Chapter 4

Establishing Good Billing Practices to Avoid Collection Headaches

In This Chapter

Getting prompt payment through effective billing practices

Keeping your billing practices organized

Training employees on billing procedures

One of the tricks of a good salesperson is to keep a steady flow of business cards, brochures, and sales materials of all sizes and shapes in front of the customer. The idea is that if you constantly remind your customers that you’re ready to provide the best products and services, they simply can’t forget about you. Well, the same theory applies to good billing practices: To facilitate timely payment and avoid collection headaches, provide prompt and accurate invoices, statements of account, credit memos, debit memos, and reminder notices to your customers.

Customers come in all sizes, shapes, and personalities. Billing practices should respect those differences and be flexible, giving a gentle nudge to customers who may have just misplaced a bill, but taking a more aggressive approach with customers who intentionally fail to pay their bills. An effective billing system respects the delicate balance between keeping pressure on a customer for prompt payment while, at the same time, maintaining a good business relationship and not jeopardizing future sales. To put it more simply, your system must distinguish between good pay customers and bad pay customers.

If your customer ignores the first invoice, sending a statement of account serves as a reminder. If the invoice and statement of account don’t trigger payment, your billing system gradually increases the pressure on your customer to pay its bill. With each follow-up you send, you try to build a sense of urgency.

In this chapter, you’ll find out what constitutes a good billing system and see how good billing documents and practices can help you keep your accounts current. You’ll also see why accuracy and prompt correction of errors can help you with both billing and collections, and you’ll discover how to train your staff to follow your credit policies.

![]() After you determine your customer hasn’t really forgotten to pay you and something more is going on that’s keeping you from getting what you’re owed, you must determine what that sticking point is. Chapter 5 discusses the multitude of reasons why a customer may not be paying your bills.

After you determine your customer hasn’t really forgotten to pay you and something more is going on that’s keeping you from getting what you’re owed, you must determine what that sticking point is. Chapter 5 discusses the multitude of reasons why a customer may not be paying your bills.

Components of a Well-Run Accounting and Billing Operation

Your accounting and billing operations form the backbone of your company’s entire accounts receivable system, and together they account for every penny of the valuable products or services you provide your customers.

A well-run accounting and billing operation is consistent, tracks the age of customer’s debts, and provides for interest charges as an incentive for timely payment. We discuss each of these topics in this section.

Consistency in billing

Consistency translates into dependability. If a customer disputes a bill, your customer will become defensive (or perhaps offensive). When an account is past due and frustration starts mounting, it’s human nature for your customer to go on the attack. If you create the opportunity, your customer will complain that she “always has problems with your billing system” or that she “never understands” what she’s being billed for.

If you have a good system in place in which you promptly issue invoices and accurate monthly statements of account (see the later section for more on these), you defuse this particular line of attack. Your billing system makes sense and your customer’s frustration isn’t warranted. If you resolve issues of credits, returns, and defective goods as they arise and then make the necessary adjustments in your billing system, your billings should be accurate and consistent.

![]() When customers raise complaints about regular, accurate billings, the problems usually relate to something else entirely, and the odds are that your customer’s account is going to turn into a collections case. See Part II of this book for more discussion of that transition.

When customers raise complaints about regular, accurate billings, the problems usually relate to something else entirely, and the odds are that your customer’s account is going to turn into a collections case. See Part II of this book for more discussion of that transition.

![]() Billing practices are a part of your customer relationships from the time they fill out their credit application and make their very first order on credit. Although you like to think you have a great relationship with all of your customers, the fact is some of them don’t pay on time. Friction results when you apply pressure for payment, and some of those customers get very defensive. Good billing practices help you avoid conflict, avoid and overcome customer arguments, and collect delinquent accounts.

Billing practices are a part of your customer relationships from the time they fill out their credit application and make their very first order on credit. Although you like to think you have a great relationship with all of your customers, the fact is some of them don’t pay on time. Friction results when you apply pressure for payment, and some of those customers get very defensive. Good billing practices help you avoid conflict, avoid and overcome customer arguments, and collect delinquent accounts.

An aging report

Using the “but that’s the way we’ve always done it” approach to a billing system works well as long as all of your customers are paying on time (as if that’s gonna happen). Inevitably some customers start to slow down their payments. And just as inevitably you must review “the way we’ve always done it” for possible improvement.

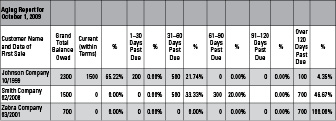

If your billing system doesn’t alert you when a customer pays slowly, that lack of information may hurt your cash flow. Your billing system should produce a written warning that delinquencies exist. This document is called an aging report. An aging report is a visual guide of customers that aren’t paying all of their bills on time. It contains

The customer’s name

How long that customer has been with you

Optionally, a contact name and phone number for the customer

Seven columns for the total amount the customer owes you:

• The grand total the customer owes you

• The portion that’s current (within selling terms)

• The portion that’s 1 to 30 days past due

• The portion that’s 31 to 60 days past due

• The portion that’s 61 to 90 days past due

• The portion that’s 91 to 120 days past due

• The portion that’s more than 120 days past due

![]() If you like to use color in your reports, color the last column (“More than 90 days past due”) red. That column should appear to be on fire, screaming a loud, clear message to you that any numbers in that column require immediate attention. That’s the column that shows you’re losing money and suffering a reduced cash flow. The delinquency must be dealt with promptly as outlined in your credit policy (described in Chapter 2). Chapter 5 describes how this information can be helpful to bring a delinquent customer back into the fold.

If you like to use color in your reports, color the last column (“More than 90 days past due”) red. That column should appear to be on fire, screaming a loud, clear message to you that any numbers in that column require immediate attention. That’s the column that shows you’re losing money and suffering a reduced cash flow. The delinquency must be dealt with promptly as outlined in your credit policy (described in Chapter 2). Chapter 5 describes how this information can be helpful to bring a delinquent customer back into the fold.

![]() If you’re using a computerized bookkeeping system, aging reports are easy to compile because they consist of information already in your computer. The aging report may be a “stock report” easily produced by your software. If not, have your computer person create the report as shown on the template that appears here as Figure 4-1, also provided as Form 4-1 on the accompanying CD.

If you’re using a computerized bookkeeping system, aging reports are easy to compile because they consist of information already in your computer. The aging report may be a “stock report” easily produced by your software. If not, have your computer person create the report as shown on the template that appears here as Figure 4-1, also provided as Form 4-1 on the accompanying CD.

Figure 4-1: An aging report.

Interest charges for late payments

When it comes to billing systems, the squeaky wheel gets the grease, as they say. Never forget that in addition to your invoices, your customer is paying bills from other suppliers, utility companies, taxing authorities, and their bank. With each billing cycle your customer sets its priorities, choosing which bills to pay first. You want your bills to get the highest possible priority.

![]() A simple measure, charging interest on delinquent accounts, can help prompt your customer to want to pay your bills before interest starts to accrue. You should disclose interest charges in your purchase contracts or credit applications. Typically, you start charging interest when payment is past due. Interest charges can wake up your customer to the importance of paying an overdue account. You can also offer a full or partial waiver of interest charges to inspire your customer to pay off the overdue balance.

A simple measure, charging interest on delinquent accounts, can help prompt your customer to want to pay your bills before interest starts to accrue. You should disclose interest charges in your purchase contracts or credit applications. Typically, you start charging interest when payment is past due. Interest charges can wake up your customer to the importance of paying an overdue account. You can also offer a full or partial waiver of interest charges to inspire your customer to pay off the overdue balance.

![]() Beware of violating your state’s usury laws — limits on the interest rates you may legally charge. Also, be aware that invoices aren’t contracts, so if you’re planning to charge interest on the past due account, disclose it in your sales or credit contract. Chapter 6 provides information on interest and usury laws.

Beware of violating your state’s usury laws — limits on the interest rates you may legally charge. Also, be aware that invoices aren’t contracts, so if you’re planning to charge interest on the past due account, disclose it in your sales or credit contract. Chapter 6 provides information on interest and usury laws.

Setting Up an Effective Billing System

An effective billing system requires the following documents and steps:

Use a credit application so your customer agrees to basic terms up front (see Chapter 3).

Obtain a purchase order number or form from your customer so your customer can’t refute at a later point and time that he ordered the goods or services from your company.

Invoice promptly to reinforce that your customer ordered the goods, you shipped them, and you expect payment for them.

Keep copies of delivery documents, if applicable, so you can show that the ordered items were delivered.

Document changes to amounts due. Track any adjustments to the amount your customer owes with credit and debit memos.

Use change orders to document your customer’s authorization for any modification of its orders.

Send a statement of account as a monthly reminder to your customer that it owes you money.

![]() Should your customer start to dispute the account, and you need to apply pressure for payment, your good billing practices will support your claim in the negotiating process and possibly even in court.

Should your customer start to dispute the account, and you need to apply pressure for payment, your good billing practices will support your claim in the negotiating process and possibly even in court.

The documents used in your billing system each play an important role in creating an account that gets paid or in supporting a collection action. The following sections discuss each of these documents and their role in getting your account paid.

Purchase orders: Proving the order was placed

A purchase order (PO) documents that your customer ordered your product or service. The PO may be preceded by a formal written or oral contract between you and your customer describing the specifics of your relationship. You should obtain a copy of the purchase order from your customer. The PO may be written or oral:

If written, the purchase order describes what your customer has ordered. A typical PO describes the date of the purchase and the items or services purchased, and includes a PO number unique to the transaction that your customer uses for purposes of internal tracking.

If oral, the PO is normally the customer’s purchase order number. You place the PO number on your invoice when billing your customer so every invoice can be matched to a PO number.

Consider a purchase order in action: After you deliver $500 worth of white, 10-inch paper plates, your customer claims he never placed the order. Your customer says he’s not going to pay the invoice and “you can come and get these plates if you want to.” How do you prove the customer ordered the plates? You show him his own purchase order.

![]() Your paperwork will stay much more organized and customer payments will arrive faster if you can quickly tie each invoice on your statement of accounts to a PO number. It’s good practice to include purchase order numbers on your invoices, even if the customer’s PO is written and describes the goods or services purchased, because customers often refuse to pay invoices that can’t be matched up with their POs.

Your paperwork will stay much more organized and customer payments will arrive faster if you can quickly tie each invoice on your statement of accounts to a PO number. It’s good practice to include purchase order numbers on your invoices, even if the customer’s PO is written and describes the goods or services purchased, because customers often refuse to pay invoices that can’t be matched up with their POs.

Invoices: Obtaining payment through effective invoicing

Your invoice is the bill for the products or services rendered by your company to your customer. The invoice describes the product or service provided, the quantity (goods) or time involved (services), pricing information, date ordered, and date delivered. It includes a reference to the purchase order, a total of the sum owed for that invoice, and sometimes a signature from the customer.

What to include on your invoice

When considering the information to include on an invoice, put yourself in your customer’s position. Ask yourself what questions you’d want answered before you pay the bill. For example, you would want to know what the bill is for, what dates are covered, who provided the goods or services described on the invoice, and the total amount due. Assuming you are a good bill payer, after your basic questions have been answered, you submit your payment. Accordingly, invoices should include

Name and address of your company.

Separate address where bills are paid (if applicable). For example, if your receivables are sent to a bank or a location where volume payments are processed, you should list this as the payment address.

Date of the invoice.

Your customer’s name.

Your customer’s account number with your company.

Your customer’s PO number.

Product or service description with itemized number of units and pricing.

Total owed so the customer knows exactly how much money it owes based on the exact goods and services you’ve provided.

Statement that goods are to be inspected promptly.

Statement of your policy for the return of goods.

Due date for payment by your customer. Common billing cycles are 30 days, although standard billing cycles may be longer or shorter depending on your industry. Whether you expect your customers to pay in 10 days, 20 days, or 30 days, the due date should be prominent on the invoice so the customer knows exactly when the bill is due.

Statement on charging interest. Because interest charges often motivate customers to pay their accounts before they become delinquent, it’s good practice to charge interest for late payments. (Remember to stay within your state’s usury laws; see Chapter 6 for more on this.)

![]() It’s good business practice to include on your invoices contract terms such as return policies and interest charges. However, new contract terms introduced on an invoice are generally not binding on your customer. Although invoices typically describe various terms of sale, such as requiring the customer to promptly inspect the item for damage or pay interest if the invoice falls delinquent, courts typically don’t consider the invoice to be any sort of contract; they often regard it as nothing more than a bill.

It’s good business practice to include on your invoices contract terms such as return policies and interest charges. However, new contract terms introduced on an invoice are generally not binding on your customer. Although invoices typically describe various terms of sale, such as requiring the customer to promptly inspect the item for damage or pay interest if the invoice falls delinquent, courts typically don’t consider the invoice to be any sort of contract; they often regard it as nothing more than a bill.

If you want to create binding contract terms for inspection, interest charges, and the like, make those terms part of a contract you enter into with your customer before furnishing the goods and services, or even include them in the customer’s credit application.

![]() An invoice template is provided on the CD accompanying this book (Form 4-2), and an example is offered in Figure 4-2.

An invoice template is provided on the CD accompanying this book (Form 4-2), and an example is offered in Figure 4-2.

Invoicing promptly

No customer has only one bill to be paid, and there’s only so much money to go around. Your ultimate goal is to have your invoice scheduled promptly for payment.

Consistent with the theory that visual reminders help your customers remember their obligations to you, your billing system should issue an invoice every time you provide a product or a service. In some industries, this means you’ll be issuing dozens or even hundreds of invoices per month.

![]() Depending on your business, you can have your representative or salesperson issue an invoice at the same time he provides your goods or performs your services, instead of issuing them by mail.

Depending on your business, you can have your representative or salesperson issue an invoice at the same time he provides your goods or performs your services, instead of issuing them by mail.

![]() The invoice should be generated promptly. Delays cause problems. Customers become upset if they’re not billed promptly. It’s a mistake to feel that your customers benefit from delayed invoicing. Your customers expect prompt billing for goods and services so they can schedule payment of that bill and move on. They may become frustrated by slow billing. You can’t expect your customers to pay before you bill them, so slow billing can also hurt your cash flow.

The invoice should be generated promptly. Delays cause problems. Customers become upset if they’re not billed promptly. It’s a mistake to feel that your customers benefit from delayed invoicing. Your customers expect prompt billing for goods and services so they can schedule payment of that bill and move on. They may become frustrated by slow billing. You can’t expect your customers to pay before you bill them, so slow billing can also hurt your cash flow.

It’s a good practice to get your customer’s signature on a credit agreement or order form, especially if a separate delivery receipt isn’t obtained for the transaction (see the next section for more on delivery receipts).

Delivery receipts: Establishing proof the product was received

Delivery receipts are provided by carriers such as trucking companies that deliver your goods to your customers. The principal purpose of the receipt is to prove that your customer received the goods. At times, the delivery receipt also establishes that the goods you delivered were correct, in working order, and in the right quantity. Needless to say, when things go wrong, proof of receipt can be an important part of your collection file.

![]() If you ship by a major carrier, such as UPS, FedEx, or the U.S. Postal Service, you can go online to verify that the goods were delivered and, if necessary, use the verification as evidence in court to document that your customer received the goods. Major carriers allow you to enter tracking numbers for packages on their Web sites to see where your shipment is in the delivery process.

If you ship by a major carrier, such as UPS, FedEx, or the U.S. Postal Service, you can go online to verify that the goods were delivered and, if necessary, use the verification as evidence in court to document that your customer received the goods. Major carriers allow you to enter tracking numbers for packages on their Web sites to see where your shipment is in the delivery process.

Figure 4-2: A sample invoice.

Credit and debit memos: Documenting changes in the balance owed

A credit memo is issued by you to document products or services that you provided to your customer but that weren’t received or were rejected or returned. It may also credit your customer for items billed in error. A debit memo is typically issued when your customer fails to pay an invoice, or pays less than the entire amount that’s due. These documents establish why your ledger shows an additional credit or debit on your customer’s account, raising or lowering the balance that’s otherwise due from the customer. It’s important to maintain a clear record of changes in the event of a later dispute or litigation.

Use credit memos when a credit is given to a customer for such items as returns or a negotiated reduction in the balance the customer owes. The paper trail should always be clear so the customer knows exactly what happened and when, and how much is still due. Here’s the process for issuing a credit memo:

1. You deliver to your customer the goods ordered, along with an invoice. The customer contacts you because something is wrong with the order.

For example, you have invoiced your customer $500 for a shipment of paper plates, but $100 worth of those plates arrived soiled. Ideally, your customer follows your process for return of defective goods and contacts you to request a return authorization.

2. Assuming you bear the risk of loss, such that it was your responsibility to have the items arrive in good condition, you have the customer destroy the goods in question or return them to you. To document the transaction, you issue a credit memo for the amount of the damaged goods and change the customer’s account balance accordingly.

In the case of the damaged paper plates, you issue a $100 credit. The balance on your customer’s account is now $400.

3. On the next monthly statement of account to your customer, the original invoice amount is shown with a deduction for the credit memo. This results in a net balance due.

So for the pesky paper plates, the statement of accounts would show the original invoice amount of $500 with a $100 deduction for the credit memo. The customer’s net balance due is $400.

Because your credit memo immediately took the $100 off the customer’s statement of account, interest is never charged on the amount that was credited. But remember, most billing programs calculate interest based on dates inserted. The prompt issuance of the credit memo, and its entry into your billing system with an accurate date, is essential to avoid inadvertent interest charges on that $100.

Use debit memos when your customer underpays the account and a balance is still due. For example, your customer orders $500 worth of paper plates that arrive damaged. You give your customer a $100 credit for the damage, but your customer demands an additional $50 credit against the $400 balance for the time it took to sort out the damaged goods. Your company rejects that request. The customer nonetheless sends you a check for $350, and invoices your company for $50. You can keep the account accurate with a debit memo:

1. You deposit the $350 check, leaving a balance due of $50.

2. You issue a debit memo for $50 to counteract the $50 invoice from your customer.

Your next monthly statement to the customer accurately states the $50 balance due.

![]() See Figure 4-3 for an example of a credit memo and Figure 4-4 for an example of a debit memo. Both of these are on the accompanying CD, as Form 4-3 and Form 4-4, respectively.

See Figure 4-3 for an example of a credit memo and Figure 4-4 for an example of a debit memo. Both of these are on the accompanying CD, as Form 4-3 and Form 4-4, respectively.

Figure 4-3: A credit memo.

Figure 4-4: A debit memo.

Change orders: Putting modification of the agreement in writing

Change orders are important to document price increases, changes in materials, services, or other changes affecting price, and the balance due from the customer. Some contracts require any changes to be in writing, while others don’t. Whatever your contracts require, even without a requirement that changes be in writing, a written change order helps you establish that a change was authorized by the customer. With the possible exception of interest charges and late fees, always document changes that are going to affect the balance that appears on the customer’s next statement of account.

The best practice is to use a form that is signed or initialed by the customer. (Electronic signatures are fine.) If you don’t get a signature, particularly when price increases are involved, don’t be surprised if your customer forgets that the change was authorized and takes issue with your billing.

![]() The change order template seen in Figure 4-5 is included on the CD materials (Form 4-5).

The change order template seen in Figure 4-5 is included on the CD materials (Form 4-5).

Figure 4-5: A change order form.

Statements of account: Sending monthly statements as a regular reminder to pay

Whether your customer’s account includes only one invoice or hundreds of invoices for the current billing cycle, the next document forwarded to your customer as a reminder for payment should be a summary statement of account.

A customer’s statement of account is a running ledger of the customer’s transactions, including all payments, debits, and credits. The statement summarizes your transactions with the customer over the course of the billing period (usually 30 days). Each invoice is listed along with its total amount. The statement ends with the exact balance the customer owes, including any extra charges contracted for by the customer since the last statement, and any interest due on the account.

If your customer is tracking the same transactions accurately, with the possible exception of interest due or add-on costs not yet factored in by the customer, the balance you state should be consistent with your customer’s own books. You should send statements of account to your customers on a monthly basis.

![]() Accumulated interest should be included on statements of account to remind the customer just how important it is to pay billings promptly. Some statements also include an aging sheet as shown in Figure 4-6, a statement of account. When the customer sees that an account is delinquent and that interest is accumulating, she may be motivated to pay you promptly.

Accumulated interest should be included on statements of account to remind the customer just how important it is to pay billings promptly. Some statements also include an aging sheet as shown in Figure 4-6, a statement of account. When the customer sees that an account is delinquent and that interest is accumulating, she may be motivated to pay you promptly.

![]() Some customers are used to paying based on invoices and become confused when they receive a statement of account. When they see a statement of account that includes charges you previously invoiced, they may perceive that they’re being double billed. But of course you’re not double billing. Customers can pay either by invoice or by statement balance and will quickly get used to your system.

Some customers are used to paying based on invoices and become confused when they receive a statement of account. When they see a statement of account that includes charges you previously invoiced, they may perceive that they’re being double billed. But of course you’re not double billing. Customers can pay either by invoice or by statement balance and will quickly get used to your system.

![]() A typical customer statement is provided in Figure 4-6, and is included on the CD materials as a template form for your convenience (Form 4-6).

A typical customer statement is provided in Figure 4-6, and is included on the CD materials as a template form for your convenience (Form 4-6).

Figure 4-6: A statement of account.

Keeping Your Bills Accurate

“How can I pay you, when you haven’t even billed me yet?”

“I never pay without a bill!”

“I need something in writing.”

Gee, those statements sound familiar. Customers want prompt, accurate paperwork — or they just won’t pay. The speed, timing, and content of the forms you use in your billing system are crucial, and they impact the paying habits of your customers — so make your billing system the best it can be. In the following sections, we explain how to make sure your billing practices accurately reflect the transactions you’ve had with your customers.

Creating an effective billing system

To be effective, your accounting and billing system should organize and properly document the items on your customer accounting ledger, and keep your customers constantly informed as to the exact balances they owe. You should be able to support every item on your statement of account with appropriate documentation, such as by matching customer purchase orders to invoices. When you can explain every item on your statement, your customers quickly run out of excuses for slow payment or nonpayment. Your customers will also be aware of your interest charges and that their unpaid balances are growing on a monthly basis.

![]() You want your statements and other communications to be clear. Even your best paying customers will raise questions from time to time if they’re confused about any item in your billing system. Take care of billing errors right away so customers are reassured that your billing system is accurate and dependable.

You want your statements and other communications to be clear. Even your best paying customers will raise questions from time to time if they’re confused about any item in your billing system. Take care of billing errors right away so customers are reassured that your billing system is accurate and dependable.

For example, if you forget to issue a credit memo for $100 worth of defective items, your customer may remind you to do that. You quickly investigate the matter and, if appropriate, promptly issue the credit. The next statement of account reflects that credit memo, and your customer is reassured.

Your prompt investigation into customers’ concerns helps you with customers who aren’t being forthright. For example, a customer with very limited cash flow may scrutinize your paperwork and try to pick it apart to justify delaying payment. Even though he owes the money, that type of customer uses any excuse not to pay because his company is juggling its money to try to stay in business.

Finally, you have customers who just won’t pay. Some are in extreme financial difficulties, while others just don’t want to pay their bills for whatever reason they have or imagine. You must use aggressive billing tactics with these customers. Should you end up in court trying to justify to a judge why these customers haven’t paid you, your good billing practices will pay off.

Maintaining precise records

Customers want to see the proper documentation before authorizing payment on their account. To this end, your billings should be prepared promptly after your products or services are provided and then sent out in an organized fashion.

![]() Having a computer helps you keep track of data, process invoices, and update accounts, but data still has to be processed by people — and garbage in, garbage out can occur without proper procedures in place. Create a clearinghouse where all the forms from your billing system are gathered in one place, and minimize the number of people who are responsible for entering data into your computer system. When too many people are responsible for forms, or data is entered from several different locations or different departments, confusion becomes more likely, and errors become more difficult to track down. (See the later section on training your billing staff for more about ensuring smooth data entry processing.)

Having a computer helps you keep track of data, process invoices, and update accounts, but data still has to be processed by people — and garbage in, garbage out can occur without proper procedures in place. Create a clearinghouse where all the forms from your billing system are gathered in one place, and minimize the number of people who are responsible for entering data into your computer system. When too many people are responsible for forms, or data is entered from several different locations or different departments, confusion becomes more likely, and errors become more difficult to track down. (See the later section on training your billing staff for more about ensuring smooth data entry processing.)

Mandate an organized approach to data entry. Your monthly statements of account will make the most sense and be complete if the supporting “cast of characters” — invoices, credit and debit memos, interest calculations, deductions for payments received, and so on — are all present and accounted for. If these supporting documents are not in your system when you generate your statements of account, you’ll create confusion for your customers.

Making sure your forms don’t conflict with each other

Your customers expect your invoices and statements of account to be accurate and dependable. That’s why they pay your bills. If a form is inaccurate, your customer immediately becomes suspicious that he is being ripped off, and payments come to a standstill. Even minor inaccuracies can generate distrust, especially for a customer who is new to the fold or for a problem customer who will use any excuse to hold up a payment on his account.

Accordingly, your forms should make sense, and the information they present to your customer should not conflict with the information from any other form. For example, if you issue a credit memo for $50, that amount has to show up as a credit item on the customer’s next monthly statement. If it doesn’t, your customer will probably interpret it as an overcharge and may hold up payment on any outstanding balance until a new, accurate statement of account is generated. Worse yet, all subsequent statements may be nitpicked, with any error of any size potentially causing distrust, argument, or delay in payment.

Keep key records, like customer checks

![]() Although your computer does a fine job of churning out the forms used in your billing system, keeping your credit files up to snuff can involve some manual labor. Key records and important paperwork should be copied and placed in your paper credit file or scanned into your paperless credit file.

Although your computer does a fine job of churning out the forms used in your billing system, keeping your credit files up to snuff can involve some manual labor. Key records and important paperwork should be copied and placed in your paper credit file or scanned into your paperless credit file.

For example, a customer’s check contains a ton of valuable information. If at some point the customer stops paying on time, you can refer to the customer’s check for its name and address, the name and address of its bank, and its bank account number. If the check is dishonored, the amount of the check can constitute an admission that the balance is owed. (Who’d write a check if they didn’t owe money?)

Sidestepping billing discrepancies by putting everything in writing

An old expression, always applicable to billing practices, states, “It isn’t done if it isn’t in writing.” Everything in the billing system must be in writing. This is usually referred to as a paper trail. As a general rule, whoever has the best paper trail wins.

Going back to the example introduced earlier in this chapter of the $500 order for paper plates. The customer received the $500 shipment, but $100 of the product was damaged. Your contract places risk of loss on the customer, so under the terms of sale, it’s the customer’s responsibility to file a claim with the carrier.

But what if it’s determined that the damage was done before the goods left your warehouse and the carrier isn’t at fault? Now you owe your customer a $100 credit. For reasons outlined earlier in this chapter, the credit memo should be issued immediately, should specifically refer to the soiled plates, and should include the amount, be dated, and be promptly entered into your billing system. Both the $500 invoice and the $100 credit memo will appear on the customer’s monthly statement.

Now let’s add a complication. During the same billing period, the customer either took an unearned discount or otherwise failed to pay an invoice in full. For example, a prior shipment of plates for $500 resulted in a check for $400. As with the credit memo for money you’re crediting to your customer’s account, you must promptly prepare and process a debit memo showing that $100 shortage so your customer knows exactly where it stands. Your paperwork remains accurate and organized, and you can document every entry on the customer’s statement of account.

![]() Never include an item on your statement of account that can’t be fully documented. Unexplained items on statements are difficult to impossible to enforce and make your billing system appear disorganized. Your disorganization or lack of documentation will become a huge problem should a customer dispute its balance. As time passes, memories fade and you’ll have to rely on your paper trail.

Never include an item on your statement of account that can’t be fully documented. Unexplained items on statements are difficult to impossible to enforce and make your billing system appear disorganized. Your disorganization or lack of documentation will become a huge problem should a customer dispute its balance. As time passes, memories fade and you’ll have to rely on your paper trail.

Getting Bad Accounts off the Books: You Gotta Know When to Fold ’Em

Sometimes it makes sense to suspend sending statements to customers. If the customer is out of business or otherwise uncollectible, sending additional statements is often futile. Chapter 14 describes circumstances when it often makes sense to stop billing or collecting, and write off an account. For example, if the customer is out of business and mail is being returned, you can stop sending statements and mark the account as uncollectible. Save yourself the paper and postage. Billing an uncollectible account wastes both time and money.

If the customer has been turned over for collection, sending statements may cause confusion. During the collection process, collection agencies make demands for payment using their own letters, forms, and statements. If you send statements of account, that may confuse the customer about how much it owes and where to make payments. After you’ve hired a bill collector for an account, your collector will want to receive all payments on that account.

![]() If a debtor files for bankruptcy and the debt is being handled by the bankruptcy court or has been discharged, you may be in violation of the automatic stay (a court order that comes into immediate effect upon the filing of a bankruptcy action, forbidding collection activity against the debtor). You are in violation of the bankruptcy law if you continue to send notices to the debtor. Be sure to stop the notices, including any that are automatically generated by your computerized billing system. Your automated billing system should be set up to allow you to stop the issuance of any further statements to a customer. We discuss bankruptcy laws in Chapter 6.

If a debtor files for bankruptcy and the debt is being handled by the bankruptcy court or has been discharged, you may be in violation of the automatic stay (a court order that comes into immediate effect upon the filing of a bankruptcy action, forbidding collection activity against the debtor). You are in violation of the bankruptcy law if you continue to send notices to the debtor. Be sure to stop the notices, including any that are automatically generated by your computerized billing system. Your automated billing system should be set up to allow you to stop the issuance of any further statements to a customer. We discuss bankruptcy laws in Chapter 6.

After you write off a debt, you may report the amount to the IRS as a tax loss using form 1099-C. You must provide a copy of the 1099-C form to your debtor, and your debtor may be responsible to pay taxes on that amount as income. Your accounting department or financial professional can advise you about the timely filing of 1099 forms and steps to take if your debtor pays a debt that you’ve written off.

Training Your Staff in Billing Matters

The documents you collect through your billing system only benefit you if they are accurate. Errors, ambiguities, and omissions create confusion, and thus cause collection headaches. Even your best, most reliable customers will refuse to pay your invoices if they are confused about the numbers that appear on the documents you send.

For example, if your customer has a practice of taking discounts even past the end of the discount period, the customer will probably be confused by debit memos for unearned discounts and refuse to pay invoices until her confusion about discounts is straightened out. This is true even if the amount of the dispute is small. The culprit is often your own inconsistency. You’ve let the customer take unearned discounts in the past, and she doesn’t understand why you’re suddenly enforcing a line she’s completely forgotten. You could conceivably have $10,000 worth of invoices held up because of a few hundred dollars worth of debit memos. If you’re like most businesses, you can’t afford to have your accounts tied up over a few hundred dollars worth of credits that should be issued or debits that shouldn’t have been issued.

Train your credit and collections staff that accuracy and consistency are essential. The following sections give you some pointers in establishing procedures that will make your billing process go more smoothly.

![]() Any customer complaints should be flagged and immediately brought either to your attention or to the attention of someone authorized to quickly and efficiently resolve disputes (Chapter 9 covers disputes). The best way to keep accounts receivable money coming in the door when problems arise is to promptly pick up the phone and communicate with your customer.

Any customer complaints should be flagged and immediately brought either to your attention or to the attention of someone authorized to quickly and efficiently resolve disputes (Chapter 9 covers disputes). The best way to keep accounts receivable money coming in the door when problems arise is to promptly pick up the phone and communicate with your customer.

Inputting data accurately

Information is entered into your billing system by people. Inevitably, people make mistakes. The measure of a good billing system is how efficiently your staff recognizes and corrects mistakes, and makes prompt, courteous corrections to customer accounts backed up by documents such as credit and debit memos.

![]() When you’ve made a mistake, don’t underestimate the power that a little sticky note with a smiley face and a handwritten notation saying “Sorry for any inconvenience” has on a customer. Customers are people too.

When you’ve made a mistake, don’t underestimate the power that a little sticky note with a smiley face and a handwritten notation saying “Sorry for any inconvenience” has on a customer. Customers are people too.

Using the correct forms

“Why does my statement show a debit when I’m entitled to a credit for a return of merchandise?”

Sound familiar? Your data entry person grabbed the wrong form and issued a debit memo instead of a credit memo. You know the difference and your customer knows the difference, but perhaps your data entry staff needs a bit more training about what each form stands for and its role in the billing system.

The proper use of the forms you’ve implemented saves headaches as customers struggle to find excuses not to pay. For example, using an invoice as a debit memo and then marking it as a “Do not pay this invoice” form only confuses the customer. Instead, use a debit memo. You’ll effectively train your customers on how your system works by being consistent in using the correct forms.

Respecting confidential and sensitive data

Never forget that your files contain a great deal of sensitive data, including business account numbers, bank account numbers, Social Security numbers, and other sensitive customer data. If you’re in the medical business, your files may include confidential patient information.

![]() State and federal laws are in place to protect customers, so you need to have a system set up for the destruction of documents. Be aware of these state and federal laws and consult with your attorneys and accountants as to the systematic destruction of sensitive documents. Train staff members, including sales and administrative staff, about your company’s legal duties, and provide sufficient supervision to ensure that they’re protecting customer data. We summarize key laws in Chapter 6.

State and federal laws are in place to protect customers, so you need to have a system set up for the destruction of documents. Be aware of these state and federal laws and consult with your attorneys and accountants as to the systematic destruction of sensitive documents. Train staff members, including sales and administrative staff, about your company’s legal duties, and provide sufficient supervision to ensure that they’re protecting customer data. We summarize key laws in Chapter 6.