MAINTENANCE OF A CODE OF ETHICS (STUDY OBJECTIVE 9)

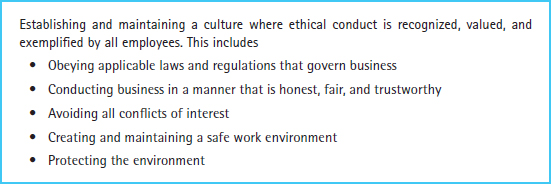

![]() In response to the many fraudulent financial reports generated in 2001, the United States Congress passed the Sarbanes–Oxley Act of 2002. The Act was intended to reform accounting, financial reporting, and auditing functions of companies that are publicly traded in stock exchanges. Chapter 5 describes the Act's major requirements regarding fraud and internal controls. One requirement is that public companies adopt and disclose a code of ethics for directors, officers, and employees. Documenting and adhering to a code of ethics should reduce opportunities for managers or employees to conduct fraud. This will only be true, however, if top management emphasizes this code of ethics and disciplines or discharges those who violate the code. Exhibit 3-3 presents the type of concepts that are usually found in a business organization's code of ethics.

In response to the many fraudulent financial reports generated in 2001, the United States Congress passed the Sarbanes–Oxley Act of 2002. The Act was intended to reform accounting, financial reporting, and auditing functions of companies that are publicly traded in stock exchanges. Chapter 5 describes the Act's major requirements regarding fraud and internal controls. One requirement is that public companies adopt and disclose a code of ethics for directors, officers, and employees. Documenting and adhering to a code of ethics should reduce opportunities for managers or employees to conduct fraud. This will only be true, however, if top management emphasizes this code of ethics and disciplines or discharges those who violate the code. Exhibit 3-3 presents the type of concepts that are usually found in a business organization's code of ethics.

Exhibit 3-3 Concepts in a Code of Ethics

THE REAL WORLD

In a recent survey of management accountants and financial managers, the effect of ethics codes on management behavior was studied. The survey concluded, in part, “Nearly 62 percent of the respondents (13 out of 21) from corporations reporting that ethics don't matter also report pressure to alter or ‘manage’ financial results. In contrast, in corporations where the tone at the top favors ethical conduct, only 19 percent (35 out of 189) reported pressure to alter results. Similar results were shown with specific financial reporting measures, such as income, balance sheet, and return on investment.”7 Another survey reported that 24 percent of accountants in the study had been “bullied” to fudge financial numbers in company reports.8