Accounting Information Systems and decision-making

Introduction

Decision-making plays a major, many times crucial, role in managers’ work as they aim to make their organizations prosper. Some of the decisions are operative ones and need to be made on monthly, weekly or even daily basis. Strategic decisions, on the other hand, are made more seldom, but they may be once in a lifetime type of decisions, framing the future of the organization. Decisions also form chains, as most decisions lead to new decision-making situations in the near or more distant future (Mouritsen and Kreiner, 2016).

In order to be able to make “wise” and justified decisions, managers need something to build their decisions on: experience, intuition, information and their combinations, depending on the situation. During the last decade the idea of fact-based decision-making has gained more momentum. This means that decisions could and should be based more on “cold facts” instead of intuition, beliefs and feelings. This development is supported by recent developments in information and communications technology (ICT), such as Big Data and business analytics (CGMA, 2013). The need for more and better information derives from the complexity and dynamics of the global markets and its implications for “success recipes”. In brief, the whole existence of modern ICT and Accounting Information Aystems (AIS) therein is based on information needs. But what are these needs today and in the future? And how can AIS meet such needs?

In this chapter, we outline how modern AIS can support managerial decision-making in contemporary organizations. We also aim to outline some future trends regarding this topic. We start by describing the factors constituting different decision-making environments and what we call data environments. This lays a foundation for describing what kind of information is needed in different contexts and how AIS can support managers in making informed decisions.

Decision-making and its environment

Decision-making contexts vary depending on many issues. Typical contingency factors (Vaassen, 2002; Chenhall, 2003) offer a valid starting point for the analysis of such contexts and the related mechanisms. Such factors include size, lifecycle stage, line of business, technology, strategy, culture and so on. These factors define what kind of information is deemed relevant and valid in each context. As soon as we know about the information needs – i.e. what are the decisions to be made and in what environment – we can start designing information systems (IS) to produce relevant decision support.

Decision-making is a process that can be organized in many ways. Some organizations have defined structured procedures for certain decision categories, whereas some rely more or less on ad hoc practices. Also decision-making styles vary by individuals: some rely more on experience and intuition, while some need and want figures, calculations and systematic analyses on which to base decision-making.

It is also interesting to ponder on the human/computer relationship here. We know that automatization and robotics are taking over many things that used to be carried out by people. Decision support is one of the fields where developments in ICT obviously play a big role in this regard. Many routine-like decisions have been handed over to IT, which can calculate the best choice under defined circumstances. Yet, even in these cases, it is people who define the parameters and algorithms and, in most cases, verify the decisions, like in case of loan decisions in banks.

In most cases, it is still people who make decisions, as decision-making often requires experience-based, analytical thinking, as well as interpretation of information. Bigger decisions are typically made in groups, where different forms of expertise come together to inform decision-making in a versatile and more comprehensive way. Altogether, decision-making involves human action and interaction, which brings along different perceptions, interpretations, misunderstandings, disputes about estimates and emotions. This is also the reason why there is a tendency to go for automatized, fact-based decision-making; it is thought to reduce the number and magnitude of human errors in the process. In this regard, it is also important to recognize that if the decision is made by a single person, there may emerge problems with cognitive and motivational biases.

Decisions are not made in a vacuum, but they are influenced by a number of factors in the decision-making environment. Information systems, such as AIS, can support people in these tasks by offering answers to specified questions, creating scenarios for learning purposes, as well as supporting decision influencing and legitimation (Burchell et al., 1980; Chong and Eggleton, 2003). An important issue to consider here is also the style with which decisions are made. Some people prefer fast and aggressive decision-making styles, whereas others act more slowly and as followers. This has natural implications for how they use AIS and other IS.

A relevant generic concept affecting management in organizations relates to institutionalized, taken-for-granted assumptions and beliefs, i.e. culture. Organizational culture tells “how things are done here”. Gradually, also, IS start carrying such assumptions and values, as they reflect managerial cognitions and logics (Kaplan, 2008, 2011). This way IS may also standardize behaviour towards common ways of operating.

As mentioned, all these issues alone and together define what decisions are needed and made, and especially what kind of information is needed to facilitate decision-making. We will also elaborate later the fact that in addition to what information is produced, the successfulness of decision-making ultimately depends on how that information is used. Getting information of good quality seems to be a common challenge of contemporary organizations. This is due to many things, not least because of the large number and fast pace of changes in the networked and global operating environment. This is also the reason why ICT has been put into the core of the development agenda of most organizations: how to get more valid, timely and relevant information to support decisions to be made regarding the short and long term. Vaassen (2002) has defined the quality of information being composed of two main characteristics: economy, i.e. the cost of producing information, and effectiveness. In this framework, effectiveness is further divided into reliability (validity and completeness) and relevance (accuracy, timeliness, understandability). This is a comprehensive basis against which to analyze contextual information needs and the design of AIS and other IS.

Data environment/ICT domain

In order to produce information that fulfils the above mentioned quality criteria, organizations have to carry out careful IS design. The simple fact is that you cannot analyze and report something on which you do not collect data. Without going into the technical details in this chapter, we simply describe the process of producing relevant information and further knowledge as the information is applied in decision-making situations.

As Taipaleenmäki and Ikäheimo (2013) explicate, this process starts from the configuration of metadata and proceeds into data collection/registration procedures and further to data storage (databases and data warehouses) through ETL (extract, transform, load) technologies. The process where these datasets are transformed into information takes place in enterprise software, stand-alone software and spreadsheets. AIS technologies include all these elements, and can be used alone or together. Some of the calculations that are run through software are automated, some made ad hoc by user requirements.

We draw here on the definition of AIS by Vaassen (2002, p. 3). He distinguishes four related elements of AIS:

• Information systems: an information system is a set of interrelated components working together to collect, retrieve, process, store and disseminate information for the purpose of facilitating planning, control, coordination and decision making in businesses and other organizations.

• Managerial information provision: the systematic gathering, recording and processing of data aimed at the provision of information for management decisions (choosing among alternative applications) for entity functionality and entity control, including accountability.

• Accounting and administrative organization.

• Internal control.

Of these four elements we focus on the two first ones, i.e. IS and managerial information provision. However, technical details in this regard are beyond the scope of this chapter. Concrete examples of this sphere are budgeting systems, performance measurement/management systems (e.g. balanced scorecard), costing systems and various ad hoc analyses to support specific decisions. Regarding informed decision-making, these systems alone or in various combinations support managers. The general idea of such AIS is to provide financial and non-financial (numeric) information that is reported in desired forms to the decision-makers. Different applications from spreadsheets to enterprise systems offer nowadays a number of ways to visualize the information. The people producing such information also increasingly apply sophisticated techniques, including data mining and simulation technologies.

Framework of decision-making and AIS

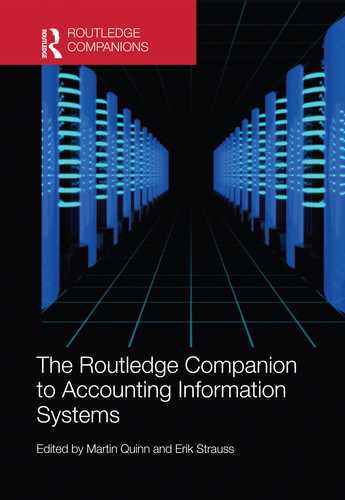

Figure 7.1 summarizes the “big picture” of AIS and decision-making. The starting point is that managers face decision-making situations for which they need specific information; sometimes detailed, sometimes more “rough”. This sets requirements for AIS design that are mediated by the context where the decision is being made. AIS designers then aim to design and develop systems that meet the requirements. In a similar vein, the decision-making environment mediates the information channels as relevant and important information is filtered in the process towards the actual decisions, which themselves entail complex filtering and interaction mechanisms.

The decisions made and the experience gained in the decision-making process feed to learning and consequent development initiatives that influence, for example, perceptions regarding the role of AIS and, in the end, system development. The AIS needs to be constantly evaluated and developed to keep up with and fit the operating environment and technological development, the question being: under the specific circumstances, how to produce efficiently and effectively information that is reliable, comprehensive (yet accurate) and offered in a timely manner in an understandable visualized format (Vaassen, 2002).

Figure 7.1 Data environment and decision-making environment framing decision-making

Decision-making situations and AIS

In this section, we are discussing the roles AIS may play in different decision-making situations. First, we will take a look at the Burchell et al. (1980) framework and then discuss its implications for managerial practice. Although the framework was presented in the 1980s, it is still today highly relevant for analysing the role of AIS in organizational decision-making, as the premises regarding uncertainty related to decision-making have not changed.

The Burchell et al. (1980) framework

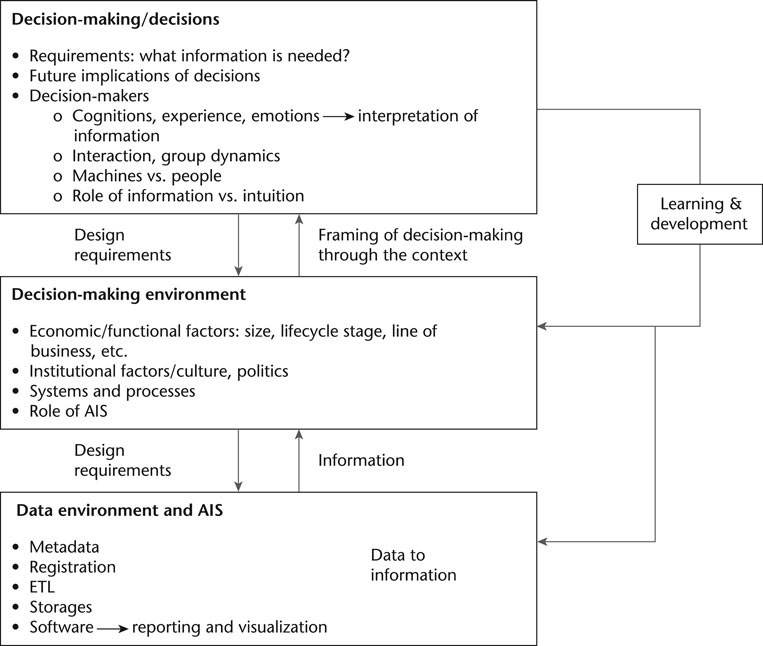

Burchell et al. (1980) (see also Figure 7.2) argued that the uses of accounting information were extended and accounting systems were not used any longer only for taxation purposes, but also for enabling more detailed financial management of the firm. They explained this by the emergence of new organizational practices and forms, which include coordinating, centralized and functional control, as well as divisional, matrix and project organizations. Organizations were also required to fulfil more extensive needs of reporting for capital markets. They stated that accountants were more and more involved in different types of management activities, such as budgeting and standard costing, planning and resource allocation, and thus they became central actors in organizational management.

Figure 7.2 Uncertainty, decision-making and the roles of accounting practice

Source: Adapted from Burchell et al., 1980; Boland, 1979

They also argued that these internal organizational changes and external pressures resulted in changes in accounting and institutionalization of accounting. Accounting had become more than only a “machine” responding to preconceived organizational needs; the role of accountants was becoming more like searching for new opportunities regarding accounting practice. In addition, new professional institutes and bodies of accounting and accountants were established. The transformation also implied that accounting procedures were increasingly defined and documented in all kinds of organizations (Burchell et al., 1980).

In addition, Burchell et al. (1980) stated that the relationship between accounting and organizational decision-making had been conceived as only normative; the role of accounting is simply to provide relevant information for decision-making and improve the decision-making processes. However, they argued that this perspective had been taken for granted and rarely examined critically. For that reason, understanding better the role of accounting in organizations, they used the framework of Thompson and Tuden (1959) to elaborate on the roles of accounting in decision-making in practice.

The Thompson and Tuden (1959) framework is divided into categories by the uncertainty regarding casue-and-effect relations (either low or high) and uncertainty regarding objectives (either low or high). Burchell et al. (1980) presented that when objectives are clear and the consequences of actions are known/certain, decision-making is possible by automation (computation). Under such circumstances decision-making may be designed and programmable, and thus accounting can serve as an “answer machine”. When the relations between cause and effect become more uncertain, decision-making will be more judgemental and subjective by the participants in decision-making. In practice, this means ad hoc analyses and what-if models. Burchell et al. (1980) call this role of accounting in decision-making process as “learning machine”. In times of Big Data, though, the IS may find relevant cause-and-effect relations without users’ knowledge. We may say that sometimes the IS “knows” more than the user even in uncertain environments. However, decision-making under such circumstances typically requires human cognition and capability to interpret whether the suggested relations are valid and reliable. When the relation between causes and effects are certain but the objectives include political rather than computational rationales, the role of accounting in the decision-making process is seen to be an “ammunition machine” (or “dialogue machine”). And finally, when both uncertainty regarding objectives and uncertainty regarding cause-and-effect relations is high, the decision-making tends to be of an inspirational nature, and accounting has been used for legitimizing and justifying actions. This role of accounting Burchell et al. (1980) describes as a “rationalization machine”.

The role of AIS in different decision-making situations

We have chosen four basic decision-making situations for further analysis, including pricing, product mix, equipment replacement and outsourcing decisions. While it is impossible to include all kinds of decision-making situations in such an analysis, we can consider these decision types to be relatively commonly relevant (capital budgeting is also excluded from the analysis as there is a chapter in this book analysing the role of AIS in investment appraisal). Overall, our approach in this analysis derives from the fact that in contemporary organizations decision-making situations have been presented as information management questions (for more detailed descriptions and calculations, see for example Burns et al., 2013).

Pricing decisions

Pricing is one of the most important decision-making situations in every organization. Too low pricing requires higher sales volumes, whereas too high pricing means higher profit margin per unit, but typically results in lower sales volume. Thus, to adjust pricing to the level where it meets the pricing strategy so that it is in line with the company’s financial objectives is a demanding task.

Porter (1980) noted early on that corporate strategy has to be targeted either to cost leadership or to differentiation. If the target is to offer the lowest price, the company follows a cost leadership strategy. If the customer segment is not price-sensitive, a differentiation strategy should be applied. In cost leadership strategy, the purpose is to win the market share having the lowest prices, or at least having the lowest price regarding value for customers.

We argue that a cost leadership strategy, in particular, requires continuous search for cost reductions in all business activities, and thus there also exists a continuous need to make decisions, which can be supported by AIS and its automatic process controlling. Sometimes decision-making models in pricing can be pre-programmed. This means that pricing models with different types of demands can be estimated. By giving the parameters, AIS will calculate the prices or control the processes. For example, regarding flight tickets, decision-makers have pre-programmed the pricing model for the tickets and the prices will be changed based on the designed demand curve. Similar situations can be found in banks regarding credit lending decisions. By giving the parameters on borrowers, IS will produce a risk assessment and the interest rate (price) for the customer. If some of the parameters are changed, a new price or risk rate will be generated. In this way, decisions on price can be automatized and the role of AIS is to support the decision-making and work as an “answer machine”. In particular, the digital environment facilitates the design of the pricing process to be computational, as it enables the cost-efficient collection of data for future pricing modelling. However, it is rarely possible to pre-program pricing decisions totally. Even if we would be able to pre-program our pricing model, we are not able to pre-program our customer buying behaviour.

When there is no uncertainty regarding the objectives but there is uncertainty regarding causes and effects, managers face questions such as: What have the prices and volumes been previously? How did our actions affect demand and profitability? And, what can be expected if we set prices now and in the near future in a particular way? Combining different data sets concerning these questions, AIS can support decision-making as a “learning machine” by producing relevant pricing scenarios for decision-makers. Accountants and managers can learn about the potential consequences of decisions by experimenting with various alternatives in the pricing model and thus generate an understanding of the pricing mechanisms. The capacity of AIS to make simulations is supported by functionality combining future plans with different types of historical data from the databases. Naturally, in the end, a decision simply needs to be made based on this understanding, which may later prove to be a good one or not, depending on our ability to estimate the consequences of the actions taken.

Pricing may many times also include subjective elements. In situations where the objectives are not clear (e.g. regarding the pricing strategy in general), but we have certain ideas regarding causalities, the role of AIS may become an “ammunition machine”, as decision-makers may use different scenarios offered by the AIS to influence other people involved with the decision of their view regarding the “correct price”. This role has also been labelled as a “dialogue machine” (Boland, 1979), meaning that AIS may in this role help managers to develop and argue different points of view which are conflicting (but consistent with the underlying facts). This view emphasises the role of AIS to encourage exploration and debate.

Regarding the “rationalization machine” or role, first of all, it may be that AIS information is used afterwards to demonstrate that the made decision was a good one. We may also state that AIS themselves may work as “rationalization machines”. Contemporary AIS include different types of simulation methods and embedded knowledge for pricing which may as such legitimise the role of AIS in decision-making vis-à-vis other bases of decision-making, such as experience and even intuition.

Product mix decisions

Product mix decisions include typically four dimensions: (1) the number of different product lines of the company, (2) the total number of items within the product lines, (3) versions of each product in one product line and (4) consistency, which tells about the relation between the product lines. Decision-making in this context may relate, for example, to the following kinds of questions: (1) Should we establish new product lines or remove some of the existing ones; (2) Should we add more items into certain product lines; (3) How many versions should we have regarding each product; or (4) Should the product lines be more consistent with each other (see for example Cooper and Kaplan, 1991; Drury, 2008)?

As we may infer from the above questions, product mix decisions are closely related to the market situation, capacity issues, cost structure, as well as the lot sizes of production (see for example Lea and Fredendall, 2002). The role of AIS is to connect sales, purchasing, logistics and marketing together in order to provide data on financial and cost management issues. A sales order may start all the transactions in the supply chain: when a sales order has been entered into the system, deliveries, production or purchasing orders may be generated. This illustrates that, particularly in real time and digital environment, IS can support decision-making even automatically. Uncertainty of objectives and causality are pretty low in this context, and AIS works as an “answer machine” in short-term planning.

In long-term planning, the role of AIS is to present historical data on demand. Managing the product mix and the supply chain is not based on sales orders, but more on mixed subjective interpretations of historical data. In this type of decision-making situation, AIS can support decision-making in the learning role (simulations) or, depending on the level of uncertainty regarding objectives, as an “ammunition machine” as the different potential choices are discussed and debated. Like in pricing decisions, contemporary AIS may also be connected to different types of production planning methods, like Lean Manufacturing, Just-in-Time production, or Activity-Based-Management. Regarding the legitimizing role, the same premises apply here as in the case of pricing decisions illustrated above.

Equipment replacement investments

Replacement investments differ from other investments in that those involve the displacement or scrapping of an existing investment. Typically, investments are made when new assets are required for the expansion of the company. We can say that replacement investments are less complex to make and they do not require such a massive search for alternatives as new expansion investments. One key characteristic in replacement investments is also the timing, referring here to optimizing: how long to keep existing machinery before it starts to be generally more cost-beneficial to replace it (see for example Dobbs, 2004; Merret, 1965). An interesting question also is what the replacement investments are like in contemporary organizations: in addition to parts or modifications regarding existing product lines they may increasingly concern service type of investments, like new versions of software. This makes the evaluation of optimal replacement even more challenging, as it is very difficult to evaluate how “worn out” the original investment is.

Today, the Internet has brought the sourcing of products and services globally available. This means that comparisons can be made easily in real time worldwide. Sometimes the sourcing is based on sourcing catalogues, which may make it possible to even automatize the decisions on replacement investments. In such a case, the IS gives the decision-makers clear guidelines on where to source and what the item and transaction costs will be. In these situations, AIS works as an “answer machine”.

When replacement investments involve high uncertainty regarding causalities but there is a clear vision on objectives (at least costs of investments can be gathered and reported), AIS include all the needed data in the database which can be used in the decision-making process for simulations and to learn about the optional paths to take. Then, we can say that AIS works like a “learning machine”.

Similarly, as in the other examples above, also here AIS can be used as an “ammunition machine” (even in a political way) as alternative calculations are produced to back up one’s own views and debate the options concerning the decisions to be made and actions to be taken. AIS databases typically include a lot of historical data, which can be used for such influencing purposes in situations where there is disagreement regarding the objectives of action. Typically, in post-auditing of investments, AIS can be used as a “rationalization machine” to evaluate and justify the decisions made. However, regarding replacement investments, this role is less apparent than in case of decisions on new expansion investments.

Outsourcing

The outsourcing decision is also known as the make-or-buy decision. This means that there may exist needs to decide whether to manufacture items or produce services in-house or purchase those from an external supplier. Two main issues have to be considered in these situations: (1) cost of outsourcing in relation to own production and (2) availability of production capacity (see for example Burns et al., 2013).

Contemporary organizations are more and more part of global alliances and networks. For example, regarding manufacturing type of organizations, they increasingly work either as subcontractors or manage their own subcontractor networks. In the leading-edge firms, the subcontractor works just like the purchaser’s own product line. In this context, modern IS need to enable control of inputs, outputs and capacity in real time. Even if the supply chain as such could be automatized, there is always an unavoidable need for supervision and control. Only people are able to manage and make decisions when something goes wrong and unexpected things happen (which are not pre-programmed into the IS). An AIS may work automatically in a “controller” role, as an “answer machine”, when we know the consequences of actions and there is no uncertainty involved with our objectives.

In situations when the objectives are clear but there is uncertainty around the cause-and-effect relations, AIS with its database can support decisions as a “learning machine”. It can be used to produce different simulations on the optional paths regarding make-or-buy, and facilitate the generation of future scenarios as the decision-makers want to speculate on the outcomes of the different paths; the possible different future states of affairs.

Also, when causalities are clear (e.g. outsourcing will advance the organization’s operations) but it is not clear which products, product lines or services should be outsourced, AIS can act as an “ammunition machine” in debates around the specific actions to be taken.

Finally, we may suggest that the role of AIS in decision-making regarding outsourcing when both the objectives and causalities are unclear (high uncertainty) is more to build the decision-making context. Contemporary AIS may thus act in a constituting role in trying to offer as many clues as possible concerning the uncertain environment; at least it may serve this role in a way to help the decision-makers realize the high uncertainty surrounding the decision to be made.

Conclusion – the role of AIS in decision-making

To summarize, for the first, we may conclude that the task of AIS in supporting decision-making, in its technical form, is to collect, retrieve, process, store and disseminate managerially relevant information to decision-makers (see Vaassen, 2002). In the digitalized environment, AIS may collect and build on massive databases in serving this task. However, as we have described, this is only one dimension in the big picture as it comes to how the decision-making environment is constituted and what factors are involved before the final decision is reached and executed. In this process, the AIS may act in different roles depending on uncertainty related to the objectives and cause-and-effect relations surrounding the particular decision situation: giving answers, facilitating learning, serving as a basis for argumentation and legitimizing the decisions (Burchell et al., 1980).

When objectives and causalities of decisions are known – in other words, when uncertainties of both objectives and causalities are low – AIS are able to present the correct options within the framework of specified parameters. Then it is possible to automatize and pre-program the decision-making models, and AIS may work as an “answer machine”. If the objectives are clear but causalities are not well-known, AIS are not able to give clear answers to the questions the decision-makers may have, but rather options and directions through simulations. AIS works then as a “learning machine”. When decision-makers have different opinions regarding the objectives but the causalities are relatively clear, AIS with its capability to produce reliable figures and facts can offer a valid basis on which to build arguments as the decision-makers try to influence the decision situation and convince each other about a specific option. AIS acts then as an “ammunition machine” as it is used for purposeful prioritizing. When there is uncertainty involved with both the objectives and causalities, AIS may work as a basis with which decisions are legitimized (ex post), i.e. as a “rationalization machine”.

Decision-making situations can be categorized either as operational or strategic. Operational decisions are of short-term and repeatable nature, and they do not require huge amounts of monetary or other resources. On the other hand, strategic decision-making situations are of long-term nature and they typically affect the whole organization. Uncertainty in operational decisions is known to be lower than in strategic decisions. This distinction also affects the roles AIS may have. In operational decisions, the decision-making model can sometimes be pre-programmed and automated, whereas with strategic decisions the situation typically exists only once; they do not occur repeatedly, but are more or less unique. Strategic decisions also typically involve higher amounts of uncertainty and risk, which means that the “ammunition” and “rationalizing” roles of AIS often get activated.

Nevertheless, both operative and strategic decisions involve behavioural aspects, the first typically less, the latter even quite a lot, as the long-term orientation makes the situation more difficult; whenever we look further into the future, the amount of uncertainty inevitably increases. This further relates to the amount of subjectivity and interpretation of information involved with both individual and group decision-making. We may assume that decision-making models that are more or less programmable imply that interpretation of information is kind of in-built into the AIS model. There is not much room or even need for interpretation, although the final decisions always require human consideration. Anyway, when decisions are made for the first time, it always requires human understanding. Later, as we have learnt from mistakes and causal effects of our actions, we can improve decision-making and information models to be increasingly programmable, especially as comes to operational decisions.

AIS can neither make interpretations, nor can they interact with their environment. The supporting role of AIS is important to note as we increasingly discuss artificial intelligence and robotics. Not even the best systems can over time accurately foresee the consequences of decisions; how customers, competitors or employees may act in the short or, particularly, long term. Burchell et al. (1980) recognized early on the interpretative nature of decision-making and thus the complex nature of AIS therein.

In this context, we should also appreciate the role of decision-making styles. Sometimes decisions are required to be made in unexpected situations and quickly, whereas in some situations decisions can be made slowly, following activity in the markets; the behaviour of competitors and consumers, for example, as comes to pricing decisions. Some decision-makers have more trust in figures whereas some may base their decisions more on intuition and feelings. AIS are part of the decision-making process, where decision-makers and AIS work together. However, the role of AIS depends on the style of decision-making. People’s sense making and cognitive characteristics are different, which makes the design of AIS always challenging.

We should also always appreciate the different organizational contexts where decision-makers operate. Each organization has its own policies and processes to prepare and make decisions. Furthermore, different decision-making processes may exist also within the same organizations, in their different business units, or divisions in different geographical locations. This is a further challenge for AIS, in the design of which it is often cost-effective to aim for standardization, which, on the other hand, may mean contextual trade-offs concerning the validity and relevance of the information produced.

We have illustrated also the role AIS themselves play in constituting decision-making environments. AIS design is often used to document and systematize previously undocumented or unsystematic (not transparent) processes with the aim of standardization of practices. In this way AIS also work as security checks for decision control: the decision-making processes are expected to be followed as documented and programmed into AIS. The intention at the more general level then is to secure that the processes are in line with the organizational rules and policies. In that sense, AIS are not only technical tools, but also kind of “social actors” in organization, as they carry common rules and procedures regarding decision-making practice. Somewhat paradoxically, the subjectivity involved with decision-making may undermine or lead to bypassing of such rules, as people follow routines that may be only loosely coupled to the formal rules.

Overall, the context of decision-making cannot be emphasized enough. The contingency factors framing AIS design and use are crucial to understand. For example, in small organizations decision-making processes are naturally different than in large ones. In small organizations, there may not exist decision-making policies. It may be that those are not even needed, if the entrepreneur-CEO is responsible for all the decisions and is responsible for their outcomes only to himself/herself. When companies grow, the need for more comprehensive systems emerges. Thus, the role of AIS in decision-making is always depending on the size, line of business, lifecycle stage, etc. of the organization.

We have been discussing the role of AIS in supporting decision-making. However, in some situations AIS may have less favourable effects; they may slow down or even create obstacles in the decision-making process. AIS are nowadays relatively complex and multidimensional, which requires a lot of knowledge from their users. The process required by the rules embedded in AIS and related systems and policies may sometimes lead to unnecessarily cumbersome and complicated practices, resulting in frustration, dissatisfaction and shortcutting. Sometimes these may be unintended consequences of the AIS design; the purpose has been something else, but for several reasons, for instance, the end-users of the systems have not been engaged in the design process sufficiently to support decision-makers in their real-life tasks. In this way, the AIS may have become, at least partly, an obstacle to efficient and effective decision-making that not only slows down the process, but may also lead to “random behaviour” where nobody can any longer separate the facts from fiction. This is also a further indication of the role AIS may play as a part of the broader socio-technical decision-making context.

We may conclude that the role of AIS should be explored through the following perspectives: (1) data and information context, i.e. decisions are based on “naked” facts and/or interpretation, (2) decision-making and organizational context, i.e. the decision-making process is either systematic and documented or not and (3) decision-makers’ context, i.e. the decision has been made individually or in a group. These elements have been presented in Figure 7.3 overleaf summarizing the role of AIS in decision-making (cf. Figure 7.1).

Future trends

This chapter has explored how AIS can support decision-making in organizations. We also briefly described how AIS may hinder or slow down decision-making. The sophistication of AIS for decision-making obviously varies a lot in practice due to different contingency factors. Our general illustration holds for most organizations, especially the larger ones. On the other hand, technology is never ready and the most advanced companies and public sector organizations have already moved to the era of Big Data and its analytics (Warren et al., 2015). When we include also non-structured data in the sphere of AIS and other IS, we enter a new world of decision support. Hadoop and other applications, not to mention data collection through the Internet of Things, facilitates already now (on-line) decision-making regarding not only pricing and operative activities, but they also transform whole business models and processes how business is being made. Robotics and automatization are inseparable parts of this phenomenon.

Interestingly, Burchell et al. (1980) pointed out the political and influencing roles of AIS partly questioning the existence of a pure “answer machine”. However, with the technological development this role gets increasingly emphasized, as the modern technology seems to enable better and better fact-based and automated decision-making. This is an important observation also because this is becoming possible even if the decision-making environment (including causalities) has become more and more uncertain and turbulent, in general. Furthermore, regarding the lower right-hand corner of the framework, also an “idea machine” role has been suggested for AIS (Earl and Hopwood, 1981): a role enabling creative solutions to be found to messy problems as objectives are ambiguous and predictive models are poor. This role was earlier considered to be unrealistic to expect from a formal AIS. We suggest that with the new technologies (Big Data, analytics, etc.), if embedded in the AIS, make this a realistic role to expect.

Figure 7.3 Summary of AIS and decision-making

With the developing ICT also comes risks. One such risk relates to the huge amount of data being generated every second. There is a real risk of “drowning” in data and information. Having more data and more versatile data, and data scientists to handle it, the role of knowledgeable managers is yet of utmost importance. This is because data/information tells little without real understanding and insight of the business. Technological complexity sets new requirements for businesses and even to existing business models. We will increasingly face radical transformations in this regard, which also implies that decision-making will change: what we will decide upon and how. Regarding Figure 7.1, this also means that the design requirements for AIS gradually change. And who knows if in the future we will any longer see AIS as we know them today, but rather embedded technologies that together form massive decision-making systems including all kinds of data collected on-line. In any case, increasingly, developments in ICT enable the delivery of different software and platforms for AIS for everyone in a cost-effective way through cloud services. Previously the bigger companies have been the pioneers in developing AIS, but this may be changing.

References

Boland, R. J. (1979). Control, causality and information system requirements. Accounting, Organisation and Society, 4(4), 259–272.

Burchell, S., Clubb, C., Hopwood, A., Hughes, J. and Nahapiet, J. (1980). The roles of accounting in organisations and society. Accounting, Organisation and Society, 5(1), 5–27.

Burns, J., Quinn, M., Warren, L. and Oliveira, J. (2013). Management Accounting. Berkshire, UK: McGraw-Hill Education.

CGMA. (2013). From Insight to Impact: Unlocking the Opportunities in Big Data. London: CGMA.

Chenhall, R. (2003). Management control systems design within its organisational context: findings from contingency-based research and directions for the future. Accounting, Organisation and Society, 28(2), 127–168.

Chong, V. K. and Eggleton, I. R. (2003). The decision-facilitating role of management accounting systems on managerial performance: the influence of locus of control and task uncertainty. Advances in Accounting, 20, 165–197.

Cooper, R. and Kaplan, R. (1991). Profit priorities from activity-based costing. Harvard Business Review, 69(3), 130–135.

Dobbs, I. M. (2004). Replacement investment: optimal economic life under uncertainty. Journal of Business Finance & Accounting, 31(5–6), 729–757.

Drury, C. (2008). Management and Cost Accounting, 7th Ed. London: Cengage Learning.

Earl, M. J. and Hopwood, A. G. (1981). From management information to information management. In H. C. Lucas Jr, F. F. Land, T. J. Lincoln and K. Supper (Eds.), The Information Systems Environment. Amsterdam: North Holland.

Kaplan, S. (2008). Cognition, capabilities and incentives: assessing firm response to the fiber-optic revolution. Academy of Management Journal, 51(4), 672–695.

Kaplan, S. (2011). Research in cognition and strategy: reflections on two decades of progress and a look to the future. Journal of Management Studies, 48(3), 665–695.

Lea, B.-R. and Fredendall, L. D. (2002). The impact of management accounting, product structure, product mix algorithm, and planning horizon on manufacturing performance. International Journal of Production Economics, 79(3), 279–299.

Merret, A. J. (1965). Investment in replacement: the optimal replacement method. Journal of Management Studies, 2(2), 153–166.

Mouritsen J. and Kreiner, K. (2016). Accounting, decisions and promises. Accounting, Organisations and Society, 49, 21–31.

Porter M. E. (1980). Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York: Free Press.

Taipaleenmäki, J. and Ikäheimo, S. (2013). On the convergence of management accounting and financial accounting: the role of information technology in accounting change. International Journal of Accounting Information Systems, 14(4), 321–348.

Thompson, J. D, and Tuden, A. (1959). Strategies, structures and processes of organisational decision. In J. D. Thompson, P. B. Hammond and R. W. Hawkes (Eds.), Comparative Studies in Administration. Pittsburgh, PA: University of Pittsburgh Press.

Vaassen, E. (2002). Accounting Information Systems: A Managerial Approach. Hoboken, NJ: John Wiley & Sons.

Warren, J. D., Moffitt, K. C. and Byrnes, P. (2015). How Big Data will change accounting. Accounting Horizons, 29(2), 397–407.