A Workbook on Transition Planning for the Family Business

The process of family transition planning requires

- time to develop;

- the involvement of the entire family (both members working in the business and those who are not) and consideration for the needs of all;

- a periodic revisiting, updating, and revising of the plan reflecting changed circumstances;

- consultation with management, consultants (bankers, lawyers, accountants, insurance agents, etc.), and advisors.

Each family business has its own style, its own unique set of circumstances to consider, its own personal and psychological dynamics, and its own goals and objectives. However, one common thread that is part of any family fabric is that different family members will have different perceptions and interpretations of the same events, conversations, and circumstances. This can lead to misunderstandings, or worse.

To ensure that these different perspectives remain in concert with each other, a written family business transition plan is essential. The planning that goes into composing a transition plan is invaluable in preserving the family firm.

After an overview of the family business transition planning process, segments of different plans from many family businesses are presented. Names and details have been changed to preserve anonymity and confidentiality. They have been included to illustrate some of the outstanding themes underlying the planning process. Although the various segments appear in a sequence, this is not meant to imply that they should be treated in this order.

Further, it is advisable to utilize an independent facilitator to assist in developing the transition plan. Family members will feel freer to voice their ideas and the facilitator will increase the opportunity for unpopular positions to be heard. This workbook assumes that a facilitator is in place.

The various sections include the following:

- The Family Business Transition Planning Process

- Family and Business Values

- Current Family Assets and Estate

- The Current Status in the Event of Death or Disability

- The Process of Choosing a Successor

- Working in the Family Firm

- Business Maintenance and Growth

- The Monitoring Process

A. The Family Business Transition Planning Process

The following is an outline of the planning process. Not all steps are needed, their order is not sacrosanct, and frequently steps are simultaneously engaged.

1. A Brief Meeting of All Family Members

This initial meeting consists of all family members, both those working in the business and those who are not. It includes spouses, as well as children old enough to be thought of as potential family business employees. This meeting provides those present the opportunity to ask questions about the process, voice whatever doubts they have, and share opinions. It also offers the family an opportunity to size up the facilitator.

2. Interviews With All Family Members

These individual interviews last approximately an hour and allow each individual to share personal and professional goals, views of the business as a family affair, concerns about being part of a family with its own business, and so on. These interviews are both confidential and anonymous (i.e., what is revealed is not shared or mentioned to others). These interviews have proven to be crucial in determining the fate of the planning process. For example, an heir apparent revealed that he really did not want to be in the business. In another, a family member revealed that her spouse really wanted to be part of the family business but was too afraid of her father to ask.

The information gathered is used by the facilitator to guide the process. For example, in the situation where the heir apparent wanted to leave the business, the facilitator supported the individual in announcing his departure and helped the father accept his decision, but the facilitator never revealed what was said in the interview.

3. A Family Retreat

A family retreat is convened to review a variety of topics. A brief written summary highlighting the major themes in the interviews is presented to the family members. The next steps in the process are explained and questions are answered. The majority of the family retreat is devoted to discussing the major themes of succession planning.

Frequently the retreat is preceded and followed by further meetings (e.g., with both parents together, with offspring and their spouses). The reasons are varied. For example, the content of parental meetings is often a preliminary discussion of the major themes of succession, particularly estate considerations. Spousal meetings range from an insistence that “their mate become president or else” to a hushed announcement of a pending divorce that will affect estate planning. These additional meetings may be initiated by the facilitator or by family members.

4. Interviews With Senior Managers

A brief senior management meeting (similar to the all-family meeting) precedes individual manager interviews, which are also confidential and anonymous and serve several objectives. They present a picture of the company (its strengths and weaknesses, positives and negatives) that is useful in planning for the choice and development of a successor. For example, a growing and creative design firm had few management systems in place and consequently was losing money. Of the two potential successors, one was a very structured and thoughtful young man, while his brother shared the same creative flair his father possessed. The father favored the one who resembled him. However, it was clear that the son who possessed a goal-oriented and structured vision of the firm’s future was the type of candidate that was needed at that time by the business.

Areas of concern or neglect revealed in these meetings can become developmental and learning opportunities for the successor. They can also serve as an assessment of the successor’s abilities. Further, the information obtained yields a good picture of the skills and abilities the successor has or must acquire (e.g., through advanced formal education, networking opportunities).

An additional aid in gathering this information is a company-wide web-based survey that reveals data on a firm’s strategy, culture, and structure.

5. Assessment of Potential Successors

Whether there is only one or several potential successors, the assessment process is a necessity. It is one way of obtaining an impartial picture of any candidate. It takes the following form:

- The administration of standard management assessment instruments to each candidate

- If the successor(s) has been working in the firm, the administration of standard 360-degree feedback instruments in which peers and supervisors supply their (confidential and anonymous) opinions about the candidate’s strengths and weaknesses

- In the situation where several candidates are seen as equally strong, a written strategic plan composed by each candidate and evaluated by outside executives

The facilitator prepares a written report for each candidate and discusses it with him or her in personal one-on-one interviews. With the permission of the individual, this information is then shared with the president. The candidates are present at this meeting. Sometimes a decision is made at this point regarding the successor.

A developmental plan for the heir apparent is created and a schedule for his or her progress is planned. This involves the president and his management team and may require several meetings to produce. Quite often a coach is assigned to the successor as well as to other family members in the business.

6. Estate Planning

A primary focus of the transition process is ensuring that legal and tax considerations are planned for and discussed with family members. Accordingly, parents are urged to meet with the family’s lawyer and accountant so that the financial welfare of the family is preserved. Some of the issues involve formulating a beneficial tax framework, providing for a surviving spouse, ensuring that the business remains in a strong competitive position, agreeing on what happens in the event of the president’s death or disability before succession occurs, along with many other considerations that your lawyer and accountant will bring to your attention.

An effective estate plan requires a thorough knowledge of your financial resources and needs. Some of the services your lawyer and accountant should provide include

- preparing an inventory of your assets at current values classified in accordance with the way the assets are titled,

- computing the amount of the estate tax payable based on the present ownership of assets,

- determining the liquidity needs of the estate and the cash flow needed to provide for the continuing living expenses and special needs of the family,

- projecting the results of any changes recommended in the estate plan.

Some of the documents that should be considered in every estate plan are wills, revocable trusts, durable powers of attorney, living wills, and designation of a health care surrogate.

7. A Meeting of the Entire Family

The family is gathered not only to announce the choice of a successor but to review and discuss the results of the written succession plan. Pertinent aspects of the estate planning process are also presented. This meeting frequently involves the presence of your lawyer and accountant to explain the financial considerations and to answer any questions that family members might have.

8. A Management Meeting

Management becomes part of the succession process in that they are the ones who quite often participate in the training and development of the successor and the siblings who are also in the business. This meeting is devoted to announcing the process to the managers not involved in its planning and to those supervisors who might be involved in the training. A common theme in these meetings is succession planning for managers themselves.

9. Follow-Up

Subsequent consultation can take many forms, and for a variety of different reasons. The following represents only a sampling of additional issues that arise in the succession process:

- Managing development and training

- Managing succession planning

- Engaging in strategic planning and company-wide goal setting

- Developing a board of directors, if one does not exist

- Facilitating a board of directors retreat

Many of these issues are ones most organizations entertain as a means of enhancing their growth. What is not as plainly acknowledged is that these very same activities ensure the success of the succession plan. When a business fails after succession has occurred, the all-too-frequent moan is, “If only the old man had remained at the helm!” However, what is not recognized is that maybe the founder’s way of doing business was imposed on the successor, and maybe it was a legacy that should have been laid to rest.

B. Family and Business Values

This section contains joint statements by the parents about the values they want reflected in the transition process and the intent of the succession planning document. The tenor of these statements reflects the immediate concerns and issues the family is addressing in developing the succession plan. Each numbered entry is from a separate family business. After the statements are presented, a questionnaire is provided to you and your spouse as a means of thinking about the values you would like to guide the transition.

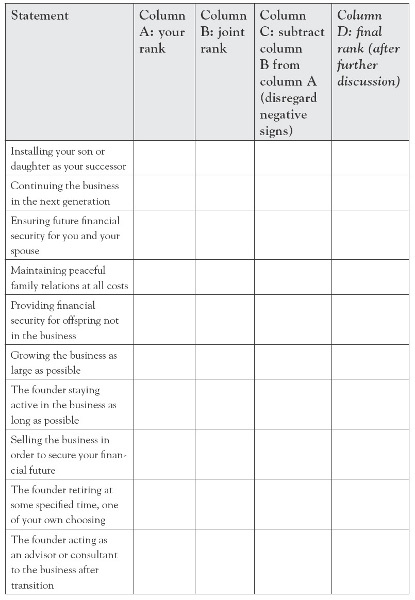

Your Goals for the Future of Your Business

For the Founder and Spouse

As a way of helping you clarify the values and goals you have for your family business, independently rank order the following statements in terms of what you feel is important to you and your future. When you each have finished, compare your rankings, discuss them, and then agree on one set of rankings. After you have arrived at a united set, enter both your individual rankings and your joint ranking in the indicated columns.

Subtract your rankings in column B from column A and enter this value in column C. Disregard the negative sign. For example, if column B is ranked as 8 and column A is 6, subtracting column B from column A gives you a –2. Disregard the minus sign and just take the absolute value—that is, 2. Add all the values in column C, divide by 13, and enter this value at the bottom of column C.

Note the extent of the discrepancy between your original individual rankings and your joint set. Discuss what this may mean in terms of how you as a couple view your future. Then discuss with your spouse a final ranking and include it in column D.

C. Current Family Assets and Estate

Many parents are reluctant to share information about their assets and estate with their children. However, not informing offspring and family members results in more down-the-road dissension, misunderstandings, and family lawsuits than otherwise. In particular, the business itself can become compromised by family members who become disgruntled with estate provisions at the reading of the will. In providing all family members with this information up front, potential problems can be raised and resolved by parents while they are still living.

In addition, knowledge of inheritance allows family members to plan their financial future more efficiently and securely.

Some important considerations regarding family assets and estates are represented in the following questions:

- What impact will estate taxes have on my family and business?

- Does everyone in my family know what will occur (e.g., the results of buy/sell agreements) in the case of any type of future event (e.g., death, serious illness)?

- What will be my personal tax status, as well as that of all family members, in the context of different scenarios (e.g., death, succession, buyout, illness)?

- Has due consideration from a tax and legal standpoint been given to the type of business form that is best suited for my company’s and family’s needs (e.g., S corporation)?

- Have appropriate gift and estate tax planning been instituted so as to reduce the future tax burden (e.g., outright sale, gift, trusts, stock redemption, recapitalization)?

- Has my tax planning included the consideration of tax-advantaged investments? And in general, do I have a good overall investment strategy?

D. The Current Status in the Event of Death or Disability

A clear statement regarding the disposition of the business in the event of the founder’s death or disability before succession is essential to the maintenance of the business. Your lawyers, accountants, and insurance agents should contribute to this section to ensure accuracy. The expected tax consequences (approximated) at an owner’s death might also be included, as well as the details of provisions taken against the tax liability.

E. The Process of Choosing a Successor

There are generally three types of succession situations:

- One in which succession is in the near term and a decision has to be made soon. One or more candidates might be available.

- One in which there is really only one potential candidate.

- One in which succession is not immediate, but where the focus is on the process of selection, on how the decision should be made down the road. There may be one or multiple potential successors.

The more specific the plan is regarding people, dates, training, and so on the less chance there is for future disagreements. Many times families do not feel they can be specific because future circumstances might change. However, a plan that will not take effect until well down the road can be periodically updated, and should be. The plan also includes provisions for how ownership is to be transferred.

A good plan should also include what role the parent, the previous president, will play in the future once succession occurs.

Keep in mind the following questions as you consider choosing a successor:

- On what basis will a successor be chosen? (Suggestion: the criteria should be as objective and impartial as possible.)

- What training, education, and experience should the successor have? If these are not now present in the successor’s history, when and how will they occur? (Suggestion: develop a calendar of specific events.)

- When will succession occur (i.e., on what date will the successor become president and assume full responsibility for running the firm)? Are there specific performance criteria that have to be met in order for succession to occur? If so, what are they?

- What will be the future role of the current president after succession? Be specific. (Suggestion: unless this is clearly defined, trouble will occur!)

- Has the management team been involved in the succession process? Have they been informed of and contributed to the decisions surrounding succession?

- Have all family members been informed about the decisions regarding succession? What have been their reactions? And if there have been disagreements about the selection, what has been done about them?

F. Working in the Family Firm

A family business is not simply a business—in fact, many businesses are not simply businesses, but that is another story. However, the presence of family members in the business can be or become at odds with the owner’s perception of the business. In particular, this crops up when the performance of the family member is in question, when the expectations of the family member are at the opposite pole to that of the founder, and when their respective definitions of the purposes of the business differ.

One way of avoiding this is to determine early on what is expected of family members entering the firm, what they can and cannot expect, and so on.

Some considerations regarding employment in the family business include the following:

- Is there an established set of criteria for including family members in the business? What are they?

- If family members enter the business at different time periods, how has the issue of “sweat equity” been addressed?

- What plans are there for including in-laws and other relatives (other than siblings) in the business?

- Given that the families of siblings may differ in size and in the number of offspring entering the business, what provisions have been made for how equity is to be distributed?

- What if there are no available or appropriate positions in the firm and family members want to enter the firm—what is the policy regarding this situation?

- Is there a compensation policy for family members in the business that has been discussed and agreed on? A related issue is the compensation and perks nonfamily members derive from the business.

G. Business Maintenance and Growth

Among the major considerations in succession planning is whether the business will or can grow under the successor(s). Among the antidotes to family business failures are the presence of an oversight committee (an advisory group or a board of directors) and a succession plan for the nonfamily members. The need for an oversight committee is perhaps self-evident, but the focus on a management succession plan for nonfamily members may not be. Consider the fact that many of the current management people have been at the firm as long as the founder and are approximately his age. Unless their succession is as well orchestrated as the founder’s, the new president either will be burdened with a team not of his own making or will face a management talent vacuum.

An aid in assessing the succession issues of management is to build a “succession chart.” The basic questions underlying its creation are based on expected changes (e.g., growth, ownership succession, increased competition). The questions include the following:

- Is every significant position in the company adequately filled now?

- Are there adequate successors for each of these positions (either in place or in training) such that they would be available when and as needed?

The chart lists each position by department, the person currently holding that position (including his or her training, experience, age, longevity, etc.), a “grade” for current performance, and a grade for future expected performance in light of the anticipated changes. Also included on the chart are the names of those who would or could be successors and the appropriate grades reflecting their training and experience, the additional training they require, and so on.

H. The Monitoring Process

An easily overlooked aspect of succession planning is the failure to update information on a regular basis. This information might include the latest estimate of the value of the estate, a change in the structure of management, a redirection of the firm’s strategy, and so on. Usually this section of the succession plan includes a statement regarding the frequency of updates, who should attend, and the information that might be made available. Frequently one statement conveys the message: