Chapter 10

Closing the Deal: Wrap It Up in Writing

In This Chapter

Confirming agreements for payment in writing

Drafting a short but mighty agreement

Reminding your debtor to pay up

Memory can be very convenient. You probably aren’t surprised when a debtor not only “forgets” to make a first payment, but also “forgets” the amount of that payment and the date it’s due. After all, it’s to the debtor’s advantage to suffer shortness of memory when it comes to promised payments, particularly when the debtor is struggling with cash flow problems and wants to conserve its cash.

They say that promises are meant to be broken, and that’s particularly true of oral ones. After a promise is in writing, however, the rules change, because the written word is more difficult to “forget” than the spoken word, and a faxed copy of your agreement quickly overcomes the objection, “That’s not how I remember it.” That’s one of the reasons we stick to the mantra, “It just isn’t done if it’s not in writing.”

After you have an agreement with a debtor, you should wrap up your deals and payment plans by putting them in writing. It takes very little extra work and can really pay off for you. This chapter guides you through the process of getting your agreements down in writing, with tips on getting your debtor to confirm the written agreement.

Creating and Completing a Written Agreement

From the day your customer becomes your debtor, you’re looking at a history of broken promises. You’ve now negotiated the resolution of its unpaid balance, but what makes this promise any different from what you’ve heard before? Even with the debtor’s renewed commitment to pay off the debt, a part of you knows that there’s a big chance that your debtor will again default in making payments. Having gone through all the work of negotiating an agreement, you may still end up having to file a collection lawsuit and drag the debtor into court.

So your goal is not only to get the new payment agreement down in writing, but also to have a clear document signed by the debtor admitting the balance owed and confirming the promise to pay it off.

Having reached this point in collections, if the debtor defaults yet again, you’re not going to start over. You’re going to court. Why all this emphasis on getting a payment agreement in writing if you’re planning to sue the debtor if a default occurs? Because the fastest way to obtain a judgment against your debtor is to show the court your debtor’s written admission of the balance due and its promise to pay off the acknowledged debt. For more on admissions and their use in court, see Chapter 9.

Even after three decades of collecting debts, I can assure you that it’s still a thrill to hear the judge declare, “Based on what I’ve seen, including written admissions of the debt, it sure seems like the debtor owes the money.” That’s why it’s important to put agreements into writing. The document can help inspire payment should the debtor’s memory become short, and the document makes it more likely that a court will rule in your favor if you have to sue to recover your money.

In this section, we show you how to create a written agreement to pay off the debt while avoiding any pitfalls of possibly saying the wrong thing.

![]() Written agreements have the effect of modifying prior agreements, both written and oral. For example:

Written agreements have the effect of modifying prior agreements, both written and oral. For example:

If you agree on the phone that your debtor is to pay $250 per month on a debt, but you type up your written confirmation with the requirement that he pays $100 per month, you’ll generally be stuck with the $100 payments instead of $250.

If you have a prior promissory note secured by a mortgage that allows for interest, attorney fees, foreclosure rights, and the like, you must take care that any new promissory note or written agreement doesn’t wipe out your remedies under the original note.

When you already have a written agreement to pay off a debt, because of the possibility that a new agreement may weaken your ability to collect the debt, seek professional advice before entering into a new written agreement.

![]() Sometimes when you’re negotiating with a debtor, she’ll request a formal release of liability. A release gives up legal remedies. By releasing the debtor, you give up the right to pursue the debtor for more money, and by getting a release from the debtor, you’re freed from any claim the debtor may have relating to your transactions, bills, and collection activities. Releases are binding in court and must be written carefully. Mistakes can leave you unable to collect a debt, extend to other matters you didn’t think you were resolving (such as a debt owed on a different invoice or to another division of your company), or potentially leave you on the hook for claims you thought you had resolved. We discuss release language in Chapter 19, and you should review that chapter before you negotiate or sign any release agreements.

Sometimes when you’re negotiating with a debtor, she’ll request a formal release of liability. A release gives up legal remedies. By releasing the debtor, you give up the right to pursue the debtor for more money, and by getting a release from the debtor, you’re freed from any claim the debtor may have relating to your transactions, bills, and collection activities. Releases are binding in court and must be written carefully. Mistakes can leave you unable to collect a debt, extend to other matters you didn’t think you were resolving (such as a debt owed on a different invoice or to another division of your company), or potentially leave you on the hook for claims you thought you had resolved. We discuss release language in Chapter 19, and you should review that chapter before you negotiate or sign any release agreements.

Composing a letter or e-mail to your debtor

When you write to your debtor, your primary goal is to motivate him to commit to repayment in writing. Reaching an oral agreement is the hardest part of the collections battle, but if you don’t get it in writing, you’ll quickly realize that your victory was only partial. You want to deprive your debtor of any wiggle room by having the terms of the deal set in stone.

Immediately after the deal is struck, set the stage for written confirmation. Without any hesitation, and while your debtor is still on the phone, say, “Okay then, we have our deal. I’m sending you an e-mail right now to confirm the details. What’s your e-mail address? Do you have it yet? Reply by typing ‘I agree’ and type your name below.” Simple enough, eh?

![]() If you sense that your debtor’s cooperation is limited (for example, he’s just playing along to get you off the phone), it’s crucial that you keep him on the line until he has your e-mail or fax. Get something in writing, even if it’s just a one-liner stating something like:

If you sense that your debtor’s cooperation is limited (for example, he’s just playing along to get you off the phone), it’s crucial that you keep him on the line until he has your e-mail or fax. Get something in writing, even if it’s just a one-liner stating something like:

This confirms our agreement made today, [today’s date], whereby you will make payments of $____ per month on a balance owed of $____, starting next Monday, [Monday’s date].

If your agreement is for a lump sum settlement, the payment terms are:

[The total amount owed, to the penny] to be paid in a full, lump sum, by or before [exact date] at [name of your company and address where you want the payment made].

![]() If the goods or services were personal or household in nature and you’re a debt collector, be certain to include the language “Our office is a debt collector.” Review the discussion of the Fair Debt Collection Practices Act (FDCPA) and possible liability for its violation in Chapter 6.

If the goods or services were personal or household in nature and you’re a debt collector, be certain to include the language “Our office is a debt collector.” Review the discussion of the Fair Debt Collection Practices Act (FDCPA) and possible liability for its violation in Chapter 6.

When you seek written confirmation, remember:

Electronic signatures are legal and enforceable. When a pen-and-ink signature isn’t possible, you can enter into binding agreements through e-mail or by other electronic means.

Speed is key. Use fast methods of delivery, such as an e-mail or fax, so you find out right away — ideally before you’re off the phone, less ideally within the hour — if the debtor is truly motivated to agree in writing to the terms you just negotiated.

![]() If you find it difficult to type the e-mail to the debtor and talk to him at the same time, have a template available. For example, you can have a word processing document or text within your e-mail program that you can quickly copy and paste into the body of your e-mail while you’re still talking to the debtor on the phone.

If you find it difficult to type the e-mail to the debtor and talk to him at the same time, have a template available. For example, you can have a word processing document or text within your e-mail program that you can quickly copy and paste into the body of your e-mail while you’re still talking to the debtor on the phone.

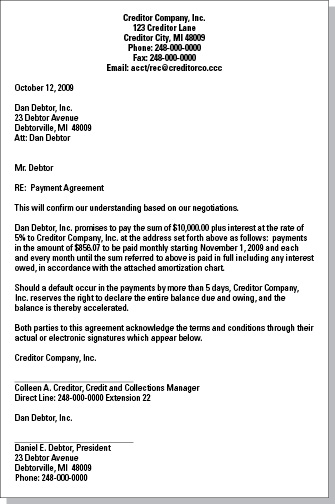

![]() We provide an example agreement for payment in Figure 10-1 and also include it as a template on the CD that accompanies this book (Form 10-1). You can use this letter as the basis for a document you can copy and paste into your faxes and e-mails.

We provide an example agreement for payment in Figure 10-1 and also include it as a template on the CD that accompanies this book (Form 10-1). You can use this letter as the basis for a document you can copy and paste into your faxes and e-mails.

Figure 10-1: An agreement for payment.

![]() If the agreement extends beyond a few payments or involves interest, you may choose to include an amortization schedule. You can find free online calculators that produce amortization schedules; simply search for “amortization schedule” in your favorite search engine. Figure 10-2 shows an example of an amortization schedule, and we include one as a template on the CD (Form 10-2).

If the agreement extends beyond a few payments or involves interest, you may choose to include an amortization schedule. You can find free online calculators that produce amortization schedules; simply search for “amortization schedule” in your favorite search engine. Figure 10-2 shows an example of an amortization schedule, and we include one as a template on the CD (Form 10-2).

![]() The debtor’s objectives are different from yours. Whatever her motive, be it shortage of funds or simply having other financial priorities, your debtor is looking for a reason not to pay you. Keep your writings as simple, quick, and straightforward as possible to minimize any excuses the debtor may raise for not signing on the dotted line.

The debtor’s objectives are different from yours. Whatever her motive, be it shortage of funds or simply having other financial priorities, your debtor is looking for a reason not to pay you. Keep your writings as simple, quick, and straightforward as possible to minimize any excuses the debtor may raise for not signing on the dotted line.

Figure 10-2: An amortization schedule.

Using a promissory note to confirm a deal

A promissory note is a formal contract for payment, typically reciting the balance due, amount of each monthly payment, interest rate, first payment date, last payment date, and possibly providing for late fees. Although a simple payment agreement as we describe earlier in this chapter usually works as well as a promissory note, if you don’t trust the debtor, you anticipate the need for litigation, or your gut instincts tell you that you could have trouble collecting, you may prefer the formality of a promissory note.

Promissory notes are widely understood and accepted. They can be linked to any personal guaranties that you may have negotiated. If you’re taking a lien on property, you should also execute a mortgage or security agreement as part of the agreement.

![]() You can find free promissory notes online, and you can obtain standard form versions through most office supply stores. We also provide a template on the CD accompanying this book (Form 5-1), along with a template for a personal guaranty (Form 3-4).

You can find free promissory notes online, and you can obtain standard form versions through most office supply stores. We also provide a template on the CD accompanying this book (Form 5-1), along with a template for a personal guaranty (Form 3-4).

![]() Your promissory note should describe exactly what you and your debtor agreed on and nothing more. Don’t try to add a new term or condition (such as the addition of interest or late fees) when you didn’t get the debtor’s agreement. Any change you make gives the debtor grounds for dispute, will likely delay payment, and may even frustrate your effort to persuade your debtor to confirm your agreement in writing. Trust works both ways.

Your promissory note should describe exactly what you and your debtor agreed on and nothing more. Don’t try to add a new term or condition (such as the addition of interest or late fees) when you didn’t get the debtor’s agreement. Any change you make gives the debtor grounds for dispute, will likely delay payment, and may even frustrate your effort to persuade your debtor to confirm your agreement in writing. Trust works both ways.

Getting the Payment Plan Underway: That All-Important First Installment

Why is it that the very first installment payment is always the most important one? All the time and effort you put into negotiating a settlement of your account is at stake, and getting the agreed payment in a timely fashion establishes whether your debtor intends to start playing by the rules. If he fails the test, you need to consider litigation, as we describe in Chapter 15.

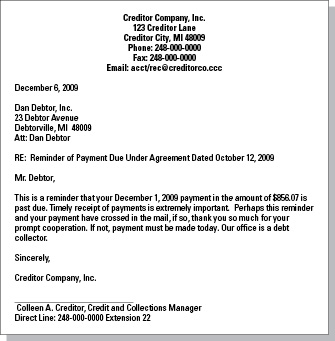

![]() What can you do to improve your odds of getting the first payment? Even with written confirmation in hand, persistence is key. A polite reminder may be a good idea, such as the reminder letter shown in Figure 10-3, which we also include as Form 10-3 on the CD accompanying this book.

What can you do to improve your odds of getting the first payment? Even with written confirmation in hand, persistence is key. A polite reminder may be a good idea, such as the reminder letter shown in Figure 10-3, which we also include as Form 10-3 on the CD accompanying this book.

For best results, fax or e-mail your first (polite) reminder before payment is due.

Figure 10-3: A reminder letter.

![]() Any follow-up correspondence, including a reminder letter, must accurately refer to your agreement with the debtor and to its exact terms. Don’t give your debtor any opportunity to argue that your follow-up letter, e-mail, or fax modified the written agreement through a misstatement of payment date, amount due, or any other term.

Any follow-up correspondence, including a reminder letter, must accurately refer to your agreement with the debtor and to its exact terms. Don’t give your debtor any opportunity to argue that your follow-up letter, e-mail, or fax modified the written agreement through a misstatement of payment date, amount due, or any other term.