chain

•Have operations, or produce or supply products or services, the security of which may have implications for U.S. national security, such as businesses that involve infrastructure that may constitute critical infrastructure; businesses that involve various aspects of energy production, including extraction, generation, transmission, and distribution; businesses that affect the national transportation system; and businesses that could significantly and directly affect the U.S. financial system

•Have access to classified information or sensitive government or government contract information, including information about employees

•Are in the defense, security, and national security related law enforcement sectors

•Are involved in activities related to weapons and munitions manufacturing, aerospace, satellite, and radar systems

•Produce certain types of advanced technologies that may be useful in defending, or in seeking to impair, U.S. national security, which may include businesses engaged in the design and production of semiconductors and other equipment or components that have both commercial and military applications, or the design, production, or provision of goods and services involving network and data security

•Engage in the research and development, production, or sale of technology, goods, software, or services that are subject to U.S. export controls

•Are in proximity to certain types of United States Government USG facilities

The Report stated the following additional considerations.

Acquisition of control by foreign persons who:

•Are controlled by a foreign government

•Are from a country with a record on nonproliferation and other national security related matters that raises concerns

•Have a historical record of taking or intentions to take actions that could impair U.S. national security (CFIUS 2014, 22–23)

The preceding discussions clearly point to the need for complete legal due diligence by Chinese enterprises before any attempts to negotiate with target companies in the United States.

The U.S. Securities Laws and Acquisition of U.S. Public Companies

In addition to the direct control of foreign acquisitions of U.S.-based companies, the government of the United States has rules and regulations that aim to protect public interest by regulating sales of securities to the public. Prominent among the federal securities laws is the Securities and Exchange Commission (SEC) Act of 1934, which created the SEC. The SEC is to enforce the securities laws and regulate sales and purchases of securities in the United States. The SEC Act requires “… disclosure of important information by anyone seeking to acquire more than 5 percent of a company’s securities by direct purchase or tender offer. Such an offer often is extended in an effort to gain control of the company” (Securities and Exchange Commission 2014).

Foreign enterprises that acquire publicly listed companies in the United States, or list their shares in the U.S. stock exchanges may be audited by the SEC or the Public Company Accounting Oversight Board (PCAOB). The PCAOB is the enforcement arm of the Sarbanes–Oxley Act of 2002, which was legislated after fraudulent practices of a number of large U.S.-based corporations that led to their bankruptcy and massive financial losses by the investing public. Among other issues surrounding the Saranes-Oxley Act, PCAOB auditing, on occasions, have led to the conflict of U.S. securities laws and the laws of the country of the company, which lists shares in U.S. exchanges (Walker 2005).

In a recent ruling, SEC required the Chinese subsidiaries of the four largest auditing firms in the United States to submit certain documents so that the SEC could examine the quality of auditing of the Chinese listed companies in the United States by these firms. These large accounting firms are PricewaterhouseCoopers, Deloitte, Ernst & Young, and KPMG also known as the Big Four. The U.S.-based accounting firms could not produce the required documents stating that doing so would violate a Chinese law that considers such documents state secrets and prohibits making state secrets public. As a result, the SEC filed a complaint against the Big Four alleging that the firms had violated Section 106 of the Sarbanes–Oxley Act by refusing to turn over the requested documents. In a ruling on January 22, 2014, a U.S. Administrative Law Judge agreed with the SEC and ordered suspension of the affiliates of the Big Four for 6 months for practicing before SEC (Black 2014).

Clayton Act of 1914 and Mergers

The Clayton Act of 1914 created the Federal Trade Commission (FTC) and empowered the commission to regulate business conduct. Section 7 of the Act prohibits the purchase of stocks of a company by another if such purchase reduces competition in the industry. Facing the difficulties Section 7 created for companies to purchase the stocks of the target firms, many firms bypassed the law by purchasing the assets of the target. As a result, the Congress amended Section 7 in 1950 by granting the FTC the power to block asset purchases too if such purchase reduced competition.

The degree of concentration in an industry provides a guideline for antitrust law enforcement agencies in determining the level of competition. A widely used measure of concentration in an industry is the Herfindahl–Hirschman Index (HHI), which we discussed in Chapter 5. The HHI uses market shares of the companies in an industry for calculation of the degree of concentration.

The FTC will not investigate a merger if the HHI in the industry of the proposed merger is less than 1,000. An index value in the 1,000 to 1,800 interval may induce an investigation if the proposed merger would increase the HHI by 100 points. Otherwise, no investigation takes place. Finally, a proposed merger that may result in a postmerger HHI value of 1,800 or higher is considered an unacceptable concentration ratio and triggers investigation by antitrust authorities.

Postmerger Class Action Lawsuits by Shareholders in the United States

Another legal issue that cross-border acquirers of companies in the United States must consider is postmerger class action lawsuits by stockholders. As was discussed earlier, many executives of acquiring and target companies face class action lawsuits by disgruntled shareholders after completion of acquisitions. Table 15.2 shows the number of shareholder lawsuits related to acquisitions of U.S. stock companies with value of $100 million or more. The table also shows the percentage of lawsuits that were litigated. Moreover, the table shows the average number of days between the announcement of the deals and the filing of lawsuits. The number of days for filing lawsuits is indicative of the speed of class legal actions undertaken by the shareholders and their legal representatives.

Table 15.2 Number of lawsuits, and numbers and percentages of litigations related to acquisitions with value of $100 million and above in the United States

|

|

2009 |

2010 |

2011 |

2012 |

|

Number of lawsuits filed |

349 |

792 |

742 |

602 |

|

Number of deals litigated |

300 (86%) |

713 (90%) |

690 (93%) |

560 (93%) |

|

Average number of days between deal announcement and suit filing |

14 |

16 |

17 |

14 |

Source: Daines and Koumrian (2013).

The percentage of lawsuits, many of which are considered frivolous, is alarming, and should be taken into consideration in M&A strategy development and in calculating the cost of acquisition. In many of these cases, the defendant pays a nuisance fee to the law firm involved, which drops the case.

The allegations for such legal actions consist of failure of the target’s board of directors to fulfill its fiduciary duties by following a questionable sales process that did not result in the shareholder’s wealth maximization, concluding agreements that were not based on competitive bidding, presence of the executives’ conflict of interests, and failure of a target’s board to disclose full information about the company to enable shareholders to make an informed choice concerning the proposed acquisition. Specifically, the complaint about inadequate information pertains to inadequacy of information about the sales process, the motivation for the board’s decisions, financial predictions, and fairness of the opinion expressed by financial advisers (Daines and Koumrian 2012).

Australian Policy Toward FDI and Chinese Experiences of Direct Investment in Australia

Traditionally, Australia has welcomed foreign investment in that country under the proviso that foreign investment should be by a privately owned and operated entity without any links to foreign governments. Foreign investment in general, particularly FDI in the Australian resource sector, has played an important role in the development of the Australian economy (Drysdale and Findlay 2009). However, the rise in China’s greenfield and M&A activities during the last decade in Australia, particularly Chinese direct investments in the Australian mining and energy sector, has caused public concerns about the potential adverse effects of these investments on Australian’s national security and sovereignty.

To appreciate the rapid growth of China’s direct investment in Australia, let us look at some figures. In 1994 to 1995, the total Chinese investment in Australia amounted to 522 million Australian dollars (Drysdale and Findlay 2009), while this sum increased to 16.190 billion Australian dollars in 2011 to 2012. Chinese investments in 2011 to 2012 involved the following sectors of the Australian economy: agriculture forestry and fishing (A$27 million), finance and insurance (A$60 million), manufacturing (A$538 million), mineral exploration and development (A$10,505 million), real estate (A$4,187 million), resource processing (A$240), services (A$634 million) (Australian Department of Treasury, 2013).

Based on the concerns of national security and sovereignty the Australian Department of Treasury, through Foreign Investment Review Board (FIRB), regulates foreign investment in Australia. However, several decisions by FIRB in blocking several direct investments by Chinese enterprises in Australia have given rise to charges of discrimination against Chinese enterprises by China’s government and corporate officials (Larum 2011).

Established in 1976, mostly in response to the growing number of foreign investments in Australian natural resources, the FIRB was to advise the treasurer on merits of FDI proposals and ensure that the proposed investments safeguarded Australian national interests. The FIRB required that private foreign investment in Australian businesses be below a certain number of dollars (in late 2013, it was roughly A$250 million, and the sum is indexed to the inflation rate in Australia). Furthermore, it requires that the proposed investment does not exceed 15 percent of the assets of the Australian target company, and a maximum of 50 percent for a greenfield investment. However, investment by SOEs and Sovereign Wealth Funds (SWFs) requires review by FIRB and approval by the Australian Treasury Department regardless of the size of the proposed investment.

In cases involving SOEs and SWFs, the FIRB reviews the proposal based on the following six questions:

1.Are the investor’s operations independent of foreign governments?

2.Does the investor adhere to the applicable laws and observe the standard business practices?

3.Could investment reduce competition in the industry?

4.Does the investment adversely impact Australian government’s tax revenues or other policies?

5.Does the investment adversely impact Australian national security?

6.Does the investment impact the operations of an Australian business?

The Australian treasurer had publicly declared that these principles were to address Australian government and public concerns regarding independence, commerciality, and national security. The principles were to uphold economic sovereignty (Principles 1 and 2); wealth generation (Principles 3, 4, and 6) and job creation (Principle 6).

The treasurer further stated that the other aims of the principles were to promote transparency in corporate governance, a goal that cannot be achieved in the governance of SOEs. Moreover, the principles aimed to eliminate the possibility that in a market an investor acts both as the seller and the buyer of a product or natural resource, thus creating an anticompetitive environment (Huang and Austin 2011). Finally, responding to the charge of discrimination against Chinese investors, the treasurer stated that “The Guidelines are non-discriminatory—we apply them to investments by all foreign government entities. They do not target or restrict any particular country” (Larum 2011, 13).

During 2008 and 2009, a number of high-profile Chinese direct investments in Australia were scrutinized by the FIRB. In 2008, Chinalco, a Chinese SOE and leading global producer and manufacturer of metal and fabricated metal products, proposed to acquire an 18 percent interest in multinational mining company Rio Tinto (Rio) for $19 billion, with $7.2 billion convertible bonds (a loan that is convertible to share equity). Roughly about the same time of announcement of the Chinalco–Rio transaction, the Australian government introduced legislation that defined convertible notes and warranty as equity. Due to the extended regulatory oversight and conditions imposed on the proposed deal by the FIRB, Rio withdrew from the proposed acquisition deal in June 2009.7

Subsequent revelations of the motive behind FIRB’s decisions regarding Chinese investments in Australia show that the FIRB acted to exclude Chinese investments. A news story in the Sydney Morning Herald stated that “The anti-China rationale was set out in confidential discussions with U.S. embassy officers in late September 2009 by the head of the Treasury Foreign Investment Division, Patrick Colmer, who is also an executive member of the Foreign Investment Review Board.” The newspaper‘s report on the story further indicated that “The Foreign Investment Review Board told U.S. diplomats that new investment guidelines signaled ’a stricter policy aimed squarely at China’s growing influence in Australia’s resources sector’” (Dorling 2011).

The previous discussions support Chinese investors and government officials’ view that Australia may have discriminated against Chinese direct investment in Australia. According to a survey, which asked Chinese investors and officials “why do you believe that Australia would discriminate against Chinese investment?” the respondents gave the following reasons: Australian nationalism, China is a communist country, Chinese government ownership of Australian natural resources, Chinese financing of FDI through state-owned banks, China’s rapidly growing economy, and Australia is an important player in the U.S. strategy of containing China (Larum 2011).

In June 2010, the six principles were replaced by amendments to Australia’s laws governing foreign investment. These principles were replaced by broader considerations, which aimed to determine whether the proposed investments are based on pure commercial interest or they are proposed with strategic geopolitical gains in mind. Furthermore, the revision considered a company government-owned if a foreign government was an owner of 15 percent or more of its assets. According to the revised rules, SOEs could acquire up to 10 percent interest in an Australian business without notifying the Australian Treasury (Larum 2011).

It should be pointed out that the increasing applications for FDI and the rising trend of approved FDI projects in Australia by the FIRB indicate that Australia is a country welcoming FDI. The trend in total applications and percentages of approved filing by the FIRB as seen in Table 15.3 are supportive of this view.

Table 15.3 Total applications considered and percentage of total applications approved by the Australian FIRB

|

Year |

Total applications considered |

Total approved |

Percentage of total approved |

|

2006–2007 |

7,025 |

6,157 |

88 |

|

2007–2008 |

8,548 |

7,841 |

92 |

|

2008–2009 |

5,821 |

5,357 |

92 |

|

2009–2010 |

4,703 |

4,401 |

93 |

|

2010–2011 |

10,865 |

10,293 |

95 |

|

2011–2012 |

11,420 |

10,703 |

94 |

Source: Australian Department of Treasury (2013).

We should point out that the applications that were not approved included withdrawals because of commercial reasons as well as burdensome requests for alteration of projects by the FIRB.

Summary

This chapter began with an overview of M&A processes in China, discussing the governmental organizations that regulate China’s outbound FDI. After brief discussions of the accounting method for business combinations in China, the postmerger experiences of Chinese enterprises were examined in the context of case studies of Chinese companies acquiring firms in Italy and the United States. Furthermore, governmental policies of Australia and the United States as host countries toward acquisition and inward direct investment were examined. The issue of postclosing shareholders’ lawsuits as an important factor for thorough legal due diligence before any major acquisitions in the United States was also discussed.