Real Option Analysis in Valuation of a Company

The discounted cash flow (DCF) approach to target company valuation is based on the implicit assumption that after the investment decision, the decision maker has no options for change. This assumption is unrealistic in that after the investment decision, the management of the acquiring enterprise may have options that could affect the results after the investment. The flexibility in managerial decision making emerges after the acquisition because investment in a new project brings additional new investment opportunities. Accordingly, any investment decision in real assets such as plants, equipment, land, and technology provides real options, that is, the right, not obligation, to choose to the decision maker. These valuable options are not captured by the traditional capital budgeting approach in asset or company valuation. These include investment timing option, growth option, abandonment option, and flexibility option. The real option method of valuation of target firm remedies this shortcoming. This chapter deals with real option analysis in corporate mergers and acquisitions (M&As).

The following flow diagram depicts the real options available to the acquiring firm.

As an example of a real call option to acquire a company, we cite Societa Metallurgica Italiana (SMI) Company’s provisional acquisition of Delta, a subsidiary of Finmeccanica, an Italian state owned conglomerate, which was a producer of copper from scraps, not from copper ore, for a modest sum, initially. The option agreement required that the acquiring firm invest heavily in Delta, and in case the firm reached a break-even point after 3 years, acquire it for a previously agreed-on price (Sebenius 1998).

Option Terminologies

It is useful to discuss option terminologies before an analysis of how options are used in M&As.

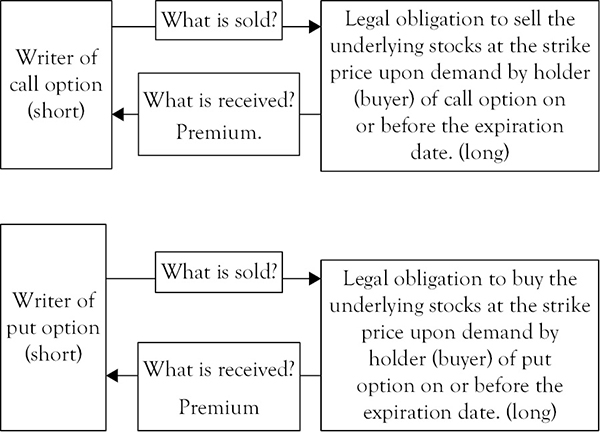

Options are derivatives, which implies that their values are derived from the underlying assets. In general, any derivative contract involves two counterparties. The counterparty that sells the contract is said to be the writer of the contract and takes a short position. The counterparty that has purchased the same contract is the derivative holder and takes a long position. The writer of an option receives a premium initially but assumes potential liabilities at a later date.

An option is the right (not the obligation) to buy, sell, or use a property for a specific period for a specific amount of money. An investor who is long holder of a call option has the right to purchase a unit of underlying asset for a predetermined price at some known time in future, T, which is called the expiration date. The predetermined price is called the exercise or strike price. If the investor is long holder of a put option, then the same arrangement applies and he or she has the right to sell a number of underlying assets at a certain agreed-on price. An investor who is short (writer) in either of the call or put options has received a premium; however, he or she may be required to buy or sell the underlying assets in future, under the terms of the option contract.

Additional elaboration is useful in comprehending the concepts of call and put options as well as gains and potential liabilities of the writer (seller) and holder (buyer) of the call and put options.

The writer of a call option sells the option to an investor (buyer). What does the investor (buyer) of the call option buy? The holder of the call option buys a legal obligation from the writer of the call option to sell the underlying asset for the call option at the strike price to the holder (buyer) of the option if the buyer requests to do so. The writer of the call option, for receiving a fee, is creating contingent liability against him or herself. By the same reasoning, the writer of a put option, for receiving a premium from the buyer of the put option, creates a contingent liability against him or herself by legally accepting to buy the underlying stocks at the exercise price from the holder of the put option.

We elaborate on the exchanges schematically next.

Schematic view of call and put option transactions

Out-of-Money Options

A call option is said to be out-of-money if the strike price is greater than the market price.

In-the-Money Options

A call option is said to be in-the-money if the strike price is less than the market price. Buy the item at a lower market price and then immediately exercise the call option by selling it at a higher strike price.

A put option is said to be in-the-money if the strike price is higher than the market price. Buy the item at a lower market price and then exercise the option by selling it at the agreed-on higher strike price.

American Option

In an American option, one can exercise the options any time before the option expires.

European Option

A European option can only be exercised on its expiration date.

The Option Premium (Option Price)

The option premium is the price the buyer pays the seller for the rights received by the option contract. It is the price of the option.

Illustration of Mechanics of Working of Call and Put Options

We illustrate the mechanism of how options work by examples.

Call Option

The payoff for a European call option with the underlying asset price S, an expiration date of T, and strike price K, that is, c(S,T) is given as follows:

![]()

This implies that if K > S, that is, if the strike price is higher than the prevailing market price of the asset, the option is worthless and the holder will abandon it. We illustrate this concept by an example as follows.

Example 9.1

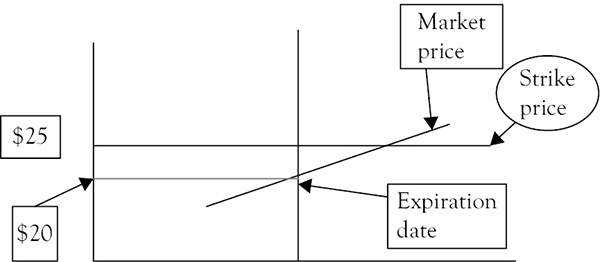

You believe that XYZ company’s stock with a closing price of $20.00 the day before will go up over the next 3 months. You buy the right to purchase 100 shares of XYZ (a call option) at the strike price of $25.00 with the expiration date of 90 days. Suppose the XYZ call option price is $0.50 per share, or a total cost of (0.5)(100) = $50.00 for the option.

Possible Scenarios of the Investment Outcomes

a. At the expiration date, the option is in-the-money (the market price is greater than the strike price). The call option holder will buy at the strike price ($25) and sell at the market price ($35), realizing a profit (see Figure 9.1) of

Figure 9.1 Call option in-the-money scenario

![]()

b. Suppose the market price = $20.00 at the expiration date. You would not exercise the option and simply lose $50.00 (Figure 9.2).

Figure 9.2 Call option out-of-money scenario

Put Option

The payoff for a European put option with the underlying asset price S and an expiration date of T, that is, p(S,T) is

![]()

Example 9.2

You believe that XYZ company’s stock with a closing price of $20.00 the day before will go down over the next 3 months. You buy the right to sell 100 shares of XYZ (a put option) at the strike price of $25.00 with the expiration date of 90 days. Suppose the XYZ put option price is $0.50 per share, or a total cost of (0.5)(100) = $50.00 for the option.

Possible Put Option Scenarios

a. Put option in-the-money scenario:

On the expiration date, the market price is below the strike price. Since you have the right to sell at the strike price, which is higher than the market price, you will purchase 100 shares at $18 per share and immediately sell at the strike price of $25 for a total profit (see Figure 9.3) of

Figure 9.3 Put option in-the-money scenario

![]()

b. Put option out-of-money scenario (Figure 9.4):

Figure 9.4 Put option out-of-money scenario

The strike price of $25 is below the market price of $35. It is not profitable to buy the stocks at $35 per share and then exercise the right to sell for $25. Do not exercise the option.

Types of Options

Two kinds of options exist: Financial options involve financial assets like stocks and currencies, and real options are based on real assets such as land, commercial real estate, equipment, licenses, copyrights, trademarks, and patents.

The motivation to buy or sell a real option is the hope that the agreed price deviates from the market price substantially during the duration of the contract. For example, suppose a firm has an option to lease an office space in downtown Chicago (the lessee) at a predetermined rent. The value of the option increases as the prevailing rent for the office space rises above the agreed-on rent. If the management of the company that wishes to lease the office space believes that rent for office spaces in downtown Chicago will rise, they would enter into a call option contract with the property owner (the lessor), obtaining the right to lease and obligating the writer of the call option (the owner of the property or the lessor) to lease the property at the agreed-on rent. The writer of the option is short and the holder of the option is long.

Of course, risks are ubiquitous in business. On many occasions, the managers of enterprises do not find large investment in a target enterprise prudent, particularly in a new industry or country. Instead of total commitment to invest in such undertaking, they may test the waters by a relatively small investment first and by acquiring the option to expand later when appropriate conditions for further outlays are present.

When merging with a target firm, many outstanding issues facing the target firm could enter as important determinants in valuation of the target company. The acquirer decision on whether to acquire the target might be contingent upon resolution of the outstanding issues. For example, acquisition of a U.S.-based pharmaceutical target firm might be contingent upon the target receiving approval from the Food and Drug Administration, the regulatory agency in the United States in marketing a new drug. Or merging with a target firm might depend on adjudication of a patent dispute or settlement of a lawsuit. These are examples of circumstances that provide preclosing options to the acquiring firm.

The management of the acquiring firm is well-advised if they include postclosing real options in the agreement also. The postclosing options involve the opportunity to expand, abandon, or postpone acquisition of the target enterprise. For example, the acquiring firm might make additional investment in the target company after closing contingent upon the actual cash flows of the target. If the actual cash flows are less than the anticipated cash flow, the acquirer might delay or abandon the target firm either through divestiture or liquidation. On the other hand, if the actual cash flows are exceeding the expectation, the acquiring enterprise might increase the level of investment in the target company.

Valuing Real Options for M&As1

On many occasions, investors have the choice of timing the acquisition of the target firm. The options are immediate investment, no investment, and delayed investment until more information becomes available or more favorable conditions prevail. In the presence of options to investment, the traditional DCF method cannot capture the value of the option present. We use the following examples to illustrate this important point.

Case 1: Expected Cash Flow and Investment Value Without and With Option to Delay Investment. No Initial Capital Outlay

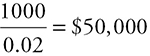

Consider an investor having the option of investing $10,000 in acquiring a target firm or foregoing the acquisition. The acquisition could generate either an annual free cash flow (FCF) of $1,000 or free cash flow of $100, each with the probability p = 0.05. The cash flows are expected to remain constant at the first year level and would last until perpetuity. The discount rate is equal to the risk-free rate of 2 percent.

Assumption 1

Invest $10,000.00 in t0.

Expected value of annual cash flows,

![]()

Expected value of the acquisition, E = (FCF) = $550 at the start of first year of investment:

Note that the expected FCF is to occur at the end of the first year; hence we should discount the value of the expected cash flow at the end of the first year. This means discounting $550 for one year at 2 percent has a discounted value of $27,500 at the start of the year of the discounting.

Net present value of acquisition:

![]()

Assumption 2

Delay acquisition for 1 year until uncertainty of FCFs is eliminated. Two situations could arise.

1.Either free cash flow is FCF = $100.

Value of acquisition:  No acquisition will take place.

No acquisition will take place.

2.Or free cash flow is

FCF = $1000.

Value of acquisition:  if

if

NPV = 50,000 – 10,000 = $40,000 a year from today.

Discounted value of acquisition a year from today

Given the probability of 0.5, the NPV of the acquisition with the option to wait is 0.5 × 39215.68 = $19,607.84.

Comparing the NPVs of the acquisition with the option to wait ($19,707.84) or acquisition without the option to wait $(17,500) reflects the value of the real option, which is $2207.

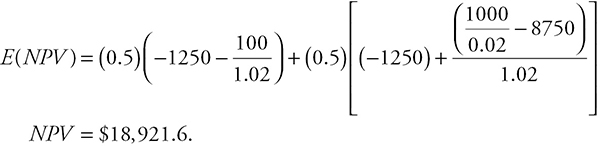

Case 2: Expected Cash Flow and Investment Value With Stages in Investment

A more realistic scenario is a situation when learning about the actual sizes of the expected future cash flows requires an initial investment. Let us use the previous example in case 1 (FCF is either $100 or $1,000, each with the probability of 0.5) but with the requirement that learning about the expected FCF needs some initial investment of $1,250.00 at t0. Suppose that in addition to the initial investment, the balance of $8,750 will be needed at the start of the second year to generate FCF from the second year onward. Suppose the cost of abandonment of the project is $100.

In such a scenario, the expected net present value E(NPV) of the acquisition is calculated as follows:

The logic of the formula follows. By assumption, we have equal probabilities of losing, the first term on the right-hand side of the equation, and gaining, the second term on the right-hand side of the equation. The loss consists of initial investment plus the discounted value of $100 abandonment cost. The gain is the discounted value of the sum of the FCF of $1000, which is to occur at the start of the second year and the remaining investment expenditure minus the initial investment outlay ($1,250) at the start of the first year.

In principle, one can continue with such calculations provided that the probability of cash flows and the cost of capital are known. These important parameters are not readily available in reality, however. Instead, many analysts use a more straightforward approach in real option valuation, a method that is known as the Black–Scholes model. We will discuss the Black–Scholes model for valuation of options in Chapter 10.

Summary

This chapter began with the argument that the traditional capital budgeting approach in valuation of companies rests on the notion that after the investment decision, the decision to invest is irreversible and that investors have no choice to alter the decision. In reality, however, investment decisions are not immutable, and several after-the-fact options are available to the investors. This brings option analysis to the forefront of the discussions.

After introducing the meanings of call and put options and other option terminologies, the chapter discussed the mechanisms of in- and out-of-money call and put options. Moreover, the idea of real options was introduced and determination of the value of real options under different scenarios was presented.