Chapter 2

Weighing Risks and Returns

In This Chapter

![]() Surveying different types of risks

Surveying different types of risks

![]() Reducing risk while earning decent returns

Reducing risk while earning decent returns

![]() Figuring out expected returns for different investments

Figuring out expected returns for different investments

![]() Determining how much you need your investments to return

Determining how much you need your investments to return

A woman passes up eating a hamburger at a picnic because she heard that she could contract a deadly E. coli infection from eating improperly cooked meat. The next week, that same woman hops in the passenger seat of her friend’s old model car that lacks airbags.

I’m not trying to depress or frighten anyone. However, I am trying to make an important point about risk — something that everyone deals with on a daily basis. Risk is in the eye of the beholder. Many people base their perception of risk, in large part, on their experiences and what they’ve been exposed to. In doing so, they often fret about relatively small risks while overlooking much larger risks.

Sure, a risk of an E. coli infection from eating poorly cooked meat exists, so the woman who was leery of eating the hamburger at the picnic had a legitimate concern. However, that same woman got into the friend’s car without an airbag and placed herself at far greater risk of dying in that situation than if she had eaten the hamburger. In the United States, more than 35,000 people die in automobile accidents each year.

In the world of investing, most folks worry about certain risks — some of which may make sense and some of which may not — but at the same time they completely overlook or disregard other, more significant risks. In this chapter, I discuss a range of investments and their risks and expected returns.

Evaluating Risks

Everywhere you turn, risks exist; some are just more apparent than others. Many people misunderstand risks. With increased knowledge, you may be able to reduce or conquer some of your fears and make more sensible decisions about reducing risks. For example, some people who fear flying don’t understand that statistically, flying is much safer than driving a car. You’re approximately 40 times more likely to die in a motor vehicle than in an airplane. But when a plane goes down, it’s big news because dozens and sometimes hundreds of people, who weren’t engaging in reckless behavior, perish. Meanwhile, the national media seem to pay less attention to the 100 people, on average, who die on the road every day.

Then there’s the issue of control. Flying seems more dangerous to some folks because the pilots are in control of the plane, whereas in your car, you can at least be at the steering wheel. Of course, you can’t control what happens around you or mechanical problems with the mode of transportation you’re using.

This doesn’t mean that you shouldn’t drive or fly or that you shouldn’t drive to the airport. However, you may consider steps you can take to reduce the significant risks you expose yourself to in a car. For example, you can get a car with more safety features, or you can bypass riding with reckless taxi drivers whose cars lack seat belts.

Although some people like to live life to its fullest and take “fun” risks (how else can you explain mountain climbers, parachutists, and bungee jumpers?), most people seek to minimize risk and maximize enjoyment in their lives. But most people also understand that they’d be a lot less happy living a life in which they sought to eliminate all risks, and they likely wouldn’t be able to do so anyway.

Likewise, if you attempt to avoid all the risks involved in investing, you likely won’t succeed, and you likely won’t be happy with your investment results and lifestyle. In the investment world, some people don’t go near stocks or any investment that they perceive to be volatile. As a result, such investors often end up with lousy long-term returns and expose themselves to some high risks that they overlooked, such as the risk of having inflation and taxes erode the purchasing power of their money.

Likewise, if you attempt to avoid all the risks involved in investing, you likely won’t succeed, and you likely won’t be happy with your investment results and lifestyle. In the investment world, some people don’t go near stocks or any investment that they perceive to be volatile. As a result, such investors often end up with lousy long-term returns and expose themselves to some high risks that they overlooked, such as the risk of having inflation and taxes erode the purchasing power of their money.

You can’t live without taking risks. Risk-free activities or ways of living don’t exist. You can minimize but never eliminate risks. Some methods of risk reduction aren’t palatable because they reduce your quality of life. Risks are also composed of several factors. In the sections that follow, I discuss the various types of investment risks and go over proven methods you can use to sensibly reduce these risks while not missing out on the upside that growth investments offer.

Market-value risk

Although the stock market can help you build wealth, most people recognize that it can also drop substantially — by 10, 20, or 30 percent (or more) in a relatively short period of time. After peaking in 2000, U.S. stocks, as measured by the large-company S&P 500 index, dropped about 50 percent by 2002. Stocks on the NASDAQ, which is heavily weighted toward technology stocks, plunged more than 76 percent from 2000 through 2002!

After a multiyear rebound, stocks peaked in 2007 and then dropped sharply during the “financial crisis” of 2008. From peak to bottom, U.S. and global stocks dropped by 50-plus percent.

In a mere six weeks (from mid-July 1998 to early September 1998), large-company U.S. stocks fell about 20 percent. An index of smaller-company U.S. stocks dropped 33 percent over a slightly longer period of two and a half months.

If you think that the U.S. stock market crash that occurred in the fall of 1987 was a big one (the market plunged 36 percent in a matter of weeks), take a look at Table 2-1, which lists major declines over the past 100-plus years that were all worse than the 1987 crash. Note that two of these major declines happened in the 2000s: 2000 to 2002 and 2007 to 2009.

Table 2-1 Largest U.S. Stock Market Declines*

|

Period |

Size of Fall |

|

1929–1932 |

89% (ouch!) |

|

2007–2009 |

55% |

|

1937–1942 |

52% |

|

1906–1907 |

49% |

|

1890–1896 |

47% |

|

1919–1921 |

47% |

|

1901–1903 |

46% |

|

1973–1974 |

45% |

|

1916–1917 |

40% |

|

2000–2002 |

39% |

* As measured by changes in the Dow Jones Industrial Average

Real estate exhibits similar unruly, annoying tendencies. Although real estate (like stocks) has been a terrific long-term investment, various real estate markets get clobbered from time to time.

U.S. housing prices took a 25 percent tumble from the late 1920s to the mid-1930s. When the oil industry collapsed in the southern United States in the early 1980s, real estate prices took a beating in that area. Later in the 1980s and early 1990s, the northeastern United States became mired in a severe recession, and real estate prices fell by 20-plus percent in many areas. After peaking near 1990, many of the West Coast housing markets, especially those in California, experienced falling prices — dropping 20 percent or more in most areas by the mid-1990s. The Japanese real estate market crash also began around the time of the California market fall. Property prices in Japan collapsed more than 60 percent.

Declining U.S. housing prices in the mid- to late 2000s garnered unprecedented attention. Some folks and pundits acted like it was the worst housing market ever. Foreclosures increased in part because of buyers who financed their home’s purchase with risky mortgages (which I recommend against in my books, including this one — see Chapter 12). I must note here that housing market conditions vary by area. For example, some portions of the Pacific Northwest and South actually appreciated during the mid- to late 2000s, while other markets experienced substantial declines.

After reading this section, you may want to keep all your money in the bank — after all, you know you won’t lose your money, and you won’t have to be a nonstop worrier. No one has lost 20, 40, 60, or 80 percent of his bank-held savings vehicle in a few years since the FDIC came into existence (major losses prior to then did happen, though). But just letting your money sit around would be a mistake.

If you pass up the stock and real estate markets simply because of the potential market value risk, you miss out on a historic, time-tested method of building substantial wealth. Instead of seeing declines and market corrections as horrible things, view them as potential opportunities or “sales.” Try not to give in to the human emotions that often scare people away from buying something that others seem to be shunning.

Later in this chapter, I show you the generous returns that stocks and real estate as well as other investments have historically provided. The following sections suggest some simple things you can do to lower your investing risk and help prevent your portfolio from suffering a huge fall.

Diversify for a gentler ride

If you worry about the health of the U.S. economy, the government, and the dollar, you can reduce your investment risk by investing overseas. Most large U.S. companies do business overseas, so when you invest in larger U.S. company stocks, you get some international investment exposure. You can also invest in international company stocks, ideally via mutual funds and exchange-traded funds (see Chapter 8).

Of course, investing overseas can’t totally protect you in the event of a global economic catastrophe. If you worry about the risk of such a calamity, you should probably also worry about a huge meteor crashing into Earth. Maybe there’s a way to colonize outer space …

Diversifying your investments can involve more than just your stock portfolio. You can also hold some real estate investments to diversify your investment portfolio. Many real estate markets actually appreciated in the early 2000s while the U.S. stock market was in the doghouse. Conversely, when U.S. real estate entered a multiyear slump in the mid-2000s, stocks performed well during that period. In the late 2000s, stock prices fell sharply while real estate prices in most areas declined, but then stocks came roaring back.

Diversifying your investments can involve more than just your stock portfolio. You can also hold some real estate investments to diversify your investment portfolio. Many real estate markets actually appreciated in the early 2000s while the U.S. stock market was in the doghouse. Conversely, when U.S. real estate entered a multiyear slump in the mid-2000s, stocks performed well during that period. In the late 2000s, stock prices fell sharply while real estate prices in most areas declined, but then stocks came roaring back.

Consider your time horizon

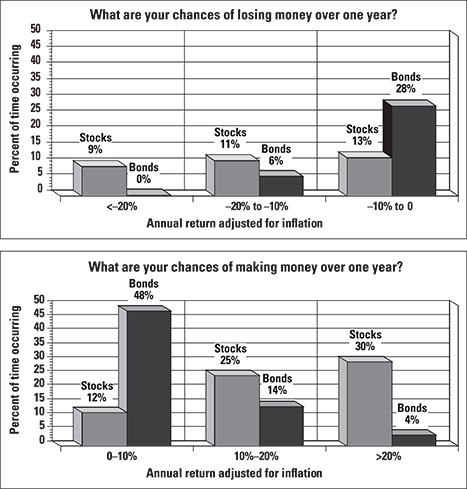

Investors who worry that the stock market may take a dive and take their money down with it need to consider the length of time that they plan to invest. In a one-year period in the stock and bond markets, a wide range of outcomes can occur (as shown in Figure 2-1). History shows that you lose money about once in every three years that you invest in the stock and bond markets. However, stock market investors have made money (sometimes substantial amounts) approximately two-thirds of the time over a one-year period. (Bond investors made money about two-thirds of the time, too, although they made a good deal less on average.)

© John Wiley & Sons, Inc.

Figure 2-1: What are the odds of making or losing money in the U.S. markets? In a single year, you win far more often (and bigger) with stocks than with bonds.

Although the stock market is more volatile than the bond market in the short term, stock market investors have earned far better long-term returns than bond investors have. (See the “Stock returns” section later in this chapter for details.) Why? Because stock investors bear risks that bond investors don’t bear, and they can reasonably expect to be compensated for those risks. Remember, however, that bonds generally outperform a boring old bank account.

History has shown that the risk of a stock or bond market fall becomes less of a concern the longer that you plan to invest. As Figure 2-2 shows, as the holding period for owning stocks increases from 1 year to 3 years to 5 years to 10 years and then to 20 years, there’s a greater likelihood of seeing stocks increase in value. In fact, over any 20-year time span, the U.S. stock market, as measured by the S&P 500 index of larger company stocks, has never lost money, even after you subtract the effects of inflation.

© John Wiley & Sons, Inc.

Figure 2-2: The longer you hold stocks, the more likely you are to make money.

Most stock market investors I know are concerned about the risk of losing money. Figure 2-2 clearly shows that the key to minimizing the probability that you’ll lose money in stocks is to hold them for the longer term. Don’t invest in stocks unless you plan to hold them for at least five years — and preferably a decade or longer. Check out Part II of this book for more on using stocks as a long-term investment.

Pare down holdings in bloated markets

Perhaps you’ve heard the expression “buy low, sell high.” Although I don’t believe that you can time the markets (that is, predict the most profitable time to buy and sell), spotting a greatly overpriced or underpriced market isn’t too difficult. For example, in the second edition of this book, published in 1999, I warned readers about the grossly inflated prices of many Internet and technology stocks (see Chapter 5). Throughout this book, I explain some simple yet powerful methods you can use to measure whether a particular investment market is of fair value, of good value, or overpriced. You should avoid overpriced investments for two important reasons:

- If and when these overpriced investments fall, they usually fall farther and faster than more fairly priced investments.

- You should be able to find other investments that offer higher potential returns.

Ideally, you want to avoid having a lot of your money in markets that appear overpriced (see Chapter 5 for how to spot pricey markets). Practically speaking, avoiding overpriced markets doesn’t mean that you should try to sell all your holdings in such markets with the vain hope of buying them back at a much lower price. However, you may benefit from the following strategies:

- Invest new money elsewhere. Focus your investment of new money somewhere other than the overpriced market; put it into investments that offer you better values. As a result, without selling any of your seemingly expensive investments, you make them a smaller portion of your total holdings. If you hold investments outside tax-sheltered retirement accounts, focusing your money elsewhere also allows you to avoid incurring taxes from selling appreciated investments.

- If you have to sell, sell the expensive stuff. If you need to raise money to live on, such as for retirement or for a major purchase, sell the pricier holdings. As long as the taxes aren’t too troublesome, it’s better to sell high and lock in your profits. Chapter 21 discusses issues to weigh when you contemplate selling an investment.

Individual-investment risk

A downdraft can put an entire investment market on a roller-coaster ride, but healthy markets also have their share of individual losers. For example, from the early 1980s through the late 1990s, the U.S. stock market had one of the greatest appreciating markets in history. You’d never know it, though, if you held one of the great losers of that period.

Consider a company now called Navistar, which has undergone enormous transformations in the past two decades. This company used to be called International Harvester and manufactured farm equipment, trucks, and construction and other industrial equipment. Today, Navistar makes mostly trucks.

In late 1983, this company’s stock traded at more than $140 per share. It then plunged more than 90 percent over the ensuing decade (as shown in Figure 2-3). Even with a rally in recent years, Navistar stock still trades at less than $50 per share (after dipping below $10 per share). Lest you think that’s a big drop, this company’s stock traded as high as $455 per share in the late 1970s! If a worker retired from this company in the late 1970s with $200,000 invested in the company stock, the retiree’s investment would be worth about $25,000 today! On the other hand, if the retiree had simply swapped his stock at retirement for a diversified portfolio of stocks, which I explain how to build in Part II, his $200,000 nest egg would’ve instead grown to more than $4 million!

© John Wiley & Sons, Inc.

Figure 2-3: Even the bull market of the 1990s wasn’t kind to every company.

Just as individual stock prices can plummet, so can individual real estate property prices. In California during the 1990s, for example, earthquakes rocked the prices of properties built on landfills. These quakes highlighted the dangers of building on poor soil. In the early 1980s, real estate values in the communities of Times Beach, Missouri, and Love Canal, New York, plunged because of carcinogenic toxic waste contamination. (Ultimately, many property owners in these areas received compensation for their losses from the federal government as well as from some real estate agencies that didn’t disclose these known contaminants.)

Here are some simple steps you can take to lower the risk of individual investments that can upset your goals:

- Do your homework. When you purchase real estate, a whole host of inspections can save you from buying a money pit. With stocks, you can examine some measures of value and the company’s financial condition and business strategy to reduce your chances of buying into an overpriced company or one on the verge of major problems. Parts II, III, and IV of this book give you information on researching your investment.

- Diversify. Investors who seek growth invest in securities such as stocks. Placing significant amounts of your capital in one or a handful of securities is risky, particularly if the stocks are in the same industry or closely related industries. To reduce this risk, purchase stocks in a variety of industries and companies within each industry. (See Part II for details.)

- Hire someone to invest for you. The best funds (see Chapter 8) offer low-cost, professional management and oversight as well as diversification. Stock funds typically own 25 or more securities in a variety of companies in different industries. In Part III, I explain how you can invest in real estate in a similar way (that is, by leaving the driving to someone else).

Purchasing-power risk

Increases in the cost of living (that is, inflation) can erode the value of your retirement resources and what you can buy with that money — also known as its purchasing power. When Teri retired at the age of 60, she was pleased with her retirement income. She was receiving an $800-per-month pension and $1,200 per month from money that she had invested in long-term bonds. Her monthly expenditures amounted to about $1,500, so she was able to save a little money for an occasional trip.

Fast-forward 15 years. Teri still receives $800 per month from her pension, but now she gets only $900 per month of investment income, which comes from some certificates of deposit. Teri bailed out of bonds after she lost sleep over the sometimes roller-coaster-like price movements in the bond market. Her monthly expenditures now amount to approximately $2,400, and she uses some of her investment principal (original investment). She’s terrified of outliving her money.

Teri has reason to worry. She has 100 percent of her money invested without protection against increases in the cost of living. Although her income felt comfortable in the beginning of her retirement, it doesn’t at age 75, and Teri may easily live another 15 or more years.

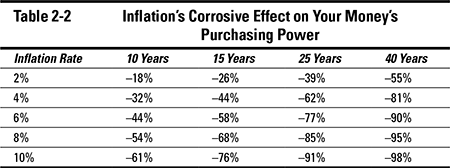

The erosion of the purchasing power of your investment dollar can, over longer time periods, be as bad as or worse than the effect of a major market crash. Table 2-2 shows the effective loss in purchasing power of your money at various rates of inflation and over differing time periods.

As a financial counselor, I often saw skittish investors try to keep their money in bonds and money market accounts, thinking they were playing it safe. The risk in this strategy is that your money won’t grow enough over the years for you to accomplish your financial goals. In other words, the lower the return you earn, the more you need to save to reach a particular financial goal.

A 40-year-old wanting to accumulate $500,000 by age 65 would need to save $722 per month if she earns a 6 percent average annual return but needs to save only $377 per month if she earns a 10 percent average return per year. Younger investors need to pay the most attention to the risk of generating low returns, but so should younger senior citizens. At the age of 65, seniors need to recognize that a portion of their assets may not be used for a decade or more from the present.

Career risk

Your ability to earn money is most likely your single biggest asset, or at least one of your biggest assets. Most people achieve what they do in the working world through education and hard work. By education, I’m not simply talking about what one learns in formal schooling. Education is a lifelong process. I’ve learned far more about business from my own front-line experiences and those of others than I’ve learned in educational settings. I also read a lot. (In Part V, I recommend books and other resources that I’ve found most useful.)

If you don’t continually invest in your education, you risk losing your competitive edge. Your skills and perspectives can become dated and obsolete. Although that doesn’t mean you should work 80 hours a week and never do anything fun, it does mean that part of your “work” time should involve upgrading your skills.

The best organizations are those that recognize the need for continual knowledge and invest in their workforce through training and career development. Just remember to look at your own career objectives, which may not be the same as your company’s.

Analyzing Returns

When you make investments, you have the potential to make money in a variety of ways. Each type of investment has its own mix of associated risks that you take when you part with your investment dollar and, likewise, offers a different potential rate of return. In the following sections, I cover the returns you can expect with each of the common investing avenues. But first, I walk you through the components of calculating the total return on an investment.

The components of total return

To figure out exactly how much money you’ve made (or lost) on your investment, you need to calculate the total return. To come up with this figure, you need to determine how much money you originally invested and then factor in the other components, such as interest, dividends, and appreciation (or depreciation).

If you’ve ever had money in a bank account that pays interest, you know that the bank pays you a small amount of interest when you allow it to keep your money. The bank then turns around and lends your money to some other person or organization at a much higher rate of interest. The rate of interest is also known as the yield. So if a bank tells you that its savings account pays 2 percent interest, the bank may also say that the account yields 2 percent. Banks usually quote interest rates or yields on an annual basis. Interest that you receive is one component of the return you receive on your investment.

If a bank pays monthly interest, the bank also likely quotes a compounded effective annual yield. After the first month’s interest is credited to your account, that interest starts earning interest as well. So the bank may say that the account pays 2 percent, which compounds to an effective annual yield of 2.04 percent.

When you lend your money directly to a company — which is what you do when you invest in a bond that a corporation issues — you also receive interest. Bonds, as well as stocks (which are shares of ownership in a company), fluctuate in value after they’re issued.

When you invest in a company’s stock, you hope that the stock increases (appreciates) in value. Of course, a stock can also decline, or depreciate, in value. This change in market value is part of your return from a stock or bond investment:

![]()

For example, if one year ago you invested $10,000 in a stock (you bought 1,000 shares at $10 per share) and the investment is now worth $11,000 (each share is worth $11), your investment’s appreciation looks like this:

![]()

Stocks can also pay dividends, which are the company’s sharing of some of its profits with you as a stockholder. Some companies, particularly those that are small or growing rapidly, choose to reinvest all their profits back into the company. (Of course, some companies don’t turn a profit, so they don’t have anything to pay out!) You need to factor any dividends into your return as well.

Suppose that in the previous example, in addition to your stock appreciating from $10,000 to $11,000, it paid you a dividend of $100 ($1 per share). Here’s how you calculate your total return:

![]()

You can apply this formula to the example like so:

![]()

After-tax returns

Although you may be happy that your stock has given you an 11 percent return on your invested dollars, remember that unless you held your investment in a tax-sheltered retirement account, you owe taxes on your return. Specifically, the dividends and investment appreciation that you realize upon selling are taxed, although often at relatively low rates. The tax rates on so-called long-term capital gains and stock dividends are lower than the tax rates on other income. In Chapter 3, I discuss the different tax rates that affect your investments and explain how to make tax-wise investment decisions that fit with your overall personal financial situation and goals.

If you’ve invested in savings accounts, money market accounts, or bonds, you owe Uncle Sam taxes on the interest.

Often, people make investing decisions without considering the tax consequences of their moves. This is a big mistake. What good is making money if the federal and state governments take away a substantial portion of it?

If you’re in a moderate tax bracket, taxes on your investment probably run in the neighborhood of 30 percent (federal and state). So if your investment returned 7 percent before taxes, you’re left with a return of about 4.9 percent after taxes.

Psychological returns

Profits and tax avoidance can powerfully motivate your investment selections. However, as with other life decisions, you need to consider more than the bottom line. Some people want to have fun with their investments. Of course, they don’t want to lose money or sacrifice a lot of potential returns. Fortunately, less expensive ways to have fun do exist!

Psychological rewards compel some investors to choose particular investment vehicles such as individual stocks, real estate, or a small business. Why? Because compared with other investments, such as managed mutual funds, they see these investments as more tangible and, well, more fun.

Be honest with yourself about why you choose the investments that you do. Allowing your ego to get in the way can be dangerous. Do you want to invest in individual stocks because you really believe that you can do better than the best full-time professional money managers? Chances are high that you won’t. (See Chapter 6 for details.) Such questions are worth considering as you contemplate which investments you want to make.

Be honest with yourself about why you choose the investments that you do. Allowing your ego to get in the way can be dangerous. Do you want to invest in individual stocks because you really believe that you can do better than the best full-time professional money managers? Chances are high that you won’t. (See Chapter 6 for details.) Such questions are worth considering as you contemplate which investments you want to make.

Savings and money market account returns

You need to keep your extra cash that awaits investment (or an emergency) in a safe place, preferably one that doesn’t get hammered by the sea of changes in the financial markets. By default and for convenience, many people keep their extra cash in a bank savings account. Although the bank offers the U.S. government’s backing via the Federal Deposit Insurance Corporation (FDIC), it comes at a price. Most banks pay a low interest rate on their savings accounts. (I discuss banking options, including the sometimes higher-yielding online banks, in Chapter 7.)

Another place to keep your liquid savings is in a money market mutual fund. These are the safest types of mutual funds around and, for all intents and purposes, equal a bank savings account’s safety. The best money market funds generally pay higher yields than most bank savings accounts. Unlike a bank, money market mutual funds tell you how much they deduct for the service of managing your money. If you’re in a higher tax bracket, tax-free versions of money market funds exist as well. See Chapter 8 for more on money market funds.

If you don’t need immediate access to your money, consider using Treasury bills (T-bills) or bank certificates of deposit (CDs), which are usually issued for terms such as 3, 6, or 12 months. Your money will generally earn more in one of these vehicles than in a bank savings account. (In recent years, the yields on T-bills has been so low that the best FDIC-insured bank savings accounts have higher yields.) Rates vary by institution, so it’s essential to shop around. The drawback to T-bills and bank certificates of deposit is that you incur a penalty (with CDs) or a transaction fee (with T-bills) if you withdraw your investment before the term expires (see Chapter 7).

Bond returns

When you buy a bond, you lend your money to the issuer of that bond (borrower), which is generally the federal government or a corporation, for a specific period of time. When you buy a bond, you expect to earn a higher yield than you can with a money market or savings account. You’re taking more risk, after all. Companies can and do go bankrupt, in which case you may lose some or all of your investment.

Generally, you can expect to earn a higher yield when you buy bonds that

- Are issued for a longer term: The bond issuer is tying up your money at a fixed rate for a longer period of time.

- Have lower credit quality: The bond issuer may not be able to repay the principal.

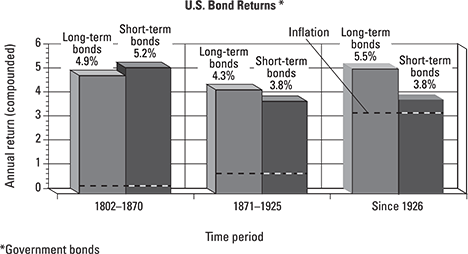

Wharton School of Business professor Jeremy Siegel has tracked the performance of bonds and stocks back to 1802. Although you may say that what happened in the 19th century has little relevance to the financial markets and economy of today, the decades since the Great Depression, which most other return data track, are a relatively small slice of time. Figure 2-4 presents the data, so if you’d like to give more emphasis to the recent numbers, you may.

© John Wiley & Sons, Inc.

Figure 2-4: A historical view of bond performance: Inflation has eroded bond returns more in recent decades.

Note that although the rate of inflation has increased since the Great Depression, bond returns haven’t increased over the decades. Long-term bonds maintained slightly higher returns in recent years than short-term bonds. The bottom line: Bond investors typically earn about 4 to 5 percent per year.

Stock returns

Investors expect a fair return on their investments. If one investment doesn’t offer a seemingly high enough potential rate of return, investors can choose to move their money into other investments that they believe will perform better. Instead of buying a diversified basket of stocks and holding, some investors frequently buy and sell, hoping to cash in on the latest hot investment. This tactic seldom works in the long run.

Unfortunately, some of these investors use a rearview mirror when they purchase their stocks, chasing after investments that have recently performed strongly on the assumption (and the hope) that those investments will continue to earn good returns. But chasing after the strongest performing investments can be dangerous if you catch the stock at its peak, ready to begin a downward spiral. You may have heard that the goal of investing is to buy low and sell high. Chasing high-flying investments can lead you to buy high, with the prospect of having to sell low if the stock runs out of steam. Even though stocks as a whole have proved to be a good long-term investment, picking individual stocks is a risky endeavor. See Chapters 5 and 6 for my advice on making sound stock investment decisions.

Unfortunately, some of these investors use a rearview mirror when they purchase their stocks, chasing after investments that have recently performed strongly on the assumption (and the hope) that those investments will continue to earn good returns. But chasing after the strongest performing investments can be dangerous if you catch the stock at its peak, ready to begin a downward spiral. You may have heard that the goal of investing is to buy low and sell high. Chasing high-flying investments can lead you to buy high, with the prospect of having to sell low if the stock runs out of steam. Even though stocks as a whole have proved to be a good long-term investment, picking individual stocks is a risky endeavor. See Chapters 5 and 6 for my advice on making sound stock investment decisions.

A tremendous amount of data exists regarding stock market returns. In fact, in the U.S. markets, data going back more than two centuries document the fact that stocks have been a terrific long-term investment. The long-term returns from stocks that investors have enjoyed, and continue to enjoy, have been remarkably constant from one generation to the next.

Going all the way back to 1802, the U.S. stock market has produced an annual return of 8.3 percent, while inflation has grown at 1.4 percent per year. Thus, after subtracting for inflation, stocks have appreciated about 6.9 percent faster annually than the rate of inflation. The U.S. stock market returns have consistently and substantially beaten the rate of inflation over the years (see Figure 2-5).

© John Wiley & Sons, Inc.

Figure 2-5: History shows that stocks have been a consistent long-term winner.

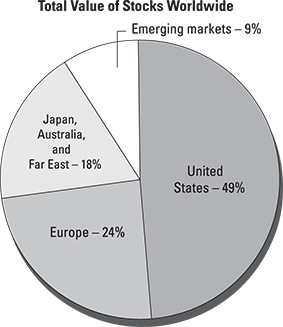

Stocks don’t exist only in the United States, of course (see Figure 2-6). More than a few U.S. investors seem to forget this fact, as they did especially during the sizzling performance of the U.S. stock market during the late 1990s. As I discuss in the earlier section “Diversify for a gentler ride,” one advantage of buying and holding overseas stocks is that they don’t always move in tandem with U.S. stocks. As a result, overseas stocks help diversify your portfolio.

In addition to enabling U.S. investors to diversify, investing overseas has proved to be profitable. The investment banking firm Morgan Stanley tracks the performance of stocks in both economically established countries and so-called emerging economies. As the name suggests, countries with emerging economies (for example, Brazil, China, India, Malaysia, Mexico, Russia, and Taiwan) are “behind” economically but show high rates of growth and progress.

© John Wiley & Sons, Inc.

Figure 2-6: Plenty of investing opportunities exist outside the United States.

Stocks are the best long-term performers, but they have more volatility than bonds and Treasury bills. A balanced portfolio gets you most of the long-term returns of stocks without much of the volatility.

Real estate returns

Over the years, real estate has proved to be about as lucrative as investing in the stock market. Whenever the U.S. has a real estate downturn, folks question this historic fact (see Chapter 11 for details). However, just as stock prices have down periods, so, too, do real estate markets.

The fact that real estate offers solid long-term returns makes sense because growth in the economy, in jobs, and in population ultimately fuels the demand for real estate.

Consider what has happened to the U.S. population over the past two centuries. In 1800, a mere 5 million people lived within U.S. borders. In 1900, that figure grew to 76.1 million, and today, it’s more than 315 million. All these people need places to live, and as long as jobs exist, the income from jobs largely fuels the demand for housing.

Businesses and people have an understandable tendency to cluster in major cities and suburban towns. Although some people commute, most people and businesses locate near major highways, airports, and so on. Thus, real estate prices in and near major metropolises and suburbs generally appreciate the most. Consider the areas of the world that have the most expensive real estate prices: Hong Kong, San Francisco, Los Angeles, New York, and Boston. What these areas have in common are lots of businesses and people and limited land.

Contrast these areas with the many rural parts of the United States where the price of real estate is relatively low because of the abundant supply of buildable land and the relatively lower demand for housing.

Small-business returns

As I discuss in Part IV of this book, you have several choices for tapping into the exciting potential of the small-business world. If you have the drive and determination, you can start your own small business. Or perhaps you have what it takes to buy an existing small business. If you obtain the necessary capital and skills to assess opportunities and risk, you can invest in someone else’s small business.

What potential returns can you get from small business? Small-business owners like me who do something they really enjoy will tell you that the nonfinancial returns can be major! But the financial rewards can be attractive as well.

Every year, Forbes magazine publishes a list of the world’s wealthiest individuals. Perusing this list shows that most of these people built their wealth by taking a significant ownership stake and starting a small business that became large. These individuals achieved extraordinarily high returns (often in excess of hundreds of percent per year) on the amounts they invested to get their companies off the ground.

You may also achieve potentially high returns from buying and improving an existing small business. As I discuss in Part IV, such small-business investment returns may be a good deal lower than the returns you may gain from starting a business from scratch.

Unlike the stock market, where plenty of historic rate-of-return data exists, data on the success, or lack thereof, that investors have had with investing in small private companies is harder to come by. Smart venture capitalist firms operate a fun and lucrative business: They identify and invest money in smaller startup companies that they hope will grow rapidly and eventually go public. Venture capitalists allow outsiders to invest with them via limited partnerships. To gain entry, you generally need $1 million to invest. (I never said this was an equal-opportunity investment club!)

Venture capitalists, also known as general partners, typically skim off 20 percent of the profits and also charge limited partnership investors a hefty 2 to 3 percent annual fee on the amount that they’ve invested. The return that’s left over for the limited partnership investors isn’t stupendous. According to Venture Economics, venture funds have averaged comparable annual returns to what stock market investors have earned on average over this same period. The general partners that run venture capital funds make more than the limited partners do.

You can attempt to do what the general partners do in venture capital firms and invest directly in small private companies. But you’re likely to be investing in much smaller and simpler companies. Earning venture capitalist returns isn’t easy to do. If you think that you’re up to the challenge, I explain the best ways to invest in small business in Chapter 15.

Considering Your Goals

How much do you need or want to earn? That may seem like an extraordinarily silly question for me to ask you. Who doesn’t want to earn a high return? However, although investing in stocks, real estate, or a small business can produce high long-term returns, investing in these vehicles comes with greater risk, especially over the short term.

Some people can’t stomach the risk. Others are at a time in their lives when they can’t afford to take great risk. If you’re near or in retirement, your portfolio and nerves may not be able to wait a decade for your riskier investments to recover after a major stumble. Perhaps you have sufficient assets to accomplish your financial goals and are concerned with preserving what you do have rather than risking it to grow more wealth.

If you work for a living, odds are that you need and want to make your investments grow at a healthy clip. If your investments grow slowly, you may fall short of your goals of owning a home or retiring or changing careers.