ACCOUNTING-RELATED FRAUD (STUDY OBJECTIVE 2)

Fraud can be defined as the theft, concealment, and conversion to personal gain of another's money, physical assets, or information. Notice that this definition includes theft and concealment. In most cases, a fraud includes altering accounting records to conceal the fact that a theft occurred. For example, an employee who steals cash from his employer is likely to alter the cash records to cover up the theft. An example of conversion would be selling a piece of inventory that has been stolen. The definition of fraud also includes theft, not only of money and assets, but also of information. Much of the information that a company maintains can be valuable to others. For example, customer credit card numbers can be stolen. An understanding of the nature of fraud is important, since one of the purposes of an accounting information system is to help prevent fraud.

In fraud, there is a distinction between misappropriation of assets and misstatement of financial records. Misappropriation of assets involves theft of any item of value. It is sometimes referred to as a defalcation, or internal theft, and the most common examples are theft of cash or inventory. Restaurants and retail stores are especially susceptible to misappropriation of assets because their assets are readily accessible by employees. Misstatement of financial records involves the falsification of accounting reports. This is often referred to as earnings management, or fraudulent financial reporting.

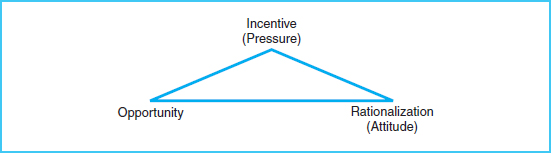

In order for a fraud to be perpetrated, three conditions must exist, as shown in Exhibit 3-1. These three conditions, known as the fraud triangle, are as follows:

- Incentive to commit the fraud. Some kind of incentive or pressure typically leads fraudsters to their deceptive acts. Financial pressures, market pressures, job-related failures, or addictive behaviors may create the incentive to commit fraud.

- Opportunity to commit the fraud. Circumstances may provide access to the assets or records that are the objects of fraudulent activity. Only those persons having access can pull off the fraud. Ineffective oversight is often a contributing factor.

- Rationalization of the fraudulent action. Fraudsters typically justify their actions because of their lack of moral character. They may intend to repay or make up for their dishonest actions in the future, or they may believe that the company owes them as a result of unfair expectations or an inadequate pay raise.

Understanding these conditions is helpful to accountants as they create effective systems that prevent fraud and fraudulent financial reporting. Fraud prevention is an increasingly important role for accounting and IT managers in business organizations, because instances of fraud and its devastating effects appear to be on the rise.

Exhibit 3-1 The Fraud Triangle

The Association of Certified Fraud Examiners publishes studies of occupational fraud cases. Some statistics from its most recent reports follow:4

- Certified fraud examiners estimate that 5 percent of revenues are lost annually as a result of occupational fraud and abuse. Applied to the World Gross Domestic Product, this translates to losses of approximately $2.9 trillion.

- The median loss due to fraud was $160,000, and one-quarter of the cases of frauds caused losses in excess of $1 million.

- Over 90 percent of occupational frauds involve asset misappropriations, and the median loss was $135,000. Cash is the targeted asset 90 percent of the time.

- Corruption schemes perpetrated by company executives and owners account for slightly less than one-third of all occupational frauds, and they caused a median loss of $250,000.

- Fraudulent financial statements account for less than 5 percent of the cases, but they were the most costly form of occupational fraud, with median losses of over $4 million per scheme.

- The average scheme in this study lasted 18 months before it was detected.

- The most common method for detecting occupational fraud is by a tip from an employee, customer, vendor, or anonymous source. The second most common method is by management review.

- Small businesses (having fewer than 100 employees) are the most vulnerable to occupational fraud and abuse. The average scheme in a small business causes $155,000 in losses, as compared with an average loss in larger companies of $164,000.

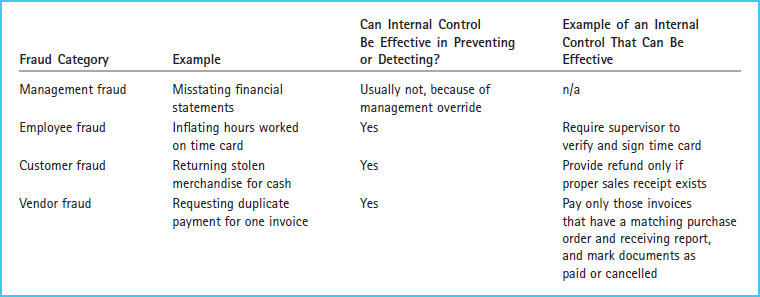

As indicated by the fraud report from the Association of Certified Fraud Examiners, fraud occurs in many different ways. The general categories of fraud and examples of these are explained in the sections that follow.

Exhibit 3-2 Categories of Accounting-Related Fraud

CATEGORIES OF ACCOUNTING-RELATED FRAUD

In an organization, fraud can be perpetrated by four categories of people: management, employees, customers, and vendors. (See Exhibit 3-2.)