Chapter 9

Business Methods

9.1 Introduction

The purpose of this chapter is to discuss selected accounting and business procedures that are commonly utilized in the conduct of a construction business. While the popular conception of construction contracting is visualized as pouring concrete and erecting structural steel, there is far more to a construction business than the contractor's construction operations. The business aspects of operating a construction company are of critical importance to the success and continuance of the enterprise. While it is certainly true that the owners and managers in a construction firm are vitally concerned with the field operations conducted in the performance of the contracts the company has entered, it is also true that the financial, business, and accounting functions which are performed by the company home office are an indispensable component of the successful operation of the construction company.

9.2 Financial Records

The failure of many otherwise well-managed construction companies is frequently caused by the lack of accurate, detailed, and timely information concerning all aspects of the company's financial affairs. Financial records of several different kinds absolutely must be maintained to serve a number of business and management purposes in the company. This, in turn, means that company management must have established a structure for defining the records and documents that must be developed, maintained, and properly stored, as well as a system of policies and procedures for the business operations of the company. In addition, of course, people having the requisite talents and skills must physically build, and operate, and maintain this financial structure and its documentation system.

One of the most basic and important reasons why construction contractors, like other businessmen, must keep accurate records is that many such records are required by law. An assortment of governmental agencies require data pertaining to taxes, payrolls, and other company financial information, along with a structure and a system of accounts to serve the purpose. Additionally, the contractor's financial records must provide the basis for financial statements and reports which are required for the construction firm's interaction with owners, bankers and other lenders, as well as sureties, insurance companies, public agencies, and others.

Beyond these considerations lies the imperative of the contractor having and maintaining a financial structure and record-keeping structure to serve the purposes of effective company management. The contractor's accounting system must serve to effectively and in timely fashion provide the information necessary to assist company management in controlling company operations and in utilizing its available capital to the greatest possible advantage. Without proper records, and the structure and policies for developing and maintaining these records, it is impossible for a contractor to establish and maintain a solid financial base, or to estimate construction costs accurately, or to control costs on current projects, or to keep the company in a fluid cash position, or to be able to make sound judgments concerning the acquisition of equipment, or to perform the numerous and varied additional functions associated with the financial management of the business enterprise.

The functions of a construction company's accounting system are not limited merely to producing and maintaining financial information and keeping records. Although such information is basic and essential to the conduct of company operations, it is also necessary for company management to analyze and summarize this data in order that it can be used to best effect. It can be said that the success of the entire process, and ultimately the success of the company itself, absolutely depend on the continuous generation, maintenance, and analysis of financial information that is critical to the successful operation and management of the company. The methods that are employed, the information generated, and the use that is made of this information in this process are the subject of the remainder of this chapter.

9.3 Accounting Methods

Although the details of record keeping vary considerably among construction firms, there is a basic accounting logic and a set of fundamental accounting procedures that are common to companies in the construction industry. The primary basis of a contractor's accounting system centers on the determination of income and expense from each of its construction projects and the cost of the operations of its office staff and management. That is, the performance of each construction project is treated as a separate profit center. In an accounting sense, a profit center is any group of associated activities whose profit or loss performance is separately measured and analyzed.

In a construction company, the original estimate of costs pertaining to each contracted construction project becomes the basis for a budget for that project. As costs are incurred on the project, they are accounted for and are charged against the project activities or work items to which they pertain. Cost summaries and reports are regularly generated throughout the life of a project, and costs incurred are compared to the project budget. Management analysis follows and forms the basis for management action to assure insofar as possible that the project will be completed within the budget. Figure 9.1 illustrates the cycle of cost estimating, cost accounting, and cost control, and the record-keeping functions that accompany.

Figure 9.1 The Cycle of Cost Estimating, Cost Accounting, and Cost Control

It is customary that the keeping of most of a contractor's business accounts be concentrated in the home office. However, on large projects and on some cost-plus contracts, a subsidiary set of accounts is frequently maintained in a field office where the record keeping pertaining to that project is accomplished. In this process however, the controlling accounts or master accounts for such projects are incorporated into a master set of accounting records that are maintained in the contractor's central office.

The two basic accounting methods employed by contractors in the conduct of their business are the cash method and the accrual method. In the cash method, income is taken into account only when cash is actually received, and expense is taken into account only when cash is actually expended. The cash method is a simple and straightforward form of income recognition, and no attempt is made in this method to match individual revenue payments received with the accompanying expenses.

The cash accounting method is used principally by small businesses, nonprofit organizations, and by some professional people for their personal records. Many small construction contractors use the cash method because of its simplicity, and because of the fact that tax liability for contract profits is recognized only when payment has actually been received. If a construction company performs only small projects, and maintains little or no materials inventory, and owns no capital equipment of consequence, the cash method is usually adequate.

However, for most construction companies the cash method does not work to the advantage of the contractor. For example, the cash method of accounting does not recognize depreciation of equipment and other capital assets because depreciation involves no recognition of cash income or outgo. Additionally, and importantly, income that has been earned but not received and expenses that have been incurred but not paid as of the end of a reporting period are not recorded or reflected in the company records in the cash method of accounting. An income statement, which is a summary document showing the company's revenue and expenses for a certain period of time, with profit or loss expressed as the difference between the expenses and revenue that is prepared on a cash accounting basis, will not present a realistic indication of true profit or loss for the company.

Similarly, a balance sheet, which is a summary of the company's assets, liabilities, and net worth at a certain point in time that does not reflect income earned but not yet paid and expenses incurred but not yet paid, does not accurately reflect the company's true financial condition. Income statements and balance sheets absent this information are therefore of limited value to management in assessing the financial condition of the company, and are entirely inadequate for use by lenders, sureties, and others outside the company who have an interest in a depiction of the company's financial position.

The accrual method is the second basic accounting procedure, and is the one most commonly used by all but the smallest construction companies. Under the accrual method of accounting, income is actually taken into account in the fiscal period during which it is earned, regardless of whether payment has actually been received. Similarly, items of expense are entered into the accounts as the expenses are incurred, whether or not they have actually been paid during the reporting period. The accrual method of accounting and income recognition is also more complicated, because by this method a connection is maintained on a continuous basis between the revenues earned and the associated expenses. The accrual accounting method requires a more elaborate system of accounting procedures and records. However, the accrual method is generally accepted as the accounting method that provides the most accurate and realistic portrayal of the financial condition of a business enterprise at any moment in time.

9.4 Accounting for Long-Term Contracts

A long-term contract is defined for tax purposes as one that is not completed within the taxable year in which the contract was formed. Tax codes mandate that one of three methods of accounting must be applied by contractors to their long-term construction contracts: the percentage-of-completion method; the percentage-of-completion capitalized cost method; or the completed-contract method. The three methods differ in the manner in which costs and expenses are matched to project revenue; they also differ in the identification of the period in which the income from a project is taken into account. The basic elements of each of these procedures will be discussed in the sections that follow.

9.5 Percentage-of-Completion Method

The percentage-of-completion method recognizes income and expenses from long-term projects as the work on the project advances. Thus, the profit is distributed and taxes are paid over each of the fiscal years during which the construction project is underway. This method has the advantage of recognizing project income periodically on a current yearly basis, rather than awaiting a summary of income and expenses until projects are completed.

Under this method, gross project income is recognized in accord with the percentage of the project that has been completed during a given fiscal year. The percentage which is used in this regard is the ratio of project costs incurred during the fiscal year to the total estimated contract cost, including any revised amounts (as from change orders), to complete the work. Applying this percentage of completion to the total contract price and then deducting the applicable project costs incurred to this point yields the net project income or loss for the fiscal year involved. The major weakness of this procedure is its dependency on estimates of costs that will be incurred to complete the work, a value that can be subject to considerable uncertainty at times.

9.6 Percentage-of-Completion Capitalized Cost Method

An alternative to the percentage-of-completion method of reporting income from long-term construction projects is the percentage-of-completion capitalized cost procedure. When this method is used, 90 percent of the revenues and expenses for the contract are accounted for using the percentage-of-completion method as described in the preceding section. The remaining 10 percent of the project costs are taken into account using the completed-contract method, which will be discussed in the following section. Thus, it can be seen that the percentage-of-completion capitalized cost method of accounting is a hybrid between the percentage-of-completion method and the completed-contract accounting methods. There are regulations in the tax code that prescribe the conditions pertaining to the contractor's use of this accounting method.

9.7 Completed-Contract Method

The completed-contract method of accounting recognizes project income and expenses only after the completion of the construction project. When this accounting method is employed, project costs are accumulated during construction, using what is referred to as extended-period cost capitalization, meaning that construction costs are capitalized over the duration of the project. The scope of contract costs that must be capitalized includes not only the costs directly related to the project but also indirect costs (overhead costs) that are attributable to the project. Costs such as general and administrative expenses and interest expense related to the performance of the contract are also included in the costs that must be capitalized.

By definition, the use of the completed-contract method of accounting requires clear delineation of project completion. What actually constitutes the completion of a contract for income-reporting purposes has been the subject of varying interpretations by the courts. Present practice tends largely to establish completion as having taken place when all of the work has been finalized and accepted by the owner. However, other interpretations have held that a contract is complete when the point of “substantial completion” has been reached.

No matter how the completion of the project is defined, however, the tax code stipulates that the completion of a contract may not be delayed by the contractor if the principal purpose is to defer federal income tax and/or other taxes. Additionally, federal tax regulations apply definitions and restrictions with regard to when and in what manner a contractor may use the completed-contract method.

The completed-contract method can be advantageous when, on long-term contracts, the contractor cannot accurately predict the economic results of its future contract performance. Frequently, project uncertainties preclude the making of accurate estimates of profits to be earned. Another advantage of the completed-contract method is the fact that payment of income taxes is deferral until the contract has been completed and final payment has been collected. By the same token, however, recognition of losses from the performance of a project is also deferred.

A disadvantage of the completed-contract method is that it does not reflect current performance for long-term contracts, and may result in irregular recognition of income. In some instances, this may result in greater income tax liabilities. Another potential disadvantage of this accounting method is that the year of completion of a project can be subject to considerable uncertainty if the end of the project coincides with the end of the accounting period, or especially if there are disputed claims remaining unsettled at the end of that year.

9.8 Financial Statements

At intervals of time called accounting periods, a determination can be made of the financial condition of a business enterprise. Accounting periods can be of variable length, such as one month, one quarter, or one year. The length of the accounting period is determined by company management policy, by management needs for this information, and by standard accounting practice, as well as by the need of external agencies to be informed concerning company financial strength.

Accounts are closed (summarized) at the end of each accounting period, and relevant statements are prepared that depict the financial position of the company at that time. Several forms of financial statements are typically derived from the company books of account. It is the purpose of such statements to group together and organize significant facts in a manner that will enable the person reading them to form an accurate judgment concerning some aspect of the company operation, such as the overall financial condition of the organization, or the profit-loss results of its operations. As would be expected, much of the usage of a company's financial statements is made by company management itself. These reports are invaluable for determining current status, as well as for the advance planning of company operations. Additionally, these documents reflect the company's borrowing capacity and bonding capacity. In addition, they provide a great deal of information concerning company policies with respect to elements of company operation such as purchasing, equipment ownership, and office overhead.

Additionally, these financial statements serve many important functions with respect to a number of external agencies that have an interest in the company and need this information. Bankers, sureties, insurance companies, equipment dealers, credit-reporting agencies, and clients and potential clients of the construction firm are all concerned with the contractor's financial status and profit experience. Stockholders, partners, and others having a proprietary interest in the company and its operations use these statements to obtain information concerning both the company's financial condition and the status of their investment. The two financial statements that are of primary importance are the income statement and the balance sheet. Each will be defined and discussed in the following sections.

9.9 The Income Statement

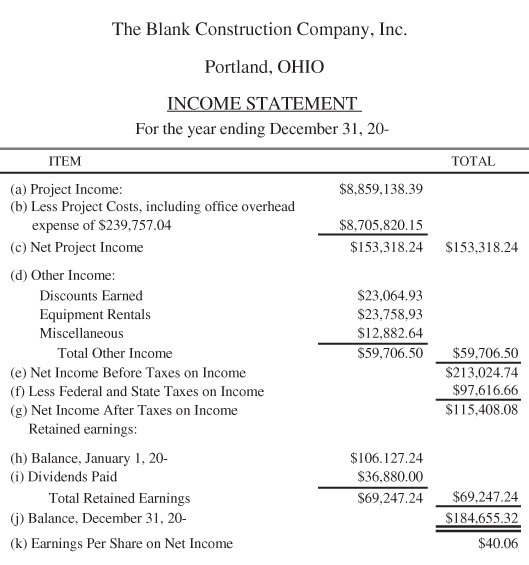

The income statement is an abstract of the nature and amounts of the company's income and expense for a given period of time, usually a quarter or full fiscal year. This document may also be known by the following terms: profit and loss statement, statement of earnings, statement of loss and gain, income sheet, summary of income and expense, profit and loss summary, statement of operations, and operating statement. This statement shows the profit or loss as the difference between the income (revenue) received and the expenses paid out during the period. Figure 9.2 is an example of an income statement for the Blank Construction Company, Inc., for the fiscal year ending December 31, 20—. The following paragraphs, keyed to the lowercase letters in parentheses as they appear in Figure 9.1, explain the various items.

Figure 9.2 Income Statement for the Blank Company

- This statement has been prepared on a completed-contract basis.

Project income is the total contract value of all projects completed during the period covered by the statement.

The total is obtained from a supporting schedule that shows the income figures for each completed project.

- Project costs include all materials, labor, equipment, subcontracts, project overhead, and other expenses that have been charged to the completed projects.

A supporting schedule of job costs lists these expenses for the individual projects.

Included with job costs is the general overhead expense that has been allocated to the completed projects.

General overhead is periodically distributed among the various projects in proportion to the costs incurred by those projects during the period.

- Subtracting project costs from project income yields net project income for the statement period.

- Other income lists the net income received from other sources.

- Total net income before taxes is the amount realized from all operations during the statement period.

- Net income after taxes is the amount available for company expansion or for distribution to stockholders.

- This sum is the earnings accumulated as of the start of the statement period.

A corporation can retain its earnings for business purposes or distribute them as dividends to the stockholders.

However, there is an accumulated-earnings tax that is a penalty tax applicable to corporate earnings which are accumulated for the purpose of avoiding income tax to its shareholders by permitting profits to accumulate in the corporation.

The allowable amount of retained earnings accumulation for use in meeting business needs, and the tax rate applicable to amounts exceeding this sum, are determined by the tax code.

- Dividends paid represent distribution of earnings made to stockholders in the form of dividends on common stock during the statement period.

This construction company has 4610 shares of common stock outstanding. A dividend of $8 per share was declared and paid during the fiscal year just ended.

- The balance represents the total retained earnings of the corporation through the end of the report period.

- In a corporate form of business, it is usual for the income statement to show net earnings for the year (after taxes) per share of outstanding stock.

It should be recognized that an income statement has several limitations. Concentrating as it does on past events, the income statement reports only the company's profit or loss experience during the reporting period. It does not show the present overall financial condition of the firm. Additionally, it should be understood that in the highly competitive and unpredictable construction industry, the profit or loss reported on the income statement at any point in time, is not always indicative of the management quality of the company.

9.10 The Balance Sheet

The balance sheet presents a summary of the assets, liabilities, and net worth of the company at a particular point in time. Balance sheets are commonly prepared at the close of business on the final day of a fiscal year, but can be prepared at any time to meet the needs of company management or an external entity. Balance sheets are universally used to describe the financial condition of business concerns of all kinds.

The basic balance sheet equation may be stated as follows: Assets = Liabilities + Net Worth. The balance sheet presents in analytical form all assets, including company-owned property, or interests in property, and the balancing claims of stockholders or others against this property. The foregoing equation expresses the equality of assets to the claims against these assets. Assets are defined as anything of value, tangible or intangible. Liabilities involve obligations for the payment of assets, or obligations to render services to other parties. Net worth is obtained as the excess of assets over liabilities, and represents the contractor's equity in the business. The term contractor is used here in the broad sense, meaning proprietor, partners, or stockholders.

The balance sheet may also be referred to by other names: statement of financial condition, statement of worth, or statement of assets and liabilities. A representative example of a contractor's balance sheet is depicted in Figure 9.3, the balance sheet for Blank Construction, Inc., on the last day of the year. Company assets are shown on the left side of the balance sheet and liabilities and net worth on the right side.

Figure 9.3 Balance Sheet for the Blank Company

The major headings of Figure 9.3 are further discussed in the paragraphs that follow, in terms of reference to the parenthesized alphabetical characters such as (a) in the balance sheet.

- Current assets include cash, materials on hand, and other resources that may reasonably be expected to be sold, consumed, or realized in cash during the normal operating cycle of the business.

When the business has no clearly defined cycle, or when several operating cycles occur within a year, current assets (and current liabilities) are construed on a 12-month basis.

This one-year-cycle rule applies to most contractors.

Prepaid expenses represent goods or services for which payment has already been made and which will be consumed in the future course of operations.

- Noncurrent notes receivable are in the nature of deferred assets, representing the value of notes that become receivable at some future date or dates.

- Property represents the fixed assets of the business.

These assets are more or less permanent in nature and cannot readily be converted into cash, at least not in amounts commensurate with their true values to the contractor.

These assets generally have a useful life of several years, although assets such as buildings, equipment, vehicles, and furnishings do wear out gradually.

These assets are capitalized at their purchase prices, or in accordance with appropriate cost appraisals in standard accounting practice.

- Accumulated depreciation represents the total decrease in value of the property as a result of age, wear, and obsolescence.

Depreciation is more fully discussed in sections to follow in this chapter.

- Total assets is the sum of everything of value that is in the possession of or is controlled by the company.

- Current liabilities are debts that become payable within a normal operating cycle of the business [see Item (a)].

It is presumed that payment will be made from current assets.

- In the example, the Blank Construction Company, Inc., is using the completed-contract method of reporting income.

Deferred credits represent the excess of project billings over related costs on current contracts that have not reached completion by the end of the reporting period.

This is treated as a current liability because the company is required to render services in the future, and payment has already been made for these services.

If the contractor had underbilled, that is, if the billings were less than related costs, the resulting amount would be treated as a current asset.

- Total liabilities is the sum of every debt and financial obligation of the company.

- This is the capital stock account, showing the classes and amounts of stock that have actually been issued and paid for by the stockholders.

In the example, 4,610 shares of $100 par-value common stock have been purchased by the owners.

- This represents the net ownership interest the corporation “owes” to the stockholders.

In the example, this amount is calculated as the sum of the common stock investments plus retained earnings (also called earned surplus).

The book value of the common stock as of December 31, 20—, is obtained by dividing $645,655.32 (the total net worth of the firm) by 4,610 (the number of shares of common stock sold), which yields a value of $140.06 per common share.

The determination of the book value of common stock excludes intangibles of all kinds that would have no value on liquidation.

The market value of this common stock, that is, the price for which the stock can be sold, may differ substantially from the book value of the stock.

What shares of stock are truly worth in a closely held corporation can be very difficult to determine. Yet such a value may be needed for estate, gift, or income tax purposes. The Internal Revenue Service has issued guides to assist in determining the value of closely held shares.

- The equality of (e) to (k) illustrates that Total Assets = Total Liabilities + Net Worth.

The balance sheet is of considerable analytical value for those who wish to determine the financial condition of a firm. It discloses the nature and composition of a company's assets and shows how these assets are financed. The sources of funds tell a great deal about the quality of management and the stability of a contractor. The balance sheet also provides a good indication regarding the liquidity of a firm, that is, its ability to meet its short-term financial obligations. A comparison of balance sheet values over time discloses trends in the company's management policies and in the company's financial position.

There are also some shortcomings associated with balance sheets. The balance sheet information applies as of a specific date, and may not be representative of the normal company financial condition. Additionally, some asset values may be approximate determinations, and the person reading the balance sheet is left to determine the true value in his or her perception. It is also true that the accounting method used for the preparation of a balance sheet can appreciably influence the data presented.

9.11 Financial Ratios

Financial ratios of various kinds are frequently utilized, both by company management internally and by external constituents of a company, as quantitative guides for the assessment of a company's financial and earning position. A number of different ratios can be used to extract further information from, and to further analyze, a company's income statements and balance sheets.

It is not as much the absolute size of the figures in the income statement and balance sheet documents that is meaningful to the financial analyst, but rather the relationships or ratios among the different values. By comparing the same ratios over a series of financial reports, the interested person can extract very significant information, and can paint a very accurate picture, regarding a company's financial performance over a span of time. Additionally, when such ratios are compared with the similar figures of other contractors, a comparative financial picture of the businesses is obtained.

A number of different ratios can be used to provide company management as well as external analysts with guidance concerning the financial condition of the firm, and to point to areas that need attention. Four different types of ratios are in widespread usage:

- Liquidity ratios. These measures reveal a company's ability to meet its short-term financial obligations.

- Activity ratios. These ratios indicate the level of investment turnover and provide information with regard to how well the company is using its working capital and other assets.

- Profitability ratios. These values relate overall company profits to various parameters such as contract volume or total assets.

- Leverage ratios. These ratios compare company debt with other financial measures such as total assets or net worth.

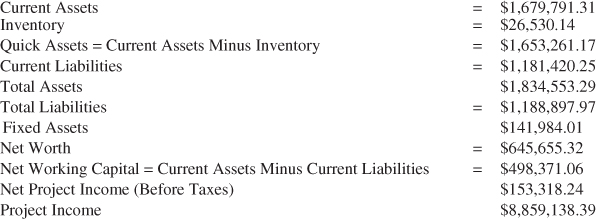

Some financial ratios that are commonly used by construction contractors are illustrated in Figure 9.4. The value of each ratio has been computed for the Blank Construction Company, Inc., using data from the company's income statement and balance sheet. The values taken from the income statement and balance sheet for the calculation of the ratios illustrated are summarized in Figure 9.5.

Figure 9.4 Financial Ratios for the Blank Company

Figure 9.5 Information from Income Statement and Balance Sheet Used for Calculating Financial Ratios

This company is represented to be a building contractor whose overall financial condition is relatively good. In brackets next to each ratio obtained for the Blank Construction Company, Inc., national median ratios for commercial building contractors as reported by the Risk Management Association, are indicated. The Risk Management Association (www.rmahq.org) is an organization that works as a consultant to banks and lending institutions. Such median values change from year to year and vary with the size of the contractor and the type of construction involved, so the values given are for illustrative purposes only.

The data in Figure 9.5 are taken from the documents illustrated in Figures 9.2 and 9.3.

The ratios and values cited in brackets at the far right in Figure 9.4 above are illustrative of contractors' financial experience in general, on a national average basis. The ratios for an individual contractor can, and often do, vary substantially from these median values. Nonetheless, to the trained eye such financial ratio tells a great deal about the business, and its financial condition, and the quality of its management.

9.12 Significance of Ratios

Each of the various financial ratios conveys its own message. The significance of the ratios determined in the previous section is further discussed next.

- Quick assets to current liabilities (quick ratio). This ratio shows the number of dollars immediately available to cover current debt of the enterprise. When this ratio is 1.0 or larger, the business is said to be liquid, and the ratio is usually considered to be adequate.

- Current assets to current liabilities (current ratio). This ratio is widely considered to be the most significant short-term financial measure. It is a test of the firm's ability to meet its current obligations. The higher the ratio, the greater the assurance that short-term debts can be paid. In the construction industry, a Current Ratio of at least 1.5 is generally regarded as being favorable.

- Total liabilities to net worth (debt to equity ratio). Indicates the relative amounts that creditors and owners have invested in the business. Values of 1.0 to 2.0 for this ratio are usually considered to be acceptable in the construction industry.

- Project income to net working capital and project income to net worth. Both of these ratios convey the same general message. These ratios measure the rate of capital turnover, showing how actively the firm's capital is being put to work. If capital is turned over too rapidly, liabilities can build up at an excessive rate. If the ratios are too low, funds become stagnant and profitability suffers. In construction, these ratios are typically higher than in most other industries. These relatively high values partially explain why entry into the construction business is so easy. A construction contractor can perform more work per dollar of invested capital than is possible for workers in most other industries.

- Fixed assets to net worth. This ratio is one that can vary greatly from one construction type to another, being much higher for engineering construction than for building construction. In general, a higher value in this ratio is undesirable because heavy investment in fixed assets (principally equipment for an engineering construction firm) indicates the firm may have low net working capital, or may indicate that the company has incurred substantial funded debt to supplement working capital.

- Percent net project income (before taxes) to project income. This ratio reveals the average profit margin realized on the field work that is performed by the company. This figure is typically small in the construction industry and reveals why the rate of contractor business failures is as high as it is. It does not require much of a change to raise the cost of a project by a percent or two, and to change the project from being profitable to incurring a loss for the contractor.

- Percent net project income (before taxes) to net worth. This is perhaps the most important of the long-term ratios because it reflects the efficiency with which invested capital is employed. Considering the risk, the contractor should expect to earn more on its investment than it could realize from current market dividend or interest rates.

- Percent net project income (before taxes) to total assets. This ratio relates company profits to the level of assets available to earn a profit. Smaller construction corporations may have somewhat lower profitability ratios that can be at least partially explained by the respectable salaries of company officers.

In most companies, a significant proportion of company gross profits is often taken in the form of personal salaries.

9.13 Construction Equipment Acquisition

For contractors such as highway and heavy construction contractors, whose business operations require substantial spreads of construction equipment, the manner in which the necessary units of equipment are acquired is an important business determination. Likewise, for building construction and industrial contractors who have need for large cranes and materials handling machinery, a very careful analysis is likewise important for the business.

Construction equipment of all kinds is very expensive. Additionally, this equipment operates on a construction site in an environment that requires major support in the form of maintenance, repairs, and parts. Deliberate management analysis and decision-making are necessary in order to maximize the contractor's investment or expense in the acquisition of the equipment that is needed for the performance of the work.

The historical pattern of equipment acquisition in the construction industry has been for the contractors to purchase and own the machines and equipment necessary for the conduct of their business. However, many contractors are coming to the realization that construction equipment is a very costly business asset that must be carefully managed in all of its aspects. Frequently today, many contractors are analyzing their equipment needs more carefully, and are availing themselves of other alternatives in addition the purchase option for their equipment.

For contractors whose construction equipment consists of units that receive regular and substantial usage in the contractor's field operations on construction projects, purchase of new or used equipment is the most common method of acquiring the machines that are needed. Considerations such as the nature of the contractor's present and anticipated future need for a piece of equipment, first cost and ownership cost, operating cost, production rate, unit size and capacity, model reliability and ruggedness, risk of obsolescence, and how the unit will fit in with the inventory of the contractor's existing equipment, all are important aspects of the determination. A major consideration in the purchasing decision is how the acquisition is to be financed.

When purchasing equipment, the contractor is well advised to investigate the source from whom to buy the equipment. Most contractors have found that equipment obtained from full service, factory-authorized distributors will usually cost more on a first-cost basis, but can offer added value in terms of customer support, service and parts support, product warranties, trade-ins, and other purchase options. It is common for most major equipment manufacturers and distributors to offer financing plans, sometimes at very attractive rates.

Most construction firms that have a relatively stable volume of work within a limited geographic area continue to find it desirable and economical to own their own fleets of construction equipment. However, contractors are increasingly finding that renting or leasing their construction equipment is economically preferable to ownership. Equipment management now requires that the contractor treat his equipment as an independent profit center, and to carefully evaluate every aspect of equipment acquisition and utilization.

Although the direct cost and short-term costs of equipment rental can be substantially higher than for either ownership or leasing, renting construction equipment can have advantages. For example, rental can provide an advantageous way in which to keep the work progressing when there is an equipment breakdown on a project, or to meet specialty job requirements or times of peak demand on the project. Rental can also prove to be a very efficient option in situations where there will be low-percentage utilization of a machine, and for short-term peak or seasonal use. Rental can be a valuable option when the job site is far removed geographically from the contractor's other operations, or for providing specialized items that the contractor may have limited use for in the future.

Rentals may also be considered as a method by which the contractor can evaluate equipment for consideration for possible subsequent purchase. Because of the high purchase price and investment cost of large equipment, rental can conserve company capital and can result in a better ratio of assets to liabilities.

When equipment is rented, it is usually not rented for a guaranteed period and therefore can be returned at any time. Equipment maintenance and repair are the responsibility of the dealer or rental yard, resulting in savings in time and expense for the contractor. These savings can offset, at least to a degree, the higher cost per unit of time for a rental.

Numerous equipment centers now specialize in the rental of construction equipment. Rental rates normally vary with the length of time the unit is needed, with short-term rates typically being higher than long-term rentals. Additionally, many rental centers can arrange rental-purchase programs where the contractor has an option to purchase.

Leasing provides another commonplace and widely used means of a contractor's acquiring construction equipment. Most construction equipment leases are written for a term of one year or longer.

Leasing equipment offers a number of potential financial advantages for the contractor. Leasing can be a useful step between renting and buying. Usually, the cost of leasing is considered as an operating expense, not a liability as with a bank loan for equipment purchase. Leasing can improve a contractor's working capital position by avoiding having funds tied up in expensive fixed assets. An equipment lease can be structured so that there is no initial cash outlay, enhancing the contractor's liquidity position. Additionally, certain tax advantages can accrue with leasing. Under certain circumstances, lease payments may compare favorably with ownership costs. Additionally, many leases provide that at the expiration of the lease period, the contractor has a purchase option, if there is a continuing need for the machine, and if he believes the machine to be worth the additional payment.

9.14 Equipment Management

Many contractors own extensive spreads of equipment, or major pieces of equipment that they use to accomplish the work on their construction projects. As noted earlier, construction equipment is very expensive, in terms of first cost and also in terms of ownership and operating costs. The contractor's investment in his equipment inventory can easily run into the millions of dollars.

Equipment purchase is economically justified only when the purpose of the equipment is to make money for the contractor. However, equipment will produce the expected income only if it is properly managed. Equipment ownership must be carefully analyzed and managed in the same manner as any other capital investment.

In the case of construction equipment, effective management involves making informed judgments about equipment acquisition and financing, establishing a comprehensive preventive maintenance program, and maintaining accurate and current records of equipment income, expense, usage, and production rates. Additionally, the contractor will find it necessary to establish appropriate company policies with regard to equipment operation and usage, and maintenance and repairs. In addition, the contractor will need to establish policies with regard to equipment replacement.

A rigorous preventive maintenance program is essential to profitable equipment utilization and management. Equipment downtime has a serious detrimental effect on project costs and schedules. A contractor's preventive maintenance program must be tailored to its own equipment specifications as well as to the job site conditions where the equipment is in operation. Special attention must be given to those machines that are critical to a project, that is, those machines whose downtime would have a particularly severe impact on production, and costs, and schedules. Therefore, proper maintenance is essential so as to minimize unanticipated equipment downtime.

Once equipment has been purchased, the contractor attempts to recover the acquisition costs by using it in order to perform work and generate revenue, and by realizing the residual value of each machine upon its final disposition. The accounting procedures that are used to allocate or to “charge” equipment costs to the construction projects where the machinery is utilized, vary substantially from one contractor to another. However, a common procedure is to establish an internal rental rate for each piece of equipment, a topic discussed previously in this chapter and also in Chapter 5.

In basic terms, the contractor will account for the ownership and operating costs of each machine he owns, with operating costs including an allowance for maintenance and repairs. These calculations produce an “internal rate,” dollars per day, or week, or month for the contractor's owning and operating the machine.

During the progress of work in the field, a charge equal to the internal rental rate multiplied by the number of equipment hours, weeks, or months the equipment is used on the project is entered as an equipment cost against the project. At the same time, an equal but opposite credit is made to the contractor's central ledger account for that equipment unit. This is the same equipment accounting procedure previously discussed, where all items of expense, exclusive of operating labor, and hours of usage are continuously maintained for that equipment item.

In a business sense, what the contractor is doing is establishing in his accounting procedures a system that is similar to a separate company that owns, services, and maintains all of his major equipment and rents it to the contractor at predetermined rates. This equipment accounting procedure provides a cumulative record of expense and earnings for each major equipment unit.

Analyzing how these figures compare from one piece of equipment to another, as well as how these costs compare to other equipment acquisition options such as renting or leasing, provides company management with invaluable information concerning the management of the company's equipment assets. In short, the company knows which machines are paying their way and which are not. Many construction firms have a company policy that provides that when the annual cost of an equipment item exceeds its annual earnings, it is to be either replaced or sold.

A number of construction companies treat their equipment division as a separate profit center within the company. This simply means that the equipment investment is treated as a separate business, with the return on the investment required to be commensurate with the risk. Whether a contractor expects a breakeven performance or a profit on its equipment investment is a matter that depends on company management philosophy and is translated into company policy.

The replacement of a large equipment item is a major decision on the part of the contractor, and one that requires careful analysis and considerable study. Deciding on the replacement life and the replacement time for a piece of equipment is accomplished by construction contractors in different ways. However, it is a well-established axiom of equipment ownership that the replacement life for a piece of equipment is not the age at which the machine is no longer able to produce, but rather, replacement life is the equipment age that optimizes its advantage to the owner.

Methods of analysis are available to assist contractors in determining the point in time where the production costs of the machine are at a minimum. Another form of study can establish when profits earned by the equipment item are at a maximum. Various forms of discounted cash flow models are also available. Financial analysts and consultants are also available, who can assist contractors in making these determinations.

Associated with the replacement of certain equipment types, is the possibility of rebuilding a presently owned unit rather than replacing it. The cost of rebuilding a machine is normally one half or less of the purchase price of new equipment. This can provide an efficient way to extend the life of older machinery and restore its original productivity. This procedure may be an attractive alternative for contractors who may have difficulty supporting the financing of new equipment models.

In summary, it can be said that every construction firm that owns significant amounts of equipment needs to have some formal system of analysis in order to indicate the most advantageous time to replace or to rebuild a given major piece of equipment. In a general sense, when the average time rate of expense for a given machine exceeds the historical rate of similar machines, it needs replacement or rebuilding.

9.15 Equipment Depreciation

From the day of its acquisition, most business property, including construction equipment, steadily declines in value because of age, usage, wear, and obsolescence. This reduction in value is called depreciation and represents a cost of doing business for the contractor. Depreciation pertains to the physical depletion of capital assets the contractor owns, such as offices, warehouses, vehicles, computers, furniture; and it certainly pertains to construction equipment of all kinds as well. Because of the continuing decline in the value of such property, its cost must be amortized over its useful life so that the contractor recovers his investment cost and has capital available when replacement of the property becomes necessary. This entire process is referred to as depreciation and depreciation analysis.

Equipment depreciation is an especially important matter for contractors who own large fleets of equipment, and/or individual pieces of expensive equipment. The average contractor specializing in heavy and highway work may well have an equipment investment of $15 million or more, which may be 20 times that of a building contractor who has a comparable contract volume.

Depreciation costs for equipment-oriented contractors account for an appreciable portion of their annual operating expense. Basically, depreciation systematically reduces the value of a piece of equipment on an annual basis. The sum of these reductions at any time is called a depreciation reserve, which, when subtracted from the initial cost of the equipment, yields the current book value for the asset.

The initial cost of an asset, for depreciation purposes, includes not only the sale price, but also the costs of taxes, freight, unloading, assembly, delivery, and setup or rigging expenses. The book value represents that portion of the original cost that has not yet been amortized. As previously noted, depreciation costs represent a cost of doing business for the contractor, and in accrual accounting, these costs correspondingly reduce company earnings. At the same time, the depreciation reserve represents capital that is retained in the business, ostensibly for the ultimate replacement of the capital assets being depreciated.

9.16 Straight-Line Depreciation

The simplest and most straightforward method of determining depreciation is called straight-line depreciation. This method writes off the depreciable value of an asset at a uniform rate throughout its service life. Straight-line depreciation assumes, for record-keeping purposes, that the amount of value loss is constant from one year to the next, throughout the service life of the asset.

Some have criticized the use of the straight-line method as being unrealistic, on the grounds that the value decline of the capital item never actually follows such a course. It can certainly be said that most assets decrease in value more rapidly during the early years of their life.

In reality, few would say that the straight-line depreciation procedure accurately measures the actual decline in asset value over a span of time. In this regard, however, it is to be recognized that accurate appraisal of the value of an asset is not the objective of depreciation accounting. Rather, depreciation accounting is concerned with spreading the cost of an asset over its useful life in a systematic and rational manner, rather than attempting to gauge depreciation charges in such a way as to parallel physical decline.

Depreciation accounting should be viewed as a process of allocation, rather than one of valuation. Straight-line depreciation is a method that is widely applied by contractors to their equipment, for internal purposes such as estimating equipment costs, and for equipment cost control on ongoing projects.

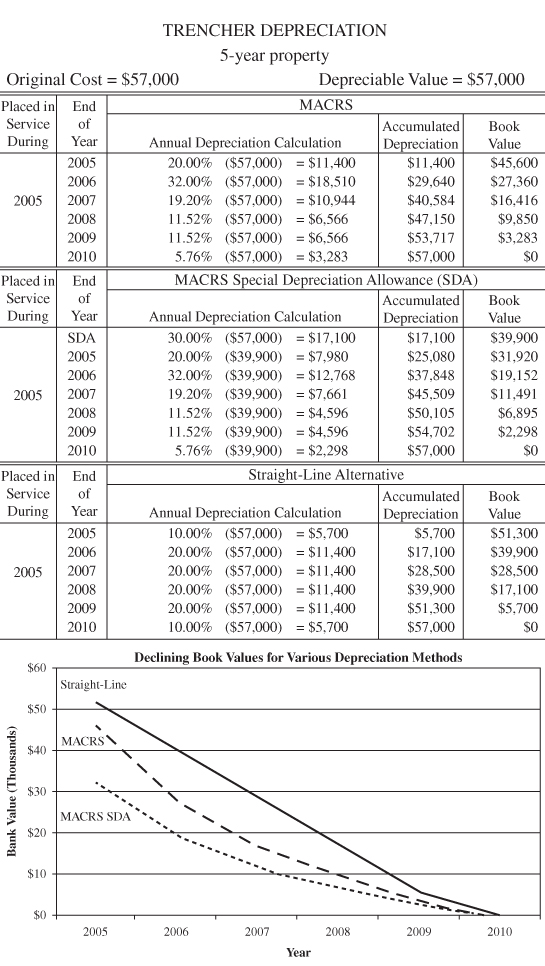

Figure 9.6 illustrates the workings of the straight-line depreciation method for a ditching machine whose purchase price was $57,000, which has an expected service life of five years, and whose salvage value is zero. It should be noted that the depreciation for the first and last years of ownership is half the annual rate for five years of ownership (10 percent rather than 20 percent) because tax codes require that in the year in which a piece of capital equipment is purchased and disposed of, its depreciation rate for that year is one half its straight line rate. This figure also illustrates year-by-year depreciation for this machine by the Modified Accelerated Cost Recovery System (MACRS) and MACRS SDA (special depreciation allowance) depreciation methods, which are accelerated depreciation methods to be discussed in the following section.

Figure 9.6 Annual Depreciation of a Trenching Machine by Three Different Methods

9.17 Accelerated Depreciation

Accelerated depreciation provides the advantage for the contractor of a faster write-off of asset cost during the first years of its life than in the later years. There is considerable opinion that a better matching of revenue and expense is achieved by applying accelerated depreciation methods to construction equipment, because new equipment is generally more productive than old, and frequently the productivity declines very rapidly after the first few years of use.

The use of procedures that afford larger depreciation deductions during the earlier years of asset ownership may also have other important tax and financial advantages for a contractor. For example, rapid initial depreciation causes cash to be retained in the business, ensuring that cash is available, and enhancing the liquidity of the business. Additionally, larger depreciation charges against regular income in a given year causes a reduction of income taxes for that year.

In addition, accelerated depreciation methods also provide for faster recovery of equipment value, thereby offering the contractor some measure of protection against unanticipated contingencies later in the life of the equipment, such as obsolescence, excessive maintenance, rapid wear, or the need for equipment of a different size or capacity. Additionally, rapid depreciation amortizes the contractor's equipment investment more quickly, and simultaneously decreases the book value at the same rate. Speedy reduction of book value leaves the contractor with much greater latitude to dispose of unsatisfactory equipment and, to some degree, can also assist in combating the problem of obsolescence, or of replacing equipment during periods of inflation. In the usual case, many contractors favor using accelerated depreciation of their equipment and other business assets within the bounds allowed by the tax codes, for purposes of income tax reporting.

9.18 Modified Accelerated Cost Recovery System (MACRS)

The Economic Recovery Tax Act of 1981 established a detailed depreciation system for business property and has gone through several subsequent revisions. It is currently known as the Modified Accelerated Cost Recovery System (MACRS). This method is required for business income tax reporting and is, basically, an accelerated depreciation procedure with the provision that the owners of an asset can elect straight-line depreciation if they wish. This system is a relatively simple and easy procedure to use. By the provisions of this legislation, equipment life and salvage value are a matter of law rather than negotiation. This system makes it possible to depreciate construction equipment to zero salvage value over time periods that are much shorter than the typical useful life of the equipment.

MACRS identifies several classes of property and defines the allowable depreciation amounts that are calculated as a stipulated percentage of the asset's adjusted cost. The personal property classes of interest to contractors are three- and five-year assets, with the year classification depending upon the property type involved. For example, three-year property includes automobiles and light-duty trucks, while five-year property includes essentially all other contractor equipment.

Using the MACRS procedure, the value of each piece of equipment is decreased annually by the depreciation charge calculated. The sum of these charges at any point in time is a depreciation reserve that, when subtracted from the initial cost of the equipment, yields the current book value of the equipment. The initial cost of an asset, for depreciation purposes, includes not only the sale price but also the cost of taxes, freight, unloading, assembly, delivery, and setup. The book value represents that portion of the original cost that has not yet been charged off or amortized in depreciation. As previously stated, depreciation charges are a cost of doing business and correspondingly reduce company earnings. At the same time, the depreciation reserve represents capital that is retained in the business, ostensibly for the ultimate replacement of the capital assets being depreciated.

Ordinarily, a contractor favors writing off construction equipment as rapidly as possible. This is done by using the prescribed MACRS deduction rates. However, contractors also have the option of using either MACRS accelerated rates or straight-line depreciation for three- or five-year property. Additionally, there are provisions allowing the contractor as taxpayer to depreciate three- and five-year property over longer periods using straight-line depreciation. These MACRS options seemingly would rarely work to the advantage of a construction firm for income tax reporting.

It is permissible by Internal Revenue Service regulations to employ different depreciation methods for internal financial reporting and tax reporting purposes. Contractors may use straight-line depreciation (or any other conventional procedure) for the preparation of their usual financial statements, and the MACRS accelerated rates for income tax purposes.

Figure 9.6 illustrates how recovery values are obtained using MACRS depreciation. The new $57,000 ditcher is used for purposes of illustration. Under MACRS, the ditcher is classified as five-year property. The depreciation values for both MACRS and straight-line depreciation for the first and last years represent the one-half-year convention rule. This rule mandates one-half year of depreciation for the first year of service, regardless of the time of year service is started. There are numerous other rules and regulations associated with MACRS. The contractor should seek advice on matters pertaining to real property, disposition of property, partial expensing, and other depreciation tax matters from tax specialists and financial advisors.

9.19 Procurement

Procurement, which can be defined as the process by which the contractor obtains the goods and services needed for company operations, is a function of primary importance in a construction contractor's organization. This activity actually includes quite a number of different functions, each playing an indispensable role in the contractor's obtaining what he needs for the performance of projects he constructs, as well as for the functioning of the company.

The procurement function may be structured in several different ways by company management. In some companies, the project manager is responsible for the procurement function for all of the company projects in his or her portfolio. In other companies, project managers and superintendents share in this responsibility. In other firms, procurement is a centralized company operation, sometimes handled by the company operations officer, or by a vice president, or by a person known as an expediter who handles this responsibility.

In some companies, especially larger firms, the procurement function may operate as a separate department within the company structure. Centralizing all procurement functions in one department can be economical in terms of both time and money. It concentrates the expertise necessary to perform this important function, and can afford protection against improper and unnecessary purchasing expenditures of many kinds.

Whatever their title and position in the structure of a construction company, procurement personnel occupy a position of great responsibility within the organization, and typically perform a number of different duties. Performing procurement functions involves the preparation and use of a number of standard document forms such as requisitions, purchase orders, and subcontracts. The principal procurement functions in a typical construction company are discussed in the following paragraphs.

9.19.1 Purchasing

Essentially, purchasing is the obtaining of equipment, tools, materials, stores, supplies, fuel, parts, motor vehicles, and services of every sort that are needed by the office organization, the storage yard and warehouse, and the projects which the company is performing. This involves the processing of requisitions, obtaining and analyzing bids, and preparation and issuance of purchase orders. The preparation of purchasing specifications is often involved with regard to the purchase of goods and services that are not related to the company's construction projects.

9.19.2 Expediting and Receiving

After an order has been placed, contact must be maintained with the vendor to ensure effective communications which will result in timely delivery. This is particularly important with regard to materials needed for the projects that are under way.

The designation of a required delivery date in a purchase order is no guarantee that the vendor will deliver on schedule. Continuous and energetic follow-up action is a necessity if schedules and delivery dates are to be maintained.

When the needed goods are shipped, adequate arrangements must be made for their receipt, unloading, handling, and proper storage.

9.19.3 Inspection

When goods are delivered, they must be inspected immediately so as to assure that they are the correct materials or products and to verify quantity, quality, and other essential characteristics. In the event of shortage, or loss or damage in transit, or erroneous goods shipped, immediate and proper corrective action is required, along with the appropriate documentation. If quality control verification tests are called for, samples must be taken for that purpose, and the tests conducted. A written receiving report should be prepared and filed for each delivery.

9.19.4 Shipping

The contractor's purchase order, in most instances, will designate the method by which goods are to be shipped. This is an important aspect of procurement and requires detailed knowledge concerning the different shipping alternatives, and the time and cost implications of each.

In the event of strikes or other disruptive events that can affect the transportation industry, expeditious and innovative changes in shipping arrangements are sometimes needed. Shipments lost or misplaced in transit must be traced and suitable claims made where goods are damaged or lost.

9.19.5 Subcontracts

In some companies the procurement function includes the preparation and processing of project subcontract agreements. The essential information needed to do this comes from the estimator or the estimating department. When a general contract change order affects subcontractors, suitable changes to the subcontracts affected must be prepared and processed.

9.20 Discounts by Vendors and Suppliers

Discounts are frequently extended to contractors by material dealers and other vendors as an inducement to attract or to reward their trade or as an incentive for their early payment of statement amounts. Some of these discounts take the form of trade discounts and are often referred to as professional discounts.

Trade or professional discounts typically allow contractors to purchase products at a price less than that which a nonconstruction person would pay at retail. In providing these discounts, vendors are encouraging the trade of the contractor professionals, and are recognizing the quantity in which contractors typically purchase, and the relative ease and effectiveness with which the vendor can complete a sale with a construction professional. Additionally, trade discounts often include quantity discounts, where the larger the quantity being purchased, the lower the unit price.

Cash discounts are frequently extended in the form of a discount in the statement price, given in exchange for the payment of an invoice before it becomes due. A number of different forms of cash discounts are in commercial usage, and several variations are presented here. The expression “2–10, Net 30” is an example of one of these practices, and is, in fact, fairly commonplace. With this expression the seller is indicating that the buyer can deduct two percent from the invoice or statement amount if payment is made within 10 days of the statement date; otherwise, full payment of the net amount is due in 30 days.

Materials dealers normally date their invoices the day the goods are shipped. If the customer's location is nearby, he has time to take delivery and to check the goods prior to paying within the discount period. A customer who is far removed geographically, however, may not be able to take advantage of the discount unless he pays before the goods are actually received. To overcome this disadvantage to distant customers, some vendors will mark their invoices “ROG” or “AOG” to indicate that the discount period begins upon “receipt of goods” or upon “arrival of goods.”

Another form of cash discount provision similar to the previous, is termed prox, which means the discount period is expressed in terms of a specified date in the month which follows the shipments being made or billed. The expression “2–10 Prox Net 30” means a 2 percent cash discount is allowed if the invoice is paid not later than the 10th day of the month following the purchase. The net due date of the account is 30 days from the first of that month.

Another common way of expressing this discount structure is “2–10, EOM,” which indicates that a 2 percent discount can be taken if the invoice is paid by the tenth day of the month after the purchases are shipped. If the buyer does not make payment within this period, the net amount of the bill is considered to be due at the end of the month thereafter.

For accounting purposes, cash discounts are treated as income, and appear as “discounts earned” on the income statement. This is illustrated in Figure 9.2.

As one considers cash discounts, a two percent discount may at first glance appear to be inconsequential. However, if a contractor purchases a million dollars worth of materials in a year's time, and pays promptly so as to avail himself of the cash discounts, he has increased his earnings in the amount of $20,000. Additionally, when an auditor, a surety company, or a creditor analyzes a contractor's income statement and recognizes that the contractor has not availed himself of discounts offered by vendors, they may view this as a demonstration of inattentive management practices, or as an indicator of cash flow problems or other financial difficulties.

The status of cash discounts is a matter of sufficient importance that it is often called out in cost-plus contracts. While agreement on this point can be negotiated in different forms, it is fairly common in such agreements for the contract language to provide that all cash discounts accrue to the contractor, except when the owner has advanced money to the contractor from which to make payments to the supplier. Cost-plus contract documents written by the American Institute of Architects (AIA) reflect this policy. However, some forms of cost-plus contracts stipulate that the reimbursable cost of materials shall be decreased by the amount of any cash discounts taken, without regard to who provides the funds to make payment.

9.21 Title of Purchases

Most contractors regularly purchase appreciable quantities of construction materials. During the process of transport, delivery, unloading, handling, and storage of these materials, a variety of loss or damage can and does occur. When such difficulties arise, the mutual rights and responsibilities of the buyer and of the seller are largely controlled by the Uniform Commercial Code. Normally, the risk of loss or damage as related to personal property rests with the person holding title. When a loss occurs, the responsibility for the loss, and the rights of each party as buyer or seller, are based on whether title of the goods has passed from seller to buyer at the time the loss occurred. For this reason, the time at which the title of a purchase passes from the vendor to the contractor is a matter of considerable importance.

In a fundamental legal sense, title to personal property that is the basis of a sale passes from seller to buyer at the time when the parties intend for it to pass. If the sales contract or purchase order states or clearly implies at what time title is to pass, the terms of the agreement will prevail. It is seldom, however, that the parties to a sales agreement insert specific provisions concerning the point at which passage of title occurs.

Consequently, the Uniform Commercial Code has established a standard set of rules for application to matters of this kind. In the absence of any expressed intention to the contrary, title passes in accordance with the following general rules.

9.21.1 Cash Sale

Agreements that call for delivery and payment to take place concurrently are called cash sales. Title of the goods passes when the goods are paid for and delivery takes place.

9.21.2 On-Approval Sale

When goods are delivered to the buyer on approval or trial, title changes when the buyer indicates acceptance, when the goods are retained beyond the time fixed for their return, or when the goods are retained beyond a reasonable time.

9.21.3 Sale or Return

Title passes when goods are delivered to the buyer. However, the buyer has the option to return the goods within a fixed period of time.

9.21.4 Delivery by Vendor

If the purchase order requires the seller to deliver the goods to the buyer's destination and delivery is made by the seller himself, the seller retains title until the goods are delivered.

9.21.5 Shipment by Common Carrier

There is a general rule that when the goods are shipped by common carrier to the buyer, title passes to the buyer when the seller delivers the goods to the carrier for transportation.

However, the following exceptions apply:

- When the seller fails to follow shipping instructions given by the buyer, such as the buyer naming a particular carrier and the seller shipping by another.

- When the seller is required to deliver at a particular place, such as the buyer's dock or railroad siding.

- When the seller is required to pay freight up to a given point, as in FOB agreements.

- When the seller is required by purchase order or by custom to make arrangements with the carrier to protect the buyer, as by declaring the value of the shipment or as in CIF agreements (see definition below), and fails to do so.

- When the goods shipped do not correspond in both quality and quantity to those ordered.

- When the seller reserves title by retaining the bill of lading.

There are several terms that are commonly used in purchase contracts and purchase orders, which relate both to terms of the sale, as well as indicating when title transfers. Definitions of some of the commonplace terminology include the following:

- FOB. Standing for “free on board,” or “freight on board,” FOB indicates that the seller shall put the goods on board a common carrier free of expense to the buyer, with freight paid to the FOB designated point. For example, contractors' purchase orders frequently specify delivery as “FOB jobsite,” or “FOB storage yard.” Under an FOB agreement, title goes to the buyer when the carrier delivers the goods to the place indicated.

- CIF. Standing for “cost, insurance, freight,” CIF indicates that the purchase-order price includes the cost of the goods, customary insurance, and freight to the buyer's destination. Title passes when the seller delivers the merchandise to the carrier and forwards to the buyer the bill of lading, insurance policy, and receipt showing payment for freight.

- C & F. Indicates the same shipping arrangement as described above, except that no insurance need be obtained by the vendor.

- COD. Meaning “collect on delivery,” or “cash on delivery,” COD indicates that title passes to the buyer, if he is to pay the transportation, at the time the goods are received by the carrier. However, the seller reserves the right to receive payment before surrender of possession to the buyer.

9.22 A Contractor's Right to Check on Project Financing

Many of the construction contract forms in commonplace usage provide that the contractor can request and receive reasonable evidence from the owner that suitable financial arrangements have been made by the owner to pay for the construction contract amount. The AIA General Conditions of the Contract for Construction contains this provision (see Appendix D).

It may be a good business practice on the part of a contractor to obtain advance information concerning a private owner's finances and credit rating. Just as the owner is concerned with the financial capacity and capabilities of the contractor so too, the contractor must be assured that the owner has the necessary financial means to fulfill contract requirements and to pay for the construction.

Case studies are on record where contractors have experienced serious financial difficulties when they failed to investigate the capability or integrity of the owner, and later discovered that the owner was unable or unwilling to make payment timely in accord with the provisions of the contract. This matter cannot safely be ignored, since the contractor must usually invest a substantial amount of his own money into a project before any monies are payable by the owner to the contractor. A default by the owner in meeting his payment obligations under the contract can have a very serious impact on the contractor's financial well being, and on the very survival of his business. The appreciable risks assumed by the contractor in the performance of construction contracts need not be increased by the chance of a default in owner payments.

Before obligating itself by bid or contract to a private owner, the construction firm does well to make some investigation and evaluation concerning the financial integrity of the owner, and the source of the owner's financing for the project. This step should be taken whether or not the owner is required by the terms of the contract to provide evidence, upon request, that he has the means to pay the amounts indicated in the construction contract. Especially if the owner is unknown to the contractor, additional credit information can be obtained from sources such as financial and credit rating services, industry trade groups, other contractors who may have previously dealt with the owner, or with the assistance of the contractor's banker.

There are also cases where the contractor must make certain determinations with regard to the owner entity with whom it is dealing. An illustrative example is the case where the owner is a shell, dummy, or subsidiary corporation that has been especially formed for the sole purpose of getting the project constructed and minimizing the liability of the principals or parent company. An owner corporation of this kind would have very limited assets, and would be a poor credit risk. Until any new corporation has had time to establish a record of financial stability, the contractor should be advised to assure that the principals or parent company must verify their capability for project funding or personally guarantee to make good on contractual debts. When dealing with a substantial corporation, the contractor must know whether it is dealing with that corporation or with a subsidiary that might be undercapitalized. Additionally, when the contractor is dealing with an agent of an owner, the contractor must insist on being provided written assurance that the agent has authority to bind the principal to the contract.

When the owner is a public agency, the contractor is generally assured that funds required to pay for public works will be available. However, there can be exceptions to this rule, especially in the case of quasi-governmental “corporations” being created by state or local governments to perform various construction functions. Such entities may not possess the full faith and credit backing of the governmental entity. Once the construction monies of these corporations have been exhausted, the contractor can find himself without recourse for payment. Therefore, some analysis regarding the reliability of the funding for these types of agencies should be performed by the contractor before bidding such projects.

On public contracts, it is a statutory requirement that all of the requirements for entering and fulfilling the contract must be fulfilled by the responsible public officials in order for a valid contract to exist. In most jurisdictions, the omission of any required procedural step by a public owner can leave the contractor without remedy to obtain payment for work performed. If a government body enters into a contract without complying with the statutory requirements pertaining to the bidding and awarding of public construction contracts, the contract is considered beyond the power of the public agency and may be declared void. There is a growing body of legal precedent however, that when an imperfect public contract was entered into in good faith by the contractor, and is devoid of fraud or collusion, the contractor is entitled to relief based on the equitable doctrine of unjust enrichment. A contractor who does business with a public entity must be aware of the laws governing its administration and the limitations on the powers and authorities of the public officers involved.

9.23 Payment to the General Contractor