ONE OF THE lasting legacies of the Great Depression is the increased use of U.S. federal agencies to aid a wide variety of consumers including homeowners, farmers, agricultural interests, and students. One way that the agencies assist consumers is by reducing borrowing costs. Since 2000, there has been a tremendous increase in the issuance of agency debt. Fannie Mae, Freddie Mac, and the Federal Home Loan Banks have issued most of the new agency debt.

The agencies issue debt securities in the form of discount notes, which come due in less than one year; notes, which come due between one year and ten years; and bonds, which come due in more than ten years. If this sounds familiar, it's because Treasuries are issued in the same way. For clarity, we'll call all the debt securities issued by the agencies "agency bonds." This chapter discusses only agency bonds. The agencies also issue mortgage pass-through securities, which we'll discuss in the next chapter. The major agencies we'll discuss in this chapter are federal government owned or government-sponsored enterprises, popularly know as GSEs. GSEs are shareholder-owned corporations that the U.S. government regulates.

Agency bonds are extremely safe because they are either owned by the federal government, by agencies financially supported by the federal government, or agencies engaged in financial activities vital to the health of the country. Agency bonds are the safest bond investment after Treasury bonds. The Bond Market Association Web site, www.investinginbonds.com, has an excellent summary regarding the safety of agency bonds under the heading "About Government Bonds".

Most agency and GSE debt is not backed by the "full faith and credit" of the federal government, but investors generally treat the securities as if they had negligible credit risk. The markets believe the federal government would prevent an agency or GSE from defaulting on its debt because of its role in promoting public policy and because of the sheer size of the largest of the agencies. As a result, agency securities have an "implicit guarantee" and trade in a narrow spread to Treasuries. (Their yields are usually slightly higher than Treasuries with comparable maturities but move in similar patterns.) However, both the agencies themselves and the federal government continually emphasize that there is no legal obligation for the federal government to support the debt of the agencies in the event of an insolvency or default.

Although most agency bonds carry an AAA rating, you must still check the rating of the bond you're considering buying because there are exceptions. For example, although Fannie Mae's senior unsecured bonds have a rating of AAA, Standard & Poor's rates Fannie Mae's subordinated benchmark notes AA– and Moody's rates them as Aa2. And as of September 23, 2004, Standard & Poor's placed Fannie Mae's subordinated benchmark notes on negative credit watch.

The four largest issuers of agency bonds are:

Other agencies that issue or previously issued debt are Financing Corporation (FICO), Resolution Funding Corporation (REFCORP), Student Loan Marketing Association (Sallie Mae), Tennessee Valley Authority (TVA), and Federal Agricultural Mortgage Corporation (Farmer Mac).

Fannie Mae and Freddie Mac are GSEs regulated by the federal government. Fannie Mae was chartered in 1938, and Freddie Mac was chartered in 1970. Both of these GSEs assist low- and moderate-income families in buying homes by providing support and liquidity to the U.S. mortgage market. They do that by borrowing in the capital market (by selling bonds discussed in this chapter) and using the funds raised to purchase mortgages, mortgage securities, and other home loans from banks and other lenders. Fannie Mae and Freddie Mac are two of the largest issuers of bonds in the United States.

Fannie Mae. Fannie Mae sells a large variety of bonds. It generally issues bonds in a minimum purchase amount of $1,000 and in increments of $1,000. It issues a large number of its bonds pursuant to its global and benchmark notes programs. These programs are huge and international in scope and, as a result, the bonds are very liquid and trade easily at small spreads. In addition, Fannie Mae issues bonds called investment notes designed for the retail market and small investor. The investment notes are continuously issued and have a put feature that allows the estate of a holder of these notes to sell them back to Fannie Mae at face value. Despite the put feature, we prefer the global notes and benchmark notes to the investment notes because the benchmark notes and the global notes are more liquid so you get a better price if you sell them. In addition, the investment notes have shorter and more call provisions than either the global or the benchmark notes.

The Fannie Mae global notes and benchmark notes generally sell at a yield that is 20 to 25 basis points (one-fifth to one-quarter of 1 percent) above similar Treasury bonds for 2-year bonds, 25 to 30 basis points for 5-year bonds, and 30 to 35 basis points for 10-year bonds. These spreads can widen or tighten depending on market conditions.

Freddie Mac. Freddie Mac sells a large variety of bonds. It generally issues bonds in minimum purchase amounts of $1,000 or $2,000 and in increments of $1,000. It issues a particularly large amount of them pursuant to its reference notes and global bonds programs. The bonds issued pursuant to these programs are very liquid and, thus, trade easily at small spreads. Freddie Mac also issues Freddie notes. These are similar to the Fannie Mae investment notes in that they are designed for the retail investor and have a put feature. We prefer the reference notes and the global bonds to the Freddie notes for the same reasons we prefer the Fannie Mae benchmark notes and global bonds to the Fannie Mae investment notes. The Freddie Mac reference notes and global bonds generally sell at a yield that is 20 to 35 basis points above similar Treasury bonds (see the discussion of Fannie Mae global notes and benchmark notes).

The FCS was established in 1971. It is a nationwide system of borrower-owned banks that sell bonds to raise funds and then lend directly and indirectly to ranchers, farmers, and certain farm-related businesses. Banks in the system generally issue a variety of bonds with a minimum denomination of $5,000 and in $1,000 increments.

The Federal Home Loan Bank System (FHLB) was established in 1932 to revitalize the thrift industry during the Depression. The FHLB includes the twelve regional Federal Home Loan banks. The system's membership consists of private savings and loan banks, and they in turn own the twelve regional Federal Home Loan banks. These banks sell bonds in the capital market and lend the money raised to thrifts, commercial banks and credit unions, and savings and loan banks, which in turn lend it to home buyers as mortgage loans. The Federal Home Loan banks issue a variety of bonds generally in minimum amounts of $10,000, with increments of $5,000. Any bond issued in the system is a joint obligation of all twelve Federal Home Loan banks; thus, if there is default by one, the others are legally liable to cover it.

FICO is a government corporation of mixed ownership chartered by the Federal Home Loan Bank Board. It began in 1987 to finance the recapitalization of the Federal Savings and Loan Insurance Corporation (FSLIC) and to help create liquidity for it after insolvency threatened many savings and loan banks. Although FICO's borrowing authority was terminated in 1991, many of its $8 billion of bonds are still outstanding. To ensure payment of principal on FICO bonds, the agency has purchased enough zero-coupon U.S. government-guaranteed securities to make total principal payable maturities approximately equal to the face value on FICO obligations.

All the FICO and REFCORP bonds that we see in the market are zero-coupon bonds. We purchased them in small and large pieces. We buy these bonds for our tax-sheltered retirement accounts so that the phantom taxable income they throw off will not affect us.

REFCORP is another mixed-ownership GSE. It was established in 1989 to fund the Resolution Trust Corporation. It provided financing to bail out the large number of thrifts that failed in the 1980s. Although the bonds issued by REFCORP are not direct obligations of the U.S. government, the U.S. Treasury guarantees the interest, and Treasury bonds secure the principal. Thus, there is little if any default risk on these bonds. REFCORP originally brought to market 30− and 40-year bond issues. Many of these bonds were stripped to create zero-coupon bonds. These zero-coupon bonds are what are generally available in the secondary market to retail investors. They are sometimes found in pieces as small as $1,000.

The TVA was created in 1933 to develop the resources of the Tennessee Valley and its adjacent areas. The TVA is both wholly owned and an agency of the U.S. government. Despite this ownership, the U.S. government does not back TVA bonds. The TVA pays the principal and interest of the bonds only from the proceeds of its power program. The TVA issues a variety of bonds. Many are called "globals," which are retail-oriented electro notes. Both are available in the secondary market. It issues these bonds in minimum amounts of $1,000 and in $1,000 increments.

Farmer Mac is a GSE established in 1988 to promote liquidity for agricultural real estate and rural housing loans. It does this by buying loans from lenders and creating pools of these loans, against which it issues bonds that investors purchase. Farmer Mac issues a variety of bonds in minimum amounts of $1,000 and in $1,000 increments.

Sallie Mae was created by Congress in 1972. It was a federally chartered GSE established to provide liquidity for banks and other lenders that originate guaranteed student loans. As a result of the federal government becoming more involved in issuing student loans, Sallie Mae was restructured in 1997 and phased out its GSE status by the end of 2004, ending its ties to the federal government.

Although most agency bonds are not well known, they are very attractive investments because of their high credit rating and yields, which are higher than Treasuries. Agency bonds are extremely safe and have negligible credit risk because the federal government is unlikely to let one of its sponsored enterprises default. Investors can use agency bonds as collateral for loans.

Although there is no significant liquidity or tax risk associated with agency bonds, they are subject to possible event and political risk. In terms of political risk, Congress has periodically become concerned about the mushrooming amount of agency bonds and has sought to curtail the amount of agency lending.

After an accounting scandel in 2005 rocked Freddie Mac and Fannie Mae, both agencies came under close ongoing scrutiny.

Most agency coupon bonds have call provisions. However, agency zero-coupon bonds generally don't have call provisions. These call provisions for the agency coupon bonds constitute the major risk of agency bonds. Many of these calls are extremely short; for example, a three-month call is not unusual. Thus, even if your agency bond has a good return, it can be called away before you have a chance to fully benefit from it. A short call subjects you to reinvestment risk because agencies will call in the bonds at times when interest rates are declining. Reinvestment risk means that if your bond gets called and you get your money back, you may have to reinvest at lower interest rates. If you buy a 20-year or 30-year agency bond with a one-year call, you're subject to market risk (that is, inflation) should interest rates go up (that's because the value of your long-term bond will go down) and reinvestment risk if interest rates go down, because your bond may be called. You can avoid this risk by not buying long-term agency bonds with short calls. However, you might buy shorter maturity issues with longer call protection. For example, you might buy 5-year agency bonds with two-year call protection.

All agency bonds are subject to federal income taxation. However, the following agency bonds may not be subject to state and local income taxation:

Farm Credit System

Federal Home Loan Banks

Financing Corporation (FICO)

Resolution Funding Corporation (REFCORP)

Tennessee Valley Authority (TVA)

The following agency securities are subject to state and local income taxation:

Fannie Mae

Freddie Mac

Bonds issued by Fannie Mae, Freddie Mac, Federal Home Loan Banks, and Farm Credit System are quite liquid and, as such, are easy to buy and sell, which results in lower trading transaction costs. We particularly like noncallable agency zero-coupon bonds for your tax-sheltered retirement accounts. For example, in 1997, the yield on 15-year agency zeros was 7.5 percent while the overall stock market was racking up 20 percent per year gains. Bond aficionados that we are, we ignored the techs and tucked into our IRAs an assortment of noncallable agency zeros with a 7.5 percent yield. These bonds doubled in less than ten years without any further action or monitoring on our part as well as without any need to reinvest the coupons. In essence, we bought a risk-free investment that was guaranteed to double in less than ten years while the stock market boomed and then busted. It doesn't sound as sexy as a new, high-tech IPO, but it sure has proved rewarding for our clients and for us.

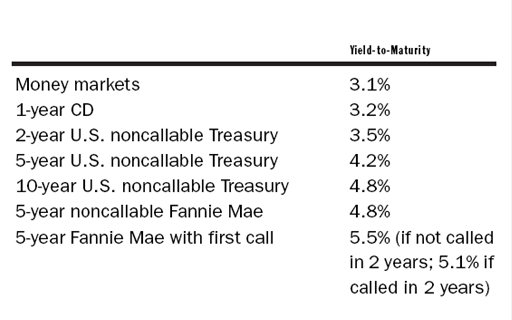

Although early call features are a risk, agency bonds of five years or less can also present an opportunity, especially in an atmosphere of rising interest rates. If agency bonds with short calls have a higher yield, consider buying them. Figure 8.1 presents the interest rates in September 2001 and the plan that a major brokerage firm presented to us.

"Even if the agency bond is called away in two years," the firm wrote, "it will have yielded 5.1 percent, which is 160 basis points (1.6 percent) higher than a comparable U.S. Treasury, which yields 3.5 percent. If the agency bond is not called and is held to maturity, it will yield 5.5 percent, versus 4.2 percent for a comparable U.S. Treasury."

We believe that if the yield difference between an agency and a Treasury is only 20 basis points (0.2 percent), you should consider buying the Treasury for your taxable account because of its greater call protection, liquidity, and safety—particularly if you can advantageously use the state tax exemption. If you can earn more than 50 basis points (0.5 percent) on an agency bond compared to a Treasury of similar maturity, we believe the agency may be more attractive if it has adequate call protection.

Sources of additional information. Excellent bond-specific Web sites are www.fhlb.com, www.freddiemac.com, www.fanniemae.com, and www.tva.com.

How much more yield, if any, am I getting on this callable bond versus a noncallable bond?

What is the reinvestment risk on this bond if it is called?

What is this bond rated? (An issuer may put out subordinated debt that has a rating below AAA.)

Does this bond have the state-tax exemption? (If you live in a high-tax state, this is critical.)

How does this bond compare in terms of after-tax yield to an equivalent Treasury bond in my tax bracket?